ZHANG, QIANYI. Seasonal Unit Root Tests: A Comparison. (Under the direction of Dr. David A. Dickey and Dr. Sastry G. Pantula .)

Three major regression-based seasonal unit root tests: the DHF test introduced by Dickey et al (1984), the HEGY test proposed by Hylleberg et al. (1990) and the Kunst test introduced by Kunst (1997) are compared. The regression model for the DHF test is a reduced form of that for the Kunst test. We modify the Kunst test by using the t-statistic instead of Kunst’s proposed joint F-statistic to study the influence of additional variables in the Kunst model. Also, we modify the HEGY test to test the presence of roots±1 and±iagainst the presence of roots±1. Through the comparison between the DHF test and the modified HEGY test, we find that the DHF test does not have an asymptotic power of one when the series only has some of the seasonal unit roots but not all of them. The asymptotic distributions derived in the paper provide the explanation of this limitation for the DHF test. Using simulation, we find that the probability that the DHF test fails to reject the seasonal unit root null hypothesis increases when the series contains more partial unit roots.

by

Qianyi Zhang

A dissertation submitted to the Graduate Faculty of North Carolina State University

in partial fulfillment of the requirements for the Degree of

Doctor of Philosophy

Statistics

Raleigh, North Carolina 2008

APPROVED BY:

Dr. David A. Dickey Dr. Sastry G. Pantula

Co-chair of Advisory Committee Co-chair of Advisory Committee

DEDICATION

BIOGRAPHY

ACKNOWLEDGMENTS

First of all, I owe a special word of thanks to my advisors Dr. David Dickey and Dr. Sastry Pantula for their guidance, time, and advice for my dissertation. They provided me with a tremendous amount of knowledge while still giving me the freedom to discover things on my own. I thank them for their encouragement to become an independent researcher. They are excellent statisticians and people. I am fortunate to work with them. I would also like to extend my sincere appreciation to my committee members for their contributions to the preparation of my dissertation. Thanks to Dr. Peter Bloomfield who provided helpful comments on the application to economic time series. Dr. Denis Pelletier also provided advice on getting the data for my analysis.

I am also thankful to Dr. Jacqueline Hughes-Oliver for her help and support during my program; I learned a lot of data mining techniques from her. I would like to thank Dr. Pam Arroway for her hard work to ensure the well-being of all students in the graduate program. I must thank Mr. Adrian Blue for his assistance in so many ways and Mr. Terry Byron for his professional technical support. My special thanks also go to Dr. Bibhuti Bhattacharyya, Dr. John Monahan, Dr. Leonard Stefanski, Dr. Sujit Ghosh and Dr. Hao Zhang for their wonderful lectures.

I would take the opportunity to thank my parents, who are always an unwavering source of support for me. They believe in me and encourage me in everything that I pursue. My parents have provided me with a tremendous amount of support. Without the love and support of my family, I would have never made it this far. Also, I am grateful for my friend, Yang Han, who encouraged me to keep trying when I thought I would never finish.

TABLE OF CONTENTS

LIST OF TABLES . . . vii

LIST OF FIGURES . . . ix

1 Introduction . . . 1

1.1 Statement of the Problem . . . 1

1.2 Literature Review . . . 3

1.2.1 Regression-Based Tests . . . 3

1.2.2 Graphical Test . . . 13

1.3 Summary of Chapters . . . 19

2 A Comparison of Seasonal Unit Root Test Criteria . . . 24

2.1 Motivations and Modifications . . . 24

2.2 Asymptotic Distributions . . . 27

2.2.1 Under the Null Hypotheses . . . 27

2.2.2 Under the Alternative Hypotheses . . . 41

2.3 Simulation Study . . . 56

2.3.1 Experimental Critical Values . . . 56

2.3.2 Empirical Powers . . . 59

2.4 Summary of Power Study . . . 84

3 Performance of Multiple-step Test Procedures . . . 87

3.1 Multiple-Step Test Criteria . . . 87

3.1.1 Introduction . . . 87

3.1.2 Three-Step Test Procedure . . . 88

3.1.3 Two-Step Test Procedure . . . 91

3.2 Simulations . . . 93

3.2.1 Simulation Design . . . 93

3.2.2 Simulation Results . . . 94

3.3 Summary of Empirical Study by Multiple-Step Test Criteria . . . 104

4 Augmented Seasonal Unit Root Models . . . 106

4.1 Extensions to Higher-Order Model . . . 106

4.2 Augmented DHF Model . . . 108

4.2.1 Introduction for Extensions of the DHF Test . . . 108

4.2.2 Empirical Comparison . . . 110

4.2.4 Improvement for the Biased Augmented DHF Models . . . 119

4.3 Augmented HEGY/Kunst Model . . . 129

4.3.1 Introduction for Extensions of the HEGY/Kunst Test . . . 129

4.3.2 Empirical Comparison . . . 133

4.4 Sensitivity to Lag Selection for the Augmented Models . . . 138

4.4.1 Over-fitting . . . 138

4.4.2 Under-fitting . . . 139

4.5 Summary . . . 140

5 An Application: Quarterly U.K. Household Disposable Income and Consumption Expenditure . . . 143

5.1 Introduction . . . 143

5.2 The Data . . . 145

5.3 Seasonal Unit Root Analysis . . . 149

5.4 Summary and Conclusions . . . 152

Bibliography . . . 154

Appendices . . . 157

Appendix A Proof of Asymptotic Diagonal for N12X′X When s=4 . . . 158

Appendix B Weak Convergence . . . 160

Appendix C The Smoothing Model for Table 2.1 to 2.3 . . . 164

Appendix D SCM for T = 400,800. . . 166

LIST OF TABLES

Table 2.1 Empirical Percentiles of ˆτρ=1, ˆτα=0, ˆτθ4=0 and ˆF1234. . . 58

Table 2.2 Empirical Percentiles of ˆτρµ=1, ˆταµ=0, ˆτθµ 4=0, ˆF µ 1234 . . . 59

Table 2.3 Empirical Percentiles of ˆτρd=1, ˆτθd 4=0 and ˆF d 1234. . . 60

Table 3.1 Models for The Two-Step (Three-Step) Approach . . . 92

Table 3.2 Empirical Critical Values for Multiple-Step Test Study. . . 97

Table 3.3 Empirical Size for Multiple-Step Test Study . . . 97

Table 3.4 Empirical Power for Stationary Simulated Series . . . 98

Table 3.5 Empirical Power for Non-Stationary Series . . . 100

Table 3.6 SCM for The Stationary Simulated Series . . . 102

Table 3.7 SCM for the Non-Stationary Simulated Series . . . 104

Table 4.1 Percentiles for ˆτξ1=0 and ˆτζ1=0for ADHF and ADHF-GLN on Simulated Series Yt=Yt−4+ǫt. . . 111

Table 4.2 Percentiles for ˆτξ1=0 and ˆτζ1=0for ADHF and ADHF-GLN on Simulated Series Yt=Yt−4+ 0.9(Yt−1−Yt−5) +ǫt. . . 112

Table 4.3 Test Statistic Percentiles for Consistent Model (ˆτξc=0) and Improve ADHF (ˆτξc′=0) on Simulated SeriesYt =Yt−4+ǫt. . . 123

Table 4.4 Test Statistic Percentiles for Consistent Model (ˆτξc=0) and Improve ADHF (ˆτξc′=0) on Simulated SeriesYt =Yt−4+ 0.9(Yt−1−Yt−5) +ǫt. . . 123

Table 4.5 Test Statistic Percentiles for AHEGY-GLN, AHEGY-P, AKUNST-GLN, AKUNST-P on Simulated Series Yt=Yt−4 +ǫt. . . 134

Table 4.6 Test Statistic Percentiles for AHEGY-GLN, AHEGY-P, AKUNST-GLN, AKUNST-P on Simulated Series Yt=Yt−4 + 0.9(Yt−1−Yt−5) +ǫt. . . . 135

Table C.1 The Coefficients for The Smoothing Models in Table 2.1 . . . 164

Table C.2 The Coefficients for The Smoothing Models in Table 2.2 . . . 165

Table C.3 The Coefficients for The Smoothing Models in Table 2.3 . . . 165

Table D.1 SCM for the Stationary Series . . . 166

Table D.2 SCM for the Non-Stationary Series . . . 167

Table E.1 Empirical Percentiles Obtained From ADHF and AHEGY-GLN Models with an Intercept and a Trend . . . 169

Table E.2 Empirical Percentiles Obtained From ADHF and AHEGY-GLN Models with Seasonal Dummies and a Trend . . . 170

LIST OF FIGURES

Figure 1.1 (a) Roots for Φ(B) = 1−B4; (b) Spectrum Estimates forY

t=Yt−4+ǫt

whereǫt i.i.d.N(0,1) . . . 3

Figure 1.2 The Run Sequence Plots for (a)Zt=Zt−4+ǫt; (b)Yt = 5×sin(π 2t)+ǫt 14 Figure 1.3 The Seasonal Subseries Plots for (a) Zt = Zt−4 +ǫt; (b) Yt = 5× sin(π 2t) +ǫt. . . 15

Figure 1.4 Autocorrelation Plots for series (a) Zt = Zt−4 +ǫt; (b) Yt = 5 × sin(π 2t) +ǫt. . . 17

Figure 1.5 Seasonal Subseries Autocorrelation Plots for Seasonal Random Walk Zt = Zt−4+ǫt: (a) mod(t,4)=1; (b) mod(t,4)=2; (c) mod(t,4)=3; and (d) mod(t,4)=0 . . . 18

Figure 1.6 Seasonal Subseries Autocorrelation Plots for Stationary Process Yt= 5 × sin(π 2t) + ǫt: (a) mod(t,4)=1; (b) mod(t,4)=2; (c) mod(t,4)=3; (d) mod(t,4)=0 . . . 19

Figure 1.7 Autocorrelation Plots for Testing Root 1 (ˆρ1). . . 20

Figure 1.8 Autocorrelation Plots for Testing Root -1 (ˆρ2) . . . 20

Figure 1.9 Autocorrelation Plots for Testing Roots±i (ˆρ4) . . . 21

Figure 2.1 The Asymptotic Behaviors Of ˆτρ=1 for Series (a) Y1,t = Y1,t−4 +ǫt, (b) Y2,t = .5Y2,t−2+.5Y2,t−4+ǫt, (c) Y3,t = 1.5Y3,t−2 −.5Y3,t−4 +ǫt. (Series (a) is under the null hypothesis, while both series (b) and (c) are under the modified HEGY alternative hypothesis with β=.5 and -.5 respectively) . . 49

Figure 2.2 Empirical Power for Zero Mean Models on DGP1: Yt=ρYt−4+ǫt. . 63

Figure 2.3 Empirical Power for Zero Mean Models on DGP2: Yt =αYt−2+ (1− α)Yt−4+ǫt. . . 65

Figure 2.4 Empirical Power for Zero Mean Models on DGP3: Yt=−(a−b)Yt−1+ b(a−1)Yt−2−b(a−b)Yt−3+ab2Y t−4+ǫt with a= 0.5 . . . 67

Figure 2.6 Empirical Power for Zero Mean Models on DGP4: Yt=Asinπt 2

+ǫt 70 Figure 2.7 Estimated Densities of Test Statistics (a) The DHF t Statistic ˆτρ=1,

(b) The Kunst t Statistic ˆτθ4=0, (c) The Modified HEGY t Statistic ˆτα=0

and (d) The HEGY Overall F Statistic ˆF1234 on DGP4: Yt =Asinπt 2

+ǫt

(T = 40) . . . 72 Figure 2.8 Empirical Power for Models with Quarterly Dummy Variables on

DGP1: Yt =ρYt−4+ǫt. . . 75 Figure 2.9 Empirical Power for Models with Quarterly Dummy Variables on

DGP2: Yt =αYt−2+ (1−α)Yt−4+ǫt. . . 76 Figure 2.10 The Asymptotic Behaviors of ˆτρµ=1 for Series Generated under DGP2

with Varying Values of 1−α and The Series under The Null . . . 77 Figure 2.11 Empirical Power for Models with Quarterly Dummy Variables on

DGP3: Yt =−(a−b)Yt−1+b(a−1)Yt−2−b(a−b)Yt−3 +ab2Y

t−4+ǫt with a= 0.5 . . . 78 Figure 2.12 Empirical Power for Models with Quarterly Dummy Variables on

DGP3: Yt =−(a−b)Yt−1+b(a−1)Yt−2−b(a−b)Yt−3 +ab2Y

t−4+ǫt with a= 0.9 . . . 79 Figure 2.13 Empirical Power for Models with Quarterly Dummy Variables and A

Single Trend on DGP1: Yt=ρYt−4+ǫt. . . 80 Figure 2.14 Empirical Power for Models with Quarterly Dummy Variables and A

Single Trend on DGP2: Yt=αYt−2+ (1−α)Yt−4+ǫt . . . 82 Figure 2.15 Empirical Power for Models with Quarterly Dummy Variables and A

Single Trend on DGP3: Yt = −(a−b)Yt−1+b(a−1)Yt−2 −b(a−b)Yt−3+

ab2Y

t−4+ǫt with a= 0.5 . . . 83

Figure 2.16 Empirical Power for Models with Quarterly Dummy Variables and A Single Trend on DGP3: Yt = −(a−b)Yt−1+b(a−1)Yt−2 −b(a−b)Yt−3+

ab2Y

t−4+ǫt with a= 0.9 . . . 84

Figure 4.1 Power Plots of ˆτξ1=0 and ˆτζ1=0 onYt= ρYt−4 +κ1(Yt−1−ρYt−5) +ǫt

with ρ= 0.9,· · ·,0.99: (a) κ1 = 0.5, (b) κ1 = 0.9. . . 113

Figure 4.2 3D Plot of The Difference between The Limit of ˆζ1 and (ρ−1) with Varyingκ1 and ρ. . . 116

Figure 4.3 3D Plot of The Difference between The Limit of ˆξ1 and (ρ−1) with Varyingκ1 and ρ. . . 118

Figure 4.4 3D plot of the difference between the limits of ˆζ1 and ˆξ1 with varying κ1 and ρ. . . 120

Figure 4.5 The Limiting Bias for ˆκ1 with Varying Values of κ1 and ρ. . . 121

Figure 4.6 Box Plot of (a) ˆκ1 and (b) ˆκc for κ1 = 0.5 . . . 125

Figure 4.7 Box Plot of (a) ˆκ1 and (b) ˆκc for κ1 = 0.9 . . . 126

Figure 4.8 Relative Improvement in Power . . . 128

Figure 4.9 Empirical Powers for AHEGY-GLN, AHEGY-P,AKUNST-GLN and AKUNST-P onYt =ρYt−4+ 0.9(Yt−1−ρYt−5) +ǫt with κ1 = 0.9 . . . 137

Figure 4.10 Empirical Powers for AHEGY-GLN, AHEGY-P,AKUNST-GLN and AKUNST-P on Yt =κ1Yt−1+αYt−2−ακ1Yt−3+βYt−4−βκ1Yt−5+ǫt with κ1 = 0.9 and α+β = 1 . . . 137

Figure 4.11 Relative Power Reduction due to Fitting AR(6) Models on AR(5) SeriesYt=ρYt−4+ 0.9(Yt−1−ρYt−5) +ǫt. . . 139

Figure 4.12 Empirical Size v.s. κ1. . . 140

Figure 5.1 Time Path of Household Disposable Income Dt and Consumption ExpenditureCt: (a) in the Original Scale (b) in Natural logarithmic Scale . 146 Figure 5.2 Quarterly Subseries Plots for dt and ct. . . 147

Figure 5.3 Time Path of ct−dt: (a) Time Path for the Complete Series; (b) Quarterly Subseries Plots . . . 147

Chapter 1

Introduction

1.1

Statement of the Problem

Many time series display seasonality. Seasonality can be defined as a pattern which repeats at regular intervals every year. Seasonality comes from human activities and natural elements. For example, the demand for energy shows a seasonal pattern in that it is affected by the weather which depends on the time of a year. For economic time series, seasonality is quite common and economists usually employ seasonal differencing △s =Yt−Yt−s, where s is the seasonal period, to remove most or some

seasonal variation(see Box and Jenkins (1970)). When using seasonal differencing, the time series is assumed to be

Yt=Yt−s+ut, t= 1,2,· · ·, T, (1.1)

where ut is a stationary process. Seasonal differencing therefore renders the differ-enced time series to be stationary and sheds light on the model configuration.

The process in (1.1) can be expressed as a polynomial in the backward shift operator B, BjY

t=Yt−j for j = 0,1,2,· · ·,:

Generally, if the modulus of each root of Φ(B) is greater than one,Yt is a stationary process; otherwise, Yt is non-stationary. With Φ(B) = 1−Bs, there are s roots

at equidistant points on the unit circle. These roots are called seasonal unit roots. The process with seasonal unit roots is non-stationary and shows cyclical fluctuations with a length of s observations. Assuming that ut is a white noise series and s is an even number, the estimated spectrum ofYt should have distinct peaks at frequencies

ωj ≡ 2πj/s, (j = 0,· · ·, s/2) corresponding to roots of (1 −Bs). The estimated

spectrum for the series Yt = Yt−4 +ǫt, where ǫt is a white noise series, for example, has a peak at zero frequency, a peak at the annual frequencyπ/2 and a peak at the semiannual frequency π corresponding to the root 1, roots of ±i and the root −1 respectively. Note that 1−B4 can be expressed as

(1−B4) = (1−B)(1 +B+B2+B3) = (1−B)(1 +B)(1 +B2).

Accordingly, roots of±iand -1 are called unit roots at seasonal frequencies, when s=4. In Figure 1.1(a), four points represent the four distinct unit roots for Φ(B) = 1−B4.

Clearly, the points are equally spaced and on the unit circle. Figure 1.1(b) illustrates the estimated spectrum based onn= 1000 observations for the processYt=Yt−4+ǫt. It is obvious that the estimated spectrum only has peaks at zero, semiannual and annual frequencies.

Seasonal differencing could cause model misspecification. For example, the sea-sonal differencing is not appropriate if the process only has some of the seasea-sonal unit roots but not all of them. Predictions and tests based on an incorrect model can lead to improper decisions. So it is necessary to verify the need of seasonal differencing before applying the seasonal differencing filter. The seasonal unit root test is used to decide whether the series should be adjusted by the seasonal differencing filter 1−Bs

or not. For quarterly data, the seasonal unit root test is used to determine whether ±1 and ±i are roots for Φ(B), thus the null hypothesis is

(a)

0

200

400

600

800

1000

1200

frequency

spectrum

0 π 2 π

(b)

Figure 1.1: (a) Roots for Φ(B) = 1−B4; (b) Spectrum Estimates forY

t=Yt−4+ǫt

where ǫt i.i.d.N(0,1)

where ut is a stationary AR(p−4) process (where p > 4) or a white noise series. The alternative hypothesis is based on which seasonal unit root test is chosen. More details of the seasonal unit root test will be given in the next section.

1.2

Literature Review

There are many ways to detect the presence of seasonal unit roots. Such methods can be divided into two groups: regression-based tests and graphical tests. A brief review of the techniques in these two groups will be given below.

1.2.1

Regression-Based Tests

hypotheses considered. Some of the widely used regression-based tests are introduced below.

DHF

Dickey, Hasza and Fuller [DHF] (1984) extended the Dickey-Fuller [DF] single unit root test (1979) to seasonal unit root test by replacing Yt−1 with Yt−s in the regression model for regular unit root test. The DHF model is:

Yt=ρYt−s+ǫt, (1.3)

where ǫt are i.i.d. (0, σ2) random variables. It is clear that Y

t is non-stationary and

contains all seasonal unit roots whenρ= 1. Also, note thatYtis stationary if|ρ|<1. Accordingly, one can test ρ = 1 against ρ < 1 to find out whether the seasonal differencing filter of (1−Bs) makes the filtered process stationary. Generally, the

t-statistic for testing ρ= 1 is used as the DHF test statistic.

There are two different extensions of the above procedure to higher order AR processes which are in the form of (1.1) with the assumption that ut is a stationary AR(p− s) (p > s) process. Dickey, et al. (1984) suggested regressing Yt − Yt−s

on Yt−1−Yt−s−1,· · ·, Yt−(p−s)−Yt−p to estimate the parameters ˆκ1,· · ·,ˆκp−s for the AR(p−s) (p > s) process ut and then regressing its residuals on (1−κˆ1B − · · · −

ˆ

κp−sBp−s)Y

t−sand Yt−1−Yt−s−1,· · ·, Yt−(p−s)−Yt−p to obtain ˆρ−1 and the estimates

of κ1 −κˆ1,· · ·, κp−s − ˆκp−s. The t-statistic corresponding to the estimator ˆρ−1, therefore, can be used to test ρ= 1. Another extension is provided by Ghysels et al. (1994). They just used one regression model:

Yt−Yt−s =φ1Yt−s+κ1(Yt−1−Yt−s−1) +· · ·+κp−s(Yt−(p−s)−Yt−p) +ǫt,

difference. In addition, the use of correct augmentation, i.e. the right number of lags p for Yt (or p−s for ut), is important to the size and power of the test in finite samples.

Stationary processes with zero mean are not common in practice. If the process is stationary except for some non-zero deterministic terms but the deterministic terms are not included in estimation, the DHF regression estimate of ρ−1 will converge to zero in most cases and the test will have asymptotic power zero. Dickey et al. (1984) suggested using the modified DHF test which uses the regression model (1.3) with appropriate deterministic terms (e.g. a constant or seasonal means). Hylleberg (1992) recommended the inclusion of deterministic terms such as an intercept, sea-sonal dummies and trend. Unfortunately, the asymptotic distribution changes with the inclusion of deterministic terms.

The DHF regression model has only one lag variable in addition to some deter-ministic variables. It is relatively easy to obtain the estimators and is straightforward to interpret the results. For higher order models, people use the augmented DHF test procedure based on the model with additional lag variables. If ρ= 1, the asymptotic distributions for the test statistics are not affected by the augmented structure as-suming that appropriate number of lags are included. Therefore, the critical values obtained from the basic DHF regression model can be applied to the test statistics from the augmented model.

A limitation for the DHF test is that it is not appropriate for testing other types of unit roots, such as roots of ±i and −1 without root 1 for the quarterly unit root series. In Chapter 2, an interesting simulation result related to this drawback will be presented. The result indicates that the DHF power will not converge to one when the true model has only some unit roots but not all of them. We will call this the case of “partial” unit roots. In addition to the simulation study, the asymptotic distributions for the relevant DHF test statistics are derived to find the reason why the DHF test is not appropriate for testing partial unit roots. Another drawback of the DHF test is that its alternative hypothesis is a specific sth order AR process. For example, when s= 4 andρ <1, the roots for Φ(B) = (1−ρB4) = (1 +√ρB2)(1−√ρB2) are±ρ−1/4

and thus, the alternative does not include models with a few, but not all, roots under the null.

HEGY

Based on Lagrange approximation, Hylleberg, Engle, Granger and Yoo [HEGY] (1990) showed that any polynomial Φ(B) can be expressed in terms of elementary polynomials and a remainder as follows:

Φ(B) = −λ1B(1 +B)(1 +B2)−λ

2(−B)(1−B)(1 +B2)

−λ3(−B2)(1−B2)−λ

4(−B)(1−B2) + Φ∗(B)(1−B4)

(1.4)

where λ1 = −Φ(1)4 , λ2 = −Φ(4−1), λ3 =−Φ(i)+Φ(4 −i), λ4 =−Φ(i)−4Φ(−i)i and Φ∗(B)(1−

B4) is the remainder. Notice λ

1 = 0 if and only if 1 is one of the roots for Φ(B); λ2 = 0 if and only if -1 is one of the roots for Φ(B); λ3 = λ4 = 0 if and only if Φ(B) has the complex unit roots±i. Thus testing the presence of roots ±1 and±iis equivalent to testλi = 0 fori = 1,· · ·,4. Apply the polynomial approximation (1.4) to the seasonal time series:

Φ(B)Yt = −λ1B(1 +B)(1 +B2)Y

t−λ2(−B)(1−B)(1 +B2)Yt

−λ3(−B2)(1−B2)Y

t−λ4(−B)(1−B2)Yt+ Φ∗(B)(1−B4)Yt

(1.5)

With the assumption that the series is generated by Φ(B)Yt=ǫt, (1.5) is replaced by

Φ∗(B)△4Yt =λ1y1,t−1+λ2y2,t−1+λ3y3,t−2+λ4y3,t−1+ǫt, (1.6)

where

y1,t= (1 +B +B2 +B3)Y t, y2,t=−(1−B+B2−B3)Y

t, y3,t=−(1−B2)Y

t.

It is clear that y1,t, y2,t and y3,t remove all unit roots except root 1, -1, and ±i

respectively.

construc-tion, the design matrix is asymptotically orthogonal and thus 1

N2X′X is

asymptot-ically diagonal (Appendix A shows that y1,t, y2,t, y3,t and y3,t−1 are asymptotically uncorrelated). Furthermore, λ1 = 0, λ2 = 0 and λ3 = λ4 = 0 are equivalent to the existence of unit roots at zero, semiannual and annual frequencies respectively. Therefore, the HEGY approach can test the presences of unit roots at different fre-quencies independently. In other words, the HEGY method can test three exclusive hypotheses independently and separately:

H00 : presence of root 1 or unit root at zero frequency,

H01 : presence of root -1 or unit root at semi-annual frequency,

H02 : presence of roots±i or unit roots at annual frequency,

It is obvious that H0 : {presence of all four unit roots} = H00∩H01∩H02 and the test of H0 is the combination of the tests for H00, H01 and H02.

The test forH0i fori= 0,1,2 or any combination of them is equivalent to test the correspondingλ(s) is(are) zero. The test for presence of root 1 (H00) is equivalent to a test forλ1 = 0, and the test for presence of root -1 (H01) is equivalent to a test for

λ2 = 0. To test the presence of complex roots ±i (H02), a joint test of λ3 = λ4 = 0 is used. To test the presence of all unit roots at seasonal frequencies (H01∩H02), a joint test ofλ2 =λ3 =λ4 = 0 is employed. The process has no quarterly unit roots if and only if all λ’s are different from zero. Thus, HEGY allows an individual test for presence of unit root(s) at a specific frequency or unit roots at two (or three) different frequencies for quarterly data. This advantage of the HEGY test has made it become a popular seasonal unit root test. Many researchers have used or modified it. One of the well known modifications of the HEGY test for monthly data was proposed by Beaulieu and Miron (1993).

When Φ∗(B) in (1.6) is equal to one, the test statistics can be obtained by

re-gressing △4Yt on y1,t−1, y2,t−1, y3,t−2 and y3,t−1. In general, Φ(B)∗ 6= 1. Ghysels

et al. (1994) extended the HEGY test to higher order AR process by assuming Φ∗(B) = 1− Pp−4

i= 1,· · ·,4 obtained from the following augmented HEGY model:

△4Yt =λ1y1,t−1+λ2y2,t−1+λ3y3,t−2+λ4y3,t−1+κ1△4Yt−1+· · ·+κp−4△4Yt−(p−4)+ǫt.

(1.7) Psaradakis (1997) proposed another extension. Similar to the augmented DHF model proposed by Dickey et al (1984), Psaradakis’s approach obtains the initial estimation ofκ1,· · ·, κp−4 via a regression of△4Yt on△4Yt−1,· · ·,△4Yt−(p−4). If ˆκ1,· · ·,κˆp−4 are

the results from OLS, the auxiliary model for the HEGY test is

△4Y˜t=λ1y˜1,t−1+λ2y˜2,t−1+λ3y˜3,t−2+λ4y˜3,t−1+ǫt, (1.8)

where

˜

Yt= (1−κˆ1B −ˆκ2B2− · · · −κˆ

p−4Bp−4)Yt

˜

y1,t= (1 +B+B2+B3) ˜Y t,

˜

y2,t=−(1−B +B2−B3) ˜Y t,

˜

y3,t=−(1−B2) ˜Y t.

More discussion of the HEGY tests based on (1.7) and (1.8) will be given in Chapter 4.

To implement any of the above two augmented HEGY tests, it is necessary to choose the order for the autoregressive part. Ng and Perron (1995) [NP] explored the choice of the truncation lag order in context of the Said-Dickey test (1984) for the presence of root 1 in a general ARMA process. They favored the sequential test on the significance of the lag coefficients (in the regression model (1.7)) following a general to specific strategy (see also Hall, 1994). Hylleberg (1995) also advocated the general to specific strategy. However, the results reported by Taylor (1997) imply that the NP rule usually underestimates the lag structure when the model includes nonzero deterministic terms and the problem becomes worse with inclusion of more deterministic terms. As a result, Taylor suggested estimating the lag length without any deterministic components and then including relevant deterministic components in the test regression model of the estimated lag length.

relatively serious when the error is a MA process rather than a white noise series or an AR process. Both results in Ghysels et al. (1994) and Hylleberg (1995) showed that the empirical size is much higher than the specified nominal significance level when an MA root is close to one of the quarterly unit roots. Although the prewhitened modification of the HEGY test presented by Psaradakis is successful in reducing size distortion for finite samples, its empirical size increases as the sample size increases or more deterministic elements are added(see Table 2 in Psaradakis 1997).

Kunst

The regression model (1.6) with Φ∗(B) = 1 can be reparametrized to

Yt−Yt−4 = (λ1−λ2−λ4)Yt−1+(λ1+λ2−λ3)Yt−2+(λ1−λ2+λ4)Yt−3+(λ1+λ2+λ3)Yt−4+ǫt.

(1.9)

Dickey (1993) gave a short discussion on the independent variables in models (1.6) and (1.9). The independent variables in model (1.6) are Fourier transforms and he suggested that they have little economic interpretation. The variable structure in model (1.9) is relatively easy to understand. A general AR(s) model proposed by Kunst (1997) for testing Φ(B) = 1−Bs follows Dickey’s comments and is defined as:

Yt−Yt−s =θ1Yt−1+θ2Yt−2+· · ·+θsYt−s+ǫt. (1.10)

To test the null hypothesis of Yt−Yt−s=ǫt, Kunst estimatedθ’s by Ordinary Least Squares (OLS) and then compared the F-statistic for the test of θ1 = θ2 = · · · =

in (1.9). Therefore, the asymptotic distribution for the Kunst F-statistic is the same as the asymptotic distribution for the HEGY overall F-statistic derived by Ghysels, Lee and Noh (1994).

The regression model for the DHF test can be considered as a reduced model of the Kunst model since Kunst’s model includes s lagged terms (Yt−1,· · ·, Yt−s) andYt−s

is the single lag variable in the DHF model. However, the asymptotic distributions ofYt−s obtained from the DHF model and the Kunst model are much different under the null hypothesis (see Chapter 2 for details). The influence of the additional lag variables (Yt−1,· · ·, Yt−s+1) can be studied by comparing the DHF test with Kunst’s t-test. Chapter 2 will compare the asymptotic distributions of the t statistics on

Yt−4 obtained from the DHF model and the Kunst model for s = 4 case. Chapter 2 will also compare the performances of the DHF test and the modified Kunst test using the t statistic onYt−4 instead of the F statistic on all lag variables for quarterly time series. The comparisons will throw some light on the influence of the extra lag variables in Kunst’s model.

The augmented Kunst model proposed by Kunst is:

△sYt=θ1Yt−1 +θ2Yt−2+· · ·+θsYt−s+κ1△sYt−1+· · ·+κp△sYt−p+ǫt. (1.11)

When s= 4, model (1.11) is only a linear transformation of model (1.7):

△4Yt = θ1Yt−1+θ2Yt−2+θ4Yt−3+θ4Yt−4+κ1△4Yt−1+· · ·+κp△4Yt−p+ǫt

= (λ1−λ2−λ4)Yt−1+ (λ1+λ2−λ3)Yt−2

+(λ1−λ2+λ4)Yt−3+ (λ1+λ2+λ3)Yt−4

+κ1△4Yt−1+· · ·+κp△4Yt−p+ǫt

Therefore, Kunst’s augmented model is also a reparametrized augmented HEGY model in the form of (1.7). Since Kunst’s model is a reparametrized HEGY model, it can also be extended to the higher order AR process using the transformation of (1.8):

where ˜Yt is the same as the one defined in (1.8). The performances of the two augmented models for the modified Kunst test will be compared in Chapter 4.

OCSB

Osborn, Chui, Smith and Birchenhall [OCSB] (1988) modified the Hasza and Fuller test (1982) for the presence of multiplicative differencing filter △1△s.

Ro-drigues and Osborn (1999) pointed out that the OCSB can also be applied to test the presence of 1−Bs through the regression model

△sYt =β1(Yt−1+· · ·+Yt−s+1) +β2Yt−s+ǫt. (1.12)

The overall F statistic for testing β1 = β2 = 0 is used to test the presence of all seasonal unit roots, and the t statistic onβ1 relates to the test of the null hypothesis that no intermediate (nonseasonal) lag is involved in the data generation.

Note that the original OCSB regression model is

△1△sYt=β1△sYt−1+β2△1Yt−s+ǫt, (1.13)

and it is used to test whether△1△sis a factor of Φ(B). The regression model (1.12) is

obtained from model (1.13) and assuming△1 is valid. Therefore the OCSB seasonal unit root test does not allow explicit testing against stationarity.

Comparing model (1.10) with (1.12), it is clear that model (1.12) is also a restricted form of Kunst’s regression model with θ1 = · · · = θs−1. The restriction has non-trivial asymptotic implications(see Osborn and Rodrigues 2002). The asymptotic distributions of θs and β2 are quite different.

CH

Hylleberg (1995) suggested applying both the CH and HEGY tests if possible because they complement each other in some respects.

Consider a regression model:

Yt=µ+Vt′α+ft′γt+ǫt, (1.14)

with

γt=γt−1+ut, (1.15) whereVtis ak×1 vector of explanatory variables which are not collinear withft′γt,ft

is a s−1 vector with fjt′ = (cos((2j/s)πt),sin((2j/s)πt)) for 2j < s and fjt = (−1)t

for 2j =s, ǫt is a random series. Under the null, the series is stationary and ut is a vector of 0. If Yt has all seasonal unit roots, ut is a vector of i.i.d. random variables (note that ǫt and ut are independent). Notice that γt is also a s−1 vector. If Yt is stationary, γjt is the parameter for fjt and corresponds to the seasonal cycle at the frequency (2j/s)π. With the set up of (1.14) and (1.15), E(utu′t) = 0 implies that

γt=γ0 (i.e. γt is a constants−1 vector) and Yt is stationary. IfE(utu′t)>0, γt is a vector of random walks and Yt must have all seasonal unit roots.

To allow for testing the presence of any subset of the unit roots at seasonal fre-quencies, the assumption (1.15) is modified as

A′γt=A′γt−1+A′ut, (1.16)

where A is a (s−1)×(s−1) matrix with rank equal to a and a is the number of roots for testing stationarity. Most of the elements inAare zero except the elements on the diagonal which correspond to the elements in γt for the stationarity test. On quarterly data, for example, set A = I3 to test for the presence of all seasonal unit

presence of roots ±i, whereA1 and A2 are defined as

A1 =

1 0 0 0 1 0 0 0 0

,A2 =

0 0 0 0 0 0 0 0 1

.

As before, the test that the roots defined byAare outside the unit circle is equivalent to testing E(A′utu′tA) = 0.

The CH test statistic for testing E(A′utu′tA) = 0 is

L(j/q)π = 1

T2tr (A

′σˆfA)−1A′XT t=1

ˆ FtFˆ′tA

! ,

where ˆFt = Pt

i=1fieˆi, ˆei are the OLS residuals from (1.14) and ˆσf is obtained by

Kernel estimation:

ˆ

σf =

m X

i=−m k i m 1 T X j

fj+ieˆj+ifi′eˆi.

The applied kernel k(.) can be the Bartlett, Parzen, or quadratic spectral. Under the null hypothesis, the roots defined in A are outside the unit circle and the test statistic L(j/q)π has the following asymptotic distribution

L(j/q)π → Z 1

0

W′a(t)Wa(t)dt,

whereWa is a vector of standard Brownian Motion of dimensionaand we use “→” to

denote convergence in distribution. Accordingly, the asymptotic distribution under

H0 only depends on the rank of A or the number of roots for testing stationarity.

1.2.2

Graphical Test

0 10 20 30 40

−4

−2

0

2

4

Seasonal random walks

t

Z

(a)

0 10 20 30 40

−6

−4

−2

0

2

4

6

Pure seasonal means with noise

t

Y

(b)

Figure 1.2: The Run Sequence Plots for (a) Zt=Zt−4+ǫt; (b) Yt= 5×sin(π 2t) +ǫt Run Sequence Plot

In a run sequence plot, the Y axis is the time series and the X axis is the time index. The run sequence plot is the first step for analyzing any time series. It provides understanding on the behaviors of the trend, seasonal, and irregular components. Figure 1.2 (a) is the run sequence plot for the series of a quarterly random walk and shows periodic behavior. However, Figure 1.2 (b) also shows periodic behavior while the series is generated by pure deterministic means with white noise. As a result, it is difficult to determine whether a series needs a seasonal differencing filter only by checking the run sequence plot.

Seasonal Subseries Plot

Seasonal random walks

mod(t,4)

Z

1 2 3 0

−10

−5

0

5

(a)

Pure seasonal means with noise

mod(t,4)

Y

1 2 3 0

−5

0

5

(b)

Figure 1.3: The Seasonal Subseries Plots for (a)Zt =Zt−4+ǫt; (b)Yt= 5×sin(π 2t)+ǫt

periods are not known, an autocorrelation plot or spectral plot can be applied to find it.

Figure 1.3 (a) and (b) are the subseries plots for the same series in Figure 1.2 (a) and (b) respectively. Since the data are simulated as quarterly time series, each tick mark on the horizontal axis is the remainder from the division of the time index by 4. Displaying the sample mean for each group (or season), both (a) and (b) in Figure 1.3 show the seasonal patterns more clearly than Figure 1.2 (a) and (b). The subseries plots in (a) look like random walks which have increasing variance as the series evolves while the subseries plots in (b) display stable variation within group (or season). It is quite evident that the series displayed in (b) is stationary except for differences in mean between any two different subseries and the series shown in (a) is non-stationary and needs more investigation on the selection of differencing filters.

Autocorrelation Plot

the sample autocovariance obtained from

ˆ

C(k) = 1

T T−k

X

t=1

(Yt−Y¯)(Yt+k−Y¯) and ¯Y = 1

T T X

t=1 Yt.

Note that some people may use 1

T−k instead of 1

T in the calculation of ˆC(k). The

sample autocovariances obtained by these two methods are asymptotically equivalent whenT is large andk is small relative toT. With the above definition of the vertical axis, it is intuitive to use the time lag as the horizontal axis.

The ACF plot can provide visual evidence for the tests of randomness and sta-tionarity. If the series is white noise, the autocorrelations should be near zero for non-zero time lags. To provide a visual check for randomness, two dashed lines are generated to show the 95% confidence band. The confidence band is defined as the vertical area within [−√1.96

T , 1√.96

T]. In this case, the confidence band has fixed width

that depends on the sample size. Therefore, most autocorrelations should be within the conficence band when the series is white noise. If the series is stationary, the autocorrelations should converge to zero very fast as the time lag increases. In the case of stationarity, people can find a lagk such that the autocorrelations for the lags greater than k are all within the 95% confidence band for the randomness test. If the series is non-stationary, the absolute value of such autocorrelations will not decay exponentially as the time lag goes up and we expect to see some autocorrelations for large time lags outside the confidence band.

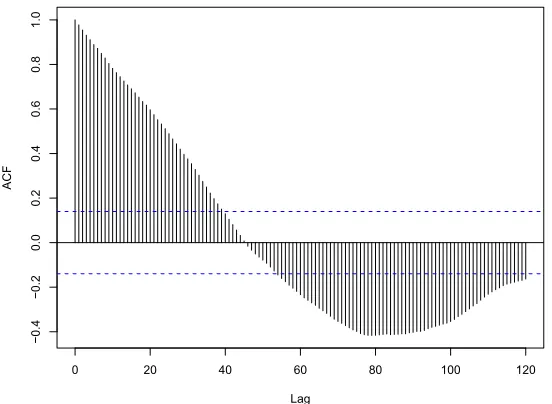

Figure 1.4 presents the ACF plots for a seasonal random walk in (a) and a series of pure seasonal means and noise in (b). In Figure 1.4 (a), the value of ACF is large and slowly decreases only if the lag is a factor of 4 and the ACF of the 48th lag is

still over the 95% confidence band (the area within the dashed lines) for randomness check. It is obvious that the ACF in Figure 1.4 (b) changes sign in a regular way. The ACF is positive when the lag is a factor of 4, negative when the lag is a factor of 2 but not a factor of 4, and 0 at odd lags. Unlike the ACF in (a), the absolute value of ACF in (b) is large and slowly decreases only if the lag is a factor of 2.

0 10 20 30 40 50

−0.2

0.0

0.2

0.4

0.6

0.8

1.0

Lag

ACF

(a)

0 10 20 30 40 50

−1.0

−0.5

0.0

0.5

1.0

Lag

ACF

(b)

Figure 1.4: Autocorrelation Plots for series (a)Zt=Zt−4+ǫt; (b)Yt = 5×sin(π 2t)+ǫt

1.6 for the series shown in Figure 1.4 (a) and (b) respectively. The ACF plots in Figure 1.5 have different patterns but all of them exhibit non-stationary behavior as the absolute value of the ACF decreases slowly with increasing lag. On the other hand, the ACF plots in Figure 1.6 look similar and the ACFs are within the 95% confidence band for the randomness check when the lags are greater than zero. The ACF pattern shown in Figure 1.6 implies that the series is stationary and the non-stationary ACF pattern for the whole series displayed in Figure 1.4 (b) is induced by seasonal deterministic components.

0 10 20 30 40 50

−0.5

0.0

0.5

1.0

Lag

ACF

(a)

0 10 20 30 40 50

−0.4

−0.2

0.0

0.2

0.4

0.6

0.8

1.0

Lag

ACF

(b)

0 10 20 30 40 50

−0.2

0.0

0.2

0.4

0.6

0.8

1.0

Lag

ACF

(c)

0 10 20 30 40 50

−0.4

−0.2

0.0

0.2

0.4

0.6

0.8

1.0

Lag

ACF

(d)

Figure 1.5: Seasonal Subseries Autocorrelation Plots for Seasonal Random WalkZt=

Zt−4 +ǫt: (a) mod(t,4)=1; (b) mod(t,4)=2; (c) mod(t,4)=3; and (d) mod(t,4)=0

odd. If the series has roots ±i, the ACF of y3,t, ρ4(k), is approximate to

ρ4(k) =

0, k is odd −1, k/2 is odd 1, k/2 is even

These results imply that sample ACFs ofy1,t, y2,t and y3,t will oscillate with period-icity i, i = 1,2,4 about a slow linear decay under H00, H01 and H02 defined in the HEGY test. Taylor and Leybourne used i׈ci/T for i = 1,2,4 as the test statistics to test H00,H01 and H02 respectively. The value of ˆci is the lag order first satisfying

ˆ

0 10 20 30 40 50

−0.2

0.0

0.2

0.4

0.6

0.8

1.0

Lag

ACF

(a)

0 10 20 30 40 50

−0.2

0.0

0.2

0.4

0.6

0.8

1.0

Lag

ACF

(b)

0 10 20 30 40 50

−0.2

0.0

0.2

0.4

0.6

0.8

1.0

Lag

ACF

(c)

0 10 20 30 40 50

−0.2

0.0

0.2

0.4

0.6

0.8

1.0

Lag

ACF

(d)

Figure 1.6: Seasonal Subseries Autocorrelation Plots for Stationary Process Yt = 5×sin(π

2t) +ǫt: (a) mod(t,4)=1; (b) mod(t,4)=2; (c) mod(t,4)=3; (d) mod(t,4)=0

the correspondingi׈ci/T is less than the critical value. Figure 1.7, 1.8 and 1.9 show the sample ACFs ˆρi for a simulated quarterly random walkZt=Zt−4+ǫt of size 200 which is the same series for the Figure 1.4 (a) and 1.5. From Figure 1.7 to 1.9, it is trivial to find ˆc1 = 46, ˆc2 = 78 and ˆc4 = 124. All the three test statistics i׈ci/T

are greater than the critical values at 5% level in Table 1 of Taylor and Leybourne (1999). In this case, the null is not rejected and this is a correct decision.

1.3

Summary of Chapters

0 20 40 60 80 100 120

−0.4

−0.2

0.0

0.2

0.4

0.6

0.8

1.0

Lag

ACF

Figure 1.7: Autocorrelation Plots for Testing Root 1 (ˆρ1)

0 20 40 60 80 100 120

−1.0

−0.5

0.0

0.5

1.0

Lag

ACF

0 20 40 60 80 100 120 140

−1.0

−0.5

0.0

0.5

1.0

Lag

ACF

Figure 1.9: Autocorrelation Plots for Testing Roots ±i (ˆρ4)

Chapter 2

In this chapter, two modified tests are developed to extend the existing methods. The two tests are modified from the HEGY and Kunst tests. A comparison of the two modified tests, the DHF test and the overall HEGY F test is presented. First, we will discuss the asymptotic distributions of these test statistics under (1) the null hypothesis, (2) the alternative hypothesis of the DHF test, and (3) the alternative hypothesis of the modified HEGY test. Then the simulation results including (1) em-pirical percentiles for the test statistics under the null hypothesis, (2) emem-pirical powers for test statistics based on the models including different deterministic components, and (3) empirical powers for the model with misspecified deterministic components, are provided.

Chapter 3

are stationary and 37 series are non-stationary) are generated to understand the prop-erties of the two multiple-step test procedures. According to the results of empirical power, which is the probability of rejecting the null when the null is not true, both multiple-step test procedures are superior to the DHF test but not much different from the Kunst t test and the HEGY test that combines the results of its subtests. According to the empirical sensitivity to the correct model, which is the conditional probability of choosing the right model given the null is rejected, the two-step test procedure is better than the three-step test procedure and it is asymptotically equiva-lent to the HEGY test. With the simulation results, we also discover some properties of the DHF, Kunst t and HEGY tests.

Chapter 4

The models in Chapter 2 assume that ut in (1.2) is a white noise series. In Chapter 4, we extend our studies by allowingut to be a stationary AR(p−4) (p >4) process. We focus on the case that ut is a stationary AR(1) process and Yt satisfies

Chapter 5

Chapter 2

A Comparison of Seasonal Unit

Root Test Criteria

2.1

Motivations and Modifications

The DHF test is a test of seasonal non-stationarity against a special seasonal stationarity. If only partial seasonal unit roots are present in Φ(B), its null and alternative hypotheses are both false. The results of Ghysels, Lee and Noh(1994) and Taylor (2003) imply that the DHF test has a non-zero probability of accepting the null hypothesis that the series admits all seasonal unit roots while the series only has partial seasonal unit roots. Taylor also provided large sample distributions of the DHF test statistics when the series is a random walk and thus validated that the DHF test can not distinguish between Yt = Yt−4 +ǫt and Yt =Yt−1+ǫt. To extend previous findings, we modify the HEGY model to test the presence of unit roots ±1 and ±i against the presence of unit roots ±1 only.

Consider the process

in (1.2). The polynomial Φ(B) for this process is

Φ(B) = 1−αB2−βB4 = (1−B2)(1 +βB2),

and the roots of Φ(B) are

±1 and ±q−1/β, β 6= 0,1 (or α∈(0,1)∪(1,2)) ±1, β= 0 (or α= 1)

±1 and±i, β= 1 (or α= 0)

To get a more intuitive expression, subtract Yt−4 from both sides of (2.1):

Yt−Yt−4 =α(Yt−2−Yt−4) +ut. (2.2)

It is trivial to see that the value of α in model (2.2) plays a critical role. When

α= 0, the process is generated by (1.2) and admits all four distinct unit roots; When

α∈(0,2) (orα >0), the process is still nonsationary but only admits unit roots±1. Consequently, the test of α = 0 against α > 0 is equivalent to the test of presence of roots ±1 and ±i against presence of roots ±1. It is obvious that model (2.2) is a reduced form of model (1.6). We call this test modified HEGY test throughout this study.

Unlike the DHF test, the modified HEGY test is a right tail test and does not allow testing against stationarity. An exploration of the properties of the DHF test statistics under the modified HEGY hypothesis can help us thoroughly understand why the DHF test does not have asymptotic power one when the series only has unit roots±1. On the other hand, the modified HEGY model is a reduced HEGY model and the independent variables in the HEGY model are asymptotically independent. A study of the properties of the modified HEGY test can reveal the properties of the HEGY subtest on H02.

introduced that Kunst’s model is a reparametrized HEGY model. From (1.9), it is trivial to find

θ1 =λ1−λ2−λ4;

θ2 =λ1+λ2−λ3;

θ3 =λ1−λ2+λ4;

θ4 =λ1+λ2+λ3.

λ’s are the coefficients in the HEGY model. λ1 = 0, λ2 = 0 and λ3 = λ4 = 0 are equivalent to the presence of root 1, -1 and ±i respectively. With the assumption

θ1 =θ2 =θ3 = 0, (2.3)

θ4 = 0 is equivalent to the presence of roots 1, -1 and ±i. θ4 <0 implies that at least one of λi for i = 1,2,3 is less than zero and thus the corresponding H0j (j = i−1) and H0 are rejected (see the definition of H0j on page 7). According to these facts, we use the t-statistic to testθ4 = 0 as the test statistic instead of using the F-statistic (F1234)to test θ1 =θ2 =θ3 =θ4 = 0. Although the t test may be not as powerful as the F test if the assumption (2.3) can not be ensured, the empirical results in Section 2.3 will show that τθ4=0 is usually preferred to F1234 for finite samples. In this study, the comparison betweenτθ4=0 andτρ=1 (whereρis defined in (1.3)) is used to validate the significance of the additional variables, Yt−1, Yt−2 and Yt−3. To be distinguished from the original Kunst test, the modified test is called Kunst’s t test in this paper.

2.2

Asymptotic Distributions

This section will provide and discuss the asymptotic distributions of the relative test statistics under the null hypothesis and the alternative hypotheses of the DHF and modified HEGY tests. The asymptotic distributions offer a good understanding of large sample behaviors for the tests under analysis.

2.2.1

Under the Null Hypotheses

To simplify the presentation, let {ut} in (1.2) be a white noise series, i.e. ut =ǫt

and ǫt ∼i.i.d.(0, σ2). The series is a seasonal random walk and can be divided into

four independent random walks:

X1,n =Yt =X1,n−1+u1,n and u1,n =ǫt, mod(t,4) = 1;

X2,n =Yt =X2,n−1+u2,n and u2,n =ǫt, mod(t,4) = 2;

X3,n =Yt =X3,n−1+u3,n and u3,n =ǫt, mod(t,4) = 3;

X4,n =Yt =X4,n−1+u4,n and u4,n =ǫt, mod(t,4) = 0.

For convenience, these Xi’s and ui’s are used to derive the relevant asymptotic dis-tributions. In the following proofs, some asymptotic results from previous work are directly used without giving full proofs. These results are summarized in Appendix B. The number of observations for {Yt} is T = 4N and thus the size of {Xi,n} for

i = 1,· · ·,4 is N. In this section, three scenarios for the deterministic components are considered: (1) zero mean; (2) seasonal means; (3) seasonal means and a single trend.

Scenario 1: Zero Mean Models

• N(ˆρ−1) andˆτρ=1

Let ˆρ and ˆτρ=1 denote the estimator and t-statistic from model (1.3) withs = 4. The estimate ofρ−1 in the DHF regression model is given by

ˆ

ρ−1 =

P

Yt−4(Yt−Yt−4)

P Y2

Under H0, Yt−Yt−4 =ǫt, we have

ˆ

ρ−1 =

P Yt−4ǫt P

Y2 t−4

=

P

{X1,n−1u1,n+X2,n−1u2,n+X3,n−1u3,n+X4,n−1u4,n} P

{X2

1,n−1+X22,n−1+X32,n−1+X42,n−1}

= 1

N 1 N

P

{X1,n−1u1,n+X2,n−1u2,n+X3,n−1u3,n+X4,n−1u4,n} 1

N2

P

{X2

1,n−1+X22,n−1 +X32,n−1+X42,n−1}

From Lemma B.1 (see Appendix B), the asymptotic distribution forN(ˆρ−1) is

N(ˆρ−1)→

P4 i=1

R1

0 Wi(t)dWi P4

i=1 R1

0 Wi2(t)dt

, (2.4)

where Wi(t) ∼ N(0, t) and are independent of Wj(t) if i 6= j, and we use “→” to denote convergence in distribution throughout this chapter. The sample t-statistic for testingρ = 1 is calculated by

ˆ

τρ=1 = q ρˆ−1

ˆ

σ2/P

{X2

1,n−1 +X22,n−1+X32,n−1+X42,n−1}

=

1 N

P

{X1,n−1u1,n+X2,n−1u2,n+X3,n−1u3,n+X4,n−1u4,n} q

1 N2ˆσ2

P

{X2

1,n−1+X22,n−1+X32,n−1+X42,n−1} ,

where ˆσ2 = 1 T−2

P

(Yt−ρYˆ t−4)2 →P σ2 and “→P ” denotes convergence in probability

throughout this chapter. With the results from (2.4), it is easy to see that,

ˆ

τρ=1→ P4

i=1 R1

0 Wi(t)dWi q

P4 i=1

R1

0 Wi2(t)dt

(2.5)

• Nθˆ4 and ˆτθ4=0

asymptotically orthogonal, it is relatively simple to derive the asymptotic behavior of ˆθ4 from the asymptotic results of the HEGY estimates.

According to the comparison between the HEGY reparametrization model shown in (1.9) and Kunst’s model, it is easy to observe that λ1+λ2+λ3 = θ4. The linear relation betweenθ’s andλ’s implies that the OLS estimate, ˆθ4, can be obtained by the sum of the OLS estimates, ˆλ1, ˆλ2 and ˆλ3. The asymptotic distributions of Nθˆ4 and ˆ

τθ4=0 can be derived from the asymptotic results given by Beaulieu and Miron (1992). In particular, when s= 4, the asymptotic results forNλˆ’s and the corresponding ˆτ’s are

Nλˆ1 → 4 R1

0 B1(t)dB1

16R01B2 1(t)dt

, τˆλ1 →

R1

0 B1(t)dB1

q R1

0 B 2 1(t)dt

Nλˆ2 → 4 R1

0 B2(t)dB2

16R01B2 2(t)dt

, τˆλ2 →

R1

0 B2(t)dB2

q R1

0 B 2 2(t)dt

Nλˆ3 → 2 R1

0 B3(t)dB3+

R1

0 B4(t)dB4

4R01(B2

3(t)+B42(t))dt

, τˆλ3 →

R1

0 B3(t)dB3+

R1

0 B4(t)dB4

[R01(B2

3(t)+B42(t))dt]1/2

Nλˆ4 → 2 R1

0 B4(t)dB3−

R1

0 B3(t)dB4

4R01(B2

3(t)+B42(t))dt

, τˆλ4 →

R1

0 B4(t)dB3−

R1

0 B3(t)dB4

[R01(B2

3(t)+B42(t))dt]1/2

Bi(t)∼N(0, t) and are defined as the following functions of Wi’s:

B1(t) = 1

2(W1(t) +W2(t) +W3(t) +W4(t)) B2(t) = 1

2(−W1(t) +W2(t)−W3(t) +W4(t)) B3(t) = √1

2(W2(t)−W4(t)) B4(t) = √1

2(W1(t)−W3(t))

With the construction of the HEGY variables, the cross product of the resulting design matrix is asymptotically orthogonal when normalized by N2. Consequently,

the variance of ˆθ4 is approximately the sum of variances of ˆλ1, ˆλ2 and ˆλ3, and the asymptotic distributions for Nθˆ4 and its t-statistic are

Nθˆ4 → 4 R1

0 B1(t)dB1

16R1

0 B12(t)dt

+ 4

R1

0 B2(t)dB2

16R1

0 B22(t)dt

+ 2

R1

0 B3(t)dB3+ R1

0 B4(t)dB4

4R1

0(B32(t) +B42(t))dt

and

ˆ

τθ4=0 →

4R01B1(t)dB1

16R01B2 1(t)dt

+4

R1

0 B2(t)dB2

16R01B2 2(t)dt

+ 2

R1

0 B3(t)dB3+

R1

0 B4(t)dB4

4R01(B2

3(t)+B42(t))dt

×qR1

0(16B12(t) + 16B22(t) + 4B23(t) + 4B42(t))dt

(2.7)

• Nαˆ and ˆτα=0

ˆ

α and ˆτα=0 are estimator and t-statistic in the regression model (2.2). The OLS estimate ˆα in the modified HEGY model can be obtained by

ˆ

α=

P

(Yt−2−Yt−4)(Yt−Yt−4)

P

(Yt−2−Yt−4)2

With the assumption that Yt is generated by Yt=Yt−4+ǫt, ˆα is equal to

ˆ

α =

P

(Yt−2−Yt−4)ǫt

P

(Yt−2−Yt−4)2 =

=

P

{(X1,n−X3,n−1)u3,n+(X2,n−X4,n−1)u4,n+(X3,n−1−X1,n−1)u1,n+(X4,n−1−X2,n−1)u2,n}

P

{(X1,n−X3,n−1)2+(X2,n−X4,n−1)2+(X3,n−1−X1,n−1)2+(X4,n−1−X2,n−1)2}

According to Lemma B.2 in Appendix B, the numerator isOp(N). When divided by N, the numerator will converge as follows:

1

N

P

{(X1,n−X3,n−1)u3,n+ (X2,n−X4,n−1)u4,n+ (X3,n−1−X1,n−1)u1,n+ (X4,n−1−X2,n−1)u2,n}

→R01W1(t)dW3+

R1

0 W2(t)dW4+

R1

0 W3(t)dW1+

R1

0 W4(t)dW2−

P4

i=1

R1

0 Wi(t)dWi;

moreover, the denominator converges at rateN2: 1

N2

P

{(X1,n−X3,n−1)2+ (X

2,n−X4,n−1)2+ (X3,n−1−X1,n−1)2+ (X4,n−1−X2,n−1)2} →2{R1

0(W1(t)−W3(t))2dt+ R1

0(W2(t)−W4(t))2dt}

Combine the limits of both denominator and numerator:

Nαˆ →

R1

0 W1(t)dW3+ R1

0 W2(t)dW4+ R1

0 W3(t)dW1+ R1

0 W4(t)dW2−P4i=1 R1

0 Wi(t)dWi

2{R1

0(W1(t)−W3(t))2dt+ R1

0(W2(t)−W4(t))2dt