Munich Personal RePEc Archive

On Privatisation and Restructuring

Schröder, Philipp J.H.

2000

On Privatisation and Restructuring

Philipp J.H. Schröder1

Department of Economics

University of Southern Denmark - Odense University DK-5230 Odense M

E.mail: [email protected]

Abstract: This essay deals with the issues of privatisation and restructuring in transition economies. The topics are addressed in both a descriptive and empirical manner, but omitting a formal treatment. The centre of the analysis is the interrelation of privatisation, the resulting ownership form and the expected and actual effect on restructuring behaviour of firms. The essay identifies a slow progress in privatisation, paired with an overweight of insider owners. Furthermore substantial evidence on slow restructuring is collected. Overmanning and excessive social assets prevail in the privatised firms - in part regardless of the new ownership structure. Finally, the link to the government’s fiscal situation is drawn, the costs of restructuring to the government budget are identified. In presenting such account of the privatisation and restructuring situation, the essay provides a basis for formal explanations of slow privatisation and sluggish restructuring.

Key words: Privatisation, Restructuring, Transition

JEL classification: L33, P20, O00

1. Introduction

Transition is the move from a centrally-planned system with nationalised enterprises, collectivised farms and housing, price controls and trade restrictions, towards a market economic system. Parallel to this economic transformation, transition countries typically have to re-installed or re-invent their entire political structure. In the initial situation of central planning both prices and quantities are controlled by the state. Accordingly, the flows of goods and supplies are planned as well and scarcity cannot be signalled by prices - this results in the characteristic queuing. Since the theory of central planning relies heavily on economies of scale, we find enormous state owned enterprises (SOEs) that in many cases assume monopolistic positions. At the outset of transition the private sector is rudimentary or non existent. Such centrally-planned system features tremendous inefficiencies: waste of resources and labour, excess demand and supply, soft budgets and economic dissatisfaction.

On the other hand, socialist economies displayed a considerable degree of social security. Education and training were free and are usually assumed to be of good quality. Firms are supposed to feature a great deal of worker involvement and there was little or no open unemployment. In principle there was wide reaching economic equality among people; further there was a large share of female workforce participation. Social institutions, like healthcare or child care have traditionally been free of charge. However, many of these social services were provided through the SOEs.

Government revenue was largely financed out of the revenues of SOEs, on top of the fact that many traditional state functions (like certain social services) were also provided via the firms. During the early years of transition tax revenue fell and demands on the state rose. This poses a common problem to all governments in transition economies. An additional disadvantage for the republics of the former Soviet Union was that no administrative or legislative body was in place, hence a tax system, monetary policy tools, government ministries, bankruptcy laws and legal enforcement all have to be created, mostly from scratch.

will install owners that face the right incentives to optimise (hence restructure) their firms. Thus, in theory privatisation promotes restructuring.

This latter point, however, depends on a fairly complex reasoning of economic theory.2

Within the envisaged mechanics there may be failures and pitfalls, a number of which are addressed in Schröder (1997, 1998a, 1998b). In fact the present essay finds that both the progress of privatisation and the actual restructuring rate falls short of expected levels. Further, it appears that the problem is in part independent of the new ownership form of a firm after privatisation. Such lack of restructuring (and the sluggish privatisation record) is a puzzle, and it is at the foundation of the continuing economic difficulties in transition economies. By focussing the present paper on the actual experience and problems of transition economies, in respect to privatisation and restructuring, we can motivate and underpin the theoretical models mentioned above. The descriptive aim - in particular on the problems associated with the lack of restructuring - matches exactly the focus of these theoretical papers.

The contents of these papers can be summarised: Schröder (1997) considers manager’s incentives to restructure in a setup of insider privatisation. The paper challenges the common claim that manager owners are eager to prove their restructuring ability. The argument is based on the fact that managers’ motivation - namely career concerns - does in fact depend on the structure of the entire economy. Hence, the restructuring effort depends on the overall outcome of the privatisation program. If it is the case that the majority of firms - after privatisation - is owned by workers and that workers dislike tough (restructuring) managers, then a manager owner of a firm might choose not to restructure in order to improve his future career opportunities. Schröder (1998a) generalises on this type of effect by formalising the shareholder/stakeholder conflict. That is, those that receive the shares in the privatised enterprises are also stakeholders in those enterprises. They may be workers, managers, suppliers, creditors, etc (i.e. hold a stake in the firm). How and when the shareholder/stakeholder conflict results in low or no restructuring is identified in the paper. Additionally a government is introduced into that framework, and the choice of a privatisation program (i.e. the mix of new owners chosen by the government) examined, given some political objective function. Finally, Schröder (1998b) identifies and formalises a

fiscal constraint to restructuring. Namely, at the governmental level full restructuring of the privatised firms strains the budget: unemployment rises, so does benefit expenditure. On the revenue side the tax base shrinks. Accordingly, governments find them selves in a squeeze of conflicting demands - promoting structural adjustment and stabilising the economy (keeping a low budget deficit). Hence, the government may opt for slow privatisation and/or install owners that only restructure moderately.

The present essay identifies three interrelated elements as crucial. The privatisation method paired with the ‘available’ new owners. The resulting ownership form, and the progress of privatisation as a whole. The new owners’ theoretical and actual preferences for restructuring.

The macroeconomic setting of transition

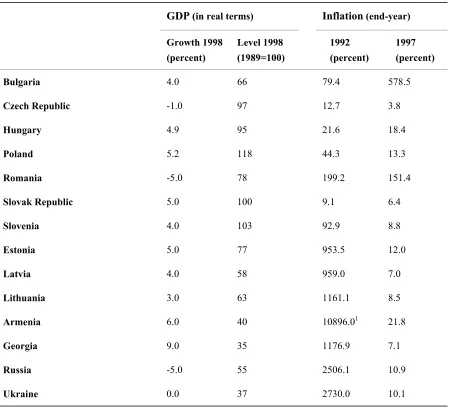

To put our examination of privatisation and restructuring into a broader economic perspective, table 1.1 presents data on GDP and inflation for a selection of transition

countries.3 Both the transitional recession and the high inflation experience can be identified.

This is the setting in which both the privatisation of SOEs and enterprise reform have to take place.

Table 1.1 (column 2) shows clearly a major economic down turn for all transition economies, in fact only 3 of the 14 shown countries are estimated to have reached above their 1989 GDP levels by 1998. Generally the collapse of GDP appears to be more severe for the former Soviet Republics, than for the Central European countries. However, we have to bear in mind that there are considerable problems in calculating GDP levels. Firstly, quality improvements are not entirely accounted for. Secondly, the high inflation of the period distorts the data. Nevertheless, as an illustration of a common feature for transition economies it is striking. More trustworthy are the estimations on GDP growth for 1998. Even though we find impressive growth levels for some countries, the weighted average for Central and Eastern Europe including the Baltic states is at only 3% in 1998, while the Commonwealth of Independent States experiences a decrease of -3.6% (mainly due to the Russian fall in GDP). In any case, talk of ‘booming’ or ‘tiger’ economies would be inappropriate. Of course, the underlying problem must be the performance of enterprises. This in turn depends on

privatisation and ultimately restructuring.

Table 1.1 GDP and Inflation in Transition Countries

GDP (in real terms) Inflation (end-year)

Growth 1998 (percent)

Level 1998 (1989=100)

1992 (percent)

1997 (percent)

Bulgaria 4.0 66 79.4 578.5

Czech Republic -1.0 97 12.7 3.8

Hungary 4.9 95 21.6 18.4

Poland 5.2 118 44.3 13.3

Romania -5.0 78 199.2 151.4

Slovak Republic 5.0 100 9.1 6.4

Slovenia 4.0 103 92.9 8.8

Estonia 5.0 77 953.5 12.0

Latvia 4.0 58 959.0 7.0

Lithuania 3.0 63 1161.1 8.5

Armenia 6.0 40 10896.01 21.8

Georgia 9.0 35 1176.9 7.1

Russia -5.0 55 2506.1 10.9

Ukraine 0.0 37 2730.0 10.1

Source: EBRD (1998), table 3.1 , table 3.3.

Note: GDP growth and level data for 1998 are EBRD projections. The inflation data is the percentage change in the year-end retail/consumer price level. Inflation data for 1992 comes from national authorities, IMF, World Bank, OECD and PlanEcon. Data for 1997 are preliminary actuals, mostly from official government sources.

1. Data for 1992 is not available the figure shows 1993 instead.

stage for structural reform: privatisation and restructuring.

Structure of the paper

The paper proceeds as follows: Section 2 deals with the topic of privatisation. We discuss theoretical methods of privatisation and the actual choices made by different transition countries. In section 3 the issue of restructuring is reviewed. Evidence of low restructuring levels and prevailing inefficiencies (including overmanning and excessive social assets) is presented. The possibility of a fiscal constraint to restructuring is discussed in section 4. The mechanics of the fiscal constraint are outlined and some evidence is provided. Section 5 concludes the paper by placing the debate on privatisation and restructuring in a broader context. In particular the link to the requirements of EU-enlargement is drawn.

2. Privatisation

The initial focus of the transition literature on the question of SOEs was on privatisation. This is the starting point of section 2. Privatisation reallocates the ownership rights - i.e. the rights to the revenue of a company - from the public domain into the private domain. An early overview on privatisation can be found in Bolton and Roland (1992) who compare strategies in Poland, Hungary, Czechoslovakia and East Germany. Hare (1994) identifies the core methods, constraints and costs of privatisation. More recent assessments can be found in the EBRD Transition Reports (1997 and 1998). Section 2.1. below starts out by Hare’s

segregation of modes of privatisation, the a priori advantages and problems associated with

each mode are discussed.

To get an overview on the actual privatisation programs chosen by transition countries we present EBRD (1997) data in section 2.2. Other such surveys can be found in the World Development Report 1996 (World Bank, 1996). The results and progress of privatisation, for example the degree to which GDP is produced in the private sector, are summarised and presented in section 2.3.

2.1. The theoretical modes of privatisation

In principle, as a phase zero of any privatisation program, socialist enterprises have to be modified into legal entities at first. Typically this will take the form of a joint-stock company, where all shares are held by the state or local municipality. Only now can the enterprise be sold (or given away). In theory there are a host of modes or methods of privatisation. However, only a few are of empirical relevance, this will become clear in section 2.2. below. What may be the cause of this will be discussed in turn for each of the methods. We will focus on their theoretical advantages and problems, their associated costs, and their necessary pre-conditions. The methods of privatisation can be grouped as shown in table 2.1.

Tabel: 2.1 Methods of Privatisation

Description of method Alternative term

a) Sale by public offering of shares Sale of shares

b) Closed or limited tender (sale by private treaty) Tender

c) Sale by public auction Auction

d) Leasing of firm assets Lease

e) Management and/or worker buyout Insider privatisation

f) Free (or token) distribution of shares/vouchers to population Voucher privatisation1

g) Free (or token) distribution of shares to wokers/managers Insider privatisation

h) Free distribution of shares to social institutions -

i) Restitution of property to former owners Restitution

Source: Hare (1994), p.194.

Note:

1. Often the term equal access voucher privatisation is used, indicating that no concession to insiders is given.

The potential ‘buyers’ of SOEs

Before we proceed to discuss some of the central methods in depth it is important to state explicitly the pallet of potential ‘buyers’ of SOEs (table 2.2). The combination of method and buyer then creates the new ownership structure - hence, is relevant for corporate governance. As was mentioned in the introduction, dependent on ownership, we expect different restructuring performance. One central theme of ownership discussed in the next paragraphs

is concentrated versus disperse ownership. The typical a priori restructuring decision per

[image:12.595.79.497.274.494.2]ownership/privatisation form is discussed in the reminder of section 2.1.

Table 2.2 Possible buyers/new owners of SOEs

Description of group Alternative term

a) Incumbent management Insider privatisation

b) Workforce Insider privatisation

c) Insiders (mix of managers and workers) Insider privatisation

d) Existing domestic firms Takeover

e) Domestic investment funds / banks Institutional

f) General population Disperse ownership

g) Foreigners (Firms, banks, private) Foreign / FDI

h) State / municipal Non-privatised

The first three owner groups/forms in table 2.2 are all cases of insider privatisation. Insiders may have a knowledge advantage when engaging in privatisation; however, they are linked to the enterprise in several ways - in particular they are also stakeholders. A manager owner can be considered a concentrated ownership form, while worker owners are more disperse. In theory a concentrated ownership form where one individual (or small group) holds all the shares should result in optimising the profits of the firm. In disperse ownership forms coordination difficulties and free riding can be expected to emerge. An extreme scenario in terms of disperse owner ship is clearly the allocation of SOEs to the general public. Each agent is endowed with a share in a certain enterprise too small to make his effort in engaging in the destiny of the firm worthwhile.

as buyers. In terms of governance, corporate owners of enterprises are expected to monitor subsidiaries effectively. However, a principal problem in transition economies is industry concentration. Given the typically few competitors a ‘German-style’ cross ownership has substantial hazards. The relevance of domestic banks and more importantly investment funds emerges in a situation of voucher privatisation. The general public posts its vouchers/shares in a fund. The fund may now have ‘critical’ mass in terms of corporate governance, i.e. problems of disperse ownership are overcome. However, banks and/or investment funds as in the Czech experience might still be short of know-how on certain industries. More critically, they are also potential stakeholders in the firms they own/monitor. For example a bank that is both the creditor and the ‘indirect’ owner of an enterprise can end up in a conflict. As a shareholder the bank might want to seek extended credit for a troubled enterprise it owns - however, as a bank, it ought not to extend such credit.

Foreign owners have advantages in terms of available wealth and expertise (ergo the possibility of concentration in ownership), yet, their practical relevance in the privatisation programs of transition economies has been minor. Sinn and Weichenrieder (1997) discuss this problem and possible remedies in depth. The general theme is that there is more or less latent resentment to foreign owners - a problem christened the ‘family silver problem’. Transition governments find it politically impossible to sell SOEs at the current ‘fire sale’

prices to foreigners. However, in terms of restructuring, foreign owners are a priori the most

rigorous. Thus, the lack of their involvement in the privatisation programs of most CEEC countries poses a grave deficit.

that in the absence of control (i.e. the planning authority is non-existent) the insiders fill the power vacuum. Such firms can be expected to behave similar to insider owned firms.

We can now turn to a discussion of the central privatisation methods introduced in table 2.1.

Sale of shares and auctions

Sale of shares and/or auctions are the traditional means of privatisation in Western Economies. In particular the British privatisations of the 1980s used these methods. The auction has the advantage that it determines the ‘right’ price of the asset to be privatised, contrary to the ‘sale of shares’ method which can undervalue the asset and give windfall gains (or loss) to the first generation of owners. On the other hand the ‘sale of shares’ method will result in widespread ownership while an auction results in owner concentration. Disperse ownership - despite the corporate governance problems introduced above - might be

considered politically desirable.4 Common to both methods is that they require a substantial

amount of wealth on behalf of the new owner. This is what makes them less-suitable for transition economies - unless, of course, foreign ownership is not met by political resentment. The problem is that in socialist economies the accumulation of private wealth has been quite difficult. What ever savings people may have had, have been eroded by the high inflation of the early transition years (see table 1.1). Ownership of land and property was forbidden or tightly regulated. Hence, assuming that only domestic ownership is aimed at, then auctions and/or ‘sale of shares’ will not yield particularly high revenue for the state. Additionally, the individuals that managed to accumulate some wealth are typically associated with the nomenclatura - awarding them with a good starting position by sale privatisation has been politically unpopular.

Despite these problems, auctions and the ‘sale of shares’ method did play some role in the mass privatisation programs of CEE countries. In particular the management and /or worker buyout of small business. Small service firms or retail outlets with only a couple of employees like restaurants, hostels, kiosks were mostly privatised in this manner. Also - if possible - households purchased the flats or houses they were living in. Yet, in particular the latter purchase - even though state owned at the outset - is not the type of asset we usually have in mind when discussing issues of privatisation and restructuring.

Lease and spontaneous privatisation

The method of leasing firm assets has been little used. The main reason for this are the immense administrative costs involved. However, in practice the sale of firms for a token value can be interpreted as an indirect lease, where the actual fee is paid continuously via the tax system.

In technical terms related to official/legal leasing is ‘unofficial’ leasing, namely asset stripping or spontaneous privatisation. These phenomena - even though not part of official privatisation programs - hence, not introduced in table 2.1, do feature in transition economies and need to be addressed. By an asset stripping arrangement we usually mean a situation, where the incumbent manager of a SOE establishes (or let’s some associate establish) some new private company. He then hires (or leases) the SOE’s productive facilities at a token price to that new company. Like this he can extract the possible surplus of the SOE, whereby the SOE is turned into an even bigger loss maker. This in turn makes the privatisation of the SOE more difficult, i.e. it is harder to find a buyer. I would describe spontaneous privatisation in fact as a similar arrangement.However, here the SOE’s assets are transferred permanently via sale or outright stealing. Naturally it is hard to measure the extent of those practices - despite for the anecdotal evidence available. It is my impression that the evidence points to an increasing frequency of asset stripping and spontaneous privatisation the further east we get.

Voucher privatisation

Voucher privatisation overcomes the main problem of the auction and ‘sale of shares’ method. For a voucher privatisation program there need not be wealth accumulated in the population. Each household or individual is endowed with a voucher, entitling it, him or her to a certain share value. Vouchers can now be used like money in the purchase of shares or an auction. The amount of vouchers, allocated to each person and/or household, may depend

on age, years of employment, previous income, etc. or simply be a flat rate.5 Further, we can

distinguish between equal access voucher privatisation, where the general population receives vouchers usable on all assets, and voucher terms with considerable concessions to insiders (e.g. the Lithuanian case introduced below).

The best known case of voucher privatisation is the Czech program. Here the emergence of investment funds made it possible for the individual voucher owners to place their portion in

a fund which then managed the deposited vouchers in a portfolio of firms. In several other cases, best known are Russian examples, the workers and management of a SOE pulled their vouchers to purchase the firm they work at (resulting in insider privatisation). In the reality of many other voucher programs, vouchers have often been used to purchase the flat a household lives in.

Insider privatisation6

Of particular importance is the case of insider privatisation, no matter if the transfer of ownership rights was compensated with money, lease fees or vouchers. Insider control of firms occurs once a decisive portion of shares is hold either, by the management, the workers

or a mix of the two groups.7 Insider privatisation is commonly held to be the fastest road to

property rights redistribution. Because of the easy administration and maybe because it was typically politically popular, this type of privatisation features extensively in many CEE countries.8

The usual claim for insider ownership is that the allocation of control rights to the management will ensure fast and complete restructuring, as opposed to worker controlled companies. The reasoning behind this argument is in fact based on a classic shareholder/stakeholder conflict. The reasoning goes as follows: The inefficiencies in SOEs are not only in the form of wasteful production methods and inferior quality products but also in the form of excess and idle labour (McMillan, 1995). Additionally, SOEs provide a wide range of social services from food subsidies to housing to their workers (Freinkman and

Starodubrovskaya, 1996).9 The extension of the firm’s activity into the sphere of municipal

duties (namely social services) parallels the excessive production depth we find in centrally planned economies (Mayhew and Seabright, 1992, p.107). Having privatised firms, it should be part of restructuring to bring down overmanning and excessive provision of firm social services. Here the problem emerges: these particular inefficiencies are in part in the workers interest, especially since overall unemployment is on the rise and state social provisions are shed in the transitional recession. Accordingly, workers' incentives to restructure are low.

6. Part of the discussion in the next paragraphs is also found in Schröder (1997).

7. Of course, in the absence of any dominant shareholder, insiders may be able to control a firm without having any property rights at all.

8. Privatisation programs where insider privatisation was a main element (at least as an outcome, even though not always intended) took place in Romania, Slovenia, Croatia, Poland, Lithuania, Mongolia, Georgia and Russia (World Bank, 1996, ch.3). The report forwards also rationales for this development. In section 2.2 the extent of insider privatisation will be shown.

The issue of insider owners that benefit from firm inefficiencies is well known in the literature. By now it should be clear that this type of conflict in general arises once shareholders are also stakeholders - i.e. supply labour to (receive social provisions from) the enterprise. Nuti (1996a+b) points out that as soon as an individual holds a smaller share in equity than in the total input supplied (benefits received) their stakeholder interests override their shareholder interests. This point is extended and formalised in Schröder (1998a). Contrary to worker owners managers are assumed - given that they are not stakeholders and that there is the right compensation scheme - to be tough in fighting inefficiencies. The motivating compensation scheme will be some share of the property rights in the firm - which

is the whole point of insider privatisation.10 Of course the managers in transition economies

might be in quite a different setting. This is the subject of Schröder (1997) where managers’ career concerns can result in a non-restructuring outcome. Additional disadvantages of manger ownership - specific to transition economies - stem from their alleged lack of know-how. The incumbent managers might be ill-suited to turn around the old ways of their enterprise. However, in practice new expertise can only be imported and is typically associated with foreign owners or foreign participation (FDI).

Finally, - and in part because of the corporate governance problems associated with insider ownership - insider owners may find it hard to raise capital on the financial markets. The reason is, that their stakeholding in the firm gives them the opportunity to defer funds away from the repayment of debt . Paired with the generally weak and short-term oriented financial sector of transition economies, this puts insider-owned firms at a particularly bad starting position.

Issues of worker ownership

In relation to insider privatisation it is important to discuss the issue of workers’ coalitions and worker ownership of firms. One of the core problems of insider owners - that we identified above - was that firms, managed or owned by workers are run inefficiently, because the employees try to maximize total wages instead of profit. In particular, via their

stakeholdings (as wage earners) the workers can defer profits to them selves. However, this argument need not hold. If the firm is really completely owned by the workers, then they must be indifferent to receiving the surplus through wages or dividends. Additionally, such firm ought also to engage in restructuring. Namely, a majority coalition of non-shirking workers would find it beneficial to dispose of their idle colleagues. Even if workers are identical, the gain can in principle be large enough to compensate the workers for the risk of being one of those that gets fired.

It can be argued that the Yugoslavian experience of worker cooperatives is exactly supporting the case for efficiently run insider-owned firms. However, some of the more recent evidence on transition economies, part of it presented in section 3.3 below, indicates that insider privatised firms underperform. Still, the reasons for this could be the lack of know-how and the lack of financial resources. Thus, it is not fully evident that worker-owned firms will and do display inefficiency, because of their stakeholdings.

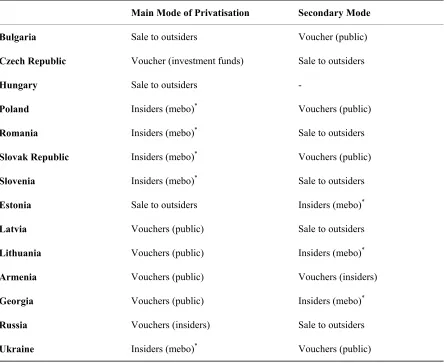

2.2. Actual choices: routes chosen by transition countries

In general all forms and mixes of privatisation methods were and are applied in transition countries. Hereby it is important to note that privatisation is far from concluded for most transition countries. The constraints of public wealth and expertise make some modes more applicable than others. In particular, as an outcome, elements of insider privatisation feature in many programs.

Nevertheless, contrary to common opinion, privatisation is far from concluded and continues

[image:19.595.79.526.167.530.2]to be a topic of paramount importance to transition countries.11

Table 2.3 Main Privatisation Methods per Country (Status 1997)

Main Mode of Privatisation Secondary Mode

Bulgaria Sale to outsiders Voucher (public)

Czech Republic Voucher (investment funds) Sale to outsiders

Hungary Sale to outsiders -

Poland Insiders (mebo)* Vouchers (public)

Romania Insiders (mebo)* Sale to outsiders

Slovak Republic Insiders (mebo)* Vouchers (public)

Slovenia Insiders (mebo)* Sale to outsiders

Estonia Sale to outsiders Insiders (mebo)*

Latvia Vouchers (public) Sale to outsiders

Lithuania Vouchers (public) Insiders (mebo)*

Armenia Vouchers (public) Vouchers (insiders)

Georgia Vouchers (public) Insiders (mebo)*

Russia Vouchers (insiders) Sale to outsiders

Ukraine Insiders (mebo)* Vouchers (public)

Source: EBRD (1997), p.90.

Note: Voucher (public) indicates that the general public had access to the vouchers, i.e. equal access voucher privatisation. Vouchers (insiders) indicates that significant concessions to insiders were made. All other terminology is used as defined in section 2.1.

*: management employee buy out.

Table 2.3 indicates clearly the important role of insider privatisation. In fact those countries that I have omitted in the table (Albania, Croatia, Macedonia, Azerbaijan, Kazakhstan, Kyrgyzstan, Moldova, Tajikistan, Turkmenistan, Uzbekistan) follow either in that pattern or

are at a very early stage in privatisation.12 In section 3 we consider whether or not this

ownership pattern has led to the a priori expected delays in restructuring.

The second most relevant method of privatisation - as shown in table 2.3 - is voucher privatisation. As discussed in section 2.1. the chief reason for this is the lack of wealth in the population. Also, on pure ideological grounds is the transfer of collectively owned assets of production most ‘fair’ via vouchers - hence, generates political support. Sale of shares (or auction) to outsiders appears to be the third most relevant means of privatisation. In the discussion of theoretical advantages this method ought to give the best results in terms of restructuring, hence, in terms of efficiency it should have featured the most.

I shall now sketch some components of privatisation and the current state of the programs for three countries. This overview aims more at variety than completeness. Comprehensive accounts of individual countries privatisation policies are found in EBRD (1995, 1997, 1998b). The three country accounts presented below build on this reports.

Czech Republic

The success and effectiveness of the Czech voucher privatisation (the first wave of privatisation) was largely determined by the emergence of investment funds. Such funds made it possible for the individual voucher owners to place their personal vouchers in a fund which then managed the deposited vouchers in a portfolio of firms. In hindsight the construction of investment funds appears to be a mixed blessing. This will be discussed in section 3.2 below. An important feature in the Czech republic is that the state held on to minority shareholdings via the National Property Fund (NPF), the privatising agency. Such minority holdings are ignored when computing the private sector share in GDP, as calculated in table 2.4. Hence, considerable privatisations remain to be completed, state holdings in strategic enterprises and banks are substantial. Currently the state continues to sale off its minority holdings (in those enterprises not designated ‘strategic’) by direct sale, auction and public tender. Despite the major first wave of privatisation by voucher, the government still holds on to a considerable amount of shares. The EBRD states that for 1996 the NPF is assumed to hold 40% of all shares, with another 30% held by the investment funds that emerged under the first wave of privatisation. Hence, we see that the resulting structure of ownership in the Czech case is far from the patterns of western economies.

Lithuania

Lithuanian privatisation was split into two waves, the first wave was voucher based in the period from 1991 to 1995. The second wave since mid 1995 tries to focus on sale for cash and the involvement of foreign investors. Of the more than 70% of all state assets that were

put up for privatisation in the first wave, only 30% were actually privatised by 1995.13 Hence,

the need for a second wave. The new strategy established a state privatisation agency - analogous to the German Treuhand. Again from the ambitious list of 400 enterprises to be sold in 1996, only 50 got actually privatised. Besides, the participation of foreign investors is still minimal and only picking up in 1997/98. As a particular concession, the Lithuanian program had for most enterprises reserved up to 50% of shares for the enterprise’s employees. Hence, resulting in considerable insider dominance.

The Lithuanian example emphasises the qualitative difference in the privatisation of small versus medium and large enterprises. Privatisation of small enterprises and the state housing stock proceeded rapidly. Actually this phase was completed in the early years of the first wave. This is in fact were most vouchers have been used. A starting problem in the Lithuanian privatisations has been that the government and privatisation agency had been relatively lax in awarding firms the title ‘strategic’ or ‘special purpose’. Such enterprises were excluded from privatisation - even though, they often were the most attractive objects. This exception policy has only been tightened in 1997/98. The Lithuanian case exemplifies that privatisation is an ongoing problem.

Ukraine

Ukraine has traditionally been one of the laggards in transition. The political landscape is marked by resentment, disagreeing reformers, U-turns and backlash. Privatisation started slowly in 1992, resulting mainly in insider ownership. The methods that were used are the lease of firms to insiders and management employee buyouts. In 1994 the president tried to step up privatisation by the introduction of vouchers and compensation certificates. The compensation certificates were paid out as a reparation of lost savings - more than 17% of the

population received such compensation certificates. Vouchers and certificates are used at auctions, parallel sale through cash auctions and tender continued. Overall privatisation proceeded slowly, the distribution of vouchers to citizens took three years, and the private sector’s share in GDP is at 55 % in 1998, one of the lowest rankings in Central and Eastern Europe (see table 2.4). By 1997 the sole progress areas were: 1) small enterprises mostly sold to the insiders and 2) housing, where 40% of the formerly state owned housing stock was privatised by 1997. Again these two areas prove to be the ‘easy wins’.

In response to the voucher based part of the privatisation program, investment funds - similar to the Czech construction - emerged. The investment fund collects the vouchers of the participants and bids then for a portfolio of privatisation objects. A core problem in the Ukrainian case is a strong lobby against the sale of agricultural land. This leaves farming in a close to collectivised state. Finally, it can be noted that the Ukrainian privatisation did not engage in any restitution of former owners. Overall the Ukrainian example shows two things: Firstly, insiders are frequently installed in the new owners of those firms privatised. Secondly, much is still to be privatised. Hence, policy advise or insight as to the design of privatisation programs - and their effect on restructuring - is not merely of academic interest. A new effort to speed up privatisation has been launched in 1998. Preliminary data suggests that this program is more successful than the previous attempts.

2.3. Privatisation results and outcomes

In this section the theoretical outlook of section 2.1 and the evidence presented in section 2.2. will be synthesised to generate a general picture of the privatisation results in transition economies. The three topics of interest are: how far has privatisation proceeded, what are the dominant ownership structures, what is the role of the entire private sector in the economy?

almost all transition countries. The main difference is that agents have a better chance to assess the value of what they purchase. Further, the wealth (or vouchers) of a few persons (household members) might suffice to purchase the object.

As to ownership we can summarise several facts. As one of the dominant ownership forms that resulted from privatisation, we identified insider ownership. Insiders have either obtained control over enterprises via management employee buyouts, via lease arrangements or by using their vouchers as a means of payment. Insider ownership is of a problematic nature due to the stakeholder/shareholder conflict. Voucher privatisation - or elements hereof - has featured in many countries. The reason for this was that private wealth was almost non-existent in socialist economies. So both on grounds of practicability and on grounds of fairness has the construction of voucher privatisation be used. As a result we find either relatively disperse ownership or the emergence of investment funds. Disperse ownership can give considerable problems in corporate governance. However, a dominant investor - maybe in form of an investment fund - can remedy such problems. A problematic issue of investment funds occurs, if they assume a dual role: once as the owner of firms and once as a creditor (via their involvement in banking activities). Such set-up gives again rise to a shareholder/stakeholder conflict. A clear-cut outside owner and/or foreign participation - which were on theoretical grounds advantageous ownership constructions - features relatively seldom in the privatisation programs of Central and Eastern Europe.

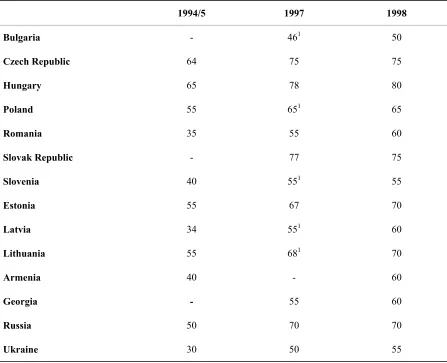

The size of the private sector

Having established the privatisation methods and resulting ownership forms, it is important to ask what role the private sector plays in the economy. In a sense this provides a measure of how far a country has moved away from central planning, i.e. an aggregate of structural reform. Estimates of the size of the private sector vary in the definitions used and in the actual numbers quoted. Typical variables used are private sector share in GDP, share in total employment, share in industrial output. Often data is distorted by including or excluding estimates for informal activity. Table 2.4 assembles an overview for three time points 1994/95, 1997 and mid-1998 using EBRD transition reports. In those cases where there is a conflict in data, the most recent report is used.14

As a means of comparison for the figures in table 2.4 note that for example the Danish private sector share in GDP is at about 80%. In table 2.4 we find that a number of countries approach levels of private sector share in GDP comparable to Western Europe. Also, a trend of increasing private sector activity across the board becomes clear. Several elements contribute to this development. Firstly, ongoing privatisation, which converts state

production into private sector production. Secondly, de novo firms are established and

[image:24.595.75.522.312.675.2]increase the private sector share even though privatisation would stand still. Finally, private or privatised firms are usually found to experience larger growth rates, hence increase their share in GDP.

Table 2.4 Share of the Private Sector in GDP (percent of GDP)

1994/5 1997 1998

Bulgaria - 461 50

Czech Republic 64 75 75

Hungary 65 78 80

Poland 55 651 65

Romania 35 55 60

Slovak Republic - 77 75

Slovenia 40 551 55

Estonia 55 67 70

Latvia 34 551 60

Lithuania 55 681 70

Armenia 40 - 60

Georgia - 55 60

Russia 50 70 70

Ukraine 30 50 55

Source: EBRD (1995, 1997, 1998b). Notes:

Overall, we have found that privatisation is not concluded. Much of the state assets remains to be privatised. In terms of the emerging ownership forms, the privatisations of transition economies have favoured constructions that install insiders as the new owners. The most effective ownership forms (foreign, and concentrated outsider) feature relatively little.

2.4 Privatisation methods and constraints - revisited

To conclude and summarize the discussion on privatisation, I return to the constraints introduced at the outset of the section. 1) Restructuring: In how far do the privatised firms

engage in restructuring (a priori). 2) Administrative demand: How easy (and swiftly) is a

certain privatisation method. 3) Need for wealth in the economy15: How much does a certain

method depend on the availability of domestic funds. 4) Political feasibility: How much public support (or rather resentment) will a certain method get.

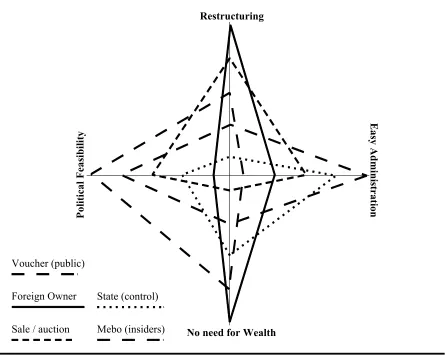

In figure 2.1 I show a ranking of five important privatisation methods (resulting ownership forms), in terms of these constraints. The inherent conflicts and tradeoffs between constraints and methods become visible. The further out on an axis a method is positioned,

the higher (positive) does the method score in this particular dimension. For example consider the ‘no need for wealth’ dimension. Privatisation to foreign owners ranks the highest (5), since no domestic funds are needed. Voucher privatisation ranks next. The worst performer in this dimension are Sale/auction methods - here the buyers (if intended to be domestic) will be severely constraint by their limited wealth. Slightly more relaxed are manager employ buyouts (mebo), reflecting the opportunity for lease arrangements Finally, continued state ownership ranks in third place. Naturally, such enforced ranking is purely subjective - and far to simplistic, however, it still captures many of the arguments forwarded in the discussions of section 2.

What becomes clear in figure 2.1 is that no single method captures the entire constraint space satisfactorily. Visual inspection shows that the ‘smallest’ area is covered by continued state control. The sale/auction method scores high in terms of expected restructuring, but loses out

Voucher (public)

Foreign Owner

Sale / auction Mebo (insiders) State (control)

Restructuring

Easy Administration

No need for Wealth

P

o

li

ti

ca

l

F

ea

si

b

il

it

[image:26.595.76.521.172.527.2]y

at the ‘no need for wealth’ constraint. Voucher privatisation scores relatively high at three

dimensions, namely political feasibility, no need for wealth and (a priori) good restructuring

results. Insider ownership (Mebo in the figure), is certainly easy in administrative terms, and will (due to lobbying) have good political support. However, in theory, their restructuring performance would be weak. Finally, foreign owners get the highest ranking on the restructuring dimension and the ‘no need for wealth’ dimension. However, they are ranked lowest on the political feasibility dimension.

The ranking within each constraint is certainly debatable. Still, the exercise can be used to interpret structural reform during transition. Policy is governed by emphasis on certain constraints. While a high degree of restructuring may be a declared objective of the government’s privatisation program, political feasibility may be the binding constraint. Alternatively, a lack of administrative capacity can be the binding constraint, and makes, the else chosen, voucher privatisation impossible. The ‘no need for wealth’ constraint certainly has played a substantial role in the reform process of many countries. In this interpretation figure 2.1 illustrates the inherent problem in designing the perfect privatisation method.

This concludes section 2 on privatisation. We will now proceed to examine the topic of restructuring closer. Hereby we will pay particular attention to evidence that can help

evaluate the a priori expected restructuring behaviour of the different ownership forms

introduced above.

3. Restructuring

The restructuring of a firm addresses the efficiency of the entity. Recall that privatisation was concerned with property rights - the rights to the revenue of a company - in particular, moving away from the nationalised construction. This chapter will examine the extent and speed of restructuring. It is found that restructuring in most transition countries has proceeded far slower than one would expect. One chief reason is the delayed advancement of privatisation identified in section 2. However there are additional delays in restructuring, we observe that employment is falling by less than output, ergo, a continued overmanning policy prevails within many firms. Also, enterprises continue to maintain a host of social assets for the benefits of their workers. Hence, inefficiency persists.

The inheritance of state owned enterprises

identify their starting position, namely the features of a socialist firm. At the outset of transition the socialist enterprises of central planning are marked by some unconventional characteristics: overly large size, excessive vertical integration, high market concentration, low quality products, excessive levels of employment, a wide range of social services to their

employees, strong employee involvement in decision making, grotesque incentive systems.16

Large size and vertical integration were a direct consequence of the mechanics of central planning. Size was opted for due to a belief in scale economics, each industry was limited to only a few or a sole producer. Also, planning was made a lot easier by dealing only with one firm. Vertical integration was a consequence of the permanent threat of (or actual) shortages in the supply chain. A highly integrated firm, could wrestle some of the planning responsibility away from the central planning authority and ensure like this a smoother flow of production. Large size and high vertical integration resulted for many SOEs in a monopolistic position. However, such high market concentration was not that easily abused - remember that prices were controlled, too. Nevertheless, large size and monopolistic position gave some power in the ‘negotiations’ with the central planning authority. The giant SOEs had, via their informational advantage, ample opportunity to influence (manipulate) their production targets (statistics). Low quality products are in fact partly based on such power. Given that no competitor can step in, and given that the price cannot be used to reap monopolistic profits, then the ‘effort’ supplied - in total the quality - can be reduced. This conclusion rests on the assumtion that effort (higher quality) is costly to the firm (and individual) supplying it. Both the supply situation and the low quality of products were easily observable to the western visitor.

Maybe less visible - but not less known - have been the other four characteristics of socialist enterprises: excessive employment levels, extensive social provisions to workers, employee involvement in decision making, distorted incentive systems. Most problematic was the extent of overmanning and idle labour. For political reasons socialist economies displayed virtually zero percent unemployment. This could only be achieved by ‘planning’ enterprises into taking on more labour than needed. The management of an SOE would not mind, as the expense of the extra wages would not affect their own salary, nor the ‘rating’ of the enterprise. To the contrary, size and the number of employees could be seen as a symbol of status and importance. Further, such system of an employment guarantee to the citizens implies that there is practically no cost of shirking. In fact there was little punishment to

shirking; most bonuses were awarded collectively, ergo, a free riding problem was pre-programmed. It is important, in this context, to understand, that even though there was an implicit or explicit right to work, there was no free choice of what job one would get. This in turn resulted often in a bad worker/job match and in low worker motivation. Parallel to their excessive production depth (vertical integration) socialist enterprises did also branch into a host of social services for their employees. For a large size SOE it was not unusual to provide housing, child-care facilities, transportation, company supermarkets (stocking goods that are else hard to get), on the job healthcare and firm run holiday resorts for free or at a token price to it’s employees. Additionally firms implicitly provided job insurance by taking on unemployable persons, and part of pensions by extended provision of housing etc. Hence, a socialist enterprise actually providesda number of services that else are provided by the state. These social services did create attachment of workers and were a rudimentary means of worker motivation. They also reflect the influence of employees in firm decision making - not so much on the bold direction, but in terms of harvesting liberties and concessions for the employees. The influence of insiders in firms increased during the last years of central planning and the early years of transition. In correspondence to the withdrawal of the state the insiders filled the power vacuum - this generated often their platform for extensive influence on the design (and exemptions) of privatisation programs. The distorted incentive system of socialist economies stemmed from an overly focus on quantity and an inability to use prices (wages) as a motivation device. There are plenty of anecdotes on incentive failures in central planning. Tales of measuring/monitoring firm output by piece or weight - and the

resulting response of the firms, are almost comical.17 The bonus system of socialist

economies invited similarly miss focus and fraud in the reporting of actual output as much as the setting of targets.

Having introduced the starting point of an SOE, which sets the agenda for initial restructuring, one more item needs to be mentioned: The quality and skill of employees. It is obvious that the qualification of a socialist manager is short of what is needed to run a firm in a market economic setting. This can only be rectified by training or import - the latter often met by the aforementioned political resentment. The general qualification and skill level of the socialist economies is usually said to be high. However, more recent views on the human capital in Central and Eastern Europe identify severe flaws. Boeri et al (1998, pp.25) present evidence of low education levels and low standards in qualifications. Møllgaard and Schröder

(1998) report, in a case study of foreign direct investment, similar problems with worker and managerial qualifications. This concludes our introduction to the type of problems inherent in socialist enterprises. A major challenge in restructuring is, of course, to tackle these obstacles.

In section 3.1 I will identify different concepts of restructuring, distinguishing reactive versus deep restructuring. Furthermore, I will introduce measures of restructuring, ranging from the more result orientated ‘business’ economics measures of profitability, to the more aggregate economics measures of employment levels and finally the provision of social services by firms. In section 3.2 I proceed to present evidence on these measures. It is found that inefficiency prevails in a number of countries and firms. Finally we will examine the relation of ownership structure to restructuring. Here we find that the ownership form (i.e. the outcome of privatisation) is not always a good predictor of firm restructuring behaviour. However, some outstanding ownership forms are identified, namely continued state ownership is related to little restructuring, and foreign participation is related to much restructuring.

3.1. Two concepts of restructuring

By now there is a consensus to distinguish restructuring into two qualities. 1) Reactive

restructuring; 2) Deep restructuring.18 By reactive restructuring we mean measures that are

executed in response to tightened outside conditions. For example the elimination of soft budgets and/or the transitional recession forces enterprises to abandon certain activities or shed part of idle labour to ensure survival. Such behaviour should in fact be independent of the ownership form of the enterprise, as long as the outside tightening is credible and enforced. Note, that in reactive restructuring inefficiency is only attacked until break-even is achieved. Deep restructuring on the other hand encompasses new investments, strategic reorganisation and an overall reorientation of the firm’s activity. By this type of restructuring the enterprise is fully trimmed and all inefficiency is eliminated. For deep restructuring we expect certain ownership forms to be more active than others.

According to this distinction we can identify different contents of the term restructuring, which in turn leads to different indicators of restructuring. Reactive restructuring - the relatively easy to do step - namely, fire idle labour and scrap social functions, does not

require know-how and/or new capital. It is important to note that reactive restructuring, even though some of the firm inefficiencies are rectified, will typically not result in complete elimination of these types of inefficiencies. However, note that firms that were striving for pure profit maximisation would go for the entire gain. Deep restructuring, on the other hand, requires capital, know-how and managerial skills. So here we can find firms that might want to engage in deep restructuring but lack one or more of the necessary inputs. Thus, in terms of expected observation, we can in fact subdivide three stages of restructuring: Reactive restructuring, complete elimination of ‘easy to rectify’ inefficiencies and deep restructuring.

In line with these distinctions we will observe different variables as indicators of progress. At one end we get measures of employment developments, and case studies of firm social assets and excess labour. At the other end we get more ‘business’ type measures like profit ratios, investment over asset ratios and surveys of the introduction of new technology as indicators of deep restructuring. All these measures are presented in section 3.2.

3.2. Measuring the restructuring performance / inefficiency

Before we proceed to a discussion on developments in excess employment and excess firm social assets, I will start by presenting some restructuring accounts reported by the EBRD

(1997, 1998b).19 In particular I examine the three countries that were presented as actual

privatisation routes cases in section 2.2. The EBRD accounts - as most business accounts - on restructuring are more focussed on profitability and growth, and not so much on the underlying mechanics of efficiency. Hence, in this ‘business’ terminology restructuring is a slightly different concept (as discussed in section 3.1.) and far more result orientated. After the restructuring cases for the Czech Republic, Lithuania and Ukraine, table 3.1 creates an overview of ‘business’ type restructuring measures for several countries.

Czech Republic

Via the NPF the Czech state continues to sell off its minority holdings in privatised enterprises. The EBRD states that for 1996 the NPF is assumed to hold 40% of all shares, with another 30% held by the investment funds that emerged under the first wave of privatisation. This constellation has a negative impact on restructuring. Even though the large block shareholdings of investment funds should smoothen corporate governance, their entanglement with banks has weakened their actual effectiveness. Furthermore, investment

funds are not allowed to hold more than 20% of the shares in any one company - thus excluding them from a decisive majority share. Some investment funds reacted to this by transforming into holding companies - which are not subject to the 20% rule.

In any case, by 1996 it is estimated that the majority of firms of the first privatisation wave has now a dominant or outright majority owner. Nevertheless, the EBRD (1997, p.164) assess that restructuring is not proceeding satisfactorily. In particular have pre-tax profits fallen by 40% in medium and large companies (more than 100 employees). Further, an increase in inter-enterprise arrears is observed. As an underlying problem the entanglement of investment funds with banks is identified. Again the effect on restructuring stems from the stakeholdings that such agents have in the firms they own - i.e. being the creditor to the firm they own/control. In recent policy packages the Czech government has attempted to regulate banks/investment funds control over firms.

Lithuania

The voucher method of the first wave of privatisation in Lithuania resulted in insider domination for many of the privatised firms. Still, restructuring, as measured by profitability, in the privatised sector by far exceeded the performance of the firms that remained in state ownership. The profit over assets ratio in 1995 is 5.8% for private enterprises and only 1.8% for state enterprises. Part of this difference can be explained by selection bias. For example, the firms that remain in state hands by 1996 are generally much larger than those that got sold off. It is argued that the problems of inefficiency are disproportionally larger as well. Nevertheless, the relative good performance of firms under extensive ‘insider’ influence has

to be reconciled with our a priori view on insider incentives. The EBRD (1997, p.184)

assesses that further increases in profitability in the privatised sector stems primarily from labour shedding and reduced capital utilisation. Redundancies have resulted in an 20% increase in labour productivity from 1995 to 1997. This tells us three things: Firstly, deep restructuring (new investment, etc) is still not found in Lithuanian enterprises. Secondly, firms in 1995 - that is after the first privatisation wave was concluded - had still considerable excess employment. Thirdly, insider dominated firms can be seen to engage in the shedding of excess labour.

Ukraine

arrears to power utilities (US$ 1.9 billion), and growing wage (US$ 2.5 billion) and tax arrears. Such defaults on payment should be interpreted as inefficiencies - and in fact the persistence of soft budgets. The low degree of restructuring, found in the Ukrainian case, mirrors both the slow pace of privatisation and the type of owners that are installed. This is

fully in line with our theoretical discussion of ownership and restructuring.20

Restructuring indicators

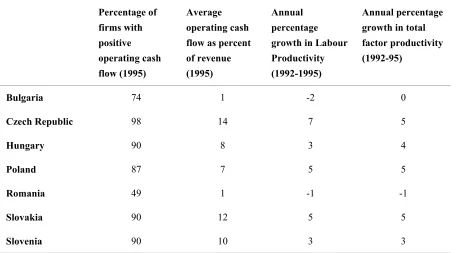

[image:33.595.72.528.349.602.2]Now, in order to create an overview on restructuring performance as measured by result, i.e. in the more ‘business’ type perception introduced above, I present a number of restructuring indicators based on Djankov and Pohl (1998). They also do present measures on productivity, which directly translate into our interests in overmanning. Table 3.1 reproduces their data which is based on survey results.

Table 3.1 Various Restructuring Measures

Percentage of firms with positive operating cash flow (1995) Average operating cash flow as percent of revenue (1995)

Annual percentage growth in Labour Productivity (1992-1995)

Annual percentage growth in total factor productivity (1992-95)

Bulgaria 74 1 -2 0

Czech Republic 98 14 7 5

Hungary 90 8 3 4

Poland 87 7 5 5

Romania 49 1 -1 -1

Slovakia 90 12 5 5

Slovenia 90 10 3 3

Source: Djankov and Pohl (1998).

Table 3.1 shows that the speed of restructuring varies across countries. We find five countries

with impressive adjustment and positive factor productivity growth rates (Czech Republic, Hungary, Poland, Slovakia, Slovenia). The other two countries - Bulgaria and Romania - experience a standstill and decline in productivity respectively. Most notable does a decline in labour productivity indicate persistent excess employment, while a rise in labour productivity will primarily stem from the shedding of idle labour. The most striking result of table 3.1 is the relatively large number of firms with negative or zero profits that remain in

some of the countries.21 While their support through direct subsidies is substantially reduced,

soft budgets (indirectly through tax arrears) might be the explanation of the observed. In any case, the evidence shows that inefficiencies prevail.

3.2.1. Persistent overmanning

In this section I will show that part of the remaining inefficiencies stems from excess labour. That is that reactive restructuring measures - firing of idle labour - are far from concluded, even though reform and privatisation have been progressing for years.

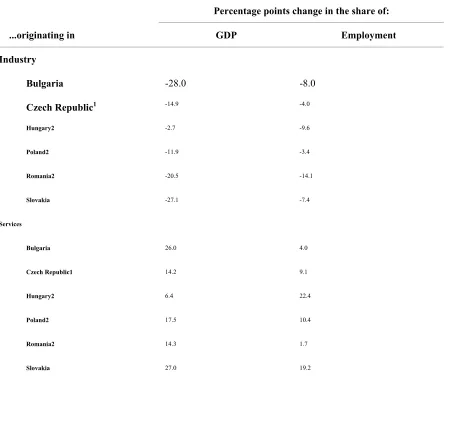

As a first indicator of overmanning one can consider the economy at a fairly aggregated level. Table 3.2 provides the development in output and employment for a number of countries. Ignoring the developments in absolute levels, table 3.2 shows the percentage point

change in the share of GDP (employment) for two sectors - industry and services.22

In terms of the composition of GDP table 3.2 shows a clear contraction of the industry sector and a matching increase in the service sector across all countries. This fits to a switch away from the industry focus of central planning times. However, the corresponding effect on employment is - with the exception of Hungary - weaker. In fact the (unweighted - across countries) average increase in the service sectors share in GDP of 17.6 percentage points is generated by only 11.1 points increase in the employment share. Accordingly the average decrease of the industry share in GDP of 17.5 percentage points in associated with a 7.8 percentage point decrease in the share of employment. There are several interpretations. Firstly the developments in the service sector could be associated with a parallel surge in labour productivity for that sector. Accordingly the labour productivity in industry must have

21. See also Blanchard (1998, p.65) who interprets on a different data set that the bunching of profits at zero indicates the appropriation of profits by insiders. An alternative deduction could be that firms hide profits from the tax authority.

been falling. This would indicate increasing overmanning in the industry sector - typically the sector where we find the privatised SOEs, and full efficiency in the service sector -

typically the sector with the most de novo firms. Secondly, the observed could simply stem

[image:35.595.79.532.296.720.2]form the absolute movements in GDP and employment. Nevertheless, I take table 3.2 to establish one thing. In relative terms the industry sector is lagging behind in productivity improvements. Also realise that this sector started out with considerable inefficiencies, including excess employment. I conclude from this evidence that by 1994/95 (some years into privatisation) reactive restructuring measures, namely labour shedding, have not been exhaustive.

Table 3.2 Output and Employment, 1989-95

Percentage points change in the share of:

...originating in GDP Employment

Industry

Bulgaria -28.0 -8.0

Czech Republic1 -14.9 -4.0

Hungary2 -2.7 -9.6

Poland2 -11.9 -3.4

Romania2 -20.5 -14.1

Slovakia -27.1 -7.4

Services

Bulgaria 26.0 4.0

Czech Republic1 14.2 9.1

Hungary2 6.4 22.4

Poland2 17.5 10.4

Romania2 14.3 1.7

Table 3.2 Output and Employment, 1989-95

Source: Boeri et al. (1998), table 4.1. They have assembled the data from various sources: EBRD Transition Reports, OECD CEET database, European Commission employment and service sector surveys.

Note: The values of the third sector (agriculture) are residual to the presented values. 1. 1991-95

2. 1990-94

Blanchard (1998) builds several arguments that are based on an assumption of persistent labour hoarding. Namely, considerable

overmanning remains, even though labour productivity has been rising for some years. Out of the evidence he provides I reproduce here one

table originally from a survey based analysis by J. Köllô (1996).23 Table 3.3 shows the elasticity of employment with respect to sales

[image:36.595.75.523.307.454.2](output) for a sample of Hungarian firms. Hungary started already in the mid 80's to introduce more autonomy of firms.

Table 3.3 Hungary: estimated elasticity of employment with respect to sales

1986-89 1989-92 1992-93

All firms 0.13 0.33 0.22

Firms with decreasing output 0.21 0.34 0.33

(Proportion of firms) (50%) (91%) (66%)

Firms with increasing output 0.01 0.04 0.04

(Proportion of firms) (50%) (9%) (34%)

Source: Köllô (1996), here quoted from Blanchard (1998) table 3.3.

Note: In the original regression by Köllô a constant term is included in the regression which is not reported in Blanchard (1998, p.72).

The table shows a stark asymmetry in the employment response to a change in output, depending on a decrease or an increase in sales (row

two and four respectively). In particular those firms suffering a decrease in output do cut employment, while those firms experiencing an

increase in output do not hire new workers in response. This implies that firms still had excess labour even in 1992-93, several years after

the start of reform. Via this excess labour, firms manage to increase production without increasing the number of workers. Further,

Blanchard (1998, p.72) concludes that given this type of evidence we can assume that the increases in labour productivity, we observe in

subsequent years, will most likely stem from labour shedding (reactive type of) restructuring measures, and not from deep restructuring. In

fact Blanchard (1998, chapter 4) stylizes the unemployment path in transition into two steps. A ‘first’ unemployment surge - purely reactive

to the tightening of the budget constraint, than a ‘second’ stage of a continuing stream of unemployment, caused by subsequent reductions in

overmanning. Whereby the later reductions depend on the firms restructuring decisions - i.e. are influenced by corporate governance and the

outside conditions.

Further evidence of two waves of labour shedding and the relation to efforts of reducing overstaffing is collected in Boeri et al (1998,

pp.32). They do also examine job creation, and find that job growth is almost exclusively obtained in the private sector. Evidence on

persistent overmanning (Boeri et al, 1998, pp.42) is introduced in order to explain the ‘jobless’ recovery of transition economies.

Related to this arguments let’s return to table 3.1. The growth in labour productivity presented in the table can be interpreted as evidence on

overmanning in Bulgaria and Romania. If one agrees that in 1992 all transition countries did suffer from excessive employment levels, then

the countries that experienced negative growth rates in labour productivity (since 1992) must continue to have excessive levels in 1995. The

simple elimination of idle labour would bring about a steady rise in labour productivity - as observed in the other countries.

Evidence for another transition country can be found in a survey of 439 Russian firms in 1994. Commander, Dhar and Yemtsov (1996, p.25)

find that 25% of firms admit to at least 10% of their employees being redundant. Another 20% of the surveyed firms believe that between

5%-10% of their workforce is not needed. Hence, we get a total of 45% of firms that admit to excess labour of at least 5% of their present

workforce. This result is from a period where the first major wave of privatisation had been concluded in Russia.

I will now briefly present a specific case, a classic example of a privatised SOE:

The case of VSZ24

Central Europe’s larges steelworks, the Slovakian VSZ has been indebted and troubled for years. To see the magnitude of the enterprise note

that VSZ accounts for 8% of Slovak GDP. Several rescue and debt restructuring operations have failed. Business analysts find that in

principle VSZ should be a healthy and profitable undertaking, having customers like Czech Skoda in its portfolio.

To relate the problems to our discussion on ownership in section 2 it is interesting to note that VSZ is owned by a consortium of politicians,

who - being stakeholders as well as shareholders - have abstained from any serious restructuring efforts, and instead obliged to their political

agenda. As a result the directly employed workforce of 25000 people25 is estimated to be four (4!) times as much as is needed for efficient

production. Sean Murphy - a steel industry analyst - comments: “the company is being run for the benefit of its employees, not its

shareholders.” (The Economist, 1999, p.63)

This case both illustrates the existence of stunning levels of over-employment, as much as it gives an indicative link to the ownership

structure of privatised SOEs.

What are the underlying issue of overmanning26

24. This case is found in: The Economist, January 2nd, 1999, pp.60-63.

25. For 1998/99. Another 75000 people are estimated to be employed through VSZ’s supply network.