A Statistical Analysis of Intensities Estimation on the

Modeling of Non-Life Insurance Claim Counting Process

Uraiwan Jaroengeratikun, Winai Bodhisuwan, Ampai Thongteeraparp Department of Statistics, Kasetsart University, Bangkok, Thailand

Email: [email protected], {fsciwnb, fsciamu}@ku.ac.th

Received October 1, 2011; revised November 19, 2011; accepted November 28, 2011

ABSTRACT

This study presents an estimation approach to non-life insurance claim counts relating to a specified time. The objective of this study is to estimate the parameters in non-life insurance claim counting process, including the homogeneous Poisson process (HPP) and the non-homogeneous Poisson process (NHPP) with a bell-shaped intensity. We use the estimating function, the zero mean martingale (ZMM) as a procedure of parameter estimation in the insurance claim counting process. Then, Λ (t), the compensator of N (t) is proposed for the number of claims in the time interval (0, t]. We present situations through a simulation study of both processes on the time interval (0, t]. Some examples of the situations in the simulation study are depicted by a sample path relating N (t) to its compensator Λ (t). In addition, an example of the claim counting process illustrates the result of the compensator estimate misspecification.

Keywords: Estimating Function; Zero Mean Martingale; Non-Life Insurance Claim Counting Process; Poisson Process; Bell-Shaped Intensity

1. Introduction

Nowadays, insurance is a common way of managing risks and the insurance industry has grown rapidly over time. Insurance industry owners, especially, consider the components of risk management, such as the premiums which are the main income of insurance businesses, re- serves, underwriting, investment planning, reinsurance planning, etc. Also, estimating claims play an important part in each component in the non-life insurance field. In the past four decades, a few researchers have studied the claim counts model for non-life insurance. Klugman et al. [1] and Denuit et al. [2] were interested in studying the frequency distribution of insurance claims, including the parameter estimation methods. Bühlmann [3,4] presented the credibility approach in the form of a linear function to estimate and predict the expected claim counts in up- coming periods, using past experience of claims as a risk class or related risk classes. Bühlmann’s credibility ap- proach is interesting and can be extended to other ap- proaches, such as the Bühlmann-Straub model, Jewell’s model or the Exact credibility approach, etc., (see Klug- man et al. [1]). Calculating the expected claim counts using the credibility approach only depends on the in- formation from prior experience of claim counts, and does not consider the occurrence behavior of claim counts over time. Some authors have found an alternative

approach to claim counts relating to a specified time or their behavior over time, for example, Mikosch [5] viewed the claim counting process as a homogeneous Poisson process (HPP) in the Cramér-Lundberg model, one of the most popular and useful risk models in non-life insurance, and Matsui and Mikosch [6] also considered a Poisson cluster model for the modeling of a total claims amount by a point of claim counts as an HPP with a constant rate of occurrence called the constant intensity. For some non-life insurance portfolios, the claim counts during a time period are caused by periodic phenomena or sea- sonality. These claim counts are modeled in terms of a non-homogeneous Poisson process (NHPP) with a period time-dependent intensity rate. Morales [7] presented the periodic risk model consisting of the claim counting process with a bell-shaped intensity function (called the Gaussian intensity) of the form

2 *

2

1 1

exp

2

1 1 2π 2

2 2

t t

;

0,1

t ,

s t

*t , where s is an initial season, s

also considered evaluating the ruin probability through a simulation study. Furthermore, Lu and Garrido [8] ex- plored the periodic NHPP model with a Beta-shaped in- tensity function.

The precision of claim count estimation is a key to running the insurance business successfully. In this study, we will present an estimation approach to non-life insur- ance claim counts related to a specification of the two different claim counting processes, i.e., HPP, and NHPP with a bell-shaped intensity function, through a simula- tion study. Our purpose is to estimate the parameters in the non-life insurance claim counting process. The pa- rameters in the insurance claim counting process, inten- sity function (

t ) in terms of mean value function

0

d

t

t u

uN

u

, makes a complicated distribution func-

tion of insurance claim counts. An estimating function, such as the zero mean martingale (ZMM), is used here as a procedure of parameter estimation of an insurance claim counts model, and the parameters of model inten- sity are estimated by the MLE method.

2. A Definition of the Non-Life Insurance

Claim Counting Process

We define the insurance claim counting process

; , and the insurance claim counts which have occurred in the time interval (0,t] where n 1 n; is a claim arrival time and i is independent and identically distributed (iid)

Exponential with the parameter , called the inten- sity rate, is a counting process which is non-decreasing, can be written as

#

1: iN t i T t

T W

W

N N t

N tt

t0W n

0 t

1

wi

;

0

d

N t

N u where dN t

is an increment ofin a small fraction period. The Poisson distribution is often considered as a common distribution modeling of insurance claim counts, and our main interest in the process of insurance claim counts is the Poisson process, i.e., HPP, and NHPP with the bell-shaped intensity func- tion. This interest lies in the intensity rate, in which the insurance claim counts occur, and whether these change over time. In an HPP, the intensity rate is constant for a given time, and the process is called an NHPP, if it changes as a function of time [2,5,9].

On a probability space

, , P

, N t

is Poissont

distributed with the parameter

, with a0

d t u

mean value function E N t

t . As

;t0

t t k t is called the multiplicative in- tensity, where

t and k t

are defined as the in- tensity rate and the exposure risk, respectively. We con-sider as a non-decreasing right continuous step func- tion 0 at time t = 0 and jumps of size 1, and

N

exp

Pr ; 0,1, 2,

!

n

t t

P N t n n

n

and Pr d

N t

1

t t E N td

d

.In this study we consider the insurance claim counting process which are the HPP with

t , a constant intensity, and the NHPP with a bell-shaped intensity function as an initial season, s = 0 [7],

2 *

2

1 1

exp

2 2

1 1 2π

2 2

t t

(1)

where * (an average number of claims over a period)

and are the parameters, *, 0.

3. Parameter Estimation in the Non-Life

Insurance Claim Counting Process

In this section, we introduce the methods which are use- ful for parameter estimation in the non-life insurance claim counting process, including the estimating function, the martingale method, and the MLE.

3.1. Estimating Function

On a probability space

Ω, , P

,where , an open interval on the real line, P p - pose that the observation N t

stimating func- tions,is p

N t ;

. Su n , the e

;

g N t , are functions of N t

an pa- rameterd the

. By solving g N t

;

es- timating equation, an estimate of is obtained. Then0 , a so-cal

led

;

g N t is an unbiased estimating function if

;

E g N t 0 fo

In t study, the parameter es- tim

tingale Method

esses relating to time. r all [10].

his

3.2. The Mar

estimating function for

ation in the insurance claim counting process is pro- vided by the martingale method.

The martingales are random proc

On a probability space

Ω, , P

, we suppose the in- creasing family

t ; 0t

, a filtration or historyt

, which is the available data at the time t. The proc- ess M

M t

; 0t

is a martingale with respect to if E M t

exist, and

M ts t

M

t for all s As a result of the maE 0.

the properties of rtingale, E

M

t

E M

0

for all t0, then E M

0

0This of the is useful for con for a ZMM [11,12].

ethod -

study martingale m

tion in the insurance claim counting process. The process takes place over a small time interval ( ,t td ]t ,

d

dE N t t t and as a res e meaning

he martingale can be written as

dN t t td dM t (2

48exp 10 1 2 2t t

.

t

of martingale property, t

)

which is a martingale-difference. Then, the following mar-

or it is rewritten in the form of

ult of th

3.3. A Maximum Likelihood Estimation of the Model Intensity

In order to get the estimate of the compensator of N t

,

ˆ t

, on the modeling of the non-life insurance claim counting process, both the HPP and NHPP, the parame- ters of the intensity function are estimated by the MLE method. GivenN t

n,we suppose that 1 2 3( )

, , , t t ,t

N t are the arrival times of the claims in the time inter-

val with a cumulative distribution function (a ge- neral order statistics model)

t (0, ]t

1 exp

F t t

likelihood function [5,13] is given by

. The tingale is

0 0

d d d

t t

N u u u M u

,

N t t M t in, is a ZMM. Based on ZMM, we obta

0

E M t E N t t .

Thus, is an estimating equation for

th

0 N t t

eter estimation i

e param n the insurance claim counting process. Also, as a result of the parameter estimate in the process, this can be interpreted as an N t

estimate or, in other words,

t is called th pensator of

N t , and this estimate is useful for predicting the times currence of insurance claim counts [12]. We can depict the systematic part of the process of insurance claim counts, N t

, related to its compensator,e com

of oc

t ,

and the associated martingale

t in ple N t t M Figures 1(a) and (b), respectively of 15 independent random times of claims occurrence in the NHPP with an intensity of, based on a sam

1

; n i exp

i

l t

θ tn

(3)where is a vector of the parameters of the model in- tensity,

θ

denotes the set of arrival times, the intensity

t in the HPP is as θ and the intensity

t

*,

in the NHPP is given in Equation (1) as θ . The estimate of can be simply found if we take the logarithm of the likelihood function and we seek a value of that maximizes the log likelihood function. The following parameter estimate of the HPP model is:θ

θ

( )

ˆ ˆ .

N t n

n t

θ For the NHPP, the calculation of the

(a) (b)

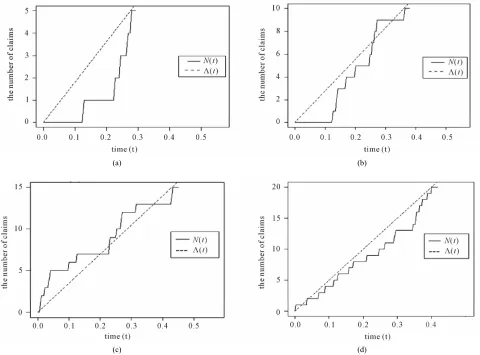

Figure 1. In a sample of 15 independent random times of claims occurrence with the intensity

2

1 48exp 10

2

t t ,

(a) Non-life insurance claim counting process N t

related to its compensator

t ; and (b) Martingale

MLE estimator of the model intensity, which is a

com-dure, i.e. the Newton-Raphson algorithm, to solve these

. Simulation Study

sity or in term

plicated system of equations, requires an iterative proce-

equations [2].

4

In this study, a simulation study is used to investigate how the observation of the non-life insurance claim counting process can be used to estimate its model pa- rameter, i.e. inten

t

tartingal ura

, using the d by the m e method HPP of the ins nce claim estimating function provid

with ZMM. In particular, t e he

counts, with

t as a constant intensity and the NHPP of the insurance claim counts, with

t given in Equation (1) as a bell-shaped intensity, we must first consider the simulation study of the HPP e insurance claim counts in the time interval (0,t] in which the ob- servation involves the claim arrival times, t t t1, , , ,2 3( )

of th

N t

t , generate lying an exponential law with the intensity

d by app

, i.e. with a mean 1 as λ = nd 10. The second simulation study of the insurance claim counting process, in which we consider the NHPP with a bell-shaped intensity function, or as the general form of mean value function

0.1 a

* [ ] 1

[ ]

2

t t

t t

, 0

t , where [ ] is the greatest integer function, the claim arrival times,

0.5

1, , , , 2 3 N t( )

t t t t

value function t mean one are independent ean one, where

, can be simulated ng the m as a claim arri- me of the HPP with ]. It implies that d expone ally by usi val ti 1 2 E E distri ean

, En

th m

[7 an3

, , ,E buted wi

nti

Ei ti ti1 , l i1, 2,3 ,n. So, in this study, the nth claim

arrival time, ( )

for al ,

N t n

t , i

1

( ) 1 2 3

s generated by

N t n n

t E E E E

(4)

where 1

1

D 0. * 5 e

is the invertibl

function of

t ,*

*

* D

D 1

2 , 1 1 2 2

D

and

1

is

tion of a standard normal distribution, with

the quantile func-

* 0.1

,

0.25

, *0.1, 5, *10, 0.25 and * 10

, 5. ulation st

In this sim udy of bo of the insurance claim co th

the number of observations, , is composed of 5, rried ou

with 5000 sample paths. In each sample path, the pa-l intensity is computed us od function, such as

h is arameter

th the HPP and the NHPP unts in e time interval (0,t],

N t n10, 15 and 20. The HPP and the NHPP are ca t

rameterestimate of the mode -ing the MLE meth and the estimat-ing

the ZMM whic used to estimate the p

t in the process (or the compensator

t of N t

), i.e. fitting the compensator estimate ˆ

t to N t

to m . Also,

ea the mean squared e r

things, fitting

rro (MSE) is provided sure

ˆ

t to N t

as the following form,

20 1 ˆ d MSE t i i p i

u N u u

p

,where p denotes the number of sample paths. Notice that the MSE of the compensator estimate ˆ

t of

N t for both processes, as shown in Tables 1 and , depends on the parameters of the mod intensi s the following details, for the HPP wit onstan tensity

0.1

2 a el

h a c

ty t in

, a small intensity rate, and the MSE of the com- pensator estimate ˆ

t of N t

increases exponen- tially as the numb vations increases. On the same er of pr obser ocess e other hand, th with 10, the MSE of the compensator estimate ˆ

t of N t

numbe occurre

decreases ease nce, and the

si ex- s until n the ty, ponentially, wh

the observed s alu

ile th 15 tim

e observatio es of claim

n r incr

[image:4.595.306.537.448.535.2]MSE v e begins to increase as the observation number increases. For the NHPP with a bell-shaped inten the

Table 1. MSE of the compensator estimate ˆ

t of N t

in the HPP of non-life insurance claim counts.λ N(t) MSE λ N(t) MSE

5 1.003785 5 11.90220

10 1.834148 5.776900

15 2.665881 15 4.904133 0.1

20 3.528792 10

[image:4.595.308.537.580.733.2]20 5.012547 10

Table 2. MSE of the compensator estimate ˆ

t of N t

in the NHPP of non-life insurance claim coun* *

t

λ σ N(t) M N( ) MSE

s. t

SE λ σ

5 0.871903 5 75.96249

10 5 0.25 0 1 997 758056 0.1 20 2.4606 10 738440 1.710731 10 5 0 0 4. 20 4. 7.631638

1 2.458339 1 5.351834

2 3.267897

0.25

2 5.378968

5 0.831601 5 23.74056

10 1.059291 7.602

15 1.625630 15

5 5

parameters of its odel m intensi ty *0.1, 0.25 and *0.1, 5

riod

(a sm m

claim SE of the

mate

all average nu com

ber of a ensator esti-s over a

pe ), the M p ˆ t

ber ea arameters o

of N

t incthe m

reases

num consid

the p tensity

as

e NHPP b

* 0.1

the observation incr ses. When we

f

er th etween 0.25 odel in ,

and *0.1, 5

f th

, we fou th

th ns

nd inte

at in th

ity *e pr0.1ocess with

e parameters o e model , 5, of the MSE of the compensator estimate ˆ

t N t

a f

is m HPP w

mod uch el intens

lower. In th

e same N ith the par meters o

ity *10, 0.25, the MSE of th e

compensator estimate ˆ

t ber incr of eases u

N t decrease ntil th

s while served 1 its observa

reas tion num

as the

e ob 5

alues be-times of claims occurrence, and then its MSE v

gins to inc e observation number increases. The MSE of the compensator estimate ˆ

t of N t

in the same NHPP with the parameters *10, 5 de-creases exponentially as its observation number increases. When we consider the NHPP betwee ra

the model in nsity te *10, 0.25n the pa meters of and *10 ,

5

, we found that in the process wi rameters

of the model intensity * 10

th the pa

, 5 e MS the compensator estimate

, th E of

ˆ t

of N t

h rthan the other one.

Some examples in these situations of both the HPP and the NHPP with a bell-shaped inte f n nsur- im ts based on a sample of 5, 10, 15 and 20 times of claims occurrence are illu in res 2 and 3, including the

is muc lowe

on-life i ance cla coun

Figu nsity o

strated

N t and its compensator

t . Figure 2 shows a sample path of t

stant he HPP with a con intensity 10. The N t

and its compensator

t are characterized by the intensity , i.e. 10, the compensator

t fits well with N t

, as the obser- vation number is 15 and 20 (slightly larger than the in- tensity 10). Simi the N t

and its com - satorlarly, pen

t in the NHPP are characterized by the pa- rameters of the model bell-shaped intensity *10,

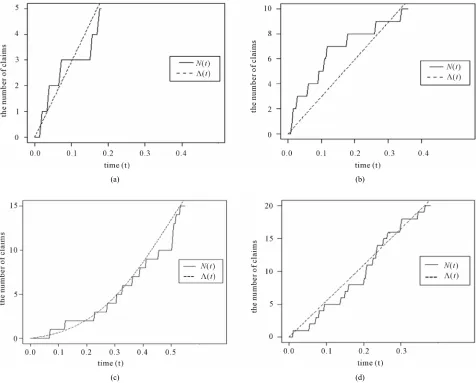

5

in Figure 3. The compensa r to

t

fits with

[image:5.595.58.538.350.705.2]N t , as the o vation number is nd 20 (slightly larger than the parameter of model intensity bser 15 a *10).

Figure 4 rates a sample path HPP, and we can see th erence with the compensator estimate which

illust of N

e diff

(a) (b)

(c) (d)

(a) (b)

[image:6.595.60.536.84.467.2](c) (d)

igure 3. and its compensator

F N t

t in the NHPP with the parameters of a bell-shaped intensity * = 10, σ = 5 [image:6.595.58.279.509.701.2]based on a sample of (a) 5 claims; (b) 10 claims; (c) 15 claims; and (d) 20 claims.

Figure 4. N t

, ˆ

t HPP, and ˆ

t NHPP in the NHPP of non-life insurance claim counts.uses the estimation method of NHPP with a period time- dependent intensity, ˆ

t NHPP, fits well with N t

SE = 5.35 nstead, th

NHPP is

hod of HPP r estim

by MSE = 1.48 shown wi ine and the M

along 5000 sample p table that if, i e

compensator estima cal-

culated more easily b ati

with a constant inten he com ate misspecification

th a dashed l aths. It is no te misspecification

y using the estim sity, and t

ˆ t

on met pensato

t HPPˆ

fluctuates a lot from

, g N t E of fittin shown on the do Figure 4. Tthe compensato ecific tted lin

r esti e in mate missp

he MS

ation ˆ

t HPP to

N t path

is 2.72, an 5.53 s are larger th of th

d the MSE = an the fitting

along 5 e comp

000 sam ensator e

ple sti- mate ˆ

t NHPP to N t

.5. Conclusion

compensator estimate to in the time inter- val depends on t param f model intensity as in e following arding the HPP with all intens with st no claim occur- ren ile the num ob ns is very small, the c ensator estim

ˆ t

he de ity rate,

ber of ate

N t eters o tails, firstly, regalmo servatio (0, ]t

th a sm ces, wh

omp ˆ

t is a good fit to N t

nstant num- nstant with less of a MSE. In with a co inten ity rate, the claim nce rate, when the ber servations i han the co inten e MSE of t r estimatethe sa s o s slight

he co me ccurre ly l m

process

arger t pensato s

of ob

sity, th ˆ

to the ity, a *

of is much regards t

with the param l intens

N t NHPP

less. Sec eters of th

ondly, as

e mode

a period, ny has a ve

o

ry small avera s over alm st no claim occurre od, and a

ge num nces

ber of claim

over a peri , e com- as th mber of ob small, th

pen stimate e nu sator e

servations is very

ˆ

ity, with t is e same pr

a g o an av

ood fit to cess with

erage

with

of Using th rame

th l intens nu

iod

N t the pamber

less ters o of claim a MSE.

e mode

f s over a per * is no less than one and any , while

the number of observations is slightly larger than the value of *, the MSE of the compensator estimate

ˆ t of N t

is m . Some examples of the situations in the simulation study are also depicted by a sample path relating N t

and its compensatoruch less

t . Furthermore, the result of the compensa te mis- specification ˆ

t of N t

is illustrated by a sample path of the NHPP so that the MSE of fitting the compen-sator estimate misspecification ˆ

t to N t

is larger than the fitting of the compensatortor estima

much

t to

N t .

REFERENCES

[1] S. A. Klugman, H. H. Panjer and G. E. Willmot, “Loss ata to Decisions,” 3rd Edition, John Wiley en, 2008.

tuarial Modelling of Claim Counts,” John Wiley & Sons, . doi:10.1002

Models from D & Sons, Hobok

[2] M. Denuit, X. Maréchal, S. Pitrebois and J. F. Walhin, “Ac-

Hoboken, 2007 /9780470517420

, pp.

ag, Be

[3] H. Bühlmann, “Introduction Report Experience Rating and Credibility,” ASTIN Bulletin, Vol. 4, No. 3, 1967, pp. 199-207.

[4] H. Bühlmann, “Credibility Procedures,” Proceedings of the Sixth Berkeley Symposium on Mathematical Statistics and

Probability, University of California Press, Berkeley, Vol.

1, 1972 515-525.

[5] T. Mikosch, “Non-Life Insurance Mathematics,” 2nd Edi- tion, Springer-Verl rlin, 2009.

doi:10.1007/978-3-540-88233-6

[6] M. Matsu T. Mik , “Prediction in a Poisson Clus- ter Model,” Journal of Applied Probability, Vol. 47, No. 2, 2010, pp. 350-366.

i and osch

239/ja 6784

doi:10.1 p/127 896

[7] M. Morales, “On a Surplus Process under a Per En- vironment: A Simulation Approach,” North American Ac- iodic

tuarial Journal, Vol. 8, No. 2, 2004, pp. 76-87.

[8] Y. Lu and J. riodic Non-Homo-

geneous Poiss e Swiss Asso-

Probability Models,” 5th Edi-

w, 2004.

w York, 1993.

Garrido, “On Double Pe on Processes,” Bulletin of th

ciation of Actuaries Swiss Association of Actuaries-Bern,

Bern, 2004, pp. 195-212. [9] S. M. Ross, “Introduction to

tion, Academic Press, Inc., San Diego, 1993.

[10] P. Mukhopadhyay, “An Introduction to Estimating Func- tions,” Alpha Science International Ltd., Harro

[11] P. K. Andersen, O. Borgan, R. D. Gill and N. Keiding, “Sta- tistical Models Based on Counting Processes,” Springer- Verlag, Ne

[12] P. Yip, “Estimating the Number of Error in a System Using a Martingale Approach,” IEEE Transactions on

Reliability, Vol. 44, No. 2, 1995. pp. 322-326.

doi:10.1109/24.387389

oftware Reliability ic Intensity Functions,” [13] J. E. R. Cid and J. A. Achcar, “Bayesian Inference for Non-

homogeneous Poisson Processed in S Models Assuming Nonmonoton

Computational Statistics & Data Analysis, Vol. 32, No. 2,