AUDIT TRANSPARENCY AND AUDITORS’ REPORTING

BEHAVIOR

Penny Fanyuan Zhang

Master of Commerce (The Australian National University)

A thesis submitted for the degree of

Doctor of Philosophy

The Australian National University

Acknowledgements

I would like to express my sincere appreciation to my supervisor, Professor Greg Shailer,

for his continuous and energetic support, patience, motivation, supervision, suggestions, and

immense knowledge in the past four years. This thesis would have not been possible without the

strength and guidance he offered. He is not only a responsible and encouraging supervisor but also

a lifelong friend who selflessly shares his career experience. I believe that everything I have learned

from him will stand me in good stead for many years to come.

I would like to take this opportunity to express my gratitude towards my co-supervisors,

Professor Neil Fargher and Associate Professor Louise Lu. Their valuable comments, suggestions,

and kind help have enabled me to refine and improve my work significantly.

I would like to thank the Director of the Research School of Accounting (RSA), Professor

Juliana Ng, for her support and understanding. I truly appreciate Dr Alicia Jiang for her endless

academic and life advice as my lecturer and friend. I also thank Dr Sorin Daniliuc for his guidance

as my master supervisor. His kindness helped to lead me into this area of research. I would also

like to express my sincere appreciation to the administration group at the RSA.

I am indebted to my friend and colleague, Ao Li, for the wonderful times and memorable

experiences we have shared in the past few years. I would also like to thank my friend, Yuria Liu,

for helping me through all the events and difficulties of these years. Thanks to all my friends in

Australia and China for your love and encouragement.

I thank Elite Editing for the thesis editing; their editorial intervention was restricted to

Last, I am deeply grateful to my parents Jun Zhang and Aiqin Wang. Without their

unreserved love, support, and understanding, I could not have gone this far in my studies. This

thesis is also dedicated to my beloved husband, Cai Li, and my upcoming baby girl, Kalie Li. Both

Abstract

This thesis focuses on the enhanced auditor’s reports that were first introduced in the United

Kingdom (UK) from 2013, with similar auditing standards subsequently introduced in many

jurisdictions. To enhance audit transparency, national regulators adopted standards for enhanced

audit reports, requiring auditors to tailor reports that identify material audit-related matters for an

engagement in a particular year. The first three implementation years of extended auditor’s reports

(EARs) in the UK, from September 30, 2013 to September 30, 2016 are examined in this thesis, to

understand better the way auditors behaved in implementing the new reporting requirements. The

thesis addresses the following three research questions (as three separate studies) that are

collectively concerned with the content of the more tailored EARs: (1) Is auditors’ standardized

wording usage in EARs a consequence of the underlying audit quality?; (2) Are auditors’ risk

disclosures in EARs influenced by the expertise of the audit committee (AC)?; and (3) Are the

year-to-year changes in EARs disclosures associated with audit effort?

Study 1 examines whether textual similarities of an EAR to other EARs within the audit

firm’s client portfolio reflect the relative audit quality at the engagement level. Similarity scores

are found to be positively related to abnormal accruals and negatively related to abnormal audit

fees. While the relations for abnormal accruals are significant for both key audit matters (KAM)

sub-sections and full EARs, they are stronger for the KAM sub-sections.

Study 2 investigates whether auditors’ reporting decisions are influenced by the expertise

of the AC. AC influence is assessed by examining the relation between auditors’ choices of KAMs

relative to the significant accounting issues (SIFs) reported by ACs in the extended audit committee

expertise significantly affects the auditor’s KAM disclosures, evidenced by fewer KAMs reported

in EARs and more consistency between KAM disclosures and ACs’ SIF disclosures. When

analyzing cases pertaining to non-alignment of KAMs and SIFs, I find that changes in the ACs’

accounting and industry expertise have significant effects on the auditors’ subsequent adoption of

SIFs that were not previously matched with KAMs. Further analysis of auditors’ subsequent

adoption of unmatched SIFs reveals a significant negative association with abnormal audit fees but

no significant relation with abnormal accruals, suggesting that, on average, an auditor’s initial

omission of subsequently adopted unmatched SIFs may be a consequence of insufficient audit

effort, but it is not necessarily a sign of lower audit quality.

Study 3 investigates whether auditors’ year-to-year changes in EARs disclosures are related

to the underlying audit effort, proxied by audit fees. Changes in EARs from year to year are

measured in terms of language usage and KAM selections. I find that audit fee changes are

negatively associated with language similarity scores (measured over time for a single company)

and “repeated” KAMs, and positively associated with “removed” and “added” KAMs, where the

“added” KAMs effect is further found to be driven by the “new” KAMs that are not borrowed from

the prior year’s EACR.

Overall, the results find that engagements with higher audit quality result in more tailored

EARs and greater changes in EARs disclosures reflect more audit effort. The findings indicate that

the contextual information included in EARs allows financial statement users to differentiate

Table of Contents

Abstract ... v

CHAPTER 1: Introduction ... 1

CHAPTER 2: Literature Review of EARs ... 10

CHAPTER 3: Study 1: Extended Auditor’s Reports and Audit Quality: A Textual Analysis ... 14

3.1Introduction ... 14

3.2Literature Review and Hypothesis Development ... 18

3.2.1.Prior Studies Related to EARs ... 18

3.2.2.Prior Studies Related to Report Transparency ... 20

3.2.3.Hypothesis Development ... 22

3.3Method ... 24

3.3.1.Measurement of EAR Similarity ... 24

3.3.2.Models for Testing the Hypothesis ... 28

3.3.3.Sample Selection... 30

3.4Results ... 32

3.4.1.Descriptive Statistics... 32

3.4.2.Regression Results ... 36

3.5Robustness Tests ... 38

3.5.1.Analyses Using Alternative Measures of EAR Similarity... 38

3.5.2.Analyses Using the Unadjusted Similarity Scores ... 40

3.5.3.Analyses Using Income-Increasing Abnormal Accruals ... 40

3.5.4.Analyses Using Abnormal Audit Fees... 41

3.6Additional Analysis ... 42

3.7Conclusions ... 45

CHAPTER 4: Study 2: The Effect of Audit Committee Expertise on External Auditors’ Disclosures of Key Audit Matters ... 47

4.1Introduction ... 47

4.2.1.Regulatory Standards and Related Studies ... 51

4.2.2.Prior Studies Related to Audit Committee Expertise ... 53

4.2.3.Hypotheses Development ... 56

4.3Method ... 60

4.3.1.Models for Testing the Hypotheses ... 60

4.3.2.Sample Selection... 63

4.4Results ... 64

4.4.1.Descriptive Statistics... 64

4.4.2.Regression Results ... 68

4.5Robustness Tests ... 73

4.5.1.Analyses Excluding Entities Not in Compliance with the Corporate Governance Code ... 73

4.5.2.Analyses Using Alternative Measures of Unmatched KAMs, Unmatched SIFs, and Count Regression ... 73

4.5.3.Analyses Using Alternative Measure of AC Expertise ... 74

4.5.4.Analyses Using Alternative Measure of UNMATCHED... 74

4.6Additional Analyses ... 75

4.6.1.Analyses on UNMATCHED_SIF Reported as KAM in the Following Year ... 75

4.6.2.Analyses for Audit Quality on SIFxPICK Behavior ... 81

4.7Conclusions ... 83

CHAPTER 5: Study 3: Year-to-year Extended Auditor’s Report Changes and Audit Effort ... 86

5.1Introduction ... 86

5.2Literature Review and Hypothesis Development ... 90

5.2.1.Prior Studies Related to EARs ... 90

5.2.2.Prior Studies Related to Audit Fees ... 91

5.2.3.Hypothesis Development ... 93

5.3Method ... 95

5.3.1.Measurement of Year-to-year EAR Modifications ... 95

5.3.2.Models for Testing the Hypotheses ... 98

5.4Results ... 100

5.4.1.Descriptive Statistics... 100

5.4.2.Regression Results ... 104

5.5Robustness Test ... 107

5.5.1.Analyses Using Cross-section Similarity Measures ... 107

5.6Additional Analysis ... 108

5.6.1.Analysis on Added KAMs ... 108

5.7Conclusions ... 111

CHAPTER 6: Conclusion ... 112

References ... 116

Appendices ... 125

Appendix 1 Variable Definitions ... 125

Appendix 2 Regression Results Using Alternative Measures of EAR Similarity ... 132

Appendix 3 Regression Results Using the Unadjusted Similarity Scores ... 134

Appendix 4 Regression Results Using Income-increasing Abnormal Accruals ... 136

Appendix 5 Regression Results Using Abnormal Audit Fees ... 137

Appendix 6 Regression Results for Analyses Excluding Entities Not in Compliance with the Corporate Governance Code ... 138

Appendix 7 Regression Results for Analyses Using Alternative Measures of Unmatched KAMs and Unmatched SIFs, and Count Regression ... 139

Appendix 8 Regression Results for Analyses Using Alternative Measures of AC Expertise . 141 Appendix 9 Regression Results for Analyses Using Alternative Measures of UNMATCHED ... 142

List of Tables

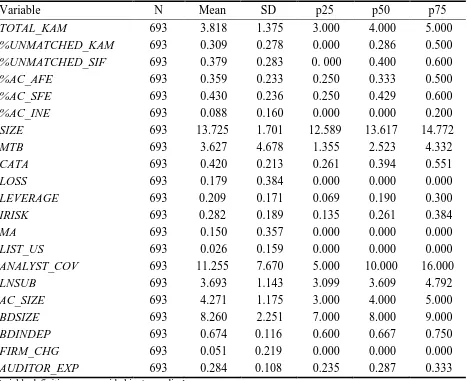

Table 3.1 Sample Selection ... 31

Table 3.2 Descriptive Statistics ... 32

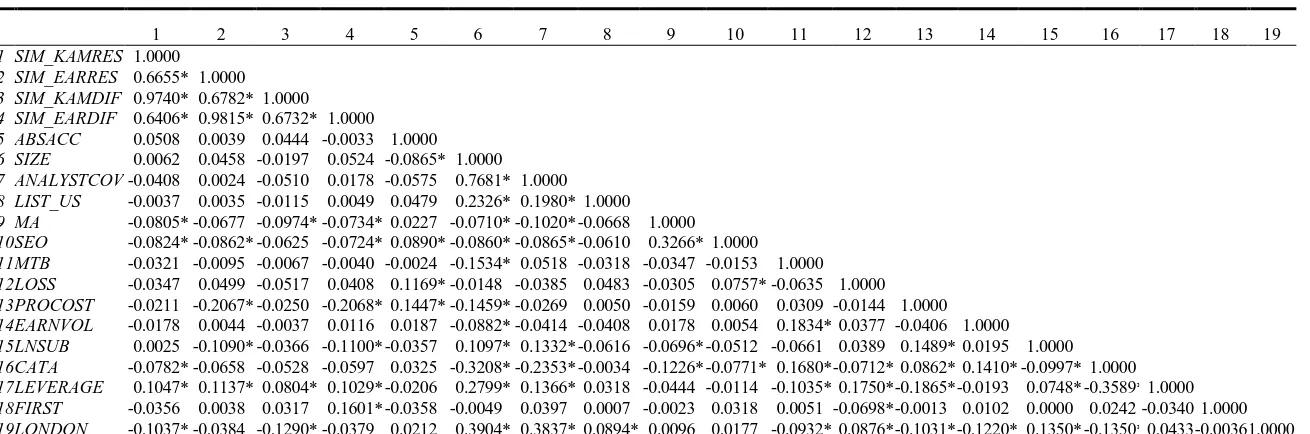

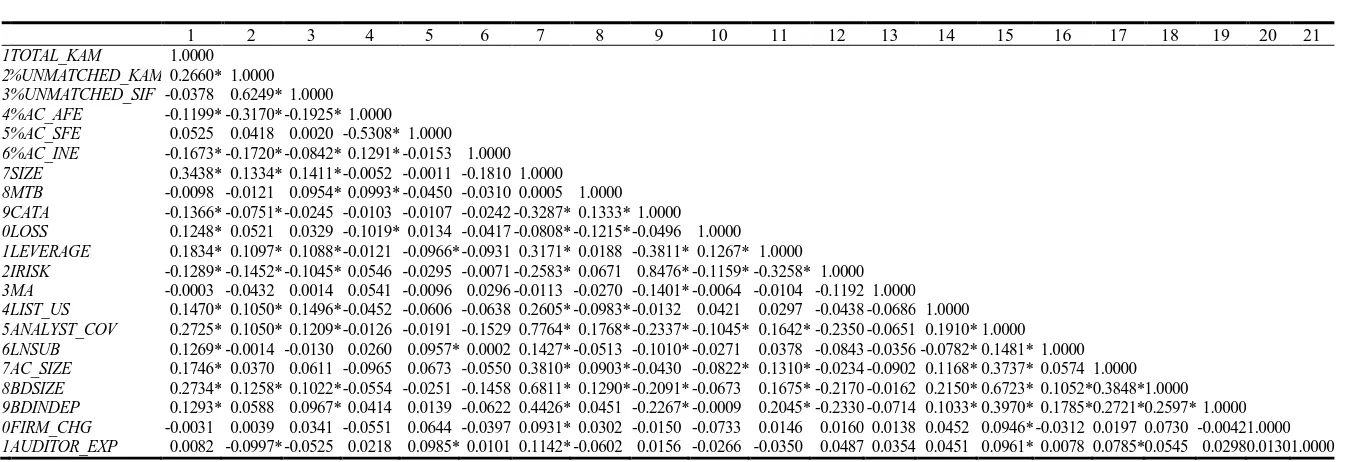

Table 3.3 Pearson Correlation Matrix ... 35

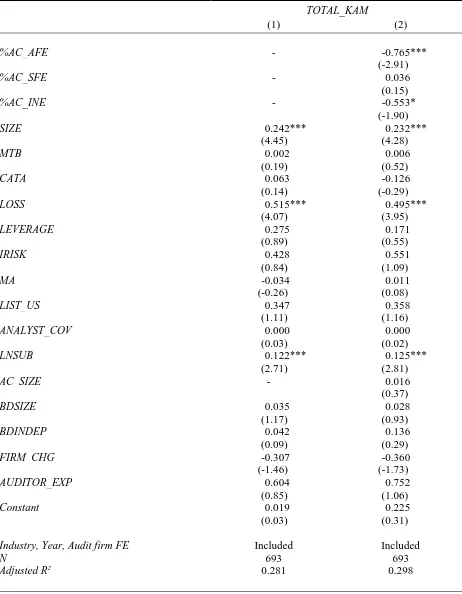

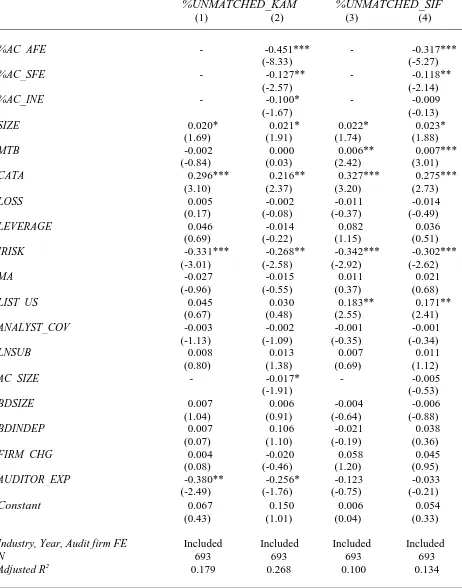

Table 3.4 Regression Results for Analyses ... 37

Table 3.5 Regression Results for Pre-Post EAR Analysis ... 44

Table 4.1 Sample Selection ... 64

Table 4.2 Descriptive Statistics for Hypotheses-testing Sample ... 65

Table 4.3 Pearson Correlation Matrix ... 67

Table 4.4 Regression Results for Hypothesis 1 Test ... 69

Table 4.5 Regression Results for Hypothesis 2 Test ... 71

Table 4.6 Sample Selection for Further Analyses ... 77

Table 4.7 Regression Results for Audit Fee Model ... 78

Table 4.8 Logistic Regression Results for PICK on AC Expertise ... 79

Table 4.9 Regression Results for Abnormal Accruals on SIFxPICK Behavior ... 83

Table 5.1 Sample Selection ... 100

Table 5.2 Descriptive Statistics ... 101

Table 5.3 Pearson Correlation Matrix ... 103

Table 5.4 Regression Results ... 105

List of Acronyms and Abbreviations

AC Audit Committee

AIM Alternative Investment Market

EACR Extended Audit Committee Report

EAR Extended Auditor’s Report

EC European Commission

EU European Union

FRC Financial Reporting Council

IAASB International Auditing and Assurance Standards Board

KAM Key Audit Matter

LSE London Stock Exchange

MD&A Management Discussion and Analysis

PCAOB Public Company Accounting Oversight Board

RSA Research School of Accounting

SEC Securities and Exchange Commission

UK United Kingdom

US United States

CHAPTER 1:

Introduction

The binary (pass/fail) auditor’s report has long been criticized because of concerns

regarding its form, wording, and limited communicative value (e.g., Church, Davis, and

McCracken 2008; Mock et al. 2013). Especially after the 2008 Global Financial Crisis, regulators

and investors put substantial emphasis on audit effectiveness, including whether the binary

auditor’s report provides adequate transparency to financial statements’ users regarding the audit

and the auditor’s insights about the entity (e.g., EC [European Commission] 2011; FRC [Financial

Reporting Council] 2015a; Simnett and Huggins 2014).

In May 2011, a consultation paper issued by the International Auditing and Assurance

Standards Board (IAASB) advocated that providing further information about the audit could

improve the communicative value of the auditor’s report: for example, disclosing “Key areas of

risk of material misstatement of the financial statements identified by the auditor” and “Areas of

significant auditor judgment” (IAASB 2011, paragraph 62). In June 2011, the Public Company

Accounting Oversight Board (PCAOB) issued a concept release to seek public comment on several

options for enhancing the auditor’s reporting model, including “a supplement to the auditor’s report

in which the auditor would be required to provide additional information about the audit and the

company’s financial statements” (PCAOB 2011, 2). Simultaneously, the EC proposed a regulation

in relation to enriching audit transparency through expanding the audit report, including “the key

areas of risk of material misstatements of the financial statements” (EC 2011, 7). Taken together,

all these proposed reforms aimed to make auditors provide greater transparency into the audited

entity, its financial statements, and the performed audit. Auditors, dealing with significant

material misstatement risks, critical accounting estimates, and judgments applied, and the

disclosure of such information would be of much value and benefit to financial statement users.

The United Kingdom (UK) FRC is ahead of the IAASB, PCAOB, and EU with regard to

implementing regulatory changes. Under the International Standards on Auditing (ISA) (UK and

Ireland) 700, for financial periods ending on or after September 30, 2013, entities that report on

application of the UK Corporate Governance Code are required to prepare an extended auditor’s

report (EAR) (FRC 2013a), with the IAASB standard, ISA 701, becoming effective for periods

ending on or after December 15, 2016 (IAASB 2015). According to the EU (2014), public-interest

entities need to adopt a new audit regime for accounting periods ending on and after June 16, 2017.

For large accelerated filers and all other companies in the United States (US), revised audit

reporting standards will become effective for periods ending on or after June 30, 2019, and

December 15, 2020, respectively (PCAOB 2017).

Although different terminologies are used in these standards, requiring auditors to disclose

significant audit matters in the year’s financial statement audit is consistent. According to the ISA

(UK and Ireland) 700, auditors are required to “describe those assessed risks of material

misstatement that were identified by the auditor and which had the greatest effect on: the overall

audit strategy; the allocation of resources in the audit; and directing the efforts of the engagement

team” (FRC 2013a, paragraph 19A).1 Under the ISA 701, the disclosed matters are named “key

audit matters” (KAMs), defined as “those matters that, in the auditor’s professional judgment, were

1 In the UK, entities applying the UK Corporate Governance Code include those with a premium listing of equity

of most significance in the audit of the financial statements of the current period” (IAASB 2015,

paragraph 8). Consistently, Regulation (EU) No. 537/2014 of the European Parliament and of the

Council states that the auditor should provide “in support of the audit opinion, a description of the

most significant assessed risks of material misstatement, including assessed risks of material

misstatement due to fraud; a summary of the auditor’s response to those risks; and where relevant,

key observations arising with respect to those risks” (EU 2014, article 10). In addition, under the

PCAOB’s standard, critical audit matters (CAMs) should be communicated in the auditor’s report,

defined as matters “communicated or required to be communicated to the audit committee (AC)

and that: (1) relate to accounts or disclosures that are material to the financial statements; and (2)

involved especially challenging, subjective, or complex auditor judgment” (PCAOB 2017, 11).

Collectively, there is a significant overlap among these reforms and the requirement of material

audit matters disclosures. Because the UK was the first jurisdiction to adopt the changes, the three

studies in this thesis are in that jurisdiction, with the FRC’s consistent regulatory improvement

making the results of this thesis generalizable to other jurisdictions.

Because the auditor’s report is the primary means by which the auditor communicates

information to financial statement users, its informativeness is of particular importance. Improving

the informativeness of audit report by enhancing their transparency in relation to the audit is the

key objective of this new reporting regime, with several suggestions to achieve this being raised

by regulators.

First, the language used to describe the auditor’s work should be non-standardized, as it is

entities and accounting periods leads to the EARs becoming longer, “boilerplate” reports.2 To make

the enhanced audit reports useful to investors and other financial statement users, regulators have

made a number of suggestions regarding the wording used in the standards. The ISA (UK and

Ireland) 700 advocates that communicated matters should be described “in a way that enables them

to be related directly to the specific circumstances of the audited entity and are not, therefore,

generic or abstract matters expressed in standardized language” (FRC 2013a, paragraph 19B).

According to ISA 701, when describing a KAM and discussing how this matter has been addressed,

auditors should relate “a matter directly to the specific circumstances of the entity” and avoid

“generic or standardized language,” to minimize the potential that EARs will “become overly

standardized and less useful over time” (IAASB 2015, paragraphs A44, A47). In addition, the

PCAOB advocates “communication will be tailored to the audit to avoid standardized language

and to reflect the specific circumstances of the matter” (PCAOB 2017, 32).

Second, standard setters have considered improving audit transparency through enriching

the AC disclosures; as ACs have specific responsibilities for a degree of oversight of the auditor or

aspects of the audit process, fuller disclosure of the AC activities in relation to the external audit

would benefit both the actual and perceived audit quality (IAASB 2014). In addition, the US

Securities and Exchange Commission (SEC) has considered whether ACs need to provide investors

with more external auditor-related information, such as the way that ACs perform their oversight

responsibilities (SEC 2015). It is worth noting that going beyond the US accounting standards,

some entities have provided additional voluntary disclosures (see SEC 2015, 22), including the

2 The terms “generic” “standardized,” and “boilerplate” (or “tailored,” “granular,” and “specific”) are used

significant areas that ACs have addressed with the auditor. In this regard, the UK is ahead of other

jurisdictions; for financial periods ending on or after September 30, 2013, ACs of companies that

report on the application of the UK Corporate Governance Code are required to issue extended

audit committee reports (EACRs). These require committee members to disclose “the significant

issues that the committee considered in relation to the financial statements and how these issues

were addressed; an explanation of how it has assessed the effectiveness of the external audit process

and the approach taken to the appointment or reappointment of the external auditor, and

information on the length of tenure of the current audit firm and when a tender was last conducted;

and if the external auditor provides non-audit services, an explanation of how auditor objectivity

and independence is safeguarded” (FRC 2012, Section C3.8). The most substantial change is the

requirement to report significant issues. Together with the simultaneous change in audit reporting,

audit transparency can be further enhanced by providing investors and other financial statement

users with different but complementary perspectives on key issues in financial reporting.

While audit transparency is the core purpose of implementing the long-form auditor’s

report, several other indirect benefits are expected (FRC 2015a; IAASB 2015; PCAOB 2017). In

particular, it is argued that by providing financial statement users with more entity-specific

information, the overall information asymmetry between investors and managers with regard to a

company’s financial performance should be reduced. The more informative auditor’s report should

facilitate investors’ ability to analyze financial statements, assess financial performance, or monitor

management’s stewardship of the company. In addition, it is argued that by requiring auditors to

provide more contextual information, financial statement users can better evaluate external

auditors’ performance and differentiate between accounting firms. Moreover, the requirement for

auditors, managers, and ACs, leading to improvements in audit quality and financial reporting

quality.

This thesis aims to gain a better understanding of auditor reporting under the new audit

transparency regime, by investigating three specific dimensions: the extent to which audit quality

differentiations can be revealed by the enhanced disclosures; the effectiveness of communications

between external auditors and ACs, with a particular focus on the influence that AC expertise has

on auditors’ disclosures; and the relation between auditors’ reporting behavior and audit effort.

The first study investigates the extent to which audit firms’ approaches to EARs can be

used to differentiate between accounting engagements in terms of audit quality. In particular, I

investigate the extent to which entity-specific information (in other words, non-standardized

language) is provided in the EARs and whether variations among the EARs’ contextual disclosures

across an audit firm’s client portfolio are associated with audit quality differentiations, and. As

noted earlier, using non-standardized wording is critical to achieving the objectives of EAR

adoption. In addition, an anticipated indirect benefit of the narrative disclosures in EARs is helping

financial statement users to differentiate between auditors’ performances. To address these issues,

I use textual analysis to examine whether the use of standardized or generic disclosures in EARs

relate to audit quality.

The second study examines the extent to which the expertise of the AC influences external

auditors’ reporting behavior. Answering this question is important because it may facilitate a better

understanding of the determinants of auditors’ risk disclosures. Examining the effect of the AC is

of particular importance because the AC is vital in monitoring external audit performance and

matters included in the EARs. According to the relevant auditing standards, there is a significant

overlap across jurisdictions with respect to the audit matters that should be communicated, not only

by definition but also by the approaches for determining those matters. Under the IAASB standard,

the disclosed KAMs should be determined from the matters communicated with those charged with

governance, particularly the AC (IAASB 2015). Similarly, the PCAOB standard notes that CAMs

are those “matters communicated or required to be communicated to the audit committee” (PCAOB

2017, 1). In addition, as discussed earlier, for financial periods ending on or after

September 30, 2013, the UK requires both external auditors and ACs for companies that report on

the application of the UK Corporate Governance Code, to report material matters in their respective

extended reports (FRC 2012, 2013a). Thus, the UK provides a unique setting for examining the

underlying interactions between external auditors and ACs. Although the UK reporting regulations

do not require matters disclosed in the extended reports of auditors and ACs to be entirely

consistent, a substantial degree of alignment is expected.3 By investigating the material matters

discussed in EARs and EACRs for a particular entity in a given year, the risk assessments of

auditors and ACs can be captured empirically. Because AC expertise has a significant effect on an

ACs’ accounting judgments and risk assessments of financial statements, I focus on AC expertise

to investigate the influence of ACs on EARs. Therefore, I examine the extent to which AC expertise

influences auditors’ risk disclosures in EARs, with particular focus on the differences between

matters communicated in EARs and EACRs.

The third study examines whether changes in auditors’ reporting behavior under this new

reporting regime are related to changes in audit effort. Specifically, this study focuses on the

year-to-year modifications of EARs, because the lack of changes in auditors’ disclosures over time is

another concern that has been raised with regard to EAR adoption. If disclosures do not

meaningfully change over time, EARs may become less uninformative (PCAOB 2017). This topic

is worth investigating because, in any company, there are inevitable similarities across a number

of years’ EARs, and if auditors use standardized words to describe similar risks and responses over

time, EARs will become longer reports more boilerplate language (PwC [PricewaterhouseCoopers]

2015). Therefore, when describing KAMs that recur over periods, auditors should highlight aspects

specific to the entity for that financial period (IAASB 2015). In the third study, the extent to which

auditors modify the disclosures in EARs from year to year is measured using textual analysis and

communicated matters (KAMs). I further examine whether year-to-year changes are related to

audit effort, as reflected in audit fees.

The first three implementation years in the UK market, from September 30, 2013 to

September 30, 2016, are examined because, as noted earlier, the UK is one of the first jurisdictions

to implement EARs and its unique regulatory setting requires both auditors and ACs to disclose

material risks in their respective extended reports. The results found in the UK should be

informative for stakeholders in other jurisdictions, because the FRC’s approach is similar to that

of the EU and narrower than the approach of the PCAOB and IAASB (Simnett and Huggins 2014).

Under the FRC’s auditing standard, the concept of material risks during the sample period is

defined as “risks of material misstatement that had the greatest effect on the overall audit strategy;

the allocation of resources in the audit; and directing the efforts of the engagement team” (FRC

the FRC extends the concept of material risks to incorporate the EU and the IAASB requirements,

and risks are discussed under the heading “KAMs” (FRC 2016a). The FRC expects that the

incorporation of the international standards will not result in a significant change in risk

identifications, because KAMs and material risks are broadly equivalent (FRC 2016b). Therefore,

for convenience, I label material risks in EARs as KAMs in this thesis.

The remainder of the thesis is structured as follows: Chapter 2 reviews prior studies

concerned with EARs. Chapters 3, 4, and 5 present the thesis Studies 1, 2, and 3, respectively.

Chapter 6 concludes the thesis by reviewing the findings, discussing the limitations, and providing

CHAPTER 2:

Literature Review of EARs

Prior archival studies of EARs are focused on the UK implementation effect, using pre-post

analyses, and yield ambiguous results.

Gutierrez, Minutti-Meza, Tatum, and Vulcheva (2018) find that the implementation of

EARs had no impact on investors’ reaction, audit fees, and audit quality. Their study implements

a difference-in-difference research design that compares the mandatory adoption companies with

the London Stock Exchange (LSE) Alternative Investment Market (AIM) entities, for a four-year

period (including two years before and after the EAR effective date, September 30, 2013). Using

cumulative absolute abnormal returns and abnormal trading volume centered on the report filling

date as the proxy for investors’ reaction, Gutierrez et al. (2018) find non-significant result that the

market perceives the EAR as a more informative and useful reporting model. In addition, the study

does not find significant incremental audit costs in relation to the requirement of additional

disclosures in EARs. No supporting evidence has been found that audit quality, measured as the

absolute discretionary accruals, is improved by the adoption of EARs. Moreover, Gutierrez et al.

(2018) also report that the non-significant results are not affected by the variations of report length,

total number of KAMs, the inclusion of unique KAMs, and materiality threshold. However,

comparatively higher audit fees are found to be paid to companies with longer reports and more

KAMs included.

Reid, Carcello, Li, and Neal (2018) also investigates the implementation effect of EARs in

the UK. Similar to Gutierrez et al. (2018), it uses a difference-in-difference research design and

two years pre and post periods. By using both European and US companies as control groups, Reid

quality, as measured by absolute abnormal accruals, the propensity to just meet or beat analyst

forecasts, and earnings response coefficients. In addition, the paper reports no significant difference

in the pre-post changes for those entities with more KAMs. Regarding the audit cost analysis, Reid

et al. (2018) report that the adoption of EARs does not result in a significant change on audit fees

or audit delay.

Lennox, Schmidt, and Thompson (2018) do not find any supporting evidence that investors

react to the KAM disclosures. The paper examines whether investors respond differently to entities

with more KAMs disclosed in their EARs, in which the cumulative abnormal returns, abnormal

trading volume, unsigned abnormal returns, and abnormal volatility are captured as the market

reaction proxies, during a one-year pre and post period. Lennox et al. (2018) further investigate

whether the market reacts differently to those more informative EARs and find that the

non-significant adoption effect is not changed whether companies have more KAMs that are at entity

or account-level, company or industry-specific, or expected or unexpected. Lennox et al. (2018)

categorize a KAM as an entity-level risk if it discusses doubts regarding the going-concern

assumption, management override of controls and accounting judgements, and as an account-level

risk if the discussion is associated with revenues, expenses, assets, liabilities, and the notes to the

financial statements. A KAM is also categorized as industry-specific if it has been disclosed in fifty

percent or more companies’ EARs in the relevant industry, and company-specific otherwise. The

number of unexpected KAMs is computed as the total number minus the expected number, which

is estimated by a prediction model. It find that the absence of any significant market reaction

persists after splitting the sample in relation to the strength of company’s information environment,

shareholders, or the number of “uncertainty” words using the Loughran and McDonald (2011)

word lists.

Lennox et al. (2018) find that investors perceive the additional disclosures in EARs as

reliable, evidenced by significantly smaller coefficients on earnings per share and net assets per

share when more KAMs are included. However, similar results are obtained when using the prior

year’s data, suggesting that investors were informed about the content of the KAM disclosures

prior to the use of EARs. In addition, they do not find any significant difference for entities having

more “new” KAMs (where “new” means the KAM was not discussed in the entity’s prior annual

report, earnings announcement, or conference call transcript), more “recurring” or “nonrecurring”

KAMs (where “recurring” means the KAM is disclosed in the next year’s EAR), or containing

more “negative” words, computed as the number of positive minus negative words, scaled by total

words, using the Loughran and McDonald (2011) word lists.

Porumb, Karaibrahimoglu, Lobo, Hooghiemstra, and de Waard (2018) investigate the

usefulness of KAM disclosures for private debt holders. For a four-year period (two years pre and

post the EAR effective date), the paper reports that the implementation of EARs benefits the UK

companies through more favorable loan contracting terms in terms of lower interest spread

(premium) and higher loan maturity, compared to the US control companies. The paper also finds

that companies with more KAMs included in the EAR get more stringent lending terms, evidenced

by larger interest spread, lower loan maturity and greater covenant intensity, suggesting that banks

perceive companies with more KAMs as risker and incorporate this information into their lending

decision process. In addition, results in Porumb et al. (2018) imply that the debt market reacts to

specific types of KAMs. The spread is positively associated with the number of KAMs pertaining

of inventory, and etc.) and going concern, and the loan maturity is negatively associated with

accounting issue-related KAMs. Covenant intensity is positively associated with going

concern-related KAMs and negatively associated with asset-concern-related KAMs.

The four EAR studies summarized above are largely concerned with user responses to the

EAR content. However, their examination of content is largely focused on the number or

characteristics of KAMs. Smith (2017), which conducts textual analysis on EARs, finds that EARs

are more readable than prior audit reports, using the Fog index as the readability measure, during

a two-year pre-post sample period. In addition, the study finds that auditors, exhibiting higher audit

quality, who are industry expertise, Big 4 auditors, and from larger offices, generate more readable

EARs compared to the others. Variations across audit firms are also found in the paper, in which

an average person needs one more year of formal education to read and comprehend the EARs

generated by Ernst & Young (EY). Using the Loughran and McDonald (2011) Negative, Positive, and Uncertain word lists to capture tone, Smith (2017) finds that, compared to the pre-ISA reports, higher frequency of negative and uncertain language is provided in EARs. Additionally, the paper

documents that analyst forecast dispersion is reduced after the adoption of EARs.

The pre-post analyses conducted in these prior studies are constrained by an implicit

assumption of homogeneous behavior among auditors, seemingly contrary to the regulators’

propositions that EARs will help financial statements users to distinguish between auditors with

CHAPTER 3:

Study 1: Extended Auditor’s Reports and Audit Quality: A

Textual Analysis

3.1 Introduction

This study examines whether transparency in auditor’s reports is positively related to the

underlying audit quality. Auditor’s reports have been standardized for the past many years and

extensively criticized because of the limited information they allow auditors to provide (e.g.,

Church et al. 2008). In response to such criticism, regulators, including the FRC, IAASB, EU, and

PCAOB, have adopted enhanced audit reporting standards that require auditors to disclose the most

significant audit matters in that year’s financial statement audit, using non-standardized language

(EU 2014; FRC 2013a; IAASB 2015; PCAOB 2017). These changes in audit reporting

requirements are intended to make audits more transparent by providing financial statement users

with information pertaining to the underlying audit work (e.g., FRC 2016a; PCAOB 2017).

However, the ability or willingness of the auditor to provide more engagement-specific disclosures

for a particular engagement may be a consequence of the extent to which they have acquired

sufficient knowledge of issues or their willingness to potentially reveal audit deficiencies for that

engagement. I examine this issue by investigating whether audit report transparency is a

consequence of the underlying audit quality.

As noted earlier, for reporting periods commencing on or after October 1, 2012, auditors of

UK companies that report on the application of the UK Corporate Governance Code are required

to implement the enhanced auditor reporting standard (FRC 2013a). The ISA (UK and Ireland) 700

requires auditors to disclose information on KAMs, materiality, and the scope of the audit.

communicating using non-standardized language is consistent to all of them (FRC 2013a, 2015a;

IAASB 2015; PCAOB 2017; Simnett and Huggins 2014). To enhance audit report transparency,

auditors are encouraged to provide contextual information regarding their approaches, judgments,

and findings. The use of tailored (granular) language, or the avoidance of standardized (generic)

wording, when discussing material risks of the audited entity is regarded as critical to achieving

the objectives of EARs (FRC 2013a; IAASB 2015; PCAOB 2017). However, when the FRC

evaluated auditors’ disclosures for each of the first two years of implementation of EARs, they

reported that a significant proportion of EAR disclosures seemed generic, becoming more tailored

in the second year (FRC 2015a, 2016a).4 It directed auditors to reduce their use of standardized

language further. Using the contents of EARs for the first three years of the UK’s application of

the EARs, I assess whether textual similarity in the EARs is negatively associated with audit

quality, as proxied by abnormal accruals, at the engagement level.

The textual similarities of the EARs are measured using the Vector Space Model (VSM).

To ensure that the engagement-level measures of textual similarities reflect audit firms’ choices at

the engagement level, rather than differences between audit firms, the textual similarity of a

specific EAR is computed as the mean of the similarity scores of that EAR’s text relative to each

of the other EARs issued by the same audit firm in the same year. This method is applied to both

4 The FRC states that their judgment is subjective and no definition of standardized wording is given from a technical

the KAM sections and the full EARs.5 I then investigate how EAR similarity scores vary in relation

to audit quality.

The implications of textual similarities in EARs for audit quality are not straightforward.

On one hand, standardization across reports may arise from deficiencies in audit effort or

competence. For example, generic disclosures may be chosen intentionally by auditors to reduce

transparency when they have concerns regarding the detectability of poor audit performance. From

this perspective, a negative association between EAR similarity scores and audit quality is expected

because the standardized disclosures, making “unlike things look alike”, fail to convey desirable

entity-specific information. On the other hand, standardization across reports may arise from

comparability, where “like things should look alike” (FASB [Financial Accounting Standards Board] 2010; Lang and Stice-Lawrence 2015)6. Comparability, which is defined by FASB as a

qualitative characteristic of disclosure that enables users to identify and understand similarities and

differences among items, might be enhanced by standardized disclosures. In that context, no

relation between EAR similarity scores and audit quality is expected. In this study, I first adjust the

measure of EAR similarity by taking into account the expected effect of standardized wording

based on industry comparability effects. Entities’ disclosures that deviate from those of the

5 I test KAM sections and full EARs separately because some sections of the EAR are likely to be standardized, such

as explanations of the respective responsibilities of directors and auditors, and matters on which auditors are required to report by exception (e.g., FRC 2015a).

6 FASB (2010) states, “For information to be comparable, like things must look alike and different things must look

company’s peers, operating in the same industry, are more likely to be firm specific (Kravet and

Muslu 2013).

I then examine the relations between textual similarities of EARs and audit quality. Based

on the proposition in DeFond and Zhang (2014) that “audit quality is a continuous construct that

assures financial reporting quality, with high quality auditing providing greater assurance of high

quality financial reporting” (276), and consistent with the extant accounting and auditing literature,

I adopt the absolute value of cross-sectional abnormal accruals as the proxy for audit quality.7

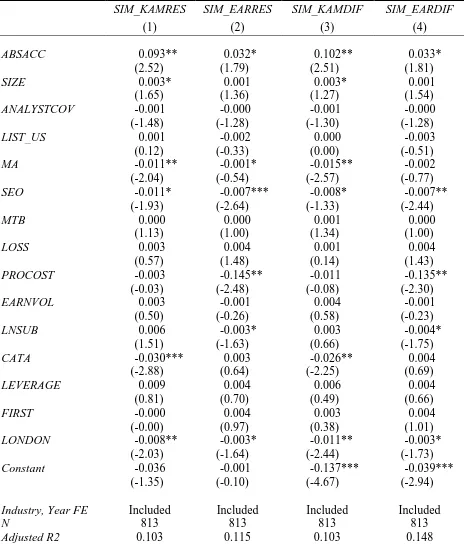

Overall, I find that abnormal accruals are positively associated with EAR similarity scores,

and the relations are more significant for the similarity scores of KAM sub-sections, compared

with the similarity scores of full EARs. This is further supported by evidence that high abnormal

audit fees are negatively related to similarity scores of KAM sub-sections. The results are

consistent with the proposition that when the underlying audit quality is lower, there is a higher

level of standardized language in EARs. In addition, I find that while overall audit quality appears

to have improved following the implementation of EARs in the UK, negative relations between

EAR similarity scores and audit quality persist.

This study contributes to policy development and the audit research literature. First, the

study informs standard setters of the effect of the revised auditing standards and may influence

regulators in their monitoring of audit reports and their future guidance to auditors. Although the

processes for determining communicated matters differ across jurisdictions, because the FRC’s

7 I cannot test other commonly used audit quality proxies, such as qualified audit opinions, going concern opinions,

approach is narrower than those of the PCAOB and IAASB, the UK experience should be

informative for stakeholders in jurisdictions adopting a broader approach.

Second, by examining the relations between audit quality and textual similarities of EARs,

this study contributes to the audit reporting literature and enriches the ongoing discussion regarding

EARs. Prior studies of EARs are mainly focused on examining overall EAR adoption effects by

conducting pre-post analyses, which implicitly assume homogeneous auditor behaviors (e.g.,

Gutierrez et al. 2018; Reid et al. 2018). I believe that the analysis of differences in auditors’

reporting behaviors at the engagement level provides a more nuanced understanding of the

association between audit quality and audit reporting.

Third, the extant literature analyzing company-related disclosures is growing rapidly to

encompass multiple textual resources, including annual reports, earnings announcements, analyst

reports, media articles, and regulatory documents (Young 2015). However, only a small number

of studies apply textual analysis to audit reports. In addition to extending the application of textual

analysis to audit reports, I augment established textual similarity methods by incorporating

adjustments for expected similarities that result from industry-based comparability effects in audit

reports. This methodological contribution may prove useful in other applications.

3.2 Literature Review and Hypothesis Development

3.2.1. Prior Studies Related to EARs

As noted in Chapter 2, the modest evidence as to whether the introduction of EARs affected

audit quality is mixed. Reid et al. (2018) find that the absolute value of abnormal accruals, the

following the implementation of EARs, but Gutierrez et al. (2018) do not find that EAR

implementation significantly affected the absolute value of abnormal accruals. As argued by the

two studies, their conflict findings may be due to research design differences.8 Reid et al. (2018)

calculate total accruals using the balance sheet method and employ both European and US

companies as control groups, while Gutierrez et al. (2018) compute total accruals as net income

minus cash flow from operations and use the non-adoption UK entities, the LSE AIM entities, as

a control group. Different from these two studies, I examine whether the auditor’s use of

standardized disclosures is associated with lower audit quality at the engagement level, during the

first three years of the EARs.

The non-significant equity market reactions to the EAR implementation reported in prior

studies might be a consequence of the existence of standardized disclosures in EARs (Gutierrez et

al. 2018; Lennox et al. 2018). As argued by Lennox et al. (2018), the information asymmetry

between investors and auditors is unlikely to be reduced if auditors use standardized language or

provide information that is not firm-specific. However, variations among auditors’ reporting

behavior have been found in prior research. Reid, Carcello, Li, and Neal (2015) find that, on

average, abnormal trading volumes around the annual report issuance increased by 13.5 per cent

following the implementation of EARs but the effect varied across audit firms. It was noted that

KPMG (EY) clients experienced the strongest (weakest) increase in abnormal trading volume while

8 In Section 5 of Gutierrez et al. (2018) and on page 5 of Reid et al. (2018), the two papers explain in detail how their

KPMG (EY) provided the most (least) entity-specific information among the Big 4 firms (Fisher

and Deans 2014, as cited by Reid et al. 2015).9 Smith (2017), a study involving a textual analysis

of EARs, finds that, on average, auditors with more industry expertise, from Big 4 accounting firms

and larger offices, produce more readable EARs. In addition, Smith (2017) finds that one additional

year of formal education is required to read EARs generated by EY.

As noted in Chapter 2, examination of the content of EARs in prior studies is focused on

the number of KAMs (Gutierrez et al. 2018; Lennox et al. 2018; Porumb et al., 2018), readability,

and tone (Smith 2017), using pre-post analyses. I extend this literature by investigating the

differentiation among EARs in relation to auditors’ standardized wording usage.

3.2.2. Prior Studies Related to Report Transparency

Prior studies examining the quality of corporate disclosures are mostly focused on

managers’ reporting behavior and do not consider audit reports. This includes a stream of studies

examining whether managers choose less transparent disclosures to reduce the detection of their

earnings management.

Lee, Petroni, and Shen (2006) find that companies with a history of strategically selling

available-for-sale securities to meet earning benchmarks are more likely to choose a less

9 Fisher and Deans (2014), as cited by Reid et al. (2015), is not publicly available. The Fisher and Deans (2014)

transparent format when disclosing information. Managers avoid reporting comprehensive income

in a performance statement, which make investors easier to detect their selective sale of securities.

Lobo and Zhou (2001) find a negative relation between the financial reporting quality, as

proxied by discretionary accrual, and corporate disclosure quality, measured as, the Association

for Investment Management Research (AIMR) scores, an industry-specific analysts’ assessment of

the informativeness of a company’s disclosures. Higher disclosure quality reduces information

asymmetry between managers and shareholders, which, in turn, decreases the flexibility of earnings

management. The results imply that managers prepare less transparent statements when they are

more engaged in earnings management behavior.

In addition, Cassell, Myers, and Seidel (2015) find that the disclosure transparency in

relation to activity in valuation allowance reserve accounts is negatively associated with

accruals-based earnings management. It is argued that because greater disclosure transparency facilitates

financial statement users’ detection of earnings management, managers by providing more

transparent disclosures, show their confidence in company financial performance and are less likely

to engage in earning management.10

Collectively, such studies support the proposition that managers reduce report transparency

to impede detection of lower earnings quality.

10 The link between transparency and accounting manipulation is supported by experimental evidence that increased

Brown and Knechel (2016) compare the similarity of companies’ narrative disclosures in

10-K filings to those of other companies in the same industry and year audited by the same Big 4

audit firms. The study examines three disclosure elements: the company business description,

management discussion and analysis, and notes to the financial statements. Of these, only the last

are audited. They find that similarity is negatively related to income-increasing accruals but

positively related to the likelihood of accounting restatements. Because Brown and Knechel (2016)

examine managers’ disclosures, they cannot form strong inferences regarding auditor behavior.11

While their paper concludes that audit quality may be associated with managers’ disclosures in the

financial statements, the role of the auditor in enabling or promoting the identified similarities is

not in evidence.12

3.2.3. Hypothesis Development

Transparency has been defined in accounting as disclosures that “reveal the events,

transactions, judgments, and estimates underlying the financial statements and their implications”

(Pownall and Schipper 1999, 262). In this regard, reports that use more standardized language and

so convey less firm-specific or fiscal-period-specific information are associated with lower

disclosure transparency (e.g., Brown and Tucker 2011; Hoberg and Maksimovic 2015; Lang and

Stice-Lawrence 2015).

11 Relatedly, Smith (2017) compares the word dictionaries generated from EARs with those generated from

management disclosures and finds that auditors’ wording usage is quite different from that of managers.

12 Brown and Knechel (2016) find that companies with lower 10-K similarity scores are more likely to switch to an

I argue that standardization or similarities across an auditor’s EARs may arise directly from

deficiencies in the auditor’s effort or competence. If an auditor pays insufficient attention to, or has

insufficient understanding of, entity-specific or fiscal-period-specific issues, the auditor is less able

to provide engagement-specific information in the EAR; in addition, this suggests a negative

relation between the extent of standardization (or similarities) in an auditor’s individual EARs and

the audit quality for individual engagements.

The prediction can be further supported by the prior discussions concerning managers’ use

of standardized wording. If preparers prefer less transparency to avoid revealing the quality of the

underlying performance, then lower transparency itself may signal lower quality when report

preparers are responsible for the reported performance as well (Cassell et al. 2015; Hunton et al.

2006; Tucker 2015). Applying the arguments to EARs, auditors are responsible for both the audit

report and audit quality, and transparency regarding audit work may facilitate the detection of poor

audit performance. Therefore, auditors seeking to avoid transparency for engagements that have

lower audit quality will prefer higher levels of standardization in the EARs for those engagements.

Taken together, the prior arguments lead to the following hypothesis:

HYPOTHESIS. Textual similarity in EARs is negatively related to audit quality.

The predicted association between textual similarity and audit quality might not be

observed if auditors strategically use seemingly tailored wording when preparing EARs to avoid

signaling performance deficiencies. If auditors expect that stakeholders value non-generic

disclosures in EARs, as evidenced by the feedback received from investors and other stakeholders

(FRC 2016a) and partially supported by Reid et al. (2015), an auditor may anticipate intended

the wording of EARs as a deliberate differentiation or obfuscation strategy. This could confound

the testing of the hypothesis, but prior research suggests the information disclosed in EARs is

regarded as reliable by financial statement users (Lennox et al. 2018).

3.3 Method

To test the hypothesis, I must measure generic disclosures in EARs. However, base

measures of textual similarities of EARs within the audit firm portfolio may be misleading and

thus confound the hypothesis tests, where textual similarities are consequences of similarities in

client-specific engagement factors; that is, if the similarities “make like things look alike”. For

example, because companies that are in the same industry and year and are audited by the same

accounting firm have more comparable accruals and earnings structures (Francis, Pinnuck, and

Watanabe 2014), and report more similar narrative disclosures in their financial statements (Brown

and Knechel 2016), it is reasonable that similarities will arise in their audit reports.13 To address

this concern, I adjust the base raw textual similarity scores for industry-based comparability effects,

as described below.

3.3.1. Measurement of EAR Similarity

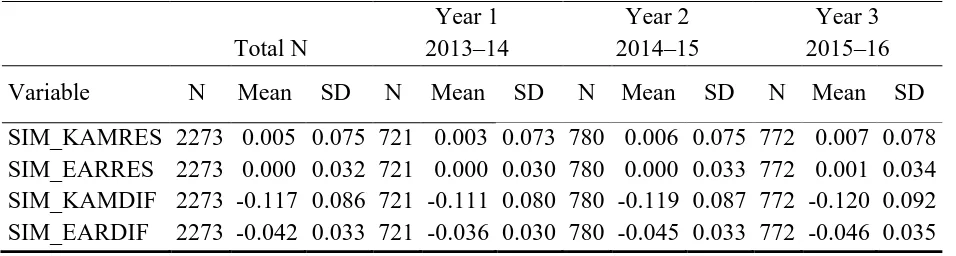

I measure the textual similarity of the EARs in an audit firm’s client portfolio for both the

KAM sections and the full EARs. Each company’s base KAM or full EAR similarity score is the

13 Although the wording used by auditors is substantially different from the word dictionaries generated from

average of its similarity scores (for the KAM section or full EAR) in relation to all the KAMs

(EARs) of other companies audited by the same audit firm in the relevant year.

The base similarity scores are computed using the VSM, which was developed to compare

strings of text or documents (Salton and Buckley 1988) and has been used to compute similarity

scores in 10-K filings (e.g., Brown and Tucker 2011; Hoberg and Maksimovic 2015; Hoberg and

Phillips 2010, 2016; Merkley 2014) and the initial public offering (IPO) prospectuses (Hanley and

Hoberg 2010, 2012). In the VSM, the selected text is represented by an m-dimensional vector, where m is the number of unique words after removing “stop words” in the defined set of documents.14 Specifically, if m unique words are included in an audit firm’s portfolio of KAM sections (or EARs), the vector for the KAM section (or full EAR) of company 𝑖 is represented as:

vi = (w1, w2, …, wm-1, wm)

(Model 3.1)

where w is the frequency of (each) word in the KAM section (or full EAR) for company i.

This method is also called cosine similarity because the similarity degree between the

vectors for EARs, vi, and vj is calculated as the cosine of the angle between the two vectors:

14 Consistent with prior papers, “stop words” are common words, such as “a,” “is,” “the,” and “will” (Li 2010;

Similarityij = (vi×vj) / (ǁ𝑣iǁ × ǁ𝑣jǁ)

(Model 3.2)

where vi×vj yields the scalar product of vi and vj, and ‖𝑣𝑖‖ and ‖𝑣𝑗‖ represent the vector lengths.15

Similarityij is bounded within (0, 1) and it approaches 1 when the similarity of two KAM sections (or two EARs) for companies i and j increases. I calculate Similarityij for each of the KAM section (KAM Similarityij) and the full EAR (EAR Similarityij) for each pair of companies (i and j) in an audit firm’s portfolio in a given year. For company i, I compute a BaseSIMKAM (and a

BaseSIMEAR) score as the average of its relevant Similarity scores in relation to all other (n-1) companies in the same audit firm portfolio (of n companies) in the relevant year. For the KAM similarity score for company i, this is expressed as:

BaseSIMKAMit = ∑jKAM Similarityij / (n-1)

(Model 3.3)

where n is the number of companies in the relevant audit firm’s portfolio in year t.

The same method is used to obtain BaseSIMEARit.

The BaseSIMKAM and BaseSIMEAR scores are then adjusted for industry-based comparability effects, for the reasons discussed in the previous section. The adjustment applied to

15 The inherent normalization makes it unnecessary to further control for EAR length (see Hoberg and Phillips 2010,

each company’s BaseSIMKAM or BaseSIMEAR is calculated using the same procedure as described by Models 3.1 through 3.3, except that the defined set of documents is the disclosures

for all companies in the same industry that are audited by the same audit firm in the relevant year.

Thus, company j must be in the same industry as company i.16 Based on Model 3.3, the adjustment for industry-based comparability effects for the KAMs section of company i is:

Ind_SIMKAMit = ∑jKAM Similarityij / (m-1)

(Model 3.4)

where m is total number of companies in the industry of company i in the relevant audit firm’s portfolio in year t.

The same method is used to obtain Ind_SIMEARit.

The Ind_SIMKAM and Ind_SIMEAR adjustments based on Model 3.4 can be obtained for company i only where the audit firm audits another company in the same industry as company i in the relevant year. I then use the following two methods to adjust the similarity scores for the

expected industry effects adjustments from Model 3.4, to obtain (1) the unexpected similarity score,

and (2) the adjusted similarity score:

1. To obtain the unexpected similarity score, I regress the base similarity scores (from Model 3.3) against the industry-based scores for each year (from Model 3.4). For the KAM scores,

this can be expressed thus:

16 This is similar to the grouping method used in Brown and Knechel (2016) to compare the similarity of the narrative

BaseSIMKAMit = b1Ind_SIMKAMit + it

(Model 3.5)

and save the residual it as the unexpected similarity score for the KAMs section for company i in year t, SIM_KAMRESit. The same method is used to obtain unexpected similarity scores for the full EARs, SIM_EARRES.

2. To obtain the adjusted similarity score, I deduct the industry-based score Ind_SIMKAM

from the base similarity scores BaseSIMKAM to obtain SIM_KAMDIF, thus:

SIM_KAMDIFit = BaseSIMKAMit – Ind_SIMKAMit

(Model 3.6)

The same method is used to obtain adjusted similarity scores for the full EARs,

SIM_EARDIF.

3.3.2. Models for Testing the Hypothesis

To test the hypothesis that KAM (EAR) similarity is negatively related to audit quality, I

estimate Model 3.7 as follows:

SIMit = β0+ β1ABSACCit + β2SIZEit+ β3ANALYSTCOVit+ β4LIST_USit+ β5MAit+ β6SEOit+ β7MTBit+ β8LOSSit+ β9PROCOSTit+ β10EARNVOLit+ β11LNSUBit+ β12CATAit+ β13LEVERAGEit+ β14FIRSTit+ β15LONDONit+ Σβ𝑗industry+ Σβ𝑘year+ it

(Model 3.7)

Consistent with prior studies, I obtain ABSACCit by estimating the cross-sectional modified Jones model (Dechow, Sloan, and Sweeney 1995) within two-digit ICB industry groups for each

year, with a minimum of 15 observations per two-digit ICB industry (Carcello and Li 2013; Reid

et al. 2018).17 I then match each firm-year observation with another firm from the same two-digit

ICB industry code and year with the closet ROA and ABSACCit is the absolute value of the difference (Kothari, Leone, and Wasley 2005). The hypothesis predicts a significant positive

coefficient on ABSACCit.18

Model 3.7 controls for client engagement factors that potentially influence auditors’ use of

standardized language in EARs. Generally, I posit that if a factor increases (decreases) audit effort,

it will be negatively (positively) associated with similarity scores.19 I include SIZE (the log of total assets) but I do not predict the sign of the coefficient. If large firms are more stable and thus have

relatively fewer risks (Campbell, Chen, Dhaliwal, Lu, and Steele 2014), then a positive relation is

implied, but if size-related political costs induce larger companies and their auditors to provide

higher-quality disclosures, then a negative relation is implied (Watts and Zimmerman 1990).

Consistent with the political costs argument, I predict that auditors use less-standardized language

in EARs for more visible companies. Therefore, similarity scores are expected to be lower for

companies followed by more analysts (ANALYSTCOV) or cross-listed in the US (LIST_US). Because entity events can also increase exposure or directly induce auditors to disclose more

17 The regression model is estimated as follows: ABSACC = α

0TOTAL_ACC – [α1 (1/TA) +α2 (𝑆𝐴𝐿𝐸𝑆 −𝑅𝐸𝐶)

+α3PPE]. Variable definitions are provided in Appendix 1.

18 For robustness, I calculate ABSACC as well, using the performance-adjusted approach, and the results (not tabulated)

are qualitatively similar to the main results.

specific information, I include indicator variables for companies engaged in

mergers-and-acquisitions (MA) and seasoned equity offerings (SEO) in the current year. More entity-specific information is also expected for companies that are financially distressed (LOSS), have a higher market-to-book ratio (MTB), significant earnings volatility (EARNVOL), more complex operations (LNSUB), current assets-related risks (CATA), or debt-related risks (LEVERAGE). I control for entity-specific proprietary costs using PROCOST (research and development costs divided by beginning total assets), a proxy for the product market competition, but I do not predict the

coefficient sign. While some prior studies find that companies are more likely to provide

entity-specific information if they are in competitive industries, others report a negative relation between

competition-related proprietary costs and the specific disclosures (see Beyer, Cohen, Lys, and

Walther 2010 for a review of related literature). I include two auditor-related indicator variables

that control for cases where the EAR is the first report issued by the audit firm for that client

(FIRST) and where the EAR is signed by an auditor who is located in the London office (LONDON), and I control for year and industry fixed effects.

3.3.3. Sample Selection

In the UK, the EAR is mandatory for that report on the application of the UK Corporate

Governance Code for fiscal years ending on or after September 30, 2013 (FRC 2013a). I obtain all

of the available annual reports of relevant companies with fiscal years ending between

September 30, 2013 and September 30, 2016, yielding 2,352 EARs that I use here to calculate base

similarity scores. Because my adjustment for industry-based comparability effects excludes cases

that are the only observation in the relevant auditor-industry-year portfolio, there are 2,273

DataStream (losing 204 unmatched cases) and during this process, I exclude 1,036 observations in

financial-related industries (for which the abnormal accruals model is not suited) and 210

observations missing the data necessary to calculate abnormal accruals or for my control

variables.20 The final sample for the main analysis is comprised of 813 firm-year observations, as

described in Table 3.1.21

Table 3.1 Sample Selection

Firm-year Observations

Total available EARs (used to calculate the unadjusted similarity scores) 2,352 Less: EARs with insufficient observations to calculate the industry-based

comparability effects (79)

Total available EARs to calculate the similarity scores (adjusted) 2,273

Less: Missing observations when merging with DataStream (204)

Less: Financial firm-year observations (including investment funds) (1,036)

Less: Observations with missing data to compute abnormal accruals (92)

Less: Observations with missing data to compute control variables (128)

Final Sample 813

20 Three early adopters are included in the sample and results remain unchanged after removing them from the analyses. 21 The final sample size is reasonable, compared with other EAR studies examining abnormal accruals in the UK. For