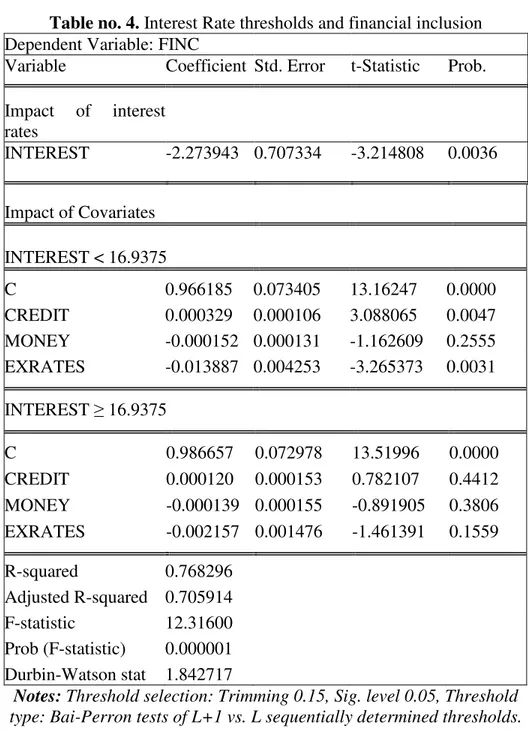

Threshold Effects in the Relationship between Interest Rate and Financial Inclusion in Nigeria

Full text

Figure

Related documents

We present a hash-based digital signature scheme customized for wireless sensor networks that offers the same signature size as ECDSA at the same security level.. We show

“I think it’s probably a good idea,” says Tresch, “to have the informed consent form signed before the day of surgery.” He cites cases where patients have signed...

Directions Additional directions to the collection point CardAvailable Bank/credit card available. CardName Bank/credit

Attorney Type of Cases Services Provided Colette Siewe Adoptions - Aeronautical/Maritime - Child Custody - Civil Damages Notary B.P. 177, Nkongsamba Collections - Contracts - Criminal

Firstly, if the average interest rates on government debt are larger than GDP growth rate (at time t ) and the primary budget balance is negative (the governmental expenditure

Those with the other three views also all consider organ donation as a good deed, but those with the “it does not go with my religion” view will not register because of their

They were perceived to play a crucial role in MOOC engagement, as a Bihar facilitator commented, ‘’Contact class has been the backbone of the MOOC’’ and completion rates

While SEDLP provided some anecdotal evidence of the value of sector programs to employers, the scope of SEDLP did not allow for any attempt to more precisely measure that value or