Issues

ISSN: 2146-4138

available at http: www.econjournals.com

International Journal of Economics and Financial Issues, 2016, 6(1), 301-307.

Mediation Effects of Firm Leverage in Malaysia: Partial Least

Squares - Structural Equation Modeling

Nur Ainna Ramli

1, Gilbert Nartea

2*

1Faculty of Economics and Muamalat, University Sains Islam Malaysia, 71800, Bandar Baru Nilai, Negeri Sembilan, Malaysia, 2Lincoln University, Faculty of Commerce, Department of Accounting, Economics and Finance, 7647, Lincoln, Canterbury,

New Zealand. *Email: [email protected]

ABSTRACT

In theory, capital structure determinant is a cause-effect model. We investigate the simultaneously of cause-effect framework on the impact of specific attributes on firm’s financial performance through leverage which acts as a mediation variable. We use the partial least squares - structural equation modeling that capable of providing a greater understanding of the prediction for the construct relationship among each other with simultaneous techniques with only one time process (Chin, 1998). We endeavor to examine in a complex model that consists with 14 construct (LVs) and 33 indicators in Malaysia for the period from 1990 to 2010. The implication is that the Malaysian firms could attempt to choose less risky route, as Malaysia is recognized as a “market-based oriented.” In addition, we find that some attributes could influence the relationship to firm’s financial performance by indirect effect (leverage). Thus, firms tend to act with partial action on their capital structure, which believe to attain a sustainable performance.

Keywords: Capital Structure, Partial Least Squares, Structural Equation Modeling, Mediation Effects

JEL Classifications: G32, F62

1. INTRODUCTION

Previous studies indicate that the capital structure of a firm is not only determined by the firm’s specific factors, but also can be influenced by the macro-economics’ specific factors. In

capital structure theory, the essential aspect is that many of the determinants of capital structure are considered as non-directly

observed variables or latent variables, i.e., there will be no single accounting indicator that can be used exactly in representing the attributes or factor in capital structure determinants (Titman and Wessels, 1988). Most literature shows that the traditional ordinary least square method was often used in capital structure research, which only takes a single accounting indicator to represent each attribute instead of considering one or more accounting indicators (often related with proxies) for each attribute. For example, asset structure (AS) variable was measured by calculating tangibility assets that consist of property, plant and equipment to total assets. However, it should also calculate the collateral value (CV), which includes the inventories and the gross plant and equipment to total assets. This is because the firm’s assets may affect the choice of

capital structure, as it can be considered as a secured debt to avoid

the cost of issuing securities, and can maximize its benefit as collateral for debt. Therefore, this study intends to use the partial least squares - structural equation modeling (PLS-SEM) approach, which extends to discern the latent construct that can be ascertained by a variation of single and multiple observable indicators or proxies. This approach can also overcome any multicollinearity that normally happens in traditional regression.

Review of international studies shows that the debt level to the

the shareholders’ perspective (Gleason et al., 2000). Hence, this study intends to demonstrate the corporate leverage in three ways: (i) How the leverage influence the firm’s financial performance; (ii) how the firm and macro-economic attributes can affect the firm’s performance directly; and (iii), whether leverage financing

may indirectly influence such a relationship. For instance,

although the use of a higher leverage or a lower equity capital ratio can increase the firm’s performance (particularly the value for shareholders), the firms may also consider investing in fixed assets in order to enhance the shareholders’ wealth. In other words, the role of asset tangibility as collateral in borrowing might lead to enlargement of the firm’s performance via increases in its leverage, rather than using internal financing to invest in business operations.

Specifically, in theory, capital structure determinant is a cause-effect model. This study is fairly complex, with a large number of latent construct and indicators. Thus, this researcher is motivated to investigate the determinants of capital structure in a comprehensive approach by scrutinizing the overall of firm- and macro-economic- specific factors in order to obtain high profits and consequently enhance the value for shareholders. This study uses the PLS modeling approach, which is consistent with the SEM precepts, capable of providing a greater understanding of the prediction for the construct relationship among each other with simultaneous techniques with only one time process (Chin, 1998).

As far as this researcher is aware, none of the previous studies have

examined the overall model of capital structure determinant and the firm’s financial performance simultaneously. To date, multi-group

comparison of PLS model for different sample population in which

to comprehend the differences in the path estimates coefficient

is still relatively naive. Apart from that, none of the literature

that this researcher has reviewed has extended capital structure determinants to the firm’s financial performance in Malaysia.

In the analysis of indirect or mediating impact of leverage between the capital structure determinant and the firm financial performance, it is observed that there is a sign that leverage is acting to mediate the role to those relationship for Malaysia. The result is consistency with Ramadhan et al. (2012) who investigated the mediating role in the UK that shows a similar finding for Malaysia, in which the firms’ manager has to make appropriate capital structure choices in order to enhance the firm’s financial

performance, as the debt level has act to mediate the role for those relationships.

The paper is organized as follows: Section 2 discusses the

literature and hypotheses for the measurement of capital structure

determinants; Section 3 explains the methodology of the PLS-SEM approach; Section 4 presents the empirical result analysis;

Section 5 provides the discussion and the conclusion of the study.

2. CAPITAL STRUCTURE DETERMINANTS

AND HYPOTHESES

In principle, capital structure or firm leverage is the effect caused

by its determinants and thus, this relationship of cause and effect in determinant of capital structure is framed by the causal model

such as the SEM in a comprehensive framework. Leverage under the capital structure is essential because it can affect a firm’ returns, as well as evaluating the ability of the firm in the competitive environment. The measurement of the leverage is closely related to agency theory (AT), which implies that shareholders can sustain their control in the firm if the firm can earn higher income from the project by debt, and the owner of the capital will get the benefit of this return. In the US, it is common to define the capital structure of the long term debt ratio (Harris and Raviv, 1991). Conversely, in Asian markets, most companies use both long term and short term debts in financing their assets, including current assets, in order to exemplify how much leverage is being used by the companies. Harris and Raviv (1991) state that definition of leverage is dependent on the research objective itself. Existing studies in the capital structure perspective assume to gauge a different measurement for leverage. Therefore, this researcher intends to use both market and book value since this is the best

appropriate measurement to view in simultaneous method1. In

addition, this study separates the dependent variable into two

models (i.e., Model A and Model B). Model A will report on the measurement of leverage by computing all the measurements that earlier studies have done, including total debt ratio, debt to capital, long term and short term debt to capital including book value and market value, correspondingly (Fan et al., 2010; Mustapha et al., 2011; Titman and Wessels, 1988). Model B, will exclude the short

term debt to capital and total debt ratio.

The relationship between leverage and a firm’s financial performance is a central point in addressing the agency cost.

Previous studies showed contradictory results about the

relationship between leverage of a firm and the firm’s performance. McConnell and Serves (1995) and Dessi and Robertson (2003), using the US and UK sample firms, respectively, split the data into “low growth” and “high growth” for the indicator of firm’s performance of Tobin’s Q, with a range of variables including debt. They found different results in their findings. McConnell and Serves (1995) claim that low growth firms tend to have less

debt in their capital structure, which is consistent with2 Jensen’s

free cash flow hypothesis but contrasts with Dessi and Robertson (2003). McConnell and Serves (1995) also find that high growth firms are consistent with the Myers (1977) hypothesis that “too much” debt induces managers (acting in shareholders’ interests)

to by-pass positive net present value projects.

The capital structure determinants that are to be tested for

the interrelationship between capital structure and level of

1 The arguments of using market and book value are numerous and even raise controversy regarding the appropriateness for the leverage measurement. Since market value is more realistic as it is closer to the intrinsic firm value and reflect to the potential future leverage. On the other hand, book value captures the better measure in the asset value and not the growth option investment that reflect by current market value (Barclay et al., 2006). 2 According to Jensen’s hypothesis, debt may act as a valuable managerial

performance are: (i) Firm attributes (i.e., AS, growth opportunities, firm size [FS], business risk [BR], liquidity, non-debt tax shield [NDTS]) and, (ii) macro-economic attributes (i.e., bond market development (BMD), stock market development (SMD), economic growth (EG), interest rate (IR), and inflation rate). Therefore, it is hypothesized capital structure (leverage) has a mediation/indirect effect on firm- and macro-economic attributes and firm financial

performance. Table 1 summarizes the expected relationship between firm-and macro-economic attributes to capital structure and firm financial performance.

3. METHODOLOGY

A unique determinant of a firm’s capital structure in the capital structure theory is often non-directly observed (latent variable). It means that accounting proxies cannot be exactly represented

for each of the capital structure attributes3. This study uses

PLS-SEM approach in the Smart PLS software 2.0 M3, which conceptually and practically simplifies and combines the multiple regressions and principle component analysis (PCA), but not particularly allow the complex cause and effect model evaluation relationship between construct (Hair et al., 2011). Hence,

PLS-3 The latent firm attributes and their indicators or proxies for this study are as follows. AS with its indicators are CV and tangibility (TANG), growth opportunity (GRW) with its indicators are growth to percentage of total assets (GRW%TA), growth of financial debt (GRW-FD), growth with market to book value (GRW-MV/BV) and Tobin Q, FS with its indicators are size with log sales sales) and size with log total assets (SIZE-TA), BR with its indicator is earning volatility, Liquidity (LIQ) with its indicator is current ratio, non-debt tax shield (NDTS) with its indicators are operating income to total assets (NDTS-OI) and depreciation, depletion and amortization to total assets (NDTS-DEP) and lastly the profitability (PROF) with its indicators are earnings before EBITDA and NPM. The macro-economic attributes and its indicators or proxies are as follows. The SMD and its indicator is the stock market capitalization to Gross domestic product (GDP), BMD and its indicator is bond capitalization to GDP, EG and its indicators are GDP and gross domestic investment, IR and its indicators are lending interest rate (Lending-IR) and real IR (real-IR) and finally the inflation (INF) with its indicators are consumer price index and GDP deflator of annual % (IF-GDP).

SEM is considered to be the best and appropriate method for this study, as the research objective is for the prediction and

theory development in determinant of capital structure and firm financial performance. The research hypotheses of this study use the sample data for the period 1990-2010 is used. The data were obtained from the Bursa Malaysia stock exchange. Data for the firm attributes were gathered from the Data Stream database; internet access is one of the tools used to acquire more information

for the macro-economic attributes4. PLS-SEM models consist of

two basis components: Measurement model and structural model.

The relation between manifest indicators and latent variable is the

measurement model and relations between the latent variables,

which depict the structural model. The measurement equation can be expressed as

x

ij=

l x d

ij i+

ij, where xij is the manifest indicators of the latent variable of ξi, λij is the matrix of factor loading for the manifest indicators of xij to the latent variable of ξi (a matrix of regression coefficient of xij on ξi) and δij isthe measurement error. The expression for the structural model equation is η=∑βξ+ζ where: η is the endogenous latent variable, β is the vector matrix of regression coefficient to the vector of exogenous latent variable ξ, and ζ is the residual for the SEM

(inner model). Specifically, the standard error and the estimation

parameter in the measurement and structural models are estimates

by using the bootstrap procedure.

3.1. Model of the Study

The model equation that can be expressed by regression as follows:

1. Direct effects

h1 b0 b x b x e

1 7

8 12

= + + +

= =

å

i iå

i i i i

FA MA

4 The data for macro-economic attributes are such as http://www.worldbank. org/, F.s.d.o.t.W.B. 2012. [Last cited on 2012]; Asian Development Bank (ADB) 2012 [Last cited on 2012 Mar 2012], Available from: http://www. adb.org/. Available from: http://www.ifc.org/., I.F.C.I. 2012 [Last cited on 2012 Apr].

Table 1: Expected relationship between firm‑and macro‑economic attributes to capital structure and firm performance

Attributes Positive Negative Expected relationship

to leverage to firm’s performanceExpected relationship

AS TOT, POT - + +

Growth

opportunities POT, liquidity risk hypothesis AT, moral hazard and signaling hypothesis ± + FS Diversification, transaction

cost, access to the market Asymmetric information, liquidity risk hypothesis ± + BR Liquidity risk hypothesis,

Atble 2gency Theory Moral hazard hypothesis, bankruptcy cost -

-Liquidity Liquidity risk hypothesis POT, AT ± +

Profitability TOT POT ±

NDTS Corporate tax based theories TOT + +

SMD Information Other sources of finance, stock prices - +

BMD Creditor rights Monitoring system + +

EG GDP, sources of finance POT + +

Inflation - uncertainty -

Where:η1 is firm’s capital structure; β0 is the intercept; β1-β2 is

a coefficient parameter; ξFA1-7 is the vector of firm attributes

(AS, growth opportunities, FS, BR, NDTS, liquidity and profitability); ξMA8-12 is the vector of macro-economic attributes

(SMD, BMD, IR, EG and inflation rate) and the error term.

2. Mediation/indirect effects

h1 b0 b x b x b x12 12 e

7 11

1 6

= + + + +

=

=

å

å

i i i ii i

FA MA LEV

Where: η1 is firm’s performance; β0 is the intercept; β1-β12 is

coefficient parameter; ξFA1-6 is the vector of firm attributes (AS,

growth opportunities, FS, BR, NDTS, liquidity);ξMA7-11 is the

vector of macro-economic attributes (SMD, BMD, IR, EG and inflation rate); ξLEV is the vector of firm’s capital structure (leverage) and the error term. To test hypothesis mediating or indirect effect, the z-statistic [19] is applied. The null hypothesis will be rejected if the z-value exceeds 1.96 (at P < 0.05) (i.e. there is no mediating/indirect effect between the determinants of capital structure and firm financial performance). The z-value formula can be derived as follows: Z statistics [19 test] =

Z a b

b sa a sa sb

= ´

´ + ´ ´

2 2 2 2 2

4. RESULT ANALYSIS

The advent of SEM with simultaneous analysis has the competence to extent the path analysis coefficient from path coefficient of firm and macro-economic attributes (X) to leverage (M) and from the path coefficient leverage (M) to firm’s performance (Y). From the Table 2, we find that the significant relationships between firm and macro-economic attributes (X) to leverage (M) are: AS and growth opportunities have the most positive effect, whereas EG, IR, FS and profitability have a negative effect. We also find that the significant relationships between firm and macro-economic attributes (X) to firm’s performance (Y) are: EG, NDTS and FS have the most positive effect, whereas AS and growth opportunities have a negative effect. The only differences between the models are: (i) BMD has an inverse significant relationship effect in Model A but not in Model B and; (ii) SMD has a positive significant on such relationships in Model B but not in Model A. The analysis from Model B indicates that leverage (M) and firm’s performance (Y) have shown a negative significant effect in Malaysia. This is consistent with most of the previous studies (Rajan and Zingales, 1995; Titman and Wessels, 1988). Clarification for the negative correlation of the path coefficient is from the perspective of the Agency conflict between the firm’s manager and the shareholders,

and also from to the asymmetric information hypothesis proposed

by Myers (1977) and Myers and Majluf (1984), who suggest that firms are dependent on internal funds (i.e., retained earnings) for their new investment and growth, since it is believed that external financing incurs high risk due to higher costs. This also indicates that borrowings will hasten the separation between shareholders and lenders, and may hinder the firms from gaining more profitable

projects. This path relationship provides additional evidence that

the path relationship from the direct effect that using operating income interest and taxation and depreciation and net profit margin (EBITDA/TA and NPM)5 for the measurement of profitability to

leverage is showing the opposite relation. Therefore, this offers a robust support for the pecking order theory (POT) which suggests that increased operating income will lead to increased market value of equity, and that firms in Malaysia should look more into internal financing rather than external financing to generate greater firm’s financing performance. In addition, because Malaysia is recognised as a country that is more “market-based oriented” than “bank-based oriented”, Malaysian firms should endeavor to finance their growth and investment development through less risky ways.

Z statistics Sobel test (1982): Z a b b sa a sa sb

= ´

´ + ´ ´

2 2 2 2 2

4.1. Mediation Effect

Therefore, the question emerges as to whether or not the firm’s leverage has mediated the role between the firm and

macro-economic attributes from the perspective of capital structure

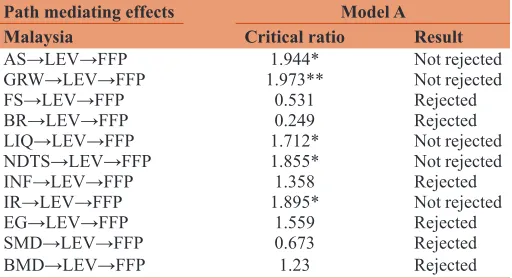

theory. As such, the introductory from the Sobel test (1982) is used to ascertain whether leverage acts as an indirect effect. The causal effects of Sobel test (Table 3)6, it seems that the factors

of capital structure choice that may be mediated by the leverage (M) (which is the variance of the path coefficient between those relationships (X and Y)) are AS, growth opportunities (GRW), Liquidity (LIQ), NDTS and IR.

The results for the capital structure choice through the mediation effects of leverage are discussed in Figure 1. This mediation effects can be concluded to be either “none,” “partial,” or “full” mediation of the three path coefficient estimates. “None mediation” effect is when there is a non-significant value for all path estimators. “Partial mediation” is when the path estimates for direct effects are all significant as well as indirect significant. “Full mediation” is when the indirect effect is significant but the direct effects (c’) are no sign of their significant value (Baron and Kenny, 1986; Iacobucci and Duhachek, 2003; MacKinnon et al., 1995). This

study concludes that both factors of the capital structure choice

have partial mediating effects because they meet the adaption from the three conditions proposed by Baron and Kenny (1982) except for the IR that shows a full mediation effects. For example, the firms with high tangibility assets have higher tendency to face the financial distress since the assets (such as property, plant and equipment) are involved in the process of a productive resource due to the tendency to attain a high liquidation value. This relationship is also supported by the trade-off theory (TOT) and the POT and AT

5 “NPM” is noted as NPM and “EBITDA/TA” is noted as the basic earning power (earnings before interest and taxes and depreciation over total assets).

that suggest that firms with larger tangible assets are stronger to face financial distress. However, the inclusion of As it is not necessary to have more leverage to enhance firm’s performance. Furthermore, in Malaysia summarizes that the firm that is high growth is believed to have sufficient earnings to support its investment results to debility in their firm’s performance if the firms have more leverage. This is when growth opportunities appear to have a positive relationship with leverage but an inversely correlation between leverage and performance. It can be summarized that the Malaysian firm intends

to use half internal financing and half debt for its investment requirements. Firms tend to act with partial action on their capital structure, partially from their earnings and partially through leverage, which believe to attain a sustainable performance.

5. DISCUSSION AND CONCLUSION

This paper introduced a factor analytic method of using the PLS, which is a variance based PLS-SEM technique, to empirically

Figure 1: Mediation test effect

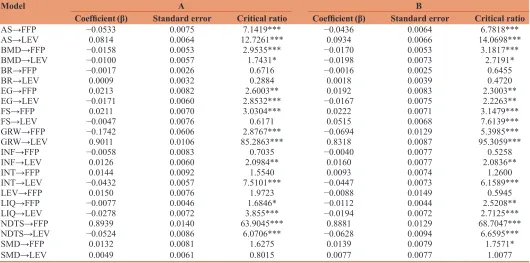

Table 2: PLS in variance based PLS-SEM

Model A B

Coefficient (β) Standard error Critical ratio Coefficient (β) Standard error Critical ratio

AS→FFP −0.0533 0.0075 7.1419*** −0.0436 0.0064 6.7818***

AS→LEV 0.0814 0.0064 12.7261*** 0.0934 0.0066 14.0698*** BMD→FFP −0.0158 0.0053 2.9535*** −0.0170 0.0053 3.1817***

BMD→LEV −0.0100 0.0057 1.7431* −0.0198 0.0073 2.7191* BR→FFP −0.0017 0.0026 0.6716 −0.0016 0.0025 0.6455 BR→LEV 0.0009 0.0032 0.2884 0.0018 0.0039 0.4720 EG→FFP 0.0213 0.0082 2.6003** 0.0192 0.0083 2.3003** EG→LEV −0.0171 0.0060 2.8532*** −0.0167 0.0075 2.2263**

FS→FFP 0.0211 0.0070 3.0304*** 0.0222 0.0071 3.1479*** FS→LEV −0.0047 0.0076 0.6171 0.0515 0.0068 7.6139*** GRW→FFP −0.1742 0.0606 2.8767*** −0.0694 0.0129 5.3985*** GRW→LEV 0.9011 0.0106 85.2863*** 0.8318 0.0087 95.3059*** INF→FFP −0.0058 0.0083 0.7035 −0.0040 0.0077 0.5258 INF→LEV 0.0126 0.0060 2.0984** 0.0160 0.0077 2.0836** INT→FFP 0.0144 0.0092 1.5540 0.0093 0.0074 1.2600 INT→LEV −0.0432 0.0057 7.5101*** −0.0447 0.0073 6.1589*** LEV→FFP 0.0150 0.0076 1.9723 −0.0088 0.0149 0.5945 LIQ→FFP −0.0077 0.0046 1.6846* −0.0112 0.0044 2.5208** LIQ→LEV −0.0278 0.0072 3.855*** −0.0194 0.0072 2.7125***

NDTS→FFP 0.8939 0.0140 63.9045*** 0.8881 0.0129 68.7047*** NDTS→LEV −0.0524 0.0086 6.0706*** −0.0628 0.0094 6.6595*** SMD→FFP 0.0132 0.0081 1.6275 0.0139 0.0079 1.7571*

SMD→LEV 0.0049 0.0061 0.8015 0.0077 0.0077 1.0077

The table demonstrated the estimated statistically significance of PLS in variance based structural equation modeling PLS-SEM for the firm and macro-economic attributes from the perspective of capital structure theory and firm’ performance. The PLS path modeling is measures the statistically significant value by using the resampling from the bootstrapping procedures for a number of samples of 5000 for Malaysia with the number of cases of (N) 5975. ***,**,*Statistically significant at the 1%, 5% and 10% levels, respectively. PLS: Partial

test the simultaneously scrutinize the cause-effect framework on the impact of specific attributes from the perspective of capital structure theory to the firm’s financial performance through leverage which acts as a mediation variable. It is believes that the simultaneous use of cause-effect frameworks in SEM is the best method to examine the objective7. It shows that firm’s capital

structure in Malaysia prefers internal financing instead of external financing, in order to enhance the firm’s financing performance

due to its inverse correlation with that relationship. Which is

consistent with most of the previous studies (Rajan and Zingales, 1995; Titman and Wessels, 1988), from the POT and from the asymmetric information hypothesis (Myers, 1977; Myers and Majluf, 1984). This finding provides a further implication to reject the argument from Jensen (1986), Modigliani and Miller (1963), Harris and Raviv (1991) and the TOT regarding the alternative of the interest/tax shield hypothesis that predicts to have a positive relationship between leverage and firm’s financial performance

in the capital structure choice. In addition, it is believed that

Malaysian firms may effect of the agency cost related to two factors: (i) Conflict between debt holders and shareholders due to the risk of default that is generated from “underinvestment,” the cost of bankruptcy, reorganization or liquidation, as well as “overhang” problems (Myers, 1977)8; and (ii) conflict between

the debt align the interest of the manager and shareholders.

7 One of the key advantage of PLS-SEM versus traditional regression is the competency to test the mediating variables as part of comprehensive model. MacKinnon, D.P., editor. Introduction to statistical mediation analysis. New York: Lawrence Erlbaum Associates ed. t. ed. 2008; MacKinnon, D.P., Lockwood, C.M., Williams, J. (2004), Confidence limits for the indirect effect: Distribution of the product and resampling methods. Multivariate Behavioral Research, 39(1), 99-128. In SEM, any of the mediating variables is fully investigate as both direct and indirect effects are assessed together in the comprehensive model.

8 From the shareholders’ perspective, as with the similar asset substitution problem, they are refused participation in low-risk projects, thus, shareholders will exchange low-risk assets for high-risk ones. This is because high-risk projects will generate higher profits thus, the larger income it gives benefit to the shareholders and the debt holders require only a fixed portion of cash flow. The agency problem exists between the debt holder and shareholder is due to that fact that debt holders are not compensated for the additional risk and shareholders enjoy the higher earnings.

Those factors advocate that when a firm has more debt consumed in its capital structure, it would result in a drop in the firm’s

performance. In addition, the implication from this relationship is

that the Malaysian firms could attempt to choose less risky route, as Malaysia is recognized as a “market-based oriented” instead of a “bank-based oriented” country (Deesomsak et al., 2004; La Porta et al., 1998). Therefore, the consideration of the “market-based oriented” tends to encourage the average consumers to search for non-banking sources for their financial capital. Also,

analysis that conducted with the Sobel test as shown in Table 3,

will make a further concrete confirmation of which of the variables could influence the relationship to firm’s financial performance by indirect effect (leverage).

REFERENCES

Asian Development Bank (ADB).(2012), Available from: http://www. adb.org/. [Last cited on 2012 Mar].

Barclay, M., Smith, C. W., Morellec, E. (2006), On the debt capacity of growth options. Journal of Business, 79(1), 37-59.

Baron, R. M., Kenny, D. A. (1986), The moderator–mediator variable distinction in social psychological research: Conceptual, strategic,

and statistical considerations. Journal of Personality and Social

Psychology,51(6), 1173.

Berger, A. N., Bonaccorsi di Patti, E. (2006), Capital structure and firm performance: A new approach to testing agency theory and an application to the banking industry. Journal of Banking & Finance, 30(4), 1065-1102.

Chin, W. W. (1998), The partial least squares approach for structural equation modeling. In: Macoulides, G. A., editor. Modern Methods for Business Research. Mahwah, NJ: Lawrence Erlbaum Associates. Dessí, R., Robertson, D. (2003), Debt, incentives and performance:

Evidence from UK panel data. The Economic Journal,113(490), 903-919.

Deesomsak, R., Paudyal, K., Pescetto, G. (2004), The determinants of capital structure: Evidence from the Asia Pacific region. Journal of Multinational Financial Management, 14(4-5), 387-405.

Fan, J. P. H., Titman, S., Twite, G. (2010), An International Comparison of Capital Structure and Debt Maturity Choices: National Bureau

of Economic Research.

Gleason, K.C., Mathur, L.K., Mathur, I. (2000), The interrelationship

between culture, capital structure, and performance: Evidence from

European retailers. Journal of Business Research, 50(2), 185-191. Hair, J.F., Ringle, C.M., Sarstedt, M. (2011), PLS-SEM: Indeed a silver

bullet. The Journal of Marketing Theory and Practice, 19(2), 139-152. Harris, M., Raviv, A. (1991), The theory of capital structure. The Journal

of Finance, 46, 297-355.

I.F.C.I. (2012), Available from: http://www.ifc.org/. [Last cited on 2012 Apr].

F.s.d.o.t.W.B. (2012), Available from: http://www.worldbank.org/. [Last cited on 2012].

Iacobucci, D., Duhachek, A. (2003), Mediating analysis. Paper Presented

at the Round table of the ACR Conference, Toronto.

Jensen, M.C., Meckling, W.H. (1976), Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305-360.

Jensen, M.C. (1986), Agency costs of free cash flow, corporate finance, and takeovers. American Economic Review, 76(2), 323-339. La Porta, R., Shleifer, A., Lopez-de-Silanes, F., Vishny, R. (1998), Law

and finance. Journal of Political Economy, 106(6), 1113-1155. MacKinnon, D.P., Lockwood, C.M., Williams, J. (2004), Confidence limits

for the indirect effect: Distribution of the product and resampling

Table 3: Mediation effect

Path mediating effects Model A

Malaysia Critical ratio Result

AS→LEV→FFP 1.944* Not rejected

GRW→LEV→FFP 1.973** Not rejected

FS→LEV→FFP 0.531 Rejected

BR→LEV→FFP 0.249 Rejected

LIQ→LEV→FFP 1.712* Not rejected

NDTS→LEV→FFP 1.855* Not rejected

INF→LEV→FFP 1.358 Rejected

IR→LEV→FFP 1.895* Not rejected

EG→LEV→FFP 1.559 Rejected

SMD→LEV→FFP 0.673 Rejected

methods. Multivariate Behavioral Research,39(1), 99-128. MacKinnon, D.P., editor. (2008), Introduction to Statistical Mediation

Analysis. New York: Lawrence Erlbaum Associates.

MacKinnon, D.P., Warsi, G., Dwyer, J.H. (1995), A simulation study of mediated effect measures. Multivariate Behavioral Research, 30(1), 41-62.

Margaritis, D., Psillaki, M. (2007), Capital structure and firm efficiency. Journal of Business Finance & Accounting, 34(9‐10), 1447-1469. Margaritis, D., Psillaki, M. (2010), Capital structure, equity ownership

and firm performance. Journal of Banking & Finance, 34(3), 621-632. McConnell, J.J., Servaes, H. (1995), Equity ownership and the two faces

of debt. Journal of Financial Economics, 39(1), 131-157.

Modigliani, F., Miller, M.H. (1963), Corporate income taxes and the cost of capital: A correction. American Economic Review, 53(3), 433-443. Mustapha, M., Ismail, H.B., Minai, B.B. (2011), Determinants of Debt

Structure: Empirical Evidence from Malaysia.Paper Presented at the 2nd International Conference on Business and Economic Research,

2nd ICBER, Proceeding.

Myers, S.C., Majluf, N.S. (1984), Corporate financing and investment decisions when firms have information that investors do not have.

Journal of Financial Economics, 13, 187-221.

Myers, S.C. (1977), Determinants of corporate borrowing. Journal of

Financial Economics, 5, 147-175.

Rajan, R.G., Zingales, L. (1995), What do we know about capital structure? Some evidence from international data. The Journal of Finance, 50, 1421-1460.

Ramadhan, A.H., Chen, J.J., Al-Khadash, H.A., Atmeh, M. (2012), A mediating role of debt level on the relationship between determinants of capital structure and firm’s financial performance. International Research Journal of Applied Finance, 111(1), 65-92. Sobel, M.E. (1982), Asymptotic confidence intervals for indirect effects in

structural equation models. Sociological Methodology, 13, 290-312. Titman, S., Wessels, R. (1988), The determinants of capital structure