Page 7 www.ijiras.com | Email: [email protected]

Social Networks, Uptake Of Business Development Programs And

Development Of Microfinance In Rural Ghana: A Case Study Of

Ahanta West District

Michael Asare-Bediako

Department of Mathematics and Statistics, Takoradi Polytechnic, Ghana

Mohammed Frempong

Department of Mathematics and Statistics, Takoradi Polytechnic, Ghana

Dr. Gabriel Asare Okyere Department of Mathematics and statistics, Kwame Nkrumah University of Science and Technology,

Ghana

I. INTRODUCTION

The field of microfinance in Ghana has observed a steady growth in recent years, especially the last decade has seen an accelerated growth in the field of microfinance in terms of activities and infrastructure by both the government and non- governmental organizations in rural areas where hitherto in some years ago would have been a no go areas.

Microfinance has been considered as an important tool to development in the Sub-Saharan Africa and third world countries in general. It has also been seen as tool for enhancing the general wellbeing of the people living in this category of countries. The term microfinance in practise relates to the lending of very small loans to poor people in order to establish a means of alleviating poverty by given the poor an opening to begin a business or to improve an existing

Abstract: The aim of this study is to examine the influence of social networks on the utilization of business development programs and the experience of improvement in businesses operated by women who are clients of microfinance in rural Ghana.

Data were collected by interviewing 225 women from 5 villages in the Ahanta West district in Western Region of Ghana using a structured questionnaire. Results from the study using both social network analysis and statistical methods indicated that experiencing improvement in business and the type of business assistance that a woman uses in her micro business are associated with the characteristics of their social networks. The higher the degree centrality of a woman in her social network, the less likely it is that she will experience improvement in her business and the experience of improvement is significantly associated with the type of business development assistance she used. Using a bivariate logistic regression to explore the likelihood of using professional business development assistance, it was realized that the higher degree centrality of a woman, the less likely she will use professional business development assistance. Investigation further revealed the use of professional business assistance has not yet saturated the villages and that the dominant norm is to use unprofessional business assistance. The perception of the women is that professional business assistance is ‘not needed’. Observations from the sociogram revealed that there was an inward connectivity between those who do not use professional business assistance. The consequence of the findings is that there is a need for norm change intervention among the rural women using a network approach and precisely using those considered as opinion leaders in the villages.

Page 8 www.ijiras.com | Email: [email protected] business. Microfinance is the provision of a broad range of

financial services such as deposits, loans, payment services, money transfers, and insurance to poor and low-income households and, their micro enterprises (ADB, 2000). According to Robinson (1998) “micro finance refers to small scale financial services for both credits and deposits that are provided to people who farm or fish or herd; operate small or micro enterprise where goods are produced, recycled, repaired or traded; provide services; work for wages or commissions; gain income from renting out small amount of land, vehicles, draft animals, or machinery and tools; to other individuals and local groups in the developing countries in both rural and urban areas”. Otero (1999) also define microfinance as “the provision of financial services to low-income poor and very poor self-employed people”. These financial services according to Ledgerwood (1999) normally include savings and credit and in some instances insurance and payment services. Schreiner and Colombet (2001) define microfinance as “the attempt to improve access to small deposits and small loans for poor households neglected by banks.” Therefore, microfinance involves the provision of financial services such as savings, loans and insurance to poor people living in both urban and rural setting. Yunus, who is accredited with the establishment of modern day microfinance used his microfinance model to disprove the belief in 1970s and showed that with new lending strategies, the rural poor who were otherwise excluded from the formal banking system because of lack of collateral can repay loans on time. He also demonstrated that the poor can in fact be beneficiaries and partakers of banking services that would be profitable and sustainable.

Microfinance thus, involves the provision of financial services such as savings, loans and insurance to poor people living in both urban and rural setting. One of the benefits of microfinance as declared by the Microcredit Summit is that microfinance encourages savings and helps the poor accumulate asset. Access to microfinance is expected to help the poor to increase their household incomes, acquire basic household assets and to minimize their vulnerability to crisis.

However, in order to maximize these advantages clients of microfinance have to be given the needed skills. Training outside the formal training system is often the most important source of skills training in developing countries. For example in Benin, Senegal and Cameroon, informal apprenticeships account for almost 90% of all trades training (ILO, 2003).

Skills, according to Ayerakwa (2012) are central to improve livelihood opportunities, reduce poverty and enhance productivity. Asiama (2007) indicated that one of the challenges facing microfinance activities in Ghana is inadequate skills

In order to deal with problems such as inadequate skills, successive governments of Ghana have implemented various business development programs such as; Rural Enterprise Project and United Nations Development Programme (UNDP) Microfinance Project to assist the development of microfinance in rural Ghana.

Even though, a number of studies have made various findings on the role of business development services on microfinance in Ghana. For example, according to Asiama (2007), majority of the business development programs had

not been successful because in most cases it is rather the non-target groups who access the programs.

Quaye (2011) indicated that business development programs in most cases should be tailored toward the needs of the clients.

Ayerakwa (2012) found that the rural enterprises project, which is one of the recent introduced business development program in Ghana had created a platform for the acquisition of skills for diverse income generating activities, skills for promoting and building a more competitive and sustainable microfinance activities in the Asuogyaman District of Ghana.

Because there remains a gap in the literature in our understanding of why certain clients of microfinance utilize business development programs to enhance their businesses and others do not, we are particularly interested in the influence that social networks may have on the utilization of business development programs utilization and how social networks also influence the outcome of micro- business in rural Ghana.

Social networks are valuable tools for fostering productivity and income growth and accumulation of wealth (Barrett, 2002). Some of the channels through which these are achieved are improved flow of information, the provision of social insurance and the facilitation of group action to resolve difficult problems. One‟s access to credit depends to a large extent on the normative environment within the person‟s social networks and the person‟s embeddedness in the social networks, as a result of factors such as genetic links and formal group formation (Townsend 1994, Platteau 2000). According to Barrett (2002), social networks are valuable tools for fostering productivity and income growth and accumulation of wealth.

According to Chowdhury (2004) Social networks play an important part in helping clients escape from poverty. Access to social networks provides clients with a defence against having to sell physical and human assets and so protect household assets.

II. AIM OF THE STUDY

The aim of the study is to investigate how the rural women in Ghana use their social networks to influence where they seek business development assistance in running their business and how they use their social networks to influence the outcome of their business. In order words the aim of the study is to find out if social interaction can be used to explain the choice of business development assistance among rural women and how social interaction affects the outcome of their business.

III. STUDY AREA

Page 9 www.ijiras.com | Email: [email protected] (GREL) and NORPALM which are two major Agricultural

companies in Ghana are situated in the district.

Majority of the people in Ahanta West are into subsistence farming, fishing and trading. Due to the remarkable growth experience in microfinance activities from both the Government of Ghana and Non-governmental organizations‟ as well as the main stream banking institutions, a lot of traders, fishermen and farmers at present have access to micro credit to expand their various forms of commercial activities

Ahanta District was purposively selected because of investment potential and the recent increase in microfinance activities in the district.

IV. DATA COLLECTION

Data were collected by interviewing 225 women face to face from 5 villages in Ahanta West District in Ghana with structured questionnaire. 225 women who are participating in microfinance activity were purposively selected from households in each of the villages and interviewed. The selected women and their network members were all included in the data set along with their socioeconomic and demographic attributes. This gave the opportunity to test network properties in each of the selected village and also to deal with the problem of leaving isolated members out of the analysis.

The villages were selected on the basis of representativeness of the district, access to local contacts and support and accessibility. The structure of the questionnaire comprised three domains: demographic, socio –economic-cultural and social network questions. The questionnaire was translated into local dialects to suit the respondents. In each sample area, two polytechnic students who are familiar with the respondents‟ local dialects assisted with the data collection.

V. METHODS OF ANALYSIS

Both statistical and social network methods were used in analysis. Following an exploratory analysis, a binary logistic regression model was used to a partial explanation to experience of success in microfinance activity (business) and if it was related to the type of business assistance used. These variables were then analysed using bivariate logistic regression to model the likelihood of a woman using professional business assistance. In developing this model a social network approach (Wassermann and Frost, 1994) was employed using UCINET-6 (Borgatti, Everret and Freeman, 2002) to help examine how women‟s relational patterns in their local social networks influenced their use of professional assistance.

Using UCINET-6 Freeman‟s degree of centrality scores were derived and used in statistical modelling. The computed Freeman‟s degree of centrality gives the centrality of each actor in the network and summarises this result as the proportion of the maximum possible degree for all actors. This

measurement shows how connected an individual is to the rest of the network.

Also, Sociograms were produced using UCINET-6 to indicate the type of business assistance used as well as to know the network structures in the villages.

The dependent variables used in this analysis were: experience of improvement in your business (yes / no) and a variable „type of business development assistance used‟. Business development services used in business were measured from the answers to the question “where do get the skills and advice to improve your business”? The respondents answers were grouped into three; none (I do not go anywhere for skills and advice), unprofessional (mainly friends and family members) and professionals (qualified personnel from government agencies such as the Business Advisory Center of National Board for Small Scale Enterprises).

The independent variables comprised of both social network data and attribute data.

VI. MEASUREMENT OF SOCIAL NETWORK DATA

To collect social network data the interviewees were asked to name up to five women in the village whom they perceived as their best friends (those they shared their feelings and emotions with them regularly and felt their opinions and various behavioural practices important in their lives). They were further asked to state the frequency of mundane advice and how influential are the named friends on them. The responses to these questions were coded as: Always=4 , Frequently=3, Sometimes=2 , Rarely=1 and Never=0. From the nominations, a square binary matrix was constructed indicating dyadic links for each village, where both the respondents and their network members were simultaneously present. The matrices depicting the patterns of contracts were entered into the social network package UNICET-6. This data arrangement gave the opportunity to examine the position of women in their social networks and the state of their business along with state of the business of their network members.

The NetDraw visualization program (Borgatti, 2002) was used to map the overall relational pattern in each village in the form of sociograms, which allowed graphical comparison of women‟s positions in their social networks and the association of these positions to the state of their business and the type of business advice their received before stating their businesses. This gave the opportunity to compare their behaviour with their network members‟ behaviour.

VII. MEASUREMENT OF SOCIAL ATTRIBUTE DATA

Page 10 www.ijiras.com | Email: [email protected] watch/clock, mobile phone, bicycle, motorcycle and sewing

machine) and then the level of husband‟s education, measured in a four point scale where 0 = none to 3 = greater than secondary. These were combined by computing z scores of the count of possessions and husbands education and then averaging all three variables to give a measure of socioeconomic status (SES).

To assess the internal reliability of representing these variables as one variable, Cronbach‟s alpha was computed and found to be 0.8, which is considered to be an acceptable level.

Respondents „Status of travelling unaccompanied‟ and „decision making power in household matters‟ were measured on a five point scale from never to always and were combined using factor analysis to a new variable called female autonomy score which accounted for 71% of the original variation.

Business experience was coded; improved =0 and no improvement = 1. These variables with other control variables were used in binary logistic regression analyses and measures of concordance and discordance were used to assess the explanatory power of the models. The variables used are summarised in Table 1.

Demographic variables Respondent‟s age, marital status, Educational level Socio economic variables Female autonomy score, socio economic status ((SES) Social Network variable Degree centrality

Communication variable Mass media as a source of receiving general information

Table 1: Variables used in the modeling

VIII. RESULTS

Table 2: Distribution of Business Development Assistance Outcomes

IX. CHARACTERISTICS OF THE WOMEN

In Table 2 a summary of business assistance used by the women in the villages is presented and from this it can be observed that there is a not much variation between the villages with regards to the percentage of women experiencing improvement in business.

With regards to the type of business development services used, on the average; 60.3% indicated that they used unprofessional, 28.4% do not use any at all and 11.3% used professional.

Table 3: Characteristics of the women interviewed in the villages

X. EXPERIENCE OF IMPROVEMENT IN BUSINESS

The degree centrality scores of those who have not experienced improvement in their business were compared with those who indicated they had experienced improvement in their business using a t-test. Those who had not experienced an improvement had a significantly higher centrality score of 5.14 compared to 3.72 for those who had experienced improvement. The test in which variances were unequal gave a p value of 0.015.

A sociogram depicting the connectedness of women who have experienced improvement in their business and those who have not experienced improvement in village A is displayed in Fig 1.

= not experienced improvement = experienced improvement

Figure 1: The pattern of those who had experienced improvement in business in village A

From the figure, those who had not experienced improvement are generally more connected than those who have experienced improvement in business.

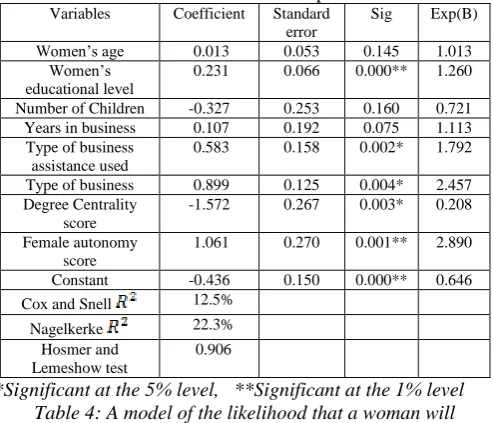

The variables summarized in Table 1 were used to develop a binary logistic regression model to depict the association of these variables to the likelihood that a woman will experience improvement in business, using Wald‟s forward selection method. The model is presented in Table 4.

Variables Coefficient Standard

error

Sig Exp(B)

Women‟s age 0.013 0.053 0.145 1.013

Women‟s educational level

0.231 0.066 0.000** 1.260

Number of Children -0.327 0.253 0.160 0.721

Years in business 0.107 0.192 0.075 1.113

Type of business assistance used

0.583 0.158 0.002* 1.792

Type of business 0.899 0.125 0.004* 2.457

Degree Centrality score

-1.572 0.267 0.003* 0.208

Female autonomy score

1.061 0.270 0.001** 2.890

Constant -0.436 0.150 0.000** 0.646

Cox and Snell 12.5%

Nagelkerke 22.3%

Hosmer and Lemeshow test

0.906

*Significant at the 5% level, **Significant at the 1% level Table 4: A model of the likelihood that a woman will

experience improvement in business

Page 11 www.ijiras.com | Email: [email protected] woman experiencing improvement in business. However,

degree centrality is negatively associated with the likelihood that a woman will experience improvement in her business.

Also, a cross – tabulation, as shown in Table 2, with a Chi- square analysis of type of business development assistance used in business with the experience of improvement in business gave a significant association . Those who obtained professional assistance experienced more success in business than those who do not.

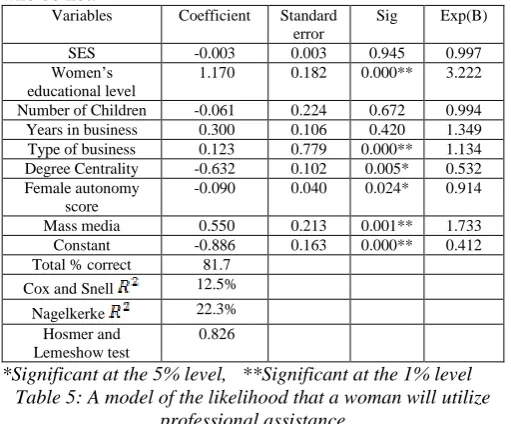

Variables Coefficient Standard

error

Sig Exp(B)

SES -0.003 0.003 0.945 0.997

Women‟s educational level

1.170 0.182 0.000** 3.222

Number of Children -0.061 0.224 0.672 0.994

Years in business 0.300 0.106 0.420 1.349

Type of business 0.123 0.779 0.000** 1.134

Degree Centrality -0.632 0.102 0.005* 0.532

Female autonomy score

-0.090 0.040 0.024* 0.914

Mass media 0.550 0.213 0.001** 1.733

Constant -0.886 0.163 0.000** 0.412

Total % correct 81.7

Cox and Snell 12.5%

Nagelkerke 22.3%

Hosmer and Lemeshow test

0.826

*Significant at the 5% level, **Significant at the 1% level Table 5: A model of the likelihood that a woman will utilize

professional assistance

From Table 5, it can be seen that the likelihood of using professional business assistance is enhanced with higher education and exposure to mass media. SES is also positively associated with using professional business assistance. However, degree centrality is negatively associated with using professional assistance.

This means that the more connected a woman is, the less likely that she will use professional assistance in her business. To illustrate the association of social networks amongst the women, the sociogram of women in the village E is displayed in Figure 2.

= using unprofessional business assistance

= using no business assistance

= using professional business assistance

Figure 2: Sociogram of village E showing relationship of women’s position in their social networks, types of business development assistance used and the assistance used by the

network members

From Figure 2, those using unprofessional assistance as well as those not using any assistance (none) tend to be connected to one another. So it appears that the two groups tend to strengthen each other within their networks. However, there is less use of professional assistance in the network. The influence of social networks is neither the only reason nor the main reason why the women do not use for professional assistance. Their stated reasons for not using professional assistance are displayed in Figure 3 below.

Figure 3: Reasons for not using professional business assistance

From figure 3, their main reason for not using professional business assistance is that, it is not needed, which constitutes 54 % of the respondents.

XI. DISCUSSION

Being highly connected as measured by degree centrality is associated with lower likelihood of experiencing improvement in business. This is confirmed by the sociogram in Figure.1. This may be due to the fact that the women who are well connected and centrally located had wrong idea about the use of professional assistance as compared to the less connected women. This contradicts the work of Griffin (2010) who found that being an active member in the social network may provide one with skills that enhances her probability of experiencing of success in business.

The experience of improvement in business is strongly associated with the type of business assistance received and some demographic characteristics such as educational level and type of business. There was a much higher likelihood of experience of improvement in business with those who receives professional advice, exposed to mass media and have higher education. This supports the research by Valdiva (2011) in Peru who found out that micro entrepreneurs who received specialized business advice often put the advice received into practice which intend improves their business.

Page 12 www.ijiras.com | Email: [email protected] XII. CONCLUSION

In accordance with the aim of the research, a significant association of social interaction in explaining experience of improvement in business of microfinance clients and the type of business assistance used was found. Those who have experienced an improvement are less connected than those who have not. Experience of improvement on business is significantly associated with the type of business assistance used. Specifically, experience of improvement in business of microfinance clients is positively associated with the use of professional assistance. The use of professional assistance is more likely with higher levels of education, Socio economic status and lower degree centrality in their network. The use of professional assistance would have been more beneficial if it was no longer seen by some of the women as last resort. To ensure that this happens, knowledge regarding the benefits associated with using professional business assistance in business in the rural communities should be increased. Another effective way of achieving this is to alter the social norm in the villages, which is „professional advice is not needed‟ to bring about a sustained change in behavior at the social level. Ways to do this is to diffuse business improvement and educational messages through mass media, using opinion leaders and through the existing social networks in the villages, which have been found to be effective in numerous behavioural change researches.

Some common examples include promoting micro insurance through social networks in China‟s main rice producing areas (Cai. et. al 2013), Result of the study showed a positive association between exposure to mass media and the use of professional assistance, however from the sociogram in Figure 2 it is evident that the idea of using Professional assistance in micro- business is not yet saturated at the village level.

From this research the foremost recommendation is to take the community norm about the use of professional development business assistance into account while preparing any microfinance policy and intervention geared towards improving the development of microfinance in the rural areas of Ghana.

REFERENCES

[1] Ayerakwa, A.A (2012). An Assessment of the Rural Enterprises Project as a Poverty Reduction Strategy in Rural Ghana: A Case Study of the Asuogyaman District.

[Online]. Available from

http://ir.knust.edu.gh:8080/bitstream/123456789/4832/1/

AUGUSTINA%20ADU%20AYERAKWA.pdf. [4th

February 2016]

[2] ADB (2000): Finance for the Poor: Microfinance Development Strategy. [Online]. Available from

www.adb.org/sites/default/files/institutional-document/32094/financepolicy.pdf. [4th February 2016]. [3] Asiama J. (2007). "Microfinance In Ghana: An

Overview". Department of Research, Bank of Ghana. 1-15.

[4] Banerjee, A., Chandrasekhar, A. G., Duflo, E & Jackson, M. O. “The Diffusion of Microfinance,” Science Magazine, 2013, 341 (6144).

[5] Barrett, J. D. (2002) "Change communication: using strategic employee communication to facilitate major change", Corporate Communications: An International Journal, Vol. 7 Issue: 4, 219 – 231

[6] Borgatti, S.P., (2002). NetDraw: Graph visualization Software. Harvard: Analytic Technologies.

[7] Borgatti, S.P., Everett, M.G. & Freeman, L.C. (2002). UNICET for windows for social network analysis. Harvard: Analytic Technologies.

[8] Buckley, G. (1997) “Microfinance in Africa: Is it either a Problem or the Solution?” World Development, Vol. 25 No 7, 1081-1093.

[9] Cai, J., Janvry, A. & Sadoulet, E. (2013). Social Networks and the decision to Insure. Available https://mpra.ub.uni-muenchen.de/46861/

[10] Chowdhury, M., P. Mosley & Simanowitz, A. (2004) „Introduction: The Social Impact of Microfinance‟. Journal of International Development, 16(3), 291–300. [11] Gayen, K., & Raeside, R. (2006). Communication and

Contraceptive in rural Bangladesh. Journal of world Health and Population, July, 1-17.

[12] Hanneman, R. (2000). Introduction to social network

methods. [Online]. Available from

http://faculty.ucr.edu/~hanneman/nettext/ [4th February 2016]

[13] International Labour Conference 91st Session 2003. Working Out Of Poverty. [Online] Available from (http://www.ilo.org/public/english/standards/relm/ilc/ilc9 1/pdf/rep-i-a.pdf). [7th April 2016]

[14] Kincaid, D.L. (2004). From innovation o social norm. Bounded normative influence. Journal of health Communication, 9, 37-57.

[15] Lapinski, M.K. & Rimal, R.N. (2005). An explication of social norms. Communication Theory, 15(2), 127-147. [16] Ledgerwood, J. Microfinance Handbook. An Institutional

and Financial Perspective. Sustainable Banking with the Poor. Washington, DC: World Bank, 1999.

[17] Nowak, A., Szamrej, T., & Latane, B. (1990). From private attitude to public opinion: A dynamic theory of social impact. Psychological Review. 97(3), 326-376. [18] Otero, M. (1999). “Bringing Development Back, into

Microfinance”. Journal of Microfinance. Vol.1, no.1, 8-19.

[19] Platteau, J. P (2000). Institutions, Social Norms and Economic Development. Harwood Academic Publishers, Amsterdam, 2000,

[20] Quaye, D. N. O. (2011). The Effect of Micro Finance Institutions on the Growth of Small and Medium Scale Enterprises (SMEs); A Case Study of Selected SMEs in the Kumasi Metropolis. Master‟s thesis, Institute of Distance Learning, Kwame Nkrumah University of Science and Technology, Ghana. Available from Quaye Daniel Nii Obli.pdf. [3rd May 2016]

Page 13 www.ijiras.com | Email: [email protected] [22] Robinson, M. ―The Microfinance Revolution:

Sustainable Finance for the Poor”, World Bank, Washington, 2001

[23] Robinson, M. “Microfinance: the Paradigm Shift From credit Delivery to Sustainable Financial Intermediation”, in M. S. Kimenyi, R. C. Wieland and J D Von Pischke (eds), 1998, Strategic Issues in Microfinance, Ashgate publishing: Aldershot.

[24] Schreiner, M., & Colombet. H. H. (2001). “From urban to rural: Lessons for microfinance from Argentina.” Development Policy Review vol.19, no.3, 339–354. [25] Simanowitz, A., &Brody, A. (2004) Realising the

potential of microfinance. Insights, Issue 51, 1-2.

[26] Townsend, R. (1994): „Risk and Insurance in Village India‟ Econometrica 62 (3)

[27] Valente, T. W., & Davis, R.L. (1999). Accelerating the diffusion of innovations using Opinion leaders. The Annals of the American Academy of the Political and Social Sciences 566, 55-67.

[28] Valente, T. W. (1996). Social network thresholds in diffusion of innovations. Social Networks 18, 69-89. [29] Wasserman, S. & Faust, K. (1994). Social Network

Analysis. Cambridge University Press.