A STUDY ON CUSTOMER PREFERENCES FOR E-BANKING

SERVICES

*Navratan Bothra

**Dr. R.K.Shukhla

***Bindiya Tater

Abstract

The rapid advancement in electronic distribution channels has produced tremendous changes in the financial industry. Increasing rate of change in technology has provided efficient, reliable, securable, and convenient financial services such as online payment, deposit/loan, clearing/settlement, via electronic channels for customers. E-banking services not only create new competitive advantages but also improve their relationships with customers for banks. The objective of this study is to explore factors such as convenience, usage, length of relationship with bank, transaction time, awareness and access to internet facility thataffect a customer’s level of satisfaction with respect to electronic banking services provided by Indian banks. Explorative research methodology has been used to accomplish the study using convenience sampling technique. The data was collected from 200 bank customers through structured questionnaire method. The area of the study was taken from the Bikaner-Jaipur region of Rajasthan. The customers using banking services with the different e-channels are more satisfied then the customers of traditional banks but the lack of awareness is a major obstacle in the spread of e-banking services. The findings of the study indicate that the latest technologies bring a large customer base for the banks and banks ensure complete security for the transaction made by customers. The findings are tabulated with the help of tables. The paper concludes with suggestion to make e-banking services more effective in the future. Keywords: Electronic distribution channels, E-banking services, customer satisfaction

Introduction

Liberalization has triggered reforms in the banking sector. In 1993-94, RBI allowed the entry of the private sector and foreign banks into the banking industry that led to greater competition and enhanced performance, with the aid of technology advancements. This provides prompt and reliable customer services with a variety of hi-tech products and services.

Electronic banking is the term used for new age banking system. Electronic banking is defined as the automated delivery of new and traditional banking products and services directly to customers through electronic, interactive communication channels. Technology in Indian banking has evolved substantially from the days of back office automation to today’s online, centralized and integrated solutions. E-Banking is also called Internet banking, on-line banking or PC banking.

*Ph.D. Research Scholar, Madhya Pradesh Bhoj Open University, Bhopal, Email Id:[email protected]

** Professor& Head, Regional College of Education, Shamala Hills, Bhopal (M.P.), Email Id:[email protected]

***Lecturer, Sobhasaria Engineering College, Sikar, Email Id:[email protected]

electronic fund transfer etc to conduct banking activities such as transferring of funds, paying bills, viewing and checking , savings account balances, paying mortgages , purchasing financial instruments and certificates of deposits. The services through e-channel are assumed to be cost effective and time saving as they do not necessitate waiting in long queues.

Electronic banking is a result of explored possibility of using internet application in one of the various domains of commerce. It is difficult to infer whether the internet tool has been applied for convenience of bankers or the customers. But ultimately it contributes in increasing the efficiency of the banking operation besides providing more convenience to customers.

The present study makes a humble contribution to assess perception, satisfaction, and awareness among customer towards e-banking services provided by banks. It also analyze factors such as age, nature of employment, convenience, usage, length of relationship with bank, transaction time, security concern that affect customer preferences with regards to e-banking. This study also attempt to compare traditional banking and e-banking services.

Objectives of the Study:

• To study and compare traditional and e-banking services.

• To analyze the awareness among customers for different e-channels provided by banks from the Bikaner-Jaipur region of Rajasthan.

• To determine customer preference for e-banking services on the basis of age, nature of employment and income.

• To assess the choice of the customer towards e-banking services on the basis of factors such as convenience, frequency of usage, length of relationship with bank, transaction time.

Methodology:

This survey is conducted to study and analyze the perception of bank customers and to ascertain preferences for e-banking services. The primary data was collected through structure questionnaires and secondary data was collected from books, research papers, journals, magazine and internet. A sample of 200 bank customers was taken from the Bikaner-Jaipur region of Rajasthan. Convenience sampling method was used to collect data from customers.

The data analyzes uses percentage and weighted average score methods. The respondents were asked to indicate their preferences on 3-point Likert scale; they were asked to choose options, not satisfied, satisfied and very satisfied. Weight of 1, 2, and 3 were assigned to the scale to calculate WAS (Weighted average score).

Limitations of the Study:

In undertaking the study, a number of problems were faced. Thus the study has several limitations which are:

(a) The survey conducted for the study is one type of exploratory research. So, it does not provide conclusive evidence. Subsequent research will be required to provide conclusive evidence.

(c) Detailed classification of respondents could not be done. Each respondent might have been classified on the basis of their “Age”, “Educational Background”; “Nature of profession”, etc. Analysis may be diversified on the basis of this classification.

(d) As the sample size is very small, geographical and regional differences could not be made.

Major findings of the study:

An attempt has been made to study the customers’ preferences towards the banking services provided by e-channels.

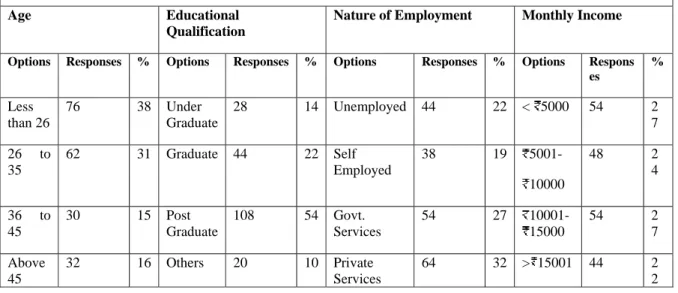

Table 1(a):Socio-economic Background of the Respondents

Age Educational Qualification

Nature of Employment Monthly Income

Options Responses % Options Responses % Options Responses % Options Respons

es

%

Less than 26

76 38 Under

Graduate

28 14 Unemployed 44 22 < 5000 54 2 7

26 to 35

62 31 Graduate 44 22 Self Employed

38 19 5001-

10000

48 2 4

36 to 45

30 15 Post

Graduate

108 54 Govt.

Services

54 27 10001-15000

54 2 7

Above 45

32 16 Others 20 10 Private Services

64 32 > 15001 44 2 2

Socio-economic background of the respondents:

The socio-economic background of customers affects their perception to a great extent. The result in table 1 reveals that out of 200 customers, 38% of the respondents belong to the age group of less than 26 years, 31% of the respondents lies between the age category of 26 years to 35 years, 15% belongs to the age group of 36 years to 45 years and 16% belong to the age category of above 32 years.14% of the people are undergraduate, 22% of respondents are graduate, 54% of respondents are post graduate and 10% belong to other category.22% of the people are unemployed, 19% are self employed, 27% belong to the category of service class and 32% belong to the category of private class.27% of the respondents have a monthly income of less than 5000, 24% of the respondents belong to the category of 5001 to 10000, 27% belong to the category of 10001- 15000 and 22% belong to the category of more than 15000.

Table 2:Relationship with bank

Saving a/c Salary a/c Current a/c Demat a/c

Responses % Responses % Responses % Responses %

144 72 14 7 28 14 14 7

Table 3:Time period associated with bank Less than 1 year Between 1 year to 3

years

Between 3 year to 5 years

Greater than 5 years

Responses % Responses % Responses % Responses %

22 11 70 35 60 30 48 24

Table 3 represents the responses regarding their time period of association with banks. It was observed that 11% of the respondents are associated with the bank for less than one year, 35% of the respondents between 1 year to 3 years, 30% of the respondents between 3 years to 5 years and 24% of the respondents for more than 5 years.

Table 4:Preference of e-banking to manual banking

Internet banking ATM banking IVRS phone banking Manual banking Responses % Responses % Responses % Responses %

57 28.5 75 37.5 38 19 30 15

Table 4 shows that customers prefer e-banking services such as internet banking, ATM banking and IVRS phone banking more than manual banking. This concludes that e-banking services are more convenient, reliable, time and cost effective as compared to manual banking services and customers are more satisfied with these services.

Table 5:ATM usage among respondents

Once in a day Once in a week Once in a month Regularly

Responses % Responses % Responses % Responses %

16 8 38 19 54 27 92 46

Table 5 shows ATM usage among customers. It was found that 8% of the respondents use ATM service once in a day. 19% of the respondents use ATM regularly, 27% of the respondents use ATM once in a month and 46% of the respondents use ATM regularly. So we can say an ATM service is most popular because it provides quick and easy transaction to the customers, save time as well as cost.

Table 6:Transaction time at ATM by respondents

Less than one minute Between 1 to 3 minutes Between 3 to 5 minutes More than 5 minutes

Responses % Responses % Responses % Responses %

34 17 94 47 58 29 11 6

Table 7:Awarness of all ATM locations by respondents

NO Yes

Responses % Responses %

130 65 70 35

Table 7 represents awareness of all ATM locations by the respondents. Out of the sample taken, only 35% users were aware of the location of their banks ATM.65% of the respondents are not aware about the location of their banks ATM. So, we can conclude that awareness of the customer about ATM services regarding their utility in different locations helps in improving the perception of the customer.

Table 8:Preferred location for ATM usage among respondents

Near to Home Near to Office AT your branch Any where in the city Responses % Responses % Responses % Responses %

92 44 54 26 28 14 34 16

Table 8 represents frequency of ATM usage by the customers. When it comes to ATM usage,44% of the respondents prefer to use ATMs near their homes, 26% of the customers prefer to use ATMs near their office, 14% of the customers prefer to use ATMs at their own bank branch and 16% of the customers prefer to use ATMs anywhere in the city.The customer finds an ATM nearer their home to be more convenient and safe.

Table 9:Level of satisfaction among respondents with ATM services

Factors Particulars Not satisfied (1)

Satisfied (2)

Very satisfied (3)

Likert 3- point scale

Responses Responses Responses Weighted score

Total score Percentile points F1 Easy

accessibility

42 70 88 446 600 74.33

F2 Convenience (24* 7) Environment

34 68 98 464 600 77.33

F3 Variety of

transaction

54 124 22 368 600 61.33

Table 10:Internet banking access among respondents

Regularly Once in a week Once in a month Never

Responses % Responses % Responses % Responses %

32 16 48 24 59 29 61 31

Table 10 represents internet-banking being accessed from the selected sample size. 31% of the respondents never used Internet banking. 24% of the respondents used internet-banking once in a week and 29% used it once a month. Only 16% use internet banking regularly.31% of the respondents had never accessed their account on the internet because customers had security and fraud concern.

Table 11:Preferred places to access internet banking

At cyber cafe At Home At office With mobile phones Responses % Responses % Responses % Responses %

23 11 133 66 33 17 11 6

Table 11 shows that 66% of customers preferred to use internet-banking services at home rather than at cybercafés and offices. At home, transactions are safer and can be kept confidential. 11% of customers accessed internet-banking at Cyber cafés which is not safe and secure.

Table 12:Level of satisfaction related to internet banking Factors Particulars Not

satisfied (1)

Satisfied (2)

Very satisfied (3)

Likert 3- point scale

Responses Responses Responses Weighted score

Total score

Percentile points F1 Internet

banking services

89 89 22 333 600 55.5

F2 Page set up 56 122 22 366 600 61

F3 Easy of use 61 106 33 372 600 62

F4 Speed loading

78 100 22 344 600 57

F5 sufficiency 78 89 33 355 600 59

F6 Transaction 39 122 39 400 600 66

F7 Visual design 50 106 44 394 600 65

Table 12 shows the customer level of satisfaction with internet banking services. This was analyzed on a 3-point scale on such parameters such as internet banking services, page set-up, easy use, speed-loading, sufficiency, transaction and visual design.55.5% of the customer are satisfied with the internet banking services, 61% of the customer are satisfied with page setup, 62% prefer internet banking because they are user friendly, 57% are satisfied with the speed of loading, 59% of the respondent are satisfied with sufficiency, 66% are satisfied with transaction, 65% are satisfied with visual design.

Table 13:Customer using IVRS phone banking

Regularly Once in a week Once in a month Never

Responses % Responses % Responses % Responses %

26 13 49 24 60 30 65 33

Table 14:Effectiveness of IVRS phone banking replying among respondents

Not effective Effective Very effective

Responses % Responses % Responses %

108 54 28 14 64 32

Table 14 represents effectiveness of IVRS phone-banking reply among respondents.54% of customers find the IVRS phone banking replying ineffective, 14% find the IVRS phone banking replying to be effective and 32% find the IVRS phone banking replying to be very effective.

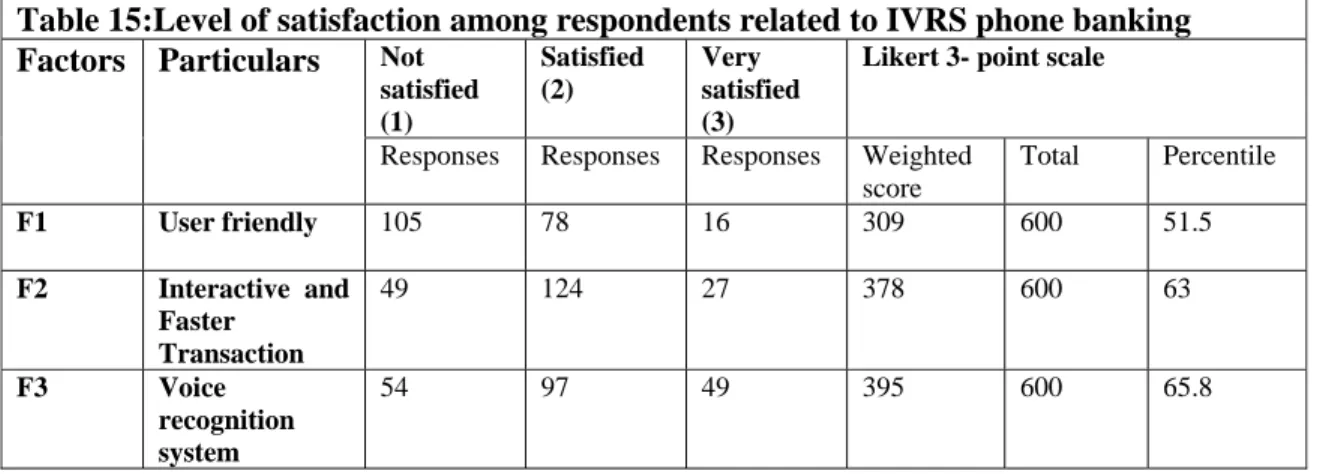

Table 15:Level of satisfaction among respondents related to IVRS phone banking Factors Particulars Not

satisfied (1)

Satisfied (2)

Very satisfied (3)

Likert 3- point scale

Responses Responses Responses Weighted score

Total Percentile

F1 User friendly 105 78 16 309 600 51.5

F2 Interactive and Faster

Transaction

49 124 27 378 600 63

F3 Voice recognition system

54 97 49 395 600 65.8

Table 15 showsthe level of satisfaction among respondents related to IVRS phone-banking. The customer level of satisfaction with IVRS phone banking services was analyzed on a 3-Point Scale on the basis of parameter of User friendly, Interactive and faster Transaction and Speech recognition system. 51.5% of the respondents prefer to have IVRS phone banking service because it is user friendly.63% of the respondents find IVRS phone banking to be interactive and handle faster transactions.65.8% of the respondent find IVRS phone banking to be more useful due to its voice recognition system. This concludes that IVRS phone banking provides much functionality, as customers can listen to the history of the last 15 transactions. It has a higher level of confidential phone banking and enables to carry out required bank transactions by means of telephone keys. IVR can be accessed through any kind of touch-tone telephone, including public phone, home phone, hand 353 phone, smart phone, or PC phone. As a result, more groups of users would be able to access the system.

Conclusion

Suggestive measures to make E-banking services more effective in the future:

After the introduction of the IT Act, Public Sector Banks (PSBs) are facing severe technological competition from their counterparts. In the present era, it is not merely an option but a necessity for the public sector banks to adapt IT, for their survival. Following are the measures to make e-banking services more effective in the future:

1. Make the customers aware of e-channels, especially through demo at the counters to clear all doubts about operating these channels and other related problems.

2. Establish computerization in the rural and urban branches. 3. Start e-banking in rural and urban areas.

4. Install IT infrastructure and e-channel at the cheapest rate. This will help to provide customer services at lower rate and hence will help to retain customers in this era of cut throat competition.

5. Arrange training programmes for the employees to make them more efficient in providing services through e-channels.

6. Financial institution management should choose the level of e-banking services provided to various customer segments based on customer needs and the institution’s risk- assessment considerations.

7. Monitor e-banking security, usage, and profitability and to measure the success of the institution’s e-banking strategy.

8. Ensure the security and confidentiality of customer information.

Bibliography

Wenninger, J. (March 2000) , “The Emerging Role of Banks in E-Commerce”, Current Issues in Economics and Finance, Vol. 6, No. 3, Federal Reserve Bank of New York.

Avasthi G P M (2000-01), “Information Technology in Banking: Challenges for Regulators”,

Prajnan, Vol. 29, No. 4, pp 3-17.

Goiporia M N (July-September 1987), “Emerging Banking Challenges”, The Journal of the Indian Institute of Bankers.

Kukuddi J and Deene S (2006), “Impact of ATMs on Customer Satisfaction (A case study of SBH in Gulbarga district of Karnataka)”, Strategies for winning organization, Ed. By Upender Dhar, Dhar S and Chauhan V.S. , Excel Books, New Delhi, pp.509-15

Srivastava C (2006), “Customer Relationship management: A key Success Factor in

Organizations, Ed. By Upender Dhar, Dhar S and Chauhan V.S., Excel Books, New Delhi, pp.481-90.

Pai D T (March 2001), “Indian Banking-Changing Scenario”, IBA Bulletin, Vol.2 No. 3, pp 20-24.

Pipreya B K (2006), “Internet banking”, The Indian Banker, Vol.23, No.3 (March), pp 20-24.

Uppal R K (2006), Indian Banking Industry and Information Technology, New Century Publication, New Delhi.

Verma D (2000), “Banking on change”, ICFAI Reader, (May), P.No.69.

Mohan R (October 2003), “Transforming Indian Banking: In Search of a better Tomorrow”,

IBA Bulletin, Vol. 22, No. 10.

Annexure

Questionnaire

Name:

Address:

Contact Number:

Q 1. Age wise classification of respondents

A. Less than 26 years

Q 2. Educational Qualification of respondents

A. Under Graduate B. Graduate C. Post Graduate D. Others

Q3. Nature of employment of respondents

A. Unemployed B. Self Employed C. Govt. Service D. Private Service

Q 4. Monthly income of the respondents

A. < 5000 B. 5000-10000 C. 10000-15000 D. >15000

Q 5. Type of relationship with bank

A. Savings a/c B. Salary a/c C. Current a/c D. Demat a/c

Q 6. Time period associated with the bank

A. < 1yr B. 1 – 3yr C. 3 – 5yr D. >5yr

Q 7. Preference of e-banking to manual banking

A. Internet Banking B. ATM Banking C. IVRS phone Banking D. Manual Banking

Q 8. ATM service usage

Q 9. Transaction time at ATM

A. Less than 1 Minute B. 1-3 Minutes C. 3-5 Minutes

D. More than 5 Minutes

Q 10. Awareness of all ATM Locations of the bank in Jaipur-Bikaner region

A. Yes B. No

Q 11. Preferred location of ATM usage

A. Near to home B. Near to office C. At your branch D. Any where in the city

Q 12. Level of Satisfaction with ATM service

Not Satisfied Satisfied Very Satisfied Easy accessibility

Convenience Variety of Transactions

Q 13. Access Internet Banking

A. Regularly B. Once in a Week C. Once in a Month D. Never

Q 14. Preferred place to access Internet Banking

A. At Cyber Café B. At Home C. At Office

D. With Mobile Phone

Q 15. Level of satisfaction related to Internet banking

Not Satisfied Satisfied Very Satisfied Internet Banking Services

Page Setup Ease use Speed Loading

Visual design

Q 16. Customers using IVRS Phone banking

A. Regularly B. Once in a Week C. Once in a Month D. Never

Q 17. IVRS Phone banking Replying

A. Not Effective B. Effective C. Very Effective

Q 18. Level of satisfaction on IVRS Phone banking

Not Satisfied Satisfied Very Satisfied User- friendliness