Munich Personal RePEc Archive

Macroeconomic Risks and

Characteristic-Based Factor Models

Aretz, Kevin and Bartram, Söhnke M. and Pope, Peter F.

Manchester University, Warwick University, City University London

2010

Online at

https://mpra.ub.uni-muenchen.de/47344/

Macroeconomic Risks and Characteristic-Based Factor

Models

Kevin Aretz S¨ohnke M. Bartram Peter F. Pope∗

Abstract

We show that book-to-market, size, and momentum capture cross-sectional variation in ex-posures to a broad set of macroeconomic factors identified in the prior literature as potentially important for pricing equities. The factors considered include innovations in economic growth ex-pectations, inflation, the aggregate survival probability, the term structure of interest rates, and the exchange rate. Factor mimicking portfolios constructed on the basis of book-to-market, size, and momentum therefore serve as proxy composite macroeconomic risk factors. Conditional and unconditional cross-sectional asset pricing tests indicate that most of the macroeconomic factors are priced. The performance of an asset pricing model based on the macroeconomic factors is com-parable to the performance of the Fama and French (1992, 1993) model. However, the momentum factor is found to contain incremental information for asset pricing.

Keywords Fama and French model, Carhart model, asset pricing, book-to-market, size, momentum, macroeconomic pricing factors

JEL Classification G11, G12, G15

This version September 1, 2009

∗The authors are at Lancaster University Management School. Thanks are due to Michael Brennan, John Campbell,

Macroeconomic Risks and Characteristic-Based Factor

Models

Abstract

We show that book-to-market, size, and momentum capture cross-sectional variation in ex-posures to a broad set of macroeconomic factors identified in the prior literature as potentially important for pricing equities. The factors considered include innovations in economic growth ex-pectations, inflation, the aggregate survival probability, the term structure of interest rates, and the exchange rate. Factor mimicking portfolios constructed on the basis of book-to-market, size, and momentum therefore serve as proxy composite macroeconomic risk factors. Conditional and unconditional cross-sectional asset pricing tests indicate that most of the macroeconomic factors are priced. The performance of an asset pricing model based on the macroeconomic factors is com-parable to the performance of the Fama and French (1992, 1993) model. However, the momentum factor is found to contain incremental information for asset pricing.

Keywords Fama and French model, Carhart model, asset pricing, book-to-market, size, momentum, macroeconomic pricing factors

JEL Classification G11, G12, G15

1

Introduction

We offer a comprehensive multivariate analysis of the relations between shocks to macroeconomic

fundamentals suggested by prior research to be important for equity pricing and the benchmark risk

factors proposed by Fama and French (1993) and Carhart (1997). Although some of these relations

have already been considered elsewhere, e.g., evidence suggests that the Fama and French (FF)

bench-mark factors, HML and SMB, capture shocks to economic growth expectations (Vassalou, 2003; Liew

and Vassalou, 2000), default risk (Hahn and Lee, 2006; Petkova, 2006; Vassalou and Xing, 2004) and

the term structure (Hahn and Lee, 2006; Petkova, 2006), the focus of these studies is on one single

macroeconomic fundamental or on a narrow set of them. Still, as most macroeconomic fundamentals

at least partially reflect the state of the economy, they are often highly correlated, opening up the

possibility that the relations found in existing studies suffer from an omitted variables bias. As an

example, a downward revision in economic growth expectations often coincides with increasing

aggre-gate default risk due to more conservative consumer behavior and decreasing interest rates to revive

the economy. In this situation, an analysis of the univariate relation between HML or SMB and one of

these macroeconomic fundamentals can offer little insights on whether the benchmark factor captures

economic growth risk, default risk or interest rate risk.

We contribute to the existing literature in the following ways. First, we explore the links between

the macroeconomic fundamentals through a correlation analysis and Granger causality tests. We then

estimate a comprehensive macroeconomic factor (MF) model which can take account of associations

between the macroeconomic fundamentals. In this way, we are able to distinguish between the true

determinants of the benchmark factors and factors which only appear important in more narrow

settings due to their ability to proxy for the omitted true determinants. As a second contribution, we

expand the set of benchmark factors by investigating the Carhart (C) momentum factor, which is often

denoted by WML. We are aware of only a limited number of other studies testing the relation between

momentum and macroeconomic fundamentals, and these studies normally fail to find any significant

associations.1 We also expand the set of macroeconomic fundamentals by adding unexpected inflation

1More specifically, although Chordia and Shivakumar (2002) show that macroeconomic fundamentals can explain

and changes in a trade-weighted U.S. dollar exchange rate index. Although prior studies indicate that

these factors both associate with equity returns (e.g., Doidge et al., 2006; Vassalou, 2000; Chen et al.,

1986), their roles in explaining SMB, HML and WML have not been studied so far. Finally, we add the

market return as a pricing factor in our MF model. In an ICAPM world, this factor rewards investors

for bearing risks unrelated to the macroeconomic fundamentals. Still, as the market return is highly

correlated with the macroeconomic fundamentals, its inclusion would distort the links between the

macroeconomic fundamentals and the stock-based characteristics. To isolate the variation in market

returns not attributable to the macroeconomic fundamentals, we follow the recommendation of Connor

et al. (2006) and Fama (1998, 1996) and orthogonalize the market return with respect to our other

macroeconomic fundamentals.

Consistent with our intuition, we find strong evidence that macroeconomic fundamentals are

sub-stantially related. As a direct result of these relations, our analysis of the links between the benchmark

risk factors and the macroeconomic fundamentals can in some cases significantly contradict the main

conclusions of other studies. In a nutshell, our analysis corroborates the findings of other studies that

book-to-market (BM), and therefore HML, captures information about shocks to economic growth

expectations and the slope of the term structure, while size, and therefore SMB, captures information

about shocks to aggregate default risk (e.g., Hahn and Lee, 2006; Petkova, 2006; Vassalou, 2003).

Still, in contrast to other studies, we also show that SMB relates to shocks to the average level of the

term structure. Importantly, some significant associations documented in the prior literature either

change sign, e.g., the relation between HML and shocks to economic growth expectations, or become

insignificant, e.g., the relation between HML and shocks to aggregate default risk. Additional tests

show that these inconsistencies are driven by the omission of correlated factors in prior studies. We

also report findings entirely new to the literature. In particular, we find that WML captures default

risk, term structure risk, and more weakly foreign exchange rate risk.

The close relation between the macroeconomic fundamentals and the benchmark risk factors

im-plies that macroeconomic exposures should be able to approximate the exposures to the benchmark

risk factors in empirical asset pricing tests. As the benchmark risk factor exposures command strongly

significant risk premia and perform well in pricing the cross-section of most characteristic-sorted

for the MF model. To test these conjectures, we compare the relative and incremental pricing ability

of the MF model with those of models based on the market return and the FF benchmark risk factors

(the FF model) and the market return and the FF and C benchmark risk factors (the C model). We

also estimate the risk premia of the pricing factors of the individual asset pricing models. Overall, our

test outcomes indicate that shocks to economic growth expectations, aggregate default risk, the term

structure, and the exchange rate are priced. The significant risk premium on exposure to aggregate

default risk contrasts with the evidence reported in Hahn and Lee (2006) and Petkova (2006), who

find an insignificant default risk premium. We conjecture that this inconsistency might be due to the

proxy variable chosen for shocks to aggregate default risk. Our proxy variable is derived from Merton’s

(1974) contingent claims analysis (see Vassalou and Xing, 2004).

Our empirical findings further reveal that the MF model and the FF model exhibit a similar pricing

performance on 25 two-way sorted BM and size portfolios, while that of the C model is somewhat

higher. Consistent with this, the macroeconomic fundamentals render the risk premia on HML, SMB

and WML insignificant on these test assets. When our test assets are instead 64 portfolios three-way

sorted on BM, size and momentum, only the C model can correctly price the test assets, with the

MF model still achieving a markedly better pricing ability than the FF model. All three asset pricing

models perform adequately well in pricing 32 managed portfolios, i.e., eight three-way sorted size,

BM and momentum portfolios interacted with lagged macroeconomic instruments. For the three-way

sorted portfolios, the macroeconomic fundamentals are never able to drive out the significant risk

premia on either HML and SMB or HML, SMB and WML.

We interpret our results as showing that the FF benchmark factors contain important

informa-tion on macroeconomic fundamentals. The macroeconomic fundamentals could matter to investors,

either because they capture common variation in equity returns, as in the APT (e.g., Connor and

Korajczyk, 1995; Ross, 1976), or because they represent hedgeable sources of state variable risk, as

in the ICAPM (e.g., Brennan et al., 2004; Campbell, 1993; Merton, 1973). Since the macroeconomic

fundamentals explain a substantial proportion of equity return variation, but also forecast current

and future consumption (Chen, 1991), these interpretations are not mutually exclusive. On the other

hand, the pricing ability of the C model is only partially explained by our chosen macroeconomic

model that could help to explain the role of WML in pricing. As characteristic-sorted factors probably

capture macroeconomic pricing information efficiently, our results provide a justification for the usage

of characteristic-based pricing models like the FF model or the C model.

Our paper is organized as follows. In Section 2, we review the literature and provide the motivation

for our research. Research design and data are described in Section 3, which also contains the analysis

of the links between our macroeconomic fundamentals. We report our outcomes from the estimation of

risk exposures, risk premia and model specification tests in Section 4. In Section 5, we document that

our findings are largely robust to our choice of macroeconomic proxy variables. Section 6 concludes.

We offer more information on estimation methods and test assets in Appendix A and B, respectively.

2

Prior Literature

The ability of macroeconomic fundamentals to explain both equity returns and prices has been known

for some time, e.g., see the studies of Chen et al. (1986) and Chan et al. (1985). However, only after the

seminal studies of Fama and French (1993, 1992), which show that factors based on stock characteristics

like size or BM can also capture variation in equity prices, has academic research started to explore

the theoretical and empirical links between stock characteristics and macroeconomic fundamentals.

Our analysis contributes to this growing literature. In Table 1, we summarize the main findings from

studies documenting links between the FF and C benchmark factors and macroeconomic fundamentals,

including shocks to GDP (or alternatively industrial production) growth expectations, inflation, the

term structure of interest rates, the aggregate default (or survival) probability and the dividend yield.

Overall, the following conclusions can be distilled from this literature:

1. The evidence reported in Liew and Vassalou (2000) suggests that economic growth over the

subsequent year can be forecasted using HML and SMB. Kelly (2004) reports weaker evidence

that SMB can also be used to forecast future inflation. Related studies show that economic

growth risk is weakly priced at the 90% confidence level (Vassalou, 2003).

2. The evidence from asset pricing studies suggests that betas on changes in the slope of the

term structure are negative, and their magnitude decreases with BM (i.e., low BM stocks have

notion that growth stocks are higher duration assets. In cross-sectional tests, term structure risk

commands a significant risk premium (Hahn and Lee, 2006; Petkova, 2006). Similarly, betas on

changes in the aggregate default probability are negative, and their magnitude decreases with

size. Still, default risk never attracts a significant risk premium (Hahn and Lee, 2006; Petkova,

2006; He and Ng, 1994; Chan et al., 1985). Prior studies have so far not identified macroeconomic

fundamentals able to explain variation in WML (Griffin et al., 2003).

A potential difficulty in interpreting the body of literature summarized in Table 1 arises because

macroeconomic fundamentals are likely to be substantially correlated. A notable feature of the table

is that the cited studies focus on only partially overlapping sets of macroeconomic fundamentals. For

example, no prior study considers economic growth and inflation risks together with term structure

and default risks. As a result, we cannot rule out that in existing studies one macroeconomic factor

proxies for another “more fundamental” factor. There is also the possibility that beta estimates in

existing studies are biased due to correlated relevant pricing factors being omitted from an asset

pricing model. We explicitly address these concerns by estimating an MF model that includes a broad

set of macroeconomic fundamentals considered in the prior literature. We also expand the set of

macroeconomic fundamentals to include unexpected inflation (not shocks to inflation expectations, as,

e.g., used in the study of Kelly (2004)) and shocks to a U.S. composite exchange rate. Prior evidence

indicates that both factors are related to equity returns (see, e.g., Doidge et al., 2006; Vassalou, 2000;

Jorion, 1991). We also add the orthogonalized market return, because in an ICAPM world this factor

rewards investors for bearing risk unrelated to the state variables (Fama, 1996, p.460).

3

Research Design

3.1 Methodology

We now review the empirical methods used to assess (1) the time-series associations between the

macroeconomic fundamentals and the firm characteristics, and (2) the cross-sectional pricing ability

model from the following time-series regression:

Rtp−1,t =β0p+β1pRMt−1,t+β2pSM Bt−1,t+β3pHM Lt−1,t(+βp4W M Lt−1,t) +εpt−1,t, (1)

whereRpt−1,tis test portfoliop’s excess return (net return minus risk-free return),RMt−1,tis the excess

return on a value-weighted stock market index, SM Bt−1,t is the return of a portfolio long on small

and short on big market capitalization stocks (keeping BM and momentum constant), HM Lt−1,t is

the return on a portfolio long on high and short on low BM ratio stocks (keeping size and momentum

constant), andW M Lt−1,tis the return on a portfolio long on winner and short on loser stocks (keeping

size and BM constant). If we impose the restriction β4p = 0, the model shown in equation [1] is the

FF model. Otherwise, the model shown in equation [1] is the C model.

The beta coefficients of the MF model can be estimated from the following time-series regression:

Rpt−1,t=βp0+β1pM Y Pt,t+12+β2pU It−1,t+β3pDSVt−1,t+β4pAT St−1,t (2)

+β5pST St−1,t+β6pF Xt−1,t+εpt−1,t,

where M Y Pt,t+12 is the change in one-year ahead industrial production growth expectations,U It−1,t

is unexpected inflation, DSVt−1,t is the change in the aggregate survival probability, AT St−1,t and

ST St−1,t are changes in, respectively, the average level and the slope of the term structure, and

F Xt−1,t is the change in a multilateral U.S. dollar exchange rate. As discussed, this model nests all

the main macroeconomic factor models shown in Table 1, but it also includes two neglected

macroe-conomic fundamentals, i.e., unexpected inflation and shocks to the exchange rate. We also consider

an augmented version of the MF model (the AMF model) which includes the market return.

Re-sults reported in Section 4 show that around 74.2% of the variance in market returns is explained by

the macroeconomic fundamentals. Since the market return cannot be treated as exogenous, we first

orthogonalize market returns with respect to the other macroeconomic fundamentals.

We use the stochastic discount factor/generalized method of moments (GMM) methodology

pro-posed by Cochrane (2001) (1) to assess whether the macroeconomic fundamentals command significant

risk premia and (2) to evaluate the pricing ability of the models. Jagannathan and Wang (2002) show

models. When analyzing excess returns, the stochastic discount factor representation is:

0 =ppt =Et(mt+1Rpt,t+1), (3)

where ppt is the market price of portfolio p (zero for excess returns),Et(.) is the expectation operator

conditional on timetinformation,mt+1 is the linear stochastic discount factor, i.e.,mt+1 = 1−b′ft+1,

where ft+1 are the models’ pricing factors, andRpt,t+1 is portfolio p’s excess return. When examining

excess returns, the average level of the stochastic discount factor is not identified. To circumvent this

problem, we choose to set the constant to unity. We can rearrange equation [3] to obtain risk premia,

whose significance levels can be inferred with the delta method (see Appendix A).

3.2 Test Assets

We use firm characteristic-sorted portfolios as test assets throughout this study, with the firm

char-acteristics being BM, size and momentum. Moreover, we employ both unconditional and conditional

portfolios, where the conditional portfolios are interacted with lagged macroeconomic instruments. We

create one-way sorted characteristic portfolios analogous to Fama and French (1993). In particular,

we observe the BM decile breakpoints in December of yeart−1 and the size decile breakpoints and the

prior eleven month compounded return (momentum) breakpoints in June of yeart. The construction

of the momentum characteristic follows Carhart (1997). Consistent with other studies, we only use

NYSE firms to obtain the breakpoints. After identification of the breakpoints, we form value-weighted

portfolios comprising all stocks from the NYSE, AMEX and NASDAQ within each relevant range of

the sorting variable in July of year t. Portfolio composition remains fixed until June of year t+1, at

which point we reform portfolios according to the same algorithm.2

We construct two-way and three-way independently-sorted portfolios from subsets of the same

breakpoints. To limit the number of test assets, we assign firms to (1) eight (2x2x2) portfolios based

on the median breakpoints, (2) 27 (3x3x3) portfolios based on the bottom 30%, middle 40% and top

30% breakpoints, and (3) 64 (4x4x4) portfolios based on the bottom 20%, lower-middle 30%,

top-2Studies in the momentum literature, as, e.g., Jegadeesh and Titman (1993, 2001), often examine various portfolio

middle 30% and top 20% breakpoints. Similar to Liew and Vassalou (2000), we create the three-way

independently-sorted benchmark factors, i.e., HML, SMB, and WML, from the (3x3x3) benchmark

portfolios (see Appendix B for more details).

3.3 Macroeconomic Fundamentals

We now introduce the variables we use in our tests to proxy for the macroeconomic fundamentals in the

MF model. Our first macroeconomic fundamental, which is changes in economic growth expectations,

should capture revisions in investors’ cash flow (dividend) expectations. To facilitate monthly data

analysis, we select industrial production growth as our measure of economic growth rather than GDP,

which is only observable on a quarterly basis. Petkova and Zhang (2005) argue thatrealized industrial

production growth is a poor proxy for the change in economic growth expectations and its usage would

result in an errors-in-variables problem. Hence, we adopt an approach initially proposed by Breeden

et al. (1989) and later refined by Lamont (2001) and Vassalou (2003), and create a mimicking portfolio

capturing changes in one-year ahead industrial production growth expectations. Portfolio weights are

obtained by regressing the log change in realized industrial production over the subsequent year on a

set of traded base assets and a set of control variables designed to capture all anticipated information

in industrial production growth and the base asset returns.

If the mimicking portfolio approach is to be powerful, the base assets must span the space of asset

returns. Besides this, theory offers little guidance on the choice of base assets, perhaps explaining the

wide range of assets used in related prior research. Since we are interested in establishing the empirical

relations between the FF and C benchmark factors (and their underlying benchmark portfolios) and

our macroeconomic fundamentals, we are careful not to include the benchmark factors in the set of base

assets. Instead, we include the market portfolio, a long-term and an intermediate-term government

bond portfolio, a high-yield corporate bond portfolio and gold. All base asset returns are in excess of

the risk-free rate, so that mimicking portfolio weights do not need to sum to unity. During two periods

in our sample period, namely the 1987 stock market crash and the Internet bubble period, market

returns are unlikely to efficiently capture news on economic growth. To control for the possibility that

slope dummies which allow the market portfolio weight to vary during these periods.3 As controls, we

use lagged instruments found in prior studies to predict variation in stock returns.4 In two alternative

specifications, we also add the one-month or one-year lagged base asset excess returns. A complete

list of the base assets and control variables is presented in the footnote of Table 2.

We follow Vassalou and Xing (2004) in using an equally-weighted average of stock-level survival

probabilities as the aggregate market estimate, where we derive a firm’s survival probability over the

subsequent year according to the contingent claims model of Merton (1974). Monthly shocks to the

aggregate survival probability are defined as changes in the original time-series. Unexpected inflation

is approximated through realized inflation minus the fitted value from an MA(1) process (Fama and

Gibbons, 1984).5 We employ two interest rate term structure risk factors: (i) the change in the average

level of the term structure (i.e., the change in the mean of the 3-month Treasury bill yield and the

10-year Treasury bond yield); and (ii) the change in the term structure slope (i.e., the change in the

difference between the 10-year Treasury bond yield and the 3-month Treasury bill yield). Finally, we

capture exchange rate risk through the change in a U.S. composite exchange rate.

3.4 Data and Sample

We obtain the data used to form the benchmark portfolios and characteristic-based factors from the

intersection of CRSP and COMPUSTAT. We exclude firms with negative book values and issues

other than common stock. Equivalent to Fama and French (1993), we define the book value as the

COMPUSTAT book value of stockholders’ equity, plus balance-sheet deferred taxes and investment

tax credits, minus the book-value of preferred stock, where the value of preferred stock is either the

redemption, liquidation, or par value (in this order). The original FF benchmark portfolios and factors

and the risk-free rate are from Kenneth French’s website. The dividend yield on the S&P500 index

is from Robert Shiller’s website. We obtain the aggregate survival probability from January 1975 to

3The exclusion of the slope dummies does not materially affect the relations between the stock characteristics and

the macroeconomic fundamentals. However, their inclusion renders the mimicking portfolio more similar to an out-of-sample rolling window estimate of it, while retaining the important advantage that we can correct standard errors for the additional uncertainty created by the generated regressor.

4See Ferson and Harvey (1991), Breen et al. (1989), Ferson (1989), Harvey (1989), Fama and French (1989, 1988),

Campbell (1987) and Keim and Stambaugh (1986).

5Unexpected inflation is therefore also a generated regressor. However, Pagan (1984) proves that, if the generated

December 1999 from Maria Vassalou’s website.6 We extend these data to December 2008 following

the approach of Vassalou and Xing (2004).7 Yield data on 3-month U.S. government Treasury bills,

10-year Treasury bonds, Aaa/Baa-rated corporate bond portfolios and the exchange rate (in foreign

currency per unit of home currency) between the U.S. dollar and a broad trade-weighted composite

currency index are from the Federal Reserve Bank’s website. Return data on the U.S. bond portfolios

and gold are from Ibbotson Associates. We obtain the seasonally-adjusted level of the U.S. industrial

production index and the consumer price index from DataStream. All our variables are at a monthly

frequency and are for the sample period from January 1975 to April 2008.8

3.5 Summary Statistics and Granger Causality Tests

In Table 2, we report the outcomes from OLS regressions used to find the base asset weights of the

mimicking portfolio on changes in economic growth expectations. As monthly industrial production

growth is measured over rolling one-year windows, we adjust t-statistics for the induced moving average

error in residuals using the Newey and West (1987) correction with the lag parameter l set equal to

eleven. Overall, the asset weights are fairly similar across the three model specifications shown in the

table. The t-statistics and exclusion tests both indicate that, of the base assets, the market portfolio,

the intermediate-term government bond portfolio and gold are most significantly related to one-year

ahead changes in the industrial production index. The weight of the market portfolio is reduced to

virtually zero during the 1987 stock market crash, but it is significantly higher during the Internet

bubble period.9 Some control variables, e.g., the risk-free rate, are also significant.

A central question is how well the mimicking portfolio reflects changes in one-year ahead economic

growth expectations. Across the three specifications, the lower-bound adjusted R2from a hypothetical

OLS regression of changes in industrial production growth expectations on the unexpected base asset

returns is at least 3.51%. Although this estimate is slightly lower than those reported in other studies,

6We thank Kenneth French, Robert Shiller, and Maria Vassalou for making these data available.

7The correlation coefficient between the monthly DSV series obtained from Maria Vassalou’s website and ours is 0.95

during the period from February 1971 to December 1999. We extend Maria Vassalou’s data from December 1999 to December 2008 through the prediction from an OLS regression of her series onto our series. The intercept and slope coefficient of this regression equal 0.002 and 0.918, respectively. Our main conclusions do not change, if we entirely use our own series in our empirical tests.

8Although most of our data extend to December 2008, we require the 12-month lead level of the industrial production

index to construct our proxy for changes in economic growth expectations.

9One explanation is that firms raised new capital during the initial rise of the stock market, which was subsequently

the low value is mainly driven by the fact that our sample period starts shortly after the oil crises

(i.e., inclusion of the oil crises would have increased the lower-bound to approximately 8%). Besides

this, our parameter estimates and significance levels are very similar to those reported elsewhere

(e.g., Vassalou, 2003; Lamont, 2001). In addition, we have also compounded the mimicking portfolio

to a bi-annual frequency and then computed its correlation coefficient with changes in industrial

production growth expectations obtained from the Livingston Surveys of Professional Forecasters over

the period from June 1975 to December 2007. For all three specifications, the correlation coefficient

is around 0.50, suggesting that our approach can capture a large fraction of changes in the survey

participants’ expectations. Our correlation estimates are conservative, as the survey data are based

on 14-month forecast horizons10and survey participants are no major equity investors. In the interests

of parsimony, we employ the second mimicking portfolio specification in the remainder of the study,

as this specification yields the highest lower-bound adjusted R2.11

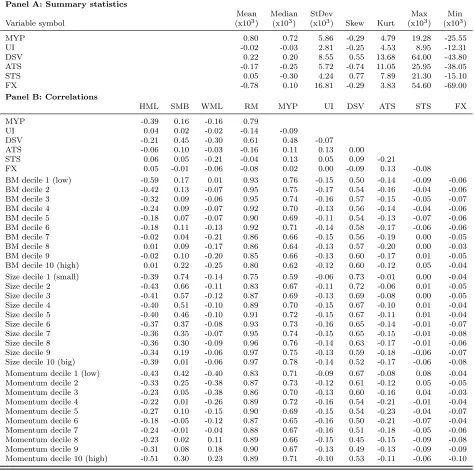

We present summary statistics on the macroeconomic fundamentals in Panel A of Table 3. The

sample mean of the mimicking portfolio on economic growth (MYP) is positive, but insignificant when

not controlling for the influence of other risk factors. Summary statistics on the benchmark portfolios

and factors are in a table in the Appendix. The most important feature of Table 3 is shown in Panel B:

several macroeconomic fundamentals are highly correlated, e.g., MYP and DSV, ATS, and STS or

ATS and STS and FX, confirming that interpretation of some prior studies could be ambiguous.

Panel B of Table 3 also shows correlations between the one-way sorted characteristic portfolios and

the benchmark risk factors and macroeconomic fundamentals. While the correlation coefficients often

suggest associations between the benchmark risk factors and the macroeconomic fundamentals, our

multivariate model results presented later will show that bivariate correlations are not always a good

guide to the sign and significance of macroeconomic exposures.

The summary statistics shown so far reveal nothing about causality between the benchmark risk

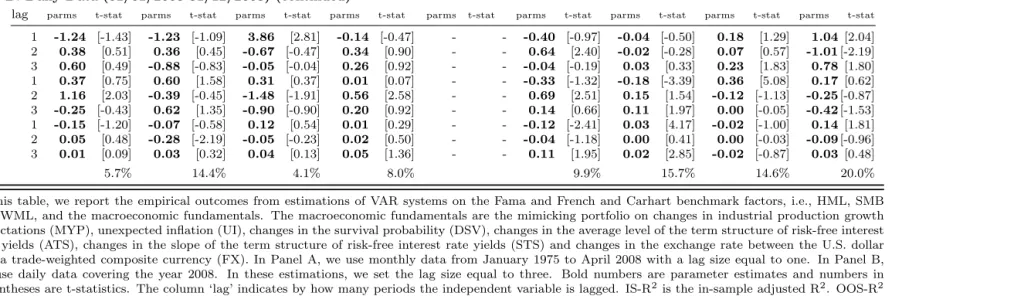

factors and the macroeconomic fundamentals. Hence, we report the outcomes from Granger causality

tests analyzing whether certain benchmark risk factors or macroeconomic fundamentals help to forecast

others in Table 4. The main idea of these tests is that, if an event causes another event, then it should

10Although survey participants are asked to predict the level of the industrial production index twelve months after

precede the other event in time. Although most of the relations between our analysis variables should

be contemporaneous, the tests in Table 4 check whether some fraction of the change in one variable

occurs before the change in another.12 In Panel A, we consider monthly data over the sample period

from January 1975 to April 2008 with the lag length set equal to one. We have checked that other lag

lengths do not substantially affect our main conclusions from these tests. Considering first the links

between the macroeconomic fundamentals, MYP and ATS seem to be exogenously determined with

respect to the other factors. However, an upward revision in economic growth expectations associates

significantly with a higher aggregate survival probability and U.S. dollar value in the future. In

a similar way, an increase in the average term structure significantly predicts a higher unexpected

inflation and U.S. dollar value and a lower aggregate survival probability and term structure slope.

In contrast, DSV and STS can be predicted by the other macroeconomic fundamentals, but cannot

predict them themselves. Both UI and FX form a feedback system with the other factors.

It is also interesting to check whether the macroeconomic fundamentals Granger-cause the

bench-mark risk factors, or vice versa. With the notable exception of UI, which will turn out to be relatively

unimportant for equity pricing, only STS can be forecasted with SMB at the 90% confidence level. In

contrast, HML can be forecasted with ATS and FX, SMB with UI and DSV and WML with MYP and

ATS. As a result, we conclude that the macroeconomic fundamentals often precede the benchmark

risk factors in time, and therefore appear more elementary. The in-sample adjusted R2s (IS-R2) are

between -0.4% (MYP) and 14.9% (FX). Finally, the low out-of-sample adjusted R2s (OOS-R2) based

on residuals constructed from estimates obtained over the prior ten years of data suggest that investors

were not able to forecast the analysis variables with any success.

We also explore whether the causality between the macroeconomic fundamentals and the

bench-mark risk factors can change during an economic recession. To this end, we estimate the VAR system

on daily data over 2008 in Panel B. While the benchmark risk factors can be obtained at a daily

frequency from Kenneth French’s website, we construct a daily time-series for the mimicking portfolio

through combining the weights obtained from the monthly estimations in Table 2 with daily data on

the base assets. To obtain a daily estimate of the aggregate survival probability, we assume that asset

volatilities are constant over one month, and then use the Merton (1974) model to first back out daily

asset values and to then construct a firm’s default probability (see, e.g., Vassalou and Xing, 2004).

Daily time-series on the 3-month Treasury Bill yield, the 10-year Treasury bond yield and the

compos-ite exchange rate can be obtained from the webscompos-ite of the Federal Reserve Bank. Unfortunately, we

are unable to compute a daily time-series for unexpected inflation, and we therefore omit this variable

from the daily estimations. Our empirical findings reveal that the links between our analysis variables

are much stronger in an economic recession. All macroeconomic fundamentals now form a feedback

system. Next, the benchmark risk factors now often also forecast the macroeconomic fundamentals,

although they can also still be forecasted by them. Finally, the in-sample adjusted R2s (IR-R2) are

often much higher than those in Panel A, but they are always higher than those from estimations on

daily data from August 1998 to December 2008 (not reported).

4

Results

4.1 Macroeconomic Risk Exposures

We now analyze the estimation outcomes from the time-series regression in equation [2] of the one-way

or three-way sorted characteristic portfolio returns onto the macroeconomic fundamentals. We use

Hansen’s (1982) GMM methodology to estimate all parameters, with standard errors corrected for

the additional uncertainty induced through the generated regressor MYP. We offer more details on

the GMM methodology in Appendix A. We show the regression coefficients and t-statistics of the

one-way sorted portfolios in Figure 1. In Panel A of Table 5, we report χ2 statistics testing whether

the spread in the macroeconomic risk exposures is significantly different from zero across the one-way

sorted characteristic portfolios. Although the table does not report adjusted R2s for the one-way

sorted portfolios, we note that these range from 49.4% to 70.4%, suggesting that the macroeconomic

fundamentals capture a large fraction of the variation in the one-way sorted portfolio returns.

In Figure 1, we illustrate that, of the macroeconomic fundamentals, MYP, DSV, and STS play

significant roles in explaining the one-way sorted characteristic portfolio returns. The absolute values

of the t-statistics on the MYP betas are greater than 2.0 on all 30 characteristic portfolios. In contrast,

their absolute values on the DSV and STS betas are only greater than 2.0 on 24 and 26 portfolios,

and negatively to STS. More importantly, the figure shows vividly that some macroeconomic exposures

strongly relate to the BM, size and momentum characteristics of the portfolios. For instance, when

we compare macroeconomic exposures across the BM deciles, the MYP exposures generally decrease,

while the DSV, STS and FX exposures increase with BM. Panel A of Table 5 reveals that the spread

in the MYP and STS exposures are strongly significant, while those in the DSV and STS exposures

are more weakly significant. The figure also illustrates that the DSV, ATS, STS, and FX exposures

almost monotonically decrease with the size characteristic of the size-sorted portfolios, while only the

smallest firm decile has a lower MYP exposure than the others. The spread in exposures is strongly

significant for MYP, DSV and ATS, and more weakly significant for STS. Finally, the DSV, STS and

FX exposures all relate to the momentum characteristic of the momentum-sorted portfolios, with all

spreads being significant at the 95% confidence level.

As the size, BM and momentum firm characteristics are themselves correlated, our evidence on the

one-way sorted portfolios is not unambiguous. More specifically, the correlation coefficients between

the BM and size decile, the BM and momentum decile and the size and momentum decile are -0.17,

0.11, and 0.17, respectively. Hence, the spread in one specific macroeconomic exposure across the size

portfolios could be driven by the fact that small (large) firms often have high (low) BM ratios. For

this reason, Fama and French (1993) orthogonalize benchmark portfolios with respect to size (BM)

when constructing the BM (size) benchmark portfolios underlying HML (SMB). We expect that the

evidence based on three-way sorted portfolios should therefore draw out more clearly the roles of each

firm characteristic in capturing macroeconomic exposures.

We report the estimation outcomes from the three-way sorted benchmark portfolios and RM,

HML, SMB, and WML in Panel B of Table 5. The t-statistics on the macroeconomic exposures of the

benchmark risk factors can be interpreted as tests of differences in macroeconomic exposures across

the top three and the bottom three BM, size or momentum deciles, respectively, after controlling for

correlation between firm characteristics. Most results in the table align with those obtained from the

one-way sorted portfolios. For example, consistent with the exposures of the benchmark portfolios,

HML loads negatively on MYP and positively on STS, SMB loads positively on DSV and ATS, and

WML loads negatively on DSV, STS and FX. Two important inconsistencies between the results on

for other firm characteristics, HML relates no longer to DSV, and SMB relates no longer to MYP. We

can explain these inconsistencies by noting that both size and momentum capture DSV risk, and that

controlling for these relations probably drives out the link between BM and DSV. In a similar way,

controlling for the relation between BM and MYP might drive out the link between SMB and MYP.

While our results on the relations between the benchmark risk factors and UI and FX and those on

the relations between WML and the macroeconomic fundamentals are entirely new to the literature,

it is instructive to compare other results in our analysis with those from the prior literature. Our

results contradict the prior literature in three main ways:

1. Liew and Vassalou (2000) and Kelly (2004) find a significantly positive relation between HML

and MYP. In contrast, we find a negative relation in Table 5. We can account for the difference

by observing that these two prior studies do not control for term structure risk. Our summary

statistics reveal that MYP has a positive correlation with ATS and STS. When we drop ATS

and STS, add RM and restrict our sample period to 1978 to 1996 (the sample period analyzed

in these studies), the relation between HML and MYP turns negative.

2. In contrast to our main findings, Hahn and Lee (2006) and Petkova (2006) obtain no evidence

that SMB associates with term structure risk. We conjecture that this difference could be driven

by correlation between ATS and STS, on the one hand, and MYP and FX, on the other. When

we end our sample period in 2001 (which is the end of their sample period; unfortunately, the

start of their sample period is before ours), include RM and drop MYP and FX, we also find an

insignificant association between SMB and ATS.

3. Vassalou and Xing (2004) find a negative relation between HML and DSV. In contrast, we find

no significant association between these two variables after controlling for other macroeconomic

fundamentals. We conjecture that the findings in Vassalou and Xing (2004) are an artifact of

the positive correlation between MYP and DSV. Dropping MYP from our MF model and ending

our sample period in 1999 (which is the end of their sample period; unfortunately, the start of

their sample period is before ours), HML loads significantly and negatively on DSV.

While our remaining results confirm those reported in the literature, the above cases confirm the

MF model includes more macroeconomic fundamentals than those in prior studies, we acknowledge

that it could also be incomplete. Our inferences are thus vulnerable to a similar critique.

4.2 Unconditional Pricing Tests

We evaluate the cross-sectional pricing ability of the MF, FF and C models in this section. If the success

of the FF and C models in pricing characteristic portfolios can be explained by the benchmark risk

factor exposures serving as proxies for macroeconomic exposures, then the macroeconomic exposures

of the MF model should at least in theory perform similarly in pricing. On the other hand, if either the

FF or C model outperforms the MF model, this indicates that the firm characteristics capture a richer

set of information on priced factors than that captured by the macroeconomic fundamentals. This

section analyzes unconditional test portfolios. In particular, we run our pricing tests on the 25 two-way

sorted BM and size portfolios that are widely used in the literature. We also consider 64 three-way

sorted BM, size and momentum portfolios, as a larger number of test assets with greater spreads in

expected returns should increase explanatory power in the presence of measurement errors endemic

in macroeconomic data, i.e., a lack of timeliness and/or predictability in revisions. We estimate all

models with the GMM to avoid a bias in standard errors (see Appendix A).

Our estimation outcomes are in Table 6, which first reports the relations between the relevant set

of pricing factors and the stochastic discount factor. Significant coefficients indicate that, conditional

on the other pricing factors of a model, a pricing factor helps to correctly price the test portfolios.

Below the loadings on the stochastic discount factor, we show the estimated risk premia, which reveal

whether each pricing factor is priced. To evaluate the pricing ability of each model, we also report

Hansen’s (1982) J-test and the adjusted R2 from an OLS regression of mean portfolio returns on

exposures. For the FF and C models, our results based on the 25 portfolios are close to those shown

on the 64 portfolios. For the MF and AMF models, we find similar parameter estimates on both sets

of test portfolios, but consistent with our expectations significance levels are lower for the smaller

set of test portfolios. As a result, we only report the estimation outcomes from the larger set of 64

portfolios. Still, it is worthwhile highlighting that the abilities of the MF and FF models to price the

25 test assets are relatively similar. For example, the adjusted R2s of the MF and the FF models are

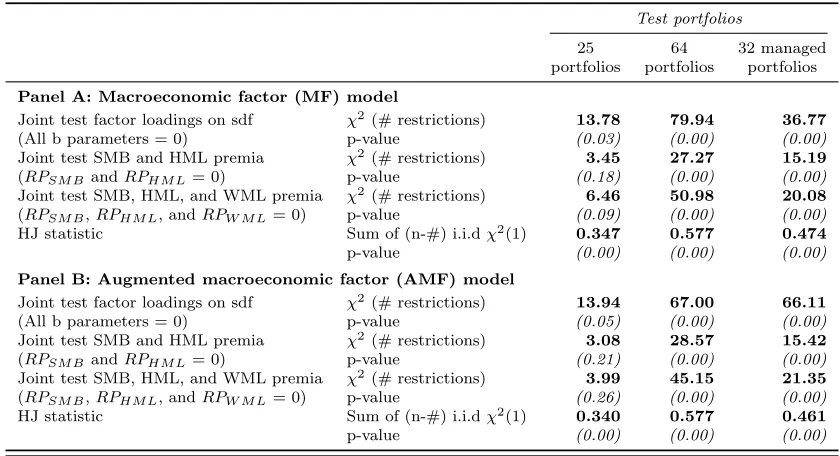

We show our results based on the 64 test portfolios in Table 6. Several of the macroeconomic

fun-damentals capture variation in the stochastic discount factor, i.e., MYP, DSV, ATS, STS, and FX are

all highly significant at conventional levels. However, a different set of pricing factors could command

a significant risk premium, as the macroeconomic fundamentals are highly correlated (Cochrane, 2001,

pp.260-262). Notwithstanding this argumentation, we find that the same macroeconomic

fundamen-tals are priced at the 99% confidence level. Augmenting the MF model by adding the orthogonalized

market return (RM*) does turn the loading on the stochastic discount factor and the risk premium of

UI significant, while it renders the risk premium of STS insignificant. In addition, the risk premium

on DSV is now only significant at the 95% confidence level. The RM* factor obtains a significant

stochastic discount factor loading and risk premium, and its inclusion in the MF model increases the

adjusted R2 from 30.9% to 35.9%.13

The sign of the risk premia are in accordance with economic intuition. We have already shown

that high (low) BM assets often have small (large) positive MYP betas and small (large) negative STS

betas. In light of the more negative risk premium on MYP than on STS and the almost equal spread in

exposures on these macroeconomic fundamentals, MYP can help to explain the average return spread

between BM portfolios. Similarly, small (big) size assets have large (small) positive DSV betas and

small (large) negative ATS betas, with the spread in the DSV betas being much larger than that in the

ATS betas. In combination with a positive risk premium, DSV can help to explain the average return

spread in the size portfolios. Finally, high (low) momentum assets have small (large) positive DSV

betas, large (small) negative STS betas and small negative (small positive) FX betas. As a result,

the positive risk premium on DSV drives up the average return prediction of losers relative to that

of winners, while the negative risk premium on STS drives the same down to a slightly lower extent.

Hence, we conclude that the macroeconomic fundamentals seem unable to explain momentum.

Our empirical outcomes on the FF and C models are consistent with prior studies. All the FF and

C benchmark factors strongly associate with the stochastic discount factor and also obtain significant

risk premia. The significant risk premium on SMB reveals that the size effect has re-emerged over the

last years. Our evaluation statistics (i.e., the adjusted R2s and the J-tests) and Figure 2 suggest that

13As a robustness check, we also use the Fama and MacBeth (1973) methodology to compute the risk premia of the

the MF and FF models cannot correctly capture variation in the equity prices of the 64 portfolios,

with the MF model working slightly better than the FF model. The C model displays the best pricing

ability, which is not surprising given that its pricing factors include a momentum portfolio (WML).

Our empirical analysis indicates that foreign exchange rate risk can be important when pricing the

cross-section of average equity returns, as FX loads significantly on the stochastic discount factor and

also attracts a significant risk premium. In contrast, inflation risk becomes only important once we

add the orthogonalized market return to the other pricing factors. Again, we find it illuminating to

compare our asset pricing results with those obtained in the prior literature. Two major differences

should be highlighted and explained:

1. Hahn and Lee (2006) and Petkova (2006) fail to obtain a significant risk premium on changes in

aggregate default risk in their cross-sectional tests. In contrast, DSV commands a significantly

positive risk premium in our tests. The difference can be explained by noting that prior studies

use the credit spread as their proxy for default risk. In this context, the findings of Longstaff et al.

(2005) and Elton et al. (2001) are interesting, which suggest that the credit spread only partially

reflects default risk (mostly <50%). Our contingent claims analysis-based proxy appears more

powerful in reflecting changes in the aggregate default probability.

2. Petkova (2006) shows that economic growth risk, computed using a methodology similar to ours,

does not command a significant risk premium in the presence of other pricing factors. We cannot

confirm this finding. While MYP and STS exhibit a high degree of correlation and clearly carry

important common information, exposures to both macroeconomic fundamentals significantly

explain average returns and both attract significant risk premia in our analysis.

4.3 Conditional Pricing Tests

Following earlier studies, e.g., Hodrick and Zhang (2001) or Cochrane (1996), we also consider the

pricing ability of the unconditional pricing models on conditional assets, i.e., on assets with

time-varying weights equivalent to dynamic trading strategies.14 To this end, we multiply the (2x2x2)

three-way sorted portfolios by an instrument set, which contains a constant, the aggregate dividend yield,

the default yield spread, and the government bond term spread, to obtain 32 managed portfolios. In

this way, the magnitude of the long and the short positions in the eight zero investment portfolios

depends on the business cycle. More information on the definition of the instruments is offered in

the footnote of Table 7. The instruments are lagged by two periods to avoid overlap with the test

assets. We ensure that the assets’ scale is roughly equal by subtracting 0.04 from the dividend yield

and multiplying all instruments by 100 (Cochrane, 1996, p.588). Given the evidence in Lewellen et al.

(2006), it is important to compare the estimates, significance, and pricing ability of the models across

alternative test portfolios to assess the robustness of our prior outcomes.

Our estimation outcomes reported in Table 7 and shown in Figure 3 suggest that the MF model

does slightly better than the FF model and somewhat worse than the C model in pricing the 32 test

portfolios. The links between the macroeconomic fundamentals and the stochastic discount factor and

the risk premia are often close to those found on the unconditional test assets. Two notable exceptions

are that the loadings of MYP and FX on the stochastic discount factor and their risk premia are no

longer significant. The differences in significance are very likely driven by smaller spreads in average

returns on the test portfolios, and thus lower statistical power. When regarding the AMF model, RM*

again loads significantly on the stochastic discount factor and also obtains a significant risk premium.

Surprisingly, however, the sign of the RM* estimates has changed. Our estimation outcomes on the

FF and C models are almost equal to those found previously. An important difference is that, in both

models, SMB no longer commands a significant risk premium at the 95% confidence level, indicating

that the characteristic-factor models also suffer from the lower spreads in average portfolio returns.

Overall, all models seem fairly capable of correctly pricing the 32 conditional portfolios.

4.4 Incremental Pricing Ability of HML, SMB, and WML

Our earlier results are informative about the relative pricing performance of the three models. An

al-ternative perspective is to consider the incremental pricing ability of the FF and C benchmark factors

when added to the MF (or AMF) model. If the FF and C factors do not contain incremental

informa-tion, the macroeconomic fundamentals should drive out their significant risk premia. In Table 8, we

offer the outcomes from model specification tests and tests of incremental pricing ability. The model

funda-mentals are always jointly significant and that the Hansen-Jagannathan (HJ) distance always rejects

the MF and AMF models at conventional levels (see Hansen and Jagannathan, 1997; Jagannathan

and Wang, 1996, on computation and asymptotic distribution of the HJ distance).

Our tests of incremental pricing ability reveal that neither the benchmark factors specified by the

FF model nor those specified by the C model contain incremental information beyond our

macroe-conomic fundamentals when pricing BM and size-sorted assets. Focusing first on the unconditional

models, if we add HML and SMB or HML, SMB and WML to the macroeconomic fundamentals, the

risk premia on the FF benchmark factors or the C benchmark factors are jointly insignificant on the

25 portfolios. Our evidence hence suggests that the macroeconomic fundamentals adequately capture

risks associated with BM and size. We can draw the same conclusions when we consider the AMF

model. Further, when we analyze three-way sorted portfolio, i.e., the 64 unconditional portfolios or

the 32 conditional portfolios, then the macroeconomic fundamentals can never drive out the significant

risk premia of the FF or C benchmark factors. We conclude that HML and SMB or HML, SMB and

WML contain information not captured by the macroeconomic fundamentals which is necessary to

correctly price portfolios reflecting risks associated with BM, size and momentum.

Overall, these results strongly suggest that the success of the FF model in pricing BM and

size-sorted test assets stems from its ability to capture exposures to the macroeconomic factors included

in our MF model. In summary, the pricing ability of the MF and the FF models are comparable on

characteristic portfolios and on alternative portfolios. Also, when we use BM and size test portfolios

the macroeconomic fundamentals render the FF benchmark factors’ risk premia insignificant. At the

same time, the C model outperforms both the MF and AMF models, as well as the FF model.

5

Robustness Tests

Our analysis is complicated by the fact that proxy variables often only imprecisely measure the true

macroeconomic fundamentals explaining variation in equity returns and prices. One manifestation of

this problem is that macroeconomic proxy variables normally relate more weakly to the cross-section

of average equity returns than return-based pricing factors, as, e.g., HML, SMB and WML (see the

discussion in Cochrane, 2001). A reason for the weaker relation is that, as a result of reporting lags, it

macroeconomic data are subject to subsequent revisions, e.g., when the definition of a macroeconomic

indicator changes, implying that investors at the time perceived different shocks to the macroeconomic

fundamentals than those suggested by the revised data. Finally, macroeconomic proxy variables are

often summary measures of broader phenomena, e.g., in our study we attempt to capture the whole

term structure of interest rates through its average level and its slope. The imprecise nature of the

macroeconomic data implies that it is important to verify that our main conclusions are not driven

by our choice of proxy variables. This is the objective of this section.15

MYP:(1) We re-compute the mimicking portfolio using real-time data from the Federal Reserve

Bank of Philadelphia. The real-time data feature the realizations of the industrial production index

as experienced by market participants at the time. Our findings reveal that our previous conclusions

continue to hold, although the relations between HML and STS and between SMB and ATS are now

only significant at the 90% confidence level. (2) If the base assets’ ability to reflect news changes over

time, then our assumption of constant mimicking portfolio weights could be problematic. As a result,

we also compute MYP using recursive out-of-sample windows of initially 48 observations. Although

we are unable to adjust standard errors for the additional uncertainty induced through MYP in this

setting, our unadjusted outcomes reveal that all benchmark risk factors now reflect economic growth

risk at the 99% confidence level. In addition, HML now relates significantly to DSV and ATS and

no longer to STS, while SMB does no longer capture interest rate risk. In the cross-sectional tests,

UI now commands a significant risk premium, whereas the risk premium on STS, while still being

significant, changes its sign. Other findings are qualitatively similar.

(3) Another concern is that the mimicking portfolio simply proxies for the market portfolio, one of

its base assets. We therefore replace the market portfolio with (a) eight three-way sorted benchmark

portfolios and (b) five industry portfolios from Kenneth French’s website. The factor loadings on HML

are -1.55 (t-statistic of -1.19)16 and -1.98 (t-statistic of -2.35), respectively. In both cases, the MYP

risk premium is significant at the 90% confidence level (t-statistics of -1.87 and -2.13, respectively).

Other findings remain unaffected, except that HML no longer relates to STS and the FX risk premium

15We thank our referee for motivating this analysis. Note that we only shortly summarize the main findings from our

robustness checks in this section. A more detailed description including tables can be obtained upon request.

16When we include the three-way sorted benchmark risk factors in the mimicking portfolio, the moments from the

is no longer significant in the first case.17 (4) As a further check, if MYP simply proxies for the market

portfolio, we should be able to replace it with the market portfolio and still find similar results. Our

evidence reveals that the spread in the market portfolio exposures across the BM deciles is, at best,

weak (from 1.18 to 0.83). In combination with an estimated market risk premium of 0.80%, the market

portfolioreduces the expected return prediction on a BM spread portfolio (BM10-BM1) by 0.22%. As

MYP increases this prediction by 0.47%, these pricing factors cannot be equivalent.

UI:We also construct UI from recursive out-of-sample windows of initially ten years. As the

cor-relation coefficient between our in-sample and our out-of-sample estimate of UI equals approximately

0.95, none of our main findings were substantially affected.

DSV:Although our proxy variable derived from Merton’s (1974) contingent claim analysis should

reflect changes in aggregate default risk more accurately than others based on bond data (see Elton

et al., 2001), we also check whether our main outcomes continue to hold under these alternative proxy

variables. To this end, we first replace DSV with the return spread between a high-yield corporate

bond portfolio and a long-term government bond portfolio. In this case, the new default risk proxy

still associates positively and significantly with SMB, but not with WML. We also find that the slope

coefficients of the interest rate variables become less significant, with, however, only ATS turning

insignificant. The lower significance levels can be explained by the fact that the new default risk proxy

also captures interest rate risk (i.e., its correlation coefficients with ATS and STS are 0.50 and 0.26,

respectively). The link between WML and FX disappears, too. Although risk premia estimates are

similar to before, they show lower significance levels, i.e., only MYP, ATS and surprisingly UI are now

significant. In contrast, when we proxy for changes in aggregate default risk through the change in the

yield spread between a high-yield corporate bond portfolio and a long-term government bond portfolio

(which should relate negatively to DSV), then our outcomes align far more closely with those in the

tables. Two important differences are that SMB now relates significantly to STS (and not to ATS)

and that UI attracts a significant risk premium in the cross-sectional tests.

ATS and STS:Most other studies use one and not two proxy variables to capture news on the

term structure. As a result, we investigate whether it is important to approximate the term structure

17The missing link between HML and STS can be explained by the fact that assets with a high interest rate sensitivity

through both its average level and through its slope by including either ATS or STS in our tests. Our

outcomes reveal that HML and WML only reflect changes in the slope of the term structure (STS), i.e.,

the absence of STS fails to render the loading of ATS on HML or WML significant. In contrast, SMB

only captures changes in the average level of the term structure (ATS). Other time-series relations,

risk premia and significance levels are close to those shown before.

FX:(1) We first replace the nominal version of the broad foreign exchange rate index with its real

(i.e., inflation-adjusted) version. This does not change any of our main conclusions. (2) We also split

the broad index into one capturing exchange rates with respect to major trading partners and one

capturing exchange rates with respect to minor trading partners. The main idea is that, in theory, an

international pricing model should include exchange rates with respect to all other countries. However,

the exchange rates with respect to major trading partners should be more important than those with

respect to minor trading partners. Our findings show that WML only reflects foreign exchange rate

risk with respect to major trading partners at the 95% confidence level. Other factor loadings and

their significance levels remain close to before. In the cross-sectional pricing tests, however, we find

that both FX indexes command a significant positive risk premium, with other risk premia not being

greatly altered. (3) Finally, as only FX can be forecasted with a positive adjusted R2 in the

out-of-sample VAR tests, we replace it with the residual from an ARIMA(1,0,1). In this case, both HML

and SMB suddenly reflect exchange rate risk, while the loading of FX on WML turns insignificant.

Further, the slope coefficient of UI on HML and SMB is now significant at the 90% confidence level.

In the cross-sectional tests, the risk premium on FX is now very close to zero.

Overall, our main conclusions seem largely robust with respect to our choice of macroeconomic

proxy variables. Next, even if one of our main findings changes, we can often explain the inconsistency

through an undesirable feature of the alternative proxy variable. However, we agree that our robustness

checks only consider alternative proxy variables, and not necessarily efficient measures of the true

macroeconomic fundamentals. As a result, one cannot completely rule out that the relations between

the benchmark risk factors and the true macroeconomic fundamentals could be different from those

6

Conclusion

Several recent studies illustrate that the success of the Fama and French (1997, 1996) model in pricing

characteristic-sorted portfolios is attributable to its ability to capture information on macroeconomic

risk factors. However, as most of these studies analyze one macroeconomic fundamental or at best

a narrow set of them (e.g., see Hahn and Lee, 2006; Petkova, 2006; Vassalou and Xing, 2004;

Vassa-lou, 2003), their empirical findings are not completely unambiguous. We contribute to this literature

through a multivariate analysis based on a more comprehensive set of macroeconomic fundamentals.

Our model controls for correlation between macroeconomic fundamentals considered in the prior

lit-erature, and it adds to them unexpected inflation and shocks to a compound U.S. dollar exchange

rate. Further, we examine for the first time the relation between the momentum-based factor WML

(see Carhart, 1997) and macroeconomic fundamentals. Finally, we follow the advise of Connor et al.

(2006) and Fama (1998, 1996) and deal with the confounding impact of the market return on the other

pricing factors by orthogonalized it with respect to the macroeconomic fundamentals.

Our analysis reveals that macroeconomic fundamentals exhibit strong contemporaneous links, and

that changes in economic growth expectations and the term structure Granger-cause several of the

other macroeconomic fundamentals. We also show that the macroeconomic fundamentals seem more

elementary than the benchmark risk factor. Next, our empirical tests confirm much of the evidence

reported in prior studies. For example, we show that BM conveys useful information about term

structure risk, and size about default risk. However, we also obtain results that directly contradict

prior research. Specifically, BM does not proxy for default risk exposure after controlling for term

structure risk. Furthermore, BM reflects exposure to economic growth risk with the opposite sign to

that reported in the prior literature. Similarly, size conveys information about term structure risk.

We also report results entirely new to the literature. For example, we find that WML is significantly

associated with default, term structure and foreign exchange rate risks.

In various cross-sectional pricing tests, we first document that the majority of the macroeconomic

fundamentals command significant risk premia. More importantly, we find that, on three-way sorted

BM, size, and momentum portfolios, the MF model can compete with the FF model in terms of pricing

ability, but not with the C model. The pricing performance of the models is more similar when we

portfolios, the macroeconomic fundamentals render the risk premia on the FF benchmark factors and

the C benchmark factors insignificant. In contrast, they cannot render the risk premia on either set of

benchmark factors insignificant when we run our tests on three-way sorted BM, size and momentum

portfolios. As a result, the ability of the C model to price momentum-sorted portfolios cannot be

explained by the macroeconomic fundamentals considered in our study.

Ultimately, our results suggest that style-based equity investment strategies are associated with

dif-ferent macroeconomic exposures. This has potentially important implications for long-term investors,

e.g., pension funds, seeking to hedge liabilities with macroeconomic exposures through the equities

markets. As an investor’s liabilities depend on macroeconomic factors, such as the term structure,

economic growth, inflation, and the exchange rate, our results suggest that style investing can have a

References

Breeden, D. T., Gibbons, M. R., Litzenberger, R. H., 1989. Empirical tests of the consumption-based

CAPM. Journal of Finance 44 (2), 231–263.

Breen, W., Glosten, L. R., Jagannathan, R., 1989. Economic significance of predictable variation in

stock index returns. Journal of Finance 44, 1177–1190.

Brennan, M. J., Wang, A. W., Xia, Y., 2004. Estimation and test of a simple model of intertemporal

capital asset pricing. Journal of Finance 59 (4), 1743–1775.

Campbell, J. Y., 1987. Stock returns and the term structure. Journal of Financial Economics 18,

373–399.

Campbell, J. Y., 1993. Intertemporal asset pricing without consumption data. American Economic

Review 83 (3), 487–512.

Carhart, M. M., 1997. On persistence in mutual fund performance. Journal of Finance 52 (1), 57–82.

Chan, K. C., Chen, N. F., Hsieh, D. A., 1985. An explanatory investigation of the firm size effect.

Journal of Financial Economics 14, 451–471.

Chen, N. F., 1991. Financial investment opportunities and the macroeconomy. Journal of Finance

46 (2), 529–554.

Chen, N. F., Roll, R., Ross, S. A., 1986. Economic forces and the stock market. Journal of Business

59 (3), 383–403.

Chordia, T., Shivakumar, L., 2002. Momentum, business cycle, and time–varying expected returns.

Journal of Finance 57 (2), 985–1019.

Cochrane, J. H., 1996. A cross-sectional test of an investment-based asset pricing model. Journal of

Political Economy 104, 572–621.

Cochrane, J. H., 2001. Asset pricing. Princeton University Press, New Jersey.

Connor, G., Goldberg, L., Korajczyk, R., 2006. Portfolio risk forecasting, Notes on Chapter 6, The

Connor, G., Korajczyk, R., 1995. The arbitrage pricing theory and multifactor models of asset returns.

In: Jarrow, R., Maksimovic, V., Ziemba, W. (Eds.), Finance, Handbooks in Operations Research

and Management Science. North Holland, Amsterdam.

Cooper, M. J., Gutierrez, R. C., Hameed, A., 2004. Market states and momentum. Journal of Finance

59 (3), 1345–1365.

Doidge, C., Griffin, J. M., Williamson, R., 2006. Measuring the economic importance of exchange rate

exposure. Journal of Empirical Finance 13 (4-5), 550–576.

Elton, E. J., Gruber, M. J., Agrawal, D., Mann, C., 2001. Explaining the rate spread on corporate

bonds. Journal of Finance 56 (1), 1229–1256.

Fama, E. F., 1996. Multifactor portfolio efficiency and multifactor asset pricing. Journal of Financial

and Quantitative Studies 31 (4), 441–465.

Fama, E. F., 1998. Determining the number of priced state variables in the ICAPM. Journal of

Financial and Quantitative Studies 33 (2), 217–231.

Fama, E. F., French, K. R., 1988. Dividend yields and expected stock returns. Journal of Financial

Economics 22, 3–25.

Fama, E. F., French, K. R., 1989. Business conditions and expected stock returns. Journal of Financial

Economics 25, 23–50.

Fama, E. F., French, K. R., 1992. The cross-section of expected stock returns. Journal of Finance

47 (2), 427–465.

Fama, E. F., French, K. R., 1993. Common risk factors in the returns on stocks and bonds. Journal

of Financial Economics 33 (1), 3–56.

Fama, E. F., French, K. R., 1996. Multifactor explanations of asset pricing anomalies. Journal of

Finance 51 (1), 55–84.