Summary

• Another week of significant spread tightening

• Moody’s set to downgrade a large number of Nordic banks

Headlines from the credit market this week

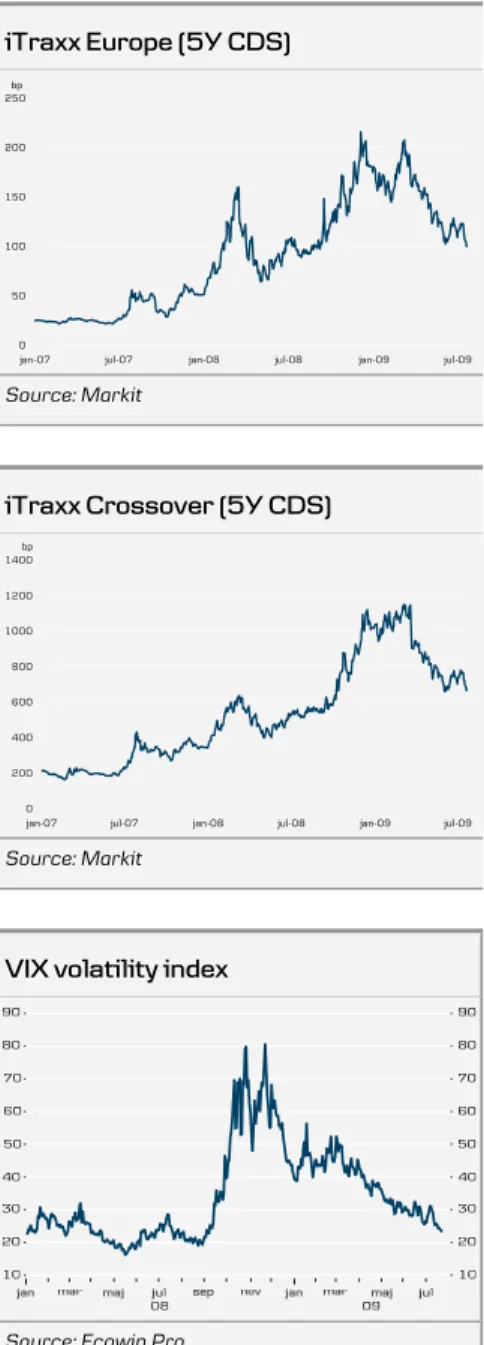

The tone in the financial markets continues to be very positive and consequently VIX is lower, spreads are tighter and equities are up. The most noteworthy event during the week was the biannual testimony by Ben Bernanke to the US congress and, although he noted that significant challenges remain for the US economy, markets eventually reacted positively to the speech.

Furthermore, data from the US housing market showed signs of stabilisation. Data from FHFA (Federal Housing Finance Agency) showed that home prices increased by 0.9% m/m in May. In our view, a stabilisation of the US housing market would be a significant positive driver as it would increase downside visibility for the value of the residential collateral banks have. Thereby it could – over time – increase the banks’ willingness to lend to the benefit of the US economy.

The investment grade index, iTraxx Europe, has tightened 12bp compared to last week whereas the high yield index, iTraxx Crossover, has tightened 55bp. The two indices now trade at 95bp and 645bp respectively. Cash spreads in the short end of the curve continue to tighten tremendously, and for the better names among the banks we now see spreads below Euribor. We believe that last month’s one-year repo auction by the ECB, where the banking system was allocated EUR442bn at the benchmark interest rate of 1%, is a key explanation for the strong rally in the short end. Going forward, we consider it likely that investors will move further out on the credit curve in order to pick up additional yield. Consequently we expect the credit curve to flatten from its current shape.

In the primary market we have seen a few deals this week (see table). Fiat came to the market with a deal that was very cheap compared to secondary levels; unsurprisingly the deal was heavily oversubscribed and performed strongly after launch (initially up 4 full figures).

Table 1. Selected new issues during the week

Name Rating Coupon Maturity Currency Size

Bond spread on issue date,

(bp)*

Fiat Ba1/BB+ Fixed 3Y EUR 1.25bn Gov +756

Gazprom Baa1/BBB Fixed 6Y EUR 0.85bn Gov +549

Note: Ratings are Moody's and S&P. * Mid-Swaps for Fixed, Discount Margin for floating Source: Danske Markets & Bloomberg

24 July 2009

iTraxx Europe (5Y CDS)

Source: Markit

iTraxx Crossover (5Y CDS)

Source: Markit

VIX volatility index

Source: Ecowin Pro

Senior Analyst Henrik Arnt +45 45128504 Henrik.arn[email protected] Senior Analyst Thomas Hovard +45 45128505 [email protected]

Weekly Credit Update

0 50 100 150 200 250

jan-07 jul-07 jan-08 jul-08 jan-09 jul-09 bp 0 200 400 600 800 1000 1200 1400

jan-07 jul-07 jan-08 jul-08 jan-09 jul-09 bp

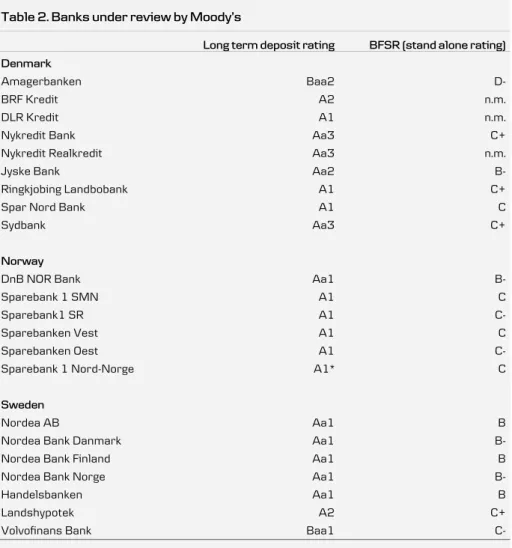

Moodys set to downgrade large number of Nordic banks

On Wednesday, Moody’s put the ratings of a large number of Nordic financial institutions on review for possible downgrade. The reason for this action is a change in the agency’s expectation for credit losses in the Nordic region, which were outlined in a recent report. In particular, Moody’s expects asset quality within the corporate sector to develop unfavourably compared to what is factored into current ratings.

Moody’s expects to finalise its reviews in 1-2 weeks and generally the agency expects it to result in downgrades of 1-2 notches. In the table below we have listed the institutions affected by the review.

As can be seen from the table attached, the larger banks currently have Aa1 ratings. Consequently, a 1-2 notch downgrade would still leave them as “Aa” banks. As long as this remains the case we do not think the downgrades by Moody’s will cause substantial negative effects in terms of higher funding costs. For the “second tier” banks that are at risk of moving from the double A class to the single A class, the downgrade could have some effects due to a smaller investor base. However, we do not consider this to be a significant issue.

Furthermore, it should be of no surprise to anybody that credit losses will further increase in the Nordic region in 2009 and 2010. This is probably going to be the rule rather than the exception for banks globally as company defaults and unemployment ratios continue to climb.

Table 2. Banks under review by Moodys

Long term deposit rating BFSR (stand alone rating)

Denmark

Amagerbanken Baa2

D-BRF Kredit A2 n.m.

DLR Kredit A1 n.m.

Nykredit Bank Aa3 C+

Nykredit Realkredit Aa3 n.m.

Jyske Bank Aa2

B-Ringkjobing Landbobank A1 C+

Spar Nord Bank A1 C

Sydbank Aa3 C+

Norway

DnB NOR Bank Aa1

B-Sparebank 1 SMN A1 C

Sparebank1 SR A1

C-Sparebanken Vest A1 C

Sparebanken Oest A1

C-Sparebank 1 Nord-Norge A1* C

Sweden

Nordea AB Aa1 B

Nordea Bank Danmark Aa1

B-Nordea Bank Finland Aa1 B

Nordea Bank Norge Aa1

B-Handelsbanken Aa1 B

Landshypotek A2 C+

C-US investment grade CDS index (CDX) US high yield CDS index (CDX)

Source: Ecowin Pro Source: Ecowin Pro

US cash indices 3M LIBOR-OIS spread

Source: Ecowin Pro Source: Ecowin Pro

Moodys global speculative default rate (LTM) 10Y Yields

Thomas Thøgersen Grønkjær +45 45 12 85 02 thomas.groenkjaer

Head of Credit Research Fixed Income Credit Research

Jakob Magnussen +45 45 12 85 03 jakob.magnussen

Thomas Hovard +45 45 12 85 05

thomas.hovard Henrik Arnt +45 45 12 85 04

henrik.arnt

Peter Tind Larsen +45 45 12 85 08 peter.tind.larsen

Peter Tind Larsen +45 45 12 85 08 peter.tind.larsen Jakob Magnussen +45 45 12 85 03 jakob.magnussen

TMT, Utilities & Energy Financials Pulp & Paper Industrials

email addresses end @danskebank.com

Thomas Thøgersen Grønkjær +45 45 12 85 02 thomas.groenkjaer

Head of Credit Research

Thomas Thøgersen Grønkjær +45 45 12 85 02 thomas.groenkjaer

Head of Credit Research Fixed Income Credit Research Fixed Income Credit Research

Jakob Magnussen +45 45 12 85 03 jakob.magnussen

Thomas Hovard +45 45 12 85 05

thomas.hovard Henrik Arnt +45 45 12 85 04

henrik.arnt

Peter Tind Larsen +45 45 12 85 08 peter.tind.larsen

Peter Tind Larsen +45 45 12 85 08 peter.tind.larsen Jakob Magnussen +45 45 12 85 03 jakob.magnussen

TMT, Utilities & Energy Financials Pulp & Paper Industrials

email addresses end @danskebank.com

Jakob Magnussen +45 45 12 85 03 jakob.magnussen

Thomas Hovard +45 45 12 85 05

thomas.hovard Henrik Arnt +45 45 12 85 04

henrik.arnt

Peter Tind Larsen +45 45 12 85 08 peter.tind.larsen

Peter Tind Larsen +45 45 12 85 08 peter.tind.larsen Jakob Magnussen +45 45 12 85 03 jakob.magnussen

TMT, Utilities & Energy Financials Pulp & Paper Industrials

Disclosure

This report has been prepared by Danske Research, which is part of Danske Markets, a division of Danske Bank. Danske Bank is under supervision by the Danish Financial Supervisory Authority. The authors of this report are Henrik Arnt (Senior Analyst) and Thomas Hovard (Senior Analyst).

Danske Bank research reports are prepared in accordance with the Danish Society of Investment Professionals’ Ethical rules and the Recommendations of the Danish Securities Dealers Association.

Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high quality research based on research objectivity and independence. These procedures are documented in the Danske Bank Research Policy. Employees within the Danske Bank Research Departments have been instructed that any request that might impair the objectivity and independence of research shall be referred to Research Management and to the Compliance Officer. Danske Bank Research departments are organised independently from and do not report to other Danske Bank business areas. Research analysts are remunerated in part based on the over-all profitability of Danske Bank, which includes investment banking revenues, but do not receive bonuses or other remuneration linked to specific corporate finance or dept capital transactions.

The Equity and Corporate Bonds analysts of Danske Bank are not permitted to invest in securities under coverage in their research sector.

Danske Bank is a market maker and may as such hold positions in the financial instruments mentioned in this report.

Please go to www.danskeequities.com for further disclosures and information.

Disclaimer

This publication has been prepared by Danske Markets for information purposes only. It has been prepared independently, solely from publicly available information and does not take into account the views of Danske Bank’s internal credit department. It is not an offer or solicitation of any offer to purchase or sell any financial instrument. Whilst reasonable care has been taken to ensure that its contents are not untrue or misleading, no representation is made as to its accuracy or completeness and no liability is accepted for any loss arising from reliance on it. Danske Bank, its affiliates or staff, may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives), of any issuer mentioned herein. The Equity and Corporate Bonds analysts are not permitted to invest in securities under coverage in their research sector. This publication is not intended for retail customers in the UK or any person in the US. Danske Markets is a division of Danske Bank A/S. Danske Bank A/S is authorized by the Danish Financial Supervisory Authority and subject to limited regulation by the Financial Services Authority (UK). Details on the extent of our regulation by the Financial Services Authority are available from us on request. Copyright © Danske Bank A/S. All rights reserved. This publication is protected by copyright and may not be reproduced in whole or in part without permission.