Kicking Maturity Down the Road:

Early Refinancing and Maturity Management in the Corporate Bond Market

Qiping Xu*∗†

June 9, 2015

Abstract

This paper studies debt maturity management through early refinancing, in which firms si-multaneously retire their outstanding bonds before the due date and issue new bonds as re-placements. Speculative-grade firms frequently refinance early to extend the maturity of their outstanding bonds, particularly under accommodating credit supply conditions. In contrast, investment-grade firms do not manage their maturity similarly. I exploit the timing of the protec-tion period of callable bonds to show the maturity extension is not driven by unobservable firm characteristics or interest-rate conditions. The evidence is consistent with precautionary matu-rity management, in which speculative-grade firms extend matumatu-rity to hedge against refinancing risk caused by credit supply fluctuations.

∗I am grateful to my advisors Douglas Diamond, Zhiguo He, Anil Kashyap, Gregor Matvos, and Amir Sufi for their

invaluable input. I would also like to thank Stephen Kaplan, Kelly Shue, and Michael Weisbach, as well as seminar participants at the University of Chicago, the Fama Miller corporate finance reading group, the London Business School Trans-Atlantic Doctoral Conference, Cheung Kong Graduate School of Business, Hong Kong University of Science and Technology, Georgia Institute of Technology, Notre Dame University, and University of Colorado at Boulder. Research support from the Deutsche Bank and Bradley Foundation is gratefully acknowledged; any opinions expressed herein are those of the author.

1

Introduction

Debt maturity has been shown to affect real firm behavior: firms whose long-term debt was largely maturing right at the time of the recent financial crisis cut their investment more than otherwise similar firms (Almeida et al. [2012]). In surveys, CFOs claim they manage debt maturity to “reduce risk of having to borrow in bad times”(Graham and Harvey [2001]) . However, there is very little evidence about how they do this or about which firms see this as a first order concern.

In this paper, I examine how firms manage debt maturity through early refinancing, in which firms simultaneously retire their outstanding bonds before the scheduled due date and issue new bonds as replacements. Early refinancing is a common practice that involves hundreds of billions of dollars each year in the corporate bond market. Previous studies mainly attribute early refinancing to firms’ desire to reduce interest expenses: for example, firms retire their outstanding bonds and issue new ones at cheaper rates when credit supply conditions are good.1 I identify a number of patterns that suggest speculative-grade firms frequently refinance early to extend debt maturity, in order to avoid having to issue when credit supply conditions are bad.

First, the majority of speculative-grade firms’ bonds are refinanced before their due date. When re-financing early, speculative-grade firms issue new bonds with longer maturity to extend the maturity structure. In contrast, only a small fraction of investment-grade firms’ bonds are refinanced early. When investment-grade firms refinance early, they replace expensive bonds with cheaper bonds of similar maturity. Early refinancing does not change the maturity structure of investment-grade firms. Second, aggregate credit supply conditions dictate early refinancing of bonds and hence the maturity structure of debt. Speculative-grade firms take advantage of favorable credit market conditions to refinance early on a large scale, resulting in a procyclical debt maturity structure. They refinance early 10%–15% of total outstanding bonds during good credit periods, such as 2004–2005 and 2010-2011, but only about 2% during credit market downturns. The maturity structure moves closely with early refinancing for speculative-grade firms—it extends significantly when firms substantially refinance early, and shortens when early refinancing dries up. Investment-grade firms, in contrast, refinance early only 1%–2% of total outstanding bonds even during good credit periods. Their maturity structure is insensitive to early refinancing.

Third, bursts of early refinancing for speculative-grade firms have investment consequences. Fol-lowing early refinancing and maturity extension, speculative-grade firms increase investment. In

1Merton [1974], Brennan and Schwartz [1977], Vu [1986], Mauer [1993], Longstaff and Tuckman [1994], Acharya

contrast, early refinancing by investment-grade firms has no impact on subsequent investment activ-ities.

I interpret the results through the lense ofprecautionary maturity management. Refinancing during credit market downturns, when credit is expensive or unavailable, can be costly: firms might have to refinance at significantly higher rates, sell assets in a fire sale, reduce investment, etc. Refinanc-ing risk motivates precautionary maturity management, where forward-looking speculative-grade firms frequently “kick maturity down the road,” particularly during favorable credit periods. The longer maturity structure reduces the possibility of being forced to refinance during credit market downturns, allowing speculative-grade firms more flexibility to invest. Investment-grade firms do not manage their maturity in the same way as they are less exposed to refinancing risk.

In the first half of the paper, I estimate the causal impact of early refinancing on maturity extension for speculative-grade firms. The task is difficult because of firms’ endogenous choice of early refi-nancing and maturity. For example, firms that choose to refinance early might desire longer maturity because of investment opportunity changes. Within-firm analysis suffers from dynamic versions of the similar endogeneity concerns. When a firm chooses to refinance early, it might experience in-vestment opportunity changes or face a downward-sloping yield curve because long-term interest rates are low compared to short-term rates. Omitted variables may bias the OLS estimates of the impact of early refinancing on maturity.

As an identification strategy, I exploit variation in the callable structure of corporate bonds. Firms commonly embed call provisions when issuing bonds, entitling them to call bonds during a defined period at prespecified prices. Call provisions have two important features. First, they make early refinancing easier for firms. Bond holders have to return the bonds when firms call. Also, when lower interest rates are available, the value of outstanding bonds increases and firms may transfer the value from bond holders to themselves by exercising the call. The value transferred essentially makes calls a subsidized way to refinance early. Second, a call provision comes with a protection period, defined as the period during which a firm cannot call the bond. This provides bond holders with a guaranteed length of time during which they will be able to hold the bonds and receive promised coupon payments. The standard practice is to set the protection period to last 50% of maturity at issuance: for example, a 10-year bond normally has a 5-year protection period. The fact that protection periods are standard in length and decided upon well in advance creates essentially exogenous variation in the ease of early refinancing.

protection period. I instrument firms’ early refinancing activities with a dummy variable indicating some bonds are scheduled to pass the protection period and become callable in a given firm-year. Bonds turning callable creates early refinancing opportunities that are not plagued by endogeneity concerns. Identification requires that the timing of when bonds become callable is uncorrelated with current unobservable factors that make firms demand longer maturity. The lengthy and standard pro-tection period plays a key role in this identification strategy, as it is unlikely that future movements of the unobservables, such as investment opportunities or the yield curve, would coincide with when bonds become callable.

The second method builds on the fact that credit supply conditions are a key driver of firms’ early refinancing and maturity extension. I instrument early refinancing activities with the interaction term between their callable fraction of outstanding bonds and credit supply conditions. The idea is that firms with higher fractions of callable bonds should be more sensitive to credit supply improvements in their early refinancing. Identification requires that firms with higher fractions of callable bonds receive larger shocks to their early refinancing ability when credit supply conditions improve, but their demand to adjust maturity due to unobservable factors is similar to that of firms with lower fractions of callable bonds.

Both instrumental variable designs deliver similar estimates of the impact of early refinancing on maturity. For speculative-grade firms, a one–standard–deviation (30%) increase in the probability of early refinancing leads to a more than 10% increase in the fraction of book debt with maturity

≥5 years, and to more than a one year extension in the average maturity for outstanding bonds. I also find that a one–standard–deviation (30%) increase in the probability of early refinancing is followed by a 1.2% higher CAPX/PPE ratio, which represents a 5.7% increase compared to the average CAPX/PPE level. In contrast, investment-grade firms do not extend maturity through early refinancing, and we do not observe changes in their subsequent investment activities.

I conduct several robustness tests to ensure the validity of the instrumental variable strategies. First, firm-years with and without bonds turning callable, or firm-years with low and high fractions of callable bonds, are statistically comparable in common financial characteristics. Second, summary statistics show that the protection periods are commonly set to be 50% of maturity at issuance for speculative-grade firms. Third, regression tests confirm that firm financial characteristics and interest-rate conditions at issuance do not affect the duration of the protection periods, ruling out concerns over firms’ endogenous choice of protection periods. Fourth, I conduct the intention-to-treat (ITT) test for the IV regressions, assuming all the bonds in the speculative-grade sample have protection periods set at exactly 50% of maturity at issuance. The IV regression estimates remain

similar.

The second half of the paper focuses on the precautionary maturity management hypothesis. Two factors expose speculative-grade firms to greater refinancing risk, driving them to conduct more precautionary maturity management. First, speculative-grade firms rarely issue bonds longer than ten years, which suggests a credit supply constraint on maturity at which they can issue. This constraint leads to significant maturity mismatch between the assets and liabilities of speculative-grade firms, forcing them to frequently tap the capital markets for refinancing. Second, changing credit supply conditions disproportionately affect the financing costs of speculative-grade firms. While financing costs remain relatively stable for investment-grade firms over a credit cycle, they increase sharply for speculative-grade firms during credit market downturns. To mitigate refinancing risk, speculative-grade firms synthesize long-term bonds via early refinancing when credit supply conditions are favorable.

I present evidence consistent with the precautionary maturity management hypothesis. Firms that are more exposed to refinancing risk should have a greater incentive to manage maturity in advance. I test this intuition in two ways. First, I group speculative-grade firms based on the degree of maturity mismatch between their assets and liabilities. Given that we do not observe the maturity of firms’ assets, I use investment-grade firms in the same industry as a benchmark, assuming they are able to issue longer bonds that better match the maturity of their assets and liabilities. I rank industries based on the difference in maturity at issuance between the investment-grade and speculative-grade bonds. Speculative-grade firms in industries with greater maturity mismatch do extend maturity more via early refinancing.

Second, I study the timing and candidate selection of firms’ early refinancing activities. Speculative-grade firms rarely wait until the due date to refinance their bonds. For these firms, less than 10% of the refinancing happens around the scheduled due date, whereas the fraction is over 70% for investment-grade firms. When refinancing early, speculative-grade firms tend to replace bonds with shorter maturity, but do not pay much attention to the yield-to-maturity of their bonds. Investment-grade firms behave in the opposite way: they target more expensive bonds, but do not take the maturity dimension into account.

The remainder of the paper proceeds as follows. Section 2 reviews the relevant literature. Section 3 describes the data and summarizes the characteristics of bonds and firms in the sample. Section 4 summarizes early refinancing activities and contract term changes through early refinancing, as well as provides institutional background for call provision and the protection period. Section 5

estimates the causal impact of early refinancing on maturity extension by exploiting variation in the callable structure of corporate bonds. Section 6 interprets precautionary maturity management and provides supportive evidence. Section 7 discusses the relationship between precautionary maturity management and other forms of internal liquidity holdings. Section 8 concludes.

2

Literature Review

This paper contributes to the existing literature on debt maturity, refinancing risk, early refinancing, and credit supply conditions. I briefly explain how it compares and contrasts with the leading papers in each of these areas.

Most previous studies on corporate debt maturity focus on firms’ desire to match the life of their assets and debt (Modigliani and Sutch [1966], Myers [1977], Vasicek [1977], Graham and Harvey [2001]), or the cross-sectional relationship between firms’ characteristics and corporate debt matu-rity (Diamond [1991, 1993], Barclay and Smith [1995], Rajan and Winton [1995], Guedes and Opler [1996], Diamond and Rajan [2001], Johnson [2003], Berger et al. [2005], Benmelech [2008]). In many leading models, maturity is treated as a stationary process, whereby firms commit to a station-ary maturity structure (Leland and Toft [1996], He and Xiong [2012]). Baker et al. [2003] and Chen et al. [2012] study how interest rate conditions and business cycles affect firms’ choice of maturity at issuance. My paper emphasizes the time–series dynamics of maturity, and the important roles that early refinancing and credit supply conditions play in determining maturity structure. It also highlights that firms across rating segments manage their maturity very differently, and suggests the importance of studying the impact of ex-post refinancing and credit ratings on the ex-ante choice of maturity at issuance.

Previous studies highlight different aspects of refinancing risk: some firms might have to refinance at significantly higher rates (Froot et al. [1993]), experience excessive liquidation by creditors (Di-amond [1991]), sell assets in a fire sale (Choi et al. [2013], Brunnermeier and Yogo [2009]), suffer increasing default risk (Leland and Toft [1996], He and Xiong [2012]), or be forced to decrease investment (Almeida et al. [2012]). Brunnermeier and Yogo [2009] show that firms minimize re-financing risk by their choice of maturity at issuance. They show that short-term re-financing allows a firm that is in good financial health to adjust its maturity structure more quickly in response to changes in asset value. However, they do not consider the possibility of early refinancing. Acharya et al. [2011] show how refinancing risk can reduce the collateral value of a security. He and Xiong

[2012] show that firms face refinancing losses from issuing new bonds to replace maturing bonds when debt market liquidity deteriorates. The surge in refinancing losses can cause the firm to default at a higher fundamental threshold, which may feed back to worse bond market illiquidity as in Mil-bradt and Oehmke [2014]. In practice, rating agencies commonly cite refinancing risk as a reason to downgrade firms,2and they also upgrade firms that successfully refinance.3 Whereas Harford et al. [2014] suggest increasing cash holdings as a way to mitigate refinancing risk, my paper presents maturity extension through early refinancing as a way to hedge refinancing risk.

This paper adds a new dimension to the literature on the early refinancing of corporate bonds. Re-searchers mainly attribute early refinancing to firms’ desire to reduce interest payments: when yields drop, firms retire their outstanding bonds and issue new ones at the less expensive prevailing rate (Merton [1974], Brennan and Schwartz [1977], Vu [1986], Mauer [1993], Longstaff and Tuckman [1994], Acharya and Carpenter [2002], Jarrow et al. [2010]). My paper shows that, particularly for speculative-grade firms, early refinancing also serves to help manage debt maturity.

This paper is also related to several studies demonstrating that capital market segmentation and credit supply conditions significantly influence observed financial structure and corporate behavior (Faulkender and Petersen [2006], Leary [2009], Sufi [2009b], Tang [2009], Lemmon and Roberts [2010], Chernenko and Sunderam [2012], Erel et al. [2012]). These studies differ from much of the existing capital structure literature, where capital supply is assumed to be perfectly elastic and capital structures are determined solely by corporate demand for debt. I add to this line of research by showing that the effect of credit supply conditions disproportionally impacts speculative-grade firms, and maturity is an important channel.

A closely related empirical paper is Mian and Santos [2011], who show that creditworthy firms try to actively manage the maturity of syndicated loans in normal times. Liquidity demand then becomes countercyclical for these firms because they choose not to refinance when liquidity costs rise. In contrast, my paper shows that weaker firms are those that display a procyclical pattern in early refinancing and maturity extension in the corporate bond market.

2On April 25, 2014, Moody’s Investors Service downgraded Black Elk Energy Offshore Operations LLC’s (BEE)

Probability of Default Rating (PDR) from Caa2-PD to Caa3-PD. BEE’s tight liquidity and heightened refinancing risk prompted these actions. BEE’s 13.75% notes will become due December 1, 2015. Without a substantial improvement in operating performance and cash flows, the company will be challenged to refinance this debt.

3On October 07, 2010, Moody’s Investors Service upgraded the ratings on West Corporation’s (West) existing senior

secured term loan from B1to Ba3 and the rating on $650 million of existing senior notes due 2014 from Caa1 to B3 upon the closing of its recent refinancing transactions.

3

Data and Sample Statistics

The Mergent Fixed Income Securities Database (FISD) is a comprehensive database of publicly offered US bonds. FISD includes the majority of corporate bonds and provides details on bond issuance and the issuers. Beginning in April 1995, FISD began tracking changes in the outstanding amount of publicly traded corporate bonds. Thus, in addition to the characteristics of the bonds at issuance, FISD contains a detailed history of changes in the amount of bonds outstanding. FISD records the actions,4the effective dates of the changes in the amount of bonds outstanding, the exact amount changed, and the remaining principal balance afterward.

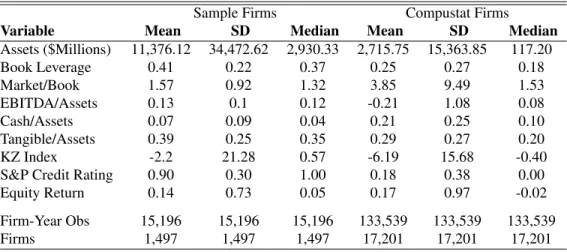

I merge the FISD data with other information from Compustat, Capital IQ, and Bloomberg.5 The final data set contains information on bonds outstanding for a firm in a given fiscal year, including bond characteristics and contract terms at issuance, yield-to-maturity, type and dollar amount of actions taken for the outstanding bonds, and the principal amount remaining after these actions. To be included in the sample, a firm has to have at least three consecutive annual observations with public bonds outstanding. The final sample includes 1,497 nonfinancial US firms and 15,196 fiscal year observations starting in 1996. The sample covers 31,640 bonds. From the Federal Reserve, I obtained the BAA-AAA spread, constant maturity Treasury rates, and effective yields on different rating indexes.

In Panel (a) of Table 1, I compare sample firms with all non-financial firms in the Compustat database during the same time period (1996–2011).6,7 Relative to the average Compustat firm, sample firms tend to be larger, more profitable, have higher leverage, and are more likely to have an S&P long-term issuer credit rating. These differences are not surprising given given sample firms can issue corporate bonds. Panel (b) presents sample firm distribution across industries.8 Although non-uniform, it is quite representative of the overall Compustat distribution. Business equipment and

4Actions, such as calls, tender offers, etc., are defined in Appendix Section A.

5To match FISD information with Compustat data, I use the mapping between entity IDs and GVKEYs provided in

the S&P Ratings database. I first match Mergent IDs to entity IDs in S&P Ratings Xpress via issuer CUSIPs, and then match entity IDs to GVKEYs. In FISD, issuer information is on the subsidiary level at issuance, whereas parent company information is backfilled. Ownership of a bond changes following mergers or acquisitions, meaning the ultimate parent for the bond is different from the original parent. I use the information provided in the issuer notes from FISD, as well as the Thomson M&A database, to identify the precise effective dates of ownership changes.

6To mitigate the impact of outliers and the possible coding errors, I winsorize all ratios at the upper and lower one

percentiles, and apply the winsorization to all the analysis in this paper.

7All variables are defined in Appendix Section B.

8I obtained 12 industry definitions from the Fama French data library, which is available at

healthcare industries have higher percentages in the Compustat sample, whereas the manufacturing industry has a relatively larger composition in the sample data. Comparing the distribution more broadly, there are similar percentages overall, particularly in consumer products and wholesale, retail, & some services. Panel (c) reports summary statistics for 31,640 sample bonds.9 The median offering amount is $100 million, with an average of $224 million. Maturity at issuance has a mean of 10.3 years, with an average coupon rate of 6.60%. Thirty percent of the bonds are rated as speculative-grade at issuance. Almost all bonds have covenants associated with them; the average covenant count is about 4.15.10

4

Early Refinancing and Institutional Background

4.1

Early Refinancing Activities

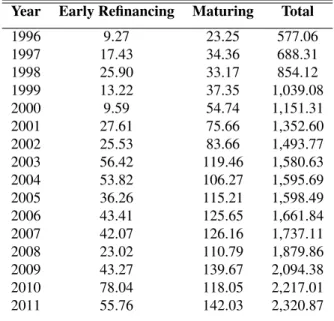

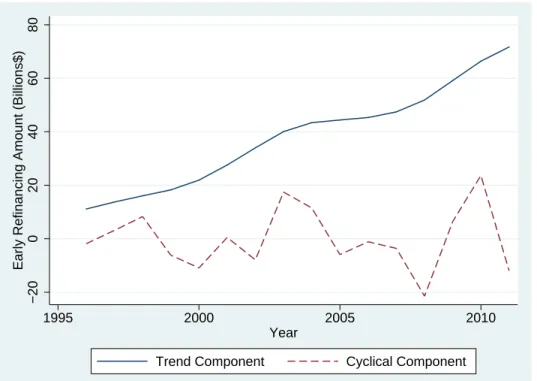

I define refinancing to have occurred if within a three-month time window centered on the month a bond is retired, firms issue other bonds with a dollar amount comparable to the retired amount. Early refinancing refers to the cases in which refinancing happens at least six months before the scheduled due date. Table 2 summarizes the dollar amount of early refinancing, maturing, and total outstanding bonds for sample firms. The total dollar amount of outstanding sample bonds grew from approximately $600 billion in 1996 to roughly $2,400 billion in 2011. The maturing amount trends similarly to the total outstanding amount of sample bonds.

The early refinancing amount is much more volatile: years such as 2000 and 2008 show sharp decreases followed by large rebounds. To better access the time-series variation, Figure 1 plots the early refinancing amount over time. The Hodrick-Prescott filter is applied to separate the cyclical component of the time series from the trend. As shown in Figure 1, early refinancing declines sharply in 2000 and 2008, coinciding with the two financial market crashes of the last decade. Early refinancing activities peak in 1998, 2004–2005, and around 2010.

The procyclical pattern in early refinancing is even stronger for the speculative-grade firms. As shown in Figure 2 panel (a), speculative-grade firms early refinance 10%–15% of total outstanding bonds during good credit periods, such as 2004 and 2010, but less than 2% during credit market downturns. Speculative-grade firms display a strong procyclical pattern in their early refinancing

9Contract terms are defined in Appendix Section C.

activities. In contrast, investment-grade firms consistently refinance early only 1%–2% of total outstanding bonds.

4.2

Early Refinancing and Maturity Extension

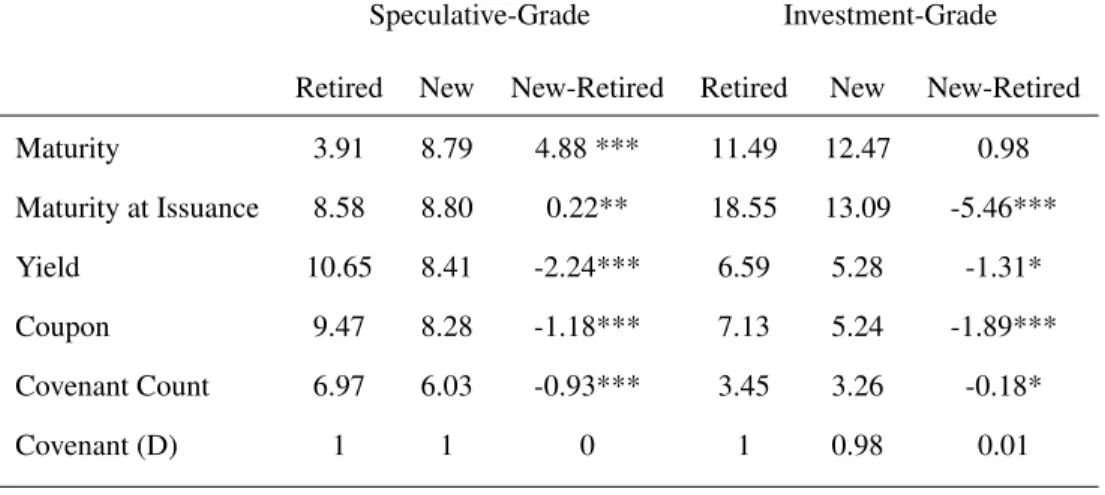

For every early refinancing case, I match the early-retired bond to the newly-issued bond and exam-ine the differences. The tests are presented separately for the investment-grade and speculative-grade firms in Table 3. The table shows that both types of early refinancers obtain cheaper rates, which is consistent with the existing literature on early refinancing. There is also some reduction in covenant strictness. Table 3 presents a new fact: speculative-grade firms get a significant extension in matu-rity, whereas investment-grade firms simply issue new bonds with a similar maturity.

Speculative-grade firms extend maturity from 3.91 years to 8.79 years. Investment-grade firms’ ma-turity moves from 11.5 years to about 12.5 years, which is statistically indistinguishable. Speculative-grade firms do not appear to adjust the maturity which they issue at, because the retired bonds and the new bonds have maturity at issuance of 8.6 and 8.8 years. Investment-grade firms shorten the maturity at issuance from 18.55 years to about 13 years.

In terms of interest payments, both groups replace more expensive bonds with cheaper ones. The average yield-to-maturity decreases by 2.24% for speculative-grade firms and 1.31% for grade firms. The coupon rate decreases 1.18% for speculative-grade firms, and 1.89% for investment-grade firms. For covenant strictness, speculative-investment-grade firms get a drop of about one covenant through early refinancing: the covenant count decreases from 6.97 to 6.03. Investment-grade firms experience a drop in covenant count from 3.45 to 3.26 . There are no significant changes in the covenant dummy.

Maturity extension through early refinancing, along with the procyclical early refinancing activities of speculative-grade firms, explains the time–series correlation between early refinancing and firms’ maturity structures in Figure 2 panel (b). Speculative-grade firms’ maturity structures extend signif-icantly when they conduct early refinancing on a large scale in 2004 and 2010. When speculative-grade firms’ early refinancing activities drop sharply in years such as 2000 and 2008, their maturity structure shortens correspondingly, leading to the procyclical maturity structure. A similar correla-tion between early refinancing and firms’ maturity structure for investment-grade firms is not found.

4.3

Institutional Background: Call Provision and Protection Period

In Figure 3, I decompose early refinancing based on methods of redemption. Calls, whereby issuers exercise call provisions to buy back outstanding bonds, are a common method of early refinancing. Tender offers account for the majority of the rest. In 2003–2004, firms called about $30 billion of outstanding corporate bonds, whereas the total amount of early refinancing was around $60 billion. Also, the plot shows the very familiar procyclical fluctuation: call amounts increase sharply in 1998, 2003–2004, and 2010–2011, and decrease during two market downturns in the previous decade. The procyclical call amounts are thus one factor behind the procyclical aggregate early refinancing activity.

Firms commonly pay a higher yield to embed call provisions when issuing bonds. If a call provision is included at issuance, the call schedule, call prices, and protection period are contracted. The protection period is the period during which the company cannot call the bond, starting from the issuing date. It provides the bond holders with a guaranteed length of time for which they will be able to hold the bond and receive coupon payments. For example, Kroger issued a callable 10-year senior debenture on June 15, 1993, with the scheduled due date on June 15, 2003. The embedded call provision states that Kroger would be able to call the debenture starting June 15, 1998, five years after the issuance day, with a price of $104.25. The call price decreased to $102.834 on June 15 1999, to $101.417 on June 15, 2000, and finally to $100 on June 15, 2001. The 5-year protection period is 50% of maturity at issuance. In my sample, 89.4% of speculative-grade firms’ bonds have call provisions. The protection period setting is fairly standard: a 10-year bond typically has a 5-year protection period, whereas a 7-year bond typically has a 3.5-year protection period.

06/93 Issuance Protection Period 06/98 104.3 06/99 102.8 06/00 101.4 06/01 100 06/03 100

Call Schedule for Kroger 10-Year Senior Debenture

Call provisions are advantageous tools for early refinancing. First, they facilitate early refinancing because bond holders have to return the bonds upon calling. In tender offers and repurchases, bond holders retain the right to not respond. Second, when a lower interest rate is available, either be-cause of a drop in the prevailing market rate or bebe-cause of better firm performance, the value of

an outstanding bond increases correspondingly. If the discounted value exceeds contemporaneous scheduled call prices, firms transfer values from bond holders to themselves by calling outstanding bonds at scheduled prices. The value transferred essentially makes calls a subsidized way to refi-nance early. Early refinancing conducted through tender offers, repurchases, and make-whole calls does not result in similar value transfers. Firms need to pay at least the market prices in repurchases, and typically plus some premium in tender offers, to induce bond holders to comply. A make-whole call is even more expensive because all the future coupons have to be paid at a discount rate close to the Treasury rate. However, if a bond is not yet callable because of the protection period, the firm can only conduct early refinancing through tender offers, repurchases, or make-whole calls.

5

The Causal Impact of Early Refinancing on Maturity Extension

5.1

Identification Goal and Challenge

The descriptive statistics show the correlation between speculative-grade firms’ early refinancing activities and maturity extension. However, estimating the causal impact of early refinancing on ma-turity extension remains difficult. The biggest challenge comes from endogeneity concerns. Firms that choose to refinance early might be those experiencing investment opportunity changes. If new long-term projects are coming up and firms want to issue long-term bonds to match the life of their assets and liabilities, the maturity extension observed would be an outcome of maturity matching for new projects. Moreover, within-firm analysis suffers from dynamic versions of the same endogene-ity concerns. When a firm chooses to refinance early, it might experience investment opportunendogene-ity changes or face a downward–sloping yield curve because long-term interest rates are low compared to short-term rates. Omitted variables making firms demand longer maturity may bias the estimates of the impact of early refinancing on maturity.

To estimate the causal impact of early refinancing on maturity extension, the ideal experiment is to randomly assign speculative-grade firms the ability to refinance early. If speculative-grade firms want to extend maturity by early refinancing, firms more able to conduct early refinancing are ex-pected to extend maturity by a larger magnitude than firms less able to conduct early refinancing. A randomly assigned ability to refinance early would rule out the concerns over the potential unob-servables driving firm demand for longer maturity.

matu-rity extension for speculative-grade firms. The idea is to look for a shock to early refinancing ability, which is uncorrelated with the contemporaneous confounding factors. The protection period of the call provision provides a great setting.

5.2

Timing of the Protection Period

My first instrumental variable strategy exploits the timing of the protection period. I instrument early refinancing activities with a dummy variable indicating that some bonds are scheduled to become callable for firm i in year t. The intuition is that bonds turning callable facilitate early refinancing, while because protection periods are fairly standard in length and decided upon well in advance, the shock is disconnected from unobservable determinants of maturity.

Consider two otherwise identical firms, A and B, that both issued a 10-year bond with a 5-year protection period. Firm A issued the bond five years ago, and the protection period ends in year t. Firm B issued the bond three years ago, and the protection period is not yet over. In year t, the timing of the protection period puts firm A in a better position to refinance its outstanding bonds and extend maturity. Firm B is constrained in its ability to refinance early, because the outstanding 10-year bond is not yet callable. Although firm B can use other methods, such as tender offers or repurchases, those methods might not be as desirable.

The following is the IV strategy 1 specification:

Maturityi,t=δ0+δ1D(Early−re f id )i,t+δicontrolsi,t+εit 2nd stage

D(Early−re f i)i,t=β0+β1D(turn−callable)i,t+βicontrolsi,t+ei,t 1st stage

1993 0 .. .. 96 0 97 0 98 1 99 0 00 0 .. .. 2003 0

Turn Callable Indicator for Kroger 10-year Senior Debenture

Here,D(turn−callable)equals one if some outstanding bonds are scheduled to pass the protection period and become callable for firm i at year t. Take the Kroger 10-year senior debenture as an

example. The turn-callable indicator for this debenture switches to one in 1998, and remains zero for all the other years, leading toD(turn−callable) =1 for Kroger in year 1998. Early refinancing

activity is indexed byD(Early−re f i), a dummy equals one if firm i refinances early at year t. The

exclusion restriction requires that the instrument D(turn−callable)i,t only relates to the outcome

variableMaturityi,t through its effect on early refinancing. The identification assumption is that the

timing of some bonds schedule to become callable is uncorrelated with current unobservables that might lead firms to adjust maturity. Protection periods are fairly standard in length and decided upon well in advance. Therefore, future movements of the unobservables, such as the investment opportunities or the term structure, are unlikely to coincide with the timing of the call schedule. Firm characteristics and interest rate conditions are controlled in the regressions. Firm characteristic controls include Ln(Assets), book leverage, EBITDA/Assets, Cash/Assets, Tangible/Assets, Mar-ket/Book, and S&P rating. Ln(Assets) measures a firm’s ability to collateralize the debt and also captures the liquidation value in a distressed state. Leverage captures a firm’s financial health. Mar-ket/Book is used to measure future investment prospects. EBITDA/Assets and Cash/Assets measure a firm’s profitability and short-term liquidity. Tangible/Assets measures the pledgeability of assets. I include the S&P rating as a general control for a firm’s default risk. Interest rate controls include the risk-free rate (3-month T-bill), term spread (10-year corporate bond yield minus 1-year corporate bond yield), and BAA-AAA credit spread. To control for time-unvarying unobservables that might also affect the firm’s maturity choice, I first-difference all the variables.

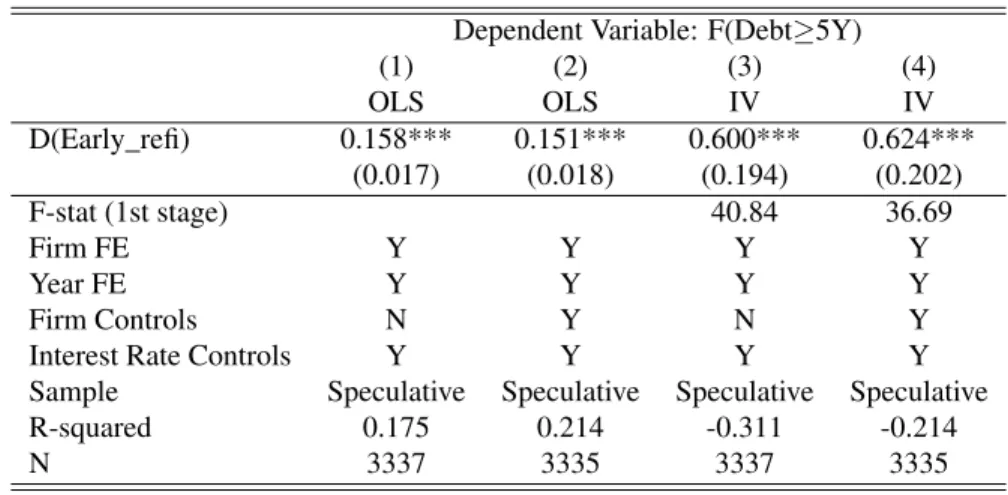

5.2.1 Timing of the Protection Period: Results

Table 4 presents the IV regression first-stage results in panel (a) and the reduced-form regression results in panel (b). I use two measures to capture early refinancing activities: the first one is a dummy D(Early-refi) indicating whether firm i conducted early refinancing activities in year t; the second one is F(Early-refi), which measures the fraction of the total amount of outstanding bonds undergoing early refinancing for firm i in year t. I also use two variables to measure firms’ maturity structure: the fraction of total book debt with maturity≥5 years, which captures the overall maturity structure of firms’ book debt, and the average bond maturity, which measures the maturity structure of corporate bonds. In panel (a), the first-stage shows strong results for both indexes of early refi-nancing activities. In terms of economic magnitudes, the dummy indicating some bonds becoming callable increases the probability of early refinancing by 7.9% and the fraction of early refinancing by 2.3%. In panel (b), the instrument is strongly correlated with both maturity measurements in

reduced-form regressions after controlling for other firm characteristic and interest rate variables. Table 5 panel (a) shows the regression results withF(debt≥5Y)as the outcome variable, and panel (b) shows the regression results with average bond maturity as the outcome variable. Both tables present the estimates from the OLS regressions (column 1 without firm characteristic controls and column 2 with firm characteristic controls), and the IV regressions (column 3 without firm character-istic controls and column 4 with firm charactercharacter-istic controls) with D(Early-refi) as the instrumented variable. OLS estimates are positive, and adding firm characteristics appears to have little effect on the coefficients of early refinancing. In IV regressions, the Kleibergen-Paap Wald F-stat for the weak instrument test is much larger than ten, which is the rule of thumb for identifying a weak instrument. IV regressions show early refinancing leading to a larger fraction of book debt with maturity ≥5 years, as well as a longer average bond maturity. In terms of economic magnitudes, the estimates indicate that a one–standard–deviation (30%) increase in the probability of early refinancing leads to a 10.4% increase in the fraction of book debt with maturity≥5 years and a 1.3 year extension of average bond maturity. Including firm characteristic controls has little impact on the IV estimates, indicating that the instrumental variable is not correlated with the observable firm characteristics. There are a few possible explanations for IV estimates being larger than the OLS estimates in Table 5. First, when a firm chooses to refinance early, it might have short-term projects coming up or face a steeper yield curve because short-term interest rates are low compared to long-term rates. That would result in firms’ demand for short-term maturity, leading to a downward bias in the OLS coefficients. Second, IV regressions estimate the local average treatment effect (LATE) on firms responding to the shock, whereas OLS regressions estimate the average treatment effect (ATE) for all sample firms. Firms that respond to the instrument are more likely to be eager for maturity extension, leading to a stronger effect of early refinancing on maturity.

5.2.2 Timing of the Protection Period: Robustness

I conduct a few robustness tests to support the validity of the identification assumption. First, I tabulate firm characteristics by separate firm-year observations according to D(turn−callable)i,t.

Internet Appendix Table 1 presents a summary for these two groups and two sample t-tests. Most measures including the Market/Book ratio, the profitability, the liquidity position, growth opportu-nities, the K-Z index, and the payout ratio are similar between firm-years with or without bonds be-coming callable. The only variables showing statistical differences are asset size and book leverage. However, the standard errors for asset size and book leverage are 1.12 and 0.22 for

speculative-grade firms. Compared to the standard errors, the magnitude of differences is not significant. In Internet Appendix Table 2, I conduct a within-firm characteristic comparison conditional on D(turn−callable) switching from 0 to 1. All the observable firm characteristics are statistically

indistinguishable when the instrumental variableD(turn−callable)switches from 0 to 1.

Second, there might be concerns regarding the endogenous choice of protection period: firms might foresee the future movements in firm fundamentals or market interest rates and set the protection period to coincide with their projection. Internet Appendix Figure 1 presents the distribution for the period ratio for bonds issued by the sample speculative-grade firms. The protection-period setting is indeed fairly standard with small variations. In the speculative-grade sample, the average protection period is 49.7 months, with a standard deviation of 11.2 months. The protection period ratio on average is 48% of maturity at issuance, with a standard deviation of only 6.6%. Third, I regress the protection–period setting on various bond characteristics, firm characteristics at issuance, and interest rate controls at issuance. The dependent variable is the ratio of the protection period to maturity at issuance. For example, if maturity at issuance is ten years and the protection period lasts five years, the protection-period ratio is 50%. Internet Appendix Table 3 shows that the protection-period ratio is uncorrelated with either contemporaneous firm characteristics or interest rate controls. The evidence is consistent with the protection period being set in a standard way to be about 50% of maturity at issuance, which alleviates concerns over the endogenous choice of the protection–period setting.

Lastly, I conduct the intention-to-treat (ITT) test for the IV regressions, assuming all the bonds in the speculative-grade sample have protection periods that last 50% of maturity at issuance. Internet Appendix Table 4 and Internet Appendix Table 5 present the results under the ITT assumption. The first-stage shows strong results for both indexes of early refinancing activities, while IV second-stage regressions show early refinancing leading to a larger fraction of book debt with maturity≥5 years, as well as a longer average bond maturity. In terms of economics magnitudes, the results are similar to the IV regressions without ITT assumption.

5.3

Sensitivity to Credit Supply Conditions

My second instrumental variable strategy explores the fact that credit supply conditions greatly in-fluence a firm’s ability to refinance early. I instrument firms’ early refinancing activities with the interaction between the callable fraction and credit supply conditions. Given that callable bonds

make early refinancing easier, firms with more callable bonds receive a larger shock in their early refinancing ability when the credit market improves. The larger shock leads to more early refinanc-ing and maturity extension.

Consider two otherwise identical firms, A and B, that both issued some 10-year bonds with 5-year protection periods. Firm A issued these bonds five 5-years ago and assume 80% of the bonds outstanding are callable. Firm B issued similar 10-year bonds two to three years ago, so none of its outstanding bonds are callable yet. When credit supply conditions improve, firm A is able to refinance early a larger fraction of its outstanding bonds, whereas firm B is constrained in its ability to take advantage of credit supply improvements.

The IV strategy 2 considers the following specification:

Maturityi,t=δ0+δ1D(Early−re f id )i,t+δ2β∗F(callable)i,t+δ3∗BAA−AAA+δicontrolsi,t+εit 2nd stage

D(Early−re f i)i,t=β0+β1F(callable)i,t∗BAA−AAA+β2∗F(callable)i,t+β3∗BAA−AAA+βicontrolsi,t+ei,t 1st stage Here,F(callable)it =total−callableamount−−amountoutstandingi,t−1i,t−1, andD(Early−re f i) equals one if firm i refinances

early at year t. I use credit spread BAA-AAA to capture credit supply conditions. Credit spread increases sharply during credit market downturns, and decreases during good credit market periods. The callable fraction and credit spread BAA-AAA are included both in the first- and second-stage regressions as controls. The exclusion restriction requires that the interaction term,F(callable)i,t∗

BAA−AAA, only relates to the outcome variable,Maturityi,t, through its effect on early

refinanc-ing. The identifying assumption is that firms with higher fractions of callable bonds receive larger shocks to their early refinancing ability when credit markets improve, but their demand to adjust maturity because of unobservables remains similar to firms with lower fractions of callable bonds. In other words, firms cannot foresee future credit supply conditions and set the call structure to take advantage of them. The fact that protection periods are fairly standard in length and determined well in advance plays an important role in this identification strategy.

Given that the callable fraction and credit spread BAA-AAA are not excluded instruments, I do not assume the choice to embed call provisions is random. Firms with different fractions of callable bonds likely have different propensities to conduct early refinancing. However, conditional on the

fraction of bonds that are callable, the improvements in credit supply conditions will have a greater effect on firms with more callable bonds. Those firms are in a better position to conduct early refinancing and lengthen maturity. By using the interaction term as an instrument, I explore only the variation of credit supply shocks through the callable structure. Firm characteristics and interest rate controls are the same as in IV strategy 1.

5.3.1 Sensitivity to Credit Supply Conditions: Results

Table 6 presents the IV regression first-stage results in panel (a), as well as the reduced-form re-gression results in panel (b). I use the same measures to capture firms’ early refinancing activities and maturity structure as in IV strategy 1. In panel (a), IV first-stage shows strong results for both indicators of early refinancing. In terms of economic magnitudes, a one–standard–deviation drop in the instrument, which is the interaction between the callable fraction and BAA-AAA, increases the probability of early refinancing by 4.6% and increases the fraction of early refinancing by 3.5%. In panel (b), the instrument is also strongly correlated with both maturity measurements in reduced-form regressions after controlling for other firm characteristics and interest rate variables.

Table 7 panel (a) shows the regression results with F(debt ≥5Y) as the outcome variable, while panel (b) shows the regression results with average bond maturity as the outcome variable. OLS es-timates are both positive; adding firm characteristics appears to have little impact on the coefficients of early refinancing. In IV regressions, the Kleibergen-Paap Wald F-stat for the weak instrument test is again much larger than ten. IV estimates show stronger effects than do the OLS estimates: early refinancing leads to a larger fraction of book debt with maturity≥5 years, as well as a longer average bond maturity. In terms of economic magnitudes, the estimates show that a one–standard– deviation (30%) increase in the probability of early refinancing leads to a 21.2% increase in the fraction of book debt with maturity≥5 years and a one-year extension of average bond maturity. The magnitude is qualitatively similar to the results from IV strategy 1.

5.3.2 Sensitivity to Credit Supply Conditions: Robustness

To support the validity of the identification assumption, I first tabulate firm characteristics by their callable fractions. To confirm that firms are comparable even though their callable fractions might vary, for each year, I separate speculative-grade firms into two groups. If the callable fraction for firm i is greater than the median callable fraction within the speculative-grade segment in year t,

firm i is put into the high group. Otherwise, I put firm i into the low group. Internet Appendix Table 6 presents a firm characteristic summary for these two groups and two sample t-tests results. Asset size, profitability, liquidity position, growth opportunity, K-Z index, and payout ratio are all similar between firms with high and low callable fractions. The only variables showing statistically different values are book leverage and Market/Book ratio. The standard errors for book leverage and Market/Book ratio are 0.22 and 0.56, respectively, for the speculative-grade firms. Compared to the standard errors, the magnitude of differences is small. Moreover, I include these factors in the instrumental variable regressions as controls.

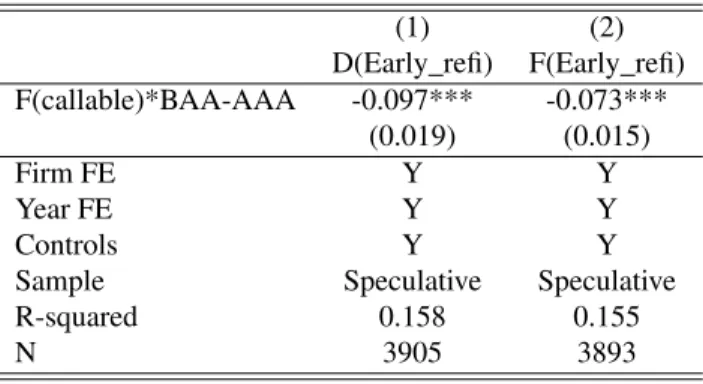

I am agnostic about what drives the variations in credit supply conditions. The drivers could be the countercyclical variation in the economy-wide prices of risk, or mispricing due to investor biases in evaluating credit risk, or investor sentiment. Instead of trying to disentangle or quantify those theories, I take the variation in aggregate credit supply conditions as given and study firms’ reactions. As a robustness check, I use two other measures of credit supply conditions. The first is the excess bond premium (EBP) from Gilchrist and Zakrajšek [2012], which is a credit spread measure purged of default risk. An increase in the excess bond premium reflects a reduction in the effective risk-bearing capacity of the financial sector and, as a result, a contraction in credit supply. IV estimates with EBP are presented in Internet Appendix Tables 7 and 8 . The second is the high-yield fraction, which is the fraction of new corporate issuance that are rated to be speculative. Greenwood and Hanson [2013] show that a decline in issuer quality is a reliable signal of credit market overheating. IV estimates with high-yield fractions are presented in Internet Appendix Tables 9 and 10 . Both measures generate similar results. The use of different indexes to capture credit supply conditions serves as robustness checks for the validity of results.

I also perform a similar IV regression by using the interaction term betweenD(turn−callable)and

BAA-AAA as the instrumental variable. The identifying assumption is that firms with or without bond(s) scheduled to become callable do not differ in their responses to credit market improvements other than through their early refinancing activities. Internet Appendix Table 11 shows the first-stage and reduced-form regressions. Internet Appendix Table 12 presents the second-stage results of IV regressions, which are of similar magnitude compared to other specifications.

5.4

Heterogeneous Maturity Extension across Credit Ratings

The findings reveal large-scale early refinancing and maturity extension only for speculative-grade firms, whereas investment-grade firms refinance early but do not extend maturity. To show the

heterogeneity in the regression form, I interact the early refinancing activities with D(speculative), which equals 1 if firm i receives an S&P domestic long-term issuer credit rating below or equal to BB+. I run both OLS and IV regressions. In the IV regressions, I interact both the instru-ment and the instruinstru-mented variables with D(speculative). I also dig deeper into the heterogene-ity by comparing speculative-grade firms with shorter maturheterogene-ity to those firms with longer matu-rity. In terms of the regression, I interact early refinancing with D(speculative), and a double-interaction term D(speculative)*D(short). D(short) equals 1 if firm i’s maturity is shorter than the median maturity among all speculative-grade firms in year t-1. In IV regressions, I interact both the instrument and the instrumented variables with D(speculative) and the double-interaction term D(speculative)*D(short).11

Table 8 presents heterogeneity results. Panel(a) displays both the OLS and the IV results with out-come variable F(Debt ≥5Y), whereas panel (b) displays the results with average bond maturity as the outcome variable. The instrument here is the interaction between the callable fraction and BAA-AAA. Both the OLS and IV results show similar results across the two outcome variables. Speculative-grade firms extend maturity through early refinancing, but investment-grade firms do not. Firms with shorter maturity are the most aggressive maturity extenders. In panel (a) columns 3 and 4, the coefficients for investment-grade firms remain insignificantly different from zero. In col-umn 3, the coefficient for speculative-grade firms is 0.297 higher than that of investment-grade firms. Within the speculative-grade segment (column 4), firms with shorter maturity are driving the positive results. Panel (b) shows a similar story. In columns 3 and 4, the coefficients for investment-grade firms remain insignificantly different from zero. In column 3, the coefficient for speculative-grade firms is 2.406 higher than that of investment-grade firms. Within the speculative-grade segment (column 4), firms with shorter maturity extend maturity significantly more than firms with shorter maturity.

6

Precautionary Maturity Management: Theory and Evidence

6.1

Precautionary Maturity Management: Theory

In Internet Appendix Section F I present a model that captures the essentials of precautionary ma-turity management. The model is set up in an environment with changing aggregate risk aversion,

while the prospect of firms’ long-term projects remains constant. A low-value firm (i.e., speculative-grade firms in the sample) is constrained by the maturity at which it can issue, because its cash flow is too uncertain for risk-averse lenders to hold a long-term claim against it. This leads to maturity mismatch between assets and liabilities, and forces the firm to access capital markets for refinanc-ing. However, refinancing is risky: if aggregate risk aversion increases at refinancing, the low-value firm has to default, which is inefficient from the firm’s point of view because risk-averse lenders undervalue the continuation value of the firm. The optimal choice for a low-value firm is to issue intermediate-term bonds, and refinance early to extend maturity when aggregate risk aversion is low. Essentially, the low-value firm synthesizes a long-term bond by refinancing the intermediate-term bond early and extending maturity. Early refinancing creates value, because it enables the low-value firm to obtain cheap funding, while reducing the probability of default. In contrast, the high-value firm (i.e., investment-grade firms in the sample) has expected payoffs high enough for it to issue a long-term bond matching the duration of the project. They refinance early for lower rates un-der low aggregate risk aversion but do not seek to change the maturity through early refinancing. The graph below shows the maturity outcomes through early refinancing for speculative-grade and investment-grade firms:

Speculative-Grade Firms

Investment-Grade Firms

Figure: Maturity Change through Early Refinancing

In the mechanism outlined above, two factors subject speculative-grade firms to severe refinanc-ing risk, leadrefinanc-ing them to conduct more precautionary maturity management than their investment-grade peers. First, changing credit supply conditions disproportionately affect the financing costs speculative-grade firms face. In Figure 4, I plot the Bank of America Merrill Lynch US corporate

index for different ratings from 1997 to 2013. This plot highlights the large time-series variation of yields for speculative-grade firms. While yields for AAA, AA, and A ratings remain relatively stable throughout the period, the yields for speculative-grades are highly volatile. Take the C-rated firms as an example: the yield was lower than 15% during normal credit periods and increased to more than 25% around 2001 and 40% during the recent financial crisis.

Second, creditors prefer to keep speculative-grade firms on a short leash for various reasons. For example, short-term debt provides creditors with additional flexibility to monitor managers fre-quently and aligns managerial incentives with that of the creditors (Calomiris and Kahn [1991], Diamond and Rajan [2001]). Short-term debt also enables the transfer of control rights (Hart and Moore [1994]), including the right to liquidate when entrenched managers have no incentive to pull the trigger. Additionally, credit rationing (Stiglitz and Weiss [1981]) leads to maturity rationing (Milbradt and Oehmke [2014]), where lending breaks down beyond a certain maturity because of asymmetric information and adverse selection. Thus, the equilibrium of maturity at issuance is one in which speculative-grade firms are offered at most the intermediate-term bonds.

6.2

Evidence: Maturity Mismatch between Assets and Liabilities

I also collect empirical evidence about speculative-grade firms being screened out of the long-term bond market, a scenario that leads to maturity mismatch in their assets and liabilities. In Figure 5, I plot the distribution of maturity at issuance for speculative-grade and investment-grade firms’ bonds in the sample, with the summary statistics given at the top. The maturity at issuance of speculative-grade firms is highly clustered: the average maturity at issuance is 8.7 years, with a standard deviation of 2.3 years. In fact, about half of the bonds are issued with maturity around 10 years, and about 40% are issued with maturity around 7 years. Speculative-grade firms rarely issue bonds longer than 10 years, and the maximum maturity is 30 years. They only issue a few bonds shorter than 7 years. In contrast, the distribution for investment-grade firms is much more spread out: the average maturity at issuance is 11.1 years, with a standard deviation of 10.2 years. Investment-grade firms commonly issue bonds longer than 10 years, and the maximum maturity can reach 100 years.12 They also often issue short-term bonds with maturity shorter than or equal to 5 years, accounting for almost 40% of the total issuance.

12For example, the Walt Disney Company issued senior debentures in 1993 that are due in 2093—the so-called

Not issuing long-term bonds does not prove the maturity mismatch between assets and liabilities. Speculative-grade firms might only invest in relatively short-term projects, which matches the ma-turity structure of their bonds. Documenting the mama-turity of investment projects is empirically chal-lenging due to not having access to the underlying characteristics. To provide supportive evidence, I plot the distribution of maturity at issuance for speculative-grade and investment-grade firms’ bonds for the oil, gas, and coal industry in Internet Appendix Figure 3 and the telephone and television industry in Internet Appendix Figure 4, with the summary statistics shown at the top. The idea is that firms in these two industries normally have long-term assets, and asset life across rating seg-ments should not be significantly different. If there is still a difference in maturity at issuance for their bonds, the differences are more likely to come from the constraint in maturity at issuance, not the length of the underlying investment projects.

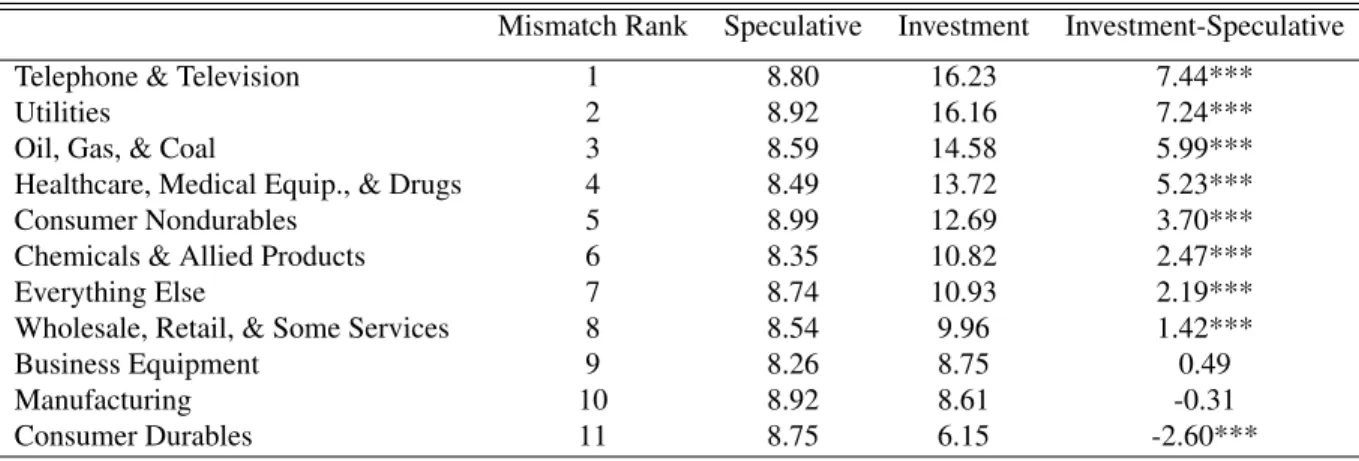

For these two industries, investment-grade firms’ maturity at issuance becomes longer compared to the full sample investment-grade firms. The 25th percentile, median, and 75th percentile for the full sample investment-grade firms are 5, 9, and 12 years, respectively. For the oil, gas, and coal industry, the 25th percentile, median, and 75th percentile become 7, 10, and 20 years, respectively. For the telephone and television industry, they are 5, 10, and 30 years, respectively. Both of these industries issue larger fractions of bonds longer than 30 years. In contrast, speculative-grade firms in these industries still have a maturity-at-issuance distribution similar to the full sample of speculative-grade firms. The 25th percentile, median, and 75th percentile remain at 7, 9, and 10 years, respectively. They again rarely issue bonds longer than 10 years, and the maximum maturity is 20 years for the oil, gas, and coal industry, and 30 years for the telephone and television industry. This evidence favors the maturity mismatch between assets and liabilities in the speculative-grade segment. Firms with larger maturity mismatch between assets and liabilities are more exposed to refinancing risk. We expect them to have a greater incentive to conduct precautionary maturity management. To test the heterogeneity across this dimension, I rank all eleven industries according to maturity mis-match between assets and liabilities. Given that the maturity of firms’ asset side is not observable, I use the investment-grade firms as a benchmark, assuming they are relatively unconstrained in matu-rity at issuance and match the matumatu-rity of their assets and liabilities better. The matumatu-rity-mismatch measure is the difference in maturity at issuance between the investment-grade and speculative-grade bonds in an industry. Table 9 panel (a) presents the industry rankings, where a lower rank number indicates a larger maturity mismatch. Industries with the largest maturity mismatch are utilities; telephone and television; oil, gas, and coal; and healthcare, medical equipment, and drug. Those industries with the smallest mismatch are wholesale and retail; business equipment; manufacturing;

and consumer durables. Rankings are aligned with the general consensus of the asset life for listed industries.

Table 9 panel (b) presents the IV regressions of early refinancing activities on two maturity mea-sures. The IV regressions are run separately for industries with the smallest maturity-mismatch measure (rank 8–11) and largest maturity-mismatch measure (rank 1–4). Firms with smaller ma-turity mismatch (columns 1 and 3) are less exposed to refinancing risk and demonstrate a smaller response in maturity extension via early refinancing. For outcome variableF(Debt≥5Y), the coef-ficient for smaller maturity-mismatch firms (rank 8–11) is 0.095 which is not statistically significant, whereas the coefficient for larger maturity-mismatch firms (rank 1–4) is 0.480, which is statistically significant at the 1% level. For the average bond maturity outcome variable, the coefficient for less mismatched firms is 0.058, which is not statistically significant, much smaller than the 3.592 for more mismatched firms (rank 1–4), which is statistically significant at the 5% level. The IV results support the concept that firms with larger maturity mismatch between assets and liabilities, that is, firms that are more exposed to refinancing risk, extend maturity more through early refinancing.

6.3

Evidence: The Timing of Refinancing

If firms are worried about the possibility of not being able to refinance maturing debt, they would likely consider early refinancing. The precautionary maturity management hypothesis predicts that speculative-grade firms will deal with the maturing principal amount earlier than their investment-grade counterparts.

Figure 6 shows the ratio of time passed when refinanced, over maturity at issuance. The figure includes only bonds that are refinanced. The figure includes a total of 9,604 refinancing cases. If maturity at issuance is 10 years and the bond is refinanced at the end of the its sixth year, the fraction of elapsed maturity at refinancing is 60%. I denote this as an instance of early refinancing. If a firm refinances a bond at the scheduled due date, the fraction of elapsed maturity at refinancing is one, and I denote this case as an instance of refinancing at maturity. I plot the distribution for both speculative-grade firms and investment-grade firms to explore the heterogeneity across these two credit segments. Maturity-at-issuance distributions for bonds refinanced before maturity and refinanced at maturity are shown at the top.

Figure 6 shows that the majority of speculative-grade firms’ bonds are refinanced before the due date; less than 10% of refinancing cases occur at the due date. The largest chunk of refinancing

happens after a bond reaches the middle of its maturity at issuance. In contrast, investment-grade firms refinance the majority of their bonds -over 70%- at maturity. I also compare the maturity at issuance for bonds refinanced at maturity with bonds refinanced before maturity. For speculative-grade firms, the maturity at issuance is similar across both groups. For investment-speculative-grade firms, bonds refinanced at maturity tend to be short-term bonds: their average length is 5.67 years. On the other hand, bonds refinanced before maturity tend to be long-term bonds: their average length is 16.79 years, which is significantly longer than the refinanced-at-maturity group.

The timing of refinancing across speculative-grade and investment-grade firms fits the different ex-posures to refinancing risk. Financing costs for investment-grade firms are relatively stable through-out good or bad credit supply conditions; hence firms can simply wait until the due date and then roll over. For speculative-grade firms, financing costs are volatile. Unable to foresee what would happen at the due date, speculative-grade firms are concerned about refinancing risks and prefer to refinance before the due date. In fact, Bank of America Merrill Lynch makes a recommendation to speculative-grade firms:“Don’t wait too long to refinance upcoming maturities. Give yourself at least 18 months before your current financing matures, so that if any segment of the market shuts down for a few months, you’ll still have time to get something done.”13 HSBC in May 2010 rec-ommended the following:“Truly global investment-grade corporations have time to arrange their refinancing. [Less highly rated companies] should be taking action now, while yields are low and margins compressed.”14

6.4

Evidence: Which Bonds do Firms Refinance Early?

If maturity extension is a major goal that speculative-grade firms desire to achieve, maturity should be a good predictor of the bonds that firms target for early refinancing. Does shorter maturity make a bond more likely to be refinanced early than others bonds? Does firm credit worthiness matter in this setting?

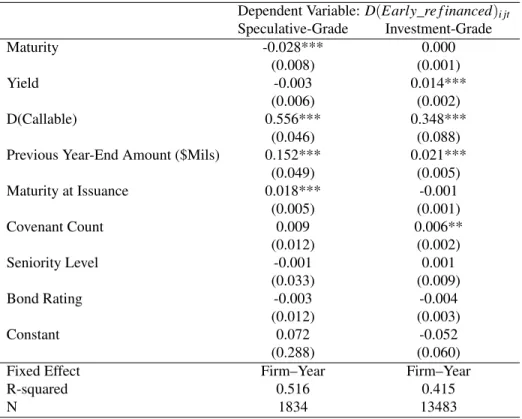

To answer these questions, I run the following regression for speculative-grade firms and investment-grade firms separately. For bond i for firm j in year t, when firm j conducts early refinancing,

D(Early−re f inanced)i,j,t=α+β∗Maturityi,j,t+θ∗yieldi,j,t+φi∗Controlsi,j,t+ηj,t+εi,j,t (1)

13Bank of America Merrill Lynch: “The shifting sands of maturity walls-mirage or real risk?”

http://corp.bankofamerica.com/documents/10157/67594/Shifting_Sands_of_Maturity_Walls.pdf

Dependent variable D(Early-refinanced) equals one if firm j refinances bond i early in year t, and zero if bond i stays untouched. The coefficient on maturityβ and the coefficient on yieldθ are the focus

here. Given that I include the firm-year fixed effect, the comparison is made among all the bonds outstanding for a given firm-year. The bond characteristics on the right-hand side of the regressions include: a dummy variable indicating whether or not bond i is callable at year t, previous year-end amount outstanding,15maturity at issuance, covenant count, seniority level,16and bond rating at the beginning of year t.

Equation 1 is estimated using a linear probability model. Table 10 presents the results for speculative-grade and investment-speculative-grade firms. Speculative-speculative-grade firms target bonds maturing sooner and do not tie early refinancing to the yield. In contrast, investment-grade firms target bonds with a higher yield when refinancing early but do not specifically consider maturity.

For speculative-grade firms, a one-year decrease in maturity increases the probability of being refi-nanced early by 0.028. Thus, if one bond is five years shorter in maturity than the average maturity of bonds outstanding, this bond is 15% more likely to be refinanced early compared to other out-standing bonds. For these firms, the coefficient on yield is not significantly different from 0. On the other hand, investment-grade firms do not appear to consider maturity when they refinance early–the coefficient for maturity is zero. Instead, they target more expensive bonds: a 1% increase in yield-to-maturity leads to a 1.4% higher probability of the bond being refinanced early. Thus, if a bond has a yield that is 5% higher than the average yield of bonds outstanding, it is 7% more likely to be refinanced early compared to other outstanding bonds.

6.5

Early Refinancing and Subsequent Investment

In this section, I study the impact of early refinancing on investment decisions. I examine one-year-forward investment activities as the outcome variable. CAPX/PPE is used to measure firms’ investment activities following early refinancing. The IV specification is:

CAPX/PPEi,t+1=δ0+δ1D(Early−re f id )i,t+

∑

jδjcontrolsj,i,t+εit 2nd stage

15I use the previous year-end amount outstanding to represent size as the amount outstanding can be different from

the issuing principle amount due to previous retirement activities.

D(Early−re f i)i,t=β0+β1F(callable)i,t∗BAA−AAAt+

∑

jβjcontrolsj,i,t+ei,t 1st stage

Table 11 presents the regression results. In panel (a) both the OLS and IV regressions show signifi-cant positive coefficients between speculative-grade firms’ early refinancing and subsequent invest-ment. Adding firm characteristics increases the explanatory power, but appears to have little effect on the coefficients on early refinancing. In IV regressions, the Kleibergen-Paap Wald F-stat for the weak instrument test is much larger than ten. The IV estimates show a one–standard–deviation in-crease in the probability of early refinancing (30%) leads to a 1.2% inin-crease in CAPX/PPE, which is about a 5.7% increase from the average CAPX/PPE ratio for speculative-grade firms. In panel (b), early refinancing does not appear to change the subsequent investment for investment-grade firms. None of the OLS or IV estimates are statistically different from zero.

Here, I offer an interpretation of regression results aligned with the precautionary maturity manage-ment model presented in Section 6.1. Maturity mismatch and refinancing risk constrain grade firms’ investment activities. After hedging refinancing risk through early refinancing, speculative-grade firms are in a better financial position to invest, leading to an increase in the subsequent invest-ment activities. 17 However, there might be other channels through which early refinancing affects subsequent investment. For example, an interest rate reduction might boost firms’ investment ac-tivities because of a lower cost of capital. Or loose covenants resulted from the early refinancing activities can also contribute to the increase in firms’ subsequent investment activities.

To understand more about the channels through which early refinancing affects firms’ investment activities, I run the similar OLS and IV regressions with interest and covenant strictness as the out-come variables. Internet Appendix Table 13 presents regression results for yield-to-maturity and covenant strictness across investment-grade and speculative-grade firms. For yield-to-maturity in columns 1 and 2, both speculative-grade and investment-grade firms decrease yield-to-maturity on outstanding bonds through early refinancing, with speculative-grade firms showing a larger reduc-tion. For covenant strictness in columns 3 to 6, firms do not exhibit significant covenant loosening through early refinancing. Covenant strictness does not appear to be the major goal that firms want to achieve when they conduct early refinancing. This finding should not be too surprising as bond covenants are generally quite uniform and less restrictive than covenants embedded in bank loans. After excluding covenant strictness, interest saving and maturity extension remain as valid

expla-17Empirically, we cannot measure firms’ investment opportunities; hence, I am unable to ascertain whether the