1

Perhaps the most important, and difficult, question in economics is, why are some countries rich and others poor? Living standards are usuallycompared by using the total annual production of goods and services in a country, gross domestic product or GDP, and dividing it by the population to get GDP per capita. This gives a rough idea of the average amount of product that each person has to live on. While Somalia has GDP per capita of around US$600, the figure for Botswana is over US$7,000, and for

Singapore it is almost US$44,000.

The rate at which the GDP of a country increases from one year to the next is referred to as its rate of economic growth. Since Botswana and Singapore had similar standards of living a half century ago, Singapore’s much higher current GDP per capita must have come about because its economic growth rate was higher than Botswana’s. So when we ask the question, why are some countries richer than others, we are really asking why have some countries managed to have higher rates of economic growth than others? A remarkable economic fact about the world around us is the variety of economic growth experiences. While much of Europe and North America enjoyed more of less sustained economic growth over the last 250 years, large parts of the rest of the world, in Latin America and the Caribbean, Africa, and Asia experienced much lower rates of economic growth if any at all. By the middle of the last century, these so-called developing countries lagged far behind their more prosperous northern neighbours.

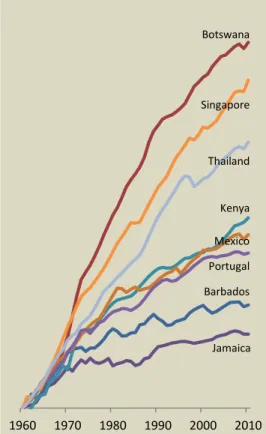

Over the last half century, the rate of economic growth has varied greatly both amongst countries and in the same countries over time. While Jamaica, for example, has grown at a meagre annual average of less than 1 percent, Portugal has managed more than 3 percent, Brazil over 4 percent, and Thailand an impressive 6 percent. Figure 1 highlights these differences by comparing how GDP has grown for a sampling of countries, artificially scaling their 1960 levels so it seems as if they are starting at the same level.

T

HE

I

MPORTANCE OF

G

ROWTH

The rate of economic growth is important, not only because growth raises the material standard of living of a country’s citizens, but also because many other indicators of well-being improve with higher levels of GDP. As GDP per capita rises in a country, the health of its citizens improves – the incidence of disease falls, infant and child mortality declines, and life expectancy rises. In addition, on average, the incomes of the poor rise proportionately with growth of GDP.1

Growth can make a big difference in a short time. When Ireland was growing at near 9 percent per annum between 1995 and 2007, it went from being one of the poorest countries in the European Union to one of the

Prepared for Principles of Economics, University of the West Indies, Mona. © Damien King, December 2011

1960 1970 1980 1990 2000 2010 Botswana

Singapore

Thailand

Kenya Mexico Portugal Barbados

Jamaica

2

wealthiest. Growth at that rate doubles the national income in only eight years!Even small differences in economic growth rates accumulate rapidly over time to make a big difference. The difference between one and two percent annual growth results in a 22 percent difference in wealth after only 20 years.

So, economic growth is of great importance, both quantitatively and qualitatively. What accounts for the vast differences we observe around the world?

G

ROWTH

F

ACTORS

How well off the residents of a country are, that is, how high an income level they have on average, is directly related to the amount of goods and services that the country produces. The amount of production, in turn, is determined by the productivity of the residents. Productivity refers to output per working person. Since, an unskilled single person without tools of any kind living on a bare landscape can produce very little, raising such a person’s productivity requires enhancing his natural ability – with tools, skills, an ideas.

T

HE

R

OLE OF

C

APITAL

One of the most obvious ways in which productivity can be raised is with the use of tools. From the poison tipped spear to the voice activated smartphone, tools allow a worker to create more output than could have been produced with a pair of bare hands. A hunter can kill more prey with a poison tipped spear than without one; and can kill more with two spears than with one. Up to a point, each additional spear carried by the hunter raises his productivity in making kills. In a similar manner, being able to instruct your phone or your computer with a voice request allows the user to accomplish more than having to enter instructions with a keyboard or even with a touch screen.

Much of the wealth of modern societies, compared to our ancestors, rests on the productivity afforded by large stocks of capital. Look around you and you will see the buildings, vehicles, machinery, appliances, tools, and computers that are part of that stock. Included in the stock of capital is the public infrastructure – roads, bridges, airports, electricity grids, and water pipelines. This capital allows each person to be more productive at manufacturing goods, producing services, and transporting commodities than would be possible without it.

There are vast differences amongst countries today in the amount of capital that each has accumulated, especially when represented on a per person basis. It obvious, even to the casual observer, that Germany has more capital per person than Colombia, which in turn has more than Niger. Further, these differences in stocks of capital are broadly consistent with levels of income. The greater the stock of capital, the richer the country tends to be.

There is another kind of capital that is just as capable of making a pair of hands more productive – skills. The various skills that people learn increase

3

their capacity to produce. Expert machete wielders cut coconuts faster; trained pianists play better; skilled seamstresses make more dresses. In this way, the collection of skills embedded in a country’s labour force is a factor in determining that country’s productivity and standard of living.Skills are often complementary to physical capital. Knowing how to drive a car is a much more useful skill if one actually has a car. At the same time, having the car is not of much use if no one around can drive it. In this way, the combination of physical and human capital raises productivity by more than the two types of capital do separately.

Capital, whether in the form of the poison tipped spears of Namibia’s San, the towering 452 meters of the Petronas Towers in Indonesia, or the deft skills of the master brewers at Presidente in the Dominican Republic, is an important determinant of productivity. Differences in the size of their capital stocks, physical and human, are therefore a key element in

understanding why some countries’ residents can produce greater wealth than others. We will come to why these differences may have arisen later in this chapter.

T

HE

R

OLE OF

T

ECHNOLOGY

The production of any good or service can be accomplished in a variety of ways, that is, with a variety of technologies. These different ways will vary in the efficiency with which they use the factors of production.

Consequently, for a given amount of labour and capital, different technologies of production will yield different amounts of output. An example of how the mere organization of production can make a difference to productivity comes from one of the most famous passages in the history of economics. Adam Smith, writing in The Wealth of Nations in 1776, describes the manufacture of pins.

[A] workman… could scarce, perhaps, with his utmost industry, make one pin in a day… . But in the way in which this business is now carried on…, not only the whole work is a peculiar trade, but it is divided into a number of branches, of which the greater part are likewise peculiar trades.

One man draws out the wire, another straights it, a third cuts it, a fourth points it, a fifth grinds it at the top for receiving the head; to make the head requires two or three distinct operations; to put it on, is a peculiar business, to whiten the pins is another; it is even a trade by itself to put them into the paper; and the important business of making a pin is, in this manner, divided into about eighteen distinct operations.

I have seen a small manufactory of this kind where ten men only were employed…. But though they were very poor, and therefore but indifferently accommodated with the necessary machinery, they could… make among them… upwards of forty-eight thousand pins in a day. Each person,

therefore…, might be considered as making four thousand eight hundred pins in a day. But if they had all wrought separately and independently…, they certainly could not each of them have made twenty, perhaps not one pin in a day.

4

Smith compares two technologies for pin making, and comes to theconclusion that the one in which each worker specializes in a “peculiar trade” results in a considerable increase in productivity.

We are accustomed to thinking of advances in technology in terms of gadgets of increasing sophistication, such as the technology of computers. But Adam Smith’s example reveals that a more advanced technology of production does not require that the underlying idea be embedded in new hardware. Indeed, it is useful to separate the contribution of more advanced machinery into separate components – the underlying idea and the capital to embody it, each making its distinct contribution to productivity. The impressive increases in living standards that has occurred in many parts of the world since the industrial revolution began in England in the late 18th century is due to continuous increases in the technology of

production. The inventions of the steam engine, electricity, the assembly line, and the world wide web have all contributed to boosting productivity and affording more comfortable living conditions.

T

HE

R

OLE OF

I

NSTITUTIONS

A stock of capital and a process of production may produce either a smaller or a larger quantity of goods and services depending on what people are allowed to do. Wherever people go about their economic activities, they are governed by laws, rules, and customs. These constitute the institutional framework within which work, production, and trade occur, and may either constrain or facilitate it..

In Saudi Arabia, women are prohibited from driving cars. This restriction reduces the commercial productivity of half the labour force. In Thailand, the normal retirement age is 60 years. The absence of able-bodied 61 year olds from the labour force lowers the average productivity of the

population of that country.

The ways in which the Institutional environment can affect the amount of commerce can take many forms. An independent central bank can better maintain the value of the currency and stable currency increases confidence in the future; a government that engages in arbitrary property seizures diminishes the incentive to invest and get rich; A slow and corrupt justice system makes all economic participants reluctant to enter into contractual arrangements.

The institutional framework includes the legislation of a country as well as the likelihood that laws are enforced. It also includes any religious

restrictions on behaviour that has commercial implication, such as disapproval of work on the Sabbath or interrupting work for daily prayer. Finally, any unwritten but socially enforced taboos would equally well be included as a part of the institutional framework. There is no law against women driving in Saudi Arabia. Nonetheless, it doesn’t occur.

In many cases, the most important part of the institutional make up is laws that specifically restrict or facilitate commerce. The laws governing bankruptcy procedures can incentivize or discourage investment by reducing or raising the cost of failure. High import duties or outright bans on certain imports would limit the opportunities for wealth creation if such opportunities included goods from abroad.

5

The varied experience with economic growth in many countries hasrevealed the importance of particular institutional elements. An emerging consensus on the institutions that are good for economic growth include the following.

Protection of property rights

Impartial enforcement of the rule of law

Effective, independent justice system for contract enforcement

Checks and balances on the arbitrary and exercise of power

Independent central bank for monetary and currency stability

Social safety nets and channels for economic inclusion

A set of simple, stable rules that facilitates and protects the pursuit and ownership of wealth is therefore key to prosperity. In the absence of such rules, investment in physical and human capital would be retarded and so not all wealth creating opportunities would be exploited. Prosperity is best achieved when people are allowed to pursue their material desires without fear that the fruits of their efforts will confiscated, nationalized, stolen, frowned upon, or undermined by change of regulation, directive or subsidy. The stock of capital, the technology of production, and the institutional framework all contribute to the high levels of productivity that are

observed in the wealthiest countries in the world. But each of those factors contributes to economic growth in different ways and those differences are important to understanding why some countries are rich while others are poor. It is to those differences that we now turn.

G

ROWTH BY

A

CCUMULATING

C

APITAL

A higher level of capital makes each worker more productive and therefore allows a greater level of output per worker. And capital can be accumulated by investing in new equipment, structures, and skills. How can investment rates be raised so that everyone can have more capital. We know that savings provides the resources from which investment can occur. So everyone should save more. To understand the broad economic

consequence of saving more, we must first call upon an important property factor use.

D

IMINISHING

R

ETURNS TO

C

APITAL

Recall that the idea of diminishing returns suggests that, if all other contributing factors are fixed in amount, increasing only one factor will eventually yield smaller benefits. This basic idea, which applies to the consumption of ice cream on a hot day as well as to the use of labourers when clearing a field with a limited supply of machetes, applies just as well to a country’s investments in capital in the presence of fixed population. The paving of roads in a country with few paved roadways to begin with will facilitate the transportation of goods and people greatly and stimulate commerce. Road construction is one of the easiest ways for a government in an economically stagnant country or region to encourage some growth. Roads reduce the cost of transporting workers and raw materials to the factory or farm and finished goods to markets.

6

Once most of the arteries within and between cities, towns and villages are paved, however, additional road construction will not have as dramatic an effect on the stimulation of new commercial activity. Indeed, after a point, additional roads will hardly have cars on them. The road network will allow the country to become much wealthier. But even more investment in roads, while still adding to wealth, will have a smaller effect than the initial investment.Additions to capital, therefore, will eventually exhaust the ability of other factors to make use of it, as long as there is a limit to the availability of other factors. The size of the potential labour force is one such limit, but the set of particular skills within that labour force are limiting factors as well.

Machine operators are limited in supply, as is computer-literate call centre workers and managerial talent. Each of these limits implies that after a while, adding more machines, computers, or offices becomes less productive.

While these examples apply to additional investment in the same type of capital, whether roads or machines, diminishing returns will apply even when considering investment across different types of capital. When comparing different types of capital, investment will naturally flow first into the projects with the highest returns, since that is where the largest profits are to be earned. Once those opportunities are exploited, though, later investments necessarily are left with projects with a lower return. In this way, additional investment necessarily yields lower returns in an economy at any point in time.

T

HE

E

FFECT OF

D

IMINISHING

R

ETURNS

The most straight-forward way for the citizens of a country to become wealthy is to save. Savings increases investment and investment in turn increases the stock of infrastructure, equipment, and skills that can produce a larger amount of goods and services in the future.

Savings rates differ greatly around the world. Whereas Brazilians save around 7 percent of their total production, in India, by contrast, nearly 35 percent of GDP is set aside for the future.2 That high savings rate is fueling

the expansion of productivity capacity in India without the need for Indians to borrow internationally to fund the investment.

While investment funded by high savings is an easy way to increase wealth, however, it cannot be the source of continuous high growth rates, and this is due to diminishing returns. A country can save a set amount of its income each period, and those savings can build and manufacture and train so that the capital stock grows, but the amount of additional goods and services that will be produced by that capital will fall off after a while.

The Soviet Union, a federation of Russia and several nearby states that existed for much of the 20th century, provided a natural experiment in both

the power and limit of capital accumulation. A communist country, the Soviet Union employed central planning of almost all production with a prohibition on private ownership of productive resources. Because of central control of production and wages, the Soviet government in the early part of the century extracted extremely high rates of savings from the population from which it invested massively in infrastructure and heavy industry. Industrial capacity expanded rapidly and spurred economic

7

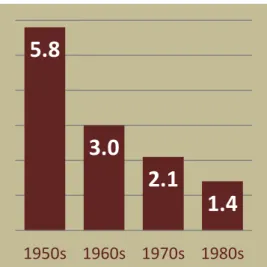

growth that transformed the country a poor, largely agricultural producer to industrial and military might. At its peak in the 1950s, the economy grew at nearly six percent per year.The problem was that, without private ownership of productive resources, there was no incentive for managers to invest in new technology, so adding capital was the only source of growth. And after a while, diminishing returns set it. Figure 2 shows how the growth rate declined every decade right up until the collapse of the regime in 1989.3

Saving and investment, therefore, eventually become subject to diminishing returns. The paving of roads, training in vocational skills, and other capital investments can have a dramatic effect on the wealth of a country, but such investments eventually begin to have only a small incremental effect on output. Indeed, by itself, high levels of savings could eventually cease to have any effect on growth at all. If the returns to investment become sufficiently low, even though still positive, savings may be directed to investments abroad or some may choose not to save at all.

T

HE

E

FFECT OF

D

EPRECIATION

Diminishing returns is not the only reason why capital investment alone cannot sustain high growth rates indefinitely. Depreciation plays an important role, too.

Physical capital often deteriorates with use. Moving parts wear out; paint gets dirty and strips; breakable items break. The cost of maintenance and repair to keep capital working like new is referred to as depreciation. It is the economic value of the deterioration of the asset.

Different types of capital depreciate at different rates. Machinery with lots of moving parts wears out relatively quickly; concrete and brick buildings depreciate much more slowly. Skills usually don’t depreciate at all, except that some knowledge based skills may become less current and therefore less useful without re-training.

The tendency of most forms of capital to require repairs and maintenance further reduces the likelihood that saving and capital investment can produce endless economic growth. The larger is the stock of buildings and equipment, the greater is the need for and the cost of maintenance. Indeed, the cost of depreciation should rise proportionately with the stock of capital.

If the cost of maintenance and repairs keeps getting larger, an increasing amount of savings has to be devoted to keeping capital running, leaving less savings left over to expand the capital stock. With a sufficiently large stock of capital, repairs and maintenance will use up all savings and no further expansion of capital is possible. In addition to the effect of diminishing returns, therefore, depreciation is another reason why saving and investment cannot be the source of continuous economic growth.

F

OREIGN

D

IRECT

I

NVESTMENT

The level of savings is not the only determinant of the amount of

investment in an economy. There is a loophole to the constraint imposed by the level of domestic savings – foreigners may want to use their own Depreciated Capital

5.8

3.0

2.1

1.4

1950s 1960s 1970s 1980s

Figure 2: Annual Average Growth Rate, Soviet Union

8

savings to make investments in your economy. Foreign direct investment (FDI) refers to investment by foreigners in productive capacity in the local economy.BP of Britain extracts crude oil in Saudi Arabia; India’s Bharti Airtel delivers mobile services in Congo; France’s Total retails petrol in Columbia. Little of the funding for these investments drew upon the pool of local savings. For this reason, many governments try to attract foreign investment to break the constraint upon growth imposed by the limited amount of local savings. The foreign source of the investment does not, however, exempt it from the imperative of diminishing returns. Even foreign investment is constrained by the limited supply of local infrastructure and labour. And, like domestic investment, FDI will try to enter the most lucrative industries first. Both of those considerations will ensure that returns to investment will gradually fall if there is other economic stimulant.

Saving and investing can, therefore, make a country rich, but it cannot sustain a continuously high rate of economic growth. After a while, diminishing returns and rising depreciation combine to throttle the boost that investing in capital alone can provide. If we want to understand how Europe and North America has been able to maintain moderately high rates of economic growth for more than 200 years, we will have to look

elsewhere.

A

M

ODEL OF

E

CONOMIC

G

ROWTH

The role of savings and investment in contributing to a higher standard of living can be represented in a simple model that captures the role of diminishing returns and depreciation. To construct it, we need to introduce the production function.

A production function relates quantities of inputs, such as the amount of capital, to the quantity of output that can be produced by it. If you have capital consisting of 2 sewing machines, a few rulers, and a pair of scissors plus 80 hours of labour, then the production function can tell you that in the course of a week you can produce, say, 25 shirts.

A production function that relates each possible level of the capital stock, designated by K, to the corresponding amount of output, Y, that it can produce, is shown in Figure 3. The production function captures a number of features of the relationship between capital and output that we have discussed. The production function shows that the more capital an economy has, the greater the output that it can produce. This is reflected by line always rising – more capital always yields more output.

The production curve also shows that increments to the capital stock add less to output when the capital stock is already high than when it is low – the law of diminishing returns. The two dashed lines in Figure 3 illustrate the point. Both represent equal increases in capital – the horizontal portion of the dashed line; but each adds different amounts to output – the vertical portion of the line.

Besides the amount of capital, there are other contributors to the level of output that are not shown on the graph, but are relevant to the production

Y

K

9

function nonetheless. There is a working population of a particular size, but our interest is in GDP per person and increased output that derives from the contribution of additional persons won’t necessarily raise that measure. Technology and institutions are relevant, but the production function is drawn on the basis of the current level of technology and state ofinstitutions in order to isolate, for now, the contribution of changing only the amount of capital.

Since savings is the source of the investment that is to produce the higher level of output, we need to be able to determine the amount of savings at any point. This is accomplished by assuming that savings is a constant fraction of income. If savings is, say, 25 percent of income, and recalling that output and income are always equal, then the savings curve can be drawn such that each point on the curve is a quarter of the height of the

corresponding point on the production function above it. This is shown in Figure 4.

Depreciation, it was noted earlier, is proportional to the amount of capital in the economy. The curve showing the amount of depreciation is therefore a straight line from the origin in Figure 4, showing that as the capital stock rises, the cost of maintenance and repairs rises proportionately.

At low levels of capital, such as is represented by K0, the capital is stock is

sufficiently small that the cost of replacing the depreciated portion is low, represented by D0. At the level, the amount of savings, S0 is large enough to

be able to cover the cost of repairing the depreciated capital stock and still have some left over that can be used to invest in new capital. The surplus savings is the gap between S0 and D0. Because of that invested surplus, the

capital stock and therefore the economy’s productive capacity will increase. The expanded capacity will produce a greater amount of goods and

services. In other words, as K increases, the production function indicates, so will Y. The economy has experienced economic growth.

However, as the capital stock grows (that is, as the economy moves to the right on the horizontal axis), the cost of depreciation rises. Despite the fact that a larger economy with a higher income can save more, the growing capital stock requires an ever larger portion of savings to be set aside for depreciation, thereby reducing the portion left over for further growth. Eventually, the capital stock is so large that the entire pool of savings is devoted to replacing and repairing depreciated capital. This is shown at K* and S*. Since there is no surplus savings left over to invest in new capital, Growth in this economy comes to a halt.

The model of economic growth corroborates the conclusion drawn earlier. If we depend only on savings and the consequent expansion of the stock of capital to generate economic growth, it can do so for a while. But eventually, the economy will stagnate. Mere investment in more productive capacity that is not a technological improvement may make a poor country wealthier, but it will not keep it growing indefinitely.

Figure 4

K

Y

Depreciation Output

Savings

K0

K*

S*

S0

D0

10

G

ROWTH BY

I

NNOVATION

T

HE

E

FFECT OF

I

NNOVATION

Adam Smith’s pin factory demonstrated that the way in which production is carried out, the technology of production, influences the productivity of the capital and labour used. Economic growth may therefore arise from seeking and implementing new and better ways of producing goods and services, that is, by innovating.

Innovation stimulates economic growth in a many different ways. First, the innovation, whether it is a farm’s irrigation method or supermarket’s barcode scanner, directly raises the productivity of the workers and the capital. The farmer’s yields will rise and the shop owner’s cashier will process more customers. So the innovation will produce a burst of economic growth as it spreads throughout the country.

The greater output and incomes that are produced by the innovation will also allow people to save more. The availability of more savings will

stimulate more investment, either because banks will be eager to lend it out or because government may tax some of it to provide better roads and utilities. Moreover, the innovation itself is often embedded in hardware and so requires additional capital spending. In this way, the adoption of a new technology permits and stimulates new investment which expands the country’s productive capacity. As productive capacity grows over time, the effect that a new technology has on economic growth is extended. The effect is not indefinite since the larger stock of capital both diminishes the return to further investment and raises the provision for depreciation, but it is prolonged nonetheless.

Another reason why a single innovation may have a long lasting effect is that new ideas can themselves stimulate even newer ones. When 17th

century scientist Sir Isaac Newton credited his considerable achievements to him having stood “on the shoulders of giants” he was referring to a peculiar characteristic of ideas. Knowledge of elementary ideas facilitates discovery of more complex ones. Knowledge of the ideas in Karl Benz’s 1885 motowagen were a key element in the design improvements that have occurred in automobiles since then.

So it is by constant innovation that the persistently growing economies in the world have managed to do so. The levels of productivity in the developed economies of Europe and North America and in the more

successful once developing ones such as South Korea and Singapore are due to a relentless ability to continually implement better ways of producing. Many production techniques now being employed in the most advanced factories and farms around the world were unheard of 20 years ago, some even 10 years ago.

S

OURCES OF

I

NNOVATION

With new ideas playing such an important role in economic growth, you may be wondering where new ideas come from. There are two possibilities. In the most technologically advanced countries, new ideas have to be invented. While some inventions are accidental, the for the most part researchers have to choose to devote time and effort to the specific goal of

11

coming up with a new technology. The more resources that are devoted to research and development rather than to the production of goods and services, the more new ideas will be discovered and the faster the technology will advance.Most countries in the world have another option for improving their technology of production. Any country that is not itself at the forefront of technology, such as developing or emerging economies, can simply copy the technology of the more advanced ones. Trinidad & Tobago extracts oil from the southern part of the country using sophisticated drilling technology that it did not itself invent. Nor did it need to. It could copy the technology by importing the appropriate machinery and investing in the training in the technical knowledge required to operate it.

In most cases, it is cheaper and faster for countries to adopt and adapt the technology of other, more advanced countries than it is to engage in the research and development necessary to re-invent it from scratch. Technology transfers can occur by mimicking the processes of more advanced firms, by importing the capital equipment that embodies the technology, or by foreign investors bringing the company’s technology with them when they set up business in local economy.

Since copying technology is cheaper and faster than discovering or

inventing it, technological laggards have the potential for faster growth than technological leaders. This is an important factor limiting the rate of growth in the world’s richest countries. Growth rates higher than eight percent are unheard of in the most advanced countries; yet, more than two dozen developing and emerging economies have managed that feat in recent years.

I

NNOVATION IN THE

G

ROWTH

M

ODEL

Each production function, like the constructed above, represents the relationship between different amounts of capital and their corresponding levels of output, for the current state of production technology. We have already concluded that if technology improves, then the existing labour force and capital will be able to produce a greater amount goods and services. So a change in technology changes the relationship between any particular amount of capital and its associated amount of output that was captured by the old production function.

Figure 5 shows such a relationship, in which K0 of capital, along with the

labour force, could produce Y0 of output. But with production innovation,

that same amount of input may now produce the greater amount of output, Y1. This change is reflected on the new, higher production. The

improvement in technology shifts the production function upward. We noted above that the higher incomes allowed by the more advanced production techniques would permit people to save more. This is depicted in Figure 6, which shows an upward shift of the savings curve such that the level of savings rises from S0 to S1.

Because the higher amount of savings, S1, is now greater than the amount

needed just to replace depreciated capital, equivalent to S0, the extra

savings can be invested in new equipment. So the capital stock will grow. As before, capital will grow until depreciation is absorbing all savings, which

Y

K

Figure 5

Output

K0

Y1

Y0

Figure 6

K

Y

Depreciation

Savings

K0

K*

Y*

S1

S0

12

occurs at K*, at which point growth ceases once again, at least until the next technological innovation is employed. Note, however, that the economy has become wealthier due to both higher productivity and also a larger capital stock.G

ROWTH BY

R

EFORM

The decision to invest or innovate is motivated by the incentive of the expected return relative to the risk involved in making the commitment. We noted above that the rules of economic engagement, institutions, affect both the return and the risk. If those institutions change in ways that facilitate or incentivise economic activity, therefore, the economy will grow as investors and innovators move to take advantage of the new opportunities opened up by the reform. The nature and strength of institutions is the main

determinant of prosperity and positive institutional change is the surest way to promote economic growth.

The institutions that are important for economic activity, whether strong or weak, good or bad, tend to be persistent. Countries with weak rule of law one decade tend to still have it the next. Most of those with secure property rights now have enjoyed it for a long time, in some cases, for over a century. Because of this persistence, the quality and character of a country’s

institutions are difficult to change. For example, the respect for

constitutional authority is derived from decades of peaceful constitutional changes of power. Without that history, usurpers may seek any opportunity to overthrow an elected government with a reasonable expectation that the society will tolerate such a transition.

The persistence of economic institutions is because they are the outcomes of political institutions which themselves derive from the distribution of political power. Whatever is the source of that power in each society, whether it is resources, culture, or military, it tends to have permanence. Moreover, every existing set of rules and circumstances will have a class of persons who benefit from that situation and have become powerful within that context. Those persons therefore represent a class of interests that will resist institutional change.

E

FFECTING

I

NSTITUTIONAL

C

HANGE

Despite the persistence of economically relevant institutions, change does occasionally occur and produce dramatic economic results. Witness the impressive growth of Singapore after 1970 and China after 1990. How, then, does a country’s institutional framework for economic activity change?

Revolutionary change can sweep old institutional structures and permit radical change in rules governing economic activity. The Cuban revolution of 1959, which all but eliminated private property, and the collapse of communism in Russia under the Soviet Union in 1991, which introduced private property, both exemplify revolutionary change.

Occasionally, a confluence of propitious political economy forces and effective leadership can bring about institutional reform. India emerged

13

from a period of economic stagnation and political crisis in the early 1990s and was able to garner broad support for a series of reforms that abolished the state monopoly in many sectors and liberalized the import licensing regime under the guidance of finance minister, Manmohan Singh. In the absence of political accident or social fortune, a few steps can be taken. First, promoting transparency and accountability limits the damage that concentrations of power can wield and increases the likelihood that policy will be to the benefit of most citizens. Second, instituting limits to the exercise of power and checks and balance will limit the economic damage that bad administrations can do.Without reform, in the presence of institutional hurdles in the way of investment and innovation, potential surplus savings may go unsaved or be saved in unproductive ways. People prefer to “waste” their earnings on consumption rather than make investments from which they may not be able to enjoy all their earnings. Innovators turn to less entrepreneurial pursuits or migrate.

I

NSTITUTIONAL REFORM IN THE

G

ROWTH

M

ODEL

As long as institutional obstacles exist to investment and innovation, An economy may remain stuck with a low level of capital and inferior

technology. Look again at an economy with a low level of capital such as K0

in Figure 4. Potential surplus savings, represented by the gap between Savings, S0, and depreciation, D0, will diminish as the absence of a secure

return on investment reduces the incentive to save in the first place. As a result, the economy will have a low savings rate, so the savings curve in the growth model will be low.

Reform that improves the rules governing economic activity will uncork pent up investment and so increase the incentive to save. For a given level of technology and production function, therefore, savings will rise. As savings rise, more investment will occur and the capital stock will grow. At the same time, the same reform that increases the incentive to

investment by local entrepreneurs will also make investment attractive to foreign investment. As a result, foreign direct investment will also rise, further expanding productive capacity without any need for local savings. Investment in upgraded technology has a longer term pay off, but improved stability and security will stimulate that, too, at some point. The upward shift of the production function that results from improved technology will further push the economy to a higher growth trajectory. Therefore, institutional reform can increase savings, investment, innovation, and growth.

E

XPERIENCES OF

E

CONOMIC

G

ROWTH

S

OUTH

K

OREA

In 1960, the Republic of Korea was one of the poorest countries in the world. Its per capita GDP, at US$1,100, was only twice the level of the average for sub-Saharan Africa and poorer than most of the Caribbean and Latin America.

South Korea

Manmohan Singh, Minister of Finance in India, 1991.

14

In contrast to the totalitarian North, South Korea established itself as a democracy with accountable, elected officials. In the 1960s, theadministration Park Chung Hee established the economic foundation as one of markets and incentives, high savings rates, good education, and targeted industrial policies.

The Korean government strongly encouraged high savings rates with large public investments in infrastructure and spending on education. In the 1970’s, its industrial policy targeted heavy industries with an

accompanying focus on expanding technical and vocational training to create a complementarily-skilled work force. At the same time, foreign direct investment was encouraged as a way to climb up the technological ladder. Later on, the focus of Korea’s industrial policy switched to

technologically advanced industries with the government investing heavily in information infrastructure. Korea has maintained a relatively open stance with respect to international trade (notwithstanding selective domestic protection of certain manufactures early on) since export promotion was a key element of its strategy.

The relentless pursuit of adopted technology has been at the centre of Korean development from the first industrial plan to the latest corporate strategy of Samsung. The targets of its industrial policy, the encouragement of FDI, and the education and training programme, all were dedicated to mimicking the technology of the advanced West. And all this in a society where private property was sacrosanct and the rule of law was ironclad. Korea’s impressive growth began straightaway from the 1960s and continued almost without let up. By 2011, GDP per capita reached nearly US$22,000, making it equal to the average for the European Union. In a generation, Korea moved from one of the poorest to one of the wealthiest countries in the world.

But the relentless copying of foreign technology as a means of rapid growth works only as long as you are technologically backward. As Korea has caught up with the technologically advanced countries, it can no longer grow faster than they do by copying their technology. It has to switch to pursuing in its own breakthroughs, which is a more difficult business. Whereas in the 1970s, it enjoyed annual growth of 10 percent, in the 2000s its rate of growth has fallen to less than 5 percent.

C

HILE

In the 1960s, the Chilean economy was typical of that poorly performing region. By the early 1970s, output was falling and prices were hyper-inflating. In 1973, Salvador Allende’s elected government was overthrown by Augusto Pinochet, who instituted an absolute military dictatorship. Both the military backing and General Pinochet’s ruthlessness meant that all other political forces and interests could be ignored or overtly repressed, leaving the General with a completely free and brutal hand. Institutional legacies were not a constraint.

A series of reforms were introduced during Pinochet’s 17-year term. In the 1970s, Chile eliminated import barriers and welcomed foreign investment. At a stroke, Chile went from being one of the most protected economies in the world, with average import tariffs of more than 100 percent and hundreds of restricted items to one of the most open trade regimes with a

15

flat 10 percent import tariff. Also in the 1970s, the system of domestic price controls was dismantled and market forces were allowed to determine the prices of all goods and services.Recognizing the importance of the institutional environment to economic growth, the government promulgated a new constitution in 1980 in which it embedded its key reforms. The security of private property and the independence of the central bank (the better to focus on sound monetary policy without fear of a meddling government) were entrenched. The constitution also limited the power of the legislature to easily change certain laws that may have great impact and also limited the power of the government to spend.

The 1980s witnessed pension reform and privatization. The pay-as-you-go pension scheme was turned into a fully funded, privately managed scheme, considerably boosting the country’s level of savings. As a result, investment rose steadily. There was also a massive privatization programme that returned hundreds of state-controlled enterprises to private ownership. GDP growth accelerated during the late 1970s and, following a severe recession, again from the mid 1980s to reach more than 7 percent per year for most of the nineties. As we should now have now come to expect, in the noughts, GDP growth fell off to around half that, but not before Chile became the richest country in Latin America.

Z

IMBABWE

Institutional reform that affects the economy and impacts the lives of citizens can change in either direction. Zimbabwe provided an example of the wrong kind of change. Along with South Africa, Zimbabwe had one of the strongest institutional regimes for economic activity in sub-Saharan Africa, even in the context of massive inequality of incomes and

opportunities. Zimbabwe had strong rule of law, secure property rights, and competent economic institutions. As a result, GDP growth averaged 4.3 percent per year after independence in 1980.

Zimbabwe exemplified the importance of property rights even before land reform undermined the security of property rights completely. The vast difference in the productivity of commercial farms compared to communal lands may have been because of the institution of land ownership. the latter were communally owned, without any individual being able to exercise secure control. In that case, there was no incentive to invest in the land since the fruits of that investment did not accrue to a single, secure property owner. Quite the opposite occurred. Since any losses were shared, communal lands become victims of overuse and degradation – an example of the tragedy of the commons.

In any event, under the dictate of President Robert Mugabe, the government authorized the seizure of some 4,500 commercial farms owned by white farmers for re-distribution to indigenous Africans. In addition to

undermining the key institutional foundation that is the incentive for economic activity, secure property rights, Mugabe went on to undermine the independence of the central bank and the court system that tried to constrain his unconstitutional exercise of power.

16

Once the rule of law and property rights began to be undermined in 2000, the collapse of the Zimbabwe economy was swift. Once a major food exporter, Zimbabwe’s food production collapsed. Commercial farm land lost nearly three-quarters of its value in a single year.4 And Zimbabwerapidly became much poorer. The economy contracted every year from 2000 to 2009, by the end of which Zimbabwe’s economy was not even half the size it was at the start of the decade.

S

UMMARY

The vast differences in living standards observed across the globe and over time, as reflected in each country’s GDP per capita, are due to differences in capital, technology, and institutions. Capital – tools, buildings, and skills – leverage the abilities each person to produce a much greater amount of output than could be accomplished on his or her own. The technology of production – the way in which production is carried out – can elevate the total productivity of all productive inputs. Institutions – the rules of the economic game – can inhibit or facilitate the activities related to production, investment, or innovation.

Since capital, technology, and institutions are the foundations of wealth, then investment (in capital), innovation (in technology), and reform (of institutions) are the sources of economic growth. Investment in capital is the easiest way to raise productivity and incomes, but does not sustain growth indefinitely. A steady stream of innovation can maintain moderate rates of growth seemingly indefinitely. The closer to the technological frontier a country is, the more it must innovate by discovery and invention; whereas if a country is less technically advanced than its neighbours, it can grow faster by importing production ideas. Institutions that are either weak or obstructive are the biggest obstacle to economic growth in poor

countries. This is because rules, customs, and capacity tend to be persistent over long periods of time and entrenched interests that benefit from the status quo resist change.

Nonetheless, institutions occasionally get reformed, technological leaps are made, and both foreign and domestic capital is invested to spur significant and sustained growth in many countries once poor. Singapore, Botswana, South Korea, Ireland, and Chile are only a few of many examples. With better understanding of the forces at work, there may be more to come.

1 David Dollar and Aart Kray, “Trade, Growth, and Poverty.” The Economic

Journal, February 2004.

2 Businessweek.com, “Savers and Spenders”, June 10, 2010, 5:00pm EST 3 Vladimir Popov, “Life Cycle of the Centrally Planned Economy: Why Soviet

Growth Rates Peaked in the 1950s,” CEFIR/NES Working PaperSeries, No. 152, Centre for Economic and Financial Research at New Economic School, November 2010.

4 Craig Richardson, “How the Loss of Property Rights Caused Zimbabwe’s

Collapse” Economic Development Bulletin, Cato Institute, November 14, 2005.