The impact of audit committee expertise on audit quality : evidence from UK audit fees.

Full text

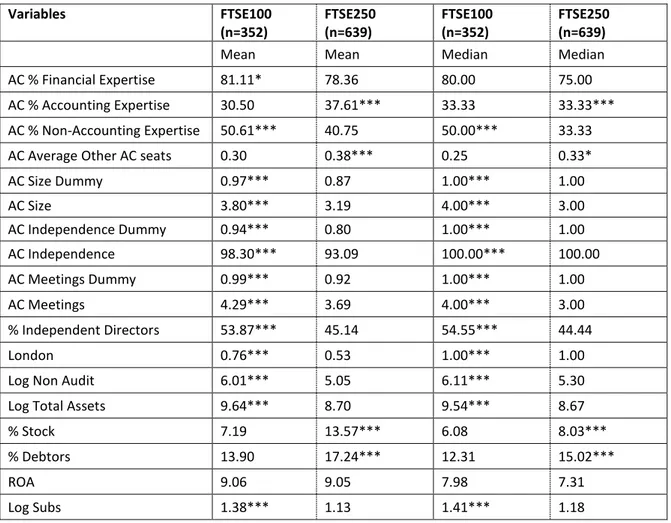

Figure

Related documents

In the process of verifying or discrediting each statement made about the Medicaid program, you will learn to research primary and secondary sources in

Our range of casement windows offer security, energy efficiency and are available in a multitude of styles and finishes to enhance the look of your home..

Customer The network of connected identification providers Bank Customer’s secure identification provider Taxation authority Insurance company Social security office Registration

Permissions for entering data is intended for using the Address book of business partners and their accounts and for preparation or import of payment orders. Permissions

While the study found that crime drama viewers were more likely to expect scientific evidence to be presented in a case, their decision making regarding a guilty verdict was

(a) Participants who have had previous experi- ence with target toys or viewed the commer- cials previously are less likely than partici- pants who have not had previous experience

Although the relationship between exposure and effects is neither simple nor direct, more than 40 years of research has indicated that television, video games, and internet

Post-Departure Trip Interruption coverage will take effect on the Scheduled Departure Date of your Covered Trip if the required plan payment and any necessary enrollment form