International Pension Plan Survey

Report 2015

International Pension

Plan Survey

Report 2015

Table of contents

Section 1 – Executive summary

Survey background...2

Overall results ...2

Section 2 – Overview of participants Industry sectors ...4

Plan size (membership) ...5

Membership criteria ...6

Objectives of IPPs/ISPs ...7

Location of membership ...7

Section 3 – Plan design features DC, DB or hybrid design ...8

Funded and unfunded plans ...8

Waiting periods and vesting criteria ...8

Plan vehicle ...9

Contribution amounts (DC plans only) ...10

Employer contributions ...11

Employee contributions ...12

Pensionable salary definition ...13

Investment options ...13

Distribution options ...14

Section 4 – Feature article for 2015 IPPs or ISPs used as pension or savings solutions in crisis countries ...15

Survey background

This report summarises the results of the 2015 International Pension Plan Survey, an annual survey conducted by Willis Towers Watson regarding international pension plan (IPP) and international savings plan (ISP) specific design elements and membership criteria. The survey covered 721 plans sponsored by 638 companies. The number of participants continues the increasing trend from previous years, showing that the survey goes on to gain interest and that new plans are being created. Among survey respondents, 23 new plans were set up in 2015.

The survey questionnaire has remained broadly the same as in previous years for continuity and comparability purposes. Also similarly to previous editions of the survey, the sample comprises large- and mid-sized multinational employers across a wide range of industry sectors, which employ expatriate and local workforces participating in IPPs/ISPs, ranging from less than 10 members to nearly 30,000. Our survey covers the basic information around IPP/ISP membership criteria (plan size and location), plan design (such as defined contribution (DC), defined benefit (DB) or hybrid), funding, waiting and vesting criteria, vehicle, employer and employee contribution amounts, pensionable salary, investment funds and retirement distribution options.

Overall results

The survey covers the same 19 industry sectors as featured in previous editions. The largest concentration continues to be from the banking and finance sector, with many IPP/ISP sponsors representing oil and gas, industrials, engineering and power, transport and travel, and food and drink sectors. The main objective of IPPs/ISPs is in most cases to provide retirement benefits (60%), however there is an increasing number of IPPs/ISPs being utilised as savings vehicles with a savings objective.

Executive summary

plan. A continuing trend is often to extend plan participation to include local workforces, where their local retirement or savings solutions are either not available or not satisfactory due to poor market conditions. IPPs/ISPs can also be established for local employees only, where local retirement or savings market conditions allow for this and where it makes sense.

The size of the IPPs/ISPs (as defined by total number of members) participating in our survey varied from less than 10 to up to nearly 30,000 members spread across the globe. Overall, the vast majority of the new plans represented in this year’s survey were set up for a ‘global’ workforce.

Funded DC remains the most prevalent design basis, with DB plans still in operation but typically closed to new members and dwindling in numbers.

Most of the new plans set up in 2015 offer immediate vesting, as was observed in last year’s survey, despite the fact that incorporating vesting criteria into the IPP/ISP design can encourage employee retention. Where vesting rules do exist, a flat (or cliff) vesting schedule continues to be more popular than phased vesting. Of those employers that do incorporate a non-immediate vesting provision, almost all of these plans have a vesting period of more than one year.

The majority of IPPs/ISPs use a trust-based vehicle to segregate and protect the member assets, as was the case in previous years, and 90% of the funded plans that were set up over the last year utilise a trust. However, contract-based plans represent an increasing share of the total, reaching 43% in 2015. This may be due to the historical cost of trust provision as well as a general aversion to trusts in certain regions. It should be noted that in parts of the world, such as the Middle East, IPPs/ISPs are sometimes used as funding vehicles for mandatory termination indemnities, gratuities or End of Service

Contribution levels and structures continue to vary in this market. The main findings for 2015 were:

The highest concentration of plans reported having a flat contribution scale as opposed to service- or age-related scales.

Pensionable salary is most commonly defined as ‘base salary only’, similar to last year (67% of responses). Other possibilities, such as ‘base plus bonus’ and ‘all remuneration’ were less prevalent, with only 13% and 11% of the responses respectively.

Around 52% of plans have no employer matching contributions. In the cases where employer matching is a feature, 1:1 matching is more prevalent than 1:2 matching.

In most plans, the minimum level of employercontributions is less than 5% of pensionable salary (after removing the ‘nil’ category – meaning no contributions at all).

The maximum employer contributions are most commonly between 5% and 9%, with 10% to 14% being the next most popular range.

The majority of plans have voluntary employeecontributions (contributions are not compulsory and not based on a set range or scale) or are non-contributory (employee contributions are not incorporated into the design or are not allowed).

Minimum employee contributions are most commonly reported as nil. The next most frequently reported amount is less than 5% of pensionable salary.

For maximum employee contributions, the mostcommonly reported level was between 5% and 9% (after removing non-contributory plans). Some of the plans also reported no maximum limit (8% of survey responses). Investment fund options continue to be increasingly sophisticated, often to meet the specific demographics of IPP/ISP members. The number of plans offering access to external fund managers on the investment platform (as opposed to internal funds only, which are typically limited to

the Provider’s proprietary investments) decreased slightly from last year’s survey, although it remains as a feature in the majority of plans.

Around 59% of IPPs/ISPs in our survey offer up to 10 investment funds for members to choose from. The remainder offer in excess of 10 investment options, with 67 IPPs/ISPs offering between 11 and 15, and another 61 IPPs/ISPs offering 16 to 20. In addition, the results this year revealed that 46 IPPs/ISPs offer more than 40 different investment funds. This is perhaps a larger number than many domestic DC markets, but IPPs/ISPs commonly have to offer investment funds across currencies, with USD, EUR, GBP and CHF being the most commonly sought options. Lifestyle funds and Lifestyle strategies (composed usually of three or four funds) continue to feature in the investment offering. Thirty-eight percent of plans surveyed offer at least one Lifestyle option, and roughly one-quarter of the plans offer more than one Lifestyle option to provide for different membership demographics, risk profiles or currencies. The most popular form of distribution at retirement continues to be a lump sum, with 68% of the plans in this year survey offering only a lump sum. An increasing share of IPPs/ISPs are offering the choice of lump sum or annuity, although this is likely to be an internal annuity or drawdown, rather than an externally purchased offshore annuity. Only 3% of plans offer annuities only. The offshore annuity market remains small and typically poor value.

As reflected by the popularity of our survey, the IPP/ ISP market continues to evolve and the number of IPPs/ ISPs in existence continues to increase. Out of the total number of plans in our survey, 4% were set up in the last year and nearly 30% were set up in the last four years. This illustrates the continuing trend for IPPs/ISPs to be set up by global companies with internationally mobile employees and local employees requiring pension provision and savings facilities, where local arrangements are inadequate or absent.

Industry sectors

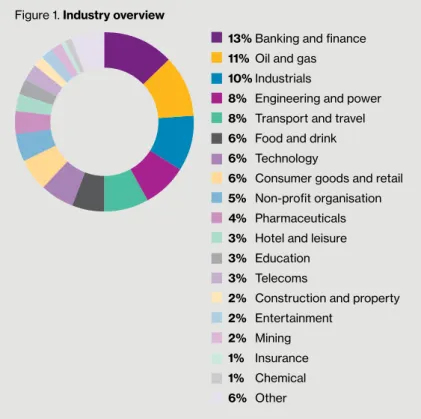

The 2015 Willis Towers Watson International Pension Plan Survey includes 638 multinational employers that sponsor one or more international pension plans (IPPs) or international savings plan (ISPs). Survey participants represent a cross section of industry sectors, with the percentage highest in banking and finance, oil and gas, industrials, and engineering and power. Forty-one of the organisations fell outside our broad industry sectors and so were classified as ‘Other’. Most industries in our survey, however, are well represented by at least five companies, each sponsoring one or more IPPs/ISPs. A full breakdown by industry is shown in Figures 1 and 2.

Overview of participants

Figure 1. Industry overview

13% Banking and finance

11% Oil and gas

10% Industrials

8% Engineering and power

8% Transport and travel

6% Food and drink

6% Technology

6% Consumer goods and retail

5% Non-profit organisation

4% Pharmaceuticals

3% Hotel and leisure

3% Education

3% Telecoms

2% Construction and property

2% Entertainment

2% Mining

1% Insurance

1% Chemical

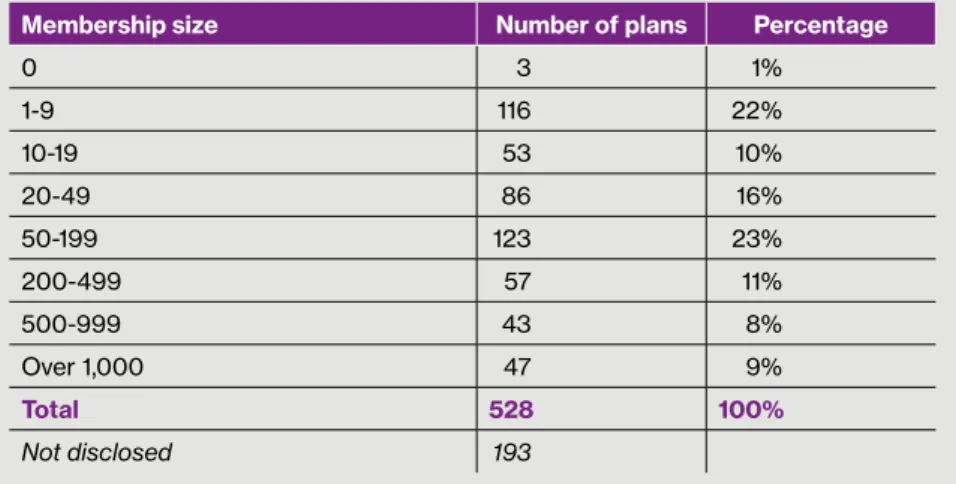

Plan size (membership)

Plan size is defined by the total number of active and deferred members. Responding IPPs/ISPs indicate great variance in membership: 27 have only one active member while three have 5,000 or more. Similar to last year, plan size is most often between 50 and 199 members (123

Figure 2. Plan by industry

Figure 3. Plan by membership size

Industry Number of companies Percentage of companies Number of plans Percentage of plans

Banking and finance 83 13% 111 15%

Oil and gas 67 11% 70 10%

Industrials 62 10% 64 9%

Engineering and power 49 8% 55 8%

Transport and travel 49 8% 51 7%

Food and drink 40 6% 56 8%

Technology 40 6% 42 6%

Consumer goods and retail 36 6% 37 5%

Non-profit organisation 34 5% 34 5%

Pharmaceuticals 28 4% 33 4%

Hotel and leisure 22 3% 25 3%

Education 20 3% 21 3%

Telecoms 16 3% 17 2%

Construction and property 14 2% 20 3%

Entertainment 12 2% 13 2% Mining 11 2% 12 2% Insurance 9 1% 9 1% Chemical 5 1% 6 1% Other 41 6% 45 6% Total 638 100% 721 100%

IPPs/ISPs), as shown in Figure 3. In addition, 378 IPPs have between one and 199 members, and 147 IPPs/ISPs have 200 or more. Fourteen of the 378 IPPs/ISPs with between one and 199 members were established this year. Headcount was undisclosed for an additional 193 IPPs that were included in the survey.

Membership size Number of plans Percentage

0 3 1% 1-9 116 22% 10-19 53 10% 20-49 86 16% 50-199 123 23% 200-499 57 11% 500-999 43 8% Over 1,000 47 9% Total 528 100% Not disclosed 193

Membership criteria

As in previous years, the strategic intent of IPPs/ISPs is often providing a ‘top-up’ or replacement benefit for international or expatriate employees who are no longer eligible for their home country plans or face a short-fall or no benefit from host country plans. An emerging trend is establishing new IPPs and ISPs, or extending the eligibility of existing ones, to enable local workforces to join. This occurs most often where the local savings or retirement plan market is underdeveloped, offers no or minimal tax advantages, or requires investment in local instruments such as bonds (which are often at high risk of default), or where investment offerings are restricted and/or few local providers offer quality administration and communication services.

As shown in Figure 4, the following membership categories were identified for our survey:

Expatriates – (54%). While the definition of ‘expatriate’ varies by organisation, this group typically contains IPP/ ISP members who can no longer remain in their home country plans and/or are unable to or should not (perhaps because of lengthy vesting periods) participate in a host country arrangement. The category includes a range of expatriates, including typical ‘out and back’ as well as career ‘nomads’.

Local employees (sometimes in addition to theexpatriate population) – (13%). IPPs/ISPs are commonly used for locals only or a combination of local and expatriate employees based in countries or regions with inadequately developed savings or retirement plan markets, but with a demand for efficient short- or long-term savings vehicles or retirement benefits. For example, IPPs might be offered to local employees to support the employer’s recruitment and retention efforts. Similar to last year, the Middle East and Latin America are common sites for this category of membership.

Executives – (circa 9%). The percentage of executives dropped slightly from 11% in last year’s survey. Survey respondents who identified executives defined these as top management enrolled in IPPs/ISPs either as nomads, meaning they have moved around throughout their career and thus need a top-up for post-retirement savings, or as current executives offered IPP/ISP membership as an incentive to take on a new role in another country.

Other – (circa 24%). This catch-all categoryencompasses other employer-defined criteria, such as all members of a legacy DB arrangement or non-US employees who are transferred to another country and are not enrolled in another pension plan (and not typically categorised as expatriates).

Figure 4. Membership criteria

Membership category Number of plans Percentage

Expatriates 323 54%

All local employees (could include expatriates) 78 13%

For executives only 56 9%

Other 147 24%

Total 604 100%

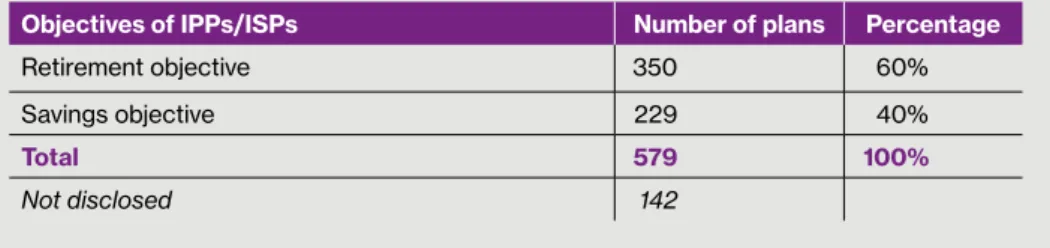

Objectives of IPPs/ISPs

As was the case last year, the overall objective of the majority of plans is to provide income at retirement. However, 229 plans reported a savings objective (ISPs) (Figure 5).

Location of membership

Of the 721 IPPs/ISPs surveyed, 693 specified a region for the plan. Similar to prior years, the largest percentage (67%) were described as global, meaning that members could be based anywhere in the world and be of any nationality. Fourteen percent of survey participants identified Europe and 7% identified the Middle East. Fourteen of the 107 IPPs/ISPs established since 2013 (13%) were for Middle Eastern populations. Figure 6 shows a location breakdown.

Figure 5. Objectives of IPPs/ISPs

Objectives of IPPs/ISPs Number of plans Percentage

Retirement objective 350 60%

Savings objective 229 40%

Total 579 100%

Not disclosed 142

Figure 6. Location of membership

67% Global 14% Europe 7% Middle East 4% Latin America 4% Africa 2% Asia 1% Caribbean 0%* South Pacific 0%* South Atlantic *Please note this is 0% due to rounding

DC, DB or hybrid design

In a well-established trend, most new plans are set up as DC arrangements. DB plans have been more prevalent historically and still exist, but on a much smaller scale since the first Willis Towers Watson IPP Survey in 2008. Among our survey respondents, only one DB plan was set up this year compared with 22 DC plans. Hybrid plans are less common than either DB or DC plans (Figure 7). In countries with a statutory ESB, termination indemnity or gratuity payment due to the employee, such as in parts of Europe and the Middle East, the benefit is sometimes incorporated or funded through the IPP. For example, IPPs can offer additional underlying DB benefits, such as applying extra-days accrual to a mandatory period-based formulae. This type of offering would be considered a hybrid design.

Funded and unfunded plans

The vast majority – 613 – DC IPPs/ISPs are funded; only 27 are unfunded, according to the survey. Of those that disclosed their funding status, roughly 63% of DB IPPs and 50% of hybrid IPPs are currently funded.

Plan design features

Waiting periods and vesting criteria

While waiting periods are relatively rare in IPPs/ISPs with a global workforce, they can be appropriate in plans that serve local workforces. In that case, the retirement savings accounts are likely to be smaller, and potentially with a higher turnover imposing an administrative burden on HR, which must maintain the accounts until distribution. This could potentially be 40 years into the future for certain IPPs. Of IPPs/ISPs providing responses on waiting periods, most offer immediate access for eligible employees. In the majority of plans that include waiting periods for eligibility, employees must wait one year or less.

Incorporating vesting criteria into the IPP/ISP design can encourage employee retention. Around 31% of responding IPPs/ISPs incorporated vesting provisions into the initial plan design. Most commonly, employer contributions vest completely within three to five years of plan participation.

Figure 7. DC, DB or hybrid design

Plan type Number of plans Percentage

DC 657 91%

DB 49 7%

Hybrid 13 2%

Total 719 100%

Figure 8. Vesting period

Figure 11. Plan vehicle Figure 9. Flat vesting period

Figure 10. Phased vesting schedule

Vesting type Number of plans Percentage

Immediate 437 69%

Phased 74 11%

Flat/cliff 126 20%

Total 637 100%

Not disclosed 84

Vesting type Number of plans Percentage

Trust 376 57%

Contract 282 43%

Total 658 100%

Not disclosed 63

Flat (or cliff) vesting Number of plans Percentage

Less than one year 9 8%

One year 11 10% Two years 22 19% Three years 20 17% Four years 3 3% Five years 27 24% Other 22 19% Total 114 100% Not disclosed 12

Phased vesting Number of plans Percentage

Immediate 1 2%

Less than one year 0 0%

One year 1 2% Two years 5 8% Three years 13 19% Four years 9 13% Five years 25 37% Other 13 19% Total 67 100% Not disclosed 7

Similar to last year, 69% of responding IPPs/ISPs vest employer contributions immediately. Fifty-nine percent of plans set up this year have immediate vesting for all contributions. Figures 8 through 10 show vesting criteria for the plans.

Vesting rules may be based on a flat or cliff scale, meaning that the member receives employer contributions after a specified number of years of participation. Phased (or tiered) vesting scales are also common, whereby the member gradually becomes entitled to employer contributions over a number of years:

Flat (or cliff) vesting schedule – (126 IPPs/ISPs). A flat vesting schedule means that employer contributions become 100% vested after a fixed number of years. Members are not entitled to any employer contributions unless they reach the requisite number of service years (see Figure 9).

Phased vesting schedule – (74 IPPs/ISPs). In a phased vesting schedule, employer contributions vest gradually over a set period. Members become entitled to a specified percentage of employer contributions after each year of service, up to the maximum service required. The proportion usually is linked to the maximum length of time up to 100% vesting, such as 20% a year over five years on a straight line basis. However, as shown in Figure 10, other designs are possible.Plan vehicle

We once again asked participants about the vehicle holding IPP/ISP assets. Both DC and DB vehicles can incorporate contract- or trust-based arrangements. As in all prior survey years, pension assets held within IPPs/ISPs are most commonly retained in trust vehicles in offshore locations. However, according to the 2015 survey data, roughly 43% of all IPPs/ISPs are contract-based, which is an increase from last year. In some parts of the world, such as the Middle East, IPPs/ISPs are sometimes used as funding vehicles for mandatory termination indemnities, gratuities or ESBs. In those cases, the sponsoring employer often needs to maintain control over the underlying assets, which is achieved through a contract-based solution (see Figure 11).

Figure 12 summarises the main features of the contribution schedules in this year’s survey. Forty-nine IPPs/ISPs are closed to new members and have only a deferred member population (hence no current contributions being accepted). The ‘Other’ category includes open DB plans and IPPs/ ISPs, which have discretionary contributions either annually or at different times (such as a top-up for an executive with another local pension plan). In addition, ‘other’ structures reported this year include employer contributions that are matched but capped either at a percentage or a monetary amount. A combination of different structures was also noted, such as age-related contributions plus a matching element which also increases with age.

Employer and employee contribution amounts also vary widely by plan, and details on the minimum and maximum scales are outlined in Figures 13 to 18.

Contribution amounts (DC plans only)

Contribution schedules vary widely amongst the IPPs and ISPs. Contribution designs fall largely into three groups: flat amounts (234 IPPs/ISPs), service-related (195 IPPs/ ISPs) or age-related (32 IPPs/ISPs), although age-related is becoming less popular with employers due to discrimination concerns. We also broke these three groups down further according to whether the plan has an employer-matching element (140 IPPs/ISPs).

Newer plans are generally moving away from service- and age-related scales and reported either a flat rate for all employees or different flat rates for different groups of employees (for example, one rate for local employees and another for executives). In this year’s survey, almost 45% of IPPs/ISPs set up after 2006 reported a flat rate, and roughly 55% of these do not offer employer matching. Figure 12. Contribution design

Description Number of plans Percentage Service-related, no matching 160 26% Service-related, 1:1 matching 32 5% Service-related, 1:2 matching 3 0%* Age-related, no matching 17 3% Age-related, 1:1 matching 10 2% Age-related, 1:2 matching 5 1% Flat, no matching 144 23% Flat, 1:1 matching 81 13% Flat, 1:2 matching 9 2% Employer-funded 14 2% Closed 49 8% Other 96 15% Total 620 100% Not disclosed 101

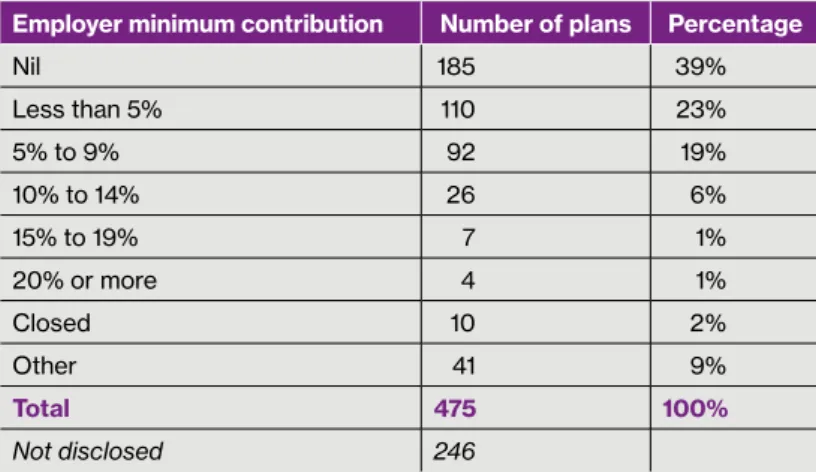

Employer contributions

Most commonly (after removing the ‘Nil’ category, meaning no contributions at all), the minimum amount of employer contributions is less than 5% of pensionable salary, with between 5% and 9% also being commonly reported. The most commonly reported amounts for maximum employer contributions are also between 5% and 9%, with 10% to

Figure 13. Employer minimum contribution

Figure 14. Employer maximum contribution

Figure 15. Employer average contribution

Employer minimum contribution Number of plans Percentage

Nil 185 39% Less than 5% 110 23% 5% to 9% 92 19% 10% to 14% 26 6% 15% to 19% 7 1% 20% or more 4 1% Closed 10 2% Other 41 9% Total 475 100% Not disclosed 246

Employer maximum contribution Number of plans Percentage

Nil 80 17% Less than 5% 23 5% 5% to 9% 133 29% 10% to 14% 82 18% 15% to 19% 48 10% 20% or more 28 6% Closed 10 2% No maximum 22 5% Other 39 8% Total 465 100% Not disclosed 256

Employer maximum contribution Number of plans Percentage

Nil 74 44% Less than 5% 12 7% 5% to 9% 35 20% 10% to 14% 12 7% 15% to 19% 11 6% 20% or more 4 2% Closed 4 2% Other 21 12% Total 173 100%

14% of pensionable salary the next most popular. Similar to last year, we also requested details of average actual employer contributions. Fewer participants reported average contributions than minimum and maximum contributions, but among those who did, the most common rates are between 5% and 9%.

Employee contributions

In the majority of IPPs and ISPs, employee contributions are voluntary (that is, contributions are not compulsory and not based on a set range or scale) or non-contributory, meaning employee contributions are not incorporated into the design or are not allowed. Two hundred and seventy-eight IPPs/ ISPs reported allowing employees to contribute additional voluntary contributions.

Minimum employee contributions are most commonly 0% (373 IPPs and ISPs). The next most frequently reported amount is less than 5%, which is in line with last year’s findings. The most commonly reported maximum employee contribution amount is 5% to 9% of pensionable salary, which was one of the largest categories last year (excluding non-contributory plans). The second most common

percentage this year is 20% or more.

Figure 16. Employee minimum contribution

Figure 17. Employee maximum contribution

Figure 18. Employee average contribution

Employee minimum contribution Number of plans Percentage

Nil 373 70% Less than 5% 91 17% 5% to 9% 39 7% 10% or more 5 1% Closed 20 4% Other 7 1% Total 535 100% Not disclosed 186

Employee maximum contribution Number of plans Percentage

Nil 215 43% Less than 5% 12 2% 5% to 9% 77 15% 10% to 14% 30 6% 15% to 19% 22 4% Over 20% 42 9% No maximum 40 8% Closed 21 4% Other 45 9% Total 504 100% Not disclosed 217

Employee maximum contribution Number of plans Percentage

Nil 146 72% Less than 5% 8 4% 5% to 9% 13 7% 10% to 14% 8 4% 15% to 19% 1 1% Over 20% 9 5%

Investment options

The investment funds in IPPs and ISPs vary from basic to very sophisticated, depending on the underlying membership as well as the Provider’s capabilities. More recently established IPPs/ISPs offer a large range of investment funds, often from ‘guided’ or ‘open’ architecture investment platforms or gateways through specialist Providers. The IPP/ISP sponsor may limit or expand the number of funds offered based on the sophistication of plan members and their needs. The funds available are often ‘best of breed’, being drawn from the wide universe of investment funds and investment managers available in the offshore market. Asset classes include global equity, regional equity, alternative investments, global bonds, diversified, commercial property, sharia and cash. More recently, ethical, frontier market and commodity funds are being requested. Many of these funds are offered in a range of currencies reflective of and convenient for the membership, for example EUR, USD, CHF and GBP.

The fund range in the offshore market includes both actively and passively managed funds, with a number of plans offering both active and passive alternatives in core asset classes, such as global equity and global bonds.

Pensionable salary definition

As for pensionable salary definitions, base salary only continues to be the most common among survey respondents (Figure 19). However, a number of IPPs and ISPs also include bonuses when calculating contributions (60 IPPs and ISPs) or even all remuneration (50 IPPs and ISPs). ‘Other’ definitions include those where contributions vary by individual contract.

For the 2015 survey, as with prior years, we requested details of the number of funds offered as well as whether funds were internal only, external only or both internal and external. The number of IPPs/ISPs offering access to external fund managers on the investment platform (as opposed to internal funds only, which are typically limited to the Provider’s proprietary investments) decreased slightly from last year’s survey. A small number of IPPs/ISPs offer access to both internal and external fund managers (Figure 20).

As in prior years, there was growth in the percentage of plans offering tailored investment options for local workforces, such as Lifestyle funds and strategies (also known as Life-cycle options, Figure 21). Sharia investments continue to be offered in the Middle East.

Around 59% of responding IPPs and ISPs allow members to choose from up to 10 investment funds, and the others offer more than 10 investment options (Figure 22). The highest concentration of plans reporting more than 10 investment funds offer 11 to 15 different funds, which is similar to last year’s results. Lifestyle funds and Lifestyle strategies (usually composed of three or four funds) continue to feature in investment offerings. Roughly 38% of plans offer Lifestyle options, with 25% offering more than one Lifestyle option to different memberships with distinct demographics, risk profiles and currencies.

Figure 19. Pensionable salary

Pensionable salary definition Number of plans Percentage

Base salary only 314 67%

Base + bonus 60 13%

Base + bonus + allowances 12 3%

All remuneration 50 11%

Other 24 5%

Not applicable (plan closed) 5 1%

Total 465 100%

Figure 20. Nature of funds offered

Figure 21. Lifestyle strategies offered

Figure 22. Number of funds

Figure 23. Distribution options

Funds Number of plans Percentage

Internal 184 34%

External 328 60%

Internal and external 10 2%

Not applicable (including unfunded) 21 4%

Total 543 100%

Not disclosed 178

Number of lifestyle options Number of plans Percentage

0 398 62% 1 86 13% 2 24 4% 3 122 19% 4 6 1% 5 or more 8 1% Total 644 100% Not disclosed 77

Number of funds Number of plans Percentage

1 to 5 216 40% 6 to 10 103 19% 11 to 15 67 13% 16 to 20 61 11% 21 to 40 49 9% More than 40 46 8% Total 542 100% Not disclosed 179

Number of funds Number of plans Percentage

Lump sum only 406 68%

Lump sum and annuity 167 28%

Distribution options

The final area of focus in our survey was around the options members have to receive their money either at retirement or upon leaving employment (if IPP/ISP rules allow for distribution before a specified retirement age). A lump sum distribution of cash was by far the most prevalent distribution

option, as was the case last year. However, an increasingly common option taken by a number of IPPs/ISPs (especially those set up since 2006) is to offer the choice of a lump sum or an annuity (often an internal annuity or drawdown, rather than an externally purchased offshore annuity). Some IPPs/ ISPs provide an annuity only, with no choice to take a lump sum, although they are in the minority of the plans surveyed.

Over the last few years, there has been a growing interest by companies to offer an international pension plan (IPP) or international savings plan (ISP) to provide retirement and savings benefits to local employees and expatriates in crisis countries, for example those suffering from economic and political uncertainty, war or other such crises (including failure of the local supplementary pensions system). Many companies with operations in such countries have opted for providing retirement or savings benefits using an IPP or ISP vehicle rather than a potentially unstable local pension solution which might, due to local requirements, have to invest in local investments carrying a high risk of default (for example, domestic bonds rated ‘junk’ by the ratings agencies). This has even been the case where the local system provides tax efficiencies for local pension solutions that are not offered to IPP or ISP alternatives. A key driver for this trend is the sponsoring employer’s desire to safeguard employee funds from any potential local losses due to defaults. This not only seeks to protect the underlying assets of the employee savings, but also avoids any risk of the employer having to pay a second round of contributions to make up the lost accrued funds.

Feature article for 2015

IPPs or ISPs used as pension or savings

solutions in crisis countries

Companies are also looking to protect the buying power of employee savings through access to hard currency investments within IPP and ISP structures. This is particularly the case where currencies have fallen dramatically over short periods versus, say, the USD and the EUR. This has been a particularly popular feature to employees who in many developing countries have found their ability to purchase imported products greatly diminished due purely to currency movements.

A less important but still relevant feature is the substantial differences between the administration and communication services offered by IPP and ISP Providers compared to local Providers in the developing markets. IPP and ISP platforms offer much more in terms of standard features at much lower costs, for example sophisticated on line portals, decision-making tools, multi-currency and a wide array of communication media, including mobile applications and even multi-language capabilities.

Further information

For further information, please contact your Willis Towers Watson consultant or Michael Brough +44 20 7170 2155 [email protected] Aino Castrén +44 20 7170 2167 [email protected]

About Willis Towers Watson

Willis Towers Watson (NASDAQ: WLTW ) is a leading global advisory, broking and solutions company that helps clients around the world turn risk into a path for growth. With roots dating to 1828, Willis Towers Watson has 39,000 employees in more than 120 territories. We design and deliver solutions that manage risk, optimize benefits, cultivate talent, and expand the power of capital to protect and strengthen institutions and individuals. Our unique perspective allows us to see the critical intersections between talent, assets and ideas – the dynamic formula that drives business performance. Together, we unlock potential. Learn more at willistowerswatson.com.

Willis Towers Watson 71 High Holborn London WC1V 6TP