Asymmetric Business Cycles and Sovereign Default

∗

Grey Gordon

†Pablo A. Guerron-Quintana

‡August 8, 2017

Abstract

What accounts for asymmetric (negatively skewed) business cycles in emerging economies? We show the asymmetry is tied to default risk and that a sovereign default model delivers negative skew.

Keywords: Skewness, Asymmetry, Business Cycles, Default

JEL classification numbers: F34, F41, F44

1

Introduction

Business cycles in emerging economies are characterized by high volatility, output being smoother

than consumption, and recurrent default episodes. A lesser known feature is that business cycles

in these countries are asymmetric, with recessions being more pronounced and lasting longer than

in small developed economies.

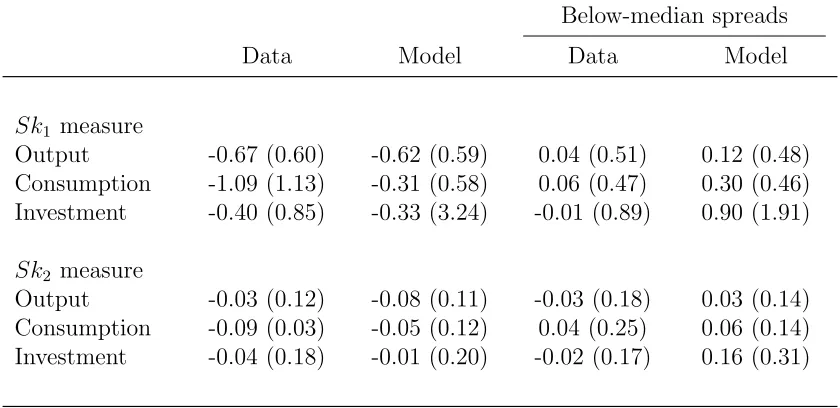

This asymmetry can be seen in Table 1, which gives the skewness for output, consumption,

and investment averaged over five emerging economies that have defaulted in recent history (the

data are described in the appendix). The standard skewness measure, Sk1, finds negative skew in

output, consumption, and investment. The other skewness measure, Sk2, which is more robust to

outliers (Kim and White, 2003), still shows negative skew in all three categories.1

The negative skew in the data is closely tied to default risk, and this can be seen in three ways. One way is to look at a subsample where spreads are below-median and thereby exclude

periods of high default risk and post-default periods. When doing this, the negative skew essentially

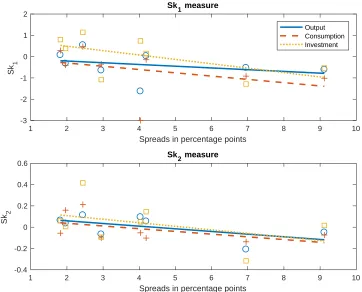

disappears as Table 1shows. A second way is to look at the relationship of spreads and skewness

∗We thank the referee for helpful comments and Diogo Lima for providing us with the EMBI and EMBI+ data.

Any mistakes are our own.

†Indiana University, [email protected]. ‡Boston College and ESPOL,[email protected].

1This measure is defined asSk

2=µ−σQ2, whereµis the mean,Q2is the median, andσis the standard deviation.

Below-median spreads

Data Model Data Model

Sk1 measure

Output -0.67 (0.60) -0.62 (0.59) 0.04 (0.51) 0.12 (0.48) Consumption -1.09 (1.13) -0.31 (0.58) 0.06 (0.47) 0.30 (0.46) Investment -0.40 (0.85) -0.33 (3.24) -0.01 (0.89) 0.90 (1.91)

Sk2 measure

Output -0.03 (0.12) -0.08 (0.11) -0.03 (0.18) 0.03 (0.14) Consumption -0.09 (0.03) -0.05 (0.12) 0.04 (0.25) 0.06 (0.14) Investment -0.04 (0.18) -0.01 (0.20) -0.02 (0.17) 0.16 (0.31)

Note: Statistics are computed using de-trended series, see the appendix for details; standard deviations are in parentheses; the data here are for Argentina, Ecuador, Mexico, Peru, and the Philippines.

Table 1: Skewness Statistics in the Data and Model

across countries. Figure 2does this for eight emerging economies (five high-spread and three low-spread), plotting the data along with best fit lines. There is a clear negative correlation between

spreads and skew for every measure. A third way to see the connection between negative skew

and default risk is to consider that developed small open economies (SOEs) have small or positive

skew. For instance, the averageSk1(Sk2) measure for the five developed SOEs in our sample range

from −0.19 to 0.18 (−0.01 to 0.04) depending on whether one looks at output, consumption, or

investment.

In the next sections, we lay out a SOE real business cycle (RBC) model with default that

delivers asymmetric business cycles. Crucially, it does so for normally-distributed productivity

shocks, i.e., there is no skewness in the underlying stochastic process. We then show how default and default risk drive the asymmetry. Intuitively, times of average or above-average productivity in

the model are as in any other RBC model. However, when productivity falls significantly, economic

activity declines for two reasons: the standard RBC reasons and increased debt-service costs.

Moreover, if default occurs, default costs lower productivity, which severely depresses consumption,

investment, and output. The reduced investment in default also depletes the capital stock, which

prolongs the recession. Consequently, the effects of upward movements in productivity have a

limited and short-lived impact while downward movements can have a drastic and long-lived

impact. This asymmetry results in an endogenous negative skew of consumption, investment, and

1 2 3 4 5 6 7 8 9 10 Spreads in percentage points

-3 -2 -1 0 1 2

Sk

1

Sk1 measure

Output Consumption Investment

1 2 3 4 5 6 7 8 9 10

Spreads in percentage points -0.4

-0.2 0 0.2 0.4 0.6

Sk

2

Sk2 measure

Figure 1: Skewness and default-risk spreads

2

Model and calibration

We briefly describe our model and calibration. For a more full description, seeGordon and

Guerron-Quintana (2017).

2.1

Model

In the long tradition of sovereign default models (Eaton and Gersovitz, 1981; Arellano, 2008;

Mendoza and Yue, 2012), a sovereign borrows in international markets to maximize the welfare of

domestic residents. The residents have consumptionc, supply laborl, and rank consumption/labor

bundles according to aGreenwood, Hercowitz, and Huffman(1988) period utility functionu(c, l) = (c−ηlω

ω)

1−σ/(1−σ) with discount factor β. The sovereign produces output y using capital k and

labor l according to y = Akαl1−α. Productivity follows logA0 = (1−ρ

A) logµA+ρAlogA+ε0A,

where εA ∼N(0, σA2).

The sovereign has access to long-term debt contracts in which outstanding debt matures at

a rate λ. Debt not maturing pays a coupon z. The sovereign’s stock of debt is denoted −b (the

literature uses b as assets by convention). New bond issuance is given by −b0+ (1−λ)b, which is

discounted by a price q.

from credit markets (i.e., goes to autarky). Third, it remains in autarky with probability 1−φ.

Last, for the duration of autarky, a fraction κ(A) of output is lost.

The sovereign’s problem is to solve

V (b, k, m, A) = max

d∈{0,1}(1−d)V

nd(b, k, m, A) +dVd(k, A),

whered is the default choice andVd(Vnd) is the value of defaulting (not defaulting). The variable

m is an i.i.d. endowment shock that aids computation. The value of not defaulting is

Vnd(b, k, m, A) = max

c,l,k0≥0,b0≤0u(c, l) +βEm0,A0|AV (b 0

, k0, m0, A0)

s.t.c+i+q(b0, k0, A)(b0−(1−λ)b) =Akαl1−α+m−Θ

2 (k

0 −

k)2+ (λ+ (1−λ)z)b

k0 =i+ (1−δ)k,

where i is investment and Θ controls the cost of adjusting capital. The value of defaulting or of

being in autarky is

Vd(k, A) = max

c,l,k0≥0u(c, l) +βEm

0,A0|A(1−φ)Vd(k0, A0) +φV(0, k0, m0, A0)

s.t.c+i= (1−κ(A))Akαl1−α−Θ

2(k

0 −

k)2

k0 =i+ (1−δ)k.

The equilibrium debt prices implied by risk-neutral foreign lenders who make zero profits

loan-by-loan (in expectation) are given by

q(b0, k0, A) =Em0,A0|A(1−d(b0, k0, m0, A0))

λ+ (1−λ) [z+q(b00, k00, A0)]

1 +r∗ ,

where b00=b0(b0, k0, m0, A0), k00 =k0(b0, k0, m0, A0), and r∗ is a risk-free international rate on a

one-period bond. Note that default risk, Em0,A0|Ad0, and spreads—an increasing function of 1/q—are

intimately linked.2

2.2

Calibration

We now summarize the calibration, which is the same as in Gordon and Guerron-Quintana(2017).

A period is a quarter. The coupon payment is 3% (z =.03) with 5% of debt maturing each period

(λ = .05), which nearly matches the Argentinean data’s 20 quarter median maturity of average

bonds and 11% value-weighted average coupon rate (Chatterjee and Eyigungor, 2012). Choosing

φ = 0.1, the average stay in autarky is 2.5 years. Following Neumeyer and Perri (2005), we

set ρA = .95, which is a value consistent with Fernandez-Villaverde, Guerron-Quintana,

Rubio-Ramirez, and Uribe, 2011 and much of the SOE business-cycle literature. Mean productivity µA,

the labor disutility parameterη, and depreciationδ are chosen so that, in the steady state without

foreign lending, output, labor, and the investment-GDP ratio equal 1, 1, and 0.05, respectively. The utility curvature σ is set to 2. The remaining parameters are chosen to match six moments

from Argentina’s data: the debt-output ratio −Eb/y, the average spreadEr, the spread volatility

σr, the volatility of investment σi, the volatility of output σy, and relative consumption volatility

σc/σy. InGordon and Guerron-Quintana (2017), we show this calibration delivers simultaneously

the business cycles and default properties of emerging economies such as Argentina.

3

Results and the model mechanism

To compute the model’s skewness statistics, we generate 20,000 simulations of length 75, which is

roughly the number of periods available for each of our developing SOEs. Of these, we keep only

the 14,101 simulations that had at least one default (in agreement with our sample selection for

countries).3 After logging and HP-filtering the model data, we compute the average and standard

deviation of the skewness measures, and these are reported in Table 1. On average, the model

delivers negative skew in output, consumption, and investment in both theSk1 andSk2 measures.

While the averages are all negative, the large standard deviations reflect it is possible to have

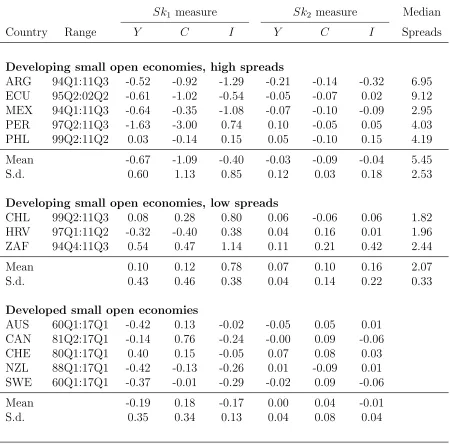

positive skew depending on the simulation. This agrees with the positive skew (depending on the

statistic) that can be found in Peru and the Philippines (see the appendix for a country-specific

breakdown).

As we argued in the introduction, the skewness in the data is driven by default risk, and this is

also true in the model. This can be seen in Table1, where—conditioning on below-median spreads

and hence low default risk—the negative skew disappears, just as in the data. Another way to see

this is that of the 5,899 simulations where a default did not occur, the Sk1 (Sk2) measures range

from −0.03 to 0.89 (−0.01 to 0.02) and so exhibit little or positive skew.

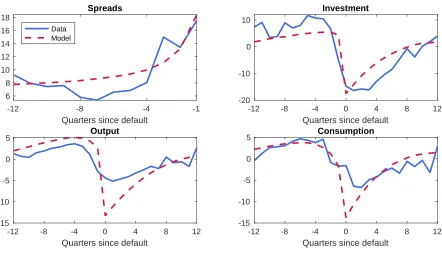

The mechanism producing negative skew can be seen in Figure2, which shows what happens, on

average, before and after a default. In the periods leading to a default, spreads are initially flat but

accelerate upwards in the year just before default. Perhaps surprisingly, investment, consumption

and output rise on average until a few quarters before default. But when spreads start to increase, this trend is reversed: Investment, consumption, and output begin to fall, gradually at first but

accelerating with a sharp collapse at default. The small movements up with larger and faster

movements down—the latter occurring in periods of high spreads and default risk—contribute to

negative skew. As the protracted recession after default is both an unusual (the average quarterly

default rate in the model is 1.3%) and severe period of economic activity, it also generates negative

3If this number seems small, note the model’s quarterly default rate of 1.3% should produce—if default occurred

-12 -8 -4 0 4 8 12

Quarters since default

-20 -10 0 10

Investment

-12 -8 -4 0 4 8 12

Quarters since default

-15 -10 -5 0

5 Consumption

-12 -8 -4 0 4 8 12

Quarters since default

-15 -10 -5 0

5 Output

-12 -8 -4 -1

Quarters since default

6 8 10 12 14 16 18

Spreads

Data Model

Figure 2: Investment Dynamics around Default

skew. The recession itself is triggered by low productivity and default costs, but it is protracted

because of a depleted capital stock due to investment that is up to 20% below trend.

Conditioning on periods where default risk is low, the model generates zero or positive skew. In

these periods, increases and decreases in productivity lead to changes in consumption, investment,

and output that are relatively small and persist at normal business cycle frequencies. In contrast,

when default risk is high, decreases in productivity cause rapid adjustments that—in the case

of a default—lead to severe and long-lasting recessions. Hence, default and default risk produce

negative skew in the model, just as they seem to in the data.

4

Conclusion

Our analysis shows that default and default risk significantly contribute to the negative skew seen

in developing small open economies.

References

C. Arellano. Default risk and income fluctuations in emerging economies. American Economic

Review, 98(3):690–712, 2008.

S. Chatterjee and B. Eyigungor. Maturity, indebtedness, and default risk. American Economic

J. Eaton and M. Gersovitz. Debt with potential repudiation: Theoretical and empirical analysis.

The Review of Economic Studies, 48(2):289–309, 1981.

J. Fernandez-Villaverde, P. Guerron-Quintana, J. Rubio-Ramirez, and M. Uribe. Risk matters:

The real effects of volatility shocks. American Economic Review, 101(6):2530–2561, 2011.

G. Gordon and P. Guerron-Quintana. Dynamics of investment, debt, and default. Review of

Economic Dynamics, Forthcoming, 2017.

J. Greenwood, Z. Hercowitz, and G. W. Huffman. Investment, capacity utilization, and the real

business cycle. American Economic Review, 78(3):402–417, 1988.

T. H. Kim and H. White. On robust estimation of skewness and kurtosis: Simulation and

appli-cation to the S&P500 index. Mimeo, 2003.

E. Mendoza and V. Yue. A general equilibrium model of sovereign default and business cycles.

Quarterly Journal of Economics, 127(2):889–946, 2012.

A. Neumeyer and F. Perri. Business cycles in emerging economies: The role of interest rates.

Journal of Monetary Economics, 52(2):345–380, 2005.

A

Data description and simulation details

National accounts data are collected from the International Financial Statistics and OECD’s

sta-tistical database. The national accounts variables are seasonally adjusted, real, logged and

HP-filtered with smoothing parameter 1600. Following Arellano (2008), the spreads are returns for

EMBI+ and EMBI Blended-Yield Maturity minus the 5-Year Treasury Constant Maturity Rate

(GS5 in FRED, averaged by quarter). Table2gives the time periods used for each country (for the emerging markets, we required spreads data to be available which restricts the sample somewhat).

Figure 2 is reproduced from Gordon and Guerron-Quintana (2017) and uses a slightly different

Sk1 measure Sk2 measure Median

Country Range Y C I Y C I Spreads

Developing small open economies, high spreads

ARG 94Q1:11Q3 -0.52 -0.92 -1.29 -0.21 -0.14 -0.32 6.95 ECU 95Q2:02Q2 -0.61 -1.02 -0.54 -0.05 -0.07 0.02 9.12 MEX 94Q1:11Q3 -0.64 -0.35 -1.08 -0.07 -0.10 -0.09 2.95 PER 97Q2:11Q3 -1.63 -3.00 0.74 0.10 -0.05 0.05 4.03 PHL 99Q2:11Q2 0.03 -0.14 0.15 0.05 -0.10 0.15 4.19

Mean -0.67 -1.09 -0.40 -0.03 -0.09 -0.04 5.45

S.d. 0.60 1.13 0.85 0.12 0.03 0.18 2.53

Developing small open economies, low spreads

CHL 99Q2:11Q3 0.08 0.28 0.80 0.06 -0.06 0.06 1.82 HRV 97Q1:11Q2 -0.32 -0.40 0.38 0.04 0.16 0.01 1.96 ZAF 94Q4:11Q3 0.54 0.47 1.14 0.11 0.21 0.42 2.44

Mean 0.10 0.12 0.78 0.07 0.10 0.16 2.07

S.d. 0.43 0.46 0.38 0.04 0.14 0.22 0.33

Developed small open economies

AUS 60Q1:17Q1 -0.42 0.13 -0.02 -0.05 0.05 0.01 CAN 81Q2:17Q1 -0.14 0.76 -0.24 -0.00 0.09 -0.06 CHE 80Q1:17Q1 0.40 0.15 -0.05 0.07 0.08 0.03 NZL 88Q1:17Q1 -0.42 -0.13 -0.26 0.01 -0.09 0.01 SWE 60Q1:17Q1 -0.37 -0.01 -0.29 -0.02 0.09 -0.06

Mean -0.19 0.18 -0.17 0.00 0.04 -0.01

S.d. 0.35 0.34 0.13 0.04 0.08 0.04

Note: Y, C,and I are output, consumption, and investment respectively; all data have been logged and HP-filtered; country codes are in ISO 3166-1 alpha-3 format.