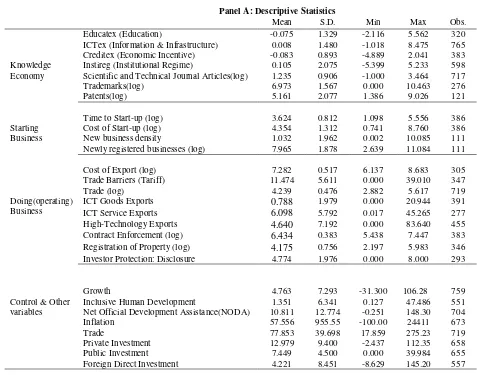

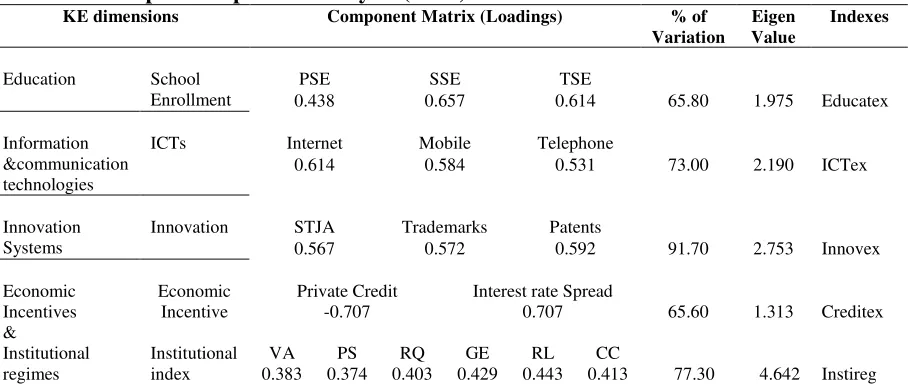

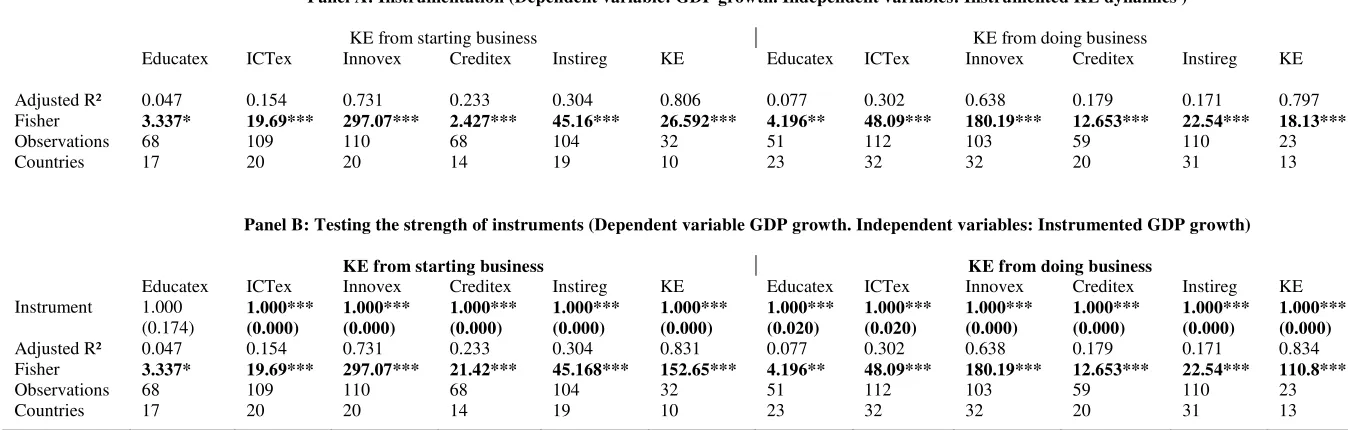

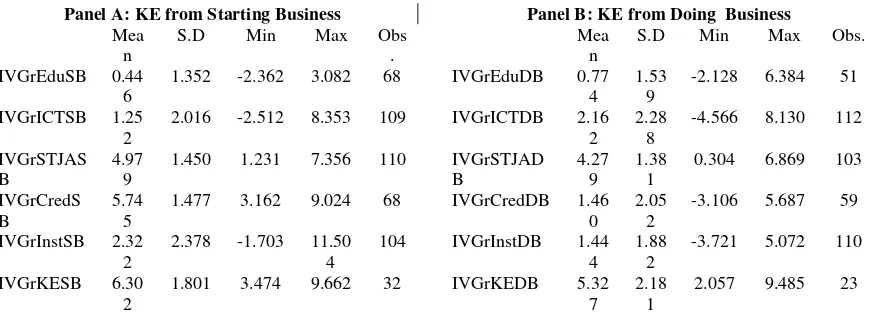

Business Dynamics, Knowledge Economy, and the Economic Performance of African Countries

Full text

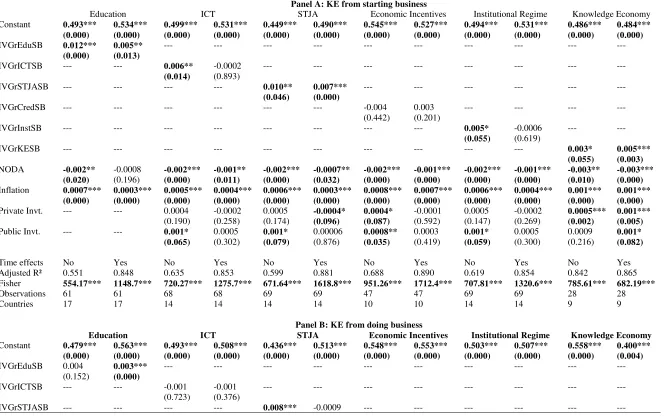

Figure

Related documents

From our results, several inequalities of Hermite-Hadamard type can be derived in terms of functions whose first and second derivatives in absolute value are s -convex functions

In this chapter we review the work related to our management framework in five aspects: functional user requirements decomposition, elasticity rule generation,

The comparison of the classification results for five-year survivors (Table 5B) and nonsurvivors (Table 5C) shows that 95.0% of the patients are correctly classified, although

languages of the same story in order to promote language learning. Stories can be read on diverse mobile devices, such as cellphones and laptops, and can also be downloaded and

Specifically, we aimed to: (a) determine whether demo- graphic characteristics such as age at abduction, age dur- ing baseline, and duration in captivity were related to

HADS: Hospital anxiety and depression scale; COPM: Canadian occupational performance measurement; CSQ: Client satisfaction questionnaire; CBT: Cognitive behavioural therapy;

If Security Areas are to be assigned to a cardholder in the import process, the area name is the Field Name in the first line of the comma delimited file and the Time Schedule ID

- Pack 100 pcs Piede magnetico senza rialzo per “VELA” Low magnetic foot for “VELA”.. Permette al messaggio di fuoriuscire dal fronte del ripiano per aumentare