USING ROLE-PLAYING EXERCISES TO PROMOTE SOFT SKILL

(PERVASIVE SKILL) DEVELOPMENT

Monique Keevy

Accountancy Department

University of Johannesburg

Johannesburg, South Africa

[email protected]

AbstractThe use of active teaching methods to develop pervasive skills has many advocates globally. As prior research provides evidence of the value of role-playing exercises in the development of pervasive skills, the objective of this article is to examine the extent to which South African (SA) accounting academics use role-playing exercises (an active teaching method) as a method of instruction, and to establish their views on whether this method can be used to develop pervasive skills. An electronically administered questionnaire was sent to SA accounting academics. The findings of this article reveal a gap in the use of role-playing exercises by SA accounting academics when compared to their counterparts globally. This gap can be attributed to the reluctance of academics to develop pervasive skills due to time constraints, an already loaded syllabus, and the perception that academics are not responsible for developing pervasive skills.

INTRODUCTION

The accounting profession and academics globally have acknowledged that role-play as a means of instruction, is a powerful approach when developing pervasive skills. However, the use of this particular method of instruction has not been adopted to the same extent in South Africa (SA) as it perhaps has in other countries. Possible reasons for this are that the academics rely on the South African Institute of Chartered Accountants (SAICA) to guide them on methods of instruction (Keevy 2016), and the academics' reluctance to embrace their academic freedom by engaging the accounting literature on suitable delivery methods (Samkin and Schneider 2014). Therefore, the objective of this article is to examine the use of role-playing exercises by accounting academics in SA, and to establish their views on whether this method can be used to transfer pervasive skills to students.

The direction of accounting education has received considerable debate for almost two decades. The debates stem back to the 1980s with the Bedford Committee Report (American Accounting

Association (AAA 1986), followed by the “Big Eight” White paper (AAA 1989), and ultimately resulting in the formation of the Accounting Education Change Commission (AECC) (AECC 1990). The role of the AECC was to promote changes in accounting teaching and learning practices with the intention of preparing graduates for the business environment (AECC 1990; Cotton, Rainsburg and Scott 2002). The business environment changed drastically due to globalization, business complexity, advances in

technology and proliferating regulations (Albrecht and Sack 2000; Shuayto 2001; International Federation of Accountants (IFAC) 2010). These overarching forces of change resulted in a need for accounting graduates to be proficient in not only technical competencies but also pervasive skills (Albrecht and Sack 2000; De Lange, Gut and Jackling 2006). As expressed by Raelin (2000, 10): “rather than learning job-specific skills, workers will be asked more and more to learn situation-job-specific principles attending to a given work domain. By mastering these principles, workers can be expected to handle ongoing variability in work demands”.

The growing body of accounting literature suggests that academics were not preparing graduates fully for the future profession (AAA 1986; Albrecht, Smith, Stocks and Woodfield 1994; Adler and Milne 1995; Adler

and Milne 1997; Anes, Hassall, Joyce and Arquero Montańo 2005; Cargill, Gammie and Hamilton 2010), given

that technical competencies were developed to the detriment of pervasive skills (Adler and Milne 1995; Adler and Milne 1997). Consequently, this necessitated a change, as academics could not “save accounting education by continuing to do more of the same” (Albrecht and Sack 2000, 3).

In light of this, the IFAC developed a set of education standards in 2003 encompassing both technical

and pervasive skills (IFAC 2014). As an IFAC member, SAICA introduced the Competency Framework in 2008

as part of its qualification model. Instead of simply focusing on the technical competencies typically taught in SA universities, this Competency Framework highlighted pervasive skills. Therefore, both technical and pervasive skills would form part of SAICA’s academic curriculum.

Authors have stressed that in order to address pervasive skills, academic programmes should supplement the traditional lecture-based classes with active learning practices (AAA 1986; AECC 1990; Adler and Milne 1997; DeNeve and Heppner 1997; Kern 1999; IFAC 2014). DeNeve and Heppner (1997, 232) posit that “effective teaching is fast becoming synonymous with the facilitation of active learning techniques”. According to Ryan and Martens (1989, 20 as quoted in Bonwell and Eison 1991), passive learning occurs when students are merely the

“receptacles of knowledge”. Role-playing exercises have been described as an active learning method (Janvrin 2003; IFAC 2014; Lazar 2014) which renders a meaningful improvement to students’ learning (Lazar 2014). By “seeing and doing”, students improve their understanding of technical matters (Kirstein and Plant 2011, 9). As conveyed by Petty (1994), “I am told, and I forget. I see, and I remember. I do, and I understand” (6).

The benefits of role-playing exercises have been widely documented in accounting literature. This article's contribution therefore is to provide insights into the use of an active learning method, such as role-playing exercises in SA, by academics whose traditional strengths are technical teaching. The reasons for the reluctance of SA academics to develop pervasive skills are also highlighted.

LITERATURE REVIEW Nature of role-playing exercises

McKeachie (1986, 174 in DeNeve and Heppner 1997) perceives role-play as the creation of an essentially unstructured situation where students are required to portray their conception of certain assigned roles. It requires improvisation (Kern 1999) and imagination, as the role-player is required to “step into the life of another without a script” (Lazar 2014, 236). In some instances, students can either create their own scenario or act out the scenario provided by the academic (Crumbley, Smith and Smith 1998). The role-players need to visualise that they are either themselves or in another person’s shoes in a specific situation (Lazar 2014). Role-playing scenarios attempt to create real-life situations that may or may not take place in reality (Babst, DeGarmo, Harth and Reinalda 2006; Baglione 2006). Otte and Truscheit (2004) advocate that role-playing exercises are equivalent to real world situations.

Role-playing exercises may involve only a few active participants, while the rest of the class observe the role-play and afterwards reflect on and discuss the scenario (Lightbody 1997; Mintz 2006; Rudman and Terblanche 2011). For example, in Amernic and Craig’s (1994) study, the entire class was briefed on the role-playing scenario and the characters. This was followed by a few students acting out the role-play while the rest of the class served as the audience. Bonwell and Eison (1991) advocate that the students who are not performing the role-play still benefit by providing a commentary on the exercise. Another form of role-play is when the lecturer debates against himself/herself in front of the class (Bonwell and Eison 1991). Kirstein and Plant (2011) used a role-playing exercise where the lecturer acted as narrator while the students had to take up different roles within the business process. Multiple role-plays can also take place within a classroom setting where various groups act out the role-play at the same time in the same room (Amernic and Craig 1994). For example, Christensen and Eining (1994) divided the class into groups of six. Each group member was assigned one of the roles within a case study and the individual groups were given time for discussion. When the class resumed, each group shared its perspective on the case study by the members taking on their different roles. Crum and Haskin (1985) are in favour of this type of role-playing exercise as opposed to having one set of players dominating the spotlight.

A benefit of role-playing is that no special equipment or material is required (Bonwell and Eison 1991). Kirstein and Plant (2011) merely used a lecture hall. This method also actively engages students in the learning process (Babst et al. 2006) by bringing “issues to life” (IFAC 2014, 122) and takes the knowledge learnt beyond the classroom setting (Babst et al. 2006). With this in mind, a role-playing exercise should involve preparation, enactment and reflection (Lazar 2014). For a role-play to be effective, Crum and Haskin (1985) suggest that there should only be two to three characters, and that the problem should have differences of opinion or values, be

non-theatrical and be based on learning objectives that highlight the problem-solving process. Moreover, the objectives of a role-playing exercise should be to create student interest in the subject matter and to apply technical content (DeNeve and Heppner 1997).

The literature criticized facilitators for not retaining control in the classroom (Amernic and Craig 1994; Babst et al. 2006; Rudman and Terblanche 2011), not having the requisite skills for this method (Amernic and Craig 1994; Rudman and Terblanche 2011), for lacking preparation (Lazar 2014), and for not allowing sufficient time to conduct the role-playing exercise (Rudman and Terblanche 2011). Furthermore, important technical knowledge may be excluded if the role-playing exercise is “too entertaining or frivolous” (Ments 1989, 27, as conveyed in Amernic and Craig 1994). However, most of these issues can be overcome by sending the facilitator for training (AECC 1998).

According to the literature, students may not cooperate or want to partake in the exercise (Lightbody 1997; Rudman and Terblanche 2011); resist being in an active learning environment (Bonwell and Eison 1991), which may not be supportive (Kirstein and Plant, 2011; Lazar 2014); and need to understand the theory before the role-playing exercise can resume (Rudman and Terblanche 2011). However, Amernic and Craig (1994) perceive that even though there are disadvantages to role-plays, the skills that are transferred to students far outweigh the negatives. Babst et al. (2006) concur, as they posited that role-playing results in deep learning and that students will remember the exercise long after the class has ended.

Role-playing exercises can take place in many forms and in combination with other methods. They can be incorporated with a case study (Berry 1993; Amernic and Craig 1994; Fatt, 1995; Boyce, Kelly, Williams and Yee 2001; Babst et al. 2006; Carrol 2007; Kirstein and Plant 2011; IFAC 2014); performed in a group (Scott 1972; Berry 1993; Lightbody 1997; Kern 1999; Mintz 2006; Carrol 2007; Paulson 2011; IFAC 2014; Lazar 2014); included in a lecture (DeNeve and Heppner 1997; Lightbody 1997; Grace 2006; IFAC 2014.) or presentation (Paulson 2011); and be used subsequently with self-assessment and reflection (Babst et al. 2006; Mintz 2006; Lazar 2014). However, regardless of how this method is employed, the literature provides a host of competencies that can be developed using role-playing exercises.

Summary of the pervasive skills that can be developed by employing role-playing exercises

This section provides a summary (Table 1) of the pervasive skills that were developed using role-playing exercises. To obtain the summary, a literature search was conducted to establish whether accounting professional bodies and academics use role-playing exercises to transfer pervasive skills to students. This assisted in answering the objective of the paper of whether there is a gap in the use of role-playing exercises by SA accounting academics compared to their global counterparts.

A literature search was used to identify and retrieve empirical studies that were relevant to whether role-playing exercises can be employed to develop pervasive skills. The search was limited to empirical studies written in English. To ensure coverage of empirical studies on the topic, the literature search included peer-reviewed journal articles, conference papers, masters’ theses and doctoral dissertations. The keywords and descriptors used in the search included accounting, accounting teaching, assessment, learning, playing exercises and role-playing learning. Based on the literature search, the pervasive skills that could be developed using role-role-playing exercises were linked to the literature search sources.

SAICA’s Competency Framework recognises pervasive skills as being part of three categories, namely ethical behaviour and professionalism (IA), personal attributes (IB), and professional skills (IC). These categories are further subdivided into eight (IA), ten (IB) and seven (IC) competencies (SAICA, 2009). The table below details the pervasive skills that could be developed using role-playing exercises in these three categories. Table 1 Summary of the pervasive skills that could be developed using role-playing exercises

(IA) ETHICAL BEHAVIOUR AND PROFESSIONALISM (IA) 1. Protects the public interest

Amernic and Craig 1994; Christensen and Eining 1994; Fatt 1995; Crumbley et al. 1998; Molyneaux 2004; IFAC 2006; Mintz 2006; Carrol 2007; Beard, Schweiger and Surendran 2008; Wu and Yang 2009; Rudman and Terblanche 2011; IFAC 2014.

(IA) 2 Acts competently with honesty and integrity

Amernic and Craig 1994; Fatt 1995; Crumbley et al. 1998; Molyneaux 2004; IFAC 2006; Mintz 2006; Carrol 2007; Beard et al. 2008; Wu and Yang 2009; Paulson 2011; Rudman and Terblanche 2011; IFAC 2014.

(IA) 3. Carries out work with a desire to exercise due care

Amernic and Craig 1994; Fatt 1995; Crumbley et al. 1998; Molyneaux 2004; IFAC 2006; Mintz 2006; Carrol 2007; Beard et al. 2008; Wu and Yang 2009; Paulson 2011; Rudman and Terblanche 2011; IFAC 2014.

(IA) 4. Maintains objectivity and independence

Amernic and Craig 1994; Christensen and Eining 1994; Fatt 1995; Crumbley et al. 1998; Molyneaux 2004; IFAC 2006; Mintz 2006; Carrol 2007; Beard et al. 2008; Wu and Yang 2009; Paulson 2011; Rudman and Terblanche 2011; IFAC 2014.

(IA) 5. Avoids conflict of interest

Amernic and Craig 1994; Fatt 1995; Crumbley et al. 1998; Molyneaux 2004; IFAC 2006; Mintz 2006; Carrol 2007; IFAC 2006; Beard et al. 2008; Wu and Yang 2009; Rudman and Terblanche 2011; IFAC 2014.

(IA) 6 Protects the confidentiality of information

Amernic and Craig 1994; Fatt 1995; Crumbley et al. 1998; Molyneaux 2004; IFAC 2006; Mintz 2006; Carrol 2007; Beard et al. 2008; Wu and Yang 2009; Rudman and Terblanche 2011; IFAC 2014. (IA) 7. Maintains and enhances the profession’s reputation

Amernic and Craig 1994; Fatt 1995; Crumbley et al. 1998; Molyneaux 2004; IFAC 2006; Mintz 2006; Carrol 2007; Beard et al. 2008; Wu and Yang 2009; Rudman and Terblanche 2011; IFAC 2014. (IA) 8. Adheres to the rules of professional conduct.

Amernic and Craig 1994; Fatt 1995; Crumbley et al. 1998; Molyneaux 2004; IFAC 2006; Mintz 2006; Carrol 2007; Beard et al. 2008; Wu and Yang 2009; Rudman and Terblanche 2011; IFAC 2014. (IB) PERSONAL ATTRIBUTES

(IB) 1. Self-manages

(IB) 2. Demonstrates leadership and initiative

Bonwell and Eison 1991; DeNeve and Heppner 1997; IFAC 2006; Paulson 2011; Lazar 2014. (IB) 3. Maintains and demonstrates competence and recognises limits

Amernic and Craig 1994; Paulson 2011; IFAC 2014. (IB) 4. Strives to add value in an innovative manner

Lightbody 1997; Janvrin 2003; Babst et al. 2006; Paulson 2011. (IB) 5. Manages change

Janvrin 2003; Rudman and Terblanche 2011. (IB) 6. Treats others in a professional manner

Bonwell and Eison 1991; Berry 1993; Amernic and Craig 1994; DeNeve and Heppner 1997; Crumbley et al. 1998; IFAC 2006; Mintz 2006; Carrol 2007; Paulson 2011; IFAC 2014.

(IB) 7. Understands the national and international environment

Crum and Haskin 1985; Amernic and Craig 1994; Fatt 1995; DeNeve and Heppner 1997; Lightbody 1997; Crumbley et al. 1998; Boyce et al. 2001; Babst et al. 2006; Baglione 2006; Kirstein and Plant 2011; Paulson 2011; IFAC 2014.

(IB) 8. Is a life-long learner

Scott 1972; AAA 1986; SAICA 2015. (IB) 9. Works effectively as a team member

Bonwell and Eison 1991; Berry 1993; Amernic and Craig 1994; DeNeve and Heppner 1997; Lightbody 1997; Crumbley et al. 1998; Baglione 2006; IFAC 2006; Carrol 2007; Paulson 2011; Rudman and Terblanche 2011; Lazar 2014; Gordan and Thomas 2016.

(IB) 10. Manages time effectively

Rudman and Terblanche 2011; IFAC 2014. (IC) PROFESSIONAL SKILLS

(IC) 1. Obtains information

Janvrin 2003; Babst et al. 2006; Paulson 2011; Gordan and Thomas 2016. (IC) 2. Examines and interprets information and ideas critically

Crum and Haskin 1985; Bonwell and Eison 1991; Amernic and Craig 1994; Berry 1993; Lightbody 1997; Babst et al. 2006; Mintz 2006; Carrol 2007; De Villiers 2010; Kirstein and Plant 2011; Paulson 2011; Rudman and Terblanche 2011; Gordan and Thomas 2016.

(IC) 3. Solves problems and makes decisions

Crum and Haskin 1985; Amernic and Craig 1994; DeNeve and Heppner 1997; Lightbody 1997; Crumbley et al. 1998; Kern 1999; Janvrin 2003; IFAC 2006; Mintz 2006; Carrol 2007; Paulson 2011.

(IC) 4. Communicates effectively and efficiently

Scott 1972; AAA 1986; Berry 1993; Amernic and Craig 1994; Crumbley et al. 1998; Janvrin 2003; Babst et al. 2006; IFAC 2006; Carrol 2007; Paulson 2011; Gordan and Thomas 2016.

(IC) 5. Manages and supervises

IFAC 2006; Carrol 2007; Paulson 2011; IFAC 2014.

Janvrin 2003; Rudman and Terblanche 2011; Gordan and Thomas 2016. (IC) 7. Considers basic legal concepts

Scott 1972; Christensen and Eining 1994; DeNeve and Heppner 1997; Rudman and Terblanche 2011; IFAC 2014.

The above summary provides evidence that all 25 (eight IA, ten IB and seven IC) of SAICA’s pervasive skills can be developed using role-playing exercises, as each competency is linked to one or more source. Therefore, this study provides one active method that can be used by academics to enhance the development of pervasive skills in their accounting pedagogy.

RESEARCH METHOD

To achieve the objective of this study, a structured web-based questionnaire was used as the research instrument to ascertain whether academics use role-playing exercises and whether this method can be used to develop pervasive skills. The questionnaire was administered to all SA accounting academics who provide instruction to aspirant chartered accountants (CAs) (SAICA 2012).

The questionnaire consisted of two sections of mostly closed-ended questions of a quantitative nature. Comments boxes comprising the qualitative aspect of the questionnaire were included at the end of each section, allowing for descriptive responses to enrich and expand the research results.

The questionnaires were pilot tested by a selected group of academics. A data controller was used to set up an online website where the questionnaire could be answered and the data recorded. The questionnaire, containing a dedicated uniform reference, was sent via email to the participants. The participants were directed to a website and asked to complete the questionnaire by clicking on the uniform reference. The completed questionnaires were electronically collated by the data controller. Means, medians, standard deviations, minimums and maximums were calculated.

Population and response rate

The population for the empirical work consisted of all SA accounting academics providing instruction to

aspirant CAs (SAICA 2012). In total, 443 emails were dispatched to the academics and 147 responses were received. It must be noted that none of the questions in the questionnaire were compulsory and the participants could refrain from answering a particular section, or questions in a section. This explains why the participants did not necessarily answer all of the questions. For section one, the effective response rate was 33% (147/443) and for section two, 32% (142/443).

EMPIRICAL FINDINGS

Academics’ views on the use of role-playing exercises during their academic programmes

In the first section, the academics were asked to indicate whether they use role-playing exercises in their academic programmes. The data analysis of this question is set out in Table 2 below and is based on the use of

role-playing exercises subsequent to the SAICA releasing its Competency Framework. This is indicated by the

percentage was calculated using the applied column, which represents the percentage of academics who indicated that they use this method.

Table 2 Academics’ views on their use of role-playing exercises for development after SAICA introduced the Competency Framework

Applied % n

The use of role-playing exercises for purposes of development 19 12.9 147

Key: Applied = number of academics who use play exercises, % = percentage of academics who use role-playing exercises, n = number of respondents who answered the question.

A mere 12.9% of respondents employ role-playing exercises in their academic programmes. However as far back as 1986, the AAA (1986) highlighted role-play as a suitable method to transfer pervasive skills. Furthermore, in 2000, Albrecht and Sacks (2000) asked academics what learning activities they view as effective. At that time, 15.3% of the academics were employing role-playing exercises in their academic programmes and 34.1% of the academics considered role-playing exercises as an effective teaching method. The summary (Table 1) provides evidence from various academics and professional bodies of the competencies that can be transferred when employing role-playing exercises. Therefore, it would be expected that more SA accounting academics would use role-playing exercises in their academic programmes.

One respondent was of the opinion that the syllabus for technical aspects was already burdensome and left little time for pervasive skills development:

The syllabi for technical competencies are too full to also have time to develop pervasive skills. Another respondent remarked that pervasive skills are difficult to address at university:

Apart from written communication, I don't see how the pervasive skills can realistically be developed and assessed at university.

However, Els (2007) and the IFAC (2014) noted that technical competencies and pervasive skills are complementary. Furthermore, several academics have succeeded in developing pervasive skills using technically orientated role-playing exercises. For example, Boyce et al. (2001) allowed students to adopt different roles such as chief executive officer, financial controller, board member and employee. Equally, Christensen and Eining (1994) used a role-playing exercise to address legal issues, which created ethical awareness among students, and Carrol (2007) used a transfer pricing role-playing scenario. Consequently, academics should integrate pervasive skills with their teaching of technical content.

A respondent commented that academics are not responsible for addressing pervasive skills:

Our job is to teach the technical stuff. The pervasive skills can only be observed indirectly when assessing the work of the student, but it is very difficult to teach it in large groups.

This view was shared by another respondent, who remarked:

Pervasive skills should predominantly be acquired during the training contract, not at university. Firms are devolving their training costs to universities where it does not belong.

While the findings of Strauss-Keevy (2014) agree with the aforesaid observation, the accounting profession generally disagrees with this view. As Otte and Truscheit (2004) and others have noted, role-playing

exercises are equivalent to real world situations. Therefore, academics should develop role-playing exercises that stimulate the business environment.

Academics’ views on the use of role-playing exercises to transfer categories IA, IB and IC of the pervasive skills

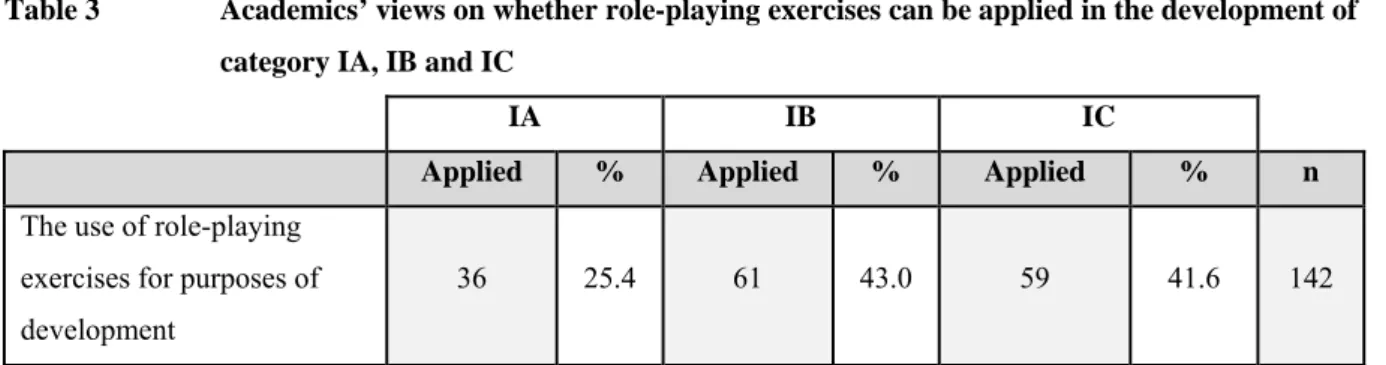

In the second section, the views of academics were sought on whether role-playing exercises can be applied in the transfer of categories IA, IB and IC. The data analysis of this question is set out in Table 3 below, and is based on whether academics hold that role-playing exercises can be applied in the development of the three categories of pervasive skills. A percentage has been calculated based on the applied column, representing the percentage of academics who indicated that this method can be applied in the transfer of each category.

Table 3 Academics’ views on whether role-playing exercises can be applied in the development of category IA, IB and IC

IA IB IC

Applied % Applied % Applied % n

The use of role-playing exercises for purposes of development

36 25.4 61 43.0 59 41.6 142

Key: Applied = number of academics who indicated that role-playing exercises can be applied; % = percentage of academics who indicated that role-playing exercises can be applied; n = number of respondents who answered the question

More respondents’ view that role-playing exercises can be employed when transferring pervasive skills (Table 3) than respondents who actually use this method (Table 2). Bonwell and Eison (1991) reveal that academics do not change their teaching practices as “things are the way they are today because that is the way they have always been” (54). Therefore, the results suggest the possibility of role-playing exercises being employed further by academics in their teaching practices.

In addition, respondents’ indicated that role-play exercises can be applied more effectively when addressing category IB and IC compared to category IA. Bearing in mind that the IA category includes skills such as honesty, integrity, due care and objectivity, one respondent remarked that the attributes relevant to category IA are difficult to address:

I do not believe that ethical behaviour and professionalism to be attributes or skills that could be taught or developed at this late stage of a persons’ life.

Another respondent supported this view by stating:

True ethics can never be examined. The only way someone will determine whether or not he/she is ethical is when they are faced with an ethical dilemma. Students know what the right answer is but that does not necessarily mean that they will make the right decision in practise.

Nevertheless, several academics have succeeded in delivering IA competencies through role-playing exercises (Janvrin 2003; Mintz 2006; Kirstein and Plant 2011; Rudman and Terblanche 2011). Therefore, academics should engage the accounting literature on creative ways in addressing the pervasive skills.

CONCLUSIONS, RECOMMENDATIONS AND AREAS FOR FUTURE RESEARCH

Academics need to move from lecture-based education pedagogy to more active learning methods. The article set out to examine the use of role-playing exercises – an active learning method – by SA accounting academics, and to establish their views on whether this method can be used to transfer pervasive skills to students. The results indicated that very few SA accounting academics use role-playing exercises in their academic programmes. . However, more hold the view that it can be used to develop pervasive skills. Therefore, the results suggest the possibility of role-playing exercises being employed further by academics in their teaching practices.

Certain academics remarked that they do not know how to develop pervasive skills. For example, one academic remarked:

Apart from written communication, I don’t know how pervasive skills can be realistically developed and assessed at university.

Time constraints and a full syllabus were reported as the reasons for not developing pervasive skills. However, the accounting literature has emphasized that technical competencies and pervasive skills are complementary. Therefore, academics should integrate pervasive skills while using a technically orientated role-playing exercise. Certain academics also expressed that they are not responsible for the development of pervasive skills, and that the training programmes should be tasked with the implementation of these abilities. However, this is in conflict with the accounting literature, where both the academic and training programmes play a part in the transfer of pervasive skills.

Therefore, it is suggested that academics from different SA universities collaborate to develop specific role-plays that simulate the business environment. Academics were also asked whether role-playing exercises could be applied in the development of the three categories of pervasive skills. Academics expressed difficulty in the development of attributes relevant to ethical behaviour and professionalism, such as honesty, integrity, due care and objectivity. This was encapsulated in the following comment: True ethics can never be examined. The only way someone will determine whether or not he/she is ethical is when they are faced with an ethical dilemma. Students know what the right answer is but that does not necessarily mean that they will make the right decision in practise.

However, as far back as 1986 (AAA 1986), it was suggested that role-playing exercises are a powerful approach in developing pervasive skills. Therefore, despite the reluctance of certain academics to use this method, it is suggested that they engage the accounting literature on how this method can be effectively utilised when addressing pervasive skills. A limitation of the study was that academics were merely asked whether role-playing exercises could be used to develop the different categories of pervasive skills.

Consequently, further research is required to ascertain why academics view that role-playing exercises are more suitable in transferring the personal attributes category consisting of skills such as leadership, life-long learning, managing change, and the professional skills category consisting of skills such as communication, problem solving and critical thinking. This study is useful from a SA context, given the adoption of the Competency Framework. However, as SAICA’s competencies are aligned to other professional bodies, this study can also inform academics from other countries who similarly have a technical focus, on the pervasive skills that can be developed using role-playing exercises.

REFERENCES

Accounting Education Change Commission (AECC). (1990). Position Statement Number One: Objectives of

education for accountants. Retrieved from: https://aaahq.org/AECC/pdf/position/pos1.pdf (accessed on 19 October 2011).

Accounting Education Change Commission (AECC). (1998). The accounting education change commission

grant experience: A summary. Retrieved from: https://aaahq.org/AECC/changegrant/cover.htm (accessed on 19 October 2011).

Adler, R.W. and Milne, M.J. (1995). Increasing learner-control and reflection: towards learning-to-learn in an

undergraduate management accounting course. Accounting Education, 4(2), 105–119.

Adler, R.W. and Milne, M.J. (1997). Improving the quality of accounting students’ learning through action-orientated learning tasks. Accounting Education, 6(3), 191–215.

Albrecht, W.S., Clark, D.C., Smith, J.M., Stocks, K.D. and Woodfield, L.W. (1994). An accounting curriculum for the next century. Issues in Accounting Education, 9(2), 401–425.

Albrecht, W. and Sack, R. (2000). Accounting education: Charting the course through a perilous future. Accounting Education Series, American Accounting Association, Sarasota, FL.

American Accounting Association (AAA). (1986). The Bedford Report, Future accounting education:

Preparing for the expanding profession. Retrieved from: https://aaahq.org/AECC/future/index.htm (accessed on 31 May 2013).

American Accounting Association (AAA). (1989). Perspectives on Education: Capabilities for success in the

accounting profession. Retrieved from: https://aaahq.org/AECC/big8/cover.htm (accessed: 31 May 2013).

Anes, J.A.D., Hassall, T., Joyce, J. and Arquero Montańo, J.L. (2005). Priorities for the development of

vocational skills in management accountants: A European perspective. Accounting Forum, 29, 379–

394.

Amernic, J. and Craig, R. (1994). Roleplaying in a conflict resolution setting: Descriptive and some implications for accounting. Issues in Accounting Education, 9(1), 28–43.

Babst, G., DeGarmo, D., Harth, C. and Reinalda, B. (2006). 2006 APSA teaching and learning conference track

summaries. Retrieved from:

http://www.jstor.org/discover/10.2307/20451795?sid=21105332407261&uid=3739368&uid=2129&ui d=2&uid=4&uid=70 (accessed on 7 January 2015).

Baglione, S.L. (2006). Role-playing a public relations crisis: Preparing business students for career challenges. Journal of Promotion Management, 12(3/4), 47–61.

Beard, D., Schweiger, D. and Surendran, K. (2008). Integrating soft skills assessment through University,

College, and Programmatic Efforts at an AACSB Accredited Institution. Journal of Information

Systems Education, 19(2), 229–240.

Berry, A. (1993). Encouraging group skills in accountancy students: an innovative approach. Accounting Education, 2(3),169–179.

Bonwell, C.C., and Eison, J.A. (1991). Active learning: Creating excitement in the classroom. Washington, DC: George Washington University.

Boyce, G., Kelly, A., Williams, S., and Yee, H. (2001). Fostering deep and elaborative learning and generic (soft) skill development: the strategic use of case studies in accounting education. Accounting Education, 10(1), 37–60.

Cargill, E., Gammie, E. and Hamilton, S. (2010). Searching for good practice in the development and assessment of non-technical skills in accountancy trainees - a global study. Aberdeen, Scotland: The Robert Gordon University.

Carrol. A. (2007). Team assessment task for Management Accounting: A divisional management case study approach. E-Journal of Business Education and Scholarship of Teaching, 1(1), 70–78.

Christensen, A. and Eining, M.M. (1994). Instructional case: Software Piracy – who does it impact? Issues in Accounting Education, 9(1), 151–159.

Cotton, W.D.J., Rainsburg E and Scott, G. (2002). Competency based professional accounting certification in

New Zealand. Paper presented at the American Accounting Association Conference, Ohio, email to:

[email protected], from: [email protected] (dated 29 November 2011).

Crum, R.P. Haskin, M.E. (1985). Cost allocations: a classroom role-play in managerial behaviour and accounting choices. Issues in Accounting Education, 109–130.

Crumbley, D. L., Smith, K.T. and Smith, L.M. (1998). Educational novels and student role-playing: a teaching note. Accounting Education, 7(2), 183-191.

De Lange, P., Gut, A. and Jackling, B. (2006). Accounting graduates’ perceptions of skills emphasis in undergraduate courses: an investigation from two Victorian universities. Accounting and Finance, 46, 365–386.

DeNeve, K.M. Heppner, M.J. (1997). Role play simulations: The assessment of active learning technique and comparisons with traditional lectures. Innovative Higher Education, 21(3), 231–246.

De Villiers, R. (2010). The incorporation of soft skills into accounting curricula: preparing accounting graduates for unpredictable futures. Meditari Accountancy Research, 18(2), 1–22.

Els, G. (2007). Utilising continued professional development of ethics amongst prospective chartered accountants. Doctoral Thesis. University of Johannesburg.

Fatt, J.P.T. (1995). Ethics and the accountant. Journal of Business Ethics, 14(2), 997–1004.

Gordan, S. and Thomas, I. (2016). The learning sticks’: reflections on a case study of role-playing for sustainability. Environmental Education Research, 2016, 1–19.

Grace, E. (2006). Instructional resources for teaching social influence in accounting courses. Social Influence, 1(3), 234–246.

International Federation of Accountants (IFAC). (2006). Approaches to the development and maintenance of professional values, ethics and attitudes in accounting education programmes. Retrieved from:

http://www.accountingweb-cgi.com/whitepapers/approaches_to.pdf (accessed on 29 September 2011). International Federation of Accountants (IFAC). (2010). International Education Information Paper –

Development and Management of Final Written Examinations. Retrieved from:

http://web.ifac.org/publications/international-accounting-education-standards-board/adoption-implementation-r. (accessed on 22 February 2011).

International Federation of Accountants (IFAC). (2014). Handbook of International Education Pronouncements. Retrieved from: http://www.ifac.org/sites/default/files/publications/files/Handbook-of-International-Education-Pronouncements-2014.pdf (accessed on 20 November 2014).

Janvrin, D.J. (2003). St Patrick Company: Using role play to examine internal control and fraud detection concepts. Journal of Information Systems, 17(2), 17–39.

Keevy, M. (2016). Using case studies to transfer soft skills (also known as pervasive skills): Empirical evidence. Meditari Accountancy Research, 24(3), 458–474.

Kern, B.B. (1999). Using role play simulation and hand-on models to enhance students’ learning fundamental accounting concepts. Retrieved from:

http://www.google.co.za/url?sa=t&rct=j&q=&esrc=s&source=web&cd=2&ved=0CCEQFjAB&url=htt p%3A%2F%2Fjosotl.indiana.edu%2Farticle%2Fdownload%2F1581%2F1580&ei=xEEBVZbPBoS9U cdv&usg=AFQjCNGEVFR-qsrksd_tTgF2D2ZgbSUUxg&bvm=bv.87920726,d.d24 (accessed on 20 November 2014).

Kirstein, M. and Plant, K. (2011). Action research in audit education: South African teachers’ perspectives. Paper presented at the Southern African Accounting Association, Fancourt, South Africa, 26–29 June 2011.

Lazar, A. (2014). Setting the stage: Role-playing in the group work classroom. Social work with groups, 37, 230–242.

Lightbody, M. (1997). Playing factory: active-based learning in cost and management accounting. Accounting Education, 6(3), 255–262.

Mintz, S.M. (2006). Accounting ethics education: Integrating reflective learning and virtue ethics. Journal of Accounting Education, 24, 97–117.

Molyneaux, D. (2004). After Andersen: An experience of integrating ethics into undergraduate accountancy education. Journal of Business Ethics, 54, 385–398.

Otte, C. and Truscheit, A. (2004). Sustainable games people play: Teaching sustainability skills with the aid of

role-play ‘NordWest Power’. Greener Management International, 48, 51–56.

Paulson, E. (2011). Group communication and critical thinking competence development using a reality-based project. Business Communications Quarterly, 74(4), 399–411.

Petty, G. (1994). Teaching today: A practical guide. United Kingdom: Redwood Books.

Raelin, J.A. (2000). Work-based learning. The New Frontier Management Development. Upper Saddle, New

Jersey: Prentice Hall.

Rudman, R.J. and Terblanche, J. 2011. Practical role-play as an extension to theoretical audit education: a conceptualising aid. Southern African Journal of Accountability and Auditing Research, 11, 63–74. Samkin, G. and Schneider, A. 2014. Using university websites to profile accounting academics and their

research output: A three country study. Meditari Accountancy Research, 22(1), 77–106.

Scott, R.A 1972. The study of partnership accounting through role playing. The Accounting Review, July 1972. Shuayto. N. 2001. A study evaluating the critical managerial skills corporations and business schools desire of

South African Institute of Chartered Accountants (SAICA). 2009. Competency Framework. Competencies of a Chartered Accountant (SA) at entry point to the profession. Retrieved from:

http://saica.co.za/Portals/0/Documents/CompetencyframeworkCAs.pdf (accessed on 8 March 2010). South African Institute of Chartered Accountants (SAICA). 2012. List of SAICA accredited programmes 2012”.

Retrieved from: https://www.saica.co.za/Portals/0/LearnersStudents/documents/List%20of%20 accredited%20programmes%202012.pdf (accessed on 30 March 2012).

South African Institute of Chartered Accountants (SAICA). 2015. Accreditation criteria: Application for new and continued accreditation. email to: [email protected], from: [email protected], (dated 29 January 2015).

Strauss-Keevy, M. 2014. Education programmes’ responsibilities regarding pervasive skills. Journal of Economic and Financial Sciences, 7(2), 415–432.

Wu, W. and Yang, H. 2009. The effect of moral intensity on ethical decision making in accounting. Journal of Moral Education, 38(3), 335–351.

Appendix

List of abbreviations and acronyms

AAA American Accounting Association AECC American Education Change Commission

CA Chartered Accountant

IA Category of pervasive skills: ethical behaviour and professionalism

IB Category of pervasive skills: personal attributes

IC Category of pervasive skills: professional skills

IFAC International Federation of Accountants

SA South Africa