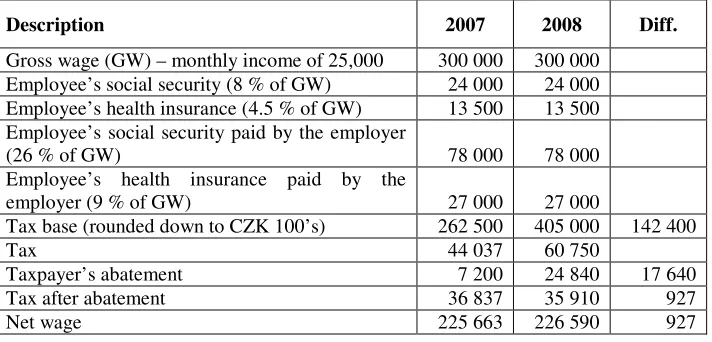

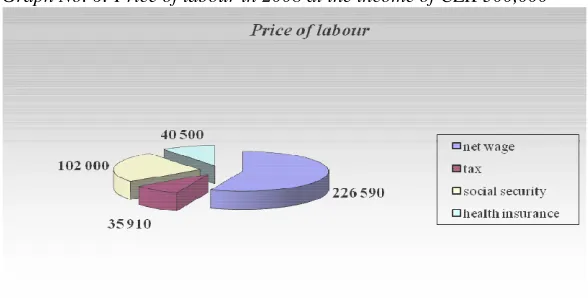

Reform of Income Taxes as a Part of Public Budgets Stabilisation

Full text

Figure

Related documents

$1,000 Grant in support of the AAF Competition Team from the Oklahoma City Advertising Club, March, 1998; February, 1999; February, 2000, March, 2001 $1,100 Grant from the

greater flexibility in handling uncertainty.. SENTIMENT CLASSIFICATION OF DRUG REVIEWS This section describes the major modules of the framework developed for sentiment

With different perceived intensity, all the export barriers such as government policy, human resource, financial, product quality, marketing knowledge and information,

Because of the delay in data releases for state claims, the insured unemployment rate used in the model represents a partial month (the average of two-three weeks of data); for

“THAT subject always to the Companies Act, 1965, and the approval of the regulatory authorities, the Directors be and are hereby empowered, pursuant to Section 132D of the

In this chapter, two cases were studied. In case 1, the real-time reliability for a radial system was calculated based on the converter model and the transformer model. In case 2,

( 4.4) has a solution in the set of stable rational transfer matrices. Indeed, the following result was essentially proved by Bengtsson [12]. High Gain Feedback.

The Company will reimburse the Insured Person for reasonable essential expenses incurred up to $50 per 12 hour period and for such amount incurred above the excess, for the