putting principles into practice

insight’s annual report on responsible investment 2013

the information presented in this document (the “information”) is for information purposes only. under no circumstances should the information be construed as: (i) legal or investment advice; (ii) an endorsement or recommendation to investment in a financial product or service; or (iii) an offer to sell, or a solicitation of an offer to purchase, any securities or other financial instruments.

contents

Foreword

//

5

responsible investment at insight

//

7

how insight meets its commitments

//

11

responsible investment activities in 2013

// 17

how insight implements its responsible investment policY

// 27

stewardship: the neXt phase in responsible investment?

// 45

managing environmental risKs in investment portFolios

// 55

in 2013, the importance of accountability across our public and private institutions came into clear focus. the discussion over how to encourage responsible practice in journalism, banking and politics intensified: perhaps most notably, revelations of widespread surveillance of citizens’ activities, often without the knowledge of our elected representatives, has driven intense debate over how we can effectively hold those in power to account.

at insight, this focus on accountability and responsible practice is not new. we remain committed to encouraging responsible investment by the world’s largest institutions, and hold environmental, social and governance issues at the heart of our investment process. we believe investors can hold company management to account and encourage them to bear such issues in mind. this is at the core of our efforts for clients, as a clear focus on sustainable and responsible conduct can support business growth and generate better returns in the long term.

this report explains insight’s continuing efforts in 2013 to ensure that responsible investing remains an integral part of our investment process. our analysts reported on issues relevant to environmental, social and governance issues for many individual companies, and last year we produced our first annual report focusing on our responsible investment processes with regard to our global farmland investments.

we remain convinced that businesses have a clear impact on the environment and their local communities, and will continue to encourage our peers to adopt a similar approach to their investments.

January 2014

Foreword

Abdallah Nauphal Chief Executive Officer

about insight investment

insight investment is a leading investment management firm. over the past decade we have grown rapidly, based on the quality and focus of our investment capabilities and an open engagement with clients aimed at delivering customised investment solutions.

insight offers multi-asset and absolute return strategies, active global fixed income and currency, real asset strategies, liability risk management and structured solutions. the business is highly rated including ranking number one for both liability driven investment and fixed income management in the greenwich associates 2013 survey1 and is well regarded by

its industry peers, demonstrated by well over 50 significant awards since 2007 including uK pension awards investment manager of the Year 2013, global investor asset manager of the Year 2013, aicio ldi manager of the Year 2013 and Financial news Fixed income manager of the Year 2012.

insight has £273bn2 under management and has been wholly-owned by bnY mellon investment management since

november 2009. insight enjoys complete investment autonomy within bnY mellon’s unique multi-boutique asset management model.

1 source: greenwich associates 2013. uKic Fi-13 fixed income investment: results are based on interviews with 15 uK consultants evaluating fixed income managers; uKic ldi-13 segregated ldi investing: results are based on interviews with 13 uK consultants evaluating ldi managers.

2 assets under management figure represents the combined assets under management of insight investment management (global) limited and pareto investment management limited, which became part of the insight group on 1 January 2013. data as at 31 december 2013. insight’s assets under management are represented by the value of cash securities and other economic exposure managed for clients.

responsible investment at insight

insight remains committed to investing responsibly on behalf of our clients as we pursue their investment objectives. we recognise that institutional investors have a role to play, both as creditors and shareholders, in holding companies’ management to account for their performance and conduct.

our responsible investment policy (see page 9) continues to be guided by three aims: • An appropriate consideration of ESG issues in investment decisions

• The efficient exercise of our governance responsibilities

• Engagement with management to better understand matters that affect the long-term performance of the business the responsible investment policy is implemented by our investment teams with the support of a dedicated responsible investment adviser. the assessment of esg risk is an integral part of our enhanced investment process and our analysts meet regularly with management to discuss all aspects of performance. insight’s investment professionals are equipped with all the information and tools necessary to assess the standards of corporate governance practised by the companies in which we may invest, as well as the management of social and environmental aspects of their business activities.

our principal data provider is gmi ratings (gmi), which provides insight with tailored access to its comprehensive global database of governance and management indicators as well as its full rating reports. this data is incorporated into a proprietary risk scoring and screening tool, maintained by the responsible investment adviser, used during a formal quarterly review of esg risks across a customised coverage universe of over 550 listed companies.

our specialist fixed income credit analysts incorporate esg risks into their investment appraisals, alongside other financial and non-financial risk factors, to form a view on the relative risk and return characteristics of each potential investment. analysts are encouraged to raise any issues of concern with the company. insight monitors all contact we have with management, recording instances where esg issues have been raised with them and the responses received. we also integrate esg considerations in each aspect of the investment process with regard to insight’s farmland

investments. we believe the most sustainable farming operations will be the most profitable. we ensure that relevant issues are identified and the implications assessed as an integral part of the due diligence and investment selection process, and we operate farms using an integrated farm management (iFm) approach, as defined by the european initiative for sustainable development in agriculture.

at a glance: KeY Figures in 2013

• 552 (2012: 492) listed companies in fixed income environmental, social and governance (ESG) coverage • 75 company ESG risk reviews completed

• 7 separate thematic ESG studies undertaken • 1,013 (2012: 903) separate management meetings

• 271 (2012: 192) management meetings in which ESG issues were raised • 2,922 (2012: 2,495) total equity votes cast

• 93 abstentions, withheld or votes against management

responsible investment team

insight investment does not have a separate responsible investment team. our philosophy and approach towards responsible investment places an emphasis on the integration of responsible investment and stewardship principles within investment decision-making. this means that responsibility for considering the environmental, social, and governance (esg) performance of the companies in which we invest rests principally with our team of 35 investment analysts and decision-makers.

insight has, over a number of years, embedded esg considerations into our standard process for investments including equities, fixed income and farmland. to assist our investment professionals in this task we have sourced data and developed proprietary toolkits, described elsewhere in this report, and provided appropriate training where necessary. the investment teams are supported in their responsible investment activities by a specialist who monitors the implementation of our responsible investment policy and acts as an adviser to the analysts and portfolio managers. outside the investment department, representatives from our risk and communications departments assist in surveillance of regulatory developments and codes of practice, and in meeting our commitment to transparency.

insight’s responsible investment policY

insight believes that management can influence the long-term financial performance of companies through an awareness of the environmental and social aspects of their business and by maintaining good standards of corporate governance. as such, responsible investment and asset ownership practices should be accepted and upheld throughout our industry. we therefore support key industry associations such as the uK sustainable investment and Finance association (uKsiF), the institutional investor group on climate change (iigcc), and the carbon disclosure project, alongside initiatives such as the principles for responsible investment in Farmland.

in addition, as a founding signatory to the united nations-supported principles for responsible investment (pri), insight is committed to the principles enshrined by this important global initiative, as well as those of the Financial reporting council’s uK stewardship code. with regard to the implementation of responsible investment practices at insight we are guided by three core aims:

(i) An appropriate consideration of environmental, social and governance (ESG) issues in investment decisions

where material, esg considerations are incorporated in our investment analysis and form a key part of our assessment of the risks inherent in the companies in which we invest. in line with the principles of the un-supported pri we encourage disclosure of esg issues, participate in industry efforts and disclose our practices to our clients. the effective management of environmental, social and other business risks gives an indication of the quality of a company’s overall management. where relevant to investment value or risk, insight’s investment teams monitor the standard of governance in its investee companies and their management of the social and environmental aspects of their businesses. in particular, our investors have access to a proprietary risk scoring framework which covers board

accountability, financial controls, risk management, as well as social and environmental considerations. detailed data is provided by gmi, a specialist governance information provider. with regard to farmland, the investment process assesses a variety of different indicators. the sustainability criteria that apply to each investment have been established with reference to guidelines for integrated Farm management. as is appropriate within each situation, an assessment will be conducted by a combination of the fund’s operational team, the sri committee and, if necessary, external sri expertise.

(ii) The efficient exercise of our governance responsibilities

at insight we take our responsibilities as shareholders seriously and believe that high standards of governance ensure management is held accountable for a company’s performance and conduct. in this regard, we believe that our investment processes are consistent with the principles of the uK stewardship code and allow us to effectively discharge our responsibilities as shareholders.

with respect to share ownership, where insight holds any physical equity positions we routinely vote on behalf of our clients with regard to the uK companies in which they have a shareholding. we employ the services of a specialist proxy voting agency, manifest, which analyses resolutions and tests them against our voting policy templates which

determine the direction of the vote.

(iii) Engagement with companies in the most appropriate way available to better understand matters that materially impact the long-term performance of the business

insight recognises that the long-term performance of the companies in which we invest is, to a considerable degree, influenced by their management and their understanding of the long-term drivers of value and the risks inherent to their businesses. we therefore engage with management where necessary to discuss issues such as strategy, deployment of capital, performance, remuneration principles, and attitudes to risk, including environmental and social issues that may have a material impact on the financial strength of the company. with regard to farmland, insight uses a dynamic integrated farm management approach. specific recommended practices are adapted and incorporated into the management plan for each farm.

subject to client confidentiality, insight is committed to transparency with regard to its research and engagement on social and environmental issues and the effective exercise of its governance responsibilities. a review of insight’s responsible investment activities is published annually.

how insight

meets its commitments

summarY oF insight’s deliverY oF the un-supported pri

the un-supported pri seek to integrate environmental, social and governance (esg) issues into investment decision-making and ownership practices, thereby improving long-term returns to beneficiaries.

they were developed by a group of investment professionals representing 20 large institutional investors from 12 countries who came together at the invitation of the then un secretary-general, Kofi annan, supported by a group of experts from the investment industry, intergovernmental and governmental organisations, civil society and academia.

at launch in april 2006, institutions from around the world managing in excess of $2 trillion of assets signed up to the principles. today, nearly 1,200 signatories representing $34 trillion of assets back the pri, demonstrating their mainstream acceptance.1

insight was a founding signatory to the principles and a member of the expert group that developed them. the six principles are designed to be compatible with the investment styles of large institutional investors that operate within a traditional fiduciary framework in any asset class. they provide strong independent endorsement for insight’s efforts over the last 11 years to invest responsibly on behalf of our clients.2

1. Incorporating ESG issues into investment analysis and decision-making processes.

insight has fully integrated esg risk analysis into its investment process. using esg risk scores and screening procedures, fixed income analysts are able to assess the materiality of esg risks as a standard element in their appraisal of potential investments. a formal esg risk review is conducted across the applicable investment universe every quarter, through which a watchlist of higher risk companies is maintained.

2. Being active owners and incorporating ESG issues into ownership policies and practices.

as a large fixed income investor, insight has good access to senior management to discuss corporate strategy, policies and attitudes to risk. our esg risk scoring and review procedures enable us to prioritise and target our esg engagement with companies on issues of concern.

3. Seeking appropriate disclosure on ESG issues by the entities in which we invest.

weaknesses in disclosure practices are revealed in our data, supplied by gmi, and reflected in our esg risk scores. insight’s engagement activities in 2013 have also been directed at improving disclosure of esg-related risks: for example, we continued to support the work of the carbon disclosure project (cdp).

4. Promoting acceptance and implementation of the Principles within the investment industry.

we regularly communicate insight’s approach to the integration and implementation of the principles to our clients and investment consultants. in addition, insight is a member of the steering committee for the Fixed income work stream of the pri, and is working to develop and promote best practice in this asset class.

5. Working together to enhance our effectiveness in implementing the Principles.

in addition to our involvement with the pri, insight has continued to support a number of other key collaborative investor initiatives, including the uKsiF, the iigcc, and the cdp.

6. Reporting on our activities and progress towards implementing the Principles.

insight regularly discloses how esg issues are integrated within our investment process and where we have engaged with companies. this annual review forms part of our commitment to transparency.

1 at april 2013, according to the pri web site: http://www.unpri.org/about-pri/about-pri/

2 For the early evolution of insight’s approach to non-financial risk, see Kerry ten Kate and andy evans, Integrating governance, social, ethical and environmental

summarY oF insight’s deliverY oF the Farmland principles

growing demand for agricultural produce is putting increasing pressure on the farming sector. institutional investors are well placed to provide support, as they can deliver the long-term capital that the sector needs to invest for growth into the future. Farmland is one of the essential supporting pillars of the global population and economy and is central to many lives and communities: it is therefore crucial that such investment is responsible and sustainable.

the principles for responsible investment in Farmland were developed in 2011 to guide institutional investors who wished to invest in farmland in a responsible manner. the Farmland principles are not part of the united nations-supported

principles for responsible investment (pri) initiative, but their agendas are aligned, and it is a requirement that all signatories of the Farmland principles are also signatories of the pri.

as part of our commitment to sri across our investment capabilities, we are also committed to an integrated Farm

management approach, which closes the gap between industrial and organic farming by encouraging farmers to do more to protect and enhance the countryside. this is championed in the uK by linking environment and Farming (leaF), which is one of the six national organisations forming the european initiative for sustainable development in agriculture (eisa).

the ceo of leaF is part of insight’s sri committee. the combination of integrated Farm management and an independent committee helps ensure sri principles are embedded both as part of the due diligence process when making a purchase and in the management of the assets. investing in farmland is not just a way to potentially generate inflation-hedged returns that match liabilities. it can also help promote sustainable agricultural practices for the long term.

1. Promoting environmental sustainability

at insight, we assess the environmental conditions and any relevant impacts of our farmland investments. we endeavour to maintain, and if possible improve, the environmental sustainability of our farming operations.

2. Respecting labour and human rights

insight seeks to employ local and indigenous people in the farmland businesses within which we invest, providing employment opportunities regardless of race or gender and being sensitive to specific local conditions and concerns.

3. Respecting existing land and resource rights

we are committed to operating within existing local frameworks, including engaging positively with local landowners and those with prior rights to land in which we invest.

4. Upholding high business and ethical standards

insight is committed to upholding high business and ethical standards across our business and at the businesses in which we invest. in our farmland investment portfolio, some of the criteria by which we assess where we might invest include a consideration of local laws and customs regarding bribery and corruption.

5. Reporting on activities and progress towards implementing and promoting the principles

insight publishes this report annually, covering all our investment processes and how sri principles are embedded within them. this report includes information on our farmland investments alongside our equities and fixed income processes. we also intend to publish regular reports focusing on our fulfilment of the Farmland principles, and published the first edition in 2013. we intend to use both these documents to show progress towards implementing the Farmland principles, and we expect these reports to encourage other investors to follow suit.

summarY oF insight's deliverY oF the uK stewardship code

as a major fixed income investor, insight welcomed the changes made to the stewardship code in 2012. the revised code has a wider focus across different asset classes and much of the equity-specific language, such as references to shareholder value, has been amended. stewardship is now described as “more than just voting” and is defined to include both

monitoring and engaging on matters of interest to investors. as before, these include strategy, performance and risk, but the revised code adds capital structure, corporate governance, culture and remuneration to the range of issues concerning which investors may wish to monitor and engage companies.

we believe that the revised code properly recognises that stewardship is not the sole responsibility of shareholders. although insight’s equity investment activities are comparatively small, we take our stewardship responsibilities as shareholders seriously. our responsible investment policy states that, where necessary and appropriate, we will engage with companies as part of both our fixed income and equity investment activities in order to understand matters which may materially impact the long-term performance of their business. with respect to our clients’ rights as shareholders, we maintain a voting policy that ensures that we routinely vote on their behalf with regard to the uK companies in which they have a shareholding. we retain the services of manifest, a specialist proxy voting service, to manage our voting activities. manifest’s sophisticated proprietary system analyses resolutions against a set of voting policy templates to determine the direction of the vote. (a summary of insight’s voting activities in 2013 can be found on page 22).

Principle 1: Institutional investors should publicly disclose their policy on how they will discharge their stewardship responsibilities.

our responsible investment policy and statement of compliance with the uK stewardship code are disclosed publicly, on insight’s website and in its annual report on responsible investment, “putting principles into practice”. the latter provides further details on how insight implements its policy and integrates stewardship activities, including monitoring and engaging with companies, within the wider investment process on behalf of our clients.

Principle 2: Institutional investors should have a robust policy on managing conflicts of interest in relation to stewardship and this policy should be publicly disclosed.

insight has a publicly disclosed policy on managing potential conflicts of interest in relation to stewardship. it sets out three overriding principles: (i) that insight does not ordinarily act as principal; (ii) equal treatment of all clients; and (iii) effective chinese walls between insight and its parent group. the policy identifies circumstances in which conflicts may arise and how they should be handled. with regard to voting, it states that insight will always seek to act in the best interests of its clients when making investment decisions or casting votes on their behalf. where bnY mellon, insight or the clients themselves have business relationships with investee companies, these will be disregarded by insight in making its investment or voting decisions.

Principle 3: Institutional investors should monitor their investee companies.

insight’s responsible investment policy states our belief that company management can influence the long-term financial performance of companies through an awareness of the environmental and social aspects of the business and by maintaining good standards of corporate governance. we routinely monitor the performance, value and risks of the

companies in which we invest. in addition, we regularly review esg risks in our fixed income investments using data provided by a specialist data provider. insight maintains and publishes a record of the contact we have with companies, the purpose of any meetings, and whether specific esg issues have been discussed.

Principle 4: Institutional investors should establish clear guidelines on when and how they will escalate their stewardship activities.

insight’s risk monitoring procedures (see principle 3) help our investment teams identify areas of concern, including issues of corporate governance or matters relating to the environmental and social aspects of an investee company’s activities. meetings with company management provide the most effective and timely opportunity to raise these issues. if insight does not already have regular meetings with a company’s management, our investment teams are encouraged, in the first instance, to request a meeting with them. where this is not possible, or additional action is deemed appropriate in order to further the interests of our clients, we may consider raising the issues with the company’s broker or, if appropriate, the chairman.

Principle 5: Institutional investors should be willing to act collectively with other investors where appropriate.

insight joins with other institutional investors when it believes it to be in the interests of clients, and it is deemed the most appropriate course of action to address a specific issue or concern. to this end, insight has worked with other investors as members of, or signatories to, industry bodies or campaigns, through collective engagement initiatives, and through its participation in working groups. we publish details of these each year in our report on responsible investment activities.

Principle 6: Institutional investors should have a clear policy on voting and disclosure of voting activity.

with respect to share ownership, where insight does hold physical shareholdings in uK companies we routinely exercise our vote on behalf of our clients. we employ the services of a specialist proxy voting agency, manifest, which analyses resolutions and tests them against our voting policy templates to determine the direction of the vote. Further details are provided in our separately published voting policy. our voting activities are disclosed annually in our report on responsible investment.

Principle 7: Institutional investors should report periodically on their stewardship and voting activities.

insight publishes a detailed annual report about its responsible investment activities, on its website, together with separate copies of its responsible investment policy and voting policy. our annual report provides detailed descriptions and data relating to policy implementation, esg risk analysis and key themes, case studies, company engagement activities, participation in collective initiatives and voting activity.

the bnY mellon code oF conduct

insight investment has been wholly-owned by bnY mellon investment management since november 2009, and its employees agree to abide by bnY mellon’s code of conduct.

titled “doing what’s right”, the code is based on the belief that working together to promote ethical behaviour generates positive social effects. building on this reputation for honesty, accountability and transparency is essential to achieving our goal of making bnY mellon the trusted global leader in investment management and investment services. we understand the company’s customers and shareholders expect the company and its employees to conduct business activities not only in full compliance with all laws and regulations, but also in accordance with the highest possible standards of ethical conduct.

when ethical situations arise in the normal course of doing business, the company encourages all stakeholders to make decisions that are consistent with its reputation for integrity. a number of resources are available, including:

• A dedicated Ethics Office to assist employees when they need guidance • The company’s Code of Conduct

• The company’s Personal Securities Trading Program

• Options to report suspected or actual breaches of law, regulations, the Code of Conduct, or the Personal Securities trading program

every employee receives annual ethics training that focuses on the importance of ethical behaviour and understanding the company's code of conduct, related policies and values. the objective is to assist employees in understanding the importance of their individual decisions in ensuring corporate-wide ethical business conduct. each year all employees are required to reaffirm their compliance with the code and related policies. employees are required to confirm their obligation to uphold the company's values and to do business in full compliance with the code.

Values and key principles

the bnY mellon values provide the framework for decision-making and guide our business conduct. incorporating these values into our actions helps us to do what is right and protect the reputation of the company. these values explain what we stand for, our shared culture, and the promises we make to our clients and other stakeholders:

• Client focus • Trust • Teamwork • Outperformance

our code of conduct is expressed under key principles which set out in detail how we put our values, policies and procedures into action:

• Respecting others • Avoiding conflicts • Conducting business • Working with governments • Protecting assets

responsible investment

activities in 2013

insight’s responsible investment policy (see page 9) incorporates three core aims:

• An appropriate consideration of environmental, social and governance (ESG) issues in investment decisions • The efficient exercise of our governance responsibilities

• Engagement with companies in the most appropriate way available to better understand matters that materially impact the long-term performance of the business

together, these three policy commitments reflect insight’s approach to responsible investment in close adherence to the practical principles laid down by both the un-supported principles for responsible investment (pri) and the Frc’s stewardship code. the pri’s first two principles concern the incorporation of esg issues into investment analysis and decision-making and to engage actively with the companies in which an investment is made. together with the stewardship code’s principles 3 and 4, regarding the monitoring of investee companies and the escalation of issues of notable concern with management, these have been explicitly reflected in insight’s responsible investment policy and put into practical effect in our investment processes.

in this section we summarise the activities and initiatives that insight has undertaken during 2013, demonstrating our ongoing commitment to being a responsible investor. with regard to our investment processes, we have implemented our responsible investment policy in two important areas of our business: fixed income and farmland. in each case, we have included esg considerations in our decision-making procedures and engage with management. these are discussed in detail later in the report.

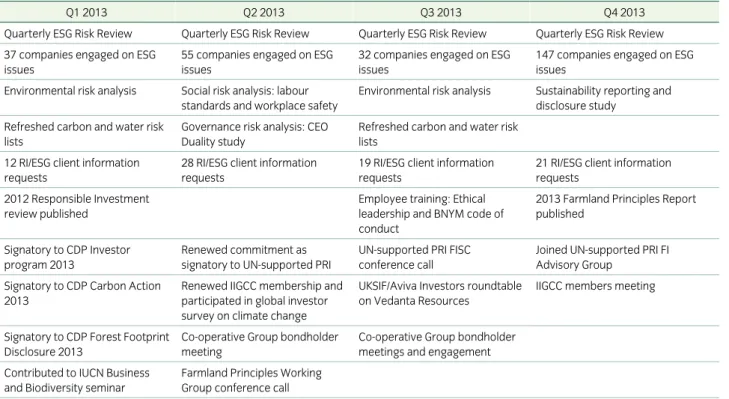

Table 1: Key activities and achievements in 2013

Q1 2013 Q2 2013 Q3 2013 Q4 2013

Quarterly esg risk review Quarterly esg risk review Quarterly esg risk review Quarterly esg risk review 37 companies engaged on esg

issues

55 companies engaged on esg issues

32 companies engaged on esg issues

147 companies engaged on esg issues

environmental risk analysis social risk analysis: labour standards and workplace safety

environmental risk analysis sustainability reporting and disclosure study

refreshed carbon and water risk lists

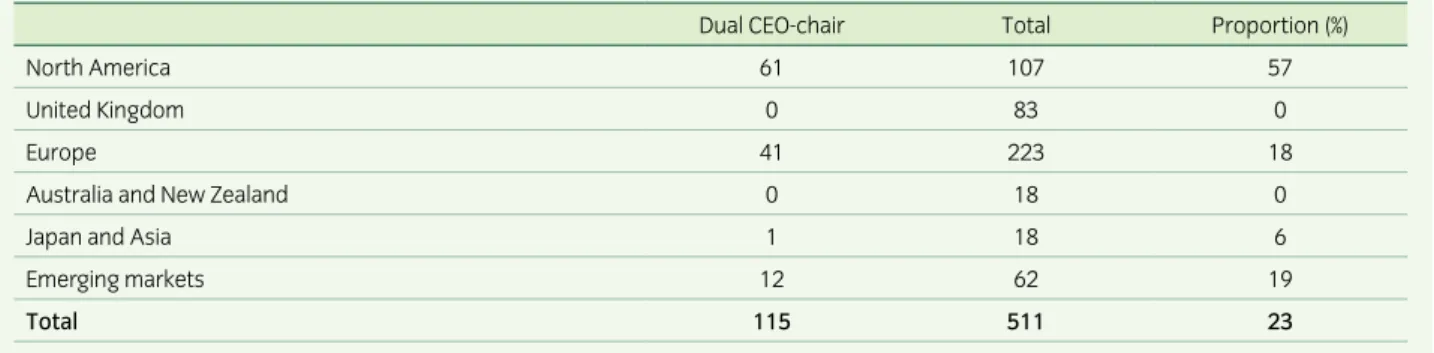

governance risk analysis: ceo duality study

refreshed carbon and water risk lists

12 ri/esg client information requests

28 RI/ESG client information requests

19 ri/esg client information requests

21 ri/esg client information requests

2012 responsible investment review published

employee training: ethical leadership and bnYm code of conduct

2013 Farmland principles report published

signatory to cdp investor program 2013

renewed commitment as signatory to un-supported pri

un-supported pri Fisc conference call

Joined un-supported pri Fi advisory group

signatory to cdp carbon action 2013

renewed iigcc membership and participated in global investor survey on climate change

uKsiF/aviva investors roundtable on vedanta resources

iigcc members meeting

signatory to cdp Forest Footprint disclosure 2013

co-operative group bondholder meeting

co-operative group bondholder meetings and engagement contributed to iucn business

and biodiversity seminar

Farmland principles working group conference call

insight’s main activities and achievements regarding responsible investment in 2013 are summarised above (see table 1), divided into internal activities, which refer to our own investment processes and client reporting, and external activities, which involved collaboration with others.

our internal activities in 2013 included the systematic integration of esg analysis and engagement within our fixed income credit area, beginning with the esg review procedure we follow each quarter covering over 550 listed companies by the end of the year (see page 27). we also conducted separate esg studies and analyses to examine important risks and themes, including carbon and water-related risks within our investment universe, the widespread adoption of sustainability reporting, the persistence of joint ceo-chairman roles on company boards, and risks relating to labour standards and workplace safety. For the first time, we tracked the volume of requests we receive from prospective clients for information on our responsible investment practices and esg in general (see Figure 1).

Figure 1: Requests for information on responsible investment practices and ESG practice Number of requests 0 5 10 15 20 25 30 Q4 2013 Q3 2013 Q2 2013 Q1 2013 ■ UK 46 ■ France 11 ■ Germany 5 ■ Japan 4 ■ Switzerland 4 ■ Australia 3 ■ USA 3 ■ Netherlands 2 ■ Europe 1 ■ Spain 1 12 28 19 21 Origins of requests 0 5 10 15 20 25 30 Q4 2013 Q3 2013 Q2 2013 Q1 2013 ■ UK 46 ■ France 11 ■ Germany 5 ■ Japan 4 ■ Switzerland 4 ■ Australia 3 ■ USA 3 ■ Netherlands 2 ■ Europe 1 ■ Spain 1 12 28 19 21

our analysis of esg issues, integrated within the investment process, aims to enhance the quality of decision-making and facilitate the careful monitoring of client investments. we routinely meet with the management of investee companies, or potential investments, to discuss all aspects of performance, and the analysis of esg risks enables our analysts to have informed and effective conversations with company management. this active role that institutional investors perform in relation to their client’s portfolios is increasingly referred to as “stewardship” (see page 45 for further discussion of stewardship). it is the application of a much broader concept of responsible management to the activities of investment intermediaries.

Stewardship

according to the Financial reporting council (Frc), stewardship activities include monitoring and engaging with companies on strategy, performance, risk, capital structure, and corporate governance, including culture and remuneration.

engagement is defined in the code as “purposeful dialogue” with a company’s management or board on these matters, as well as on issues that are the subject of votes at general meetings.

in the spirit of the Frc stewardship code and principle 1 of the un-supported pri, insight does not make a sharp distinction between esg and other investment considerations. within fixed income, for example, esg is regarded as a subset of risk factors which form an integral part of our credit analysis and subsequent investment appraisal. as a result, esg issues are frequently raised as part of our normal dialogue with company management (see Figure 2).

during 2013 insight recorded 1,013 separate interactions between its decision-makers in the fixed income and equities areas and company management. this represents a 12% increase on 2012, partially reflecting a generally buoyant environment for capital markets: 264 meetings were held to discuss proposed new issuance of corporate securities compared to 201 in the previous year. nevertheless, over half of the meetings attended by insight’s analysts and portfolio managers were unrelated to new capital raising and provided an opportunity to receive an update on company performance and to discuss management’s future plans. in nearly two-thirds of all meetings the ceo or cFo was in attendance or,

Figure 2: Dialogue with company management in 2013 Management contact 0 100 200 300 400 500 600 700 ■ Private meetings (1:1) 389 ■ Group meeting 313 ■ Telephone (1:1) 23 ■ Conference call 43 ■ AGM/EGM 1 ■ Presentation 102 ■ Other event 4 ■ Site visit 4 ■ Not classified 134 ■ General update 495 ■ Results update 77 ■ New issue/IPO 264 ■ Strategy 13 ■ M&A 17 ■ ESG-specific 14 ■ Not classified 133 ■ Chairman 6 ■ Board member 2 ■ CEO 357 ■ CFO/FD 286 ■ CRO 0 ■ Treasurer 88 ■ Capital markets 39 ■ CSR officer 11 ■ IR officer 115 ■ Senior manager(s) 49 ■ Not classified 60 2013 2012

■ Yes ■ No ■ Not classified Management contact

Purpose

Senior officer present

ESG issues discussed

271 603 139 192 575 136 Number of meetings

Numbers of meetings with senior officer present

0 100 200 300 400 500 600 700 ■ Private meetings (1:1) 389 ■ Group meeting 313 ■ Telephone (1:1) 23 ■ Conference call 43 ■ AGM/EGM 1 ■ Presentation 102 ■ Other event 4 ■ Site visit 4 ■ Not classified 134 ■ General update 495 ■ Results update 77 ■ New issue/IPO 264 ■ Strategy 13 ■ M&A 17 ■ ESG-specific 14 ■ Not classified 133 ■ Chairman 6 ■ Board member 2 ■ CEO 357 ■ CFO/FD 286 ■ CRO 0 ■ Treasurer 88 ■ Capital markets 39 ■ CSR officer 11 ■ IR officer 115 ■ Senior manager(s) 49 ■ Not classified 60 2013 2012

■ Yes ■ No ■ Not classified Management contact

Purpose

Senior officer present

ESG issues discussed

271 603 139 192 575 136 Number of meetings Purpose of meeting 0 100 200 300 400 500 600 700 ■ Private meetings (1:1) 389 ■ Group meeting 313 ■ Telephone (1:1) 23 ■ Conference call 43 ■ AGM/EGM 1 ■ Presentation 102 ■ Other event 4 ■ Site visit 4 ■ Not classified 134 ■ General update 495 ■ Results update 77 ■ New issue/IPO 264 ■ Strategy 13 ■ M&A 17 ■ ESG-specific 14 ■ Not classified 133 ■ Chairman 6 ■ Board member 2 ■ CEO 357 ■ CFO/FD 286 ■ CRO 0 ■ Treasurer 88 ■ Capital markets 39 ■ CSR officer 11 ■ IR officer 115 ■ Senior manager(s) 49 ■ Not classified 60 2013 2012

■ Yes ■ No ■ Not classified Management contact

Purpose

Senior officer present

ESG issues discussed

271 603 139 192 575 136 Number of meetings

ESG issues discussed

0 100 200 300 400 500 600 700 ■ Private meetings (1:1) 389 ■ Group meeting 313 ■ Telephone (1:1) 23 ■ Conference call 43 ■ AGM/EGM 1 ■ Presentation 102 ■ Other event 4 ■ Site visit 4 ■ Not classified 134 ■ General update 495 ■ Results update 77 ■ New issue/IPO 264 ■ Strategy 13 ■ M&A 17 ■ ESG-specific 14 ■ Not classified 133 ■ Chairman 6 ■ Board member 2 ■ CEO 357 ■ CFO/FD 286 ■ CRO 0 ■ Treasurer 88 ■ Capital markets 39 ■ CSR officer 11 ■ IR officer 115 ■ Senior manager(s) 49 ■ Not classified 60 2013 2012

■ Yes ■ No ■ Not classified Management contact

Purpose

Senior officer present

ESG issues discussed

271 603 139 192 575 136 Number of meetings

since esg factors form an integral component of our decision-making process, esg issues have become an area of specific focus in our discussions with company management. insight believes that companies are increasingly prepared and willing to discuss esg issues with current and potential investors. over the course of 2013, esg issues were raised with

management on 271 separate occasions, compared to 192 the previous year. the ceo or chairman was present in 73 of these meetings, compared to 56 meetings in 2012. in only 42 of these meetings was the csr officer or an investor relations specialist the most senior company officer present.

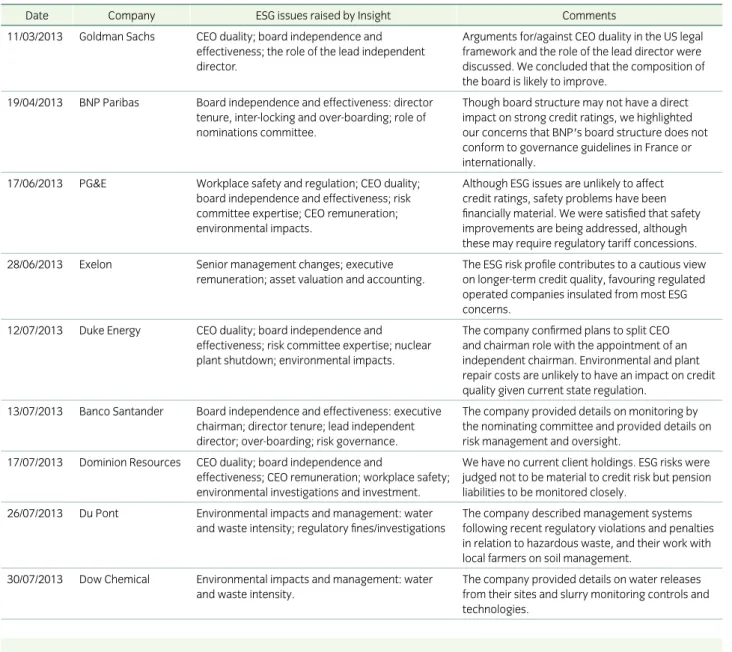

insight also holds meetings or conference calls with company management specifically to discuss esg issues. a total of 17 such meetings took place in 2013, compared to only two in 2012. however, on only one occasion was the ceo present. in most cases specific enquiries of this kind are handled by a dedicated csr officer, as in 11 meetings over the year, or an investor relations specialist, as was the case in four meetings. see table 2 for details of some meetings between insight and company management that were focused specifically on esg concerns.

0 5 10 15 20 25 30 2013 2012 2011 %

Proportion of management meetings in which ESG issues were raised (%)

sustainabilitY reporting in insight’s esg universe

insight considers access to company management to be very important. it provides a vital opportunity to hear at first hand the management’s view of business prospects, their attitude to risk, and to seek clarification on key policies, governance and internal controls. sometimes these meetings enable our decision-makers to learn more about the company or its industry than we can glean from their published reports and statements alone. indeed, as a result of our fixed income esg review process our analysts will often recommend that the investment implications of the issues identified through our risk screening procedure are inconclusive, pending clarifications from the management. in general, greater transparency by companies leads to accurate and efficient decision-making by investors. the initial identification of esg issues or risks relies heavily on companies’ own reporting and disclosure. the better the esg information we, and our information provider gmi ratings, have access to, the more effective the time we spend with management can be. insight therefore encourages companies to release appropriately detailed information, ideally in a standardised and harmonised reporting framework, that can assist our analysts in understanding the esg and other non-financial risks and opportunities facing the companies in we invest on our client’s behalf.

we therefore welcome sustainability reporting frameworks such as the global reporting initiative (gri) and that of the international integrated reporting council. corporate reporting facilitates stewardship by ensuring that the dialogue between companies and their investors is indeed purposeful and effective.

Table 2: Examples of ESG-specific engagement

date company esg issues raised by insight comments 11/03/2013 goldman sachs ceo duality; board independence and

effectiveness; the role of the lead independent director.

arguments for/against ceo duality in the us legal framework and the role of the lead director were discussed. we concluded that the composition of the board is likely to improve.

19/04/2013 bnp paribas board independence and effectiveness: director tenure, inter-locking and over-boarding; role of nominations committee.

though board structure may not have a direct impact on strong credit ratings, we highlighted our concerns that bnp's board structure does not conform to governance guidelines in France or internationally.

17/06/2013 pg&e workplace safety and regulation; ceo duality; board independence and effectiveness; risk committee expertise; ceo remuneration; environmental impacts.

although esg issues are unlikely to affect credit ratings, safety problems have been financially material. we were satisfied that safety improvements are being addressed, although these may require regulatory tariff concessions. 28/06/2013 exelon senior management changes; executive

remuneration; asset valuation and accounting.

the esg risk profile contributes to a cautious view on longer-term credit quality, favouring regulated operated companies insulated from most esg concerns.

12/07/2013 duke energy ceo duality; board independence and effectiveness; risk committee expertise; nuclear plant shutdown; environmental impacts.

the company confirmed plans to split ceo and chairman role with the appointment of an independent chairman. environmental and plant repair costs are unlikely to have an impact on credit quality given current state regulation.

13/07/2013 banco santander board independence and effectiveness: executive chairman; director tenure; lead independent director; over-boarding; risk governance.

the company provided details on monitoring by the nominating committee and provided details on risk management and oversight.

17/07/2013 dominion resources ceo duality; board independence and

effectiveness; ceo remuneration; workplace safety; environmental investigations and investment.

we have no current client holdings. esg risks were judged not to be material to credit risk but pension liabilities to be monitored closely.

26/07/2013 du pont environmental impacts and management: water and waste intensity; regulatory fines/investigations

the company described management systems following recent regulatory violations and penalties in relation to hazardous waste, and their work with local farmers on soil management.

30/07/2013 dow chemical environmental impacts and management: water and waste intensity.

the company provided details on water releases from their sites and slurry monitoring controls and technologies.

In Q4 2013 we repeated an earlier survey of our entire ESG coverage universe, consisting at that time of 548 listed companies, to see how many of them publish sustainability reports, and what proportion of these adopted the gri framework for doing so.

high environmental and social impact

Sustainability reporting No Yes Total

Yes 31 402 433

no 0 115 115

Total 31 517 548

source: insight and gmi ratings.

We found that 402 (78%) companies which operate in either environmentally or socially sensitive industries published information on their sustainability performance, either in a separate report or on a dedicated part of their corporate website. a much smaller proportion however published their sustainability information to the gri reporting standard. less than half of the same group of companies (230 or 44%) report in accordance with the gri framework.

sustainability reporting

Country Yes No

basic materials 49 9

cyclical consumer goods / services 64 19

energy 26 10

Financials 110 41

healthcare 12 5

industrials 58 11

non-cyclical consumer goods / services 39 5

technology 15 2

telecommunications services 27 5

utilities 33 8

Total 433 115

source: insight and gmi ratings.

Across Insight’s coverage universe, we found that between 71% and 89% of the companies in each of the industry groups undertook some kind of sustainability reporting. the range of gri reporting was however both lower and wider at between 29% (cyclical consumer) and 82% (technology).

sustainability reporting

Country Yes No Total

australia and new Zealand 16 3 19

Japan and asia 13 5 18

emerging markets 38 24 62 canada 13 0 13 united states 98 29 127 europe 188 38 226 united Kingdom 67 16 83 Total 433 115 548

source: insight and gmi ratings.

geographically, the proportion of companies that publish sustainability information within each region ranged from 100% in Canada (13 companies) to 61% in emerging markets. Of the major regions, the US (77%) lagged Europe (83%).

VOTING POlICY

with respect to share ownership, in the majority of the current equity investment strategies insight does not have material investments in physical holdings. where insight does hold physical equity positions we routinely vote on behalf of our clients with regard to uK companies in which they have shareholding.

insight retains the services of manifest information services for the provision of proxy voting services and votes at meetings where it is deemed appropriate and responsible to do so. manifest provides research expertise and voting tools through sophisticated proprietary it systems allowing insight to take and demonstrate responsibility for voting decisions.

independent corporate governance analysis is drawn from thousands of market, national, and international legal and best practice provisions from jurisdictions around the world.

independent and impartial research provides advance notice of voting events and rules based analysis to ensure

contentious issues are identified. manifest analyses any resolution against insight-specific voting policy templates which will determine the direction of the vote. where contentious issues are identified, these are escalated to insight for further review and direction.

Insight 2013 voting statistics

meeting type number of meetings number of resolutions (votes)

agm 173 2842 class 5 5 court 0 0 egm 10 27 gm 17 48 sgm 0 0 Total 205 2922

Insight 2013 abstentions and withheld votes

resolution type abstain against withhold total

annual report 1 1

auditor remuneration 1 1

director election 13 13

dividend 1 1

ltip / share plan 9 3 12

remuneration report 33 1 26 60

share issuance 1 3 4

share repurchase 1 1

Total 60 1 32 93

COllABORATIVE ENGAGEMENT

both the principles for responsible investment (pri) and the Frc stewardship code call on institutional investors to work together to promote responsible and active ownership across the industry. the pri’s principle 5 encourages investors to act together to enhance effective implementation of the principles. activities may include supporting or participating in

networks, information sharing platforms or other collaborative initiatives. principle 5 of the stewardship code is somewhat narrower, calling investors to be willing to act collectively with other investors, where appropriate, to improve the

effectiveness of their engagement with companies.

we believe that collective efforts are particularly appropriate to address issues of common concern beyond specific investment decision-making. these include matters such as disclosure and reporting, as well as other aspects of good

case studY: investor roundtable on vedanta resources

insight was invited to attend an investors' roundtable with vedanta resources, a global natural resources company, hosted by uKsiF and aviva investors. the purpose of the meeting was to examine the progress vedanta has made in improving its sustainability performance. it followed the publication of the fourth progress report by esg research specialist eiris. insight accepted the invitation to attend the meeting; it was a good opportunity for a number of concerned investors to engage collectively with the company and express commonly-held concerns. the meeting took place on 22 July 2013. mark eadie, the company’s chief sustainability officer, presented an update at the meeting while also in attendance were representatives from eiris and amnesty international.

vedanta resources featured on our esg watchlist during 2012 and 2013 due to its overall esg performance and also its environmental risk score. as such, vedanta has been closely monitored by insight’s analyst team and subject to periodic review. the company has had a chequered recent history with a number of esg events within the last three years: these stretch back to a controversial mining operation in orissa, india, accused in 2010 of ignoring the rights of local people, as well as violating environmental regulations. these have resulted in a drive by the company to improve its esg performance, signalled by the appointment of a chief sustainability officer and a strengthening of sustainability programs and reporting. these have not halted concerns raised by continuing regulatory investigations and fines relating to environmental failings. moreover, its environmental impacts remain significantly higher than its peers. to its credit, vedanta is working hard to improve its reputation. Following the meeting with the company insight’s credit analyst updated his esg review of the company. he acknowledged the improvements the company was making to its environmental governance and systems, including internal controls and risks management, which we expect will lead to an improvement in its esg performance and risk scores. these improvements include processes for engaging with and seeking the informed consent of local stakeholders in relation to new projects. however, our analyst had residual concerns about the complex organisational and legal structure of the group, and therefore the strength of the lines of accountability and responsibility down to the level of individual operations around the world. this remains a great challenge for management but the company, we feel, is moving in the right direction.

corporate governance practice. collective engagement, advocacy and joint campaigning can also be particularly effective by mobilising the weight of the investor community to influence company or industry behaviour and occasionally to pursue agreed public policy goals.

with respect to these important principles, insight supports a small number of collaborative industry initiatives and investor forums where we believe doing so is likely to be more effective than acting alone. we review the support we give each year and at the start of 2013 insight chose to continue to participate in six initiatives:

• Investor CDP program • CDP Carbon Action 2013 • CDP Water program 2013

• Forest Footprint Disclosure project

• 2013 Global Investor’s Statement on Climate Change • Institutional Investors Group on Climate Change

in addition, insight renewed its membership of the uK sustainable investment and Finance association (uKsiF), the uK’s leading network for sustainable and responsible financial services.

case studY: addressing social risKs in the waKe oF the rana plaZa tragedY

on 24 april 2013, rana plaza, an eight-storey building in the savar district of dhaka, bangladesh collapsed killing over 1,100 people. about 2,500 people were rescued alive from the building in the days after its collapse. the building contained garment factories which supplied apparel for several well-known international clothing brands.it was subsequently revealed that the upper storeys of the building had been built without a permit and that the building was never designed to house factory machinery. the dhaka authorities filed a case against the owners of the building and on international worker’s day on 1 may workers protested on the streets. demonstrations continued over the following months while the government stepped up workplace safety measures, closing 18 garment factories in the immediate aftermath of the rana plaza collapse and promising more to follow. the tragedy brought widespread

condemnation from politicians and advocacy groups, as well as a threat of litigation. in london, protesters demonstrated outside the offices of primark, which subsequently offered to pay compensation to the families of the victims.

the rana plaza tragedy drew a prompt response from the apparel industry which drew up a new accord on Factory and Building Safety a week after the collapse. By 23 May, 38 companies had signed the accord but a group of 17 US

companies refused to do so, preferring an alternative plan already under negotiation to improve factory safety in bangladesh. unlike the accord joined by most european retailers, the us plan does not include legally binding commitments to pay for safety improvements.

these events prompted insight to undertake a survey in may 2013 of the social performance of the companies in its esg coverage universe, across a total of eight separate indicators covering the following themes:

• Overall social impact • Human rights violations • Labour standards and practices • Forced and child labour in supply chains • Workplace safety, auditing and reporting

we found that failings of a relatively minor or more significant nature are commonplace in our investment universe. across our universe which consisted of over 500 companies at the time, 365 companies with high social impacts had been flagged for a failure in at least one of these areas. of these 329 had not met the criteria for admission to insight’s esg watchlist. wal-mart headed the list with a total of four flags in the areas of human rights, labour practices, sweatshops, and workplace safety. a much smaller number of companies had been subject to allegations or

investigations in relation to human rights violations or labour standards, including sweat shops or child labour within the last two years. a total of 43 companies met this criterion for supply chain risks. to examine these risks by industry group we constructed a simple index by calculating the average number of flags per industry (the sum of flag counts divided by the number of observations in each group).

only 29 companies had experienced a workplace safety incident within the previous two years. however, most companies (321) had been flagged for either not having implemented an OSHAS 18001 health and safety management system, or not having disclosed its workplace safety record. this suggests workplace safety remains an important area of attention for insight’s analysts when considering the esg risks in a potential investment.

Insight’s role in the PRI Fixed Income Work Stream

at the end of 2012 the strategy working group of the un-supported pri Fixed income work stream was disbanded. in its place, a smaller steering committee was established to oversee the next phase of the project. insight is one of the 13 institutions represented on the committee, which includes asset managers, asset owners, service providers and industry bodies.

the purpose of the steering committee is to oversee and advise the pri secretariat in its delivery of the Fixed income work stream, the objectives for which are:

• Supporting fixed income investors in their implementation of the Principles

• Promoting responsible investment in this asset class among signatories and non-signatories • Thought leadership on responsible investment in fixed income

• Reaching out to key industry stakeholders to promote this agenda further

during 2013 the main area of focus for the work stream was to develop a better understanding of both esg integration and engagement in the fixed income asset class. its objectives include the wider involvement of major fixed income players, the sharing of knowledge and experience with smaller institutions, the creation of greater clarity around complex esg issues, their integration into decision-making and impact on fixed income portfolios, and widening the adoption of responsible investment policies and best practice.

under the guidance of the steering committee, the work stream is set on a three-phase plan: 1. identify the relationship between esg factors and credit risk

2. investigate the different ways fixed income investors apply esg analysis

3. explore how investors might engage bond issuers to influence their disclosure and management of esg factors a project initiated in Q3 2013, focusing on incorporating esg into credit risk analysis, relates to the second of these three phases. its goal is to promote better application of esg analysis in fixed income by helping investors to understand how their peers are doing this. a project consultant has been retained to undertake the research, the findings and conclusions of which will be presented in a report due to be published in may 2014. the pri has established a small advisory group of signatories with first-hand experience of applying esg analysis to fixed income to directly oversee this project. given its long experience of esg integration in fixed income, insight was asked to join the advisory group and accepted the opportunity to contribute further to the ongoing efforts of the Fixed income work stream.

how insight implements its

responsible investment policY

Responsible investment in fixed income

insight is one of the uK’s largest active fixed income managers. our credit team has an average industry experience of 12 years and a broad range of expertise across the credit market covering investment grade, high yield, loans, distressed debt and asset-backed securities (abs). in addition to traditional benchmarked portfolios, insight also offers its clients a “buy and maintain” bond strategy, which provides institutional investors with diversified exposure to a portfolio of global issuers without the drawbacks of market-weighted index strategies. the strategy is managed to minimise and avoid default risk, while maintaining low to medium portfolio turnover by taking investment decisions based on long-term return potential. our credit selection process incorporates an assessment of environmental, social, and governance (esg) risks alongside financial and other investment considerations. while this is true of all our client portfolios that hold corporate credit risk, it is a particularly important feature of our buy-and-maintain strategy. access to management, confidence in standards of corporate governance, and long-term drivers of risk and return are central features of its approach. as we often intend to hold bonds to maturity, our decision-makers need to be confident in the long-term financial position of the companies in which we invest and have trust in its management.

in this section, we explain how our responsible investment policy plays an integral role in our approach to credit investment, issuer selection and engagement activities.

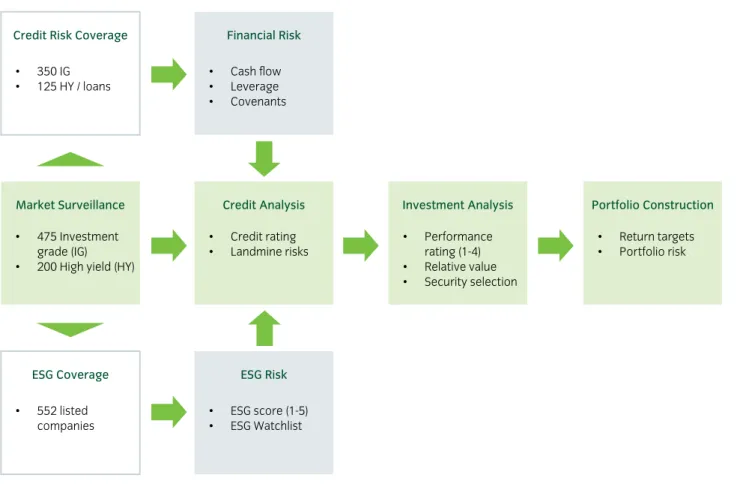

Figure 3: Investment process for credit

Financial Risk

• Cash flow • Leverage • Covenants

Credit Risk Coverage

• 350 IG • 125 HY / loans Credit Analysis • Credit rating • Landmine risks Market Surveillance • 475 Investment grade (IG) • 200 High yield (HY)

Investment Analysis • Performance rating (1-4) • Relative value • Security selection Portfolio Construction • Return targets • Portfolio risk ESG Risk • ESG score (1-5) • ESG Watchlist ESG Coverage • 552 listed companies

CREDIT UNIVERSE

the universe for credit within our fixed income portfolios covers four main areas: investment grade, high yield, loans and abs. within each of these areas, we also consider the merits of cash bonds versus the derivative alternative. the credit universe consists of approximately 475 investment grade issuers, 200 high yield issuers and 1,300 asset-backed issuers under surveillance by our investment teams.

we apply various filters to the market universe to arrive at a smaller group of investable issuers, subject to rigorous fundamental analysis by our credit analysis team, which is one of the largest in-house teams in the uK. we screen out the companies disqualified by insufficient access to financial data and company management and issues which are

insufficiently liquid.

of the investment grade and high yield corporate issuers within our investment universe, our credit analysts also have access to comprehensive esg risk data for over 550 of these companies. this data covers 150 individual indicators provided by gmi ratings inc., which provides detailed information on companies’ esg performance through an online system. a database of these esg risk scores and indicators is maintained by insight’s responsible investment adviser. gmi ratings supplies updated data on a weekly basis and this is used for esg risk screening purposes and to populate our esg watchlist (see page 32).

our credit universe is screened on a regular basis by our credit analysis team and reviewed on a weekly basis to establish research priorities in consultation with portfolio managers.

CREDIT RISK ANAlYSIS

to evaluate the likelihood of future changes in a company’s credit rating and the potential for a sudden change in credit quality, our analysts conduct a detailed credit risk analysis. particular attention is paid to the scoring of key risks using a checklist. this checklist, for so-called “landmine risks”, examines important sources of risk that can lead to a sudden

deterioration in credit quality or that may not be readily apparent from an examination of a company’s financial performance (see box). the key risks are scored on a scale of 1 to 5, with higher numbers indicating greater risk and scores of 5 indicating areas of significant concern. an overall esg risk score is also assigned to each issuer within our esg coverage.

ultimately, default risk is the prism through which the analysts consider esg issues. insight’s credit analyst team is charged with determining the

materiality of esg risks, defined as the contribution these make to the default likelihood of a potential investment. a failure to meet recognised standards of good governance and responsible management may represent threats to financial performance that are not adequately compensated by the expected returns; indeed, effective management of the environmental and social aspects of the business are useful indicators of the overall quality of management. our esg data can provide evidence that management have adopted and implemented appropriate policies, systems, and controls to manage risks and comply with relevant codes, laws and regulations and go beyond them to meet the expectations of key stakeholders.

the analysts will also perform a comprehensive financial analysis, which will typically include an examination of the earnings of an issuer as well as its balance sheet structure, together with a forecast of a company’s future cash flows, debt burden and credit metrics which can be benchmarked against other companies. insight’s analysts assign credit ratings and a trend indicator to the companies they cover, providing our portfolio managers with an opinion on the creditworthiness of a borrower or bond issuer. a full

investment analysis is required to inform an investment decision but esg risk scores are a necessary element in assigning a credit rating that indicates the relative risk of default loss.

the landmine checKlist

• Environmental • Social • Governance • Overall ESG • Liquidity • Contingent liabilities • Regulatory risk • Event riskinsight’s esg risK scores and indicators

insight’s esg information partner, gmi ratings inc, publishes ratings on over 6,000 companies worldwide. it provides an independent assessment of the “sustainable value” of public companies based on 150 separate indicators which insight receives as a weekly updated data feed. gmi’s ratings are mapped on to the five-point risk scale insight has used for its checklist of non-financial risk factors.

our analysts use separate scores for environmental, social and governance categories of risk, along with an overall esg score, as part of their analysis of non-financial risks in their standardised credit risk templates. these scores are also used, in combination with a flag of a companies’ social and environmental impact, to construct our esg watchlist of companies whose esg performance may be below par (see page 32).

insight uses the database of 150 separate indicators to perform other esg screening and analysis. For example, we routinely assess the carbon and water-related risks across our investment universe and during 2013 have also undertaken studies of labour practices and workplace safety standards, as well as other corporate governance issues. the database contains indicators in the following categories:

Governance

• Board accountability and effectiveness • Executive pay policy and oversight • Ownership structure and control • Integrity of accounting practices

Social

• Vendor standards • Employee relations • Bribery and corruption • Diversity

• Political contributions

Environmental

• Climate change risks and disclosure • Environmental reporting

• Board-level environmental governance • Environmental management systems

Events

• Securities class actions

• Transactions, including mergers, acquisitions, divestitures and financings

• Changes in executive compensation • FCPA, bribery and corruption • Events related to product safety

QUARTERlY ESG RISK REVIEW

insight conducts a formal quarterly review of esg risks across its coverage universe of over 550 issuers, along with the evaluation of esg risks for each issuer considered for inclusion in client portfolios. we have developed a screening procedure to target and prioritise those companies for which esg risks may be of particular concern. these companies are then admitted to insight’s esg watchlist maintained and updated by our in-house responsible investment adviser.

the esg watchlist comprises any companies within our esg issuer coverage that score 5 on their overall esg performance. this corresponds to the bottom 5% of companies across gmi ratings’ global database of over 6,000 companies. in addition, we also add to the esg watchlist any issuers operating in industries which have a high social or environmental impact and for which the corresponding social or environmental risk score is also 5.

the esg watchlist is updated each quarter, with particular attention paid to new entrants, issuers whose esg scores have deteriorated, and issuers in which we have client holdings. the head of credit analysis prioritises issuers to be subjected to an in-depth review of the issues revealed by the esg scores and the underlying risk indicators. each special review is subject to sign-off by the head of credit analysis with the burden of proof on the analyst to demonstrate that the risks are not sufficiently material to the investment to merit exclusion from client portfolios.

our credit analysts may reach one of three conclusions from their review of esg risks: avoid, non-material, or engage. with regard to the latter, in many cases, the esg risk review will identify issues or concerns which may need to be resolved through dialogue with the company’s management. a meeting or call may be arranged specifically to raise these issues (see page 19 for statistics from 2013). otherwise, our analysts are expected to enter into a dialogue during our regular round of meetings with a company’s management to gather any further information necessary for a full understanding of the issues raised by the esg screening and review procedure.

Figure 4: Insight’s quarterly ESG screening and risk review

Risk scores Watchlist Analyst review

Overall ESG = 5 or for ‘High impact’

issuers: Environmental = 5 or Social = 5 Overall ESG (1-5) Governance (1-5) Environmental (1-5) Social (1-5) Avoid Engage Non-material • 10 companies • 24 companies • 16 companies • c.140 companies • 50 companies* • >500 companies