Best Practices On

Property Tax Reforms

In India

Submitted to

Ministry of Urban Development

Government of India

National Institute of Urban Affairs

I & II floor, Core 4B, India Habitat Center, Lodhi Road New Delhi – 110003;Phone: 91-11-24643284; 24617517

www.niua.org; www.indiaurbanportal.in

i National Institute of Urban Affairs PREFACE

Property tax is one of the most important sources of revenue for urban local bodies in India. The growth in revenue from this source has not been commensurate with the potential due to inadequate policies, legal problems and inefficient administration. Property tax reforms have been a matter of debate in the country for a very long time. Some cities have introduced improvements in property tax assessment and/or administration. These reforms have helped to rationalize the property tax system and increase revenues.

Property Tax reform is one of the mandatory reforms under the Jawaharlal Nehru National Urban Renewal Mission. In this context, present report has reviewed recent reforms in property tax system in ten selected cities India in terms of legal/policy and management issues. The experiences can help to pave the way for improved practices and property tax revenue increase in the country. The major objective of the report has been to learn from these experiences of reforms and suggest guidelines. One of the most important findings of the study is that change in assessment system of the tax is necessary but it has to be accompanied by administrative measures to sustain improvements in the revenues overtime.

We hope the report will be helpful to urban policy makers and professionals implementing property tax reforms in the country.

We wish to express our sincere thanks to Dr. M. Ramchandran, Secretary (UD), Ministry of Urban Development for giving us the opportunity to work on the study.

Prof. Chetan Vaidya Director National Institute of Urban Affairs

ii National Institute of Urban Affairs ACKNOWLEDGEMENTS

The report is an outcome of collective hard work of several individuals. Firstly we wish to express our sincere thanks to Ministry of Urban Development (MoUD), Government of India for supporting the study at such a right time when property tax reforms has become a mandatory reform for ULBs under JNNURM. Special thanks are due to Mr. A.K. Mehta, Joint Secretary (UD) and Ms. E.P. Nivedita, Director (UW & LSG) of MoUD for guiding the study at different stages.

The study has immensely benefited from the guidance, keen interest and patience shown by Prof. Chetan Vaidya, Director, NIUA. His knowledge and expertise in this area added with the positive comments and suggestions he provided towards betterment of the report in every stage, has helped in successful completion of the project. The team is grateful to him. Dr. Mukesh P. Mathur, Professor, NIUA, who was instrumental in initiating this study, has encouraged, supported and worked with the team from the very beginning till the end. The team takes this opportunity to acknowledge his contribution. Many other individuals at NIUA have contributed positively towards the report’s completion; Mr. Sandeep Thakur for clarifying doubts related to municipal finance many a times, deserve special gratitude.

We are grateful to the Municipal Corporations for providing excellent hospitality during our visit to the cities; Officers and the concerned staff of the Revenue and PT department in the cities who have cooperated and provided their valuable time (during detailed discussions in the field visits) as well as data and information for our research (when ever required). We acknowledge with thanks the contribution of our three partners Ms. Manvita Baradi, UMC, Ahmedabad, Shri Vasanth Rao, BBMP, Bangalore and Shri Y Tripathi, KNS Institute, Patna in compilation of the three city reports of Ahmedabad, Bangalore and Patna. A very special thank you is due to Prof. O.P. Mathur, Professor, NIPFP and Shri R. M. Kapoor, Local Governance Synergy, Kolkata, both experts in this field, for patiently going through the draft report and offering valuable suggestions. We would also like to thank Shri K. Dharamrajan for his inputs on our understanding of property tax reforms, and Shri Gangadhar Jha, Advisor, IPE Pvt. Ltd, New Delhi, for his guidance during the project.

Finally the report would not get completed without the immense hard work put in by the core research team members Dr. Rajesh Chandra and Shri Ajay Nigam as well as the other members. Efforts by Shri T. C. Sharma and Ms. Sangeeta Vijh towards editing and formatting the report in the final stages are also appreciated.

We have all been enriched by the experiences gained and shared during this endeavor. We hope the report will contribute in some way towards implementation of property tax reforms in our country in the near future.

Dr. Debjani Ghosh Research Coordinator & Senior Research Officer National Institute of Urban Affairs

iii National Institute of Urban Affairs Advisors Chetan Vaidya Mukesh P. Mathur Coordinator Debjani Ghosh Core Members Rajesh Chandra Ajay Nigam Other Members Naveen Mathur Nilanjana Dasgupta Sur Satmohini Isha Srivastava Ray

Preeti Chauhan Priyam Sharma Computer Team T. C. Sharma Indu Senan Sangeeta Vijh Partners

Urban Management Centre Ahmedabad

Shri Vasanth Rao, Deputy Commissioner (Resources) Bangalore Bruhat Bangalore Mahanagara Palike

Shri Y. Tripathy, Director Patna

K. N. Sahaya Institute of Environment and Urban Development

iv National Institute of Urban Affairs Chapter I Introduction 1-7

1.1 Background

1.2 Overview of Reforms

1.3 Review of Past Efforts

1.4 Objectives of the Study

1.5 Study Methodology

1.6 Outline of the Report

Chapter II Ahmedabad Municipal Corporation 8-20

2.1 City Profile

2.2 Urban Governance

2.3 Overview of Finances

2.4 Existing System

2.5 Assessment System

2.6 Billing and Collection System

2.7 Exemptions

2.8 Benefits from New System

2.9 Use of Modern Technology

2.10 PT in Newly Merged Areas

2.11 Impacts of JNNURM

2.12 Issues

2.13 Replicability and Sustainability

2.14 Lessons Learnt

Chapter III Bruhat Bangalore Mahanagara Palike 21-43

3.1 Introduction

3.2 City Profile

3.3 Urban Governance

3.4 Overview of Finances

3.5 Existing System

3.6 Reforming the Property Tax System

3.7 Appraisal of the Reform

3.8 Benefits of the System

3.9 Reduction of Compliance Cost

3.10 Elasticity 3.11 Transparency

3.12 Administrative Costs

3.13 Horizontal Equity

3.14 Key Benefits and Lessons Learnt

v National Institute of Urban Affairs

8.3 Overview of Finances

8.4 Property Tax System

8.5 Issues

8.6 New Assessment Mechanism

8.7 Impact of JNNURM

8.8 Initiatives/ Innovative Measures

Chapter IV Bhubaneswar Municipal Corporation 44-52

4.1 Introduction

4.2 Urban Governance

4.3 Overview of Finances

4.4 Property Tax System

4.5 Issues, Problems, Suggestions

4.6 Reform Interventions

Chapter V Corporation Of Chennai 53-61

5.1 Introduction-City Profile

5.2 Urban Governance

5.3 Overview Of Finances

5.4 Importance of Property Tax on Revenue Generation

5.5 Existing Property Tax System

5.6 Benefits of New System

5.7 Impacts of JNNURM

5.8 Innovations, Replicability, Sustainability

Chapter VI Greater Hyderabad Municipal Corporation 62-71

6.1 Introduction

6.2 City Profile

6.3 Urban Governance

6.4 Administrative Set Up of Property Tax Department

6.5 Overview of Finances

6.6 Demand and Collection

6.7 Property Tax System

6.8 Issues and Reforms

Chapter VII Indore Municipal Corporation 72-83

7.1 Introduction

7.2 City Profile

7.3 Urban Governance

7.4 Overview of Finances

7.5 Existing Property Tax System

7.6 Benefits of New System

7.7 Impacts of JNNURM

7.8 Innovations/Replicability/Sustainability

7.9 Issues and Problems

Chapter VIII Kolkata Municipal Corporation 84-96

8.1 Introduction

vi National Institute of Urban Affairs Chapter IX Ludhiana Municipal Corporation 97-104

9.1 Introduction

9.2 Urban Governance

9.3 Overview of Finances

9.4 Property Tax System

9.5 Issues and Problems

9.6 Innovative Measures

9.7 Impact of JNNURM

Chapter X Patna Municipal Corporation 105-118

10.1 City Profile

10.2 Urban Governance

10.3 Overview of Finances

10.4 Property Tax System

10.5 Benefits of New System

10.6 Use of Modern Technology

10.7 Impact of JNNURM

10.8 Innovations, Replicability and Sustainability

10.9 Issues and Problems

10.10 Suggestions

Chapter XI Pune Municipal Corporation 119-130

11.1 Introduction

11.2 Urban Governance

11.3 Organisational Framework of the PMC

11.4 Overview of Finances

11.5 Status of Demand and Collection

11.6 Property Tax System in PMC

11.7 Concessions/Exemptions 11.8 Issues

11.9 Reforms under JNNURM

11.10 Innovative Measures adopted for PT Collections

Chapter XII Summary of Findings and Way Forward 131-151

12.1 Context

12.2 Comparison of Findings

12.3 Issues

12.4 Impact of JNNURM Reforms

12.5 Major Guidelines

12.6 Conclusions

Bibliography 152-153 Annexure 154

A1 Recommendations of 13th FC on Property Tax from 13th CFC Report

A2 Some Indicators of Property Tax in Selected Cities

vii National Institute of Urban Affairs Chapter I Introduction 1-7

1.1 Cities and their Assessment Mechanisms

Chapter II Ahmedabad Municipal Corporation 8-20

2.1 Reductions In The Number Of Litigation Cases

2.2 Zone wise demands during the period of 2000-02

2.3 Property Tax Collection vs Demand

Chapter III Bruhat Bangalore Mahanagara Palike 21-43

3.1 Comparison of BMP and BBMP

3.2 Trend of BBMP Revenue Receipts

3.3 Trend of BBMP Revenue Expenditure

3.4 Selected Measures of Property Tax Revenue Performance

3.5 Classification of properties and rental rates: Residential Groups

3.6 Categories of Properties and Zone-Wise Rates: Non-Residential Groups

3.7 Property Tax Revenue in Bangalore City Corporation

Chapter IV Bhubaneswar Municipal Corporation 44-52

4.1 Overview of Income and Expenditure Profile

4.2 Summary of Revenue Account

4.3 Steps to Calculating Annual Value among Property Categories

4.4 Composition of Own Sources of Tax Revenue

4.5 Demand-Collection-Balance of Holding Tax from Government and

Private Properties

4.6 Number of Holdings Assessed

Chapter V Corporation Of Chennai 53-61

5.1 Financial Statement of the Corporation of Chennai 5.2 Tax Revenue Structure of the Corporation of Chennai

5.3 Grades in Annual Values for Tax Calculation

5.4 Demand and Collection of Property Tax

Chapter VI Greater Hyderabad Municipal Corporation 62-71

6.1 Present Scenario of Greater Hyderabad Municipal Corporation

6.2 Taxation Zones

6.3 Municipal Revenue Receipts

6.4 Demand and Collection

6.5 Composition of Property Tax

6.6 Number of Properties

viii National Institute of Urban Affairs Chapter VII Indore Municipal Corporation 72-83

7.1 Financial Statement of the Indore Municipal Corporation

7.2 Percentage of Property tax (PT) to Own Source Revenue and Municipal Revenue Receipts

7.3 Demand and Collection of Property Tax

Chapter VIII Kolkata Municipal Corporation 84-96

8.1 Municipal Revenue Receipts (levied and collected)

8.2 Property Tax features

8.3 Tax Revenue Structure

8.4 Demand and Collection of Property Tax

Chapter IX Ludhiana Municipal Corporation 97-104

9.1 Financial Statement of the Ludhiana Municipal Corporation

9.2 Tax Revenue Structure

9.3 Demand Collection Status

9.4 Selected Measures of PT Revenue Performance

Chapter X Patna Municipal Corporation 105-118

10.1 Income and Expenditure

10.2 Financial Statement

10.3 Tax Revenue Structure

10.4 Structure of ARV for Tax Calculation

10.5 Demand and Collection

10.6 Circle wise number of assessed holding

10.7 Staff Deployment in Property Tax Department

Chapter XI Pune Municipal Corporation 119-130

11.1 Income Statement

11.2 Details of Receipts and Expenditure

11.3 Demand and Collection

11.4 Municipal Corporation Tax Rate

11.5 Number of Properties

Chapter XII Summary of Findings and Guidelines 131-151

12.1 Methods of Assessment

12.2 Factors for Grouping of Properties in Selected Cities 12.3 Basic Tax Rates in Selected Cities

12.4 Status of Computerisation and GIS in Selected Cities 12.5 Status of Self-Assessment in Selected Cities

ix National Institute of Urban Affairs Chapter II Ahmedabad Municipal Corporation 8-20

2.1 Organisational Structure-Billing and Collection

Chapter IV Bhubaneswar Municipal Corporation 44-52

4.1 Organisational Structure, Holding Tax Department

Chapter VI Greater Hyderabad Municipal Corporation 62-71

6.1 Organisational Structure, Property Tax Department

Chapter VII Indore Municipal Corporation 72-83

7.1 Organisational Structure, Property Tax Department

Chapter VIII Kolkata Municipal Corporation 84-96

8.1 Organisational Structure, Property Tax Department

8.2 Calculation of Property Tax

Chapter IX Ludhiana Municipal Corporation 97-104

9.1 Organisational Structure, Property Tax Department

Chapter X Patna Municipal Corporation 105-118

10.1 Administrative structure

Chapter XI Pune Municipal Corporation 119-130

11.1 Organisational Structure, Property Tax Department

11.2 PT System in PMC

Chapter XII Summary of Findings and Guidelines 131-151

12.1 Share of Property Tax to Own Revenue Sources in Cities

12.2 Per Capita Property Tax in Cities

12.3 Share of Property Tax to Total Revenue Receipts in Cities 12.4 Share of Own Source Revenue to Total Revenue Receipts

12.5 Collection Efficiency in Cities

12.6 Per Capita Assessed Property in Cities

x National Institute of Urban Affairs

ALV Annual Letting Value

AMs Assistant Managers

AMC Ahmedabad Municipal Corporation

ARV Annual Ratable Value

AV Annual Value

ATPM Automatic Teller Payment Machine

BBMP Bruhat Bangalore Mahanagara Palike

BCC Bangalore City Corporation

BMC Bhubaneswar Municipal Corporation

BMP Bangalore Mahanagara Palike

CMC City Municipal Councils

CoC Corporation of Chennai

CVS Capital Value Scheme

DMC Deputy Municipal Commissioner

GHMC Greater Hyderabad Municipal Corporation

GIS Geographical Information System

HC High Court

IMC Indore Municipal Corporation

KMC Kolkata Municipal Corporation

LMC Ludhiana Municipal Corporation

MoUD Ministry of Urban Development

MRV Monthly Rental Value

MVC Municipal Valuation Committee

PMC Patna Municipal Corporation

PMC Pune Municipal Corporation

PT Property Tax

RLV Reasonable Letting Value

RWAs Residential Welfare Associations

SAS Self-Assessment System

SFC State Finance Commissions

UAM Unit Area Method

ULBs Urban Local Bodies

xi National Institute of Urban Affairs

Executive Summary

Context: Property Tax (PT) is one of the most important sources of revenue for urban local bodies in India. Theoretically, this tax should be a buoyant source of own revenue as the value of properties rise over time. Legal hurdles and poor administration have made property tax inelastic in most of the ULBs. Inability to de-link property tax from Rent Control Act had also played a crucial role in hampering this process. In this context, the MoUD issued guidelines on Property Tax in 1997.

In the last 10 years, many cities in the country have introduced innovative practices in PT assessment and administration. Reform of the property tax systems is one of the mandatory reforms under the Jawaharlal Nehru Urban Renewal Mission (JNNURM). The mandate under the JNNURM as well as the Standardised Service Level Benchmarks for e-Governance in Municipalities by Ministry of Urban Development (MoUD) emphasizes the need for implementation of on-line system for property tax through a proper mapping of properties using a GIS system. This will enable the ULBs to have a full record of properties in the city and bring them under the tax net, leading to improved collections. In the long run, it will help the ULBs to move towards a more user friendly, simple and transparent property tax system. With a view to documenting the reforms taking place in some of the cities, which may be replicated a best practices, NIUA undertook the study in 10 cities, which has examined the issues causing them.

Selected Cities: The study has covered 10 selected municipal corporations in the country, which are also JNNURM cities- State Capitals and Class I cities. The purpose of selecting the cities is that they are those, which have undergone or are undergoing a system and process change in property tax by highlighting the reform process. They are Ahmedabad, Bangalore, Bhubaneswar, Chennai, Hyderabad, Indore, Kolkata, Ludhiana, Patna and Pune.

Assessment: Patna, Indore, Chennai, Hyderabad, Bangalore and Ahmedabad have introduced unit area assessment system using certain criteria like area, use, location, age, etc. In Ahmedabad, the tax is directly calculated based on certain criteria. Whereas in other cities, the annual value is estimated first and then the tax rate is applied to estimate the tax. Bangalore had introduced area-based system on voluntary basis and has recently taken a decision to introduce capital valuation system. Kolkata and Bhubaneswar have amended their municipal laws to introduce area-based system but have not implemented it as yet. Pune and Ludhiana continue to have the Annual Ratable Value (ARV) system of assessment. In Ahmedabad, one of the benefits after implementing the area based assessment system is that the number of litigations in the last two years has become nil due to increased level of transparency.

Contribution of PT in Revenue Generation: In terms of revenue generation, the figures are fairly self-explanatory. The collection efficiency in 6 of the 10 cities is above 70%. It is low in Indore and Patna. Poor collection in Patna could be attributed to, among others, absence of a strong and integrated database of properties, lack of an effective or committed administration, weak enforcement etc. Higher collections are also directly linked to the rate structure as applied to property categories, higher coverage of assessed

xii National Institute of Urban Affairs properties, efficient monitoring and enforcement mechanism. This is seen in Bangalore, Hyderabad and Pune.

The share of property tax to own source revenue are high in cities like Bangalore, Chennai, Hyderabad, Kolkata, Bhubaneswar and Patna indicating that property tax is the primary source of revenue among tax sources while other tax and non-tax sources are low in these cities. The situation is vice-versa in cities like Ahmedabad, Ludhiana, Indore and Pune where in most cases Octroi being the primary source of revenue, property tax share becomes low.

PT per capita varies between Rs. 81 to Rs. 670. It is highest in Chennai closely followed by Kolkata, Ahmedabad, Bangalore and Pune. It is the lowest in Patna and other cities with relatively low per capita tax rate are Bhubaneswar, Indore, and Ludhiana. Number of properties per 1000 population varies between 400 and 62 in the selected cities. It is the highest in Ahmedabad and the lowest in Ludhiana.

GIS and Mapping: A high quality computerized database of the properties backed by digitized mapping through GIS is seen in Ahmedabad, which tops the list for number of assessed properties per 1000 population, followed by Pune, Indore and Bhubaneswar. Bangalore and Hyderabad, in spite of being two cities who have adopted reforms and undergone system improvements to enhance revenue generation, has moderate to low assessed properties per 1000 population. Efforts for mapping properties using GIS for property tax collection has also led to one of the highest collection efficiency in the city.

Administration: Reforms are taking place in various cities but due to various local circumstances, the implementation is in various stages. The analysis in the cities has shown that there is much to learn from the good practices, which have led to visible system improvements. Bangalore has shown stark increase in percentage of property tax revenue collected, number of assessed properties and per capita tax collection after implementing area based assessment method. A high quality computerized database of the properties backed by digitized mapping through GIS is seen in Ahmedabad, which tops the list for number of assessed properties per 1000 population. Incentivising honest and timely taxpayers with rewards in Hyderabad have also made considerable difference in increased tax recovery. Pune and Chennai have undergone certain administrative reforms, which have led to efficiencies in the system. This also gets reflected in their revenue enhancement. Exemptions are very high in Indore, Ludhiana and Chennai and low in Ahmedabad, Hyderabad and Patna.

Patna was the first city to introduce area-based assessment method but has not been able to sustain the revenues from this source due to poor administration.

Impact of JNNURM: Various steps in the Memorandum of Agreement emphasize the need for: a) proper mapping of properties using a GIS system so that the ULB is able to have a full record of properties in the city and bring them under the tax net b) making the system capable of self-assessment (that is a system which is formula driven and where

xiii National Institute of Urban Affairs the property owner can calculate the tax due); c) rationalize exemptions; and d) improve collections to achieve at least 85% of demand.

Pune has introduced self-assessment system. Bhubaneswar and Kolkata have enabling provisions in the Acts to introduce SAS but have not introduced it. Ahmedabad, Hyderabad, Bangalore, Kolkata and Pune have shown advanced progress in survey and verification of properties through GIS mapping. Increase in number of assessed properties in these cities is also directly related to the survey and mapping. Collection efficiency is highest among the cities in Ahmedabad followed by Chennai, Hyderabad, Bangalore and Pune. Out of 10 cities, coverage ratio in 8 is 80% or above. Among the selected cities, Ludhiana has made least progress in introduction of PT reforms.

The study findings reveal that reforms have, to a great extent helped the cities towards system improvement in property tax. The JNNURM reform agenda has given the cities the impetus required to bring in changes, which will streamline the property tax system and strengthen the revenue base of the cities.

Way Forward

• Change in the PT assessment system is necessary but it should be accompanied by suitable administrative improvement to sustain the reforms.

• Self-assessment should be made mandatory which should be publicized through public notice etc. This will also avoid unnecessary defaults by property owners. In order to detect under assessment in declaration of area, wrong declaration in the usage of properties and wrong declaration on the type of construction, the Corporation should conduct periodic surveys, random sampling of self-assessment forms and cross checking with license data.

• Property survey, mapping and GIS should take place together as a package to ensure full coverage of properties. This should also include reassessment of under assessed properties.

• Computerisation of the property tax system (which is an important component of e-governance reform), should take place in phases beginning with issuing of demand notices, billing, collection and issuing receipts and preparing DCB statements.

• Regular revision of rates is required among all categories of properties as per the prevailing market conditions in the cities.

• Collection system can be improved by making them more users friendly. This can be done by providing payment gateways like web-based system of tax collection using online payment, banks, longer and flexible timings for collection etc.

• Tax enforcement must be a priority. The self-assessed property tax liability should be randomized for inspection. The gross negligence in not conducting verification has resulted in loss of revenue that the Corporation can ill-afford.

1.0 Introduction

1.1 Background

The process of urbanization in India has been emerging immense pressure on infrastructure and services for last many years. Most of the Urban Local Bodies (ULBs) are not able to meet the increasing demand for infrastructure and services due to their slow growth in municipal revenues. Consequent to the abolition of the Octroi in most states of India, the Property Tax (PT) has become the major source of revenue for ULBs. However, the tax yield from this source remained low because of numerous problems: administrative problems, legal issues and corrupt practices. A large number of properties in cities stay outside the tax net due to poor information base and collection efficiencies.

In view of the poor financial condition of the ULBs, it is being recognized that the PT must be made a revenue productive tax instrument through appropriate reform strategy. The last decade, especially the post 74th Constitution Amendment Act, 1992 phase has witnessed considerable interest in PT reform both from the administrative and the taxpayer’s perspectives. Many cities in the country have introduced innovative practices in various areas related to the tax administration, assessment and collection. Under JNNURM, improvement in PT is a mandatory reform. In this context, the study to document best practices on PT reforms in India has been completed.

1.2 Overview of Reforms

1.2.1 Context:

Property tax is one of the most important sources of revenue for urban local bodies (ULBs) in India. Property tax (also called general purpose tax or general tax) is a generic term, which not only include property tax but also include a variety of service taxes and cesses. Service tax includes water tax, sewerage tax, scavenging tax, drainage tax, conservancy tax, education tax, fire tax, education cess and tree cess. This PT tax structure differs from state to state in India and many states have problems related to the fixation of tax base and tax rate, tax assessment, tax collection, tax exemptions, dispute resolution etc. If assessed on the Annual Ratable Value (ARV) of land and building, it may include service taxes on water supply, drainage, street lighting etc.

The ARV system of taxation which is a rent-based rateable valuation system where the annual value or the annual rental value of the property shall be deemed to be “the gross annual rent at which the land or buildings might, at the time of assessment, be reasonably expected to be let from year to year.

Capital value reflects the market’s assessment of the income to be derived from a property in future including income generated by more intensive use of the property. The tax base comprises the assessed value of land and improvements i.e., the value at which a willing buyer and seller would agree in a free market. It follows that the capital value is extremely elastic and the property tax will have a base that will grow with the economy.

The unit area assessment (UAA) system is a simple arithmetical system of calculation of property tax based on covered area of the building and the unit area value or unit area tax for the category (of locality or amenity etc.) in which the premises is located through which it is possible for any citizen to self-assess his property tax and file his return form. (This could also be applied to vacant land)

In the unit area value system the entire city has to be grouped into somewhat homogenous categories for specifying a unit area value. Such groupings could be done taking into consideration factors like average rental value, average capital value of land, quality of physical infrastructure, availability of social and market infrastructure, type of development, economic classes of occupants etc

In principle, the base of the property tax should respond to the increasing value of properties. In practice, there is growing evidence that this tax has not been a buoyant source of revenue. The growth in revenue has not been commensurate with the potential due to inadequate policies, legal problems and inefficient administration (Vaidya.C, 2000). Property tax reforms have been a matter of debate in the country for a very long time. Some cities have introduced improvements in property tax assessment and/or administration.

1.2.2 Legal/Policy Issues:

The ARV method of assessment was one of the most prevalent systems in India. The major legal/policy problem for increasing revenues from property tax was the conflict between the provisions of Rent Control Acts and the assessment of the property tax. Since the linkage with rent control has undermined the revenue generating potential of the property tax, there was a need to de-link property tax assessment from “standard rent” concept of rent control acts. The Government of India had also issued guidelines for property tax reforms in 1997. Some states have introduced the area-based method of tax assessment. Some states like Bihar, Andhra Pradesh, Delhi, Gujarat, and Karnataka have introduced legal reforms in property tax assessment.

1.2.3 Management:

Proper management of the property tax system is as important in improving revenue generation as improving the policy and legal framework of the system. Management consists of public information, identification of properties, computerized record management and collection. Unless all of these aspects are effectively addressed, administrative reform will not necessarily produce a better property tax system with resulting revenue increases. ULBs of Chennai, Hyderabad, Bangalore, Mirzapur, Indore, and Ahmedabad have introduced management improvements in the tax.

These legal or management reforms have helped to rationalize the property tax system and increase revenues. These experiences can help to pave the way for improved practices and property tax revenue increase in the country.

1.3 Review of Past Efforts

Patna was the first city where area based system was introduced. In the city, the constant harassment of house-owners and threats of arbitrary revision of tax rates led to the notification of the Assessment Rules, 1993 (Singh, 1996). These rules sought to eliminate or at least minimize the discretion of those officials concerned with tax collection, especially in matters of tax assessment. The Rules laid down certain definite criteria for assessment of the property tax, which included the particular situation of a land holding; use of the holding; and, the type of construction. The Rules were, however, challenged before the High Court (HC) by a number of concerned parties. The HC invalidated certain rules on the grounds that they violated Article 14 of the Constitution (right to equality). However, the Supreme Court struck down the HC judgment in this regard, saying that the new system was designed with “good intentions.” This particular judgment was perhaps sustained since the new rules were considered to be reasonable, simple and transparent. The question of conflict with the Rent Control Act was not tested because the court stated that this was not a matter that was argued in the lower court and, for this reason, it left this issue specifically unresolved. The total collection rose dramatically in a couple of years as people responded to the low and fair rates. But then it stagnated. Low rates did not improve matters, since compliance remained low. As a result, cases were filed in courts in vested interest (Mathur, 2004).

Hyderabad: A paper on ‘Reforming Property Tax in Hyderabad’ (Mohanty, 2002) presents a critical analysis of the property tax reforms carried out in the city. It provides a number of lessons, some of which are:

Some principles such as close involvement of tax payer, tax service linkage, incentives for filing tax returns, disincentives for non-filing, tax education etc. are important in designing of successful reforms.

Arbitrary adoption of slab rates of tax in the name of elimination of discretion in the levy of tax is not desirable;

Correction of inequities in the tax system can be an important source of enhanced mobilization of PT revenues;

Tax education and organized publicity campaigns to address the psychology of taxpayer are more important than economic factors;

Direct involvement of tax payers in the provision of civic services is a must for better tax compliance and

Tax reforms may need to be pursued in an incremental manner.

In the study, at that time the Self Assessment Scheme of Hyderabad Municipal Corporation had not yet fully realized its potential; yield from PT was improving with corrections of the 20 year old inequities taking place. The revenue from PT would go up significantly if the systematic issues were tackled rather than dealing with traditional economic aspects such as tax rate and tax base.

The paper titled “Fiscal and Distributional Implications of Property Tax Reforms in Indian

Cities” by Somik V. Lall and Uwe Deichmann (2006) has examined the fiscal and distributional

implication of the ongoing and potential assessment reforms in two Indian cities – Bangalore and Pune. The main finding of the paper is that reform efforts that bring assessment of the property tax base closer to market values have significant positive impacts on revenue generation, and do not have adverse consequences in terms of the tax burden faced by the poor. Further, regulations such as rent control significantly impinge on the growth of revenues from the property tax and in fact do not serve the interests of the poor. While current assessment reforms are a good first step towards increasing the performance of the property tax, structural issues such as improved valuation, increasing buoyancy of the tax, and building taxpayer confidence need to be addressed to make these reforms sustainable.

A report prepared by the ICRA Advisory Services on “Assessment of Property Tax Innovation in

Ahmedabad, Bangalore, Hyderabad, and Patna”(2003) looks into the process through which

innovations were adopted in four major cities- Ahmedabad, Bangalore, Hyderabad, and Patna to develop a framework for PT assessment on the basis of the lessons learnt form the innovations. Self-assessment of properties has proved to be useful to remove assessors’ discretion and independent collection mechanism of PT through banks, common utility payment centers has resulted in increased collection etc.

In case of Delhi, the positive aspects of Unit Area Method (UAM) have given a general sense of satisfaction among the tax payers, e.g considerable reduction in the rates of tax particularly for rented, newly purchased or rebuilt properties, substantial relief for disputed cases (pending for many years), simplified procedure with self-assessment and reduced specter of Inspector-Raj. People living in self-owned flats or premises will have to pay less tax under the new system while rented and commercial properties may end up paying more or as much as they are paying now. For ushering in the new system, the New Delhi Municipal Council (NDMC) has amended house tax byelaws and the new system is a modified version of the unit area method applicable to the rest of Delhi governed by MCD.

In Kolkata, the reform from existing system to the unit area based system taking place presently, needs exhaustive in house exercise as well as extensive consultative procedure at different level, collection of data from external and internal sources, analyzing the same, getting first hand experience of other Corporations and at last arrive at policy decision on the basis of consensus (KMC, 2005). A series of administrative changes, identification of properties, necessary action for broadening the tax net, better monitoring, enforcement, introduction of citizen centric system to ease the process of tax assessment and payment as well as legislative changes in the statute of related departments to catalyse the above goals are necessary.

Based on review of various studies, it is concluded that legal and policy innovations in property tax reform relate to de-linking of assessment of annual rental value from provision of standard rent as per the RCA. Specific administrative tasks to help increase revenues from the property tax include simple tax mapping, enumeration, self assessment, improved records management, simplified collection and close monitoring systems. These improvements can be introduced in a phased manner.

Reform of the property tax systems is one of the mandatory reforms under the Jawaharlal Nehru Urban Renewal Mission (JNNURM).. This will enable the ULBs to have a full record of properties in the city and bring them under the tax net, leading to improved collections. In the long run, it will help the ULBs to move towards a more user friendly, simple and transparent property tax system.

Reform of the property tax systems is one of the mandatory reforms under JNNURM as well as the Standardised Service Level Benchmarks for e-Governance in Municipalities by Ministry of Urban Development (MoUD). Both emphasize the need for a) proper mapping of properties using a GIS system so that the ULB is able to have a full record of properties in the city and bring them under the tax net b) making the system capable of self-assessment (that is a system which is formula driven and where the property owner can calculate the tax due); c) rationalise exemptions and d) improving collections to achieve at least 85% of demand.

The 13th Central Finance Commission (CFC) Report, which was released in February 2010, suggested that all local bodies should be fully enabled to levy property Tax (Annex 1). It also recommended that state governments must put in place a state level property tax board which will assist all ULBs to have an independent and transparent procedure for assessing the tax.

1.4 Objectives of the Study

The present study has examined the issues reforming the property tax system in various parts of the country and has suggested guidelines based on the analysis of the present system in the cities as well the summary of issues arising from it under Property Tax reforms. The emphasis has been on the transition, capturing issues such as how the change happened and why the change was successful. Towards this end, the objectives are:

(i) To examine the current practice associated with property tax assessment, which will bring out the problems faced in the present system in the urban local body;

(ii) To analyse the process through which innovations were adopted and the impact of reform measures already put in place in selected cities; and

(ii) To develop a framework or guidelines on PT reforms which will help in ultimately strengthening the revenue base of the urban local body.

1.5 Study Methodology

In the cities selected for the research study, the property tax assessment in Ahmedabad, Bangalore, Bhubaneswar, Ludhiana and Pune is based on demand. However, the self-assessment of property tax is seen in Bangalore, Hyderabad and Pune. The property tax based on unit area is prevalent in Ahmedabad and Bangalore only. The rateable value is the base of Property Tax in Ludhiana, Hyderabad, Bhubaneswar and Pune. The information related to Property Tax in the sample cities may be seen from the table below:

Table 1.1: Cities and their Assessment Mechanism Sl. No. Name of the City Method of Assessment

Basis of Determination: Frequency of revision of Guidance Value (yrs)

1 Ahmedabad Self Assessment & Demand Based

Unit Area Every 4 years (to be done annually shortly) 2 Bangalore Self Assessment &

Demand Based

Unit Area* Once in 4 years

3 Bhubaneswar Demand Based ARV Not revised since

initiation 4 Chennai Self Assessment Unit Area Once in 5 years

5 Hyderabad Self Assessment Unit Area Every 5 years

6 Kolkata Demand Based ARV Every 6 years

7 Indore Self Assessment Unit Area Once in 5 years

8 Ludhiana Demand Based ARV Annual

9 Patna Self Assessment Unit Area Once in 5 years

10 Pune Self Assessment & Demand Based

ARV Annual

Source: ULBs

* To be on capital valuation basis

The study is based both on primary and secondary data. Secondary data sources include Municipal Acts, Annual reports, budgets, and other related documents. Primary data sources include discussions, observations and structured questionnaire.

Based on the above objectives, the study has been conducted in the following stages:

Stage I: The collection of information has been done at various levels. Initially information has

been collected from secondary sources pertaining to the subject for desk review. Following this, information pertaining to current status as well as reform measures adopted in property tax by each of the 10 sample cities has been collected through a questionnaire format sent to them. Data gaps were met by visit to cities through discussions and interviews with officials of the urban local bodies including Commissioners, Additional Commissioner /Chief Manager (Revenue), Assistant Commissioner (Finance), Chief Accounts Officers-Finance and Budget, Chief Assessor-Collector etc.

Stage II: Information collected has been analysed and the merits and demerits of pre and post

reform phases have been compared and highlighted. These have been issues pertaining to statutory provisions, assessment methods, collection mechanism, administrative issues and future recourses.

Stage III: Based on summarisation of findings and conclusions drawn from Stage II, a framework

/ guidelines (prescriptive) on property tax reforms has been suggested as guidance for other ULBs to improve their financial base.

The study has covered 10 selected municipal corporations in the country, which are also JNNURM cities- State Capitals and Class I cities. The purpose of selecting the cities is that they

are those, which have undergone or are undergoing a system and process change in property tax all of which has ultimately enhanced revenue generation. The study has thus endeavoured to highlight the reform process and document these best practices for replication. Documentation of a best practice ideally should have elements such as situation before the initiative, challenges faced by innovators, strategy adopted, results achieved and sustainability, learning and replicability.

UN defines best practices as outstanding contributions for improving the living environment. International committee of the UN considers best practices as successful initiatives which have a demonstrable and tangible impact on improving people’s quality of life; are the result of effective partnerships between private, public and civil societies; are socially, culturally, economically and environmentally sustainable. Best Practices are promoted and used as a means of

Improving public policy based on what works;

Sharing and transferring knowledge, expertise and experience through networking and peer-to-peer learning;

The Second UN Conference on Human Settlements (Habitat II) launched the call of Best Practice as a means of identifying what works in improving living conditions on a sustainable basis.

1.6 Outline of the Report

The report is initiated in the first chapter by giving a background to the property tax issue in our country. The context and need for the study and the various issues related to the property tax system have been explained subsequently. Review of past efforts traces the various studies undertaken in this area, all of which have detailed the various measures taken and to be taken by cities towards improvement in the property tax scenario. The objectives of the present study, the methodology, database and the various stages in the study complete this section.

The next section of the report details the property tax system in the 10 sample cities in ten chapters by elaborating on the present scenario, highlighting the reform measures put in place and the impact of the same on the revenue generation, achievements under JNNURM, the key benefits and the lessons learnt from it.

The final chapter details the summary of findings and the way forward to the study. The comparison of the findings, summarizing of the findings under certain common parameters and the issues arising from it has been elaborated upon after this. Impact of JNNURM reforms in the cities focuses on their status under the reform agenda. The study concludes by giving specific guidelines based on the findings and issues, which would help the ULBs to strengthen their revenue base in the long run.

2. Sewerage Tax. 3. Drainage Tax. 4. Conservancy Tax.

1. The initial drive to increase the properties in the tax net

i d th t i ithi t d h

Major Reforms/ Innovative Measures

Share of PT to own Sources (07-08)

Map

Composition of Property Tax

Share of PT to Total Rev. Rect. (07-08)

1. Water Tax.

Demand and Collection

145 00 150.00

10% 84%

6%

PT Other Tax Receipts Non Tax Receipts

4% 96%

PT

Other Rev. Rect. (Tot. Rev. Rect. - PT)

increased the tax revenue income within two years and has increased steadily since then.

3. AMC has already initiated efforts for mapping the properties using GIS for property tax collection. It plans to start a full fledged GIS powered property tax database by 2009-2010.

Growth in PT Collected Growth in Assessed Properties

4. In 2001-02 when the new area based system was introduced, the number of exempted properties came down drastically from 62% to 28% and the number of litigations has become nil because of increased level of transparency.

2. The property tax was de-linked from the Rent Control Act,

Per Capita Property Tax

100.00 105.00 110.00 115.00 120.00 125.00 130.00 135.00 140.00 145.00 150.00 2005-06 2006-07 2007-08 128.84 130.14 136.70 Collection E fficiency (% ) 10% 84% 6%

PT Other Tax Receipts Non Tax Receipts

4% 96%

PT

Other Rev. Rect. (Tot. Rev. Rect. - PT)

300 400 500 600 2005-06 2007-08 569.97 597.46 0 50 100 150 200 250 300 2005-06 2007-08 200.63 298.73 P rope rt y Ta x (i n Cr or e s ) 0 5 10 15 2005-06 2007-08 10.6 14.1 A ssessed Pro p e rt ie (in L akh s)

2.0

Ahmedabad Municipal Corporation

2.1 City Profile

The Ahmedabad Municipal Corporation (AMC) governs the city of Ahmedabad. AMC is the seventh most populous city as per Census 2001. The AMC’s limits have expanded to almost 464 sq. kms in 2006 and the Municipal Corporation boundary houses a population of almost 50 lakh.

2.2 Urban Governance

AMC was formed in 1950 under the Bombay Provincial Municipal Corporation Act. The main infrastructure services as provided under the Act include a protected water supply, sewerage and storm water drainage, the construction and maintenance of roads, street-lighting, disease prevention and monitoring, solid and liquid water disposal, public transport, and parks and gardens. The city has 54 wards and the city's Mayor is elected for a term of two-and-a-half years. AMC is divided in to 6 zones and 54 wards for better administration. Three corporators are elected from each ward, who in turn elects the Mayor. Executive powers are vested with the Municipal Commissioner, appointed by the Gujarat state government. AMC has forged partnerships with NGOs, private industry, educational institutions and international agencies for enhancing its urban development capacities and for improving municipal service delivery. The Ahmedabad Municipal Corporation has set a unique example of e-governance. The corporation has a tie-up with a private bank, which accepts tax collections from citizens through Internet. The completion and operation of the Sardar Sarovar Project of dams and canals has improved the supply of potable water and electricity for the city. In recent years, the Gujarat Government has increased investment in the modernization of the city's infrastructure, providing for the construction of larger roads and improvements to water supply, electricity and communications. The water supply needs of the city are met mainly from surface water supply through Raska Project, French well in Sabarmati River and from intake wells constructed in Sabarmati River.

2.2.1 Organisation Structure

Any change in the policy structure is always followed by some or the other change in the organisational structure for the implementation of the same. However, in the case of AMC,except for the recruitment of the Assistant Managers (AMs), at the middle level, there has been no significant change in the organisational structure for the assessment and collection of the property tax. In all, a staff of around 350, including administrative staff is active in the property tax department. The specifics are explained in subsequent chapters for assessment and collection. Also, the ward inspector who is in charge of around 5000-6000 properties, in each ward is the one point contact for property tax assessment, billing and collection in his particular ward (Figure 2.1).

Figure: 2.1 Organisational Structure-Billing and Collection, AMC Deputy Municipal Commissioner (Zonal Office) Assistant Tax Collector Deputy Assessor and Tax Collector One for each zone

Assistant Manager (Zonal Office)

Two for each DATC

Assistant Manager (Zonal Office)

Two for each DATC

Divisional Superintendent 2-4 under each Asst.

Manager 1 ward inspector for 5000-6000 properties in each ward 1 ward inspector for 5000-6000 properties in each ward Divisional Superintendent

2-4 under each Asst. Manager

2.3 Overview of Finances

In terms of financial health, the Ahmedabad Municipal Corporation (AMC) is considered to be one of the strongest urban local bodies in India. However, before 1993, AMC was a loss-making urban local body with accumulated cash losses of Rs. 350 million and bank overdraft to the extent of Rs 22 crore. During a deteriorating financial situation in 1994, AMC launched a major effort to strengthen its capacity to develop commercially viable projects. As a result, AMC was able to wipe off the cash losses in just five months, cleared all overdrafts, and became a surplus city by the end of 1994-95. In 1995-96 a surplus of 60 crores and in 1996-97 a surplus of 70 crores was registered by the corporation which helped in leveraging large funds, turn around its financial position and achieve a closing cash surplus of Rs. 2,142 million in March 1999.

Octroi continued to be the major source of revenues of the ULB till November 2008 when the Government of Gujarat abolished it. In this perspective, property tax becomes an extremely important source of revenue for the AMC.

2.4 Existing System

2.4.1 System before the Initiative

The AMC’s system of property tax assessment prior to 2001-02 was very complicated and in many ways irrational. Being based on notional rental value of properties, the assessed values were very low. These could not be revised due to the constraints of the Rent Control Act and related judicial decisions. Consequently, the AMC could only raise the tax rates, which stood at 73% of the annual ratable value in the case of residential properties and 83% for non-residential properties. These high rates had a psychological impact on the property owners, which lowered their willingness to pay the tax.

Another undesirable outcome of the low assessment of property values was that 72% of the total number of residential properties in Ahmedabad and 31% of the commercial properties were exempted from paying the general property tax. There was also enormous disparity between assessment of self-occupied and tenant-occupied properties. The ratio of tax burden was 1: 15 in favour of the former.

The end result of this irrational structure of the property tax system was that people perceived the system to be grossly unfair and non-transparent. It also led to corrupt practices in the tax department of AMC and the system was commonly described as “Inspector Raj”

2.4.2 Present System

Property tax is the second most important source of revenue for AMC. Especially after the elimination of octroi tax, property tax has become a very important source of revenue generation for the corporation.

In order to utilize this source to the maximum of its efficiency, AMC administration understood the deficiencies of the existing system of property taxation and replaced it with an alternative more rational system.

AMC initiated reforms in a phased manner to accommodate and minimize the legal and administrative challenges that are usually attached to reforms of this nature.

In the first phase of reforms, a number of effective steps were taken to increase property tax collection with immediate effect. First, the municipal records of properties were updated and a large number of previously unrecorded properties were added. Next, all existing properties whose assessed value was grossly inadequate were reassessed. Finally, a number of punitive actions were taken against property tax defaulters. These included disconnection of water supply and drainage services; attachment of movable and immovable properties; and occasionally auction of properties for tax recovery.

In the second phase of reforms, the AMC decided to evolve an “area-based property tax system” to replace the existing system based on annual ratable value. The groundwork for the same began in 1999. It was an elaborate exercise involving large-scale survey of properties through out the city and computerization of data. Nearly one million properties were surveyed. Corporation appointed teams of a practicing valuer and a helper who measured the property carried out this survey.

As far as the policy matters were concerned, certain amendments had to be made to the Bombay Provincial Municipal Corporation Act (applicable to Gujarat) to accommodate the new system. Also, AMC became the first Municipal Corporation in India to adopt the amendment.4

This again was a very comprehensive exercise consisting of special task group meetings, brain storming, publication of special notices and bills to the property owners, conducting hearings to receive objections, and piloting the proposed changes through the standing committee and finally seeking an approval of the state government.

The entire process was completed in about two years and the new system was introduced in the second half of 2001-02.

AMC has amended the Act instead of making a permanent change to it, which gives it an option of switching to the old rent based method as well. Thus, property tax can either be collected under Section 129 for Rateable Value based system or under Section 141B for Carpet Area based system.

4

Under the new formula, the property tax is computed by applying a per unit tax rate to the total carpet area of the property and adjusting for location, age, type of use and whether the property is owner or tenant occupied.

2.5 Assessment System

The new assessment mechanism was adopted in the year 1999 through the Gujarat Act 3 of 1999. All the details related to property were computerized by the AMC in the year 1994. Section. 141-B (1) of the 141-BMPC Act, 1949 (amended in Gujarat Act 3 of 1999) provides that property tax shall be levied annually on buildings and lands on the basis of the rate per square meter of the carpet area. Multiplying factors giving weightage for:

Location :( 4 gradations based on land value)

Age :(5 gradations)

Residential Properties: Type of building (5 gradations)

Non-Residential Properties: Use of building (6 gradations)

Occupancy :( Self Owned / Tenant)

Any addition to building treated as separate unit for assessment.

Property Tax = Area X Rate X Location factor X Age factor X Type of building or use factor X Occupancy factor.

Other Rules

a) Minimum – Maximum Rates prescribed by State Govt.

Residential building: Rs.10 to Rs.40 per sq.mt. per year.

Non-Residential building: Rs.20 to Rs.80 per sq.mt. per year. b) Minimum total Property Tax fixed by the State Govt.

Huts: Rs.84

Chawls: Rs.264

c) The Municipal Commissioner authorized to decide location factor based on land value. d) The Municipal Commissioner’s classification cannot be challenged in Court.

Rebate Structure

a) Rebate in certain cases

20 % in case of Govt. buildings

15 % in case of non-water zone area.

20 % for Cellar and other than ground floor in case of other than residential buildings b) Additional Rebate in case of industrial structures

15 % for buildings having Pacca Walls but non-RCC roof

25 % for buildings having enclosed shads with corrugated or iron or cement sheets with non-RCC roof.

35 % for non-enclosed buildings or sheds i.e. open shed with roof

70% for open land used for commercial or industrial purpose.

100 % for open unused land

Updation

In order for the new system to work effectively, it is very important that the property records, and other guidance values are updated at a regular interval.

a) Owing to this, the property records are updated periodically. The last update happened in the year 2004 and currently, a zone wise updating of property records is being carried out. b) The guidance values were last revised in the year 2005 and it is decided that they would be

revised every four years.

c) However, recently the Govt. of Gujarat has adopted the method of revising land value records every year. Hence, frequency of revision of guidance value would be done on annual basis. However for doing so an amendment in the provisions of the BPMC Act will be required to be carried out.5

d) AMC has town planning & development department, which sanctions plans for new building constructions as well as addition/alteration in existing buildings.

e) Moreover, town-planning department issues Building Use Permission to the new constructions. One copy of building plan approval as well as building use permission is sent to Property tax department for the purpose of assessment.

f) Change of ownership / occupation is captured whenever any amendment for taxpayer's details is applied for.

g) Also, the land values are usually identified from the “Jantri” (the year 2000) i.e. the ready reckoner used for the assessment of stamp duty on property transactions.

5

h) Due to the very recent revision of “Jantri”, the new values have not been amended in the property tax bills for year 2008-2009, the new land values are expected to be used from the next billing cycle i.e. from April 2009.

2.6 Billing and Collection System

The property tax bills are raised at the Head Office of AMC for all the properties and are subsequently sent to the zonal offices for collection purposes. The Deputy Municipal Commissioner (DMC) of each zone is responsible for ensuring that the tax is collected on time in each of the zones. Each zone has six collection centers where the assesses are supposed to make the payments. The Chief Assessor and Collector reports on any defaulters to the DMC of each zone who, subsequently sends notices to the defaulters and takes measures as per the provisions of the Municipal Act. Thus, disputes pertaining to the billing and collection of property taxes are resolved at the level of the zonal offices. The Ward Inspector is responsible for hand-to-hand delivery of all the property tax bills for the properties coming under his jurisdiction. Bills go out in April of each year. This is to be paid within 21 days or else 18% per annum is charged as fine. Both the tax paid and tax due details are available on the AMC website by merely entering the tenement number. Collections are largely taken care of at ward level by the Divisional superintendent and Ward Inspectors.

Mode of payment can be through

Cheque

Credit card

Bank- As an innovative approach, AMC has partnered with a private bank (Kalupur Commercial Bank), which gives the citizens an added ease and option to pay their property tax bill at the nearest branch. Thus, bills can be paid at the 24 civic centers in the city and 13 bank branches.

Internet: www.egovamc.com

Recovery measures for default / delay in payment of property tax leads to

Disconnection of water supply connection

Disconnection of sewerage connection

Sealing of property

Auction of property

2.7 Exemptions

Type of Exemption Qualifying

Institution /individual

Revenue implication of exemption

Property Tax exempted by w assigning Zero value to u property

Non - Residential – Religious Pla sanctorum of such places of worsh

In the present property tax system exemption is not given to any type of property except religious places where property tax is exempted only for the area of sanctorum. Such properties have to pay water and sewerage charge. Thus no property is issued a bill of zero demand. Also, for closed and unused building, 3/4 property tax is exempted.

2.8 Benefits from New System

The various initiatives of AMC for increasing property tax revenues have shown impressive results.

The initial drive to increase the properties in the tax net and actions against defaulters produced immediate results. The tax revenue income doubled within two years and has increased steadily since then.

Another major jump came in 2001-02 when the new area based system was introduced.

The property tax was de-linked from the Rent Control Act, which was thought by the citizens as a very complex and irrational method to calculate property tax.

Dispute of assessment was totally removed among old and new buildings.

Self-assessment is possible and hence discretion availed by lower level staff and corrupt practices can be easily curbed.

There are several tangible advantages of the new system. First being, the number of exempted properties came down drastically from 62% to 28%.

The disparity between owner-occupied and renter occupied properties also went down from 1:15 to 1:2.

In addition, there was an increased flexibility in increasing the tax rate every year.

The most impressive of all these being, the number of litigations has become nil because of increased level of transparency.

Table 2.1 Reductions In The Number Of Litigation Cases-AMC

Year 1999-00 2000-01 2001-02

Cases 42378 38500 Nil

Source: Ahmedabad Municipal Corporation

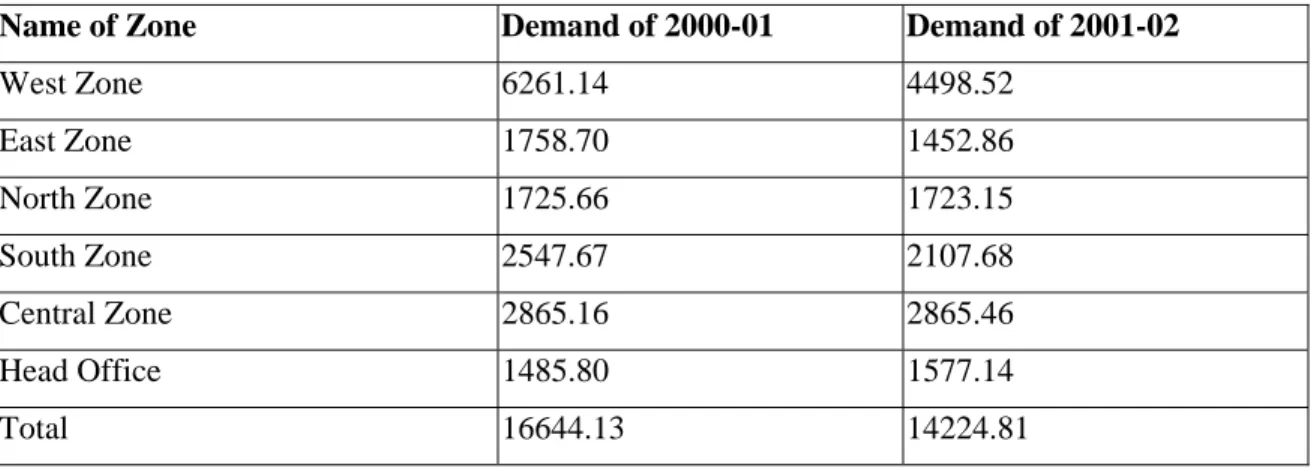

Due to rationalization of the property tax assessment system, the zone wise demand of property tax too went down with the implementation of the new system.

Table 2.2 Zone wise Demands during 2000-02-AMC (Rs in lakhs)

Name of Zone Demand of 2000-01 Demand of 2001-02

West Zone 6261.14 4498.52 East Zone 1758.70 1452.86 North Zone 1725.66 1723.15 South Zone 2547.67 2107.68 Central Zone 2865.16 2865.46 Head Office 1485.80 1577.14 Total 16644.13 14224.81

Source: Ahmedabad Municipal Corporation

2.9 Use of Modern Technology

E-governance as a tool for Self Assessment of Property Tax and an Aid in Billing and Collection has played a very important part in the success of the property tax reforms carried out by AMC and hence, it forms an integral part of the system. In order to provide a very transparent process of assessment of property tax and hence avoid any discretion and litigation, AMC provides a tool on its website. This tool helps the citizens in self-assessment of the property tax on their individual properties by plugging in very basic information. The user friendliness of the website and ease in navigation has made this a widely accepted initiative among the citizens. The following screen shots from the AMC website (www.egovamc.com) illustrate this tool. Apart from this, the citizens can also get the amount of property tax on their property assessed by going to any one of the 25 civic centers. Not only in the assessment of property tax, Egovernance also plays an important role in billing and collection of the same. The tool available on the website also helps in generating the annual bills and keeps the records of bills paid and those that are due. The use of same database throughout the entire system has also lead to increased amount of ease in data maintenance and management.

Apart from these, the AMC has already initiated efforts for mapping the properties using GIS for property tax collection. AMC plans to start a full-fledged GIS powered property tax database by 2009-2010.The city civic centers and Kalupur Bank branches spread throughout the city have gone a long way in ensuring increased convenience to the taxpayers.

2.10 PT in Newly Merged Areas

For the newly merged areas into AMC in 2006, the Gujarat Municipal Finance Board already surveyed most of the properties. This was done under the initiative to implement area based property tax assessment systems in all ULBs of Gujarat. For the municipalities, wherein the survey was not conducted, AMC conducted surveys. It was decided to offer a gradual increase in property taxes to these newly merged areas. If tax calculated as per new formula was more than what the property owners were paying earlier, the owners were given an option of paying the difference over three years time period. 25% of the difference could be paid in the first and second years respectively and remaining 50% of difference could be paid in the third year.

2.11 Achievements of PT reform under JNNURM

2.11.1 Self-Assessment System (SAS)

All the records of property tax in the system have already been placed on AMC website (www.egovamc.com) where any citizen can find out details for not only his property but those of his neighbour also. AMC has also placed a ready reckoner for the calculation of property tax explaining various factor values and calculation thereof. Thus, method of tax assessment is way beyond self-assessment. It is almost an auto-assessment for any property.

2.11.2 Collection Ratio

The collection ratio for last three year (2005-06 to 2007-08) shows increase in the property tax collection after the new carpet area based method adopted by AMC. Last three years figures show that growth in property tax collection is more than 100% of the current demand and with arrears, collection efficiency is also over 70%.

Table 2.3: Property Tax Collection vs Demand-AMC

Type of Property Residential Commercial Industrial Total

* Demand Raised (In Crores) 2005-06

37.43 101.78 16.54 155.75

Demand Collected (In Crores) 2005-06

42.62 134.84 23.17 200.63

% Collected vs demand raised 113.87 132.48 140.08 128.82 *Demand Raised (In Crores)

2006-07

40.89 122.32 18.36 181.57

Demand Collected (In Crores) 2006-07

49.78 158.01 28.43 236.22

% Collected vs demand raised 121.74 129.18 154.85 130.10 *Demand Raised (In Crores)

2007-08

43.12 152.37 23.05 218.54

Demand Collected (In Crores) 2007-08

51.94 215.91 30.88 298.73

% Collected vs demand raised 120.45 141.70 133.97 136.69

Source: Ahmedabad Municipal Corporation

*Note: It may be mentioned that only current demand has been taken into consideration and not arrears.

2.11.3 Coverage Ratio

The coverage ratio for the year 2004-05 was 44% for residential and 38% for industrial and commercial properties. AMC had anticipated the same to be around 70% in the current year.