Inside

Meet the Former Millionaire What Makes a Former Millionaire Finding the “Comeback Millionaires” Actions to Consider 3 4 5 6

The Comeback Millionaire

Summary of findings

The recent financial crisis decimated the wealth of some U.S. millionaires with a swift and brutal decline in the value of virtually all assets. According to Phoenix Marketing International, the recession reduced the number of U.S. households with at least $1 million in investable assets by 14% between the heyday of the market in June 2007 and June 2009.1 But just as quickly as the recession stole away wealth, the subsequent recovery will likely bring prosperity once again to many of these households. The 2009 Fidelity Millionaire OutlookSM study examines one of

the outcomes of the recent recession — former millionaires. The findings reveal that the youngest among former millionaires are poised to rejoin the ranks of millionaires. In addition to having age on their side, younger former millionaires are far more optimistic and willing to take risks than older former millionaires are. You will see this younger group prowling for opportunities ahead, investing more aggressively than other former

millionaires, and taking full advantage of a strengthening economy. Building a close relationship with these “comeback millionaires” can be a profitable endeavor for advisors.

The Fidelity Millionaire OutlookSM Series March 2010

BusIness-BuIldIng InsIght from fIdelIty Investments

This report profiles investors whose liquid assets have fallen below $1 million and identifies who among that group may be most likely to regain millionaire status after the economic recovery.

In the following pages, you will:

• Understand:what sets former millionaires apart — beyond a difference in investable assets

• Identify:the former millionaires who are likely to regain their wealth in the recovery

2

IdentIfyIng the ComeBaCk mIllIonaIre

Although the recession decreased the net worth of most millionaires, not all millionaires were affected equally. This report provides advisors with insight into investors whose assets fell below the $1 million mark during the recent crisis and identifies those who are poised to regain their millionaire status during the subsequent recovery.

aBout the Fidelity Millionaire outlooksm survey

Fidelity Investments (Fidelity) conducts surveys of U.S. households with investable assets of at least $1 million, excluding workplace retirement accounts and any real estate holdings. The research analyzes millionaires’ attitudes and behaviors on a variety of investing topics, including financial concerns, economic outlook, and use of financial advisors. This research brief is based on a survey which was conducted online in February 2009 by Richard Day Research and received completed responses from 1,012 financial decision-makers in U.S. millionaire households and 1,185 financial decision-makers in U.S. mass-affluent households — with investable assets

between $250,000 and less than $1 million. Among the latter group, 292 completed responses were from financial decision-makers in households with investable assets of at least $1 million before the recent financial crisis. The data are representative of all U.S. millionaire households and mass-affluent households, with a margin of error of +/- 3%. The survey did not identify Fidelity as the sponsor. Richard Day Research is an independent third-party research firm not affiliated with Fidelity Investments.

about millionaires

more mIllIonaIres use fIdelIty Investments than any other fInanCIal provIder In the unIted states

According to the Fidelity Millionaire Outlook survey, Fidelity is the No. 1 financial provider for U.S. millionaire households, with the highest penetration among them: 37% of households with at least $1 million in investable assets have at least one account with Fidelity.

Fidelity Investments Bank of America/U.S. Trust/Merrill Lynch Vanguard Wells Fargo/Wachovia/Calibre/A.G.Edwards Charles Schwab Citi Smith Barney TD AMERITRADE JPMorgan Chase/Washington Mutual/Bear Stearns T. Rowe Price E*TRADE FInAnCIAL InG TIAA-CREF UBS Morgan Stanley Ameriprise

Source: Fidelity Millionaire Outlook, February 2009

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 1.0 1.2 1.4 1.6 1.8 2.0 0% 20% 40% 60% 80% 100% 0% 5% 10% 15% 20% 25% 30% 35% 40% 37% 28% 27% 27% 20% 14% 13% 13% 11% 11% 10% 7% 7% 6% 6% 87% 80% 83% 79% 79% 74% 71% 54% 48% 44% 35% 26%

3 meet the former mIllIonaIre

The recent recession reduced the number of U.S. millionaire households from 5.97 million in June 2007 to 5.14 million by mid-2009, according to Phoenix Marketing International. Many of those households simply had less wealth to start with. Still, the Fidelity research reveals that, compared with investors who held onto their millionaire status during the crisis, former millionaires share unique characteristics. These investors:

• Were younger and less experienced. At an average age of 56, former millionaires are younger than millionaires who retained that status through the crisis (age 59, on average). Given that, former millionaires are more likely to still be in the workforce (only 41% are retired, compared to 55% of those who retained their millionaire status). Their slightly younger age could be one reason why eight out of 10 former millionaires say the recent recession is the worst crisis they have experienced, compared to 77% of investors who retained their millionaire status. • Were hit harder by the crisis. Investors who entered the recession with fewer millions lost a larger proportion

of their wealth compared to those who remained millionaires throughout the crisis (see Figure 1). Former millionaires saw their wealth decline from an average $1.85 million in investable assets to $758,000. Those who maintained millionaire status throughout the recession saw their average investable assets fall from $4 million to $3.2 million. At the same time, former millionaires could not build back their wealth as quickly as their peers who remained millionaires. Former millionaires earn an annual household income of $185,000, on average, compared to $307,000 for all millionaires.

• Felt more stress, anger. Former millionaires’ asset losses led to a psychological toll. Compared with those who remained millionaires, former millionaires were more likely to feel ongoing stress specifically due to the financial crisis (49% versus 40%). In addition, almost three in 10 former millionaires admit they felt angry at themselves (27%) due to their financial performance during the crisis, compared with just over one in 10 (15%) of those who remained millionaires. Moreover, 10% of former millionaires admitted to feeling desperate during the crisis, compared to just 5% of those who remained millionaires.

figure 1: former millionaires lost a higher proportion of their assets than those who retained that status.

Source: Fidelity Millionaire Outlook, February 2009

0% 5% 10% 15% 20% 25% 30% 35% 40% 37% 28% 27% 27% 20% 14% 13% 13% 11% 11% 10% 7% 7% 6% 6% –70% –60% –50% –40% –30% –20% –10% 0% –59% –21% 30% 40% 50% 60% 0% 2% 4% 6% 8% 10% 12% 11% 3% 2% 9% 3% 5% 1% 10% 52% 42% 46% 36% 30% 23% Former Millionaires Maintained Millionaire Status

4

What makes a former mIllIonaIre?

What are some of the reasons former millionaires lost their millionaire status? Their portfolios may have been less likely to include the safety of fixed-income investments. Many shell-shocked former millionaires are now cautious and reluctant to make more aggressive investments needed to capture the potential gains from a recovery. Former millionaires surveyed:

• Hold less of a safety cushion. While most former millionaires have investments in fixed-income securities, they are still 12% less likely than those who remained millionaires to invest in fixed-income instruments (75% versus 85%). That may have deprived many former millionaires of a safety net for their portfolios when more volatile asset prices collapsed.

• Are now more uncertain investors. Former millionaires are less likely than those who remained millionaires through the crisis to plan on investing in key asset classes, such as stocks and annuities. Why? Almost 20% say they feel paralyzed when it comes to making financial decisions, compared to 13% of investors who retained their millionaire status. Almost four in 10 (36%) admit they don’t know where to invest. That paralysis may mean that some former millionaires aren’t putting money into asset classes that would benefit from the economic recovery.

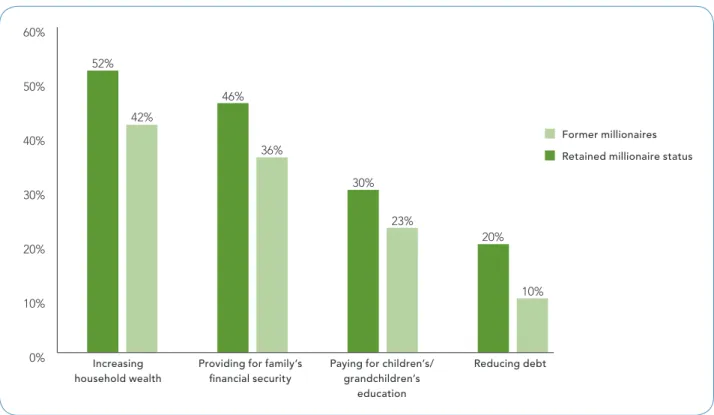

• Are anxious to regain lost ground. Increasing household wealth tops the list of several areas of concern former millionaires feel more acutely than their counterparts who retained their millionaire status (see Figure 2). Most former millionaires (55%) say their primary investment objective is to grow, as opposed to preserve, wealth; less than half (46%) of those who remain millionaires seek wealth accumulation.

figure 2: former millionaires are more likely to share pressing financial concerns.

Source: Fidelity Millionaire Outlook, February 2009

0% 5% 10% 15% 20% 25% 30% 35% 40% 37% 28% 27% 27% 20% 14% 13% 13% 11% 11% 10% 7% 7% 6% 6% –70% –60% –50% –40% –30% –20% –10% 0% –59% –21% 0% 10% 20% 30% 40% 50% 60% 0% 2% 4% 6% 8% 10% 12% 11% 3% 2% 9% 3% 5% 1% 10% 52% 42% 46% 36% 30% 23% 20% 10% Increasing household wealth

providing for family’s financial security

paying for children’s/ grandchildren’s

education

reducing debt

former millionaires retained millionaire status

5 fIndIng the “ComeBaCk mIllIonaIres”

The economic recovery may likely help many former millionaires regain their old status as the value of their assets rise. But a market recovery won’t push all former millionaires back to the $1 million mark. The Fidelity survey reveals that the youngest former millionaires share the highest likelihood of regaining their millionaire status. According to the research, former millionaires up to age 51 — representing one-third of all former millionaires—are far more likely than those above this age group to become millionaires again. Former millionaires age 51 or younger:

• See more opportunity ahead. Almost half (46%) experienced a sense of opportunity due to the financial crisis, compared with only 17% of the older former millionaire group. A majority of the younger group (54%) were actively looking for new investments during the recession, compared to 42% of older former millionaires. Why? The younger group is more optimistic and more likely to see the economy improving.

• Plan to invest more aggressively. Sensing an economic recovery, younger former millionaires plan on making more aggressive investments in almost all asset classes than their older counterparts. For instance, 30% plan to increase their stock holdings this year, compared to only 12% of the older former millionaire group. And younger former millionaires are far more likely to make new investments in multiple riskier asset classes (see Figure 3). Because these investments are riskier, they may or may not help lift these investors back to millionaire status even if the economy improves.

figure 3: the youngest former millionaires plan for aggressive new investments this year.

Source: Fidelity Millionaire Outlook, February 2009

• Share distinct financial concerns. Given their age and need to juggle multiple priorities, younger former millionaires have more pressing financial concerns than older former millionaires do. Most (53%) younger former millionaires worry about supporting their current lifestyle (compared to 45% of older former millionaires), and almost three-quarters (73%) fret about their ability to support their retirement (versus 61% of older former millionaires). In addition, the younger former millionaires are more concerned than their older counterparts are about increasing their wealth, paying for college, and reducing debt. 0% 5% 10% 15% 20% 25% 30% 35% 40% 37% 28% 27% 27% 20% 14% 13% 13% 11% 11% 10% 7% 7% 6% 6% –70% –60% –50% –40% –30% –20% –10% 0% –59% –21% 0% 10% 20% 30% 40% 50% 60% 0% 2% 4% 6% 8% 10% 12% 11% 3% 2% 9% 3% 5% 1% 10% 52% 42% 46% 36% 30% 23% 20% 10% derivatives alternate Investments real estate hedge funds 51 or younger 52 or older

6

aCtIons to ConsIder

Advisors looking to help former millionaires take advantage of the recovery may want to:

• Lower your minimums. While former millionaires may not be the sweet spot for an advisor focused on the most affluent clients, spending extra attention on them can pay off in the future. Tap your current client roster or lead generator to scope out possible referrals or prospects who were hit particularly hard by the recession. Consider lowering your minimum asset requirements to accommodate these post-crisis less-affluent prospects, regardless of their age. Look to competitors’ clients who, due to asset erosion, may have been “demoted” to less than a premier service; offer them the same top-flight attention to which they have grown accustomed. The economic recovery may bring many of these former millionaires back to that status, and your business can grow accordingly. Working diligently now to help these former millionaires means you will most likely remain a vital and valued partner when they once again cross the millionaire threshold.

• Broaden your investment offerings. To match younger prospects’ zeal for untapped opportunities, bring them a variety of investment options that they may not have previously considered—for instance, ETFs that focus on specific sectors of emerging markets, or even help them make direct investments in those countries’ equity markets. Consider introducing them to more exotic investment strategies like options contracts, structured products, or limited investment partnerships. Help them create an income strategy through exposure to higher-yielding municipal and corporate bonds in their fixed-income portfolios. However, make sure they are aware that while these strategies or asset classes can play a role in a broadly diversified portfolio, they carry considerable risk of loss even if the economy continues to improve.

• Help younger clients address long-term financial concerns. You may want to consider showing younger clients that establishing college savings and retirement accounts are tax-efficient investment strategies for the long term—not just another form of savings. Help them model future retirement income scenarios for their desired lifestyle, and adjust their investment strategy to help them reach that goal. Consider suggesting that they take advantage of 2010’s lifting of income caps on Roth IRA conversions.2 Why? Tax rates will likely be higher when they retire; they will welcome the tax-free withdrawals from a Roth IRA account and the ability to pass on untapped Roth IRA accounts to their heirs.

• Introduce older former millionaires to income-focused investment strategies. These former millionaires may feel they don’t have the luxury of time to grow their assets with more aggressive investments. Instead, they will welcome help balancing their current assets with lifestyle demands and income plans for their retirement years. For many, a bond-laddering strategy could help maintain the value of their portfolio while creating a regular income stream and giving them some protection from future interest-rate hikes. But remind them that even with a shorter investment time horizon, diversification should be kept in mind to help smooth volatility in the value of their portfolio. They would also likely welcome a long-term strategy to liquidate their accounts in the most tax-efficient way.

for more information, please contact your fidelity sales or relationship manager.

1Phoenix Marketing International, “Phoenix AMS Market Sizing Report”, June 2009, page 9.

2A distribution from a Roth IRA is tax-free and penalty-free provided that the five-year aging requirement has been satisfied and one of the

following conditions is met: age 59½, death, disability, qualified first time home purchase.

For Investment Professional use only. not for distribution to the public as sales material in any form.

The content provided in this white paper is general in nature and is for informational purposes only. This information is not individualized, and is not intended to serve as the primary or sole basis for your decisions as there may be other factors you should consider. Fidelity Investments is providing this white paper as a service to your firm and is not responsible for your action or inaction as a result of this service.

The estate planning and tax information herein is general in nature and should not be considered legal or tax advice. An attorney or tax professional should be consulted regarding any specific legal or tax situation. Fidelity Investments does not provide estate or tax advice. Fidelity Investments cannot guarantee that such information is accurate, complete, or timely. Laws of a particular state, or laws which may be applicable to a particular situation, may have an impact on the applicability, accuracy, or completeness of the information contained in this white paper.

Fixed-income investments entail interest rate risk (as interest rates rise, bond prices usually fall), the risk of issuer default, issuer credit risk, and inflation risk.

Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

Diversification does not ensure a profit or guarantee against a loss.

Foreign investments may involve greater risk than U.S. investments, including political and economic risks and the risk of currency fluctuations. Exchange-traded funds are subject to risks similar to those of stocks and will fluctuate in response to the activities of individual companies and general market and economic conditions domestically and abroad. When redeemed, you may gain or lose money.

A bond ladder, depending on the types and amount of securities within the ladder, may not ensure adequate diversification of your investment portfolio. This potential lack of diversification may result in heightened volatility of the value of your portfolio. You must perform your own evaluation of whether a bond ladder and the securities held within it are consistent with your investment objective, risk tolerance, and financial circumstances.

Fidelity Family Office Services is a division of Fidelity Brokerage Services LLC. Fidelity Family Office Services, 155 Seaport Boulevard, Boston, MA 02210

Fidelity Institutional Wealth Services, 200 Seaport Boulevard, Z2B1, Boston, MA 02210 national Financial Services LLC, 200 Seaport Boulevard, Z2P, Boston, MA 02210

Fidelity Institutional Wealth Services provides brokerage products and services and is a division of Fidelity Brokerage Services LLC. national Financial is a division of national Financial Services LLC through which clearing, custody, and other brokerage services may be provided. Both members nYSE, SIPC.