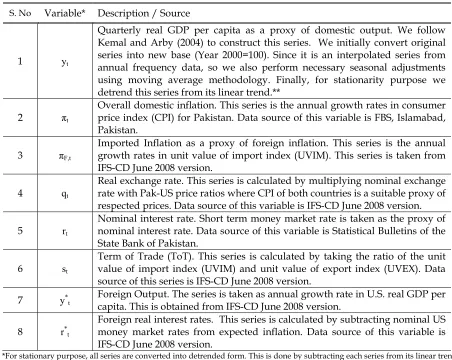

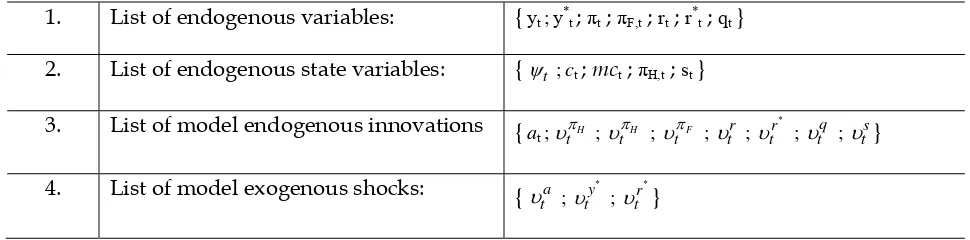

A Small Open Economy DSGE Model for Pakistan

Full text

Figure

Related documents

W2K3 W2K3 W2K3 XEN XEN Citrix Presentation Server 4.5 Top-Tier JKCS Mid-Tier JKCS Mid-Tier Websites Active Directory Adobe Connect Failover H H H Active Directory Adobe Flash

Vision Mission Values People Technical Skills Development Leadership Development Routine Management Supporting Staff Contract Development Add value to clients Comau´s

a (AZFa) region of human Y chromosome caused by recom- bination between HERV15 proviruses. Localization of factors con- trolling spermatogenesis in the nonfluorescent portion

In this paper, we consider a general MSV model with cross leverage and heavy-tailed errors and propose a novel and efficient MCMC algorithm using a multi-move sampler that samples a

In a recent work on deep auto encoder (DAE)[10], stereo training data were created by artificially adding noises to clean speech samples and training the DAE with the noisy data

More recently, Piterbarg (2010) [8] has used the similar formula given in [7] to take the collateral cost into account for the option pricing in general, but he has not discussed

Circulating MicroRNAs in Alzheimer's Disease: The Search for Novel Biomarkers..

The Generic Risk Library may be read by the relevant approving authority to assess if all important risks have been considered in the Risk Assessment Note which is submitted with the