Incentives for Strengthening the Adoption of Modern Costing Techniques

Manmeet Kaur

Assistant Professor in Commerce

Govt. College, Sector -14

Gurgaon [India]

Abstract

________________________________________________________________

The paper studied the incentives use by the sample companies for the satisfaction of their

employees. Employees are very important for the well implementation of both modern costing

techniques namely target and kaizen costing. For full involvement of their members

automobile manufacturing companies use different incentives for their employees. For

commitment of members it is necessary that automobile companies should focus their

inventive plans and systems. The study concludes that the full commitment from the side of

members requires some stimulus and automobile companies should use different incentives to

encourage their members.

Introduction

In current competitive business environment target and kaizen costing, are accepted as

modern cost management tools for reducing the manufacturing cost of a product. These

methods have been used by many leading firms. Target costing was invented by Toyota in

1965 (Tanaka, 1993). It was pioneered by Japanese company Toyota to achieve high quality

and desirable features at a competitive price. The target costing (genka kikaku in Japanese)

seeks to bridge the gap between the cost determined through market research and the cost at

which the firm can supply its product. Target costing was initially a market oriented cost

calculation approach consisting on determining the target cost of a product at the product

design stage before the beginning of manufacturing stage by subtracting from the target

selling price (taken from the market) the target profit fixed by the company in order to assure

desired profit margin is subtracted from the estimated selling price to determine the target

cost for the new product and its formula is:

Target Cost = Estimated Selling Price —Desired Profit Margin

Target costing is a process for ensuring that a product launched with specified functionality,

quality and sales price can be produced at a life cycle cost that generates the desired level of

profitability (Cooper & Slagmulder, 1997).

Kaizen costing was originated as cost management practice in Japanese companies after

World War II. Kaizen costing is known “Genkakaizen” in Japanese companies. Kaizen

costing method is used in manufacturing stage of the existing products as cost reduction

process. Kaizen costing focuses on continuous improvement in all processes, customers‟

satisfaction and on involvement of all employees of company. Kaizen costing is derived by

Japanese automobile companies. In 1960 Toyota established the cost management technique

namely kaizen costing (Toyota Motor Corporation, 1987). Yasuhiro & John (1993)

commented that kaizen costing works on the establishment of a cost reduction target amount

through continuous improvement or kaizen activities in operations. Guilding et al. (2000)

stated that kaizen costing is a strategic management accounting practice which is

forward-looking and closely aligned to a quest for competitive advantage. According to Yasuhiro &

John (1993) kaizen costing activities maintain the current level of the existing production

costs and further reduce costs to an expected level based on the plans of firm. A major feature

of kaizen casting is that shop floor workers are given the responsibility to decrease cost and

to improve processes. The basis of many of the cost improvement ideas is that the shop floor

workers closest to the product and production process.

The cross-functional team structure is the critic component for the implementation of target

costing and kaizen costing. Target costing and kaizen costing successful implementation

depend on the employees of different departments of the company. Literature said that

motivational consideration is very important for well execution of these techniques in

company. Target cost and kaizen cost targets can be met by the company through the

assignment and decomposition of total target costs and kaizen costs among different

departments. The amount of kaizen cost targets must not be affected by the organizational

power instead of this self control autonomous involvement should be prevailed. Targets

should be determined through consultation between managers and other members. For target

reduction optimistically thus, company needs to motivate employees by different incentives

such as information provide to employees, cooperation etc. Target costing and kaizen costing

require people involvement at all levels members of the company for successful

implementation of Japanese total cost management system.

Review of literature

Target costing is adopted as a philosophy that has gained recognition due to the need to

produce a product at a pre decided cost level. This method is used with the help of team not

to control employees and teams. In target costing process top management and all remaining

employees are important (Ansari & Bell, 1997). Typically there are four main teams in a

manufacturing process of product: the business planning team, the product team, the design

team and the product manufacturing team (Ansari & Bell, 1997). The effectiveness of this

method usually increases with the involvement of personnel. The members of team should be

trained to apply the target costing process. This system motivates employees think and act

strategically. Multidisciplinary teams are crucial (Cooper & Slagmulder, 1997). These teams

play very important role in achieving cost/price, quality and functionality objectives. Without

these teams shop floor workers commit no cost reduction. Target costing process focuses on

designing the new products and cross functional teams to assess the possible design

alternatives. Commitment of workers towards task requires trust and respect among team

members. Support of all employees is vital for target costing. Kato et al. (1995) supported

cross functional teams and they use the term “people involvement”. An integrated and skilled

product development team having members from different departments can satisfy the

requirements of market (Butscher & Laker, 2000).

Kato et al. (1995) presented some common importance of cross functional teams for target

costing. Cross functional team members are from different departments and all worked

together for smooth functioning of target costing. Active support of upper level management,

empowered cross functional teams and internal reward structure are important elements for

the success of target costing. Cross functional cooperation is also important for strategy

formulation process. Team members often negotiate to set the level of target costs but there

negotiation is not seen as bargaining. There negotiation is the rationality of the team members

and it motivates employees in positive way with their commitment to achieve assigned

The target costing method decides cost objectives and goals for teams and it is the base of

their performance measurement. Target costing can achieve its goal with the participation of

all departments and departments help in different ways. Target costing process requires the

involvement of different departments‟ employees of the organization. Different departments

perform in different ways in target costing process for the attainment of target costs.

According to Kaplan & Cooper (1998) kaizen costing is an approach to develop a costing

system to carry continuous improvement activities in a company. Kaizen costing

implementation needs the culture in which work groups can always try to meet their cost

targets and be able to identify the progress during the period. Kaizen targets or cost reduction

targets must be both attainable and satisfactory to meet generally company objectives because

if the cost target is too high workers cannot attain these and it will frustrate them and if cost

target is too low they will not take interest in these targets. It is assumed that work groups are

able to identify the place of waste existed in a process. Literature stated that the

implementation of the kaizen costing method involves the improvement of the production

process with staff or shop floor workers formation, motivation and encouragement, with the

identification of cost reduction possibilities. The main criticism of this method is stress on the

staff. Literature said that this continuous cost reduction method is stressful by its nature. This

philosophy is so deep-rooted that the team leaders and foremen in manufacturing companies

are required to meet regularly to discuss their progress for reducing costs.

Kaplan & Cooper (1998) mentioned that kaizen philosophy favours to delegate more

authority and responsibility to the specific teams in order to provide them freedom in

improving their parts in the process. In this system every activity is supported by a work team

that shares the result. Kaizen costing is carried out by the team members and it is mainly

related to operational measures. The team members are asked to produce weekly product

costs which could be decreased over time against cost target. Cheser & Tanner (1993)

indicated the use of kaizen costing within a given framework and with the involvement of

groups. They stated that after the estimation of investment working groups which are working

with that issue are informed about these estimates to make them understand about the earlier

stage of the challenges and this also provides a clarification about the problem issues and cost

rationalization to the working groups.

Monden & Hamada (1991) described the system of total cost management used by Japanese

main pillars and the first pillar target costing is used to reduce the cost of new products in the

design and development stage while kaizen costing is used by the Japanese companies for the

cost reduction of existing products in the manufacturing stage and through these two methods

Japanese companies control the overall cost of product during the whole life cycle of product.

Objective of the study

The objective of the study is to evaluate the stimuli posses by the members in implementation

of two modern costing techniques namely target costing and kaizen costing in the sample

companies. To know what are incentives behind the silent acceptance of these techniques,

from the side of employees working in sample companies.

H0- There is no stimuli posed by the members in the implementation of target and

kaizen costing techniques.

Methodology

In the present study data collected from sample companies from automobile industry is

analysed to accomplish the objective of the study.

Research Population

The research objective of the study is concern with the use of kaizen and target costing

techniques in Indian automobile companies. The target population of this study identified in

this concern is Indian automobile companies. This study concentrates only on this sector in

order to avoid confusion arising from variations between different sectors. Automobile sector

is suitable for this study because according to literature this sector have a higher proportion of

firms who are most likely to use kaizen and target costing techniques.

Sample Selection

The study has been conducted on automobile manufacturers in India. The modern costing

techniques were originated in Japanese automobile companies which provide an ideal base

for the present study on target and kaizen costing in Indian automobile companies. Cost

management is a vital area in automobile manufacturing companies and these companies

automobile companies is that they are the large-sized firms, having good image in their field

and have larger resources available for investment in new techniques such as kaizen and

target costing. The three rational criteria for sample selection were: Research objective,

existing literature and data availability and accessibility

The sample of study should be representative of the population. In this view, purposive as

well as convenience sampling have been applied to select the sample of the study, because it

is believed that selected sample companies providing the typical information for the

accomplishment of the study. Therefore, three large companies were selected which were

considered relevant to the purpose of the study.

Sample of the Study

A sample of three automobile companies was taken for the study. For the study following

companies have been taken as sample companies-

1. Maruti Suzuki India Limited

2. Hero Motocorp Limited

3. Honda Motorcycle and Scooter India Private Limited

Sample Size

The sample size from each of the sample company in this study after response of respondents

has been used as under:

Maruti Hero Motocrp Honda

I] Non Managers 87 75 48

II] Managers 39 34 20

In the above stated way total sample size of 303 has been used (and data is collected) for the

attainment of the objectives of the study.

Data collection

For the completion of the study both primary as well as secondary data have been used.Data

visits in companies, structured questionnaires which were distributed among respondents,

also e-mail of questionnaires, discussions with the officials of sample companies, feedback

from managers at different level, people at operational level, through telephone calls, face to

face conversations and interaction with employees of companies. Data from secondary

sources have been obtained from financial statements of companies, annual reports of

companies, research and development statistics of the sample companies, other documents

underlying cost management, websites of companies (Maruti Suzuki, Hero Motocorp and

Honda Motorcycle & Scooter), textbooks, web pages (internet search), trade and scholarly

Journals (literature or previous studies) related to cost management and control in

manufacturing companies.

Research Instrument

In this research, the most applicable method of primary data collection is deemed to be

questionnaires. The Two questionnaires had been developed containing various questions in

this study, one for managers and other for non-managers. The survey instrument sought

objective information about the incentives use by the sample companies, incentives change

by companies and satisfaction of employees with the incentives provide by the companies.

Statistical techniques

Analysed data is presented in form of frequency tables and in percentages. The descriptive

analysis of the data is used to provide a summary of responses of the respondents, which are:

frequency distributions and percentage. Descriptive statistics have been used to draw

percentages of frequencies. Chi-square test has been used mainly for data analyses. It is used

to find out any significant difference between observed and expected responses.

Data Analysis

The analyses regarding this objective have been done on the basis of questions in the

Table1: Incentives Provided by the Companies

MARUTI HERO HMSI

Freq-uency Per

cent

Total Freq-

uency

Per

cent

Total

Freq-uency Per cent Total Financial incentives

118 93.7 126 109 100 109 68 100 68

Good working

conditions

108 85.7 126 109 100 109 61 89.7 68

Good cooperation 94 74.6 126 108 99 109 49 72 68

Seniority base

wage system

79 62.7 126 107 98 109 59 86.8 68

Recognition 106 84.1 126 106 97.2 109 54 79.4 68

Nonfinancial

incentives

86 68.3 126 106 97.2 109 18 26.5 68

Suggestion

scheme

114 90.5 126 107 98 109 58 85.3 68

Gain / Profit

sharing

72 57.1 126 3 2.8 109 28 41.2 68

Life time

employment

facility

75 59.5 126 4 3.7 109 38 55.9 68

Welfare systems 111 88.1 126 109 100 109 66 97 68

Training 104 82.5 126 104 95.4 109 58 85.3 68

Awards 87 69 126 103 94.5 109 37 54.4 68

Bonus 86 68.2 126 102 93.6 109 53 77.9 68

Prizes 107 84.9 126 106 97.2 109 65 95.6 68

The above table 1 has elucidated the incentives provide by the sample companies to their

employees. The table depicts the frequency of responses and their percentages on the

different types of incentives provide by the sample companies. The table shows 14 incentives

companies. The table shows that Hero Company uses all incentives except gain/profit sharing

and life time employment facility incentives because in this company the percentage of

responses on these two incentives is very low. The table shows that Maruti Company and

HMSI use all incentives but there is a variation in the percentages of the responses on the

incentives of these companies. From the table it is observed that two incentives gain/profit

sharing and life time employment facility have low percentages in all companies but in HMSI

with these two incentives awards and non financial incentives have also low percentages. The

researcher notes that the difference in percentages may be due to the awareness of employees.

It is clear from the table that all companies provide different incentives to stimulate their

[image:9.595.69.529.361.656.2]employees but may be different incentives for different levels of employees.

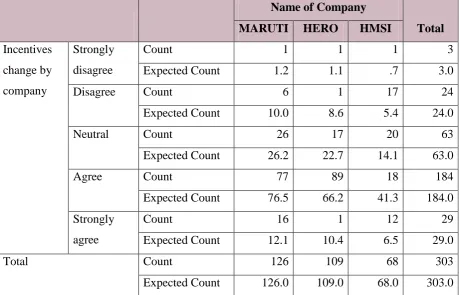

Table 2: Incentives Change by Company

Crosstab

Name of Company

Total

MARUTI HERO HMSI

Incentives

change by

company

Strongly

disagree

Count 1 1 1 3

Expected Count 1.2 1.1 .7 3.0

Disagree Count 6 1 17 24

Expected Count 10.0 8.6 5.4 24.0

Neutral Count 26 17 20 63

Expected Count 26.2 22.7 14.1 63.0

Agree Count 77 89 18 184

Expected Count 76.5 66.2 41.3 184.0

Strongly

agree

Count 16 1 12 29

Expected Count 12.1 10.4 6.5 29.0

Total Count 126 109 68 303

Chi-Square Tests

Value df

Asymp.

Sig.

(2-sided)

Pearson

Chi-Square

72.892(a

) 8 .000

Likelihood Ratio 75.387 8 .000

Linear-by-Linear

Association 12.319 1 .000

N of Valid Cases 303

a 3 cells (20.0%) have expected count less than 5. The minimum expected count is .67.

In order to analysis the strategy of sample companies to change incentives; an empirical study

has been carried out in this context. The above table 2 shows that expected and count figures

indicate a considerable difference in company strategy to change incentives. It is observed

that the calculated value of chi square at 8 df. @ 5% level of significant, indicate 72.892.

Meaning thereby, that calculated value of chi square is higher than that of given value that is

15.51. Hence, the null hypothesis is rejected. Hence, it is quite obvious that the all three

companies time to time change their strategies for incentives. It is clear from the observation

that in total (213) employees has marked on „strongly agree and agree‟. It indicates a

clear-cut picture that companies time to time change their strategy regarding incentives to

employees. The table also presents that Maruti and Hero are more concern about the change

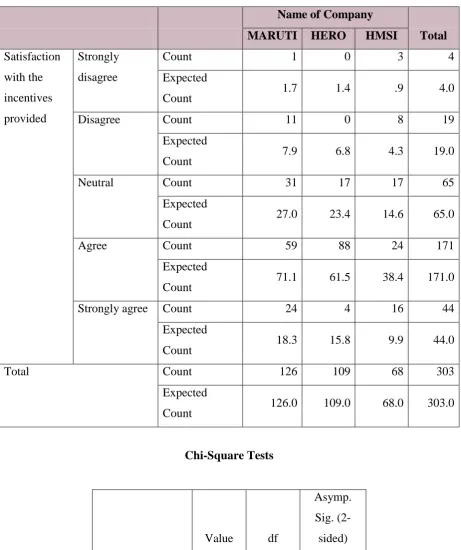

Table 3: Satisfaction with the Incentives Provided

Crosstab

Name of Company

Total

MARUTI HERO HMSI

Satisfaction

with the

incentives

provided

Strongly

disagree

Count 1 0 3 4

Expected

Count 1.7 1.4 .9 4.0

Disagree Count 11 0 8 19

Expected

Count 7.9 6.8 4.3 19.0

Neutral Count 31 17 17 65

Expected

Count 27.0 23.4 14.6 65.0

Agree Count 59 88 24 171

Expected

Count 71.1 61.5 38.4 171.0

Strongly agree Count 24 4 16 44

Expected

Count 18.3 15.8 9.9 44.0

Total Count 126 109 68 303

Expected

Count 126.0 109.0 68.0 303.0

Chi-Square Tests

Value df

Asymp.

Sig.

(2-sided)

Pearson

Chi-Square

53.942(a

Likelihood Ratio 62.354 8 .000

Linear-by-Linear

Association .466 1 .495

N of Valid Cases 303

a 4 cells (26.7%) have expected count less than 5. The minimum expected count is .90.

The above table 3 has revealed the satisfaction level of employees regarding incentives

provided by the sample companies, an empirical study has been carried out in this context.

The expected and count figures indicate a considerable difference in the satisfaction level of

employees toward incentives provided by companies. In this context, it is observed that the

calculated value of chi square at 8 df. @ 5% level of significant, indicate 53.942. Meaning

thereby, that calculated value of chi square is higher than that of given value that is 15.51.

Hence, the null hypothesis is rejected. It is quite obvious that the employees are satisfied with

the incentives provided by the companies. It is clear from the observation that in total (215)

employees has marked on „strongly agree and agree‟. It indicates a clear-cut picture that

employees of the all companies are satisfied with the incentives provided by the companies to

motivate their employees. The table also shows that employees of Hero are more satisfied

with the incentives provided by the company than Maruti and HMSI.

Conclusion

In current market environment modern costing techniques are required in every

manufacturing company and the requirement of proper cost management is more in

automobile companies due to fast changing market and customers desires. For proper

application and benefits of the use of modern costing techniques both target and kaizen

costing, commitment and involvement of employees is necessary. Without the support and

involvement of employees these techniques cannot give best results. If employees work well

then they expect something from companies. After the analyses of statements in respect of

the objective which is concerned with the stimuli posses by the members in implementation

of kaizen and target costing techniques in sample companies it is clear that for the long period

commitment of employees‟ automobile companies use different incentives and they time to

time change their incentives. Companies try to satisfy their employees and for this they

different companies use different incentives and their policies to change incentives are also

different. Finally, it is found that employees accept change and work with new techniques

when they are satisfied and for their satisfaction companies use different incentives to

encourage them.

References

Ansari, S. L. & Bell, J. E. (1997). Target costing: the next frontier in strategic cost

management. New York: McGraw-Hill.

Butscher, S. A. & Laker, M. (2000). Market-driven product development using target

costing to optimize products and prices. MM, Vol. Summer, pp. 48-53.

Cheser, R. & Tanner, C. (1993). Critikon declares war on waste, launches kaizen drive.

Target, Vol. 9, pp. 12-22.

Cooper, R. & Slagmulder, R. (1997). Target costing and value engineering. Portland:

Productivity Press, IMA Foundation for Applied Research.

Guilding, C., Cravens, C. K. & Tayles, M. (2000). An international comparison of

strategic management accounting practices. Management Accounting Research, Vol. 11,

pp. 113-135.

Kaplan, R. S. & Cooper, R. (1998). Cost and effect-using integrated cost systems to drive

profitability and performance. Boston: Harvard Business Press.

Kato, Y., Boer, G. & Chow C. W. (1995). Target costing: an integrative management

process. Journal of Cost Management, Spring, pp. 39-51.

Monden, Y. & Hamada, K. (1991). Target costing and kaizen costing in Japanese

automobile companies. Journal of Management Accounting Research, Vol. 3, pp. 16-34.

Tanaka, T. (1993). Target costing at Toyota. Journal of Cost Management, Spring, pp.

4-11.

Toyota Motor Corporation. (1987). History of Toyota Motor Corporation for 50 years.

Toyota Motor Corporation.

Yasuhiro, M. & John, L. (1993). How a Japanese automaker reduces costs?. Health Care