MYHAMMER HOLDING AG

GERMANY /

INTERNET SERVICES

PRICE TARGET: €3.00 PREVIOUS CLOSE: €2.70 RETURN POTENTIAL: 11.1%F

IRST

B

ERLIN

Equity Research

ADD

INITIATING COVERAGE

7 SEPTEMBER 20107 September 2010 MyHammer Holding AG

F

IRSTB

ERLIN Equity Research CONTENTS PAGE MYR – Overview... 1 Investment Case ... 2 SWOT Analysis... 3 Risk Analysis ... 4Recent Results & Outlook... 5

Business Description ... 8

Management...11

Market Analysis...12

Income Statement Analysis...13

Balance Sheet Analysis...14

Cash Flow Analysis...15

7 September 2010 MyHammer Holding AG

F

IRSTB

ERLIN Equity Research MYR – OVERVIEW 7 September 2010 RATING: Add PRICE TARGET: €3.00 RETURN POTENTIAL: 11.1%RISK RATING: High

MYHAMMER HOLDING AG

GERMANY / INTERNET SERVICES Frankfurt Stock Exchange

Bloomberg symbol: MYR GR ISIN: DE0005680300

COMPANY PROFILE

MyHammer Holding AG (formerly Abacho AG) operates a handyman internet search portal through its subsidiary MY-HAMMER AG, in which it owns a 68.8% stake. MyHammer is market leader in Germany and Austria. In H1/10, it accounted for 98.9% of group sales. MyHammer Holding AG is based in Berlin and had 61 employees at the end of June 2010. TRADING DATA Closing price (06.09.10) €2.70 Shares outstanding 15.49m Market capitalization €41.82m 52-week range €1.97 / 3.58

Average volume (12 months) 17,984

STOCK OVERVIEW 0 0.5 1 1.5 2 2.5 3 3.5 4

Jan-09 Apr-09 Jul-09 Oct-09 Jan-10 Apr-10 Jul-10

0 200 400 600 800 1000 1200 MyHammer NMDP Index

COMPANY DATA (as of 30 June 2010)

Liquid assets €3.08m Current assets €4.49m Intangible assets €1.38m Total assets €9.40m Current liabilities €3.66m Consolidated equity €5.74m SHAREHOLDERS INITIATING COVERAGE

MyHammer’s handyman internet search portal, MyHammer, not only makes it easier for customers to find the right handymen. It also increases the overall quality of the client experience by allowing them to view tradesmen’s performance ratings and qualifications. Dynamic sales growth over the last two years and market share gains attest to the viability of the MyHammer concept. MyHammer’s penetration of its market remains low. Long-term growth potential is high. We initiate coverage with a DCF-based price target of €3.00 and Add rating.

How does MyHammer work? The MyHammer internet portal puts handymen in contact with their customers. Customers describe their job on the MyHammer website and receive quotes from rated and experienced handymen or directly pick their handyman from the MyHammer Directory. MyHammer currently has two main sources of revenue. The company bills handymen for a percentage of each job they receive through MyHammer. It also generates revenues from subscriptions to the MyHammer Partner scheme, which allows tradesmen to market themselves more effectively on the MyHammer website.

Rapid growth In H1/10, MyHammer revenues increased by 94.3% y-o-y to €7.6m (H1/09: €3.9m), helped in large measure by strong sales of the MyHammer Partner scheme. Other metrics also developed favourably. The number of registered users rose to 1.3m (31 Dec 2009: 1.2m), of which 250k were tradesmen (31 Dec 2009: 230k). The operating loss was reduced to €1.8m (H1/09: €2.1m) and net loss to €1.3m (€1.7m) mainly due to a much lower share of personnel expenses (33.9% vs 51.6% in H1/09) and CoGS (19.9% vs 25.7%). CoGS comprise costs of online marketing.

Successful internationalisation MyHammer expanded to Austria in 2006 and the UK in 2008. In Austria, it has attained market leadership. Sales outside Germany are expected to account for 10-20% of total sales in 2010. This figure is expected to rise well over 20% in the medium term as the company enters other markets. In Juli 2010, MyHammer announced that it is going to expand its business into the US from Q4/10.

FINANCIAL HISTORY & PROJECTIONS

2008 2009 2010 2011 2012 2013 Revenue (€m) 5.54 10.48 16.36 27.15 35.69 46.78 Y-o-y growth na 89.2% 56.1% 66.0% 31.5% 31.1% EBITDA (€m) -4.74 -2.39 -0.97 2.05 4.05 5.73 EBITDA margin -85.6% -22.8% -6.0% 7.5% 11.4% 12.3% EBIT (€m) -4.96 -2.69 -1.31 1.63 3.53 5.10 EBIT margin -89.6% -25.7% -8.0% 6.0% 9.9% 10.9% Net income (€m) -3.61 -1.80 -0.53 1.13 2.47 3.63 EPS (diluted) (€) -0.24 -0.12 -0.03 0.07 0.16 0.23 P/E (x) na na na 37.0 17.0 11.5 DPS (€) 0.00 0.00 0.00 0.00 0.00 0.00 Yield 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% FCF (€m) -3.94 -0.50 -1.23 0.90 3.27 4.79 Net gearing -42.7% -44.9% -25.7% -50.5% -99.5% -134.9% Liquid assets (€m) 4.53 1.74 0.82 1.76 5.04 9.83 Holtzbrinck Networks GmbH 55.0 %

European Founders Fund 2.9 %

Free float 42.1 %

7 September 2010 MyHammer Holding AG

INVESTMENT CASE

MARKET LEADERSHIP IN GERMANY AND AUSTRIA

With over 15.2m page impressions, 2.4m visits (Source for both: IVW, June 2010) and currently 1.3m registered users according to the company, MyHammer is the number one online search portal for tradesmen and other service providers in Germany and Austria. In the UK, MyHammer.com has recently overtaken its biggest competitor MyBuilder.com in the number of posted jobs.

MYHAMMER HAS HIGH POTENTIAL

The MyHammer business model has high potential in our view. At the end of June 2010, the number of registered tradesmen was 250k. This compares with 970k handyman companies in Germany alone. So, there is plenty of scope for MyHammer to increase penetration of its domestic market and – in due consideration of the announced expansion strategy – international markets. As MyHammer’s business model has a high degree of operating leverage, we expect high double digit annual sales growth to push the EBIT margin into positive territory in 2011 (subject to further investments in the aforementioned internationalisation) and into the 10-15% range in the medium-term. In August 2010, the company introduced an iPhone application which will also make the MyHammer portal available on smartphones and thus increase its competitive advantage.

POSITIVE CASH FLOW FROM 2011?

At the end of June 2010, MyHammer’s equity ratio was 61%. The company’s net cash position amounted to €2.8m. In June, the company completed a share issue (737.6k new shares at a price of €2.50 per share). We forecast a cash outflow of €1.2m for the current year - investment activity this year is likely to focus on further improvements of the MyHammer portal and marketing of the MyHammer Partner scheme (generates higher sales and margins) - implying that MyHammer is well financed into 2011, when we expect cash flow to turn positive.

MANAGEMENT HAVE STRONG SECTOR EXPERTISE

MyHammer’s management have long experience in the internet and technology sector. For example, the CEO Markus Berger-de Leon was previously CEO of VZ Netzwerke, which operates one of the most popular German social community sites, StudiVZ, and also of Jamba!, a provider of mobile content. Management are supported by the main shareholders Holtzbrinck Networks (55%) and European Founders Fund (2.9%), who have already conducted several investments in internet companies e.g. Experteer GmbH (online job listing service), Zalando GmbH (online shop for shoes), Nasza-Klasa Sp. z.o.o (Polish social community site).

VALUATION MODEL SUGGESTS UPSIDE OF 11.1% AT PRESENT

We have based our valuation of MyHammer on discounted cash flow analysis. Our valuation does not take the peer group into account as in our view there is no publicly traded company comparable to MyHammer in terms of products and size. Our DCF model generates a fair value for the stock of €3.00. Although we see high long-term potential for the company, we have been conservative with our valuation as MyHammer has not yet reached profitability.

7 September 2010 MyHammer Holding AG

SWOT ANALYSIS

S

TRENGTHS• MyHammer is the market leader in the area of handyman search portals in Germany and

Austria. According to a study by Innofact from May 2010, it is twice as well known in Germany as all of its competitors put together. Moreover, the portal is the second most popular trade directory in Germany after Gelbeseiten.de

• According to Fraunhofer Institute, MyHammer is very helpful for handymen when it comes

to gaining new orders and expanding the business

• Strategic partnership with the second biggest do-it-yourself store in Germany, Praktiker,

which advertises the MyHammer portal to its customers

• In August 2010, MyHammer introduced a mobile application which makes the MyHammer

portal also available on the iPhone

• Established real-time reporting and performance measurement system

• Net cash position of €2.8m at the end of June 2010

• Management/shareholders have extensive experience in the internet and technology sector

W

EAKNESSES

• MyHammer has not yet reached profitability

• MyHammer only owns 68.8% of the shares in MY-HAMMMER AG, which operates the

MyHammer portal

• According to management, MyHammer has not been able to collect c. 30% of its

receivables so far. In H1/10, receivables losses and write-downs amounted to €3.2m

• The success of MyHammer is totally dependent on the MyHammer internet portal

O

PPORTUNITIES• Strengthened focus on the distribution of the MyHammer Partner scheme, which generates

higher revenues and margins

• Better receivables management due to a cooperation with a specialised third party

• Stronger growth of the number of registered users due to investments in marketing,

intensified distribution activity, optimisation of customer service and improvement of the usability of the MyHammer portal

• Expansion to other countries e.g. USA with a high GDP per head and share of owner

occupiers

• Stronger use of social community sites e.g. Facebook in order to stay in touch with

customers

T

HREATS• Highly competitive segment with low technological entry barriers

• Access to external financing may prove problematic while the company remains lossmaking

7 September 2010 MyHammer Holding AG

VALUATION

DISCOUNTED CASH FLOW MODEL

In order to determine MyHammer’s Weighted Average Cost of Capital (WACC), we use our proprietary multi-factor risk model, which takes company-specific risk factors into account, such as management strength, balance sheet and financial risk, competitive position and company size. We assign a High risk rating to the company.

Our WACC calculation of 12.4% is based on a risk-free rate of 2.2%, a market risk premium of 4% and an effective tax rate of 30%. In our DCF model, we use a planning period until 2020 and a terminal sales growth rate of 2%.

In our DCF model, we account for 612.2k options in total. These were granted to employees of MyHammer Holding AG and MY-HAMMMER AG in November 2008 (509k with an exercise price of €1.18) and June 2009 (103.3k with an exercise price of €2.26). 306.1k of the options have a two year lock-up period. 153.1k have a three year lock-up period and 153.1k have a four year lock-up period. Each option gives the holder the right to buy a new common share without a nominal value.

Due to the treasury stock method, the number of shares which we use for calculating our DCF-based fair value is 15.8m. According to Bloomberg, MyHammer’s current number of shares outstanding is 15.5m.

DCF Valuation

2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E

Total sales 16,355 27,145 35,686 46,781 58,027 70,472 81,058 92,363 y-o-y change 56% 66% 31% 31% 24% 21% 15% 14% Operating profit -1,308 1,629 3,533 5,099 6,905 9,091 11,267 13,762 operating margin -8% 6% 10% 11% 12% 13% 14% 15% NOPLAT -801 1,629 3,533 5,099 4,834 6,364 7,887 9,633 + depreciation 334 418 518 635 762 893 1,020 1,130

Net operating cash flow -467 2,046 4,051 5,734 5,595 7,257 8,907 10,764

- Total investments -793 -1,161 -831 -1,128 -1,141 -1,290 -1,222 -1,340

Capex -696 -1,001 -882 -1,085 -1,160 -1,362 -1,373 -1,548

Working capital -97 -160 51 -42 18 73 151 209

Free cash flows -1,260 886 3,221 4,606 4,454 5,967 7,684 9,424

PV of FCF -1,189 743 2,405 3,061 2,634 3,139 3,597 3,925

All figures in T€

PV of FCFs in explicit period 29,670

PV of FCFs in terminal period 37,479

Enterprise value 67,149

+net cash / -net debt 2,834

Equity value before mins 69,982

Minorities 21,869

Shareholder value 48,113

Number of shares outstanding 15,826

WACC 12.4% 11.3% 12.3% 13.3% 14.3% 15.3% 16.3% 17.3%

cost of equity 12.4% 8.4% 5.67 6.06 6.46 6.85 7.25 7.65 8.04

pre-tax cost of debt 5.0% 9.4% 4.56 4.87 5.18 5.49 5.80 6.11 6.42

normal tax rate 30.2% 10.4% 3.72 3.97 4.22 4.47 4.71 4.96 5.21

after-tax cost of debt 3.5% 11.4% 3.06 3.27 3.47 3.67 3.87 4.08 4.28

share of equity 100.0% 12.4% 2.54 2.71 2.87 3.04 3.21 3.37 3.54

share of debt 0.0% 13.4% 2.11 2.25 2.39 2.53 2.67 2.80 2.94

14.4% 1.76 1.87 1.99 2.11 2.22 2.34 2.45

Fair value per share 3.04 15.4% 1.46 1.56 1.66 1.75 1.85 1.95 2.05

WACC

Terminal-EBIT margin

7 September 2010 MyHammer Holding AG

RISK ANALYSIS

RISKS RELATING TO THE ECONOMY

Weaker consumer spending and construction activity could have a negative impact on the demand for handyman services. In order to limit this risk, MyHammer regularly collects relevant data on its target sectors and evaluates and uses this in its medium-term planning. The company also gathers information from its customers in order to assess the future development of its target sectors.

RISKS RELATING TO FINANCING

A very important factor in the realisation of the company’s growth plans is the timely availability of liquidity. This is being ensured by continuous monitoring of the economic environment and its impact on short-term liquidity. The process of receivables collection is also important in this respect. MyHammer has addressed this issue by changing the standard way of payment from invoice to direct debit and by shortening of payment terms. In addition, the company is now working together with a third-party provider, who is specialised on receivables management. The raising of additional liquidity through the capital markets could be difficult as long as the company keeps generating losses.

RISKS RELATED TO CUSTOMER STRUCTURE

It is difficult to entirely eliminate incidences of fraudulent behaviour on the MyHammer website. Media coverage of such fraud could have a material negative effect on the company’s reputation and business performance. MyHammer prevents fraud by developing and expanding internal security systems. For example, it now requires participating handymen to present documentation verifying their qualifications.

LOSS OF KEY PERSONNEL

The success of MyHammer is highly dependent on the experience and contacts of its key personnel. The loss of a key employee without suitable and timely replacement could adversely affect MyHammer’s business, operations and future growth.

7 September 2010 MyHammer Holding AG

RECENT RESULTS & OUTLOOK

SALES AND EARNINGS

For H1 2010, MyHammer reported sales of €7.6m (94.3% y-o-y). Revenues developed favourably mainly due to high sales of the MyHammer Partner scheme which was introduced in H1/09. However, due to the outsourcing of receivables management, revenue deferral has been changed from monthly to daily calculation causing a reduction in revenues of €296k in H1/10. As competition for advertising budgets in the area of online portals has been high, sales from advertising and barter deals decreased from €242k in H1/09 to €82k in H1/10.

Sales split H1 2010 and H1 2009

in €'000 H1/2010 Share H1/2009 Share

Advertising orders + barter deals 82 1.1% 242 6.1%

Online orders (MyHammer.com) 7,484 98.9% 3,701 93.9%

Total sales 7,566 100.0% 3,943 100.0%

Table 1 Source: MyHammer, First Berlin

In the future, sales will only come from the MyHammer portal as the company plans to give up all operations, which have been (1) not able to compete successfully for advertising budgets due to their low reach and (2) overly much dependent on the economy and the advertising market. In September 2009, MyHammer sold its property in Neuss and in February 2010 its chat business (ChatCity, Chatfun, Chatworld, Chat.at) as well as several domains (two of which for a low six-digit Euro amount each). For 2010, it plans to dispose of other non-core assets including the search engine/portal Abacho.

Sales split 2009-2012E

in €'000 2009 Share 2010E Share 2011E Share 2012E Share

Advertising + barter deals 299 2.9% 150 0.9% 0 0.0% 0 0.0%

Online orders (MyHammer.com) 10,176 97.1% 16,205 99.1% 27,145 100.0% 35,686 100.0%

Total sales 10,475 100.0% 16,355 100.0% 27,145 100.0% 35,686 100.0%

Note: MyHammer is going to concentrate on the operation of its handyman portal from 2010

Table 2 Source: MyHammer, First Berlin EBIT in H1/10 came in at €-1.8m (H1/09: €-2.1m) and net loss at €1.3m (loss of €1.7m). One reason for the improvement in both figures was a much lower share of personnel costs (33.9% vs 51.6% in H1/09). MyHammer’s business model has a high level of operating leverage.

Another reason was a share of CoGS in total sales of 19.9% compared to 25.7% in H1/09. CoGS comprise costs of online marketing.

Receivables losses and write-downs (are part of other operating expenses) increased from €1.2m to €3.2m between H1/09 and H1/10. According to management, MyHammer has not been able to collect c. 30% of its outstanding receivables so far.

7 September 2010 MyHammer Holding AG

We believe MyHammer’s financial results will improve steadily in 2010 and coming years. The main sales drivers will be investments in the MyHammer portal (marketing, optimisation of customer service, improvement of usability etc.) and expansion to other countries (plans are currently focussing on the US). For fiscal year 2012, we expect sales of €35.7m, an EBIT of €3.5m (9.9% margin) and a net profit of €2.5m. Due to tax-loss carry forwards of €25.3m, we do not expect that MyHammer will pay taxes before 2014.

BALANCE SHEET AND CASH FLOW

At the end of June 2010, MyHammer had an equity ratio of 61% and net cash of €2.8m. On 31 December 2009, the company had an equity ratio of 67.1% and net cash of €1.7m.

At the end of June 2010, total financial debt amounted to €247k (31 Dec 2009: €0). In the course of 2009, MyHammer repaid bank debt of €2.5m, relating to a property in Neuss that the company sold in September 2009.

The most important asset positions were other intangible assets (€1.4m), which comprised capitalised software development costs, software rights and domains, cash of €3.1m and deferred tax assets of €3.3m. MyHammer expects that it will be able to generate sufficient profits to utilise its tax-loss carry forwards of €25.3m in the coming years. The other financial assets of €356k comprised a long term receivable as well as a short term liability related to a subsidy from the Federal State of Berlin. The subsidy was granted to the company in October 2009 in order to support the creation of new jobs. It has a volume of up to €1.5m and is valid from June 2008 to June 2011. MyHammer has to create 206 new jobs during this period.

For the fiscal-year 2012, we forecast an equity ratio of 40.9% and net cash of €5.0m. We believe the equity ratio will decrease in the coming years as trade payables (and working capital) are likely to rise significantly in line with the company’s forecast growth. We expect MyHammer’s liquid funds position to be affected by better financial results following an increasing number of registered users of the MyHammer portal and improvements in cost efficiency.

7 September 2010 MyHammer Holding AG

BUSINESS DESCRIPTION

BUSINESS SUMMARY

MyHammer Holding AG (MyHammer) was founded in 1996 as Endemann!! Full Service Werbeagentur GmbH in Neuss. It changed its name to Abacho AG in 1999. Previously, the company operated and marketed an internet search engine, portal and chat services in Germany and other European countries (e.g. Austria, Switzerland, Spain, UK). It also provided advertising as well as market research services. MyHammer is headquartered in Berlin and had 61 employees at the end of June 2010.

MY-HAMMMER AG, in which Abacho owned a 100% stake at the beginning of 2005, of which a 31.3% stake was sold to venture capitalist Holtzbrinck Ventures GmbH in 2006, has developed very successfully. The management of Abacho had decided to focus solely on this business and to dispose of non-core operations. Since 2009, the company has sold its property in Neuss, several domains and its chat business. In June 2010, it changed its name to MyHammer Holding AG. The Abacho search engine/portal will be sold in 2010.

With over 15.2m page impressions, 2.4m visits (Source for both: IVW, June 2010) and currently 1.3m registered users (thereof more than 250k registered tradesmen) according to the company, MyHammer is the number one online search portal for tradesmen and service providers in Germany, Austria and the UK, where it has recently overtaken its competitor MyBuilder.com when it comes to the number of posted jobs. MyHammer has been present in Germany since June 2005, in Austria since August 2006 and in the UK since June 2008.

Company structure

Chart 1 Source: MyHammer, First Berlin

MyHammer Holding currently consists of MY-HAMMMER AG, which operates the internet search portal for handymen, MyHammer, as well as CCC Asset Verwaltungs GmbH, which has no operations anymore. MyHammer Holding currently owns only 68.8% of the shares in MY-HAMMMER AG and thus does not have full control over its most important asset. Other shareholders of MY-HAMMMER AG are the venture capital funds Holtzbrinck Ventures (26.3%) and European Founders Fund (5.0%), which was set up by the German internet entrepreneurs Oliver, Marc and Alexander Samwer. Among other companies, the Samwer brothers founded Jamba!, a provider of mobile content and Alando Deutschland, which later became a subsidiary of eBay Inc. MyHammer Holding AG MY-HAMMER AG, 68.8% CCC Asset Verwaltungs-GmbH, 100% (no operations anymore)

7 September 2010 MyHammer Holding AG

HOW DOES MYHAMMER WORK?

On the MyHammer portal, which has also been available as an iPhone application since August 2010, both private and commercial customers can quickly get quotes from tradesmen, builders and service providers. A diverse range of services are offered including building work, general repairs, renovation, removals, babysitting and teaching. Two search methods are available to customers: (1) customers can post a short job description online and receive multiple quotes from tradesmen and other service providers (2) they can search for specific tradesmen in the MyHammer Directory according to qualifications, area of expertise and locality. The customer can contact the tradesman of his choice by email, phone or through the MyHammer forum. After the tradesman has completed the job, the customer as well as the tradesman can rate each other based on factors such as the quality of work and friendliness. The higher the rating of the handyman, the higher his position will be in the next MyHammer search and the higher the probability that he will be chosen again.

Once a tradesman creates his profile on the MyHammer portal, his qualifications are checked by MyHammer’s service personnel. For example, if a tradesman claims to have a master craftsman certificate, MyHammer will only accept this once he has shown them the relevant documentation. After creating the profile, the tradesman will receive daily emails with jobs, for which he can bid.

WHO ARE THE CUSTOMERS?

Tradesmen, who post their offers on the MyHammer portal, are either self-employed or work for a bigger firm. The MyHammer platform is a very helpful tool when it comes to finding new clients. This is demonstrated by the fact that MyHammer continued to develop strongly during the recession year of 2009.

According to MyHammer’s management, the typical MyHammer customer is 25 to 44 years old, has education to tertiary level and lives with his/her family in a one- or two-family-house. Quality is more important to them than price. 70% of the handymen on the MyHammer portal are mandated because of their high rating, not because they offer the lowest price.

MyHammer has established blogs and websites on the most important social networks such as Facebook and Twitter, which allow the company to stay in touch with its clients and give them the possibility to participate in the development of the MyHammer portal.

7 September 2010 MyHammer Holding AG

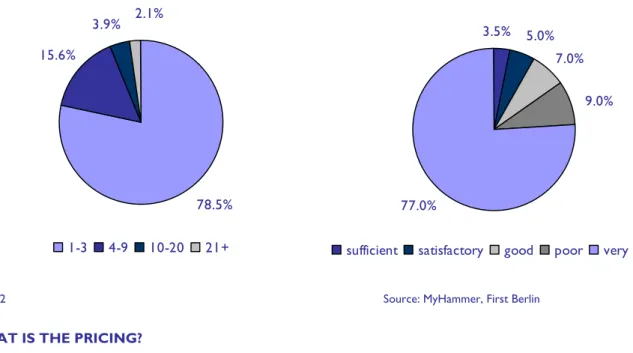

MyHammer’s handymen: number of employees and assessment of work quality

78.5% 15.6% 3.9% 2.1% 1-3 4-9 10-20 21+ 5.0% 77.0% 3.5% 7.0% 9.0%

sufficient satisfactory good poor very good

Chart 2 Source: MyHammer, First Berlin

WHAT IS THE PRICING?

MyHammer only charges tradesmen a fee if they were mandated by a customer for a job. The minimum fee, which is calculated on the basis of the job value, is €5 per job offer + VAT.

Value of the job Fee

less or equal €24,999 4% + VAT

up to €99,999 3% + VAT

more than €99,999 2% + VAT

Table 1 Source: MyHammer, First Berlin

Since August 2010 tradesman have only been allowed to bid on jobs if they order a MyHammer Partner scheme starting at c. €74 + VAT per quarter in Germany and Austria and c. GBP 59 + VAT per quarter in the UK. There are four different MyHammer Partner schemes: 500 (maximum value of a job €500), 1,000, 5,000, 10,000 and Flat (no limit on job value). All include the following features:

(1)Detailed company description with several pictures

(2) Freedom to quote on all jobs (3) Sending contact details for free

(4) Free access to the MyHammer Directory (5) Upload of documents allowed

(6) Direct communication with customers for free (7) Top placement in search engines such as Google

In February 2009, MyHammer introduced the MyHammer Directory. According to the company, the directory is already the second most popular in Germany after Gelbeseiten.de.

7 September 2010 MyHammer Holding AG

HOW IS MYHAMMER MANAGED?

In order to make the administration of the MyHammer website and service more efficient, MyHammer has outsourced some key tasks. The first level customer service, accounts receivable management, distribution and parts of IT operations are now managed by specialised third-party providers. Thus, MyHammer is able to concentrate on the further strategic development of the MyHammer portal.

We welcome the fact that key aspects of the operation of the MyHammer portal have been outsourced. We believe this is especially positive with regard to receivables management which is a major issue at MyHammer. According to management, the company has been able to collect only 70% of its outstanding receivables. Due to a cooperation with a specialised third-party provider, we expect this figure to improve significantly in the coming years, which should have a positive effect on the company’s financial results.

MANAGEMENT

Markus Berger-de Leon has been CEO of MyHammer Holding AG since January 2008. In

March 2009, he was appointed Head of the Supervisory Board of MY-HAMMMER AG and became CEO of VZ Netzwerke (operates StudiVZ, a very popular social community site in Germany), where he staid until February 2010. Between December 2005 and December 2007, he was also CEO of Jamba! / Jamster (a provider of mobile content). Mr Berger-de Leon studied Business Administration at the WHU Koblenz and the Columbia Business School.

Oliver Beyer has been a member of MyHammer’s management board since March 2009. In this

role, he is in charge of legal issues, human resources, investor relations as well as government relations. Between October 2008 and February 2009, he was Director Legal & HR of Abacho AG and from April 2002 to October 2008 the company’s Legal Counsel. Mr Beyer studied Law and Law Informatics at the University of Münster and Saarbrücken.

Gerrit Müller has been CEO of MY-HAMMMER AG since February 2009. In July 2010, he has

taken over the new internationalisation department of MyHammer Holding AG and became COO of the company. Prior to joining MY-HAMMER AG, he was Senior Director Product at Yahoo! from December 2007. Before this, he was Key Account Manager at Packard Bell Germany and Senior Product Manager at eBay Germany. Mr Müller studied at the Technical University in Berlin, where he received an engineer’s degree with a specialisation in Logistics, and at the University of California/Berkeley.

Jan Seidler has been the Chief Technology Officer (CTO) of MY-HAMMMER AG since June

2008. Prior to that, he spent four years in the Product Strategy & Innovation department at eBay in Berlin and San Jose. Earlier, he founded and managed the IT company Section 8 GmbH in Frankfurt, where he worked between July 1995 and October 2002. Mr Seidler has a degree in Business Administration and Informatics from the University of Frankfurt. He also studied at the faculty of arts & sciences of the Harvard University.

7 September 2010 MyHammer Holding AG

MARKET ANALYSIS

THE E-COMMERCE MARKET

According to market research firm TNS Infratest, sales of the global E-Commerce sector in 2008 amounted to €7.4tr, corresponding to y-o-y growth of 33%. The Business-to-Customer (B2C) segment of the E-Commerce sector generated 2008 sales of €760bn, equivalent to c. 10% of the total E-Commerce market.

In 2008, Germany accounted for E-Commerce sales of €637bn. With a market share of 31%, it was number one in Europe. Worldwide, it had a market share of 8.6% and the highest per capita E-Commerce sales (€913 compared to a global average of €113). For 2010, TNS Infratest expects Germany to generate E-Commerce sales of €816bn, +28.1% compared to 2008.

With regard to B2C E-Commerce, Germany had a worldwide market share of 10% and a Europe-wide share of 31% in 2008. For 2010, TNS Infratest expects Germany to increase its B2C E-Commerce sales by c. 100% to €145bn.

TNS Infratest has identified the following factors as important in the growth of the E-Commerce market: (1) E-Commerce allows for higher price transparency and lower distribution costs (2) today’s customers have higher price sensitivity (3) E-Commerce makes customer participation in the development and design of the products and services possible (“Social Shopping”).

COMPETITION

There are some websites on the internet, which offer a similar service to MyHammer. However, blauarbeit.de, jobdoo.de, myBuilder.com and Quotatis.de are the only ones, which on the basis of their market shares can be regarded as the company’s direct competitors. MyBuilder.com was until recently the market leader in the segment in the UK.

Blauarbeit.de, jobdoo.de and Quotatis.de have different pricing models than MyHammer. For example, Blauarbeit.de has a package model, which means that it does not charge the tradesman a fee for his job mandate. On the other hand, Quotatis.de aims at attracting mainly big job mandates as it tries to establish itself as a premium provider.

No competitor in the US e.g. ServiceMagic offers a similar pricing model as MyHammer. Most charge a fixed fee for every job which is suggested to a handyman. As in addition internet penetration and home ownership rates are very high in the US (75.2% and 68.0% respectively), MyHammer sees a big potential for its business there.

7 September 2010 MyHammer Holding AG

INCOME STATEMENT ANALYSIS

All figures in T€ 2008 2009 2010E 2011E 2012E 2013E

Revenues 5,536 10,475 16,355 27,145 35,686 46,781

Other operating income 1,136 666 991 1,563 1,948 2,413

Cost of goods sold -3,017 -2,226 -3,475 -5,768 -7,583 -9,941

Gross profit 3,655 8,915 13,871 22,940 30,050 39,253

Personnel expenses -3,756 -3,659 -4,416 -5,049 -5,210 -5,240

Depreciation and amortisation -223 -299 -334 -418 -518 -635

Other operating expenses -4,635 -7,650 -10,429 -15,845 -20,789 -28,280

Operating income (EBIT) -4,959 -2,692 -1,308 1,629 3,533 5,099

Net financial result 128 24 56 15 54 184

Income before taxes & minority interests -4,831 -2,668 -1,252 1,644 3,587 5,283

Taxes 575 1,233 486 0 0 0

Result from discontinued operations -668 -603 0 0 0 0

Net income (before minorities) -4,924 -2,038 -766 1,644 3,587 5,283

Minority interest -1,312 -233 -239 514 1,121 1,651

Net income / loss -3,611 -1,804 -527 1,130 2,466 3,632

EPS€ -0.24 -0.12 -0.03 0.07 0.16 0.23 Diluted EPS€ -0.24 -0.12 -0.03 0.07 0.16 0.23 EBITDA -4,736 -2,393 -975 2,046 4,051 5,734 Ratios Gross margin 66.0% 85.1% 84.8% 84.5% 84.2% 83.9% EBIT margin -89.6% -25.7% -8.0% 6.0% 9.9% 10.9% EBITDA margin -85.6% -22.8% -6.0% 7.5% 11.4% 12.3%

Net income margin -65.2% -17.2% -3.2% 4.2% 6.9% 7.8%

Tax rate -11.9% -46.2% -38.8% 0.0% 0.0% 0.0%

Expenses as % of revenues

Cost of goods sold -54.5% -21.2% -21.2% -21.2% -21.2% -21.2%

Personnel expenses -67.8% -34.9% -27.0% -18.6% -14.6% -11.2%

Other operating expenses -83.7% -73.0% -63.8% -58.4% -58.3% -60.5%

Y-o-y growth

Total revenues n.a 89.2% 56.1% 66.0% 31.5% 31.1%

Operating income n.a -45.7% -51.4% n.a 116.9% 44.3%

Net income / loss n.a -50.0% -70.8% n.a 118.2% 47.3%

Market multiples based on implied fair value

P/E -12.42x -24.86x -87.60x 42.58x 19.51x 13.25x

P/Tangible BVPS 9.76x 14.90x 14.48x 13.47x 9.30x 6.46x

EV/Sales 7.74x 4.09x 2.62x 1.58x 1.20x 0.92x

EV/EBITDA -9.04x -17.89x -43.93x 20.93x 10.57x 7.47x

7 September 2010 MyHammer Holding AG

BALANCE SHEET ANALYSIS

All figures in T€ 2008 2009 2010E 2011E 2012E 2013E

Current assets, total 5,394 3,158 2,264 4,083 7,837 13,357

Cash and equivalents 4,533 1,743 818 1,764 5,039 9,829

Trade receivables 619 979 1,348 2,156 2,584 3,247

Other financial assets 97 379 0 0 0 0

Other assets 145 58 98 163 214 281

Non-current assets, total 5,277 4,170 4,690 4,934 4,558 3,919

Property, plant & equipment 423 266 415 690 907 1,188

Intangibles 662 1,078 1,291 1,600 1,747 1,915

Investments in real estate 2,600 0 0 0 0 0

Deferred tax assets 1,592 2,825 2,983 2,644 1,905 815

Total assets 10,671 7,328 6,954 9,017 12,395 17,275

Current liabilities, total 1,949 2,409 2,143 3,339 4,025 5,034

Short-term bank debt 153 0 0 0 0 0

Trade payables 703 463 752 1,303 1,706 2,227

Other financial liabilities 183 770 0 0 0 0

Other provisions 750 954 1,145 1,629 1,784 2,105

Other liabilities 160 222 245 407 535 702

Long-term liabilities, total 2,333 0 0 0 0 0

Long-term bank debt 2,333 0 0 0 0 0

Shareholders' equity 4,593 3,010 3,188 3,495 5,065 7,287

Minority interests 1,796 1,909 1,670 2,183 3,304 4,955

Total shareholders' equity and debt 10,671 7,328 7,000 9,017 12,395 17,275

Ratios

Current ratio 2.77 1.31 1.06 1.22 1.95 2.65

Quick ratio 2.64 1.13 1.01 1.17 1.89 2.60

Equity ratio (as %) 59.9% 67.1% 69.4% 38.8% 40.9% 42.2%

Net debt to equity ratio (net gearing as %) -42.7% -44.9% -25.7% -50.5% -99.5% -134.9%

Equity per share 0.31 0.20 0.21 0.23 0.33 0.47

Net debt -1,961 -1,352 -818 -1,764 -5,039 -9,829

Capital employed (CE) 8,722 4,919 4,811 5,678 8,369 12,242

Return on equity (ROE) -78.6% -47.5% -17.0% 33.8% 57.6% 58.8%

Return on capital employed (ROCE) -48.8% -21.0% -15.8% 31.3% 51.1% 51.3%

Return on assets (ROA) -35.0% -20.3% -8.2% 14.0% 22.5% 23.2%

Days of sales outstanding (DSO) 41 28 26 24 24 23

7 September 2010 MyHammer Holding AG

CASH FLOW ANALYSIS

All figures in T€ 2008 2009 2010E 2011E 2012E 2013E

Net income -3,611 -1,804 -527 1,130 2,466 3,632

Depreciation 223 299 334 418 518 635

Decrease (increase) in net working capital 189 -1,362 -97 -160 51 -42

Others -730 858 -239 514 1,121 1,651

Net operating cash flow -3,929 -2,009 -530 1,901 4,157 5,875

Capital expenditures -6 1,508 -696 -1,001 -882 -1,085

Free cashflow -3,935 -501 -1,226 900 3,275 4,790

Financial cash flow 6,182 -2,289 301 46 0 0

Change in cash 2,247 -2,790 -925 946 3,275 4,790

Cash, start of the year 2,286 4,533 1,743 818 1,764 5,039

Cash, end of the year 4,533 1,743 818 1,764 5,039 9,829

Free cash flow per share (€) -0.27 -0.03 -0.08 0.06 0.21 0.31

Free cash flow yield -9.9% -1.3% -3.1% 2.3% 8.2% 12.0%

Y-o-y growth

Net operating cash flow n.a -48.9% -73.6% n.a 118.6% 41.3%

CAPEX n.a n.a -146.1% 43.8% -11.9% 23.1%

Financial cash flow n.a -137.0% n.a -84.7% -100.0% n.a

7 September 2010 MyHammer Holding AG

FIRST BERLIN RATING AND PRICE TARGET HISTORY

Report No.:

Date of publication

Previous day

closing price Rating

Price target Interim high % change to high Initial

Report 7 September 2010 €2.70 Add €3.00 - -

F I R ST B ER L I N D IS C L AI M E R

Disclaimer

Adrian Kowollik First Berlin Equity Research GmbH Mohrenstrasse 34 10117 Berlin Tel. +49 30 8093 9 690 Fax +49 (0)30 - 80 93 96 87 [email protected] www.firstberlin.comFIRST BERLIN POLICY

In an effort to assure the independence of First Berlin research neither analysts nor the company itself trade or own securities in subject companies. In addition, analysts’ compensation is not directly linked to specific financial transactions, trading revenue or asset management fees. Analysts are compensated on a broad range of benchmarks. Furthermore, First Berlin receives no compensation from subject companies in relation to the costs of producing this report.

ANALYST CERTIFICATION

I, Adrian Kowollik, certify that the views expressed in this report accurately reflect my personal and professional views about the subject company; and I certify that my compensation is not directly linked to any specific financial transaction including trading revenue or asset management fees; neither is it directly or indirectly related to the specific recommendation or views contained in this research. In addition, I possess no shares in the subject company.

INVESTMENT RATING SYSTEM

First Berlin’s investment rating system is five tiered and includes an investment recommendation and a risk rating. Our recommendations, which are a function of our expectation of total return (forecast price appreciation and dividend yield) in the year specified, are as follows: STRONG BUY: Expected return greater than 50% and a high level of confidence in management’s financial guidance

BUY: Expected return greater than 25% ADD: Expected return between 0% and 25% REDUCE: Expected negative return between 0% and -15% SELL: Expected negative return greater than -15%

Our risk ratings are Low, Medium, High and Speculative and are determined by ten factors: corporate governance, quality of earnings, management strength, balance sheet and financing risk, competitive position, standard of financial disclosure, regulatory and political uncertainty, company size, free float and other company specific risks. These risk factors are incorporated into our valuation models and are therefore reflected in our price targets. Our models are available upon request to First Berlin clients.

Up until 16 May 2008, First Berlin’s investment rating system was three tiered and was a function of our expectation of return (forecast price appreciation and dividend yield) over the specified year. Our investment ratings were as follows: BUY: expected return greater than 15%; HOLD: expected return between 0% and 15%; and SELL: expected negative return.

ADDITIONAL DISCLOSURES

This report is not constructed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer would be illegal. We are not soliciting any action based upon this material. This material is for the general information of clients of First Berlin. It does not take into account the particular investment objectives, financial situation or needs of individual clients. Before acting on any advice or recommendation in this material, a client should consider whether it is suitable for their particular circumstances and, if necessary, seek professional advice. The material is based upon information that we consider reliable, but we do not represent that it is accurate or complete, and it should be relied upon as such. Opinions expressed are our current opinions as of the date appearing on this material only; such opinions are subject to change without notice.

Copyright © 2010 First Berlin Equity Research GmbH. All rights reserved. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without First Berlin’s prior written consent. The research is not for distribution in the USA or Canada. When quoting please cite First Berlin as the source. Additional information is available upon request.