Volume 14, Number 1, March 2019

Effect of Deliberate Practice and Previous Knowledge

on Academic Performance

Helen Wong a [email protected]

Carmen Sum a [email protected]

Stephen Chan a [email protected]

Raymond Wong b

Corresponding Author: [email protected]

a

The Hong Kong Polytechnic University Kowloon, Hong Kong

b

School of Accountancy The Chinese University of Hong Kong

New Territories, Hong Kong

ABSTRACT

The determinants of academic performance have always been the concern of educators. This study examined the effect of deliberate practice and previous knowledge on the academic success of a sample of 181 first-year business students in an elementary accounting course at a self-financed college in Hong Kong. The study had three objectives: (1) to ascertain the role of deliberate practice in their academic success; (2) to determine whether the role of deliberate practice would remain the same if the students’ previous knowledge was considered; and (3) to compare the contribution of different measures of previous knowledge to the students’ performance in the course. The authors developed hypotheses and a research model and conducted multiple linear regression analyses to measure the relationships between deliberate practice, previous knowledge, and academic success in the course. The authors also developed suggestions for future research.

International Journal of Business and Information

1.

INTRODUCTION

The literature includes many empirical studies on the determinants of academic success in an accounting course. These studies focus, for example, on effort and time spent, previous knowledge, proficiency in English, and mathematical ability (Eskew & Faley, 1988; Gist, Goedde, & Ward, 1996; Gul & Fong, 1993; Koh & Koh, 1999; Lee, 1999; Maksy & Wagaman, 2015; Maksy & Zheng, 2008; Tho, 1994; Wong & Chia, 1996).

Time spent studying has been considered a reasonable contributor to students’ academic success; i.e., the more time students spend studying, the better academic results they will have. We believe that students should increase the time they spend studying in order to improve their academic performance, but such a relationship is not as strong as some think. Some studies have found a weak, negative, or unreliable relationship between the time spent studying and academic performance (Beer & Beer, 1992; Guney, 2009; Lahmers & Zulauf, 2000).

The literature on deliberate practice provides more insights into the relationship between the time spent studying and academic performance.

Deliberate practice is the considerable effort spent in structured activities created to improve performance in a specific domain (Macnamara, Hambrick, & Oswalk, 2014). It is usually tailor-made by teachers and trainers to focus attention and thus maximize performance in a specific domain; for example, education (Pintrich, 2000), music (Krampe & Ericsson, 1996), and sports (Helsen, Starkes, & Hodges, 1998). Some studies have found that the amount of high-quality practice, rather than time alone, has a significant relationship to better academic performance (Frisbee, 1984, Naser & Peel, 1998).

The first research objective of the current study is to determine the role of students’ deliberate practice in their academic success in an elementary accounting course at the college level. Inconsistent findings regarding the relationship between high-quality practice and academic performance were reported in studies such as Guney (2009) and Michaels and Miethe (1989). In other studies, the relationship between students’ study time (practice) and grades disappeared entirely after students’ previous knowledge was statistically controlled (Schuman, Walsh, Olson, & Etheridge, 1985).

Volume 14, Number 1, March 2019

Previous knowledge has been found to have a significant relationship to later academic success in different subject areas, such as elementary accounting (e.g., Alcock, Cockcroft, & Finn, 2008; Eskew & Faley, 1988), first-year accounting and business economics performance (Duff, 2004), advanced accounting (Al-Twaijry, 2010; Maksy & Zheng, 2008), mathematics (Parsons, Croft, & Harrison, 2009), and principles of finance (Baard & Watts, 2008). Scores on standardized aptitude tests such as SAT and ACT were usually adopted to assess students’ previous knowledge, and a positive relationship was confirmed (Lahmers & Zulauf, 2000; Schuman et al., 1985). In other studies, previous performances in mathematics and English were considered predictors of academic success at the college level (Al-Twaijry, 2010; Fabros-Tyler, 2014; Garkaz, Banimahd, & Exmaeili, 2011; Guney, 2009). Different types of measurement were used to assess students’ previous knowledge. It is interesting to explore the possible differences between these different types of previous knowledge in predicting later academic success.

The third research objective of the current study is to compare the contribution of different measures of previous knowledge earned in secondary school to the academic success in an accounting course at the college level.

The current study addresses the following research questions:

• What would be the impact of deliberate practice and previous knowledge on later academic success?

• Would the significance of deliberate practice remain strong and significant if students’ previous knowledge is considered?

• Would there be any differences between the effect of previous knowledge on students’ academic achievement if different measurements were used to assess students’ previous knowledge?

The answers to these questions will provide additional insight into the contribution of students’ deliberate practice and their previous knowledge with regard to determining their success in an elementary accounting course at the college level.

2.

LITERATURE REVIEW AND HYPOTHESES

DEVELOPMENT

International Journal of Business and Information 2.1. Deliberate Practice

The consensus of the literature on deliberate practice is that the amount of high-quality practice is tightly associated with better performance in a wide variety of domains (Ericsson, 2002; Ericsson & Lehman, 1996). Deliberate practice involves extensive practice, but not all types of practices are equally helpful in improving superior performance (Ericsson & Lehman, 1996). The cumulative effect of engagement in deliberate practice with an explicit goal and target helps one acquire expert performance (Ericsson, Kramer, & Tesch-Römer, 1993). It is also argued that a number of prerequisites define deliberate practice, including a distraction-free study environment, easy access to training resources, and the capacity to sustain full concentration (Plant, Ericsson, Hill, & Asberg, 2005).

Similar research findings are evident in studies of college education. Quantitative measures of study effort – such as the amount of study, the hours spent in study, or class attendance – were commonly adopted in predicting the college grade. Some studies found a positive relationship (e.g., Michaels & Miethe, 1989; Naser & Peel, 1998; Stinebrickner & Stinebrickner, 2004). Other studies, however, found a weak or unreliable relationship between study effort and academic performance (Beer & Beer, 1992; Lahmers & Zulauf, 2000; Rau & Durand, 2000). Rau and Durand (2000) argued that a more comprehensive measurement is needed to improve the explanatory power of study effort to academic performance. Others argued that effective learning should involve regulation of effective learning activities, self-regulated practice, and appropriate study environment within an educational setting (Ericsson, 2002; Pintrich, 2000; Zimmerman, 2002). Students’ efforts should, therefore, address the qualitative attributes rather than the quantitative aspect alone (Schuman et al., 1985).

The current paper addresses students’ effort spent in study through effective learning activities and a regulated educational setting. The paper uses the concept of deliberate practice to define students’ effort. It is predicted that deliberate practice would have a positive and significant contribution to later academic success:

Hypothesis 1. Students’ deliberate practice has a positive and significant impact on academic success in an elementary accounting course at the college level.

Volume 14, Number 1, March 2019

therefore, seeks to answer the following questions: Is previously earned knowledge or performance a strong predictor of later academic success? How strong is it?

2.2. Previous Knowledge

Research into previously acquired academic knowledge indicates that it could explain significant portions of variance in overall academic performance at a later stage. A positive and significant relationship between previous knowledge and later academic success was supported in different domains, such as elementary accounting (Alcock et al., 2008; Eskew & Faley, 1988), first-year accounting and business economics performance (Duff, 2004), advanced accounting (Al-Twaijry, 2010; Maksy & Zheng, 2008), mathematics (Parsons, Croft, & Harrison, 2009), and principles of finance (Baard & Watts, 2008). Usually, previous GPA, grades in a relevant subject or course, and SAT and ACT scores at the high school or college level are adopted as measures of previous knowledge (e.g., Baard & Watts, 2008; Christensen, Nance, & White, 2012; Lahmers & Zulauf, 2000; Schuman et al. (1985).

In prior studies, scores on standardized aptitude tests such as SAT and ACT were usually used to assess students’ previous knowledge, and a positive association was confirmed (Lahmers & Zulauf, 2000; Schuman et al., 1985). Those aptitude tests were considered a relatively stable construct for measuring previously acquired knowledge (Lahmers & Zulauf, 2000), but these types of measures were found to vary from context to context.

In Hong Kong, the standardized aptitude test reflecting students’ abilities and knowledge at the high school level is the Hong Kong Diploma of Secondary Education (HKDSE). It is a public examination developed for the 3-3-4 education scheme begun in 2009, involving 3 years of junior secondary school, 3 years of senior secondary school, and 4 years of university education (Cheung, 2010). The HKDSE was first implemented in the new education scheme in 2012 (Cheung, 2010).

International Journal of Business and Information programs, including associate degree and higher diploma programs, the minimum admission requirements are Level 2 for Chinese language and English language, with the requirements for the other subjects being set by different institutions (Cheung, 2010). The scores for these subjects were usually summed and labeled the “Best Five Score.”

The aggregate scores obtained from these types of aptitude tests were commonly used in prior studies to assess students’ background or previous knowledge, and positive association with the academic performance was confirmed (e.g., Lahmers & Zulauf, 2000; Lane & Porch, 2002; Schuman et al., 1985).

In the current study, it is posited that the Best Five Score would have a positive and significant effect on performance in an accounting course at the college level:

Hypothesis 2. Students’ Best Five Score has a positive and significant impact on academic success in an elementary accounting course at the college level.

In addition to Chinese and English languages, mathematics is usually taken into consideration for admission to sub-degree programs. Research on previously acquired knowledge in mathematics and English provides substantial support for this consideration, particularly for admission to business programs, courses, or modules (e.g., Gul & Fong, 1993; Koh & Koh, 1999; Lane & Porch, 2002; Naser & Peel, 1998; Wong & Chia, 1996).

Volume 14, Number 1, March 2019

The current study posits that students’ previous knowledge or ability in mathematics would have a positive and significant effect on performance in an accounting course at the college level:

Hypothesis 3a. Students’ previous knowledge in mathematics has a positive and significant impact on academic success in an elementary accounting course at the college level.

Other than mathematics, proficiency in English was regarded in prior studies as one of the selection criteria for admitting students to sub-degree programs. Except for studies conducted in Hong Kong by Gul and Fong (1993) and Wong and Chia (1996), English was not found to be a critical determinant in introductory accounting courses in most research studies conducted in Western countries (e.g., Keef, 1988). Other studies argued that English is a significant factor in students’ performance in non-English-speaking countries (Wong & Chia, 1996).

Similar to these two studies, the current study posits that English would have a positive influence on students’ academic performance:

Hypothesis 3b. Students’ previous knowledge in English has a positive and significant impact on academic success in an elementary accounting course at the college level.

Gul and Fong (1993) and Wong and Chia (1996) also revealed that the English language would be less important than mathematics ability in achieving academic achievement in an accounting course. It was predicted that similar results would be shown in the current study. Other than that, the Best Five Score appeared to represent students’ general entry qualification to the sub-degree programs. It is proposed that the Best Five Score (i.e., the use of aggregate score) would have greater power in explaining later academic success than scores in mathematics and English language alone (Lane & Porch, 2002).

Hypothesis 4a. Students’ previous knowledge in mathematics has a greater impact than the English language on academic success in an elementary accounting course at the college level.

International Journal of Business and Information 2.3. Deliberate Practice Versus Previous Knowledge in

Predicting Academic Success

In prior studies, measures of students’ effort varied; therefore, the importance of this effort to academic success differed. When students’ effort was measured in terms of the hours spent in study, their previous knowledge was found to have significant and greater effect in determining academic success (Maksy & Wagaman, 2015; Maksy & Zheng, 2008). When students’ effort was assessed by the number of quizzes taken during the term, their effort outperformed previous knowledge in contributing to academic performance (Eskew & Faley, 1988). Some studies proposed to improve the explanatory power of students’ effort by considering the qualitative attributes of effort, such as students’ ability to concentrate and study skills (Michaels & Miethe, 1989; Schuman et al., 1985); whereas, other studies recommended considering continuous record of study time (Lahmers & Zulauf, 2000; Schmidt, 1983), as well as the measurement of continuous and term-time performance in the curriculum (Maksy & Wagaman, 2015). Dinis (1991) found that the role of previous knowledge in determining academic success in the early stage is undeniable, but that its contribution would not be that strong in a course at a later stage.

The current study predicts that students’ deliberate practice might outperform previous knowledge in achieving performance at the final assessment if the course is structurally defined with continuous feedback and assessment, extra guidance and attention from instructors, and class activities to enhance students’ concentration, time, and effort.

Hypothesis 5a. Students’ deliberate practice would have a greater impact than students’ Best Five Score on academic success in an elementary accounting course at the college level.

Hypothesis 5b. Students’ deliberate practice would have a greater impact than students’ previous knowledge in mathematics on academic success in an elementary accounting course at the college level.

Hypothesis 5c. Students’ deliberate practice would have a greater impact than students’ previous knowledge of English on academic success in an elementary accounting course at the college level.

Volume 14, Number 1, March 2019

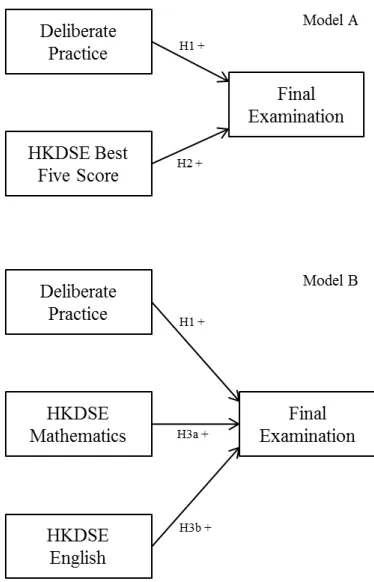

addressed the aggregate score of previous knowledge and deliberate practice in achieving the final examination score in an elementary accounting course. This model also addressed Hypothesis 5a. The second model (Model B) considered the individual scores of HKDSE mathematics and English, as well as deliberate practice, as the independent variables. Hypothesis 5b would then be addressed. The coefficients of the paths and the explanatory power of the two models were then compared to provide support for hypotheses 4a and 4b.

Figure 1. Proposed Models of Deliberate Practice, Previous Knowledge, and Academic Success

3.

RESEARCH METHOD

International Journal of Business and Information 3.1. Data and Sample

This study targeted first-year students pursuing a business associate degree at a self-financed college in Hong Kong. These students were invited to voluntarily provide their previous academic background at the beginning of an elementary accounting course. Students’ deliberate practice was recorded for each continuous assessment, along with weekly activities during the term. Their academic success was their performance on the final examination at the end of the term. A total of 181 qualified samples were obtained.

3.2. Independent Variables

Deliberate Practice. Deliberate practice was well regulated with educational setting and environment, plus deliberate and effective learning activities. Students were required to attend a one-hour reinforcement class each week for 13 weeks. The class covered concepts recap and calculation practice, as well as feedback and explanation given by the facilitators. Students’ engagement, attendance, and cumulative effort in the weekly classes were quantified and recorded. Besides deliberate activities in classes, students were required to complete two continuous assessments during the term. These assessments were drafted to support students’ learning in financial accounting. Their performances on the two assessments were then measured. The total score out of 100 was calculated for each student.

Previous Knowledge. Previous knowledge was measured using the results of HKDSE. Three measurements were collected from students on a self-reporting basis. The measurements include the total scores of the best five HKDSE subjects, the overall HKDSE English score, and the HKDSE mathematics score (compulsory part). Scores from 1 to 5 were directly recorded, whereas 5* was converted as 6 and 5** was coded as 7.

3.3. Dependent Variable

Academic Success. To assess later academic success, we obtained the performance achieved at the end of the term on the final examination in financial accounting at the associate degree level. The raw score out of 100 was recorded for each student.

4.

RESULTS

Volume 14, Number 1, March 2019 4.1. Descriptive Statistics

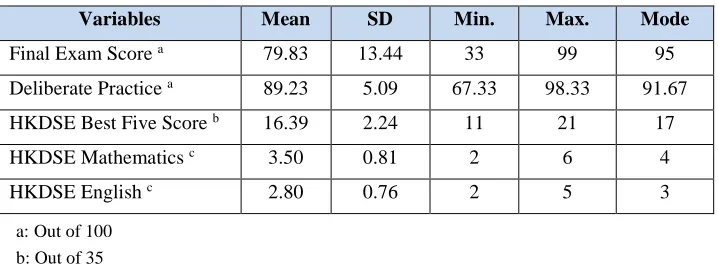

A total of 181 associate degree students were involved in this study. All were Stage One students in business at a community college in Hong Kong. Descriptive statistics of the students’ performance are presented in Table 1. The final examination score that the students achieved in an elementary accounting course ranged from 33 to 99, with an average of 79.83. Their average performance earned through deliberate practice in this course was 89.23. Compared with their performance at the college level, their previous academic knowledge was average. The mean of Best Five Score was 16.39, with mathematics at 3.50 and English language at 2.80.

Table 1

Descriptive Statistics of Students’ Performance (N = 181

)

Variables Mean SD Min. Max. Mode

Final Exam Score a 79.83 13.44 33 99 95

Deliberate Practice a 89.23 5.09 67.33 98.33 91.67

HKDSE Best Five Score b 16.39 2.24 11 21 17

HKDSE Mathematics c 3.50 0.81 2 6 4

HKDSE English c 2.80 0.76 2 5 3

a: Out of 100 b: Out of 35

c: Codes from 1 to 7 to represent 1, 2, 3, 4, 5, 5*, and 5**

4.2. Hypotheses Testing

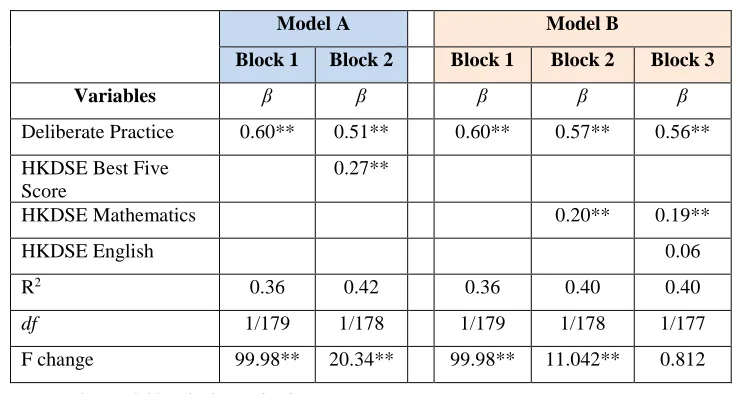

Multiple linear regression analyses were conducted to measure relationships between deliberate practice, previous knowledge, and academic success in the elementary accounting course. All analyses were free from a multicollinearity problem. Hypothesis 1 tested whether students’ deliberate practice has a positive and significant impact on academic success in an elementary accounting course. This hypothesis was strongly and significantly supported in both models, as shown in Table 2. When deliberate practice was considered the sole variable in the relationship to the final examination, its contribution was found to be strong, with a standardized coefficient of 0.60 (R2 = 0.36; p < 0.01). The result concurred with

International Journal of Business and Information Table 2

Regression Analysis in Predicting Academic Performance (N = 181)

Model A Model B

Block 1 Block 2 Block 1 Block 2 Block 3

Variables β β β β β

Deliberate Practice 0.60** 0.51** 0.60** 0.57** 0.56** HKDSE Best Five

Score

0.27**

HKDSE Mathematics 0.20** 0.19**

HKDSE English 0.06

R2 0.36 0.42 0.36 0.40 0.40

df 1/179 1/178 1/179 1/178 1/177

F change 99.98** 20.34** 99.98** 11.042** 0.812 Dependent variable: Final Examination

p < 0.10 *p < 0.05 **p < 0.01

Hypothesis 2 measured the relationship between an aggregated measure of previous knowledge (i.e., HKDSE Best Five Score) and the academic performance achieved on the final examination. This relationship was statistically confirmed in Model A when deliberate practice was also included. Similar results were found in prior studies, which showed that students’ previous knowledge is one of the contributors to later academic success (Lahmers & Zulauf, 2000; Lane & Porch, 2002; Schuman et al. 1985). This result also supported the use of HKDSE Best Five Score to admit quality candidates to sub-degree programs in Hong Kong.

Volume 14, Number 1, March 2019

study. This result was similar to that of most previous studies indicating that English is not a critical variable in achieving academic success in introductory accounting courses (Keef, 1988; Ward, Ward, Wilson, & Deck, 1993). English might not be an influencing factor in performance in an introductory accounting course at the college level in non-English-speaking countries when deliberate practice and previous mathematics ability are taken into account.

The preceding findings also provided answers to Hypothesis 4a that the role of previously developed mathematics ability (β = 0.19; p < 0.01) is more important than English language (β = 0.06; p = 0.37). This hypothesis was supported, and the result was similar to previous research findings (e.g., Gul & Fong, 1993; Wong & Chia, 1996). In addition, the explanatory power of Model A (R2 = 0.42) was

found to be slightly greater than Model B (R2 = 0.40). It showed that the use of

HKDSE Best Five Scores is more effective than the use of mathematics and the English language in achieving academic success. This result proves that the use of an aggregated measure of previous knowledge has more explanatory power in academic success (Lane & Porch, 2002). Hypothesis 4b was therefore supported. Hypotheses 5a, 5b, and 5c compared the importance of deliberate practice and the three measures of previous knowledge (i.e., HKDSE Best Five Score, mathematics ability, and English language) in achieving academic success in an elementary accounting course at the college level. The regression results, shown earlier in Table 2, indicate that deliberate practice has greater power than previous knowledge in explaining academic success. Model A shows that, with every increase of one standard deviation in students’ deliberate practice, their academic performance rose by 0.51 standard deviations (p < 0.01), while the Best Five Score was held constant. With an increase of one standard deviation in the Best Five Score, students’ academic performance increased 0.27 standard deviation (p < 0.01), while students’ deliberate practice held constant. Hypothesis 5a, therefore, was supported. From the regression results of Model B, students’ deliberate practice (β = 0.56; p < 0.01) had a greater impact than previous mathematics ability (β = 0.19; p < 0.01) and English language (β = 0.06; p = 0.37). Thus, both hypotheses 5b and 5c were supported. These results strongly justified the use of both quantitative and qualitative attributes for improving the explanatory power of students’ effort in their study (Lahmers & Zulauf, 2000; Maksy & Wagaman, 2015; Michaels & Miethe, 1989; Schmidt, 1983; Schuman et al., 1985).

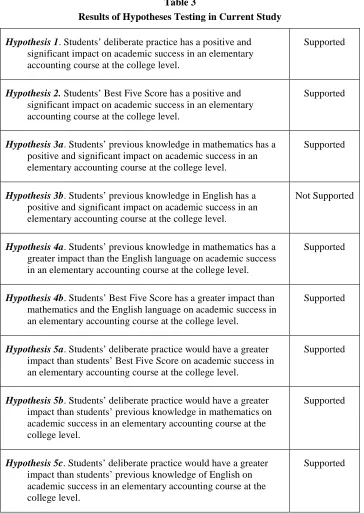

Table 3 summarizes the results for all hypotheses in the current study. As indicated, all hypotheses were supported, except for Hypothesis 3b.

International Journal of Business and Information Table 3

Results of Hypotheses Testing in Current Study

Hypothesis 1. Students’ deliberate practice has a positive and significant impact on academic success in an elementary accounting course at the college level.

Supported

Hypothesis 2. Students’ Best Five Score has a positive and significant impact on academic success in an elementary accounting course at the college level.

Supported

Hypothesis 3a. Students’ previous knowledge in mathematics has a positive and significant impact on academic success in an elementary accounting course at the college level.

Supported

Hypothesis 3b. Students’ previous knowledge in English has a positive and significant impact on academic success in an elementary accounting course at the college level.

Not Supported

Hypothesis 4a. Students’ previous knowledge in mathematics has a greater impact than the English language on academic success in an elementary accounting course at the college level.

Supported

Hypothesis 4b. Students’ Best Five Score has a greater impact than mathematics and the English language on academic success in an elementary accounting course at the college level.

Supported

Hypothesis 5a. Students’ deliberate practice would have a greater impact than students’ Best Five Score on academic success in an elementary accounting course at the college level.

Supported

Hypothesis 5b. Students’ deliberate practice would have a greater impact than students’ previous knowledge in mathematics on academic success in an elementary accounting course at the college level.

Supported

Hypothesis 5c. Students’ deliberate practice would have a greater impact than students’ previous knowledge of English on academic success in an elementary accounting course at the college level.

Volume 14, Number 1, March 2019

5.

DISCUSSION

This study sought to provide additional insights into the contribution of students’ effort and their previous knowledge in achieving academic performance in an elementary accounting course at the college level.

The first research objective was to ascertain the role of student’s deliberate practice in their academic success. The results for Hypothesis 1 clearly proved the significant role of student’s effort in enhancing their academic performance (Eskew & Faley, 1988). For improving student’s academic performance, students’ learning should be supported by structured and engaging learning activities, self-regulated practice, and continuous feedback and guidance, as well as an appropriate learning environment (Ericsson, 2002; Macnamara et al. 2014; Pintrich, 2000; Schuman et al., 1985; Zimmerman, 2002). The course should be well structured with continuous feedback and assessment, extra guidance and attention from instructors, and class activities to facilitate students’ learning and effort in their study (Maksy & Wagaman, 2015). In other words, students should be reminded to put time and effort in their learning activities, and teachers should tailor their courses to engage students’ involvement and facilitate learning to enhance academic performance. We recommend that students’ effort in learning be measured from both quantitative and qualitative aspects, as it could strengthen the power in explaining student performance.

The second research objective sought to determine whether the role of deliberate practice would remain the same if students’ previous knowledge was also considered in predicting students’ academic performance. Hypothesis 1, as well as hypotheses 5a, 5b, and 5c, indicated that the strength of students’ deliberate practice remained strong and significant when students’ previous knowledge was taken into account (Eskew & Faley, 1988). The results revealed that students’ effort is more powerful and stable in achieving their academic success, whereas previous academic knowledge has only a subordinate role in predicting their academic performance. Students who have a weaker academic background will not be disadvantaged if they work harder in their study. They have to be motivated to develop their abilities through hard work and dedication. Students with a better academic background should avoid relying on previous knowledge to continue their study. They should understand that previous knowledge may help their learning at an early stage, but that commitment and continuous effort are key to academic success at the later stage (Dinis, 1991).

International Journal of Business and Information course at the college level. Three measures were tested in the current study. The first measure used the HKDSE Best Five Score, which is an aggregated measure of students’ previous academic performance. The second and the third measures were non-aggregate measures – HKDSE mathematics and HKDSE English language. Hypotheses 2 and 3a confirmed the importance of Best Five Score and mathematics ability in influencing students’ academic performance. The result of Hypothesis 3b was, however, not supported. Students’ previous knowledge in English was found not to be a significant factor in determining their academic success in the elementary accounting course. These results supported the use of the standardized aptitude test (i.e., HKDSE in this case) as an appropriate measure of students’ previous knowledge (Lahmers & Zulauf, 2000; Lane & Porch, 2002). In comparison, the use of Best Five Score as the aggregate measure was found to be better than the use of individual mathematics and English scores in predicting students’ performance in their accounting study (Hypothesis 4b). It also confirmed the use of the best five subject scores as the entrance requirements for sub-degree programs (Cheung, 2010). The results of Hypothesis 4a further supported the greater importance of previous mathematics ability than English language in an accounting course (Alcock et al., 2008; Gul & Fong, 1993; Koh & Koh, 1999; McCarron & Burstein, 2017; Wong & Chia, 1996).

These findings suggest that students who intend to enroll in an accounting course or program should strengthen their mathematics ability. Numerical ability would enhance students’ cognitive ability in managing accounting records (Babalola & Abiola, 2013). The college or school may also consider mathematics as one of the core admission criteria to screen potential candidates, other than Chinese and English languages. They may also offer mathematics courses to support students’ learning in accounting.

6.

CONCLUSION

Volume 14, Number 1, March 2019

With regard to future research, we offer five suggestions:

• First, the same set of variables and relationships could be replicated and examined in other business courses or non-business courses to verify the importance of deliberate practice in academic study.

• Second, the composition of deliberate practice deserves attention in future studies. Both qualitative and quantitative attributes under structured and engaging class activities should be considered.

• Third, previous discipline-related knowledge could be measured to predict students’ academic performance. Its effect might be greater than non-discipline-related knowledge earned in previous schooling.

• Fourth, the importance of a mathematics background could be explored in other courses that require numerical ability; for example, engineering, finance, economics, and science.

• Fifth, scholars may assess the effect of previous knowledge and students’ effort on performance in a course during the middle of the semester and at the end. The effect might be stronger in the early stage of study and become weaker at a later stage.

REFERENCES

Alcock, J.; Cockcroft, S.; & Finn, F. (2008). Quantifying the advantage of secondary mathematics study for accounting and finance undergraduates, Accounting & Finance 48: 697-718. DOI:10.1111/j.1467‐629x.2008.00261.x

Al-Twaijry, A.A. (2010). Student academic performance in undergraduate managerial-accounting courses, Journal of Education for Business 85(6): 311-322.

DOI: 10.1080/08832320903449584

Baard, V., & Watts, T. (2008). The value of prerequisites: A link between understanding and progression, E-Journal of Business Education & Scholarships of Teaching 2(1): 1-10.

Babalola, Y.A., & Abiola, F. R. 2013. The importance of mathematics in the recording and interpretation of accounting, International Journal of Financial Economics 1(4): 103-107.

Beer, J., & Beer, J. (1992). Classroom and home study times and grades while at college using a single subject design, Psychological Report 71: 233–234.

International Journal of Business and Information Burdick, R., & Schwartz, B.N. (1982). Predicting grade performance for intermediate

accounting, Delta Pi Epsilon Journal 24: 117-127. Cheung, T. (2010). Introduction of HKDSE Education.

Retrieved 18 July 2018 from:

www.hkeaa.edu.hk/DocLibrary/HKDSE/Progress_promote_HKDSE/HKDSE.pdf Christensen, D.G.; Nance, W.R.; White, D.W. (2012). Academic performance in MBA programs: Do prerequisites really matter? Journal of Education for Business 87: 42-47. DOI: 10.1080/08832323.2011.555790

Dinius, S.H. (1991). Accounting students: Secondary-level study and academic performance and characteristics, Journal of Education for Business 66(4): 244-250. DOI: 10.1080/08832323.1991.10117480

Duff, A. (2004). Understanding academic performance and progression of first-year accounting and business economics undergraduates: The role of approaches to learning and prior academic achievement, Accounting Education 13(4): 409-430. DOI: 10.180/0963928042000306800

Ericsson, K.A., & Lehmann, A.C. (1996). Expert and exceptional performance: Evidence on maximal adaptations on task constraints, Annual Review of Psychology 47: 273– 305. DOI: 10.1146/annurev.psych.47.1.273

Ericsson, K.A. (2002). Attaining excellence through deliberate practice: Insights from the study of expert performance. In M. Ferrari (ed.), The Pursuit of Excellence in Education: 21–55. Hillsdale, NJ: Erlbaum.

Ericsson, K.A.; Krampe, R.T.; & Tesch-Römer, C. (1993). The role of deliberate practice in the acquisition of expert performance, Psychological Review 100: 363–406. DOI: 10.1037/0033-195X.100.3.363

Eskew, R., & Faley, R. (1988). Some determinants of student performance in the first college-level financial accounting course, Accounting Review 63: 137–147.

Fabros-Tyler, G. (2014). English, mathematics, and programming grades in the secondary level as predictors of academic performance at college level, In Information, Intelligence, Systems and Applications, IISA, 5th International Conference, 427-431.

Volume 14, Number 1, March 2019

Garkaz, M.; Banimahd, B.; & Esmaeili, H. (2011). Factors affecting accounting students’ performance: The case of students at The Islamic Azad University, Procedia - Social and Behavioral Sciences 29: 122-128. DOI: 10.1016/j.sbspro.2011.11.216 Gist, W.E.; Goedde, H.; & Ward, B.H. 1996. The influence of mathematical skills and

other factors on minority student performance in principles of accounting, Issues in Accounting Education 11(1), Spring: 49-60.

Gul, F.A., & Fong, S.C.C. (1993). Predicting success for introductory accounting students: Some further Hong Kong evidence, Accounting Education 2(1): 33-42.

DOI: 10.1080/90639289300000003

Guney, Y. (2009). Exogenous and endogenous factors impacting student performance in undergraduate accounting modules, Accounting Education 18(1): 51-73.

DOI: 10.1080/096392807017400142

Helsen, W.F.; Starkes, J.L.; & Hodges, N.J. (1998). Team sports and the theory of deliberate practice, Journal of Sport and Exercise Psychology 20: 12–34.

DOI: 10.1123/jsep.20.1.12

Keef, S.P. (1988). Preparation for a first level university accounting course: The experience in New Zealand, Journal of Accounting Education 6(2): 293-307. DOI: 10.1016/0748-5751(88)90010-3

Koh, M.Y., & Koh, H.C. (1999). The determinants of performance in an accountancy degree course, Accounting Education 8(1): 13-29.

DOI: 10.1080/096392899331017

Krampe, R. Th., & Ericsson, K.A. (1996). Maintaining excellence: Deliberate practice and elite performance in young and older pianists, Journal of Experimental Psychology: General 125(4): 331–359. DOI: 10.1038/0096-3445.125.4.331

Lahmers, A.G., & Zulauf, C.R. (2000). Factors associated with academic time use and academic performance of college students: A recursive approach, Journal of College Student Development 41(5): 544-556.

Lane, A., & Porch, M. (2002). The impact of background factors on the performance of nonspecialist undergraduate students on accounting models – a lognitudinal study: A research note, Accounting Education 11(1): 109-118.

DOI: 10.1080/90639280210153308

Lee, D.S. (1999). Strength of high school accounting qualification and student performance in university-level introductory accounting courses in Hong Kong, Journal of Education for Business 74(5): 301-306.

International Journal of Business and Information Macnamara, B.N.; Hambrick, D.Z.; & Oswald, F.L. (2014). Deliberate practice and

performance in music, games, sports, education, and professions a meta-analysis,

Psychological Science 25(8): 1608-1618. DOI: 10.1177/0956797614535810

Maksy, M.M., & Wagaman, D.D. (2015). Factors associated with student performance in advanced accounting: A comparative study at commuter and residential schools, Journal of Accounting and Finance 15(1): 72-94.

Maksy, M.M., & Zheng, L. (2008). Factors associated with student performance in advanced accounting and auditing, Accounting Research Journal 21(1): 16-32. DOI: 10.1108/10309610810891328

McCarron, K.B., & Burstein, A.N. (2017). The importance of mathematics as a prerequisite to introductory financial accounting, Community College Journal of Research and Practice 41(9): 543-550.

Michaels, J.W., & Miethe, T.D. (1989). Academic effort and college grades, Social Forces 68(1): 309-319. DOI: 10.2307/2579230

Naser, K., & Peel, M.J. (1998). An exploratory study of the impact of intervening variables on student performance in a principles of accounting course, Accounting Education 7(3): 209-223. DOI: 10.1080/096392898331153

Parsons, S.; Croft, T.; & Harrison, M. (2009). Does students' confidence in their ability in mathematics matter? Teaching Mathematics and Its Applications 28(2): 53-68. DOI: 10.1093/teamat/hrp010

Pintrich, P.R. (2000). The role of goal orientation in self-regulated learning, In M. Boekaerts, P. Pintrich, & M. Zeidner (eds.), Handbook of Self-Regulation: 451–502. San Diego, CA: Academic Press.

Plant, E.A.; Ericsson, K.A.; Hill, L.; & Asberg, K. (2005). Why study time does not predict grade point average across college students: Implications of deliberate practice for academic performance, Contemporary Educational Psychology 30(1): 96-116.

Rau, W., & Durand, A. (2000). The academic ethic and college grades: Does hard work help students to "make the grade"? Sociology of Education 73(1): 19-38.

DOI: 10.2307/2673197

Schmidt, R.M. (1983). Who maximizes what? A study in student time allocation, The American Economic Review 73(2): 23-28.

Volume 14, Number 1, March 2019

Stinebrickner, R., & Stinebrickner, T.R. (2004). Time-use and college outcomes, Journal of Econometrics 121(1-2): 243-269. DOI: 10.1016/j.jeconom.2003.10.013

Tho, L.M. (1994). Some evidence on the determinants of student performance in the University of Malaya introductory accounting course, Accounting Education 3(4): 331-340. DOI: 10.1080.096393894000000031

Ward, S.P.; Ward, D.R.; Wilson, T.E., Jr.; & Deck, A.B. (1993). Further evidence on the relationship between ACT scores and accounting performance of black students, Issues in Accounting Education 8 (2), Fall: 239-47.

Wong, D.S., & Chia, Y. (1996). English language, mathematics and first-year financial accounting performance: A research note, Accounting Education 5(2): 183-187. DOI: 10.1080/906392896000000019

Zimmerman, B.J. (2002). Achieving academic excellence: A self-regulatory perspective, In M. Ferrari (ed.), The Pursuit of Excellence in Education (85-110), Hillsdale, NJ: Erlbaum.

ABOUT THE AUTHORS

Helen Wong is a principal lecturer in the Division of Business at the Hong Kong Community College of the Hong Kong Polytechnic University. Her research interests include accounting and finance, management and marketing, and education.

Carmen Sum is a senior lecturer in the Division of Business at PolyU Hong Kong Community College. Her research interests include services marketing, customer relationship management, consumer behavior, and education.