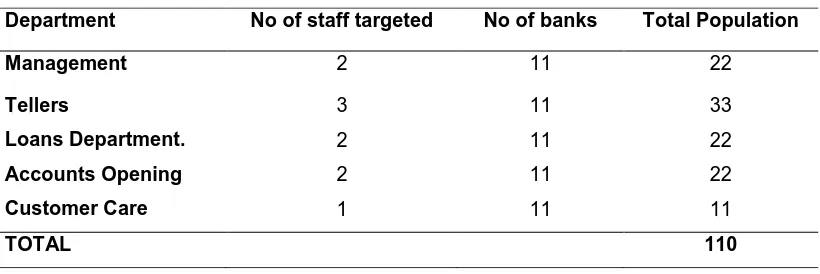

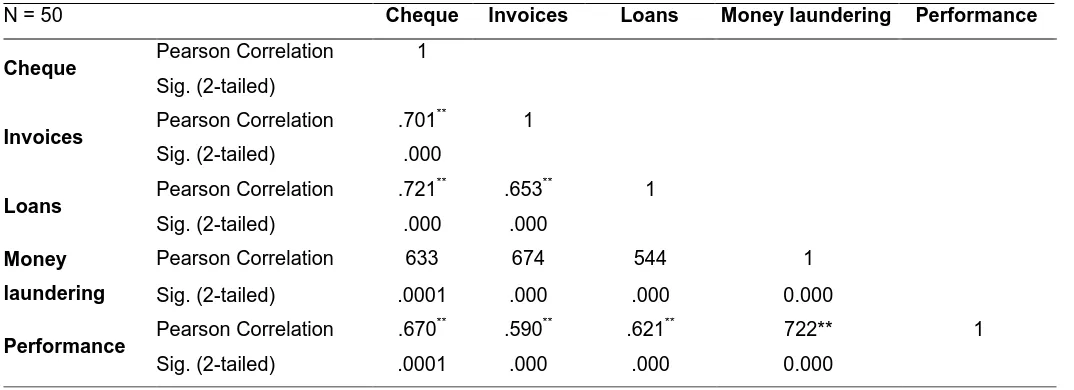

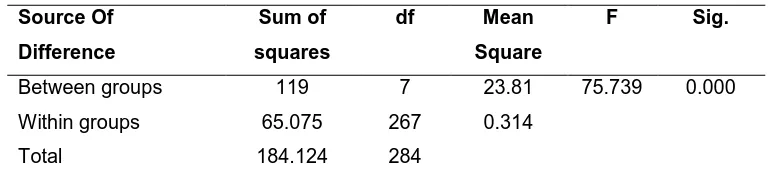

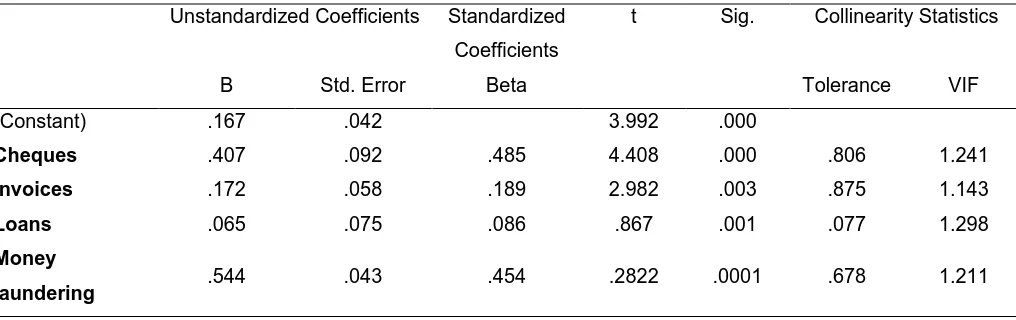

EFFECT OF FINANCIAL FRAUD ON THE PERFORMANCE OF COMMERCIAL BANKS: A CASE STUDY OF TIER 1 BANKS IN NAKURU TOWN, KENYA

Full text

Figure

Related documents

Group 1: Normal diet as a control (C); Group 2: Lead acetate treatment with normal diet and saline supplement (negative control (CCl 4 -con); Group 3: Lead acetate treatment

The Ministère de l’Immigration, de la Diversité et de l’Inclusion is committed to protecting the personal information you provide when you open a Mon projet Québec account.

Aus unseren Ergebnissen zum Zusammenhang von Lernerfolg und Lernstrategien folgern wir zunächst, dass die Strategien selbstorganisierten Lernens grundsätzlich gefördert werden

The extract did not produce any significant effect on haematological parameters after 60 days of administration in all the treatment groups when compared with the control

This research is trying to fill this important gap by divided the whole word into three regions…….this classification is in line with the recent report

COMPASS hadron beam data has been discussed, confirming the (3 π ) − PWA results published from the 2004 data (3 charged pion final states) in two di ff erent decay modes (charged

nucleatum (Figure S2). Selective disruption of the biomass of the bridge colonizer F. nucleatum may explain the effects on multispecies biofilms. To confirm if disruption

Abbreviations: ACCORD, Action to Control Cardiovascular Risk in Diabetes; ADvANCe, Action in Diabetes and vascular Disease: Preterax and Diamicron MR Controlled evaluation;