ISSN: 2306-9007 Javed, Nawaz & Gondal (2014) 222

I

www.irmbrjournal.com March 2014I

nternationalR

eview ofM

anagement andB

usinessR

esearchV

ol. 3 Issue.1R

M

B

R

Impact of Financial Developments on an Economic

Performance: A Study of Pakistan

TARIQ JAVED

PhD Scholar, MAJU Islamabad Pakistan Email: [email protected]

Tel: +923335291792

SANIA NAWAZ

PhD Scholar, MAJU Islamabad Pakistan Email: [email protected]

MAQBOOL AHMED GONDAL

Director General Audit Government of PakistanEmail: [email protected]

Abstract

This paper investigates the role of financial development toward economic performance in Pakistan. To examine the role of financial development on economic performance in Pakistan we have taken 42 years’ time period. The regression analysis is used to check the relationship among variables. Findings of the study suggest that GDP growth is having highly significant and positive relationship with domestic credit, imports and exports. However GDP growth is having negative relationship with trade openness and liquid liabilities. Results also suggest that there is a need of relaxation of monetary policy to distribute productive credit in business community. This expansion of funds will improve productivity and positive impact on GDP growth.

Key Words: GDP,OLS, Trade Openness, Productive, Domestic Credit, Imports.

Introduction

Economic growth of a country is dependent on different elements, each one of them plays an important

role in the achievement ofeconomic goals. Among these elements financial development is very important, relationship between economic performance and financial development has been discussed dating back to 1873 by Bagehot. Kıran, Yavuz and Güriş (2009) argue that the financial development plays fundamental role in the process of economic growth. They further argue that in the policy development process the direction of causality between financial development and economic growth has different implications. “Economists hold different views on the existence and direction of causality” in this context (Al-Yousif, 2002). Financial development is a source of economic growth; it allocates resources to the more productive sectors of the economy. The basic reason of positive impact on the economic growth from financial structure is an efficient undertaking of investment. Significant attention has been given to its empirical aspect by Bagehot (1873) and Schumpeter (1912).ISSN: 2306-9007 Javed, Nawaz & Gondal (2014) 223

I

www.irmbrjournal.com March 2014I

nternationalR

eview ofM

anagement andB

usinessR

esearchV

ol. 3 Issue.1R

M

B

R

development towards economic performance, which was a motivational factor and basic reasons to restrict our study tothe economy of Pakistan. According to (Aghion et al. 1999) countries with less developed financial systemare having highly volatile economic growth.

This study is designed to find out the impact of financial developments on an economic performance in Pakistan. Different proxies are used to capture the financial development i.e. Domestic Credit, private sector credit, liquid liabilities, exports, government expenditures, imports inflation, trade openness and capital formation. Economic performance is measure by per capita GDP growth. Results indicate that the government should have financial reforms to extend productive loan to businesses without political influence. In addition they should make economic reforms to control inflation, non productive government expenditure, and import of capital goods rather than consumer goods.

Literature Review

Friedman and Schwartz (1963) argue that finance in fact responds to the changes in the real sector. When there is an economic growth this creates demands for the development of financial institutions and services. According to Patrick (1966) there is a transfer of resources from low growth sectors to the modern high growth sector which stimulates an entrepreneurial response in these modern sectors. Lucas (1988) rejected the proposition that there is any relationship between finance and growth. Demetriades and Hussein (1996), Greenwood and Smith (1997) pointed out bi-directional relationship between economic growth and financial development.

The above defined four views have been summarized by Apergis et al., (2007) as:

demand following view

supply-leading view

no relationship between finance and growth

mutual impact of finance and growth

Different studies have different opinions about the relationship between financial development and economic growth. The empirical results are not consistent. According to Pagano (1993) secured growth rate is positively dependent on ratio of saving diverted towards investment. Berthelemy and Varoudakis (1996) argued by using theoretical model that the economic growth rate is positively dependent on the number of banks or degree of competitiveness in the financial system in an economy.

Different empirical studies give ambiguous results. The results of cross country and panel data studies give positive impact of financial development on growth. Whereas, time series studies have contradictory results. Chistopoulos and Tsionas (2004) used a panel co-integration analyses to examine a long-run relationship between financial development and economic growth of developing countries, their results found a uni-directional relationship from financial development to economic growth. According to Al-Awad and Harb (2005) there may be a direct relationship between financial development and growth in the long run, their analysis was based on panel co-integration and time-series co-integration. Apergis et al.(2007) find a positive relationship between financial depth and economic growth by using panel data co-integration. According to Demetriades and Hussein (1996) finance is a leading factor in the process of economic growth. Luintel and Khan (1999) examine the relationship between financial development and economic growth by using a sample of ten less developed countries and find a bi-directional causality between financial development and growth.

ISSN: 2306-9007 Javed, Nawaz & Gondal (2014) 224

I

www.irmbrjournal.com March 2014I

nternationalR

eview ofM

anagement andB

usinessR

esearchV

ol. 3 Issue.1R

M

B

R

According to Favara (2003) there is a conventional positive interpretation of financial development and economic growth which is based on an average effect that are difficult to interpret.

In an extensive review of theoretical and empirical work on the relationship between financial development and economic growth Levine (2005) concluded: Theory and empirical evidence make it difficult to conclude that the financial system merely and automatically responds to economic activity, or that financial development is an inconsequential addendum to the process of economic growth. In the recent studies there is a great number of contributions in academia like Beck and Levine, 2004, Favara, 2003, Loayza and Rancière, 2006, Saci et al., 2009) provided evidences of negative and significant impact of banking activities upon economic growth in the short-term.

Loayza and Rancière (2006) empirically investigated and provided an evidence that there is a significantly positive relationship between financial variables and economic growth in the long-run by means of a model with domestic credit by banks and other financial institutions as a percentage of GDP as their financial development variable and a number of other well established control variables. Their used technique is panel error correction model which allows the estimation of both short and long run effects from a general autoregressive distributed lags (ARDL) model. Loayza and Rancière (2006) argued that the phenomenon may be explained by the effect of financial liberalization. There is also another explanation suggested by Dell’Ariccia and Marquez (2006) and Rajan (1994) that the credit growth tends to be pro-cyclical (rates of growth in GDP tends to induce a high rate of growth in credit).

Favara (2003) found a strong relationship between domestic credit by banks and other financial institutions as a percentage of GDP and economic growth after controlling for the effect of inflation, government consumption to GDP, initial GDP per capita, domestic investment to GDP, average years of school of the population aged 15 and over, trade openness to GDP, black market premium and dummy legal origin variables. However, this strong relationship weakens when an instrumental variable (IV) estimation method is applied with dummy variable of the origins of the legal system of each country used as instruments.

Saci etal. (2009) estimated the relationship with annual data over the period 1988-2001 applying two-step GMM. They found that the variable domestic credit by banks and other financial institutions as a percentage of GDP has a significantly negative coefficient with stock market traded value over GDP. When stock market traded value over GDP is replaced by, stock market turnover ratio, the effect of domestic credit by banks and other financial institutions as a percentage of GDP became insignificant. However, in each case the effect of the stock market variables on growth is positive and significant.

Methodology

ISSN: 2306-9007 Javed, Nawaz & Gondal (2014) 225

I

www.irmbrjournal.com March 2014I

nternationalR

eview ofM

anagement andB

usinessR

esearchV

ol. 3 Issue.1R

M

B

R

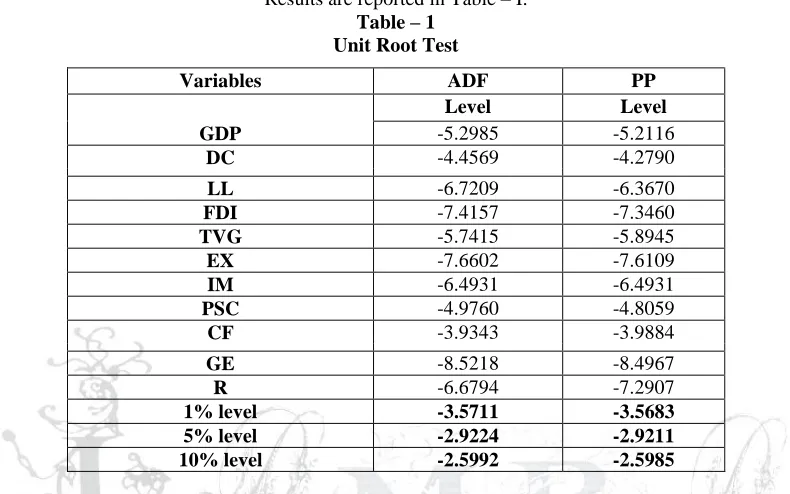

The data used for analysis is time series data, which may create problems for econometric model. The most popular test of stationary is “Unit Root Test”. Stationary proprieties of data are checked by applying augmented dickey fuller test (ADF) developed by Dickey and fuller (1981) and Phillips – Perron (PP) developed by Phillips and Perron (1988) unit root test. Both the test gave consistent results; all the variables are stationary at level.

Results are reported in Table – I.

Table – 1 Unit Root Test

Variables ADF PP

Level Level

GDP -5.2985 -5.2116

DC -4.4569 -4.2790

LL -6.7209 -6.3670

FDI -7.4157 -7.3460

TVG -5.7415 -5.8945

EX -7.6602 -7.6109

IM -6.4931 -6.4931

PSC -4.9760 -4.8059

CF -3.9343 -3.9884

GE -8.5218 -8.4967

R -6.6794 -7.2907

1% level -3.5711 -3.5683

5% level -2.9224 -2.9211

10% level -2.5992 -2.5985

One very important assumption of classical linear regression model is that the data should be homoskedastic, i.e. equal spread or variance. If problem of heteroscedasticity exists in the data the derived coefficients will be unbiased – the calculated β will be equal to true β, however derived out confidence interval and T-test and F-test will be misleading. Therefore if the problem of heteroskedasticity is not addressed and conclusion is drawn by using standard OLS regression package the inference we make may be ambiguous. The existence of heteroskedasticity is checked by applying “White Test”. The results indicate that there is no heteroskedasticity in the data; residuals are equally distributed – equal spread and variance.

The results are presented in Table – II.

Table – 2

Tests

Obs*R-squared

P-value

Breusch-Godfrey Serial Correlation LM Test 0.119658 0.9419

White Test 8.719608 0.1900

Another potential problem of time series is the existence of serial correlation commonly named as autocorrelation, serial correlation means correlation between the members of the series. The assumption of OLS is that there should not be an autocorrelation in the disturbance / error term. Simply the disturbance term relating to any observation should not be influenced by the disturbance term of another observation. In order to check the existence of autocorrelation “Breusch-Godfrey Serial Correlation LM Test” is applied. The results are presented in Table – II.

ISSN: 2306-9007 Javed, Nawaz & Gondal (2014) 226

I

www.irmbrjournal.com March 2014I

nternationalR

eview ofM

anagement andB

usinessR

esearchV

ol. 3 Issue.1R

M

B

R

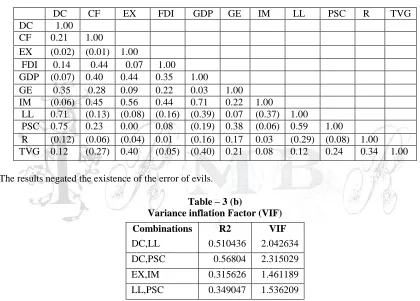

variables are indeterminate and have infinite standard errors. But if multicollinearity is less than perfect, the coefficients although determinate, has large standard errors – means coefficients cannot be estimated with great precision and accuracy. There will be a certain level of colinearity in the variables or the existence of imperfect multicollinearity is mandatory. Therefore correlation analyses are performed to find out co-movement among variables. Variables with high correlation value i.e. 0.5 or above are further analysed by applying “Variance Inflation Factor”. This method is used to find out whether the correlation is within tolerable limit. Multicolinearity for all the variables is within acceptable limit. Asteriou (2007) said that acceptable limit is VIF = 10.

VIF = (1/1-R2)

The results of VIF are reported in Table – III (b)

Table – 3 (a) Correlation Matrix

The results negated the existence of the error of evils.

Table – 3 (b)

Variance inflation Factor (VIF)

Combinations R2 VIF

DC,LL 0.510436 2.042634 DC,PSC 0.56804 2.315029 EX,IM 0.315626 1.461189 LL,PSC 0.349047 1.536209

The fourth assumption of OLS is that the model should not be functionally miss-specified. The functional specification is checked by “Ramsey RESET Test”. The value is F-statistic is 0.1431 is statistically insignificant, similarly FITTED^2 is also insignificant. It means that the model is not functionally miss-specified.

Regression Analysis

The regression analysis is used to examine the impact of financial development on economic growth. Where the GDP is used as the proxy of economic development (Y) is dependent variable. Financial development is independent variables and the proxies of financial development are private sector credit (PSC), liquid liabilities (LL), domestic credit (DC), government expenditures (GE), capital formation (CF), trade openness (TVG), foreign direct investment (FDI), exports (EX), imports (IM) and inflation(R).

DC CF EX FDI GDP GE IM LL PSC R TVG

DC 1.00

CF 0.21 1.00

EX (0.02) (0.01) 1.00

FDI 0.14 0.44 0.07 1.00 GDP (0.07) 0.40 0.44 0.35 1.00

GE 0.35 0.28 0.09 0.22 0.03 1.00 IM (0.06) 0.45 0.56 0.44 0.71 0.22 1.00

LL 0.71 (0.13) (0.08) (0.16) (0.39) 0.07 (0.37) 1.00

PSC 0.75 0.23 0.00 0.08 (0.19) 0.38 (0.06) 0.59 1.00

ISSN: 2306-9007 Javed, Nawaz & Gondal (2014) 227

I

www.irmbrjournal.com March 2014I

nternationalR

eview ofM

anagement andB

usinessR

esearchV

ol. 3 Issue.1R

M

B

R

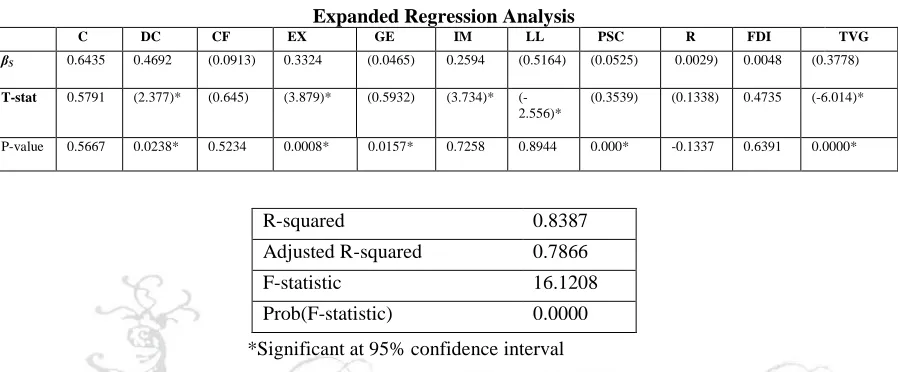

Y = α + β1PSC + β2LL+β3DC + β4GE+β5CF+ β6TVG + β7FDI + β8EX + β9IM +β10R+µ

Different variables have been used in the literature to find out an impact of financial development on an economic system, which may have potential impact on the economic performance. However initial regression was run to find out the impact of financial development on the economic performance. Some of the variables are insignificant at 5% level of significance as evident by the t-stat and P-value enumerated in Table - IV.

Table – 4

Expanded Regression Analysis

C DC CF EX GE IM LL PSC R FDI TVG

βS 0.6435 0.4692 (0.0913) 0.3324 (0.0465) 0.2594 (0.5164) (0.0525) 0.0029) 0.0048 (0.3778)

T-stat 0.5791 (2.377)* (0.645) (3.879)* (0.5932) (3.734)* (-2.556)*

(0.3539) (0.1338) 0.4735 (-6.014)*

P-value 0.5667 0.0238* 0.5234 0.0008* 0.0157* 0.7258 0.8944 0.000* -0.1337 0.6391 0.0000*

*Significant at 95% confidence interval

Explanatory power of the variables is also strong as evident by R-squared and adjusted R-squared which have respective values of 0.8387 and 0.78669. Explanatory power means the growth in GDP is significantly explained by the independent variables incorporated in the model. Adjusted R-squared is a more conservative estimate of the percent of variance explained.

The overall significance of the mode is tested by "F value'' and "Prob(F)'' statistics, they test the Null hypothesis against all the regression coefficients are equal to zero. Its value would range from Zero to an arbitrarily large number. The lowest value of Prob(F) would imply that at least some of the regression parameters are non zero and the regression equation does have some validity in fitting the data. The probability of F-Stat is very low i.e. 0.0000, it indicates the fitness of the underlying model.

Some of the variables incorporated in the model are significant and some are insignificant, here an important decision is that whether all these variables should be a part of the model or some of the variables may be excluded from the model. Therefore “Redundant Variables Test” is applied to find out whether these variables if excluded from the model will change the explanatory power or significance of the left-over variables. “Redundant Variables Test” is run on each variable and found insignificant value for certain variables, which recommends that if these variables may not be a part of the model will not significantly change explanatory power of the model. Therefore these variables may be excluded from the model.

Interpretation

The new model with the reduced variables is as under:

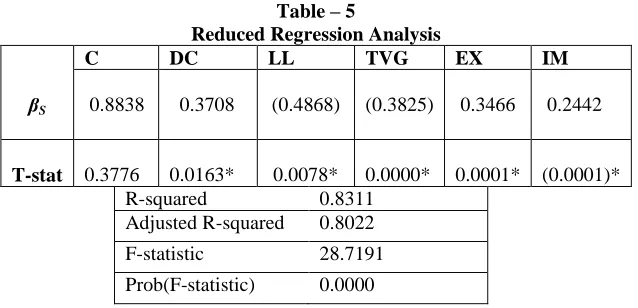

Y = α + β1DC + β2LL+β3TVG +β4EX+ β5IM +µ

The results of regression analysis are presented in the Table – V.

R-squared 0.8387

Adjusted R-squared 0.7866

F-statistic 16.1208

ISSN: 2306-9007 Javed, Nawaz & Gondal (2014) 228

I

www.irmbrjournal.com March 2014I

nternationalR

eview ofM

anagement andB

usinessR

esearchV

ol. 3 Issue.1R

M

B

R

Table – 5

Reduced Regression Analysis

C DC LL TVG EX IM

βS 0.8838 0.3708 (0.4868) (0.3825) 0.3466 0.2442

T-stat 0.3776 0.0163* 0.0078* 0.0000* 0.0001* (0.0001)*

R-squared 0.8311

Adjusted R-squared 0.8022 F-statistic 28.7191 Prob(F-statistic) 0.0000

All the left over variables are significant and explanatory power of the model is also significantly high. Prob(F) represents goodness of fit which is also significant. Therefore it can be argued that the model significantly explains the economic performance on the basis of financial developments in Pakistan.

The coefficient of domestic credit is significantly positive. In statistical terms the significant means probably true. This implies that 1 unit increase in Domestic Credit will cause a growth of 0.3708 units in per capita GDP. This gives a positive indication towards private sector investment and suggests that domestic credit should be extended in an economy which will significantly contribute in the economic development and growth. Higher economic growth will ultimately improve standards of living and welfare. The results are consistent with those of Berthelemy and Varoudakis (1996) Levine (1998) Beck and Levine (2004) and contradict with those of Beck and Levine (2004), Favara (2003), Loayza and Rancière, (2006), Saci et al., (2009).

Regression analysis indicates that liquid liabilities have significant negative value which exhibits that 1 unit growth in liquid liabilities has negative 0.4868 unit impact on per capita GDP growth. The banking liabilities are the deposits by the residents; they extort their funds from business or suspend their expansion plans and prefer to keep deposits with the financial institutions. These increased deposits haul out investment from the business, which ultimately negatively affects the productivity. However these deposits are channelized by the financial institutions through direct investment or through lending to other businesses which positively contributes in productivity.

Trade value of goods is taken as a proxy for trade openness, which has negative significant impact on per capita GDP growth. This indicates that as trade barriers are relaxed it causes to negatively affect the GDP; the possible reason is that imports of consumer goods dominate the capital goods and exports in monetary terms. People prefer to use imported goods rather than local products which cause low production and input in national productivity. Therefore for the period under study trade openness will negatively affect the GDP growth for Pakistan.

Exports have positive significant relationship with per capita GDP growth. The coefficient value indicates that 1 unit increase in exports will causes to improve GDP growth by 0.3466 units. Exports are considered to be acatalyst of economic growth, which increase per capita income which leads towards higher purchasing power and ultimately causes technology transfer. This technology transfer improves production and ultimately improves economic conditions by improving GDP. Higher exports may cause improvement in employment, balance of payment and living standard of people.

ISSN: 2306-9007 Javed, Nawaz & Gondal (2014) 229

I

www.irmbrjournal.com March 2014I

nternationalR

eview ofM

anagement andB

usinessR

esearchV

ol. 3 Issue.1R

M

B

R

two types i.e. capital goods – which are used to manufacture more goods or services – and consumable goods – which do not contribute in national GDP – rather countries spend significant foreign exchange on them. Therefore the capital goods improve GDP because they improve national productivity, however the consumer items do not add anything in national economic system. In the case of study under reference time is span is around 42 years which covers the period of industrialization and nationalization, therefore most of the imports during this period was of capital goods which contributed in the national development and causes positive impact over GDP growth.

Conclusion and Policy Implication

This paper examines the role of financial development towards economic performance in Pakistan. The analysis is performed on 42 years which is considered to be as significant period for observing long-term financial impact. At the same time itcovers financial development and liberalization along with output expansion, flow of investment, money growth, phases of financial institutions development and industrialization in Pakistan. Different proxies aligned with the literature have been used to measure the financial development and economic performance. In the process of data analysis ADF and PP unit root test is applied to examine the stationary characteristics in data. Both the variables suggested that the series are stationary at I(0) (level). The residuals are normally distributed; there is no autocorrelation and heteroskedasticity. Co-movement of the variables is also within the tolerable limit and functional form of the model is also correct.

The findings suggest that Domestic Credit, Exports and imports have highly significant positive relationship with GDP growth over the sample period. Other variables like Liquid liabilities and trade openness - measured as trade value of good – have negative relationship with GDP growth in the sample period.

Results also suggest that monetary policy should be relaxed to distribute productive credit in the business community which is a back bone of any economic system. The availability of funds will facilitate expansion programs and ultimately improve productivity. This enhanced productivity will make the goods available to local as well as international consumers. Moreover expansion programs will also facilitate import of capital goods and technology transfer which likewise have direct impact on growth in GDP. However the point of consideration specifically for developing countries like Pakistan is that they should discourage the import of luxurious and consumer goods, as these have negative impact on GDP growth.

Sound financial system causes higher economic growth,this makes availability of goods at cheap rates and improves living standard. Consequently, it is strongly recommended that government should bring in reforms to control inflation this will have positive impact on economic growth. An efficient allocation of resources will also improve economic performance. The core point in public policy is an economic improvement by creating employment and poverty reduction. It is equally important to bring financial reforms in the country to have significant impact on an economic growth.

The planners in the financial sector should take it as a challenge to restructure the financial sector. They should promote private lending to productive businesses and energy sector which will make dead units alive. They should ensure lending at lowest possible default risk and proper management as mismanagement will welcome mega disaster. The government should ensure the lowest level of nonperforming loans; financial institution should not have any politic influence. All the economic decisions should be supportive to economic performance. They should not be made on the political grounds.

Further Research

ISSN: 2306-9007 Javed, Nawaz & Gondal (2014) 230

I

www.irmbrjournal.com March 2014I

nternationalR

eview ofM

anagement andB

usinessR

esearchV

ol. 3 Issue.1R

M

B

R

factor productivity. Levin (1998) used legal system as an instrumental variable. Berthelemy and Varoudakis (1996) argued that educational system is pre-conditional for economic development. Therefore the stock market development, rate of private savings, total factor productivity, educational level and legal system of Pakistan may also be incorporated on the model to assess their role towards economic performance. This model would give comprehensive view to financial and economic policy makers.

References

Aghion P., A. Banerjee, and T. Piketty (1999). Dualism and Macroeconomic Volatility. Quarterly Journal of Economics,114(4):1359-1397

Al-Awad, M., and N. Harb, 2005. “Financial Development and Economic Growth in the Middle East” Applied Financial Economics15, pp. 1041-1051.

Al-Yousif, Y.K., 2002. “Financial Development and Economic Growth. Another Look at the Evidence from Developing Countries” Review of Financial Economics11, pp. 131-150.

Apergis, N., I., Filippidis and C. Economidou,2007. “Financial Deeping and Economic Growth Linkages: A Panel Data Analysis” Review of World Economics143, pp. 179-198.

Bagehot, W., 1873. Lombard Street, Homewood, IL: Richard D. Irwin.

Beck, T and A Demirgüç-Kunt (2009): “Financial institutions and markets across countries and over time: data and analysis”, World Bank Policy Research Working Papers, no 4943.

Beck, T. & Levine, R. (2004) Stock markets, banks and growth: panel evidence. Journal of Banking and Finance, 28, 423-442.

Beck, T. & Levine, R. (2004) Stock markets, banks and growth: panel evidence. Journal of Banking and Finance, 28, 423-442.

Beck, T., Levine, R. & Loayza, N. (2000b) Finance and the sources of growth. Journal of Financial Economics, 58, 261-300.

Beck, T., Levine, R. & Loayza, N. (2000c) Financial intermediation and growth: causality and causes. Journal of Monetary Economics, 46, 31-77.

Berthelemy, J., Varoudakis, A., 1996. Economic growth, convergence clubs, and the role of financial develop-ment. Oxford Economic Papers 48, 300–328.

Berthelemy, J., Varoudakis, A., 1996. Economic growth, convergence clubs, and the role of financial develop-ment. Oxford Economic Papers 48, 300–328.

Chuah, H., & Thai, W. (2004).Financial development and economic growth: Evidence from causality tests for the GCC countries. IMF Working Paper.

Cysne, R., W.L. Maldonado, and P.K. Monteirol (2004), “Inflation and Income Inequality: A Shopping- Time Approach,” Journal of Development Economics, 78, 516-528.

D.K. Christopoulos, E.G. Tsionas / Journal of Development Economics 73 (2004) 55–74 73

Demetriades, P.O. and K.A. Hussein (1996) Does Financial Development Cause Economic Growth? Time Series Evidence from 16 Countries Journal of development Economics51, 387 - 411.

Dickey, D.A., and W.A. Fuller (1981), “Likelihood Ratio Statistics for Autoregressive Time Series with a Unit Root,” Econometrica, 49, 1057-1072.

Edison, H. J., Levine, R., Riccia, L. & Sløka, T. (2002) International financial integration and economic growth. Journal of International Money and Finance, 21, 794-776.

Favara, G. (2003) An empirical reassessment of the relationship between finance and growth. International Monetary Fund Working Paper Series, WP/03/123, 1-46.

Friedman, M., and A.J. Schwartz, 1963. A Monetary History of the United States, Princeton, N.J.: Princeton University Press.

Greenwood, J., Smith, B., 1997. Financial markets in development and the development of financial market.

Kıran, B. Yavuz, Ç., N., Güriş, B. (2009) "Financial Development and Economic Growth: A Panel Data Analysis of Emerging Countries International Research Journal of Finance and Economics." 30, 87-94 Levine, R. & Zervos, S. (1998) Stock markets, banks, and economic growth. American Economic Review,

ISSN: 2306-9007 Javed, Nawaz & Gondal (2014) 231

I

www.irmbrjournal.com March 2014I

nternationalR

eview ofM

anagement andB

usinessR

esearchV

ol. 3 Issue.1R

M

B

R

Levine, R. (2005) Finance and growth: theory and evidence. IN AGHION, P. & DURLAUF, S. (Eds.) Handbook of Economic Growth. 1 ed. Amsterdam, North-Holland Elsevier Publishers.

Loayza, N. & Rancière, R. (2006) Financial development, financial fragility, and growth. Journal of Money Credit and Banking, 38, 1051-1076.

Loayza, N., and R. Ranciere (2006), “Financial Development, Financial Fragility, and Growth,” Journal of Money, Credit and Banking, 38, 1051-1076.

Lucas, R. E. (1988). On the mechanics of economic development. Journal of Monetary Economics, 22, 3– 42.

Luintel, K.B., and M. Khan, 1999. “A Quantitative Re-Assesment of the Finance-Growth Nexus: Evidence From a Multivariate VAR” Journal of Development Economics60, pp. 381-405.

Pagano, M. (1993). Financial markets and growth: An overview.European Economic Review, 37, 613–622. Patrick, H.T., 1966. “Financial Development and Economic Growth in Underdeveloped Countries”

Economic Development and Cultural Change14, pp. 174-189.

Phillips, P.C.B and P. Perron (1988), "Testing for a Unit Root in Time Series Regression", Biometrika, 75, 335–346

Rajan, R., and L. Zingales (2003), “The Great Reversals: The Politics of Financial Development in the Twentieth Century,” Journal of Financial Economics, 69, 5-50.

Rousseau, P. L. & Wachtel, P. (2002) Inflation thresholds and the finance-growth nexus. Journal of International Money and Finance, 21, 777-793.

Saci, K., Giorgioni, G. & Holden, K. (2009) Does financial development affect growth? forthcoming Applied Economics.

Saci, K., Giorgioni, G. & Holden, K. (2009) Does financial development affect growth? forthcoming Applied Economics.

Schumpeter, J.A., 1911. The Theory of Economic Development. Cambridge, Mass: Harvard University Press.

Appendix

Dependent Variable

Economic growth Percentage change of Real GDP per capita

Independent Variables

Private sector credit(PSC) Domestic credit to private sector to GDP

Liquid liabilities(LL) Liquid Liabilities are the sum of currency and deposits in the central bank (M0),

plus transferable deposits and electronic currency (M1), plus time and savings

deposits, foreign currency transferable deposits, certificates of deposit, and securities repurchase agreements (M2), plus travelers checks, foreign currency

time deposits, commercial paper, and shares of mutual funds or market funds held by residents.

Domestic credit(DC) Domestic credit (DC) provided by the banking sector includes all credit to various sectors on a gross basis, with the exception of credit to the central government. The banking sector includes monetary authorities and deposit money banks, as well as other banking institutions.

Exports(EX) Exports of goods and services represent the value of all goods and other market services provided to the rest of the world. They include the value of merchandise, freight, insurance, transport, travel, royalties, license fees, and other services, such as communication, construction, financial, information, business, personal, and government services.

Imports(IM) Money value of all the exports

Foreign direct investment(FDI) All foreign direct investment made in the country

Government consumption(GE) General government final consumption expenditure to GDP Capital formation(CF) Gross capital formation to GDP

Trade openness (TVG) Trade value of goods is taken as a proxy for trade openness. It is the sum of exports and imports to GDP.