Radial Basis Function Networks

Gyusik Han, Daewon Lee, and Jaewook Lee Department of Industrial and Management Engineering

Pohang University of Science and Technology Pohang, Kyungbuk 790-784, Korea {swallow,woosuhan,jaewookl}@postech.ac.kr

Abstract. Nonparametric approaches of estimating the yield curve have been widely used as alternative approaches that supplement parametric approaches. In this paper, we propose a novel yield curve estimating algorithm based on radial basis function networks, which is a nonpara-metric approach. The proposed method is devised to improve accuracy and smoothness of the fitted curve. Numerical experiments are conducted for 57 U.S. Treasury securities with different maturities and demonstrate a significant performance improvement to reduce test error compared to other existing algorithms.

1

Introduction

Along with stocks and loans, bonds are the main asset class with which the gov-ernment or a private enterprise can raise money. The term structure of interest rates plays a key role in the reasonable bond-pricing. Because it is based on an interest rate model, the model need be calibrated before using it. The fundamen-tal object to calibrate against is the yield curve of bonds. The fitting techniques of yield curves to yield data or maturity data are divided into two categories, parametric approaches and nonparametric approaches. A popular parametric ap-proach is a family of Nelson-Siegel curves [2]. Despite its simple structure, many parametric approach, however, revealed poor performance in yield curve fitting. As alternative approaches, nonparametric approaches have recently been widely used. Especially, cubic B-splines, which are the kernel functions for estimating a bond yield, are popularly chosen among various nonparametric approaches [3], [5], [13], [14].

In this paper, we propose a novel fitting method for the yield curve. The proposed method comprises two phases. The first phase finds an initial yield curve using a radial basis function network (RBFN) whose inputs are maturities of bonds and outputs are their yields. In the second phase, the initial yield curve predicted by the RBFN in the first phase is calibrated to minimize bond-pricing error. The performance of the proposed algorithm is verified concerned with improving the curve-fitting accuracy and regularization by applying it to notes and bonds issued by U.S. Treasury Department.

J. Wang, X. Liao, and Z. Yi (Eds.): ISNN 2005, LNCS 3497, pp. 885–890, 2005. c

2

Existing Yield Curve Fitting Algorithms

To verify the merits of our proposed nonparametric and computational method for fitting the yield curve, the performance of this method needs to be measured against widely used alternative models. In this paper, a smoothed spline model is used for this purpose. It assumes that the forward rate curve, δ, is a linear combination of basis functions. Cubic B-splines, a linear nonparametric interpo-lation method, are considered as basis. Let{Pi}1≤i≤N be theith bond price at

settlement date. δis chosen to minimize the following objective function

N

i=1

{Pi−Pˆi(δ)}2+θ

τK

0

[δ(t)]2dt (1)

over the space of all cubic B-splines with knot points(time) τ0< τ0<· · ·< τK.

ˆ

Pi(δ) is theith theoretical bond price from the estimated yield curve [14]. Another approach to be considered is Nelson and Siegel curves [1], [2]. The forward rate curve modeled by Nelson and Siegel is

δ(τ) =β0+ (β1+β2τ)e−kτ (2)

whereβ0, β1, β2, andkare parameters to be estimated in the following way:

(β∗0, β∗1, β2∗, k∗) = arg min (β0, β1, β2, k)

Υ |Υ =

N

i=1

[Pi−Pˆi(δ)]2

3

The Proposed Method

3.1 Phase I: RBFN-Based Initial Curve-Fitting Phase

In the first phase, we train a RBFN to estimate the spot rate curve with a given bond information on prices and maturities. A (generalized) radial ba-sis function network (RBFN) involves searching for a suboptimal solution in a lower-dimensional space that approximates the interpolation solution where the approximated solutionF∗(w) can be expressed as follows:

F∗(w;τi,T,L) = l

j=1

wjΦj(τi)

=

l

j=1

wjφ(τi−tj

λj ) (3)

been fixed, the network weights will be directly estimated by using the least squares algorithm.

To apply RBFNs to estimate the spot rate, we first calculate the spot rate (ri) with respect to maturity (τi) on the basis of bootstrapping through bond

information. Then an initial yield curve is fitted as minimizing the criterion function

J(w) =1 2

N

i=1

ri−F∗(w;τi,T,L)2. (4)

The network weights can be directly estimated by using the pseudo-inverse, w= (ΦTΦ+λΦ0)−1ΦTR (5)

whereRis the vector of the spot rates obtained from the bootstrapping method, Φ= [φ(τi, tj)]i=1,...,N, j=1,...,K,Φ0= [φ(τi, tj)]i,j=1,...,K andλis a regularization

parameter of the generalized RBFN [9].

The estimated spot rates, obtained from the trained RBFN, can be used to predict bond prices. Because the ultimate aim of the yield curve fitting is to construct a bond pricing model, in the second phase, we have to additionally optimize the weights of the trained RBFN to minimize bond pricing error.

3.2 Phase II: Trust Region-Based Optimal Yield Curve Search The second phase solves an unconstrained nonlinear programming to minimize the bond pricing error as follows:

min

w E(w;R,T,L) = N

i=1

Pi(r(τ))−Pˆi(F∗(τ;w,T,L))

2

(6)

where Pi is the ith bond price for the true spot rater(τ) at time τ and ˆPi is

the ith bond price for the spot rateF∗(w) obtained from the initially trained RBFN in the first phase. To minimize Eq. (6) the second phase employs a trust region algorithm as follows. For a given weight vectorw(n), the quadratic ap-proximation ˆE is defined by the first two terms of the Taylor approximation to E atw(n);

ˆ

E(s) =E(w(n)) +g(n)Ts+1 2s

TH(n)s (7)

whereg(n) is the local gradient vector andH(n) is the local Hessian matrix. A trial steps(n) is then computed by minimizing (or approximately minimizing) the trust region subproblem stated by

min

s Eˆ(s) subject to s2≤∆n (8)

where∆n>0 is a trust-region parameter. According to the agreement between

predicted and actual reduction in the functionE as measured by the ratio

ρn=E(w(nˆ))−E(w(n) +s(n))

∆n is adjusted between iterations as follows:

∆n+1=

s(n)2/4 ifρn<0.25

2∆n ifρn>0.75 and∆n =s(n)2

∆n otherwise

(10)

The decision to accept the step is then given by

w(n+ 1) =

w(n) +s(n) ifρn≥0

w(n) otherwise (11)

which means that the current weight vector is updated to be w(n) +s(n) if E(w(n) +s(n)) < E(w(n)); Otherwise, it remains unchanged and the trust region parameter ∆n is shrunk and the trial step computation is repeated [8], [10], [11].

The proposed method has several advantages. At first, since RBFN has a universal property of approximating an arbitrary curve, it can provide a good fitting for the true yield curve. In addition, the use of a trust region-based search procedure makes much better estimation for the curve fitted by RBFN.

4

Experimental Results

In this section, we verify how well the proposed method works compared with three existing fitting algorithms of the yield curve which include

– Cubic B-splines (Fisher’s method; FM): [14] – Nelson-Siegel curve (NS): [1], [2]

– MLP method (MM) : [4], [6], [8], [9]

The data used in the empirical analysis are 57 U.S. Treasury securities settled on November 3, 1997. U.S Treasury securities are semiannual-coupon bonds issued in order for U.S. Treasury Department to finance government borrowing needs at the lowest cost over time. The 57 securities have two quoted prices, bid price quotes and asked price quotes. We regard bid price quotes as real clean prices of the securities and use them in the empirical analysis. We used the spot rates bootstrapped from 50 of the 57 securities for training models, and the remaining 7 bonds for testing them. The kernel function for the proposed method is the Gaussian kernel function. The MLP method employed a multilayer-perceptron network instead of RBFN in Phase I.

0 5 10 15 20 25 30 0.05

0.052 0.054 0.056 0.058 0.06 0.062 0.064 0.066 0.068

Time(τ): year

yield(r)

FM’s curve Bootstrapped spot rate

MM’s curve

Proposed NS curve

Fig. 1.Comparison of results for the fitting of the yield curve

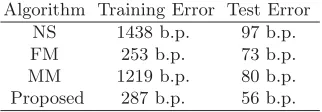

Table 1. Simulation Result using four yield-curve fitting techniques. (b.p.(basis point)=0.01%)

Algorithm Training Error Test Error NS 1438 b.p. 97 b.p. FM 253 b.p. 73 b.p. MM 1219 b.p. 80 b.p. Proposed 287 b.p. 56 b.p.

5

Conclusion

Acknowledgement

This work was supported by the Korea Research Foundation under grant number KRF-2004-041-D00785.

References

1. James, J., Webber, N.: Interest Rate Modeling. John Wiley & Sons Ltd, London (2000)

2. Nelson, C.R., Siegel, A.F.: Parsimonious Modeling of Yield Curves. The Journal of Business,60(1987) 473-489

3. de Boor, C.: A Practical Guide to Splines. Springer-Verlag, Berlin Heidelberg New York (1978)

4. Lee, D.-W., Choi, H.-J., Lee J.: A Regularized Line Search Tunneling for Efficient Neural Network Learning. Lecture Notes in Computer Science, Springer-Verlag, Berlin Heidelberg New York3173(2004) 239-243

5. Dierckx, P.: Curve and Surface with Splines. Oxford Science Publications, New York (1995)

6. Choi, H.-J., Lee, H.-S., Han, G.-S., Lee, J.: Efficient Option Pricing via a Globally Regularized Neural Network. Lecture Notes in Computer Science, Springer-Verlag, Berlin Heidelberg New York3174(2004) 988-993

7. Hastie, T., Tibshirani, R., Friedman, J.: The Elements of Statistcal Learning: Data Mining, Inference, and Prediction. Springer-Verlag, Berlin Heidelberg New York (2001)

8. Lee, J.: Attractor-Based Trust-Region Algorithm for Efficient Training of Multi-layer Perceptrons. Electronics Letters, 39(2003) 71-72

9. Haykin, S.: Neural Networks: A Comprehensive Foundation. Prentice-Hall, New York (1999)

10. Lee, J., Chiang, H.-D.: A Dynamical Trajectory-Based Methodology for Systemat-ically Computing Multiple Optimal Solutions of General Nonlinear Programming Problems. IEEE Transactions on Automatic Control,49(2004) 888-899

11. Nocedal, J., Wright, S.J.: Numerical Optimization. Springer-Verlag, Berlin Heidel-berg New York (1999)

12. Bliss, R.R.: Testing Term Structure Estimation Methods. Advances in Futures and Options Research,9(1997) 197-231

13. McCulloch, J.H.: The Tax Adjusted Yield Curve. Journal of Finance, 30 (1975) 811-830