Regulated Microfinance in Bangladesh- Prosper and Challenges

Full text

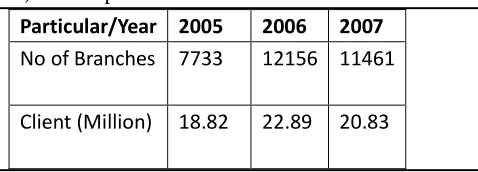

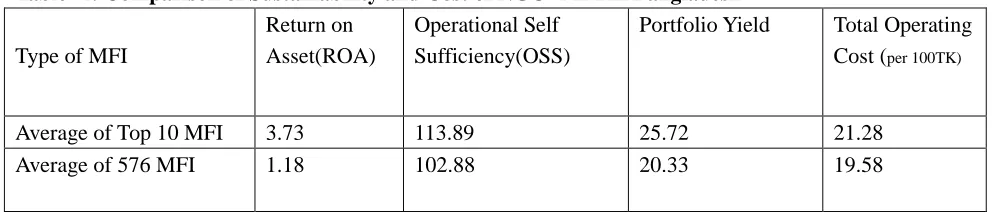

Figure

Related documents

National Conference on Technical Vocational Education, Training and Skills Development: A Roadmap for Empowerment (Dec. 2008): Ministry of Human Resource Development, Department

Currently, National Instruments leads the 5G Test & Measurement market, being “responsible for making the hardware and software for testing and measuring … 5G, … carrier

innovation in payment systems, in particular the infrastructure used to operate payment systems, in the interests of service-users 3.. to ensure that payment systems

The corona radiata consists of one or more layers of follicular cells that surround the zona pellucida, the polar body, and the secondary oocyte.. The corona radiata is dispersed

Petrescu-Mag Ioan Valentin: Bioflux, Cluj-Napoca (Romania) Petrescu Dacinia Crina: UBB Cluj, Cluj-Napoca (Romania) Sima Rodica Maria: USAMV Cluj, Cluj-Napoca (Romania)

The empirical results show that the actual manufacturing enterprise income tax rate is not only affected by national macroeconomic policies and regional economic development,

The projected gains over the years 2000 to 2040 in life and active life expectancies, and expected years of dependency at age 65for males and females, for alternatives I, II, and

expanding host range of DMV, testified by the present report and by numerous cases of DMV infection reported in the last 5 years in the Mediterranean Sea ( Mazzariol et al., 2013,