GSJ: Volume 7, Issue 12, December 2019, Online: ISSN 2320-9186 www.globalscientificjournal.com

CBN CASHLESS POLICY IMPLEMENTATION AS PREDICTOR OF SUSTAINABLE ADMINISTRATION OF HIGHER EDUCATION IN SOUTH-SOUTH

NIGERIA: IMPLICATION FROM MANAGEMENT PERSPECTIVE

1

Obia Eniang-Esien PhD & 2Martha Daniel Ekpe PhD

1&2

Department of Educational Management, Faculty of Education Cross River University of Technology, Calabar Cross

River State, Nigeria

ABSTRACT

The paper focused on assessment of the CBN’S cashless policy implementation as predictor of sustainable administration of higher educationin south-south Nigeria: Implication on educational management. Two hypotheses were formulated to guide the study. The study adopted the descriptive survey research design. It became expedient to adopt survey design because this method allowed the researchers to obtained data from a representative sample from a wider area of coverage (for an objective analysis and valid inference). The population for the study comprised 16, 238 administrative staff of tertiary institutions in south-south, Nigeria. The stratified and simple random samplings were employed in the study and relevant data for this study was obtained from the sampled respondents. The sample size for study was 627 respondents drawn from among six selected tertiary institutions in south-south, Nigeria. A well structured questionnaire titled “Cashless Policy and Sustainability of Higher Education Questionnaire (CPSHEQ)" which was face validated by three experts two in Educational Management and one in Measurement and Evaluation. The reliability was carried out using split half reliability method and the coefficient of internal consistency obtained ranged from .87 to .91. The data obtained from the research instrument were analyzed using descriptive statistics (simple percentages and bar charts) and inferential statistics (population t-test and multiple regression analysis). The results revealed the level of cashless policy implementation is significantly low. Also, there is a significant prediction of cashless policy in terms of infrastructure, security and awareness on sustainable administration of higher education. The study recommended that with the creation of numerous payment options, the process of cash collection will be made simple and the cost and risk associated with cash transfer and processing reduced. This will have a strong implication of the management of tertiary institutions across the country.

INTRODUCTION

Cashless implies an economy policy in which banking including all administrative

transaction can effectively be carried without necessarily carrying physical cash as a means of

exchange of transaction but rather with the use of credit or debit card payment for goods and

services. The cashless economy policy initiative of the Central Bank of Nigeria (CBN) is a move

to improve the financial terrain which will in turn support administration of educational activities

(Ejiro, 2012). This implies that a Cashless economy is an environment in which money is spent

without being physically carried from one person to the other. The first issue in the cashless

economy is the issue of electronic purse. This is electronic information that is transmitted to a

device which reveals the information about how much a person has stored in the bank and how

much he can spend.

The CBN cash policy stipulates a daily cumulative limit of N150, 000 and N1, 000,000

on free cash withdrawals and lodgments by individual and corporate customers respectively in

the Lagos State with effect from March 30, 2012. Individuals and corporate organizations that

make cash transactions above the limits will be charged a service fee for amounts above the

cumulative limits. The policy through the advanced use of information technology facilitates

fund transfer, thereby reducing time wasted in Bank(s). The idea of introducing cashless policy

in Nigeria began in Lagos State, Nigeria. According to Central Bank of Nigeria (CBN, 2011)

Lagos state accounted for 85% of POS and 66% of cheques transaction in Nigeria. Cashless

economy aims at reducing the amount of physical cash circulating in the Nigeria economy and

thereby encouraging more electronic–based transaction. According to Central Bank of Nigeria

(CBN, 2011) the policy is expected to reduce cost incurred in maintaining cash-based economy

by 90% upon its full implementation in Nigeria. This study aims to look at the impact of cashless

economy in Nigeria.

Cashless economy is not the complete absence of cash, it is an economic setting in which

goods and services are bought and paid for through electronic media. According to Woodford

(2003), Cashless economy is defined as one in which there are assumed to be no transactions

frictions that can be reduced through the use of money balances, and that accordingly provide a

reason for holding such balances even when they earn rate of return. In a cashless economy, how

much cash in your wallet is practically irrelevant (Roth, 2010) observed that developed countries

electronic ones, especially payment cards. Some aspects of the functioning of the cashless

economy are enhanced by e-finance, e-money, e-brokering and e-exchanges. These all refer to

how transactions and payments are effected in a cashless economy (Moses-Ashike, 2011). This

means that increased usage of cashless banking instruments strengthens monetary policy

effectiveness and that the current level of e-money usage does not pose a threat to the stability of

the financial system.

In spite of how robust the CBN cashless policy seems to be there are inherent challenges

of the cashless policy According to Ikechukwu (2017), the change from cash based economy to

cashless economy moved people inconvenienced the stakeholders, especially the populace, due

to lack of understanding and proper guidance on its implementation. These has hampered the

adoption and fuelled conspiracy theories among stakeholders. Okoli (2015: 12) stated that “There are several complaints from different quarters that sufficient facilities have not been

provided to make the system smooth. The e-payment system is said by many who have tried to

use it to be filled with hitches. Sometimes, one is charged for service not successfully rendered.

Infrastructure The use of e-cash, commonly known as “cashless” contains challenges that

are readily amplified by the inadequacies of physical infrastructure]. Access to the internet at

affordable price is poor and the lack of credible energy utilization (power supply) has led to a

series of challenges of its own as regards e-services. Other infrastructure and services that are

related to the policy and are inadequate in supply include the Point of Sale (POS) terminal,

Automated Teller Machine (ATM), Mobile banking (Ejoh, 2014).

Security system in the country is pivotal in the emergence of the cashless policy and can

be a deterrent if not handled well (Yaqub, Bello, Adenuga and Ogundeji (2013) report reveals

the first year of the scheme saw diverse fraudulent activities reported. These compromise the integrity of the monitoring bodies in Nigeria. In the CBN Annual report” Central Bank of

Nigeria (2018) a record of 25,043 fraud cases were raised as opposed a reduced rate of 19,531 in

2016 in which some of the funds were recovered.

Ndifon and Inah (2014) conducted a study on implementation of the cashless policy on

January 1st, 2012 in Lagos state which is aimed at reducing the high cost of cash production, circulation and distribution in Nigerian economy, the set-out goals have not been fully achieved

due to several on-going challenges. This survey research was conducted to review challenges of

of electronic payment for exchange of value. The Unified Theory of Acceptance and Usage of

Technology (UTAUT) were employed to identify various challenges from data gathered through

questionnaires distributed to different stakeholders in the economy. A total of 410 questionnaires

were collected and the research work adopted used Partial Least Square (PLS) method and used

Smart PLS software during the data analysis. The attendant findings were pivotal to

understanding the challenges encountered in implementing cashless policy in Nigeria. This study

shows that despite the implementation of this policy, a lot of users are still being faced with

various challenges and more efforts are still being required to achieve an effective cashless

society

Awareness coupled with literacy that is lacking, as most adults do not understand it,

hence are at a loss to actively participant in financial policies. Financial literacy, involves understanding how money works, its management pattern, how it’s earned, how to invest money.

Many people in the country lack banking culture as a result they save by crude and informal

means, while some lack access to banking services; for such people, e-transaction is a mere

story.

Sustainability of cashless policy on administration of higher education such as,

universities, colleges of education, polytechnics, Monotechnics and other institutions offering

correspondence courses. According to the National Policy on Education (FRN, 2014), the goals

of tertiary education include the following, to; (a) contribute to national development through

high level of relevant manpower training; (b) develop and inculcate proper values for the

survival of the individual and society; (c) develop the intellectual capability of individuals to

understand and appreciate their local and external environment; (d) acquire both physical and

intellectual skills which will enable individuals to be self-reliant and useful members of the

society; (e) promote and encourage scholarship and community services; It has been documented

that university education shall make optimum contribution to national development: intensify

and diversify its programmes for development of high level manpower within the context of the nation’s needs, among others (FRN, 2014).

In this environment of restricted revenues and mandated expenditures, higher education

funding is a tempting target to cut, not only because it is discretionary but also because colleges,

unlike many other state programmes, can tap from other revenue sources, and because a growing

education is increasingly viewed by both policy makers and the general public as primarily a

private benefit, rather than a broader social good. Many Nigerian adults believe that every

potential candidate who wants a four-year higher education should have the opportunity to gain

one, because to them, education is the right of individuals and should be provided by the

government. By implication therefore, state and federal governments are expected to invest more

money in higher education, while a few people believe that students and their families should

pay the largest share of the cost of a tertiary education. Given ongoing access barriers, these

perceptions may make it more difficult than in the past now that spaces for candidates in public

tertiary institutions could not meet the high demand from the intending candidates, hence, the

resort to private institutions that are not more often reliable compared to the conventional ones.

The Central Bank of Nigeria (CBN) stated that the introduction of cashless economic

policy in Nigeria would moderate the cost of cash management, encourage the use of electronic

payment channels and reduce lending rates to further make credit accessible to big and small

businesses. Central Bank of Nigeria (2012) maintained that the cashless Economic development

and modernization of the Nigeria in payment system in line with vision 2020, reduces the

amount of physical cash circulation in the Nigeria economic and thereby encouraging movement

of electronic-base transactions, reduce cost incurred in maintaining cash base economy by 90%

when fully implemented in Nigeria.

Ikpefan, Akpan, Godswill Evbuomwan and Ndigwe (2018) sought to determine the

impact electronic banking tools have on cashless policy in Nigeria for a ten year period which

spans from 2006 to 2015. In this research work, the ordinary least square method was used to

analyze the data. The data used for this research work was collected from the Central Bank of

Nigeria (CBN) annual report and the Nigerian Interbank Settlement System (NIBSS) website.

The major findings of this research work showed that there is no significant impact of electronic

banking tools on the currency in circulation. The study recommends that transaction charges

should be further reviewed to a little (single digit) or no charge, to encourage more patronage of

e-payment platforms and CBN, Deposit money banks (DMBs), and other non-banks financial

institutions should provide public enlightenment and awareness programs that will create

awareness and entice the unbanked individuals into the banking system especially those in the

Akpan (2009) observed that the introduction of cashless economic policy in Nigeria aims

at reducing the cost of banking services and drive financial institutions by providing more

efficient transaction options and greater reach to customers, improve the effectiveness of

monetary policy in managing inflation as well as curbing negative consequences associated with

the high usage of physical cash in the economy such as risk of cash related crimes , revenue

leakage arising from too much of cash handling , inefficient treasury management due to nature

of cash processing and high inflation of the economy. Despite the benefits posited by cashless

economic policy and its importance in sustainable and developing the economy of Nigeria, it has

brought confusion among the masses as many misconceived the term to be an economy there

will be no more cash in the circulation but card and other instruments. Many still believed that,

the cash limit set by Central Bank of Nigeria (CBN) in respect to cashless economic policy is too

low and query and how the Central Bank of Nigeria arrived at the bench-mark. Notwithstanding

the fact that the cashless policy come with enormous benefits; there are also some missing links

that confronted the policy such as financial constraints, infrastructure, deficit, literally levels,

fraudulent activities and poor power supply in Nigeria. Consequently, the policy failed to

achieve its objectives. Apart from the physical challenges, economic data and indicators are not

fully available and reliable. There is a great challenge in attempting to analyze the true impact of

the cashless policy on the economy of Nigeria as only few monetary and macroeconomic

indicators can be traced with subject matter.

This is a road map; of action plan for achieving sustainability in any activity that uses

resources and where immediate and intergenerational replication is demanded. Sustainable

development is the organizing principle for sustaining fruit resources necessary to provide for the

needs of future generations of life on the planet (Odior & Banuso, 2012). Sustainable

development is development that meets the needs of the present without compromising the

ability of the future generations to meet their own needs. Limitations imposed by advanced

technology vices within the environment and the ability to meet the present and future needs of

customers. Babalola (2008) opined that sustainable development is a roadmap and action plan for

achieving sustainability in any activity that uses resources and where immediate and

intergenerational replication is demanded. As such, sustainable development is the resource

necessary to provide for the needs of future generations. Okey (2012) said that sustainability is a

the needs of the present and future generation to meet their needs. Sustainable development is an

approach to growth and to manage natural product and social welfare of their generation.

Statement of the problem

The introduction monetary policy as a technique of economic was to bring accountability

and sustainability in economic growth and development through cashless policy. Since the

introduction of the cashless policy, there have been series of problems ranging from economic

data, administrative issues which have a lasting effect on the administration of education for

sustainable development. There is a great challenge in attempting to analyze the true impact of

the cashless policy on the economy of Nigeria as only few monetary and macroeconomic

indicators can be traced with relation to the subject matter. Several scholars have attempted to

analyze the cashless system or e-banking. However, it becomes clear that few studies present a

comprehensive evaluation of cashless banking implications in sustainable educational

development. In-spite of numerous studies conducted There impact on educational management

has not been fully outlined. Thus, the problem of this study is: what is the impact of cashless

policy implementation on sustainable administration of higher education in south-south Nigeria?

What are the possible implications of cashless policy from management perspective? Seeking

answers to these questions constitutes a central problem for this research study.

Research Questions

The following questions were answered in the study

1. How effective is the cashless policy on sustainable administration of higher education

policy?

2. What are the benefits accrued in the implementation of cashless policy in south-south,

Nigeria?

Statement of Hypotheses

The following null hypothesis were stated and tested at .05 level of significance

1. The level of cashless policy implementation is not significantly low

2. There is no significant prediction of cashless policy in terms of infrastructure, security

and awareness on sustainable administration of higher education.

This study adopts the descriptive Survey Research Design. It became expedient to adopt survey

design because this method allowed the researchers to obtained data from a representative

sample from a wider area of coverage (for an objective analysis and valid inference). The

population for the study comprised all administrative staff of tertiary institutions in south-south,

Nigeria. The stratified and simple random sampling were employed in the study and relevant

data for this study was obtained from the sampled respondents. The sample size for study was

627 respondents drawn from among six selected tertiary institutions in south-south, Nigeria. A

well structured questionnaire titled “Cashless Policy and Sustainability of Higher Education

Questionnaire (CPSHEQ)" which was face validated by three experts two in Educational

Management and one in Measurement and Evaluation. The reliability was carried out using split

half reliability method and the coefficient of internal consistency obtained ranged from .87 to

.91. The data obtained from the research instrument were analyzed using descriptive statistics

(simple percentages and bar charts) and inferential statistics (population t-test and multiple

regression analysis). The result is presented below.

RESULT

The result of the research questions are presented in Table 1 and 2.

Research Question 1: How effective is cashless policy on sustainable administration of higher

education. To answer this research question, descriptive statistics was employed as presented in

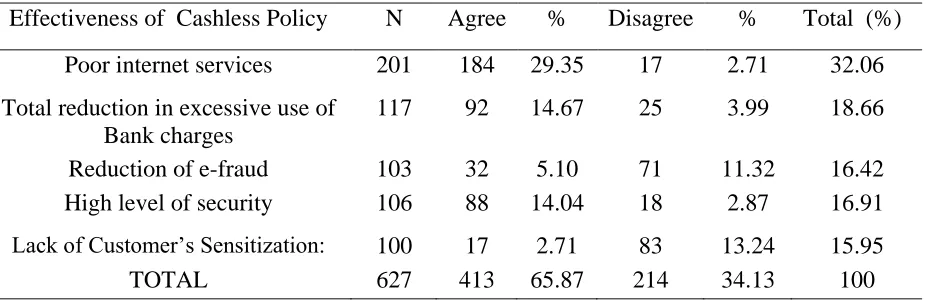

TABLE 1. Effectiveness of cashless policy on sustainable administration of higher education

Effectiveness of Cashless Policy N Agree % Disagree % Total (%)

Poor internet services 201 184 29.35 17 2.71 32.06

Total reduction in excessive use of Bank charges

117 92 14.67 25 3.99 18.66

Reduction of e-fraud 103 32 5.10 71 11.32 16.42

High level of security 106 88 14.04 18 2.87 16.91

Lack of Customer’s Sensitization: 100 17 2.71 83 13.24 15.95

TOTAL 627 413 65.87 214 34.13 100

Table 1 revealed the result of the level of effectiveness of cashless policy on sustainable

administration of higher education .as majority of the respondents 184 (29.35%) said that

cashless policy is not effective due to poor internet services while 17 (2.71%) disagree that

total reduction in excessive use of Bank charges while 25 (3.09%) disagree that it leads to total

reduction in excessive use of Bank charges. 32 (5.10%) agree that it leads to reduction of e-fraud

while 71 (11.32%) disagree that it does not lead to reduction in e-fraud. For high level of

security 88 (14.04%) agreed while 18 (2.87%) disagreed. Finally, lack of Customer’s

Sensitization: 17 (2.71) agreed that it leads to lack of Customer’s Sensitization: while 83 (13.24%)

disagreed that it does not lead to lack of Customer’s Sensitization: the result is further presented in

figure 1:

Figure 1: Level of effectiveness of cashless policy on sustainable administration of higher

education.

TABLE 2: Benefits accrued in the implementation of cashless policy in south-south, Nigeria.

Increase employment

opportunities %

Reduce employment opportunities Enhanced economic activities Foster economic development Reduce cash related

fraud TOTAL

N N % N % N % N % N %

13 2.07 274 43.56 31 4.93 33 5.25 278 44.2 629 100

Table 1 shows the view of respondents on benefits of CBN cashless economy in Nigeria. The

lowest percentage, 2.07 % of the respondents, believed that cashless policy will increase

0 100 200 300 400 500 600 700 Poor internet services Total reduction in excessive use of Bank charges

reduction of e-fraud

employment opportunities. A higher percentage, 44.2% of the respondents, believed that cashless

policy in Nigeria will reduce cash related fraud, followed by 43.56% who re of the view that

Figure 2: Benefits accrued in the implementation of cashless policy in south-south, Nigeria

0 100 200 300 400 500 600 700

N N % N % N % N % N %

Increase emp. Opp

% reduce emp. Opp. Enhanced economic

activities

Foster economic development

Reduce cash related fraud

TOTAL

Test of hypotheses

The results of the hypotheses are presented in table 3 and 4.

Hypothesis 1: The level of cashless policy implementation is not significantly low. To test this hypothesis, population t-test is employed as presented in table 3.

Table 3: Level of cashless policy implementation in south-south

level of cashless policy implementation N Mean Std. Deviation

Std. Error Mean

626 15.6507 3.85448 .15393

level of cashless policy implementation

Test Value = 0 t Df Sig.

(2-tailed)

Mean Difference 95% Confidence Interval of the Difference

Lower Upper

101.672 626 .000 15.65072 15.3484 15.9530

Table 3 revealed the one sample t-test analysis of the level of cashless policy implementation on sustainability of higher education. The p-value of .000 is less than the chosen alpha of .05. Thus, the hypothesis is rejected. This implies that the level of cashless policy implementation is on sustainability of higher education is significantly low

Hypothesis Two

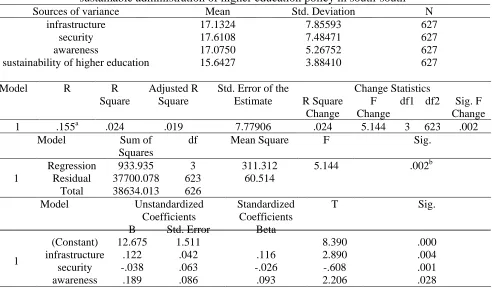

There is no significant prediction of cashless policy in terms of infrastructure, security and awareness on sustainable administration of higher education policy in south-south. To test this hypothesis, multiple regression analysis was employed as presented in Table 4.

Table 4

Multiple regression analysis of cashless policy in terms of infrastructure, security and awareness on sustainable administration of higher education policy in south-south

Sources of variance Mean Std. Deviation N

infrastructure 17.1324 7.85593 627

security 17.6108 7.48471 627

awareness 17.0750 5.26752 627

sustainability of higher education 15.6427 3.88410 627

Model R R

Square

Adjusted R Square

Std. Error of the Estimate Change Statistics R Square Change F Change

df1 df2 Sig. F Change

1 .155a .024 .019 7.77906 .024 5.144 3 623 .002

Model Sum of

Squares

df Mean Square F Sig.

1

Regression 933.935 3 311.312 5.144 .002b

Residual 37700.078 623 60.514 Total 38634.013 626

Model Unstandardized

Coefficients

Standardized Coefficients

T Sig.

B Std. Error Beta

1

(Constant) 12.675 1.511 8.390 .000

infrastructure .122 .042 .116 2.890 .004

security -.038 .063 -.026 -.608 .001

awareness .189 .086 .093 2.206 .028

The result in table 4 of the hypothesis that states there is no significant prediction of cashless

policy in terms of infrastructure and awareness on sustainable administration of higher education

policy in south-south revealed that the p-value of .004. .001 and .028 were found to less than the

chosen alpha of .05 for infrastructure, security and awareness. This implies that there is a

significant prediction of infrastructure, security and awareness (literacy) on sustainability of

higher institution in the study area.

Discussions of Findings

The findings of the study are discussed hypothesis by hypothesis as presented below

H01: The level of cashless policy implementation is not significantly low

The finding revealed that the level of cashless policy implementation is significantly low. This

may be due to poor implementation of te policy by stake holders in the academic environment.

The findings Ndifon and Inah (2014) whose findings were pivotal to understanding the

challenges encountered in implementing cashless policy in Nigeria. This study shows that

despite the implementation of this policy, a lot of users are still being faced with various

challenges and more efforts are still being required to achieve an effective cashless society the

authors also found that awareness coupled with literacy that is lacking, as most adults do not

understand it, hence are at a loss to actively participant in financial policies. Financial literacy,

involves understanding how money works, its management pattern, how it’s earned, how to

invest money. Many people in the country lack banking culture as a result they save by crude and

informal means, while some lack access to banking services; for such people, e-transaction is a

mere story.

H02: There is no significant prediction of cashless policy in terms of infrastructure, security

and awareness on sustainable administration of higher education policy in south-south. The

result revealed that there is a significant prediction of cashless policy in terms of infrastructure,

security and awareness on sustainable administration of higher education policy in south-south.

thus, the level of infrastructural development, security consciousness and level of awareness has

a significant relationship. The result is in harmony with that by Ikpefan, Akpan, Godswill

Evbuomwan and Ndigwe (2018) findings showed that there is no significant impact of electronic

should be further reviewed to a little (single digit) or no charge, to encourage more patronage of

e-payment platforms and CBN, Deposit money banks (DMBs), and other non-banks financial

institutions should provide public enlightenment and awareness programs that will create

awareness and entice the unbanked individuals into the banking system especially those in the

informal sector in Nigeria. The findings also agrees with Akpan (2009) observed that the

introduction of cashless economic policy in Nigeria aims at reducing the cost of banking services

and drive financial institutions by providing more efficient transaction options and greater reach

to customers, improve the effectiveness of monetary policy in managing inflation as well as

curbing negative consequences associated with the high usage of physical cash in the economy

such as risk of cash related crimes , revenue leakage arising from too much of cash handling ,

inefficient treasury management due to nature of cash processing and high inflation of the

economy.

CONCLUSION

The study was carried assess the CBN’S cashless policy on economic development of public

servants in south-south, Nigeria. It is expected that its impact will be felt in modernization of

Nigeria payment system, reduction in the cost of banking services as well as reduction in high

security and safety risks. This should also include curbing banking related corruptions and

fostering transparency. It is also assumed that the introduction of cashless policy in Nigeria will

help to reduce the amount of bills and notes circulating in the economy. This should, therefore,

reduce handling operation cost incurred on conventional money, as well as reduction in cash

related crimes. It should also help to provide easy access to banking services for Nigerians.

Recommendation

Based on the findings, the following measures on how to efficiently and effectively improve the

cashless policy are recommended:

1. Creating an awareness program for both literates and non-literates is a major way to

encourage the use of the system, educational seminars for late adopter of the cashless

policies should be considered and this should be done at reduced prices or no price to aid

participation.

2. Efficient and effective administration tools should be provided to facilitate these policy

3. Improved security systems should be installed in the various platforms and facilities

involved in e-banking which will help to reduce scamming among internet fraudsters and

other forms of fraudulent practices in the banking and administrative industries.

Policy implication on educational management in Nigeria population

1. With the creation of numerous payment options, the process of cash collection will be

made simple and the cost and risk associated with cash transfer and processing reduced.

This will have a strong implication of the management of tertiary institutions across the

country.

2. It is a good tool in the tracking of corruption and money laundering accustomed with a

number of internet fraud among administrative staff in all ministries in the country.

3. It will increase transparency in business transactions. It will increase the involvement of

in sustaining higher education hereby increasing public participation in decision making

that will help to facilitate growth and development of tertiary institutions.

REFERENCES

1. Akpan, I. (2009). Cross channel integration and optimization in Nigerian banks. Telnet

Press Release, 20 (1), 1-4.

2. Akpan, R. (2009). Cashless Banking in Nigeria: Challenges, Benefits & Policy

Implications. European Scientific Journal. 8, (4), 12 – 16.

3. Babalola, E. (2008). Monetary Policy, Monetary Areas and Financial Development with

Electronic Money, IMF Working Study, IMF.

4. Central Bank of Nigeria (2011): Towards a Cashless Nigeria: Tools & Strategies. Nigerian

Journal of Economy. 3(2), 344 – 350.

5. Central Bank of Nigeria (2012): Towards a Cashless Nigeria: Tools & Strategies. Nigerian

Journal of Economy. 21(6), 124 – 132

6. Central Bank of Nigeria (2018): Towards a Cashless Nigeria: Tools & Strategies. Nigerian

Journal of Economy. 9 (4), 76 – 81.

7. Ejiro, O. (2012): What Nigerians Think of the Cashless Economy Policy. Nigerian Journal

8. Ejoh, N. (2014). The Workability of the Cash-less Policy Implementation in, 5(17), 179–

192. [25]

9. Federal Republic of Nigeria (2014). National policy on education (4th Edition). Lagos:

NERDC Press

10. Ikechukwu, A. (2017). Cashless Policy in Nigeria : The Mechanics, Benefits and Problems

Innovative Journal of Economics and Financial Studies Cashless Policy in Nigeria : The

Mechanics, Benefits and Problems.

11. Ikpefan O. A., Akpan E Godswill O. O., Evbuomwan, G. & Ndigwe, C. (2018).

International Journal of Civil Engineering and Technology. 9, (10), 718–731.

12. Moses-Ashike, H. (2011). Cashless Economic can Reduce Risk of Carrying Huge Cash,

retrieved Available: http://www.businessdayonline.com/…/22217.

13. Ndifon E.. & Inah O. (2014). The Workability of the Cash-less Policy Implementation in

Nigeria. Journal of Economics and Sustainable Development 5, (17), 1-16.

14. Odior, S. E. & Banuso, B. F. (2012). Cashless Banking in Nigeria: challenges, benefits and

policy implication, European Scientific Journal, 8 (12), 13-17.

15. Okey, O. O. (2012). The Central Bank of Nigeria’s cashless policy in Nigeria: Benefits and

challenges, Journal of Economics and Sustainable Development, 3(14), 128-133.

16. Okoli, N. H. (2015). The Cash-Less Policy in Nigeria: Issues, Challenges and Prospects”

author-me.com, [Online]. Available: http://www.author-me.com/nonfiction/cashless.htm.

[Accessed: 17- Nov-2018].

17. Woodford, F. (2003). Electronic Retail Payment Systems: User Acceptability & Payment

Problems in Nigeria. Arabian Journal of Business & Management Review. vol.5, pp. 60 –

63.

18. Yaqub, J. O., Bello, H. T., Adenuga, I. A. and Ogundeji, M. O. (2013). The cashless policy

in Nigeria: Prospects and challenges. International Journal of Humanities and Social