Analysis of the Applicability of Micro-Economic Variables on

Stock Market Performance

I

Emmanuel Benson,

IIUzoamaka Gloria Chris-Ejiogu,

IIISimon Terdue Utsev

I,IIIDept. of Accounting and Finance, University of Agriculture, Makurdi Benue State, Nigeria

IIDept.of Financial Management and Tech., Federal University of Tech. Owerri, Imo State, Nigeria

I. Introduction

Stock markets have been at the center of economies for centuries. Any instabilities or crises occurring in these markets have partial or general effects on the economy. Since the 17th century, the world

economy experienced many crises that arose from financial and more specifically, stock exchange markets [1]. Thus, economy

administration of countries and policymakers carefully observe the progress of stock markets so as to take precautions in case of

unexpected instabilities. Daily fluctuations of the stock markets

might stem from economic and political affairs. However, stock markets are not independent of domestic and global microeconomic conditions. Investors are directly or indirectly affected by the changes in microeconomic factors and make their decisions on

shares by considering the overall situation of the market. Therefore, it examines the determinants of stock market fluctuations matters for economies and investors [2].

Many developing economies have attempted to develop capital markets, not only to raise capital rather capital markets are expected to meet two basic requirements: it should support industrialization through savings mobilization, investment funds allocation and maturity transformation. Besides, it must

be safe and efficient in discharging the aforesaid function. In

emerging economies like Nigeria, stock markets are expected

to function like a barometer of the financial performance of the organizations, efficiency of the financial markets and an icon of

the development of economic activity. But such conditions do not usually exist due to prevalence of informal credit markets

that tend to limit the capacity to mobilize financial savings, a

low degree of ownership-management separation associated with the drawbacks of informational asymmetry and low level of

accumulated of financial assets making maturity transformations difficult. Of course, these conditions differ widely from country

to country [3].

Investors invest in financial securities for competitive and

satisfactory returns. They generally consider the ex-post and ex-ante returns of the securities while making and investment decision. This is because the investment in financial assets is always associated

with different types of risks which are expected to be driven partly by company oriented factors, partly by industry factors, partly by

market oriented factors and partly by macroeconomic factors. A clear knowledge about the volatility and sensitivity of each and every factor with respect to behavior of the stock prices help an investor to enjoy a competitive advantage over those who do not have such knowledge in the process of generating satisfactory

return from investment in financial assets. That’s why researchers

and academicians from all over the world have given their effort

to identify those real factors that significantly contributes to the volatility of stock prices. They developed and explained different

theories and models to identify the factors truly responsible to the

volatility of stock prices. Their results also differ with respect to

developed economy and those of emerging economy.

Some characteristics in developed countries have shown a

strong ability in forecasting stock returns. “Reference [4] shows

the degree of explanatory power of variable(s) on stock market

returns might depend on the country and period of study”. The

impact of macroeconomic variables on the stock market has been empirically proven for the developed countries. Nonetheless, the

empirical findings for the case of developing economies are still

a puzzle. Hence changes in the share prices are affected by the changes in microeconomic performance in the well-developed markets, but results are inconclusive for the emerging markets

[5]. Emerging markets, as mentioned by [6], have, on average,

higher stock return than developed countries, which consist of the

European Union, Japan, and the United States. Based on another study conducted by [7], there is rapid growth and low correlations between emerging markets in the South-East Asian regions, which

offers lower portfolio risk and higher return for international

investors. These make their stock markets interesting for both

domestic and international investors seeking new opportunities to diversify their portfolio. Moreover, another study conducted by

[8] stated that investors have paid more attention to ASEAN-5, especially Malaysia and Singapore, in the last three decades. These

and many more other studies has proven that Nigeria is a virgin area for this kind of research, that is why this study is carried out

to explore the applicability of Micro-Economic Variables on Stock

Market Performance in Nigeria.

The broad objective of the study is to analyse how the applicability

of micro-economic variables affect stock market performance in Abstract

This study investigates the analysis of micro-economics variables on the stock market with specific reference to deposit money

banks in Nigeria. The study adopts the ex-post facto research design in the investigation. Data used for the study was sourced from

the annual financial statements of selected deposit money banks listed on the Nigeria stock exchange from 2012-2017. Descriptive

statistics and multiple regression technique were used in the analysis of data. Findings from the study revealed that micro-economics

variables proxied by Debt-To-Equity and Dividend Per Share significantly affect sock performance surrogated by share price of listed deposit money banks in Nigeria while Quick ratio does not significantly affect share price of listed deposit money banks in Nigeria.

The study therefore recommends the urgent need to control the operations of stock brokers and agents of NSE in order to safeguard the public investments in the stock market. This shall ensure that what has been happening lately after collapsing of various stock brokers is not repeated in the future.

Keywords

Nigeria. Specifically, the paper seeks to investigate how; d

ebt-To-Equity Ratio affect share price of listed deposit money banks

in Nigeria, dividend Per Share affect share price of listed deposit money banks in Nigeria and quick ratio affect share price of listed deposit money banks in Nigeria.

The research questions to be tackled in the study are what effect does Debt-To-Equity Ratio have on share price of listed deposit

money banks in Nigeria?What effect does Dividend Per Share has on share price of listed deposit money banks in Nigeria?And what effect does Quick ratio has on share price of listed deposit money banks in Nigeria?

The hypotheses of the study are debt-To-Equity Ratio does not significantly affect share price of listed deposit money banks in Nigeria. Dividend Per Share does not significantly affect share

price of listed deposit money banks in Nigeria. Quick ratio does

not significantly affect share price of listed deposit money banks

in Nigeria.

II. Literature Review

The Concepts of Stock Market and Microeconomic Variables

The researches show that stock market is treated as a part of

securities market where the stock trade is organized and performed.

The main purpose of stock market indices is to ensure for investors

possibility to estimate not only the state of separate stocks but the state of the entire market, sector or region. Stock market indices are analyzed according to such criteria as capitalization and geographical spread. It is found that stock market indices

estimated in the countries of the world reflect general fluctuations of the market of those companies’ stocks which are quoted in the country, and in order to find fluctuations in separate regions or

all over the world international and world stock market indices

are selected. On the other hand, microeconomic indicators are

treated as statistical indicators which are used for assessment of

individual state of the country’s economy during a certain period of time [9] or as regularly published governmental statistics which reflects the economic situation in the specified country [10]. Microeconomic indicators may be classified by their connection with the country’s individual business cycle, the rate of declaration

in different statistical editions, the character of economic process

what facilitates initiative identification of certain economic

processes.

Research on microeconomic variables and their effect on stock return in developed countries have been adequately documented. However, the impact of microeconomic variables on stock return in developing countries including Nigeria is comparatively limited and show contradicting results.

Debt-To-Equity Ratio: Based on the signaling theory, investors

view debt as a signal of firm value and firms with high anticipated profits will take on high level of debt. Moreover, Modigliani and Miller’s tradeoff theory of leverage suggests that stock price increases with leverage. The pecking order theory, however,

which has been empirically observed to be the most used in

determining companies’ capital structure, suggests that profitable firms use less debt. Prior research on these theories has reached contradictory results. Titman and [11], [12], [13] and [14] found that the most profitable firms more likely borrow less. These results are consistent with the pecking-order theory. However, [15], [16], [17], [18], [19] and [20] supported the trade-off theory and found

a positive relationship between debt-to-equity ratio and stock

returns. These contradictory results could be because of different

economic conditions (according to Modigliani and Miller`s capital structure theory) or maybe due to the period or scope of study

or lack of mediating or moderating variables. Therefore,

debt-to-equity ratio is selected as one of the microeconomic variables in this study.

Dividend Per Share: The dividend irrelevance theory by

Modigliani and Miller essentially indicates that an issuance of dividends should have little to no effect on stock return. However, bird-in-hand theory which was developed by Myron Gordon

and John Lintner contradicts the Modigliani and Miller dividend

irrelevance theory. Bird-in-hand theory indicates that investors care whether their returns are from dividends or capital gains. Based on the bird-in-hand theory, shares with high dividend payouts have higher demand by investors and consequently command

a higher market price. “Reference [21] found that dividend per share negatively influence stock return”. Conversely, [22], [23], and [24], found a direct relationship between dividend per share and stock return. Therefore, in order to help resolving the existing contradictory findings, this study examines the impact of dividend

per share on stock return.

Quick ratio (QR): It has been selected in this study as an indicator

of a company’s short-term liquidity. Liquidity of company describes the company’s ability to meet its short-term liabilities. In

the current unstable economy in Nigeria, the ability of companies

to pay their debt is among the highest concerns of investors. The

analysis of short-term liquidity is often important as it gives

confidence to investors about a company`s ability of short-term success in paying debts [25].

Investors’ Perception: It is a well known fact that the investor

(individual or corporate body) is the supplier of funds in the

market. This is achieved by purchasing of fresh securities in the

primary market, making funds available to the issuer in the process or buying of existing securities (shares, bonds) from the secondary market to enable those who want to convert their investments to

cash do so. In essence, investors’ participation in the market is very important, without them there is no market. The investor

is in the market for the returns he or she expects to make on his investment. It follows that investors do sometimes forfeit present consumption if they perceive that their utility would be maximized

in the future. Such perception may be influenced or determined by the investors’ adviser who is usually a stocker. It is the integrated decisions of investors which should ultimately influence the prices

of securities.

From the other two theories other factors that influence an investor’s demand for stocks include: Time, Price of stocks, Accessibility to stock brokers, Ease of liquidating stocks, Investment Returns, Company Profitability and Availability of funds. These factors

contribute to economic indicators thus determining the level

of economic growth in an economy. Economic Indicators are important signals of the state of the nation’s economy and these influence investors’ confidence in the economy and its stock

market. Such indicators include:

Investment Returns: This factor is however dependent on

profitability as there is no company that can pay good investment

returns in terms of dividends and or bonus issues to its shareholders

without a solid profitability report. The profits declared by listed

companies are of great importance when it comes to choosing which stocks to buy. Investors are attracted to companies which

declare high profits since it gives an assurance of high returns on

Expected rates of return: The return on an asset measures how

much we gain from holding that asset. It should be no surprise that

the rate of return which savers expect to earn on assets influences

their willingness to buy assets.

Time: this is the most important factor in determining the amount

of stocks that one can buy. It is the time factor that dictates

whether floated stocks can be afforded or not. Therefore, no retail

investor can ignore the role that time plays in the demand of his/ her stocks.

Speculation: The volatility in the stock market creates price

instability, which in turn encourages speculation on the stock price movements. Share prices in the secondary market change

continuously. The changes could be as a result of government policies and or companies’ corporate actions as well their financial

positions. It is however up to the investor to critically assess the many variables that are likely to impact on the fortunes of the company in whose shares he is to invest. By whatever method he chooses to do this and whatever skill he decides to apply (personal or professional), it is certain the investor through the interplay of demand and supply including other highlighted factors determine the movement of share prices on the secondary market. However, it is indeed advisable to seek professional advice before investing.

Wealth: This the total value of assets. The current value of

wealth affects people’s willingness to buy certain assets for their

portfolio.

Accessibility of an asset: The proximity of an asset affects how

many people shall be interested in investing in it. If stocks and securities are made available to the retail investors it is likely that more investors shall show up Information on the market: It is of paramount importance that investors be informed about the stock market. An informed investor invests out of wisdom and not out of euphoria.

Investor Education - Investing in the Stock Market NSE should

increasingly play an educational role and embark on a vigorous campaign to market itself and educate potential investors about the opportunities available in the market and how to effectively

exploit them. The efforts by NSE to improve public awareness of

the opportunities available in the capital markets in Nigeria need to be strengthened by using a variety of means of communication such as media campaigns through the radio, television and

newspapers, engaging in one-on-one meetings with eligible firms and potential investors, and distribution of literature to firms and potential investors across the country [26]. Investor education

is an important supervisory tool to promote investor protection.

To this end the NSE identified public and investor education as

a key driver of its market growth agenda. But while Authority will always endeavour, as part of its mandate, to provide as much protection to investors as the law permits it, it also believes that the best protection is, and will always be an informed and knowledgeable investor. An educated investor is a protected investor, and a protected investor is a more willing player in the market. All too often, investors chase rumours resulting in losses through poor risk management and following of the guide.

Therefore, investors should continuously take interest in their

investments and seek all the information they need to know about a target company to enable them to act as effective watchdogs

over their investments. They should know their rights, ask the right questions of their financial advisers, and know where to check to verify and clarify their doubts. The Authority has set

out elaborate rules that specify minimum disclosure requirements

for issuers of securities and listed companies in order to elicit full and accurate disclosure of material information that will

enable investors make informed decisions [27]. Many factors,

some of which are perceptual and subjective in nature, combine to determine the quality of a stock.

Management: Is the company a solid and reputable firm and does

it have able, efficient and seasoned management? A company

with well-established and organised management team is likely

to produce good financial results which would attract investors.

Products: Is the company producing goods and services for

which there will be a continuing demand for the foreseeable

future? Market share: Is the company operating in a field that

is dangerously overcrowded, and is it in a strong competitive position?

Earnings: Does the company have a satisfactory earnings record,

and have reasonable dividends been paid regularly to shareholders? What are its future prospects? Asset base: Are the net assets per share reasonable relative to the market price of the share?

Liquidity: It measures the ease of converting an asset into funds

that can be used to pay for goods and services or debt. Holding

liquid assets is beneficial when investors might need to pay for

goods and services or debt quickly. Are the shares issued available

in sufficient numbers and dispersion to enable the script to be

bought and sold at any given time?

Corporate governance: How strong is the company in terms of

corporate governances corecard? Investors have widely divergent

investment tastes and some are more risk averse than others. This is likely to reflect in the choice of securities in which they invest.

Some Investors will be more concerned about capital preservation and growth while others are more attracted by liberal and generous

dividend payouts. The type of investor you are will be a rough guide to the type of securities you should buy into. [28]. “Reference [29] shows that microeconomic factors affecting the average returns of stocks traded in Stock Exchange Istanbul (BIST) were analyzed by panel ARDL method”. For this purpose, 25 microeconomic variables owned by 130 companies which operate

in the manufacturing sector and being processed continuous trade

on stock exchange in the 2000:Q1 – 2017:Q3 period and 4 dummy variables belonging to Turkey’s economy were used and there were established 23different econometric models to investigate

the relationships between these variables. In this study, of time

series analysis methods [30], [31] and [32] Panel unit root tests and Panel ARDL methods were used with [33] multiple structural

fractured unit root tests.

As a result of the analyzes made, it was found that the rise in stock

turnover rate and net profit to total assets ratio affected positively

share earnings both in the short term and in the long term and it was seen that the effect in the short term was higher.

It was designated that total sales increased share earnings of growth of increase rate and increases in the growth of total assets in the long term. It was determined that increases of on current ratio, on the ratio of equity capital ratio to tangible assets, on the ratio of own capital to assets, on accounts receivables turnover

rate, net profits, on the ratio of equity, the marketing values of

companies, on the ratio of book value increased share earnings in a short term and increases of on the ratio of debt to tangible assets and asset turnover decreased share earnings in a short term

significantly.

[34] examines the relationship between the stock market and

microeconomic policy variables in South African for the period

restricted VAR model were employed to analyse the relationship between the variables of interest. The chosen method explicitly

calculates the disturbances by inverting an estimated structural

VAR of the relationship among the contemporaneous VAR residuals. The findings from the study suggest that there exists

a long-term relationship between the selected macroeconomic variables and the stock market in South Africa.

The results show that changes in money supply, interest rate,

inflation, exchange rate and government expenditure are

transmitted into the stock market. Thus achieving macroeconomic

equilibrium is of great importance as any disequilibrium will be fed into the stock market which eventually might compromise its

role of mobilising and allocating development financial resources

to productive sectors of the economy.

[35] empirically investigate the effect of microeconomic variables

on stock return with moderating role of money supply (MS).

The selected microeconomic variables in this study are debt-to-equity ratio (DE), dividend per share (DPS), and quick ratio (QR).

Firm size and book-to-market value are considered as controlling variables.

The period of the study is from 2003 to 2012 and the sample population of this study is 300 companies listed on Kuala Lumpur Stock Exchange (KLSE). Secondary data were collected from Data Stream International, financial annual reports, and the World Bank databank. Generalized least squares (GLS) technique was used

to estimate the predictive regressions in form of multiple models

of panel data sets. According to the findings, MS moderates the impact of DE and QR on stock return, but does not moderate the

effect of DPS on stock return. Besides, MS moderates the impact of all selected predictors on stock return.

The findings of this study further show that an increase in value of a firm’s debt relative to its equity would cause a decrease in the firm’s stock return. The results also indicate that firms with higher QR and DPS are likely to have a higher stock return. Overall, the findings of this research are consistent with Modigliani and Miller’s capital structure theory, as well as Pecking Order and Bird In Hand theory. The findings of this study would be of interest

to domestic and international investors, stockbrokers, board of

directors, financial managers, and policy makers.

[36] aim to analyze the micro-economic factors that affect

performance of the cement sector focusing particularly on

Pakistani firms. The study further finds the impact of size on

performance, to examine the relationship between age of the

firm and firm performance, to measure the effect of growth on firm’s performance and to highlight the impact of leverage on performance of the firm. There are twenty six cement companies listed in KSE. However, for the purpose of this paper only twenty

companies were selected whose data was readily available over

the period of eleven years from 2002 to 2012.

Methodology: The data for the study was extracted from the annual

reports of all the companies. In this study panel data analysis is used. Findings: After analyzing the data we have come to a point that all

of the four variables have significant impact on the performance of the firm. We have seen that leverage has a positive impact effect on the performance of the firm when ROA is analyzed. Size, age and growth have a positive impact on return on equity(ROE) while

leverage has a negative impact. Recommendations: This paper

shows new insights for policymakers to improve the performance

of Pakistani firms.

[37] examines the long-run equilibrium relationship and the

direction of causality between stock prices at Dhaka Stock

Exchange (DSE) and a set of four stock market oriented factors technically can be defined as microeconomic variables. Through utilizing the methods of Unit–Root tests, [38] Cointegration test and the long–run Granger Causality test proposed by [39], we have

investigated the long-run equilibrium relationship as well as causal

relationships between the DSE all share price index (DSI) and the

four microeconomic variables (i.e. market dividend yield, market price-earnings multiples, monthly average market capitalization and monthly average trading volume) using monthly data from

the period January 2000 to December 2010. Significant findings

include long-run equilibrium relationship among the variables under study.

However, DSI, in any way, do not granger cause dividend yield; but

DSI has bi-directional causal relation with market price earnings

multiples and the first lag of the monthly average trading volume. On the other hand, unidirectional causality is found from DSI to the first lag of monthly average market capitalization but no

causality is found from the opposite direction.

III. Research Methodology

The study seeks to examine the analysis of the applicability of micro-economic variables on stock market performance. This study is based on the expost facto research design. 14 deposit

money banks were selected whose data was readily available over

the period of six years from 2012 to 2017. The data for the study

was extracted from the annual reports of all the companies.

The data is secondary in nature. In this study panel data is used.

Number of researchers claim that panel data can control individual heterogeneity, can give more volatility, more information, more degree of freedom, less co linearity and more informative data. Panel data is better able to identify and measure effect that are not detectable in pure time series or in pure cross section data. It helps us to construct and test more complicated behavioral modes than pure time series or cross section.

Multiple regression is used when we have more than one variables.

Technique of data used in this study is ordinary least square (OLS)

multiple regression for checking how the applicability of micro-economic variables affect stock market performance. OLS is used for estimating the unknown parameters. This method minimizes

the sum of squared vertical distances between the observed responses in the dataset and the responses predicted by the linear approximation.

Model Specification

SP = a0 + a1DTE + a2DPS + a3QR (1)

Where: a0 = Constant

a1 - a3 = Regression coefficient of DTE, DPS and QR

u = Error term

SP = Share Price

DTE = Debt to Equity Ratio

Q = Quick Ratio

IV. Result and Discussion of Findings

Model Validity Check

In an attempt to ensure that the results of this study are robust and valid for interpretation, several diagnostic tests such as

Test for Autocorrelation

The Durbin Watson statistics is used to test for the presence of autocorrelation among the variables in this study. The Durbin Watson statistics for the model is estimated at 0.846. This figure is less than 2 (see table 3). This indicates that the assumption of independent error is not tenable for this study since this figure is far less than 2. This also shows that the model is not suffering from

incidence of autocorrelation and as such, there is no possibility of spurious regression [40].

Test for Multicolinearity

Table 1: Correlations Matrix

ROE FL FS FG

Pearson

Correlation

SP 1.000 .504 .213 -.245 DTE .504 1.000 .791 -.229

DPS .213 .791 1.000 -.223

QR -.245 -.229 -.223 1.000

Sig. (1-tailed)

SP . .000 .038 .021

DTE .000 . .000 .028

DPS .038 .000 . .032

QR .021 .028 .032 .

N

SP 70 70 70 70

DTE 70 70 70 70

DPS 70 70 70 70

QR 70 70 70 70

Source: Researchers Computation via SPSS version 20

Table 1 of correlation matrix above shows the absence of multicollinearity among the explanatory variables. These types

of checks are imperative because high correlation cause problems about the relative contribution of each predictor to the success of the model [41]. From the table 4.1, all the correlation values in

respect to the study variables are less than 0.8 which is considered

harmful for the purpose of analysis [42].

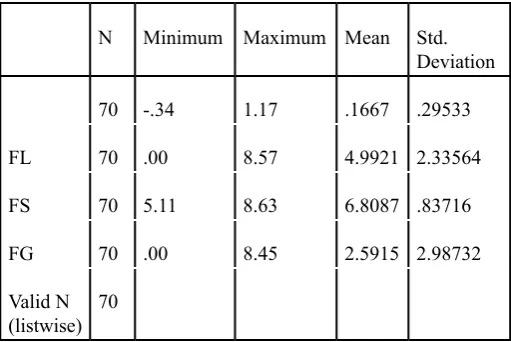

Table 2: Descriptive Statistics for All Variables

N Minimum Maximum Mean Std. Deviation

70 -.34 1.17 .1667 .29533 FL 70 .00 8.57 4.9921 2.33564

FS 70 5.11 8.63 6.8087 .83716

FG 70 .00 8.45 2.5915 2.98732 Valid N

(listwise) 70

Source: Researchers Computation via SPSS version 20

Table 4.1 presents the descriptive statistics of all the variables.

N represents the number of paired observations and therefore

the number of paired observation for the study is 70. The stock market is proxied by Share Price (SP) reflects a low mean of 16.67 with fluctuations of just 0.29533. This means that on average, Nigerian deposit banks has SP of 16.67 during the period under investigation. This reveals poor performance of the sampled

industrial goods companies.

The Debt to Equity Ratio (DTE)at the end of the year has an average of 4.9921 with a fluctuation of 2.33564. The result also reveals that dividend per share (DPS) is estimated 6.8087 with a

low 0.83716). This indicates that the sampled DMBs were more liquid enough to meet their current obligations effectively with

high rate of returns. Finally the mean of Quick Ratio (QR) reflects a mean of2.5915 with a deviation of 971.22.

Table 3: Model Summaryb

Model R R Square Adjusted R

Square Std. Error of the

Estimate

Change Statistics Durbin-Watson R Square

Change F Change df1 df2 Sig. F Change

1 .608a .370 .342 .23964 .370 12.933 3 66 .000 .846

a. Predictors: (Constant), DTE, DPSQR b. Dependent Variable: SP

Source: Researchers Computation via SPSS version 20

Table 4.3 presents the results of the model summary. The predictor variables (DTE, DPS and QR) were regressed with SP. The interpretations are presented in the subsequent paragraphs. The R value of 0.608 indicates that there is a strong association between determinants of profitability surrogates (DTE, DPS and QR) and firms’ SP.

The R2 is estimated at 0.342. The R2 shows the percentage of the

total variation of the dependent variable: SP that can be explained

by the independent variables DTE, DPS and QR. Thus the R2 value

of 0.342 indicates that DTE, DPS and QR account for only 34.2%

of the total variation in the SP of Deposit Money Banks in Nigeria,

while remaining 65.8% of the variation could be explained by

other variables not included in this model.

The F-statistics otherwise known as the Fisher’s statistics for the models are also estimated at 12.933 respectively. This indicates

that the set of independent variables were as a whole were contributing to the variation in the dependent variables and that

there exist a statistically significant relationship at 0.000 between SP and the set of predictor variables (DTE, DPS and QR). This further implies that the overall equation is significant at 0.000% which is below 5% level of significant for a two tail test. The adjusted R2 is estimated at .342 or 34.2%. This shows that if

the entire population is considered for this study, this result will

Table 4.4 shows the contributions of each of the variables in determining the SP of deposit money banks in Nigeria. The

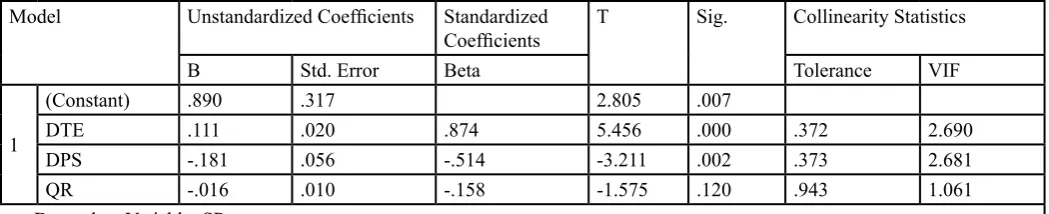

standardized beta values assess the contribution of each variable towards the determination of the dependent variables.

The regression results as presented in table 4.4 to investigate the contribution of each predictor variables (DTE, DPS and QR) on

the dependent variable (SP) revealed that when all the predictor

variables are not considered; SP is estimated at 89%. This simply

implies that when all the other variables are not considered,

SP is significantly estimated at 89% occasioned by factors not incorporated in this study. However, DTE of selected banks has beta coefficients of 0.874. This implies that a unit change in it will bring about a significant change in SP by 87.4%.

More so, the DPS of the selected banks reflects a beta coefficient of -0.514 (see table 4). This means that a unit change in the DTE will lead to a significant and negative change in the SP of selected banks in Nigeria by 51.4%.

Finally, firms QR reflect a beta coefficient of -0.158 (see table 4) which means that a unit increase in QR will lead to an insignificant decrease in return on equity (SP) of banks in Nigeria by 15.8%.

Test of Hypotheses One

Ho1: Debt-To-Equity Ratio does not significantly affect share price

of listed deposit money banks in Nigeria. Given that the critical

value of t is ± 2.000 and the calculated values of t is 5.456 which lies outside the region of acceptance. The researcher therefore

rejects the null hypothesis and accepts the alternative hypothesis and thus concludes that Debt-To-Equity Ratio significantly affect

share price of listed deposit money banks in Nigeria.

Test of Research Hypothesis Two

Ho2: Dividend Per Share does not significantly affect share price of

listed deposit money banks in Nigeria. Given that the critical value

of t is ± 2.000 and the calculated values of t is --3.211 which lies outside the region of acceptance. The researcher therefore accepts

the alternative hypotheses and thus concludes that Dividend Per

Share significantly affect share price of listed deposit money banks

in Nigeria.

Test of Research Hypothesis Three

Ho3: Quick ratio does not significantly affect share price of listed

deposit money banks in Nigeria. Given that the critical value of

t is ± 2.000 and the calculated values of t is -1.575 which lies within the region of acceptance. The researcher therefore accepts

the null hypothesis and rejects the alternative hypothesis and thus concludes that Quick ratio does not significantly affect share price

of listed deposit money banks in Nigeria.

Discussion of Findings

The first objective of this study was concerned with investigating

how Debt to Equity Ratio affect stock market measured in terms of share price. Consequently, the null hypothesis was formulated

in line with this objective and was tested using the t-test statistics

at 5% level of significance. Findings from this test reveal that Debt-To-Equity Ratio significantly affect share price of listed

deposit money banks in Nigeria.

More so, the second objective of this study which was interested

in investigating whether dividend per share significantly affect

stock market measured in terms share price of deposit money

banks; Consequently, the null hypothesis was also formulated in

line with this objective and was tested using the t-test statistics

at 5% level of significance. Findings from this study reveal that Dividend Per Share significantly affect share price of listed deposit

money banks in Nigeria.

Finally, the third objective of this study which was interested in

investigating whether the applicability ofquick ratio significantly affect stock market in terms of share price; Consequently, the null

hypothesis was also formulated in line with this objective and was

tested using the t-test statistics at 5% level of significance. Findings

from this study reveal that Quick ratio does not significantly affect

share price of listed deposit money banks in Nigeria.

V. Summary, Conclusion And Recommendations

Summary of Findings

This paper investigated the applicability of micro-economics variables on the stock market with specific respect to deposit money banks in Nigeria. The study adopts the ex-post-facto research design in the investigation. The following are the summary of major findings arrived at through the test of research hypotheses

of the study: debt-to-equity ratio significantly affect share price

of listed deposit money banks in Nigeria, dividend Per Share

significantly affect share price of listed deposit money banks in

Nigeria and quick ratio does not significantly affect share price

of listed deposit money banks in Nigeria.

VI. Conclusion

This research was motivated by the overwhelming participation

of retail investors in the stock market recently. It was fuelled more by collapsing of various giants stock brokers and a big number of

retail investors were queuing to place their claims. The researcher

was therefore interested in answering some of the questions that

since the difference between the population and the result is insignificant. Table 4: Coefficientsa for Independent Variables

Model Unstandardized Coefficients Standardized

Coefficients T Sig. Collinearity Statistics

B Std. Error Beta Tolerance VIF

1

(Constant) .890 .317 2.805 .007

DTE .111 .020 .874 5.456 .000 .372 2.690

DPS -.181 .056 -.514 -3.211 .002 .373 2.681

QR -.016 .010 -.158 -1.575 .120 .943 1.061 a. Dependent Variable: SP

emerged during those periods on how retail investors (micro-economics) were reacting to loosing of funds and their stocks.

The study was designed to assess those specific factors that retail

investors put into consideration as they demand stocks in the stock

market. The study set out to seek empirical evidence on whether

retail investors are driven by perceptions and emotions which are

shaped by various factors which the researcher classified as micro – economic factors since they are directly affecting the investor. At the findings from the study revealed that micro economics

variables measured by debt to equity ratio, dividend per share and

quick ratio significantly affect the stock market measured in terms

of stock price of listed deposit money banks in Nigeria.

VII. Recommendations

In line with the findings of the study, the following recommendations are proffered. There is an urgent need to control the operations of stock brokers and agents of NSE in order to safeguard the public investments in the stock market. This shall ensure that what has

been happening lately after collapsing of various stock brokers is not repeated in the future.

There is also a dire need for the stock market authorities to set rules and regulations which will make the investor’s of the market safe. The results indicate that unequal distribution of shares from IPO’s

discouraged the retail investors in participating in the market.

There is need therefore, to ensure that all participants of the market play on a level ground. This shall create more confidence on the investors’ mind and shall be more than willing to participate more

and more in the market.

Inflation and unemployment rates should also be minimized since

they are affecting the demand for stocks negatively indirectly by

reducing the investors’ income. It is therefore paramount that the

government designs proper mechanisms of dealing with these two.

References

[1] Adeghzadeh, K. (2018). The effects of microeconomic factors on the stock market:A panel for the stock exchange in Istanbul ARDL analysis

[2] ibid

[3] Ahmed, Z. (2002). Capital Structure Effect on Firms Performance : Focusing on Consumers and Industrials

Sectors on Malaysian Firms. International Review of

Business Research Papers, 8(5), 137–155.

[4] Idris, I., &Bala, H. (2015). Firms ’ Specific Characteristics and Stock Market Returns ( Evidence from Listed Food and beverages Firms in Nigeria ), 6(16), 188–201.

[5] Rahman, A. A., Sidek, N. Z. M., &Tafri, F. H. (2009).

Macroeconomic determinants of Malaysian stock market.

African Journal of Business Management, 3(3), 95–106. [6] Lim, L. K. (2009). Convergence and interdependence between

ASEAN-5 stock markets. Mathematics and Computersin Simulation, 79(9), 2957–2966.

[7] Cohen, R. (2002). The relationship between the equity risk premium, duration and dividend yield. Wilmott Magazine, 44(April), 84–97.

[8] Auzairy, N. A., Ahmad, R., & Ho, C. S. F. (2011). Stock Market

Deregulation, Macroeconomic Variables and Stock Market

Performances. International Journal of Trade, Economics and Finance, 2(6), 495–500.

[9] Rogers, R. M. 1998. Handbook of Key Economic Indicators. New York: McGraw-Hill.

[10] Mohr, P. (1998). Economic Indicators. Pretoria: Unisa

Press.

[11] Titman, S., &Wessels, R. (1988). The Determinants of Capital Structure Choice. The Journal of Finance, 43(1), 1–19. [12] Rajan, R. G., &Zingales, L. (1995). What do we know about

capital structure? Some evidence from international data.

The Journal of Finance, 50(5), 1421–1460.

[13] Hall, G., Hutchinson, P. and Michaelas, N. (2000) Industry Effects on the Determinants of Unquoted SMEs’ Capital Structure. International Journal of the Economics of Business, 7, 297-312.

[14] Fama, E. F., & French, K. R. (2002). Testing Trade-Off and Pecking Order Predictions About Dividends and Debt. TheReview of Financial Studies, 15(1), 1–33.

[15] Hovakimian, A., Opler, T., Titman, S., The, S., Analysis, Q., Mar, N., Titman, S. (2001). The Debt-Equity Choice Published by : Cambridge University Press on behalf of the University of Washington School of Business Administration Stable URL: The Debt-Equity Choice,36(1), 1–24.

[16] Korajczyk, R. A., & Levy, A. (2003). Capital structure choice:

Macroeconomic conditions and financial constraints.

Journal of Financial Economics, 68(1), 75–109.

[17] Hovakimian, A. (2004). The Role of Target Leverage in Security Issues and Repurchases. The Journal of Business, 77(4), 1041–1072.

[18] Hovakimian, G. and Tehranian H. (2004). Determinants of

target capital structure: The case of dual debt and equity

issues. Journal of Financial Economics, 71 (3): 517-540 [19] Frank, M. Z., & Goyal, V. K. (2003). The effect of market

conditions on capital structure adjustment. Finance Research

Letters, 1(1), 47–55.

[20] Idris, I., &Bala, H. (2015). Firms ’ Specific Characteristics and Stock Market Returns ( Evidence from Listed Food and beverages Firms in Nigeria ), 6(16), 188–201.

[21] Hartono, J. (2004). The Recency Effect of Accounting Information. GadjahMada International Journal of Business, 6(1):21-26.

[22] Docking, D. S., & Koch, P. D. (2005). Sensitivity of investor

reaction to market direction and volatility: dividend change

announcements. Journal of Financial Research, 28(1), 21– 40.

[23] Kothari, S. P., Lewellen, J., & Warner, J. B. (2006). Stock

returns, aggregate earnings surprises, and behavioral

finance. Journal of Financial Economics, 79(3), 537–568. [24] Al-Shubiri, F. (2010). Analysis the Determinants of Market

Stock Price Movements: An Empirical Study of Jordanian Commercial Banks. International Journal of Business and Management, 5(10), 137.

[25] Subramanyam, K. R., & Wild, J. J. (2009). Financial statement analysis. McGraw-Hill.

[26] Kibuthu G.W. (2005), Capital Markets In Emerging Economies; A Case Study Of The Nairobi Stock Exchange, MBA Thesis, Available at: http:// fletcher.tufts.edu. [27] Capital Markets Authority (CMA). (2009) Homepage

operations.

[28] ibid

[30] Levin, A., Lin, C. F and Chu, J. C. S. ( 2002). Unit root tests in panel data: asymptotic and finite-sample properties, Journal

of Econometrics, Elsevier, vol. 108(1):1-2.

115:53-74

[32] Hadri, K. (2000). Testing for stationarity in heterogeneous

panels data. Econometrics Journal, 3, 142-161.

[33] Khanyisa, N., Kapingura, F. M. and Makhetha, M. P. (2016). The Interaction between the Stock Market and MacroeconomicPolicy Variables in South Africa. Journal of Economics, 7(1), 1-10

[34] ibid

[35] Borhan, S. & Ghazali, M. Z. (2017). The Impact of

Microeconomic Variables on Stock Return by Moderating

of Money Supply. Asian Social Science; 13(12), 191-13. [36] Ahmed, I. H., Muhammad, I. C., Sehrish, J., Sana, N. &

Muhammad, S. I. (2014). Impact of Micro Economic Variables on Firms Performance. International Journal of Economics and Empirical Research, 3:25-28

[37] Mohammad, B. A. (2011). Stock Prices and Microeconomic Variables: T-Y GrangerCausal Evidence From Dhaka

Stock Exchange (DSE).Research Journal of Finance and Accounting 2(6), 1-13.

[38] Michaelas, N. (2000). Industry Effects on the Determinants of Unquoted SMEs’ Capital Structure. International Journal of the Economics of Business, 7(3), 297–312.

[39] ibid

[40] Friedman, M. (1968). The role of monetary policy. The American Economic Review, 58(1), 1–17.

[41] ibid

Author Profile

Emmanuel Benson Ph.D is a lecturer II in

the Department of Accounting and Finance, University of Agriculture, Makurdi, Benue

State, Nigeria.

Uzoamaka Gloria Chris-Ejiogu Ph.D is a

lecturer II in the Department of Financial Management and Technology, Federal

University of Technology Owerri, Imo

State, Nigeria.

Simon Terdue Utsev is a Master Degree student in the Department of Accounting and Finance, University of Agriculture,