The transfer of statistical equilibrium

from physics to economics

Parrinello, Sergio and Fujimoto, Takao

Università di Roma "La Sapienza", Okayama University

1995

Online at

https://mpra.ub.uni-muenchen.de/30830/

THE TRANSFER OF STATISTICAL EQUILIBRIUM

FROM PHYSICS TO ECONOMICS

Sergio Parrinello (University of Rome “La Sapienza")

and Takao Fujimoto (Okayama University)

1995

ABSTMCT

Two

applications

of

the

concept

of

statistical

equilibrium, taken

from

statisticalmechanics, are compared: a simple model

of

a pure exchange economy, constructed asan alternative to a walrasian exchange equilibrium,

and

a simple modelof

an industry,in which

statisticalequilibrium is

used asa

complementto

the

classicallong

periodequilibrium.

The postulateof

equalprobability

of

all

possible microstatesis

critically

re-examined. Equal probabilities are deduced as a steady state

of

linear and non-linear2

Introduction

The

concept

of

statistical

equilibrium

is a

fundamentalanalytical

tool

in

physics and

particularly

in

statistical mechanics.After

having borrowedthe

classicalmechanics concept

of

equilibrium,

economic

theory has

occasionally

turned

itsattention

to

the

other

concept

of

probabilistic equilibrium.

In

fact,

since

thecontributions

which

appearedin

the

50s andthe

early 60s

it

is

only

recently

thatserious

attemptshave

beenmade

to

revise

and

develop

the notion

of

statisticalequilibrium

in

economics. Past contributionsinclude

Champernown(1953),

Simon-Bonini

(1958),Newman-Wolf

(1961) and Steindl (1962) and weremainly

related toGibrat's Law

(1931)

andto

Paretodistribution.

Recentworks,

explicitly linked

to thermodynamics, areE.

Farjoun

-

M.

Machover(1983)

and, in paficular,

Foley (1991, 1994) .In

economics a statisticalequilibrium is

a most probable distributionof

certain economic entities (say firms or individuals) which cannot all be distinguished onefrom

another, rather

than a particular configuration

in

which

eachentity is

identified.

In

other words,

this

equilibrium

is

a

macrostatewith

maximum numberof

realizations(microstates) and, as such,

is

a distinct

conceptfrom

a

state obtainedby

the

simpleinclusion

of

some random

variable

in

the

relations

which

determine

a

classicalequilibrium.l

In

thiswork two

applications of the conceptof

statisticalequilibrium

toeconomic theory

will

be formulated and compared using simple models. Furthermoreit

will

be

shown

that, under sufftcient

conditions,

a

state

of

equal

probability

of

microstates - a basic postulatein

statistical mechanics-

in the long period is consistentwith

unequal transition probabilities.In

section

1 the

first

application

is

a

model

of

a

pure

exchange economy, constructed as a special caseof

Foley's (1994) modelin

which

statisticalequilibrium

appears

as an

altemative

to

the

Walrasian

equilibrium.

In

section

2

the

secondapplication

is

a

model

of

an industry

in

which

statisticalequilibrium

is

usedas

acomplement

to

the

classicallong

periodequilibrium.

It will

be

arguedthat

only

thelatter application maintains the notion

of

statisticalequilibrium

adoptedin

thefield

of

physics; whereas the former differs fromit

on an essential point and resolvesitself

intoa

concept

of

equilibrium

similar

to

that

of

temporary

equilibrium

adopted

in

economics.

In

section3

the

postulateof

equalprobability

is re-examined

and

a simple case of linear Markov chains is presented, in which equalprobability

is a steadystate

of

a

stochasticprocess.

In

section4

this

uniform probability

outcome is generalizedto

non-linearMarkov

chains, applying a theorem provedby Fujimoto

and Krause (1985).Let

us

make

a

simple

exampleof

statistical

equilibrium

for

an

exchangeeconomy, as

a

special caseof the

statisticaltheory

of

markets developedby

Foley(1991-1994). In this theory the elementary unit of analysis is the

individual offer

set :"The marlret

beginswith

agentsdefined

by offer

setsreflecting

their

information,technical pos sibilitie s, endowments and preferenc e s " (p. 3 2

4.

"In

termsof

standard production-exchange model,...., offer sets consistof

technicallyfeasible

transactions leading toJìnal

consumption bundles that arepreferred to

initial

endowments" ( Foley p.32a)

Suppose

that

there are

only

4

agentse,o2,bt,b2

and

two

goods

X,Y

thequantities

of which

are measuredby

integers. There is a totalof

4 unitsof

goodX

and4

of

goodY

which

are equally distributed at the beginning: eachindividual

therefore has an endowment of one unit of each good. V/ewill

athibute to the agents very simple preferences: agerrtsar,a.,

like

goodX,

but

areindifferent

to

goodY;

whilst

agentsbr,b, like

goodY,

but

areindifferent

to

goodX. An

agent's transactionis

a vectorof

quantitiesof

thetwo

goodswith

a plus signto

indicate a net acquisition, a minus signfor

a net cession and zeroif

theinitial

endowment is maintained.The

offer

setof

an agent is the set of transactionswhich

areweakly

preferableto and feasible for

him

in relation to hisinitial

endowment. In Foley's model theagents

that

havethe

sameoffer

set are considered indistinguishable and represent atvoe

of

asent.In the figures below the lattices represent parts

ofthe

offer sets ofagentsoftype

A

andB

as

feasible transaction

sets.The

null

transaction

(0,0)

is

included among

theType A

2

Type B

In

the

examplewe

can thereforefind two

typesof

agents:type

A

(to which

ar,a,

belong) and type

B

(to whichbr,brbelong).

These types can be identified by theiroffer

sets

which

are

distinct

asfar

astheir

preferences are concemed,but not

for

their

endowments.

Table

I

describes the feasible microstates of the exchange economy.TABLE.

I

(0 0)

(r

-1) (-1l)

ar ra, ,br rb,ar rb qr b,

Ar,b. a1 b1

a"b, al b.,

arb, ar b1

0t ,Cl, br,b,

It

isto

be noted that no exchange takes placein

thefirst

microstate and each agentin

the last one acquires one

unit

of

his preferred good against oneunit

of

his indifferent

good.

In

the otherfour

microstatestwo

agents make one preferred transaction,whilst

the other

two

remain in theirinitial

position.Let us

consider

the

feasible

statistical

aggregatesor

macrostatesof

theexchange

economy

by

treating

agentsof

the

sametype as

indistinguishable

and [image:6.604.65.523.60.290.2]we

find

three macrostates,two

of which are madeof

only one microstate (thefirst

and the last one represented in tableI)

and one made by four microstates (the others).Let us assign equal probabilities to all feasible microstates.

A

statisticalequilibrium

is

a macrostatewith

maximumprobability, that

is with

themaximum number

of

feasible equally

probablemicrostates.

In

the

example thismacrostate is the one

with

four microstates, in which, for each typeof

agent, one of thetwo

benefits from the exchange by acquiring aunit

of his preferred good andby giving

up a

unit

of the indifferent good, whilst the other agent remains at the status quo.A

market statistical equilibrium in the model developed by Foley possesses thefollowing

interesting featuresthat

contrastwith

those sharedby

a

walrasian generalequilibrium:

1.In general

it

is not Pareto-efficient;2.It

doesnot

imply

auniform

exchange ratio betweeneach

pairof

commodities overall

transactions;

3.A uniform

entropy priceis

associatedto

eachgood:

this

priceis

a shadow pricedetermined

by

solving

an entropymaximizing

problem under thetotal

endowment constraints.Property

I

is

straightforwardin

our exchange model, as the most probable macrostateis Pareto-inferior compared to that in which all the agents obtain a

unit

of the preferred goodin

exchangefor

the other good. Instead properties2

and 3 are not evidentin

this simple model andwe

shallnot

be concernedwith

themfor

the sakeof

thefollowing

argument.

It

should

be

emphasizedthat

the

statistical

equilibrium

of

the

exchangeeconomy

is

determinedby offer

setsthat

dependon the

initial

endowmentsof

eachindividual.

In

general

the

offer

sets undergo endogenous changeif

the

economy is conceivedin

real time. To make this point clear,it

is

suffrcientto

assume that thetwo

goods are

non

perishableand

that the

economyis

subjectto

two

trials

and two

corresponding observations. Let us suppose that the

following

microstate is realizedin

thefirst trial:

Then at the second

trial

the individual endowmentwill

differ

from that at the beginningof

thefirst

trial.

Therefore the typesof

agents and the numberof

each typewill

differ

macrostate

which

has beendefined

as statisticalequilibrium

at the first

trial

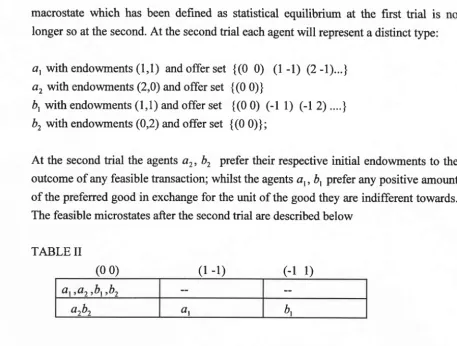

islonger so at the second.

At

the secondtrial

each agentwill

represent a distinct type:a, with

endowments(1,1)

and offerset

{(0

0)

(l

-l)

(2 -l)...\

a,

with

endowments (2,0) and offerset

{(0 0)}

ór

with

endowments (1,1) and offerset

{(0

0)

Cl

1)

Cl

2) ....} b2 wfth endowments (0,2) and offerset

{(0

0)};

At

the secondtrial

the agentsar,

b,

prefertheir

respectiveinitial

endowmentsto

the outcome of any feasible transaction; whilst the agents ar,b,

prefer any positive amountof the preferred good

in

exchangefor

theunit

of the good they are indifferent towards. The feasible microstates after the secondtrial

are described belowTABLE

II

(0 0)

(l

-l)

(-l

1)ar ro, ,br rb,

o"bt qr bl

From the statistical

point

of

view

the sample space has changed. Thetwo

microstatesin table

II

each haveprobability

ll2

at eachtrial.

Howevef, as the trials are repeated anindefinite

numberof

times,the

second microstatewill

be

realizedwith probability I

and

when

that

happens

the

economy

will

have

reached

a

Pareto-efficient configuration.2At

that point theof[er

setof

each agentwill

be represented by thenull

vector (0,0), that is by the absence of any further transaction.

One

may

well

ask whetherthe

statisticalequilibrium

of

exchange, as defined above, preservesthe

conceptof

statisticalequilibrium

in

physics.The

answeris

no.The latter has the relative persistence

of

its determinantsin

commonwith

the classicalequilibrium

in

economics;

by

contrast,

the

statistical

exchangeequilibrium,

asillustrated

in

the

example, doesnot

possessthis

prerequisite andfrom this point

of

view

it

is similar to

the conceptof

temporaryequilibrium

in

economics. Furthennore,if

the modelof

statisticalequilibrium

of

the exchange economyis

interpretedin

realtime,

it

becomes

a

model

of

statistical disequilibrium,

with

certain

transitionprobabilities

that

imply an

absorbingmicrostate.

This

state

is a

Pareto-efficient2In a certain sense the agenl.s ar,a2,b1,b, cottld not be distinguished into type A and B right from the very first

trial if "distinguishability" also requires "observability". In fact at the beginning all agents have the same initial

[image:8.612.75.532.66.411.2]equilibrium.

The stochasticfeature

is

inherentonly

in

the adjustment(or

relaxation)process but not

in

thefinal equilibrium

of the exchange.In

a more general modelwith

many Pareto-effrcient microstates, we

would

find

a problemof

indeterminacysimilar

to

the

onefound

in

a Walrasian exchangemodel

if

we

assume that transactions canoccur at

disequilibrium

pricesin

the

adjustment process towardsequilibrium.

In

thiscase

the

convergenceof

the

stochastic process towardsa

Walrasianequilibrium

is possible,but

in

generalthis equilibrium

state isnot

a walrasianequilibrium relatively

to

the

initial

endowments.As

a

consequence,the

statistical exchangeequilibrium

is"statistical"

only

becauseit

is reachedby

a successionof

stochastic disequilibria whenit

is stable, butit

is not statisticalin

so far asit

coincideswith

a microstate which takesprobability

I

at thelimit.

2.

A

model of stotisticol eauilibrium of the industrvNow we

shift

to

a morepoúe

applicationof

statisticalequilibrium.

Let

us supposenow that an

industry

is

in

a

long period

competitive

equilibrium,

under constant retums to scale at thefirm

level. Suppose that its product can takeonly

integer numbers 1,2,3,...Let

Q be the quantity produced andN

the number of firmswhich

canproduce at

the minimum

cost perunit of

output.With

these hypotheses,if

D

is

the demandfor

the product atthe long

period prices, the theoryof

classicalequilibrium

determines Q from the equation

Q:

D, but does not determine the size of eachfirm.

Let us

considernow the

feasible microstatesof

the industy which

can

be obtainedby

distributing

in

every possibleway

theN

firms

among the possible sizes measuredby the

quantities 0,1,2,3....In

orderto

illustrate

this we

will

present an example similar to that used byothers (A.

F.Brown,

1967) to introduce the conceptof

statistical

equilibrium

with

referenceto

thedistribution

of

a given

amountof

energy amongagivennumberof

particles of aperfect gas.Letus

assume

Q:3;

N:4

andI

TABLE

III

Firm

size measured by amounts of outputt2

1l (a) (b) (c) (d)

2l (a)

(b)

(d) (c)3l

(a)

(c)

(d) (b)4l

(b)(c)

(d) (a)sl (a) (b) (c) (d) 6l (a) (b) (d) (c)

71(a)

(c) (b) (d)8l

(a)

(c) (d) (b) el(a)

(d) (b) (c)101

(a)

(d) (c)o)

l

ll

G)

(c) (a) (d)I2l

(b)

(c) (d) (a)131

(b)

(d) (a) (c)r4l

o)

(d) (c) (a)151

(c)

(d) (a) (b)161

(c)

(d) (b) (a)t7l

(a)(b)

(c)

(d)181

O)

(a) (c)

(d)lel

(c)(a)

(b)

(d)201

(d)(a)

(b)

(c)Let

us

adopt

the term

"macrostate"to

indicate

a

statistical

aggregateof

microstates (a distribution), obtained by assuming that the firms are not distinguishable

from

each other. The firms are not distinguished either because we are not interestedin

their identification

or

becausethey

cannotbe

distinguished.In

our

example three macrostates of the industry are feasible- three inactive

firms

and afirm of

size 3;J

[image:10.612.57.578.71.774.2]-

two

inactivefirms,

asize-l firm

andasize-2frmr;

- one inactive

firm

and threesize-l

firms.The

first

macrostateis

generatedby

thehrst four

microstates; the secondby

the next12 and the

third

by the last four.In the general case let us indicate

n:

(no,n1,/t2,....,ne)

a feasible macrostatein

which

nofirms

are size0, n, firms

are size|,....,no

firms

are size Q on the condition thatno+nt*nr*....nn=N

(l)

Let w(n) be the

number

of

feasible

microstates

with

distribution

n :

(no,nr rÍ12,....rflg).

Combinatorial analysis gives

rr(n)= . .t'.

,nolnrlnr!...nn1,

where by convention

0!:1.

(2)

A

macrostaten:

(n0,nr,fi2,....,flg)

is

feasibleif

it

satisfies, besides theequality

(l),

the conservation condition of the total quantity Q

Ùno

+ln,

+2n,

+'..+

Qro

=

Q

(3)The total number of feasible microstates is

z

=lw(n),

with

summation over all macrostut",whiclisatisfr

(1) and(3).We may have an idea of the order of change in

w(n)

in response to variationsin

n,

as the numberof firms

isslightly

larger than the number representedin

the table,if

we assume3

N:

20

andQ:20.

In this case, wewill

have for the macrostate made upof

8 inactivefirms, 6

size-l frrms, 4 size-2firms

and2

size-3 firms:201

w =

-

=2x108.

8t6l4t2l

By

contrast for the macrostate in which all the firms are of auniform

size equalto

I

wefind

201

w- '-1.

201

It

is clear how enormous the difference is between themultiplicity

of microstates in thefirst

case,

which

representsa

decreasingdistribution

comparedwith the

single10

microstate

with a

uniform distribution. So

far we

have

followed

combinatorialanalysis.

To move onto the

conceptof

statistical

equilibrium we

have

to

assume aprobability

distribution.

In

statistical physicswe find

morethan

one assumptionof

probability on this point.

In

the so-called Maxwell-Boltznann distribution

equalprobability is

athibuted to each microstate; different assumptionsof probability

can befound, however, at the basis of the Bose-Einstein and of the Fermi-Dirac distributions.a

V/e

will

adopt the Maxwell-Boltzmann hypothesisof

equiprobabilityinitially

as an apriori;

then wewill

obtain this uniform probability from other assumptions.In

the

example illustratedin

table

III,

each microstate hasprobability

1/20;whilst

the three macrostates have respectively probabilitiesl/5, 315,ll5.

The statisticalequilibrium

of

the industryis

the second macrostatewith

probability

3l5.In

this

casethe small number

of

microstates, usedfor

the purposeof

the exposition, doesnot

yetenable

us

to

attribute a useful theoretical roleto

this equilibrium

macrostate.In

fact statisticalequilibrium

needs asufficiently

large numberN

(atypical

case is thatof

the particlesof

gas consideredin

statistical physics).In

general,in

orderto

determine!,

thefollowing

maximum problem hasto

be solvedmaxr.r,(n)

=noftt*-"ne

nolnrlnrl...nnl

subject

to

no + ntt

n2r....nn

=

N

Ùno

+ln,

+2nr+...+Qnn

:

Q.By

adopting asimilar

demonstration to that givenin

statistical physicss, thefollowing

solution,

as

shown

in

Appendix

I,

can

be

obtainedby

an

approximation

in

thecontinuum and for

N

and Q large numbers.N!

e-pt

4 = ^i o

I

s =

o,1,...,e.

S

tv--F"

L/

s=0

(4)

with

p =

l^(I

+

where

ln

is the natural logarithm.;)

>0.

(s)

4 For a comparison of Maxwell-Boltanann's, Bose-Einstein's and Fermi-Dirac's so-called statistics, see

W. Feller (1970).

Hence

the

mostprobable

macrostaten

is

a

distribution

offirms

which

decreasesaccording to a geometric progression as the size increases; as

no nl

...,....nr_,

=

",

.

(6)nt

n2 neFrom (5) we obtain

eF

-r

Having reached

this

result, theinitial

assumption that Q, the quantity producedby

theindustry,

is a

quantity

in

non-statistical classical

equilibrium,

determinddon

the demand side, becomes important. SubstitutingQ:

D in

(7), we obtain:eF

-l

Equations

(6)

and

(8)

showthat

asthe

demandD

increases,

ceterisparibus,

the coeffrcientp

decreases and, therefore,the

dispersionof firms

among classesof

everincreasing size grows.

It

is worth noting

that theratio

DA.{,

demand per numberof

ftrms, plays

a

similar role

to

that

played

by

temperatureT

in

the

correspondingphysical problem determining the most probable

distribution

of

particlesor

harmonic oscillators among a certain amount of energy.Entroplt

We can interpret the

equilibrium

of the industryin

termsof

entropy.Let

p,

be theprobability

ofmicrostate

i;

and let us measure the improbabilifyof

microstatei

by

the logarithm

010

J-XI,---LrLp..

P,

tWe can then define entropy

S(n)

of ttre macrostate n the averageimprobability of

the microstates of whichit

is composed, where the weights are the probabilitiesp,:

O_

N

(8).

D

N

(7)

w(n)

S(n)

: -I

L

1,2

If

all

microstatesin

the macrostaten

haveprobability

p,

nis

the entropy

of

S(n)

=

!^*6)

and

the

entropy

of

a

most

probable

macrostate

n is S(n) = I*

w

(n).

Therefore

s

statistical equilibrium of

the industryis

a

macrostatethat

has maximum entropy; hence, under the assumption of equal probability, a macrostatewith

maximumh/(n)

number

of

possible realizations.As

N

increases,the

ratio

;

decreases,whilst

t)

lxù

rnl(n)----n-

tendsto

1, where mis

the total numberof

microstates. Then,for

N

large,Lnm

the

entropy

of

the

industry

in

its

most

probable

state

can

be

written

n

S(w(n)

) = lnn.

Since

the

improbability

of.

a

macrostate

n

is0m0n

LrL-

- Ln m-dn

w(n),

we

canalso

saythat

for

a

largeN

a

statisticalw(n)

equilibrium belongs to a set of macrostates

with

almost zeroimprobability,

in the sensethat

w(n)turns

out

incomparably greater

than

w(n)

associatedwith

any

othermacrostate n outside the equilibrium set.

This property means that a macroscopic regularity

(equilibrium)

existsin

termsof

firm

distribution.

Suchregularity

emergesin

real

time,

if

we

supposethat

the number ofpotential

firmsN

and the quantityin

demandD

are stationary.A

statisticalequilibrium

can therefore be consideredlike

the imageof

afilm,

which is

made upof

the same perceived scene repeated on a large numberof

frames, interspersed every sooften

with

picturesof

other scenes: when thefilm

is run

at asufficiently high

speed,the viewer

is

hardly

awareof

theseodd

scenesat

all, whilst

he perceivesthe

main. scene.Leaving

this

metaphorto

one side,

it

must

be

stressedthat the notion

of

statistical

equilibrium

which has

been formulated here, does

not

substitute

theclassical

equilibrium

of

the

industry,

but

it

does

presupposeit

and

standsas

a complementto it. In

fact the stationarityof

Q is not

a physical necessity(like

energy conservation), but rather a propertyof

classicalequilibrium

in

which

Qis

determinedby

theeffective

demand at thelong run

competitive prices.It

is

to

be noted that thestationarity of the most probable distribution of firms hides an incessant movement at a

microeconomic level:

if

it

were possible to observe the trajectory of eachfirm

(a not soimpossible task compared

with

the caseof

a trajectoryof

a particlein

physics) over asuffrciently long period, a

ftrm

would be

seento

move throughthe whole

rangeof

1

sizes and the industry would pass through

all

feasible microstates. Thiswould

be truein principle.

In

economics, asin

the physicsof

gas, the numberof

units involved hasto

belarge

for

this

conceptto

beof

usefor

the analysis. Thusin

the modelof

the industrythe number

of

firmsN

has to be large enough.It must be noted, incidentally, that thereare some

diffrculties

in

observingN,

in

sofar

as manypotentially active

firms

areinactive

in

equilibrium. Also

the quantity Q,which

is measuredby

integers, hadto

be assumedto

be largefor

the pu{poseof

the

solutiongiven

in

appendixI.

Clearly

theproblem of the numerosity

of

Q differs from the one concerningN,

asit

does not seem so harmful to assume a suffrcientdivisibility

of the product.3. The choice of the sample space and the assumofioh of eaual

probability

In all main formulations of the method

of

statistical equilibrium inphysics

(theMaxwell-Boltzrnann

distribution, the Bose-Einsteindistribution

and the Fermi-Diracdistribution),

a

setof

feasible microstates(the

sample space)is

definedat a

certainlevel

of

analysisand then

equalprobability

is

assignedto

these microstates. This analytical level is chosen on the basis of thelogic

of the problem,of

a separate theory orof

anintuition,

the usefulness of this choice being tested by its predictive capability.In

applying the statisticalequilibrium

approach,two

methodologicalpitfalls

should beavoided.

With

respect to the phenomenon under investigation: a) the assumed sample spacemight

lack

persistency andb)

the

assumed microstatesmight not

have equalprobability.

Let

us

examine

now

the

applications

of

the

statistical equilibrium

approach

to

the

exchange economy (section1)

andto

the

economyof the

industry(section

2)

atthelight

of the above criterion.In

the

applicationto

the

exchange economy,the

choiceof

the

sample space and the hypothesisof

equalprobability

must be assessed on the basisof

someimplicit

assumption

of

"rational" individual

behaviour.sIn

this

caseit

is

hardto

explainwhy

the

probability

of

a

Pareto-effrcient microstateis

and remainsnot

greaterthan

theL4

probability

of

anyinefficient

microstatewhich

werenot

Pareto-inferiorto

the

initial

state.

For

example,the

microstate describedin

the

first

row

of

Table

I

does notrepresent any Pareto-improvement,

but

it

has, nevertheless, been athibutedthe

sameprobability

as anyof

the other microstates (describedin

the other rows) that doin

factimply

an

improvement. We

observethat the latter

problem preventsthe

exchangestatistical

equilibrium from

strengtheningits

theoreticalrole

in

thefollowing

case,'inwhich

the

diffrculty

arisingfrom

the non-persistenceof

theinitial

endowments doesnot arise.

In

the pure exchange economy let us assume the goods to be labour services, insteadof

durable goods, and theinitial

endowments to be made uponly of

persistentlabour capacities

of

workers to provide those services.By

this hypothesis,if

we assignall

the

feasible microstates equalprobability,

it

is

possibleto

formulatea

statisticalequilibrium

for

the

exchangeof

labour servicesin

realtime,

insteadof

a temporary statisticalequilibrium.

In

spiteof

this,

therestill

remainthe

same objectionsto

thehypothesis

of

equalprobability:

asif

on eachtrial

the agents describedby

the modelwould

lookfor

each other and acceptwith

equal chance any transaction which does notentail

an inferior position

for

them,

comparedto

the

absenceof

exchange. Therationality

of these agents seem to be minimal.It

would be more reasonable to attributeequal

probability

to

those

microstateswhich

imply

Pareto-efficient allocations

of

labour-services and lower probabilitiesto

all

the other microstates?. Unfortunately no generalcriterion

seems to be available apriori for

assigning non-uniform probabilitieswithin

exogeneously given offer sets.Also in

the application to the economyof

the industry, illustratedin

section 2,the

appropriatnessof

the

choice

of

the

sainple spaceand

of

the

equalprobability

assumption can be questioned, albeit for different reasons. .

On the one

hand,

we observe that the choiceof

the sample space, madeof

all

possible microstates of the industry, belongs to

the

general model of placing randomlya

given

number

of

balls

(firms)

in a

given

number

of

cells

(firm

sizes);

then aggregation runs by treating the balls as indistinguishable, whereas the cells are kept asdistinct

entities.I

This

modelmight not

be appropriate,if

the distribution

of

manycustomers among

many

firms

is

an essential

elementin

the

enumerationof

the microstatesof

a production systemwith

exchange.

Supposefor

simplicity

thatin

themodel

describedby

TableIII

there are three customers and each customer demandsone

unit

of

outptut,

asif he

would

represent an economic "quantum".In this

case,7 Foley himself in his working paper (Foley, l99l) assumed as feasible only those microstates which

imply Pareto-superior and efficient allocations.

many microstates

listed

in

tableIII

must be re-interpretedas

composed events:for

instance

row

1would

stiill

describe

a simple eventwith

a single realization,in

which

firm

(d)

supplies one

unit

of

output

to

each customer, whereasthe other

firms

(a),(b),(c) are

inactive;

by

contrastrow

5

would

describe a composedevent

with

3rcalizations, as

firm

(c)

can supply oneunit

of

outputto

eachof

the three customersaltematively,

whereasfirm (d)

suppliesone

unit

to

eachof

the

two

residrlalcustomers

and

firms (a),

(b)

remain

inactive.

From

this

perspective,

many microstatesin

TableIII

should be conceived as macrostates that must be decomposedin

further

microstatesby

replacing

the occupancymodel

of

balls

and cellswith

amodel

that

counts

all

possible

ways

for

assigning

three

quanta, initially

distinguishable,

to

four

particles,

initially

distinguishableas

well.

Only at

thisextended

micro-level, the

equalprobability

assumption shouldbe applied

and thedefinition

of the macrostates should be chosen.On the

other

hand,

the

equal

probability

assumptionrefers

to

absoluteprobabilities.

It

remainsto

be proved that a stateof

uniform

absoluteprobability is

a steady state outcomeof

a stochastic process and that this outcome is independentfrom

the

initial

probability

vector.In

particular,in

the

industrymodel,

gradual structural changes could be more probable than major alterationsin

the sizeof

thefirms

duringthe

sameperiod

of

time.

Thus,

in

the

example describedin

Table

III, it

can

be supposed that,if

theinitial

microstate is the one describedin line

I

(with

flrms

a,b,c,inactive and

firm

d

of

size 3),it

can be more probable that microstate 5(with

firms

aand

b

still

inactive,

f,rrmc

af

size

I

andfirm

d

at

síze2)

will

be

realizedin

thefollowing trial

than microstate2 (firms

a,b,d inactive andfirm

cof

size 3). However,under certain assumptions, these unequal conditional probabilities are compatible

with

equal

absolute

probability

of

all

possible

microstates.

In

particular

it

can

beimmediately proveds, using the theory

of Markov

chains that,if

thetransition

matrix

is

given andit

is

adoublv

stochastic andprimitive,lo

thenall

microstates take equalprobabilities

atthe

limit

of

a

seriesof

repeatedtrials

andthis uniform probability

isindependent

of

the

initial

microstate(or,

more

generally,of

the

initial

probability

vector).

A

special caseof

doubly

stochastic transitionmatrix

arisesif

we

assume thatreversibility

existsin

theprobabilistic

sense between eachpair

of

microstatesof

thee See Feller (1970), chapter XV page 399; and Seneta (1973). 10

Let

pii

be the transition probability from microstate i to microstatei

in one trial and let"

= t;l1) the mxmL6

industry at each

trial;

that is theprobability

that the microstatei

occurs,following

therealizatíonof

the microstatej,

is the same as the probability thatj

occurs,following

therealization

of

i.

This

hypothesisis

representedby

a

mxm

symmetrical transition matrix.In

thenext

sectionit

will

be proved that equal probabilities can be deduced asa

limit

property under assumptions less restrictive than that of double stochasticity.4.

Equalprobabílity through

non-línearMarkov

chainswith

lagged variables.Let us introduce time

lags

andwrite

xr*l

= f(x,

,xr-,,....rxt-^)

for

t

= 0r1r2,....The

vector

x,

=

(r,r ,xp1...exs,)'

shows the absoluteprobability x,,

of microstatei

in

period

f

.

A

prime

indicates transposition.V/ith

no

fearof

confusion,we

alsowrite

î

=(ft,fz,...,fn)'

. Let

X,

=(x,-,

,xr-m+',...,Xr)'.

When

the

given

function/

is homogeneousof

degree onein

each vector variable and continuously differentiable,the above equation is now written as

Xr*r

=AX'

O)

where

A

is(ram)by

(nxm) and010000

001000

0001

A=

,,r^,

"tt-tl

:

:

.

fO,

A

typical

elementof

F(*)

1,--òl-.

"

úr-k,i

To apply the

Propositionin

AppendixII,

the assumptions we now make are:Ass

l. f

is non decreasing in each variable.Ass2.

f,

is homogeneous of degree one.F(t)

has at least onepositive

diagonal enfry. Ass 4. e =f(e,e,...,e),

where

e =(l

In,

I I n,...,11n).

Originally,

f

is defined on a subsetof

Bl.'

because

x, is a

vector

of

probability

distribution.To

satisfi

Assl,

f

isfirst

to be extendedto

thewhole

ni*'

in anatural

way. Ass 3 is

to

assure theprimitivity of

the process, i.e. thematrix

A;

while

Ass

4

requires

that

if

the

equal probabilities have been

observedin

theconsecutive

m

past periods,then

that

situation

be

continuedas

an equilibrium.

It

should be noted that this is more general than the assumption

of

double stochasticityin

the

linear case. More

importantly, the equaldistribution

of

the presentperiod is

notenough to enswe the equilibrium state to be repeated.

Now

we can apply the Propositionin

AppendixII,

and can assert that startingfrom any

Xo

in

B1*^,

the

process(p)

,

i.e. X,*,

=AX,,

yields

a

serieswhich

converges to a unique

X*.

By the special formof A,

we can deduceX*

:

(x*,x*,

...,x*).Finally

by Ass4,

x*:

e

if

eachx*

should be normalized so thatit

belongs to theunit

simplex.

With

time

lags being introduced, a more natural interpretationof

the model isnow possible. That is, a society has a chain

of

memory, and accumulate the experienceof

shift from

one microstateto

another, and thesepiled up

"experience"or

"memory"affect the transition probabilities most plausibly

in

non-lineat

way.

Besides,in

thelinear case, the speed

of

convergence is quick and at a geometric rate.Let

us hope this nice property continuesto

hold

alsoin

the non-linear case, and establishesthe

equalprobabilities

in

ablink

as Nature may wish. Nature somehow seems tolove

"equality"or at least equal opportunities for all.

Strong ergodicity in the case of nonlinear positive mappings has been extended

to

the

transformationson

Banach spaces (seeFujimoto

and Krause

(1994).

The arguments above can hence be carried overto the

spacesof

aninfinite

dimension.It

may

serve

also

to

give

a

lower-level

foundation

to

the

equal-shareprinciple in

thermodynamics and,

in

spirit, to that in quantum theory.5.

Fìnal

consideralionsThe

two

applications developedin

sectionsI

and2 have enabled us to point out certainlimitations

on the transfer of the statistical equilibrium method from physics to18

The basic

difficulty

for

that transfer liesin

the changeover from particlesin

physics tointelligent units

with

memory and leaming

skills. The

method

seemsto

be fully

successful only in those theoretical areas of economics where the microstates cannot be

ordered

in

termsof

preferencesor

profrtability

and furthermorethe

determinantsof

statisticalequilibrium

are relativelypersistent.

These requirements have provedto

beplausible

in

the applicationto

the economicsof

the industry, but they appeared ratherproblematical in the application to a pure exchange economy.

It

should be noticed that,in

the application to the economics of the industry,rationality

is not absent, becauseit

underlies

the given

demandD for

the product,that

canbe

interpreted asa

classicalequilibrium

quantity determined by a wider model of the economy.Although the arguments presented in these notes have shown some comparative advantage

of

the transferof

statisticalequilibrium

as a complementof

classical longperiod equilibrium,

againstthe

transfer

of

the

same conceptas

a

substitutefor

awalrasian

notion

of

equilibrium,

some basic questionsremain

unanswered herefor

further applications

of

the notion of statistical equilibriumwithin

the former approach.First,

are therereally

any important

areasof

indeterminacystill left

by

the classicalequilibrium

method apart from that of the constant returns industry examined here ? We believe thisto

be so, even under the assumptionof

free competition wherethere are

no

casesof

indeterminacy dueto

strategic interactions among agents. Oneimportant

case

of

indeterminacy

can

be

found

in

classical

theory

of

value

anddistribution

if

the

labourforce

is

supposedto

be homogeneous asfar

as productiveefficiency

is

concemed,but

to

have non-homogeneous tastes.Suppose

an economicsystem

with

single product industries, constant returns to scale, free competition and afixed

interestrate. In

this

case the non substitution theorem holds: the choiceof

thecost-minimising technique and the long period prices of the commodities are uniquely determined, but the amount and the composition of employment in terms

of individual

tastes cannot

be

determined

by

the

same economic criterion, even

if

somecorrespondences are supposed

to

exist among prices,incomes

and effective demand. Hence the composition of social product remains indeterminate aswell.

Secondly,

in

the caseof

the industry,it

was assumed that the classicalmethod

of

equilibrium

first

determines thetotal

output atthe long

period prices and then the methodof

statistical equilibrium step in tofrll

the gap of indeterminacyleft by

the

first

stageof

analysis.In

the

more general cases sucha

logical

sequencein

theapplication

of

two

equilibrium

methodsmight not work. This

could

happenin

theindustry

example,if

the demandD

would

be affectedin tum by

some characteristicvalue

of

the

most probable structureof

the industry

itself,

e.g.by

the

multiplier

BThirdly,

the

conceptsof

Pareto-effrcient and Pareto-superior statesof

the economy should be re-examined,if

we adopt the methodof

statistical equilibrium.In

particular

the notion

of

exoectedutility

seemsmore

suitable comparedto

thedeterministic one

adoptedin

section

I

in

orderto

characterize some propertiesof

Foley's model.It

is

left for

future research programmesto

explore thetwo routes

throughwhich

the

concept

of

statistical equilibrium can

be

exported

from

physics

to economics.On the

side

of

the

classical approach,it

is

left

to

study whether

thatconcept is capable of

filling

other gaps of indeterminacy and to ascertain to what extentthe logical

succession betweenthe

two

stagesof

analysis mentioned above can beusefully

maintained. On the sideof

the approach proposedby

Foley,it

is

left

a moreambitious task;

in

so far as that approach aimsto

replace other notionsof

equilibrium

l

Appendix

I

Solve

41w(n)

=-

l/!

to,t b-.,t

o

nolnrlnrl...nnl

subject

to

no + nrt

nrt....nn

=

N

(a)0no

+ln,

+2nr+...+Qn,

=Q

(b).For

n

large,

the following

approximation can

be

shown

to

hold using

Stirling's fomrula:{nrt

-

n.l,rnn-

n

where

h

t"the

natr.ral logarithm.We

will

freat

t4orflr.rfrrr....fre

as

continuous

variables

and apply

Lagrangemultiplier

method. We obtain the solution:e-p"

4 = t -g- ^ |

s = 0,1,---rQ-

(c)I

"-P'

s=0

where p is an undetermined coeffrcient.

Let us consider the geometric progression:

a

Z"-'"

=

I

+

x

*

x2+....+xa,

with

r

=

e-e.s0

o1

Hence,

as

Q

I

@r

Z"-u"

+ ;--.

Substituting thelimit

in

(c), we get:s=o

I-

X4 =

Ne-p'(l

-

"-0)

.

s:0,1...Q

(d)Substituting (d) in the constraint (b):

a

N(l-e").>se-e"=Q

(e)To solve (e)

with

respectto

B, we use the equation which holds at thelimit

$ ^-u'

1?u= 1-"

Differentiating

both sides of this equation, we get:a

e-9I

t"-u"

s=o

(l-

"*)'

By

substitutionof

(f) in

(e):o-F

*.---e

(g)l-e

From (g)

p

-hQ*{l

Q,

which make solution (c) determined.Appendix

II

Suppose there exist n microstates, and

letx

be an n-column vector whose Èthelement represents the

probability

of microstatei.

The symbolR"

denotes the Euclidean spaceof dimensionn,

Ri

the non negative ortantof R,,

ands'

=

{r

e

Rile''x

=

1}, where e is an n-column vector whose elements are all unity.In

-R", an order > is induced by the coneRi.

we

writex>y

whenx

>y

andx

+y.

and also writex

>>y

whenx

-y

is in the interiorof

,R "Now

a given continuous transformation/

mapsRí

i;;o

itself, and satisfies thefollowing

assumptions.Assumptionl:

f

is monotone,i.e.,

l@)>/(y)

whenx

>y.

Assumption2:

f

isweakly

homogeneous,i.e.,for

anyx

e

Ri,

î.eR*,

we havef(),x):

h(Ì,")f(x),where

:

h:R*

J

R*

is such that h(?,')/Ì,, is non increasing andft(0):0.

Assumption3:

f

isprimitive,

i.e., there exists a natural number m such thatforxy

eRi,

x>y

impliesf'

(x)

>>f'

(y).

Assumption 4:

'Whenx

e

S,then

/(x)e

S.a

l_ l_ l_

Using the theorem and

corollary

I

in Fujimoto and Krause (1985),it

is easy to show that Assumptionsl-4

are sufficient to have a unique strictly positivex*

e

S.Since

x*

is unique, this must coincidewith

elnbecatse of Assumption 5.Summaized

fts