COSTING SUPPORT AND COST CONTROL

IN MANUFACTURING

A COST ESTIMATION TOOL APPLIED IN THE SHEET METAL DOMAIN

PROEFSCHRIFT

ter verkrijging van

de graad van doctor aan de Universiteit Twente, op gezag van de rector magnificus,

prof.dr. F.A. van Vught,

volgens besluit van het College voor Promoties in het openbaar te verdedigen

op vrijdag 3 mei 2002 te 15.00 uur.

door

Erik ten Brinke geboren op 15 maart 1973

Dit proefschrift is goedgekeurd door: de promotor prof.dr.ir. H.J.J. Kals.

Costing support and cost control

in manufacturing

A cost estimation tool applied in the sheet metal domain

ISBN 90-365-1726-5 © Erik ten Brinke, 2002

Preface

This thesis is the result of five years of research in the field of costing support and cost control in manufacturing. The research has been performed in the framework of a research program focussed on sheet metal manufacturing as part of the IOP-research program supported by the Dutch Ministry of Economic Affairs. The research has been supervised by Prof. H.J.J. Kals, former chairman of the laboratory of Design, Production and Management at the University of Twente. The research has been a continuation of two previous research projects at the laboratory mentioned above. The result of the project ”An architecture for cost control in manufacturing: the use of cost information in order-related decisions” by Arthur Liebers has been a starting point for this research. In addition, the results of the project “Manufacturing integration based on information management” by Eric Lutters have been employed in this research.

I could not have accomplished this research without the help of others. First, I want to thank Prof. Kals and Ton Streppel for their support. Though our discussions weren’t that frequent and easy, they helped me to find a proper path in my research. Further, I want to thank Arthur Liebers for passing on the results of his research including his library of cost literature. Also, I want to thank Eric Lutters for his, sometimes philosophical and sometimes repeatedly, explanations of some of the principles of his Information Management approach. Furthermore, I want to thank all of my colleagues at the laboratory. I have appreciated their companionship at work, at activities outside work and at activities outside work at work.

Within this research, two students finished their master assignment, resulting in valuable input for my research. Therefore, I want to thank René Veltman and Alex Huttinga for accomplishing their, in their eyes abstract, assignments. In spite of their lack of interest and lack of experience in programming, they made a valuable contribution to the prototype implementation.

Finally, I want to thank my parents and sister for their support and patience.

Enschede, 24 February 2002

Summary

In the product development cycle several engineering tasks like design, process planning and production planning have to be executed. The execution of these tasks mainly involves information processing and decision-making. Because costs is an important factor in manufacturing, adequate information about costs is extremely valuable for all engineering tasks. Therefore, a cost estimation system for the generation of cost information and for cost control, integrated in the product development cycle, is required.

The integration of engineering tasks in the product development cycle has been a major research topic in the last decades. Because engineering tasks can be seen as information processing tasks, information is the proper base for integration. The Manufacturing Engineering Reference Model developed at the Laboratory of Design, Production and Management, is based on the use of a central information management kernel that facilitates both the availability and the accessibility of meaningful representations of the evolving manufacturing information. Because this reference model is designed especially for the integration of engineering tasks, it is used for the development of the cost estimation system.

Based on a literature review on cost control and cost estimation in manufacturing and the Manufacturing Engineering Reference Model, a generic cost estimation architecture has been developed. The architecture consists of six functional modules arranged around the information kernel of the Manufacturing Engineering Reference Model. The separate modules are: Cost Models, Cost Determination, Cost Reports, Risk Analysis, Data Analysis and Data Tuning. The Cost Model module is used for the definition and the management of cost models. Multiple cost models can be defined in order to support all engineering tasks and to be able to compare cost models. Based on a cost model, the Cost Determination module calculates the costs. A cost model can be selected based on a specific cost model, the required accuracy or the available information. Cost reports can be created with the Cost Report module. Information about the quality, the accuracy and the sensitivity of the costs has to be provided by the Risk Analysis module. The analysis of (historic) data is a task for the Data Analysis module, while the Data Tuning module has to tune data. A new method for variant based cost estimation is proposed and positioned in the architecture.

The cost models are defined based on the cost structure. With the aid of the cost structure, costs can be defined for any object causing costs. Because cost structures can be attached to the information structures related to the Manufacturing Engineering Reference Model, the costs can be calculated for any object at any aggregation level. Additionally, the cost structure enables the differentiated storage of cost information. Based on the information structures and the cost structures, cost views can be constructed. These cost views visualise the differentiated costs for the user.

The cost estimation architecture and the cost structure enable the use of four cost control loops: the engineering and planning feedback loop, the order acceptance feedback loop, the production feedback loop and the accounting feedback loop.

Some parts of the cost estimation architecture have been implemented in a prototype system. The prototype system is demonstrated by means of an example from the product development cycle in the sheet metal manufacturing domain. Generative and variant based cost estimation are used to demonstrate cost support and cost control. For generative cost estimation two distinct cost models, direct costing and activity based costing, are used.

Samenvatting

In de ontwikkelingscyclus van een product moeten verscheidene engineeringstaken worden uitgevoerd. De uitvoering van deze taken bestaat voornamelijk uit informatie verwerken en beslissingen nemen. Omdat binnen het hele voortbrengingsproces van een product de kosten een belangrijke rol spelen, is geschikte informatie over de kosten voor de engineeringstaken zeer waardevol. Daarom is een kostprijsschattingssysteem voor de generatie van kosten informatie en voor de beheersing van de kosten, geïntegreerd in de ontwikkelingscyclus van een product, noodzakelijk.

In de laatste decennia was de integratie van engineeringstaken in de ontwikkelingscyclus van een product een belangrijk onderzoeksthema. Omdat engineeringstaken als informatieverwerkingstaken gezien kunnen worden, is informatie de juiste basis voor integratie. Het binnen het laboratorium Ontwerp, Productie en Management ontwikkelde “Manufacturing Engineering Reference Model” is gebaseerd op een centrale “information management kernel”, die de beschikbaarheid en de toegankelijkheid van betekenisvolle representaties van de zich ontwikkelende informatie mogelijk maakt. Omdat dit referentie model speciaal voor de integratie van engineeringstaken is ontwikkeld, is het gebruikt voor de ontwikkeling van het kostprijsvoorcaclulatiesysteem.

Gebaseerd op een literatuurstudie naar het schatten en beheersen van kosten en het “Manufacturing Engineering Reference Model” is een generieke kostprijsschattingsarchitectuur ontwikkeld. De architectuur bestaat uit zes functionele modules, die rond de “information management kernel” zijn geplaatst. De afzonderlijke modules zijn: “Cost Models”, “Cost Determination”, “Cost Reports”, “Risk Analysis”, “Data Analysis” en “Data Tuning”. De “Cost Model” module wordt gebruikt voor het definiëren en beheren van kostenmodellen. Om alle engineeringstaken te kunnen ondersteunen en om kostenmodellen met elkaar te kunnen vergelijken, is het mogelijk om meerder kostenmodellen te definiëren. Gebaseerd op een kostenmodel berekent de “Cost Determination” module de kostprijs. Een kostenmodel kan worden geselecteerd op basis van een specifiek kostenmodel, een geëiste nauwkeurigheid of de beschikbare informatie. Kostenrapporten kunnen met de “Cost Report” module worden gegenereerd. Informatie over de kwaliteit, nauwkeurigheid en gevoeligheid van de kosten moet door de “Risk Analysis” module worden geleverd. De analyse van (historische) data is de taak van de “Data Analysis” module en de “Data Tuning” module moet data op elkaar afstemmen. Een nieuwe methode voor variant gebaseerd schatten van de kostprijs wordt voorgesteld en in de kostpijsvoorcalculatiearchitectuur gepositioneerd.

De kostenmodellen worden gedefinieerd op basis van de kostenstructuur. Met behulp van de kostenstructuur kunnen de kosten voor ieder object dat kosten veroorzaakt worden gedefinieerd. Omdat kostenstructuren aan de informatiestructuren, gerelateerd aan het “Manufacturing Engineering Reference Model”, kunnen worden verbonden, is het mogelijk voor ieder object en op ieder aggregatieniveau de kosten te berekenen. Bovendien maakt de kostenstructuur de gedifferentieerde opslag van de kosten mogelijk. Op basis van de informatiestructuren en de kostenstructuren kunnen kosten “views” worden geconstrueerd. Deze kosten “views” visualiseren de gedifferentieerde kosten voor de gebruiker.

De kostprijsvoorcalculatiearchitectuur en de kostenstructuur maken het gebruik van vier feedbackloops voor de beheersing van de kosten mogelijk: de engineering en planning feedbackloop, de orderacceptatie feedbackloop, de productie feedbackloop en de accounting feedbackloop.

Sommige delen van de kostprijsvoorcalculatiearchitectuur zijn geïmplementeerd in een prototype kostprijsvoorcalculatiesysteem. Het prototype systeem wordt aan de hand van een voorbeeld uit de ontwikkelingscyclus van een product in het plaatwerk domein gedemonstreerd. Voor de demonstratie van kostenondersteuning en kostenbeheersing wordt gebruik gemaakt van generatief en variant gebaseerd schatten van de kostprijs. Voor het generatief schatten van de kosten wordt gebruik gemaakt van twee verschillende kosten modellen, nl. “direct costing” and “acitivity based costing”.

Table of contents

Preface ... i

Summary...iii

Samenvatting ... v

Part I: The framework

1 Introduction... 11.1 Cost estimation in manufacturing ... 1

1.2 Sheet metal manufacturing ... 1

1.3 Problem definition ... 2

1.4 Scope of the thesis ... 2

2 Literature review on cost estimation and cost control in manufacturing... 3

2.1 Cost ... 3

2.1.1 Cost types... 5

2.1.2 Cost allocation ... 7

2.2 The use of cost information in manufacturing... 8

2.2.1 Task oriented cost information ... 8

2.2.2 The need for information management... 10

2.3 Cost control... 10

2.3.1 The manufacturing planning and control reference model ... 10

2.3.2 The (cost) control architecture... 13

2.4 Cost estimation... 14

2.4.1 Generative cost estimation... 14

2.4.2 Variant based cost estimation ... 16

2.4.3 Hybrid cost estimation ... 18

2.5 Cost modelling ... 18

2.5.1 Determination of the scope ... 19

2.5.2 Determination of the allocation base ... 19

2.5.3 Determination of the cost functions... 20

2.6 Sheet metal manufacturing ... 22

2.6.1 General... 22

2.6.2 Mechanical cutting... 23

2.6.3 Non-mechanical cutting... 24

2.6.4 Joining operations ... 26

2.6.5 Bending operations ... 27

2.7 Restatement of the problem definition... 27

3 Information Management ... 29

3.1 The Manufacturing Engineering Reference Model ... 29

3.3 The information structures ... 32

3.4 Ontologies ... 35

3.5 Process architectures related to Information Management ... 36

Part II: A generic cost estimation architecture

4 Design of a generic cost estimation architecture ... 394.1 Functional specifications ... 39

4.2 Cost information and the information structures ... 40

4.3 The cost estimation architecture ... 43

4.3.1 Cost Models ... 45 4.3.2 Cost Determination ... 47 4.3.3 Data Analysis ... 47 4.3.4 Risk Analysis ... 48 4.3.5 Data Tuning ... 48 4.3.6 Cost Reports... 48

4.4 Variant based cost estimation and its position in the architecture ... 49

5 Employment of the architecture... 53

5.1 Cost control... 53

5.2 Cost modelling ... 57

5.3 Costing support ... 59

5.4 Concluding remarks ... 59

Part III: A prototype cost estimation system

6 Implementation of a prototype cost estimation system ... 636.1 System specifications... 63 6.2 Cooperating systems ... 63 6.2.1 Creation of databases ... 63 6.2.2 Design ... 66 6.2.3 Process planning ... 66 6.2.4 Production planning... 69

6.3 The cost estimation system ... 72

6.3.1 Cost Models module ... 72

6.3.2 Cost Determination module ... 76

6.3.3 Cost Reports module... 77

6.4 Variant based cost estimation ... 79

6.5 Concluding remarks ... 82

7 Application of the prototype cost estimation system in the sheet metal domain... 83

7.1 Example product and context information... 83

7.2 Example cost models ... 86

7.2.1 Direct Costing ... 86

7.2.2 Activity Based Costing ... 87

7.3 Example cost calculations... 88

7.3.1 Generative cost estimation... 89

7.3.2 Variant based cost estimation ... 90

7.3.3 Hybrid cost estimation ... 91

ïð

8 Conclusions and recommendations ... 93

8.1 Conclusions... 93 8.2 Recommendations... 94 ïð References... 95 Terminology... 99

Appendices

A Time and cost functions from literature... 103A.1 Punching ... 103

A.2 Nibbling ... 103

A.3 Cutting... 105

A.4 Water jet cutting... 107

A.5 Laser cutting... 107

A.6 Laser welding... 108

A.7 Bending ... 109

B Example cost structures ... 111

B.1 Resource information structure... 111

B.2 Product information structure ... 112

B.3 Order Information Structure ... 113

C Regression analysis... 115

D Neural networks... 119

E Example product and context information ... 121

E.1 Components ... 121

E.2 Information structures ... 128

Part I

1 Introduction

1.1 Cost estimation in manufacturing

Within this thesis, the focus is on cost estimation in manufacturing. Manufacturing refers to the series of interrelated activities and operations involving the design, the materials selection, the planning, the production and the quality assurance of the products (Chisholm, 1990). The product development cycle consists of a combination of manufacturing activities resulting in a product. Production is only a part of manufacturing and the product development cycle. Production is the act or process (or the connected series of acts or processes) of actually physically making a product from its material constituents. Production can consist of fabrication and assembly operations (Chisholm, 1990). Fabrication addresses those operations applied during production that are not assembly operations. The preparation of the actual production of a product is dealt with by engineering. Therefore, engineering includes activities as design, process planning and production planning.

During the product development cycle, the execution of engineering tasks includes many decisions to be taken. The decisions are concerned with the product, the production of the product and the disposal/recycling of the product. The decisions are based on several criteria, e.g. technical constraints, but costs are also an important criterion. In order to be able to use costs as a decision criterion, the costs of all aspects of the product have to be known. Because the costs are not known in advance, a cost estimation system is required to generate the required cost information. The cost estimates have to be based on the product information, which is available at a certain stage of the product development cycle. Because the available information is different in amount and detail in different stages of the product development cycle, it is difficult to support all engineering tasks.

Besides the use of cost estimation for decision-making, it can also be used to control costs. When the costs can be controlled, it is possible to propose specific product changes reducing the costs. In order to reduce the time span of the product development cycle concurrent engineering is used. In concurrent engineering, the engineering tasks are partially performed simultaneously. Concurrent engineering requires the integration of the engineering tasks in the product development cycle. In order to support the engineering tasks with cost information, cost estimation has to be integrated in the product development cycle as well.

1.2 Sheet metal manufacturing

The investigation reported in this thesis has been performed in the framework of a research program focussed on sheet metal manufacturing as part of the IOP-research program supported by the Dutch Ministry of Economic Affairs.

Trends in small batch manufacturing in the sheet metal industry are a further decrease of batch sizes, shorter delivery times and lower prices. Therefore, in the sheet metal industry it is crucial to be able to generate cost estimates and to control the costs in order to make fair profit. Many sheet metal companies in The Netherlands are supply companies. Especially these companies have to be able to generate cost estimates quickly and accurately. The cost estimates have to be generated quickly because quotations have to be offered to potential customers in a short time period. The cost

estimates have to be generated accurately because the margins between cost price and sales price are small due to (inter-) national competition.

1.3 Problem

definition

The success of a company largely depends on the profit that it can realise. The profit is determined by the costs that are made and the extent in which these costs are recovered. Therefore, it is essential for a company to know the (future) costs and being able to control them. When the (future) costs are known throughout the entire product development cycle, the engineers can make use of cost information during the decision-making processes. Therefore, it is necessary to integrate the cost estimation activities in the product development cycle. For this a system is required that can support engineers and other systems in cost estimation and cost control.

The objective of this research is to develop a prototype cost estimation system that can provide cost information throughout the whole product development cycle and that can be used for cost control. In order to be independent of the manufacturing environment, the cost estimation system has to be generic. An implementation of the system has to be applied in the sheet metal domain.

1.4 Scope of the thesis

This thesis is composed of three parts: the framework, a generic cost estimation architecture and a prototype cost estimation system.

Part I: The framework

In the chapter “Literature review on cost estimation and cost control in manufacturing”, the terminology used in literature and used in this thesis is explained. Furthermore, some methods in the field of cost control and cost estimation are discussed.

First, it is explained what costs are, how they can be characterised and how they can be assigned to products. The use of cost information in manufacturing is discussed. For different engineering tasks different cost information is used in a different manner. Furthermore, the cost information produced by different engineering tasks has to be managed properly in order to be able to use it effectively.

Second, one method for cost control is discussed. This method is positioned in manufacturing and the distinguished functions are explained. The two most important functions: cost estimation and cost modelling are clarified based on literature.

Third, common sheet metal processes are described. Furthermore, time and cost functions from literature are given per process.

Finally, an information management approach is described that is very suitable for the integration of engineering tasks in the product development cycle based on information. The related information structures and process architectures are explained.

Part II: A generic cost estimation architecture

In this part, the design of a generic cost estimation architecture is explained. Based on information from the literature review, functional specifications and information structures, a cost estimation system is designed. The functional modules are described and the function and the use of the architecture are clarified.

Part III: A prototype cost estimation system

The cost estimation architecture was partially implemented in a prototype cost estimation system. The prototype cost estimation system is demonstrated by means of an example taken from the sheet metal domain.

2 Literature review on cost estimation and

cost control in manufacturing

This chapter provides a literature overview on cost estimation and cost control in manufacturing. First, the notion cost will be discussed in general in section 2.1. Next, the use of cost information in the product development cycle is discussed in section 2.2. The use of cost information by different engineering tasks and the need for an information management system is described. Besides the ability to estimate costs, it is necessary to be able to control the costs. Section 2.3 positions cost control in manufacturing and will discusses the sub functions of cost control. The two most important functions: cost estimation and cost modelling are discussed in section 2.4 and 2.5. Section 2.6 deals with the most common sheet metal processes and the related cost and time functions. Finally, the problem definition is restated in section 2.7.

2.1 Cost

The broad definition of costs is related to the economic resources (manpower, equipment, real facilities, supplies and all other resources) necessary to accomplish work activities or to produce work outputs (Stewart, 1995a). Usually, costs are expressed in terms of units of currency. Therefore, costs are the amount of money representing the resources spent for the production of output. A resource is a physical entity that is required to be able to execute a certain operation. Resources can be e.g. machine tools, tools and fixtures, but also operators and materials. Output can be products and services.

During the product development cycle, engineering tasks cause and fix costs. Figure 2.1 shows the influence of several company departments on the product costs as taken from a German research project in machine design (Wierda, 1990). The engineering tasks cause costs because of their contribution to the development of a product. At the start of the product development cycle, no costs are fixed yet (Figure 2.2). The consecutive engineering tasks fix the costs because of the decisions taken. The decisions taken during an engineering task at the beginning of the product development cycle can significantly influence the costs caused by engineering tasks later in the engineering cycle because the solution space for the engineering tasks is reduced by it. Figure 2.1 shows that design itself takes only about 10% of the product costs, whereas it fixes about 70% of the product costs. It has been argued that the latter percentage is misleading because the product specifications already imply some minimal costs. According to Ehrlenspiel, design is responsible for 20 to 30% of the total product costs (Wierda, 1990).

The way in which engineering tasks contribute to the product costs depends on the production environment. Figure 2.3 shows a comparison between high-tech production and classic mass production (Thompson, 19??) . The figure shows that for high-tech production the costs caused before production are about 5 times higher than for mass production, while the costs of production are about one fifth. For mass production, it is required to be able to estimate the costs of production more accurately than the costs of design and engineering. For high-tech production, the opposite applies.

Figure 2.1 Experimentally determined influence of the main departments of a company on the product costs (Wierda, 1990).

Figure 2.2 Decreasing costs not fixed and increasing costs caused during the product development cycle (Wierda, 1990).

Figure 2.3 Product life-cycle costs (Thompson, 19??).

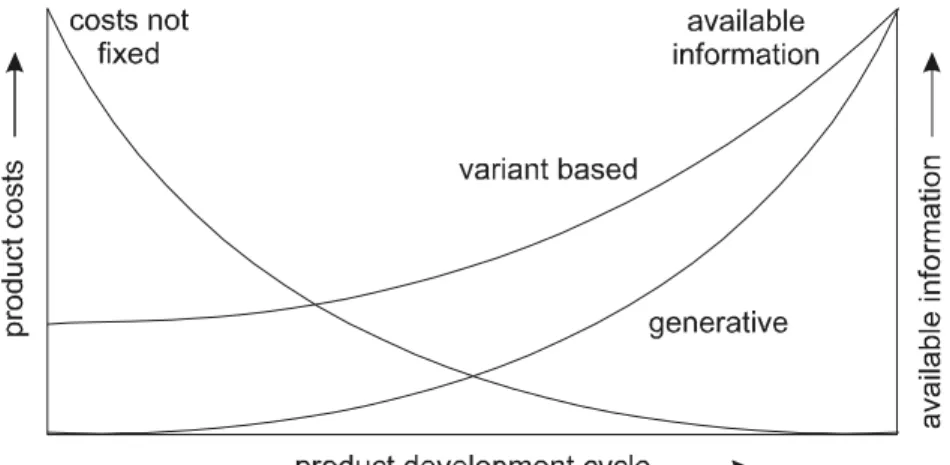

It is easier to estimate costs accurately when more detailed information is available. Since design fixes about 70% of the product costs, it is required to make accurate cost estimates during design. However, during the design process the product information is not yet available in full detail, so it is

difficult to make accurate estimates. This phenomenon is known as the cost estimation paradox, see Figure 2.4.

Figure 2.4 The cost estimation paradox (Bode,1998a).

2.1.1 Cost types

Total product costs are composed of several different cost items. Possible breakdowns of the product costs are the cost breakdown structures of Fabrycky & Blanchard (Asiedu, 1998) and Liebers (Liebers, 1998) (Table 2.1 and Table 2.2). These two examples show that multiple breakdown structures are possible. A general cost break down structure seems hardly possible. Two important criteria for a good cost breakdown are: all costs must be covered and no costs must be counted twice.

Total product cost Research and development cost Production and construction cost Operations and maintenance cost Retirement and disposal cost - Product management - Product planning - Product research - Design documentation - Product software - Product test and

evaluation - Manufacturing/ construction management - Industrial engineering and operations analysis - Manufacturing - Construction - Quality control - Initial logistic support - Operations/ maintenance management - Product operation - Product distribution - Product maintenance - Inventory - Operator and maintenance training - Technical data - Product modification - Disposal of repairable - Product retirement - Documentation

Table 2.1 The cost breakdown structure of Fabrycky & Blanchard (Asiedu, 1998).

The costs from a cost breakdown structure are caused by different resources and the way these costs are related to those resources can be different. In order to get a better perception of costs, costs are classified in different types according to their cause and the relation to their cause. Therefore, it is advantageous to know the costs per cost type

Two general cost classifications are on the one hand direct versus indirect costs and on the other hand variable versus fixed costs. Direct costs are costs that can be identified specifically and consistently with an end objective (such as a product, service, software, function, or project), while indirect costs cannot be identified specifically and consistently with an end objective (Shuford, 1995). This means that direct costs can be allocated directly, i.e. the allocation base is known, whereas for the allocation of indirect costs an allocation base has to be defined (Cooper, 1991). The allocation of costs will be treated in more detail in the next section.

Variable costs are costs that change with the rate of production or the performance of services (Stewart, 1995a). Fixed costs are costs that do not vary with the volume of business (Stewart, 1995a). Furthermore, semi variable costs and step-fixed costs can be distinguished. Semi variable costs are costs that vary somewhat in relation to volume, but their percentage of change is not the same as the percentage of change in volume (Shuford, 1995). Step-fixed costs are fixed costs that alter their behaviour as the activity level moves from one relevant range to another (Shuford, 1995).

Product cost

Costs of executing a production plan Costs of generating a production plan Costs of successfully executing a production plan Costs of re-planning Externally imposed burdens - Marketing and promotion - Company management, including control - Sales and order intake - Resource, process and

product design - Process planning - Production planning - Having production resources - Using production resources - Materials included in the products - Waste

- Repair, rework and scrap

- Resource repair, including down time - Late delivery

- Contingency allowances - Cost increasing

taxes (as opposed to profit reducing taxes)

Table 2.2 The cost breakdown structure of Liebers (Liebers, 1998).

The distinction between recurring & non-recurring and relevant & irrelevant costs is also often used. Recurring costs are repetitive costs that vary with the quantity being produced (Stewart, 1995b) . Non-recurring costs are elements of development and investment costs that generally occur only once in the life cycle of a work activity or work output (Stewart, 1995b). Relevant costs are costs that are present in one of several alternatives but are absent, either in whole or in part, in other alternatives (also called differential costs) (Shuford, 1995). These costs play a role in specific decision-making processes, whereas all other costs are irrelevant costs (Liebers, 1998).

Other cost types that are frequently distinguished are listed here to illustrate the diversity of cost types:

Acquisition costs: Total expenditures estimated or incurred for the development, manufacture, construction and installation of an item of physical or intangible property, or the total acquisition costs of a group of such items (Stewart, 1995a).

Conversion costs: A grouping of direct labour and manufacturing overhead into a single summary cost element (Shuford, 1995).

Development costs: Costs of a system up to the point where decision is made to procure an initial increment of the production units or the operational system (Stewart, 1995a). Disposal costs: The costs of disposing of a facility, property item, equipment item, scrap,

by-products or excess material (Stewart, 1995a).

Life-cycle costs: All costs incurred during the projected life of the system, subsystem or component (research, development, test, evaluation, production, maintenance and disposal) (Stewart, 1995a).

Opportunity costs: Loss of income due to not selecting the optimum alternative from a financial point of view (Liebers, 1998)(Blommaert, 1998).

Prime costs: Costs of direct material and direct labour (Shuford, 1995).

Removal costs: The costs of dismantling a unit of property owing to retirement from service (Stewart, 1995a).

Sunk costs: The total of all past expenditures or irrevocably committed funds related to a program/project (Shuford, 1995).

2.1.2 Cost allocation

The allocation of cost is important for a correct interpretation of costs. Cost allocation is a method or combination of methods that results in a reasonable distribution of costs (Stewart, 1995a). For direct costs, this allocation is straightforward. The costs can be calculated from:

Q P

C= × (2.1)

with: C: the costs

P: the price variable Q: the allocation base

In the case of direct labour costs, C is the direct labour costs, P is the hourly rate and Q the number of hours. In the case of indirect costs, the allocation base has to be defined. After this, the price variable can be calculated from:

Q C

P= (2.2)

with: P: the price variable, usually called rate

C: the indirect quantity Q: the allocation base

The values of the indirect quantity and the allocation base can be obtained from historic information or from prognoses or a combination of both.

If, for example, the total direct costs are chosen as the allocation base for the total indirect costs, P is the direct cost burden rate, C the total indirect costs and Q the total direct costs. When the rate is known, the costs can be calculated with equation 2.1. This example illustrates the way in which indirect costs are calculated with the traditional costing method. With this method, the overhead is allocated to products using volume based allocation bases e.g. labour hours, machine hours. When the allocation base is chosen incorrectly, incorrect conclusions can be drawn from the indirect costs. When the indirect costs are calculated with the direct cost burden rate, it would mean that every product with high direct costs also has high indirect costs, which is not the case. Therefore, this can lead to wrong conclusion about the cause of costs.

The ratio between direct costs and indirect costs has changed drastically over the past decades because of increasing automation, in both machinery and computers, as illustrated by Figure 2.5 (Thompson, 19??). In the 1950’s, the indirect costs were only a small part of the total product costs while direct labour constituted the biggest part of the total product costs. Therefore, it was not necessary to estimate the indirect costs in a very detailed and accurate manner and traditional costing was an adequate way to calculate the overhead.

Nowadays, the opposite situation is true. Overhead constitutes the biggest part of the total product costs while the direct labour costs are only a small part. The part of the material costs in the total costs has hardly changed. Because of this change, it has become necessary to calculate the overhead more accurately and more detailed. The allocation of the overhead requires the use of other allocation bases that allocate the overhead in a more realistic way. Other methods for the allocation of overhead costs will be discussed in section 2.5.

2.2 The use of cost information in manufacturing

Different engineering tasks have different information available for generating relevant cost information. In addition, the tasks use different kinds of cost information for different purposes. In section 2.2.1, an overview will be given of the use of cost information for the next tasks: design, process planning, production planning and management. This overview indicates a considerable interrelation between the different tasks and the information that is used. Therefore, the importance of an information management system will be indicated in section 2.2.2

2.2.1 Task oriented cost information

In the embodiment design phase, decisions about materials, surface roughness, tolerances, shape, dimensions, production methods, etc. have to be made. Because all decisions are mutually dependent, a decision about one aspect can lower the costs for that aspect while increasing the costs of another aspect. For instance, the selection of a cheap material can lead to extra operation steps in order to achieve a certain surface tolerance, which increases the production costs. Several of these dependencies are present. From an analysis of the product design process and its decision making it can be concluded that the costs fixed during product design are caused by the following interrelated cost drivers: geometry, material, production processes and production planning (Weustink, 2000). Next, the interrelation of the cost drivers will be illustrated. The interrelation of the cost drivers causes the interrelation between the engineering tasks, which influences the use of cost information by these engineering tasks.

Interrelated cost drivers

The geometry includes the shape, dimensions, accuracy, etc. and it determines the material quantity and the production processes that are required. The influence of the geometry on the product costs is obvious. For instance, a higher level of accuracy requires more accurate resources (e.g. machine tools, equipment), which can result in higher production costs. The shape can also cause increasing production costs; a pocket with straight corners requires generally a more expensive machining process (e.g. electrical discharge machining) than a pocket with rounded corners (made by e.g. milling).

Material is one of the most obvious cost driving product characteristics, because material costs constitute a large part of the total product costs (see for instance Figure 2.5).

Production processes are required to transform (raw) material into a component or to assemble components and/or assemblies into higher-level assemblies. Resources (e.g. operators, machine tools, tool sets, fixtures) are needed to perform the required production operations. The resources have a certain capability, which means that resources have technical restrictions, concerning the power of the machine tool, accuracy, maximum dimensions of the workpiece, etc. The limited capability of resources restricts the execution of certain operations. This has to be taken into account in the planning phases of the product development cycle. The type of production method selected has a significant influence on the production costs.

Besides the technical restrictions, resources have also logistic restrictions, which means that a resource will not always be available. With the knowledge of these restrictions, operations can be allocated to the available resources. It is necessary to ensure the due date, because otherwise a fine could be incurred. These time, and therefore, cost consequences must be regarded in the planning phases.

The goal of production planning with regard to costs is to minimise the variable costs that are a result of production planning decisions (Giebels, 2000). The variable costs to be regarded are: extra payments for overtime work, the price for subcontracting minus the variable costs for in-house production, inventory costs due to excessive Work In Process (WIP), lateness cost (in particular penalty costs) and earliness costs for short time delivery of blank materials. A prototype of a decision support system for integrated order planning, which incorporates these variable costs, will be discussed in more detail in section 6.2.4.

The cost drivers and the engineering tasks

In the design phase, the primary decisions are concerned with geometry and material. For proper decision-making, it is advantageous to have information from other engineering tasks, usually performed later in the product development cycle, like process planning and production planning. Initially the designer can get benefit out of cost information related to geometry and material. When cost information about production processes and production planning would be available, this would be of great help to the designer. Because geometry does not cause costs directly, the designer cannot calculate costs for geometry. A way to solve this problem is to use cost information from products that have been manufactured in the past. The assumption is made that geometrically equal products (of the same material) will cost the same. This method will be discussed in section 2.4.2 in detail. This method can give cost information quickly because no other engineering tasks, like process planning, are required to generate more information. The designer can estimate the material costs relatively easy when he has access to a material database, which also contains cost information. Another way to solve the problem is to perform other engineering tasks, like process planning, and to use the generated information for cost estimation. The designer must frequently choose between alternative solutions. In the choice between alternatives, the overhead costs are usually less important because they are made anyway. Therefore, only the direct costs are considered in choices between alternatives.

In the process-planning phase, the primary decisions are concerned with production processes. A cost based decision between production processes is difficult because cost information about a process largely depends on the resources that are used. Similarity, based on production processes, with products from the past could be used in this case. When resources are selected, the extent of use can be estimated and costs can be calculated with the appropriate cost rates. The choices about the production processes are made based on the technical constraints and the technical ability of the resources. If the availability of resources would be incorporated in the decision making of the process planner, the choices made would probably be more adequate. The unavailability of a resource can result in the use of a more expensive resource than chosen by the process planner, consequently leading to higher costs.

In the production-planning phase, the primary decisions are concerned with production planning. Usually, production planning is one of the last phases in the product development cycle before production starts. Production planning determines which resources are used and when they are used. The final decision about which resource will be used for a product, not only influences the costs of that product but also the costs of other products that have to be produced. When a resource is selected for one product, this resource cannot be chosen for another product, which could mean that a more expensive resource has to be chosen for the other product. For the production planner, besides the product costs, the costs of all products in the manufacturing cycle can be important. The primary interest of management is information about the costs and revenues at the end of a certain period, rather than the costs and revenues of a specific product. For the analysis of the costs, it is advantageous to have the costs split up in the different types. Furthermore, based on the analysis of the resource utilisation rates, management can adapt the resources rates. The cost information about products and resources can be used when considering buying new resources.

2.2.2 The need for information management

From the previous section, it can be concluded that decisions of different engineering tasks influence each other. Furthermore, engineering tasks use information from and/or generate information for other engineering tasks. In order to tune the need for and the availability of information from different engineering tasks, the structuring of information has to be unified and communication between the engineering tasks has to be made possible. When concurrent engineering is applied in the product development cycle, the need for communication increases even more. Concurrent engineering, i.e. the simultaneous execution of shared tasks by separate departments and the control of cooperative decision-making, requires additional tuning of engineering.

The possibility of communication between the engineering tasks is based on both the availability and accessibility of coherent information (Lutters, 1997a). In the automation of the product development cycle, engineering databases play a key role (Billo, 1987). An engineering database can contain geometric, physical, technological and other properties of “technical” objects and the relations between these properties (Billo, 1987). Usually, the engineering tasks require information from multiple databases. Therefore, for the integration of engineering tasks in the product development cycle an information management system is indispensable. In chapter 3, an information management model based on the accessibility of transparent information will be discussed.

2.3 Cost

control

The function of cost control is twofold. On the one hand, it has to detect cost values and sources of these costs. It can initiate a well-founded product modification in order to keep costs within a predetermined range or to cut costs in general. On the other hand, it must be possible to compare cost estimates with the actual costs. In this way, cost models can be improved. The feedback of cost information is an essential part of cost control.

A way of describing and understanding a complex system such as the manufacturing system is the decomposition of the system. A possible representation of decomposition is a reference model. A reference model represents a system as an organisation in terms of its structure of relatively independent, interacting components, and in terms of the globally defined tasks of these components (Biemans, 1989). Many reference models for the manufacturing system have been developed in the last decades, see for example (Lutters, 2001). In section 2.3.1 the manufacturing planning and control reference model of Liebers will be discussed. This reference model was developed especially to clarify the relation between cost control and manufacturing.

When the position of cost control in the manufacturing system is known, the cost control component can also be decomposed. Another possible representation of decomposition is an architecture. An architecture is a framework which defines the functions, which are required to perform the task of a system, with their input and output (Arentsen, 1995). The cost control architecture that was developed in the context of the manufacturing planning and control reference model of Liebers will be discussed in section 2.3.2.

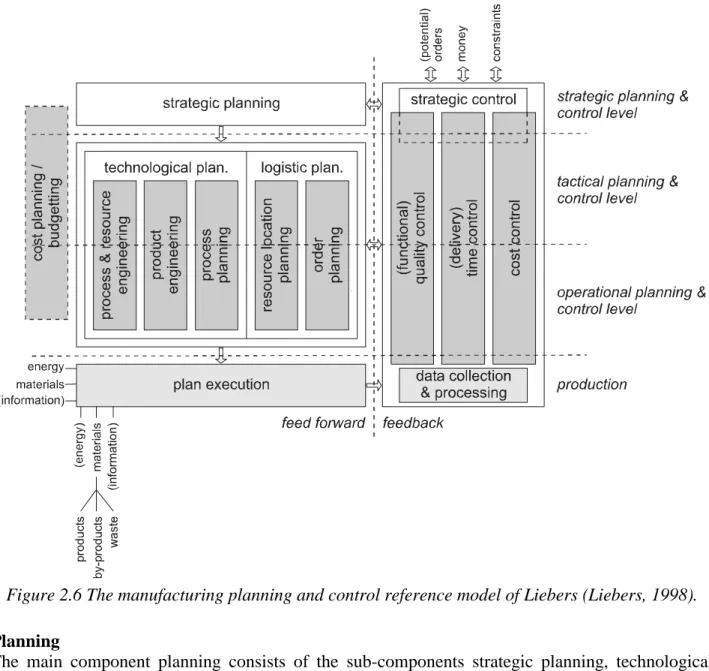

2.3.1 The manufacturing planning and control reference model

The manufacturing planning and control reference model of Liebers depicted in Figure 2.6 consists of three main components, namely planning, execution and control. The three main components are subdivided into several sub-components. In the reference model, hierarchical planning is assumed. The four planning & control levels that are discerned are the strategic level, the tactical level, the operational level and production. However, for the implementation of the components other planning and control levels can be used.

Figure 2.6 The manufacturing planning and control reference model of Liebers (Liebers, 1998).

Planning

The main component planning consists of the sub-components strategic planning, technological planning and logistic planning. Technological planning is again subdivided into process planning & resource engineering, product engineering and process planning. Logistic planning is subdivided into resource location planning and order planning. The task of planning is the generation of a valid production plan.

Strategic planning decides on the goals of the organization and the strategies for attaining these

goals. Closely related to strategic planning is the selection of types of products and the amounts of products to be manufactured. The policy of how to deal with (potential) customers, vendors, make-buy decisions, hourly resource rates etc. are determined by strategic planning.

Technological planning generates all required technological information, i.e. the process plan. Process and resource engineering deals with the development of processes and resources as well as

the planning of the technical aspects of maintenance, service and repair. Product engineering and

process planning comprises the generation of product information and the selection of processes

and resources required for the production of the product.

The final allocation of work to resources is done by logistic planning, it determines the time frame for the technological applicable resources, i.e. the production plan. Resource location

planning sees to it that the right resources, including materials, are in the right place at the right

time. Order planning selects the final resources from the set of technically applicable resources determined by process planning. Furthermore, it assigns work to time periods and it decomposes work into smaller units.

Execution

Plan execution creates the physical product according to the production plan. During production

several deviations between the required product and the realised product occur. This can lead to rework that also requires additional planning.

Control

The main component control consists of the sub-components data collection & processing,

strategic control, (functional) quality control, (delivery) time control and cost control. In order to be

able to detect deviations between the planned product and the resulting product, it is necessary to collect data by monitoring the plan execution. The data can refer to the product or the processes. After processing the collected data, models for the planning activities can be created or adjusted.

Strategic control determines the targets for the performance indicators and the initial solution

space for planning activities. The three control components for the performance indicators (functional) quality, (delivery) time and cost have to evaluate the results of a planning and execution activity for each indicator. For the evaluation, the consequences of the results of an activity on the performance indicators have to be compared with the targets set for the performance indicators.

For the development of a valid production plan, frequent communication between the components is necessary. Communication with the company environment is dealt with by strategic control. The targets for the performance indicators are passed from strategic control to the other control components. Because the performance indicators affect each other, communication between the control components is essential. The input for the planning components comes from strategic planning. Communication between the components of technological planning and between the components of logistic planning is required. In addition, communication between technological and logistic planning is required.

Although a reference model does not contain information flows, the information flow in the reference model is divided into a feedforward and feedback part. In the feedforward part, the planning and execution components generate and process information for the execution of other components. In the feedback part, the control components process and generate information for the improvement of the execution of other components.

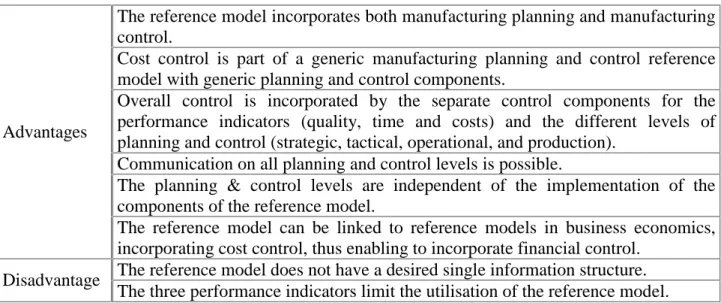

The main advantages and disadvantage of the reference model of Liebers (Figure 2.6) are listed in Table 2.3 (see also Liebers, 1998).

The reference model incorporates both manufacturing planning and manufacturing control.

Cost control is part of a generic manufacturing planning and control reference model with generic planning and control components.

Overall control is incorporated by the separate control components for the performance indicators (quality, time and costs) and the different levels of planning and control (strategic, tactical, operational, and production).

Communication on all planning and control levels is possible.

The planning & control levels are independent of the implementation of the components of the reference model.

Advantages

The reference model can be linked to reference models in business economics, incorporating cost control, thus enabling to incorporate financial control.

The reference model does not have a desired single information structure. Disadvantage

The three performance indicators limit the utilisation of the reference model.

Table 2.3 Advantages and disadvantages of the manufacturing planning and control reference model of Liebers

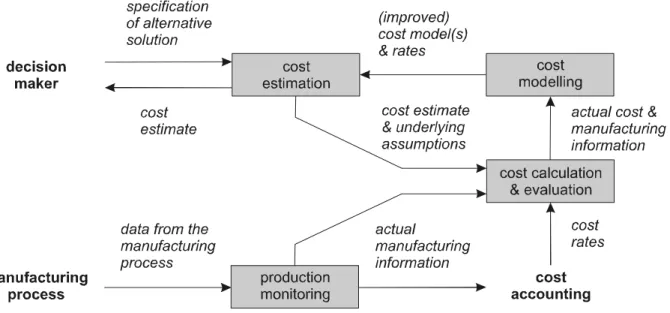

2.3.2 The (cost) control architecture

According to Liebers the cost control component can be decomposed into four functions: cost estimation, production monitoring, cost calculation & evaluation and cost modelling (Liebers, 1998). The functions of cost control and their input and output are depicted in Figure 2.7.

Figure 2.7 The generic cost control architecture of Liebers (Liebers, 1998).

The cost estimation function generates cost estimates based on the specification of a solution by a decision maker and a cost model with cost rates. The production monitoring function has to collect all actual relevant information from the execution of the production plan. The actual manufacturing data is passed on to cost calculation & evaluation and cost accounting. Based on the actual manufacturing information cost calculation & evaluation generates the actual costs. These actual costs are compared with the cost estimates with the underlying assumptions. Based on this comparison, the actual costs and actual manufacturing information is passed on to cost modelling. Cost accounting generates cost rates based on the actual manufacturing information. Based on the actual costs and actual manufacturing information, cost modelling can improve the cost models.

Four feedback loops can be distinguished in the architecture: the engineering and planning loop, the order acceptance loop, the production loop and the accounting loop. The engineering and planning loop provides decision makers with cost information about different alternative solutions. In this case, qualitative information would be enough in order to make a choice between alternatives, but quantitative information can be used as well. The decisions made for one product obviously influence the total costs in a company. Therefore, the order acceptance loop provides cost information to the decision maker about the cost consequences for all products. In this case, the cost information has to be quantitative cost estimates. In the production loop, information from the actual production of a product is fed back in order to compare the cost estimate for the product with the actual costs for that product. Based on this comparison, the cost model can be improved. In the accounting loop, information from production over a certain period is fed back. In this case, the estimated costs of the period are compared to the actual of the period. Based on this comparison, rates can be improved. The advantages of the cost control architecture are listed in Table 2.4.

The architecture is a generic control architecture. The individual functions are generic functions. Advantages

Short term and long term control loops are incorporated.

Disadvantage The architecture does not have a desired single information structure.

2.4 Cost

estimation

One of the four (sub-) functions of cost control is cost estimation. Within manufacturing, cost estimation is the procedure of approximating the cost of manufacturing a product before all stages of the product development cycle have been executed, based on the information available or that can be collected at the stage of the product development cycle.

Two basic approaches for cost estimation can be distinguished: generative cost estimation and variant based cost estimation. The principle of generative cost estimation is the composition of the costs from its constituents while variant based cost estimation uses similar products manufactured in the past to determine the costs. The difference in applicability of both approaches is illustrated by means of the cost estimation paradox depicted in Figure 2.8. Because variant based cost estimation uses information from products manufactured in the past, more information is available in the beginning of the product development cycle than is the case with generative cost estimation. Furthermore, it is possible to combine the two approaches in a hybrid cost estimation method. The next three sections will elaborate on these three approaches.

Figure 2.8 The cost estimation paradox for generative and variant based cost estimation (Bode, 1998a).

2.4.1 Generative cost estimation

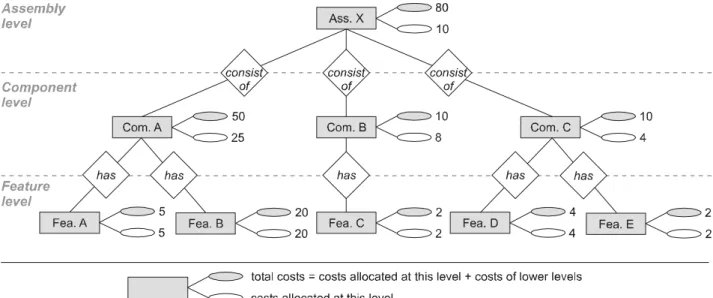

When cost estimation is based on a decomposition of the expected production processes, the approach is called generative cost estimation. The costs caused per production process, direct or indirect, have to be calculated. Consequently, generative cost estimation will largely depend on process planning information. An important issue in generative cost estimation is the aggregation level of the manufacturing activities on which the costs occur and have to be determined. Figure 2.9 depicts an aggregated cost division (modified ABC Hierarchical Model (Cooper, 1991)), which illustrates where the most common costs occur.

The most common lowest level is the (form) feature level. A form feature is a group of faces of a product that together have an engineering meaning. Different types of form features are distinguished, the most common being design features and manufacturing features. These features have a specific engineering meaning for designers and process planners respectively and do not necessarily consist of the same faces.

Two reasons to use design features to assign costs are (Wierda, 1991):

1. Cost functions are derived for classes of similar objects. These objects can serve as the building blocks for global cost estimation. Features are very useful objects, because they have an engineering meaning and they are used commonly.

2. A designer is interested in the causes of costs. If the costs can directly be linked to design features, the designer is able to influence the costs directly.

In fact, these reasons are valid for any kind of feature. Because of these considerations feature based cost estimation is often aimed for.

Figure 2.9 Aggregated costs division (Cooper, 1991).

From an analysis of different types of costs, three categories of costs related to design features, can be distinguished (Wierda, 1991):

1. Costs that can be assigned directly to individual design features. 2. Costs that are incurred for a collection of design features. 3. Costs that cannot be assigned reasonably to design features.

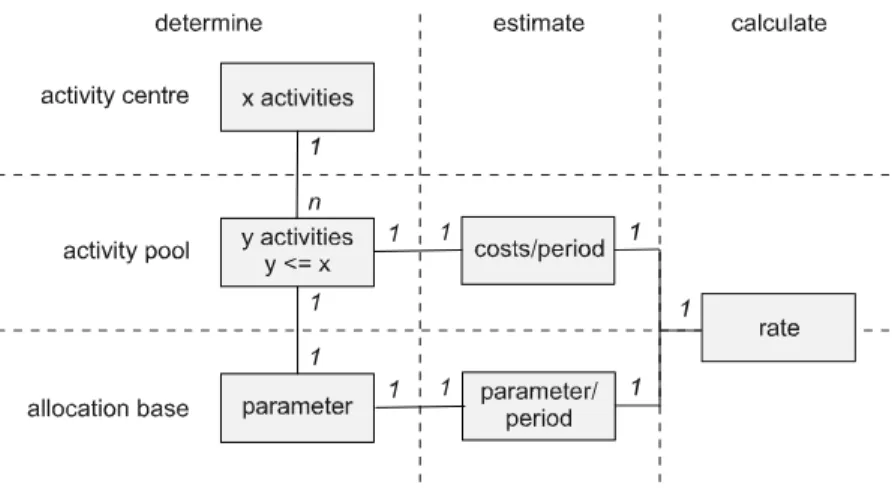

These three categories are valid for any class of similar objects to which costs are related and illustrate the difference between the allocation of direct and indirect costs. The costs that can be assigned directly to design features are costs on feature and assembly level. The costs incurred for a collection of design features are costs on component and batch level. The costs that cannot be assigned reasonably to design feature are costs on order and facility level. When no feature interrelationships are considered, resource selection can be done for every feature separately. Therefore, production times and consequently costs are easily calculated per feature. In (Geiger, 1996) specific time formulas are developed for each standard (design) feature. The time formulas use feature parameters and machine rates. It is also possible to assign machining operations to surfaces and to calculate the costs (Kiritsis, 1996). Some consider a rough process plan to be sufficient for manufacturability and cost analysis (Schaal, 1993). A rough process plan consists of process plans for every feature. A feature process plan only takes into account information about features and information from one higher aggregation level, which could mean the component level. The separate process plans have to be unified based on manufacturing rules. When used during design, for instance the sequence of operation steps does not matter for cost calculation since at this stage the accuracy will be low anyhow because only less detailed information is available, so a cost estimate can be generated based on a rough process plan. When more detailed production information becomes available, cost estimates with higher accuracy can be obtained by using more detailed process plans.

The production of a component usually starts with a blank, to which the material costs can be related directly. The material costs can be related directly to the blank, which is usually considered

a design feature. However, additional design features usually affect the material costs, which have to be accounted for. In (Wierda, 1991) a possible method is described:

• If a (design) feature implies a positive volume, material costs can be directly assigned to it.

• If a (design) feature implies a negative volume, negative material costs (waste revenue) could be directly assigned to it. However, a negative volume could also be created directly by casting or injection moulding for instance, which would not imply any removal of material.

Complications are possible when positive and negative volumes of different features overlap. Furthermore, often parts of the blank that lie outside the final product are not described by design features. Therefore, the material costs of these parts cannot be assigned to design features directly. Further complications as a result from intersecting features as may arise in prismatic parts do not occur frequently in the sheet metal domain.

Most operations are carried out for groups of features in one set-up. The costs involved with these tasks have to be assigned reasonably to the features involved. However, the use of such assignments can be confusing and misleading (Wierda, 1991). When for instance a feature is removed, the costs will not drop with the costs of that feature since the costs are incurred anyway resulting in a cost increase of the other features involved. A related problem is that the assignment of component costs to individual features in order to enable pure feature based costing will result in an attempt to minimise the costs for the individual features, while the overall costs will not necessarily be minimised. To overcome these problems (Wierda, 1991) suggests the use of high-level features. Considering the remarks about component costs, these high-high-level features have to include the component and the assembly. It is therefore sufficient to calculate the costs on the product levels on which they occur without assigning them to the feature level or any other lower level.

For assembly, batch, order and facility level the same remarks about the costs (except the material costs) on component level apply. For the costs on assembly, batch and order level usually a direct relation exists with one of the product levels and therefore these costs can be allocated to a product level relatively easy. The relation between the costs on facility level and product level is usually not straightforward and has to be defined explicitly, see section 2.5.2.

2.4.2 Variant based cost estimation

For manufacturing companies, the increasing diversity of customer’s demands has led to high product variety. If high product variety is not taken into account in the product development cycle, it will result in inefficient manufacturing. Examples of inefficiency are large set-up times, high tooling costs, large work-in-progress, large throughput times (Srikantappa, 1994) and complex production planning.

A manufacturing concept that overcomes the problems related to high product variety is group technology (GT). Mitrofanov, one of the first authors to write about GT, defined GT as a technique for manufacturing small to medium lot size batches of parts of similar process, of somewhat dissimilar materials, geometry and size, which are produced in a committed small cell of machines which have been grouped together physically, specifically tooled, and scheduled as a unit (Srikantappa, 1994). More recent broad definitions state GT as the technique of applying the same solution to similar problems. Therefore, GT can eliminate duplication and redundancy (Baer, 1985). The essence of GT is the comparison of a new product with products that have been manufactured before. This comparison requires the determination of similarity criteria, which is very important for the proper use of GT. Application of GT in cost estimation, i.e. variant based cost estimation, means that the cost estimate for a product under consideration is based on the actual costs of similar products manufactured before. In this case, the similarity criteria have to be based on cost driving product characteristics.

The automation of GT in an integrated product development cycle using engineering databases is mainly determined by the layout of the engineering databases. It is possible to create an interface between the GT system/database and the other systems/databases or it is possible to maintain duplicate databases (Billo, 1987). From an information management point of view these solutions

are unsuitable, see chapter 3. A better solution would be to map the GT onto the general structure of the engineering database. A general-purpose, relational database is the best alternative in the case of GT (Bill, 1987).

In GT, different approaches can be distinguished: classification, clustering (Kusiak, 1990) and production flow analysis (Agarwal). Classification is the process of grouping parts into families of similar parts; similarity is based on some set of rules and principles (Agarwal, 1994). The families of similar parts are identified by a code, representing similarity criteria of interest. Therefore, coding is the arbitrary assignment of one or more symbols to a part, which, when deciphered, communicates specific meaning or intelligence (Mosier, 1993). Three types of code structures exist (Agarwal, 1994): Hierarchical (monocode) structure Chain (attribute, or polycode) structure Hybrid structure Principle Each character is a

further expansion of the previous character

The meaning of each character is independent of any other character A combination of the monocode and polycode structure Advantages Information can be

represented with a relatively small number of digits

Simple to implement The advantages of the monocode and

polycode structure Disadvantages Complicated and very

difficult to implement

A large number of digits may be required to represent

information

-

Examples DCLASS (Brigham

Young University)

MICLASS (TNO) OPITZ (Opitz),

KAMKODE (Kamrani)

Table 2.5 Code structures (Agarwal, 1994).

In literature, it is generally assumed that no universal method exists for classifying and coding parts (Bear, 1985), (Lewis, 1987), (Agarwal, 1994). Therefore, most research is concentrated on the development of various classification systems to support specific engineering tasks, specific production processes and product types.

Classification can be based on geometrical information. This type of classification is particularly suitable for the support of the designer. In the context of cost estimation, the assumption is made that equal geometry is produced in the same way. This implies that equal geometry will cost the same. This assumption can be refined by considering cost factors like tolerances (Molengraaf, 1993). In the case of equal geometry and equal cost factors, it is more likely that the probable production processes and therefore the costs will be the same. In order to include manufacturability aspects, technological information is incorporated in classification (Lewis, 1987), (Peklenik, 1980), (Wu, 1992), (Luong, 1989). This type of classification is suitable for both process planners and designers. Even for some specific tasks of process planning, classification algorithms can be developed like for fixturing (Nee, 1992).

Examples of classification for specific processes and product types are: sheet metal, die-casting, forming, machining, joining/welding, heat treatment and finishing (Lewis, 1987), (Agarwal, 1994), (Greska, 1995). It is possible to combine multiple processes in one system (Agarwal, 1994).

Advantages of classification related to cost estimation are (Schuttert, 1995):

• Quick retrieval of historic data;

• Improvement and consistency in cost estimation;

• Support in quotation procedures and acquisition of new machine tools. However, classification systems have several disadvantages (Vliegen, 1993):

• Insufficient retrieval chance;

• Dependency on human interpretation;

• Excessive coding effort;

• Lack of flexibility, feedback of the performance and integration with other systems;

Inflexibility is caused by the fact that only a limited set of characteristics is used. These geometrical and technological characteristics, of a selected part range, are chosen empirically and evaluated statistically (Peklenik, 1980).

• Discussions about how to classify and who should classify;

• High investments.

Besides the primary function of classification systems, being basic retrieval of information, classification systems have to be usable for all interested parties within the firm (Mosier, 1993). Coding should reflect the patterns that have emerged in analysis and be compatible with the company’s other systems (Bear, 1985).

Clustering is the process of grouping similar objects based on a similarity coefficient (Agarwal, 1994). A similarity coefficient represents the similarity between two objects and usually ranges form 0 to 1. Different characteristics can be used for the calculation of a similarity coefficient. Four types of similarity coefficients are usually distinguished: distance coefficients, association coefficients, correlation coefficients and probabilistic coefficients. Production flow analysis is the process of grouping products based on the sequence of operations. It consists of four steps: factory flow analysis, group analysis, line analysis and tooling analysis (Agarwal, 1994).

From the description of clustering and production flow analysis, it can be concluded that both methods are very similar to classification. Clustering can be seen as temporary classification with only one part family. Only the objects with a sufficiently high similarity coefficient constitute the part family for the object under consideration. This means that the part family to be used is created every time the part family is needed. Therefore clustering is more adaptable and flexible than classification. Production flow analysis can be seen as classification, in which the creation of part families is based on the sequence of operations.

2.4.3 Hybrid cost estimation

Both variant based and generative cost estimation can be applied at the same time for one product resulting in a hybrid cost estimation. In the development cycle of products, it can occur that different parts of a product will be in a different phase of the product development cycle. Therefore, the available information of different parts of the product will be different. When the costs of different parts of a product are calculated in a different way, the total product costs can be calculated by summing the costs for the different parts. When different cost models are used, a prerequisite is that the calculation of the overhead costs is carried out in the same way. If the overhead costs are calculated in a different way, it can occur that some overhead costs are counted more than once or that some overhead costs are excluded.

In order to ensure a consequent calculation of the overhead costs, an aggregated product information structure and cost structure is required. Only in that case, it is possible to store the way the overhead costs are calculated and on which aggregation level the overhead costs are calculated.

2.5 Cost

modelling

Cost modelling represents the determination of the data, ground rules, assumptions and equations that permits the translation of resources or characteristics into costs (Stewart, 1995a). The most common steps in cost modelling are:

1. Determination of the scope, i.e. the costs subdivided in different types, which have to be modelled.