The Dynamics of Car Sales: A Discrete

Choice Approach

J´erˆome Adda

University College London

and Russell Cooper

Motivation

• How can we understand the aggregate dynamics of durables?

– role of income and price shocks.

– role of evolution of stock.

Aggregate Level:

• How can we resolve the Mankiw (1982) puzzle?

– PIH implies an ARMA(1,1) specification for durables expenditures.

– MA coefficent is parameterized by the rate of depreci-ation.

– From US data, estimated rate of depreciation is close to 100%!

Micro Level:

• From micro studies, infrequent adjustment and lumpiness. Lam (1991), Attanasio (1997).

Key Points

• Document the time series of durable goods.

We show that the representative agent model (PIH)

– Fails to explain time series properties of durable goods.

– Structural interpretation of parameters is difficult (de-preciation rate).

• Specify and estimate a dynamic discrete choice model of car ownership.

=⇒ No need to rely on PIH or ad hoc (S,s) bands.

• D.D. Choice model predicts aggregate behavior well.

• Match aggregate sales with estimated micro model.

– sensible depreciation rate at the micro level (3 to 6%).

Evidence on Time Series Dynamic

DATA:

• Two countries: US, France.

• Aggregate durables, new car registrations, car expenditure.

• Relative prices and household income.

TOOLS:

• ARMA(1,1) for sales. Mankiw (1982).

• ARMA(1,q) for sales. Caballero (1990).

ARMA(1,1)

Mankiw (1982): PIH, quadratic utility and durable goods im-plies:

et+1 = δα0 + α1et +εt+1 −(1−δ)εt. δ: depreciation rate.

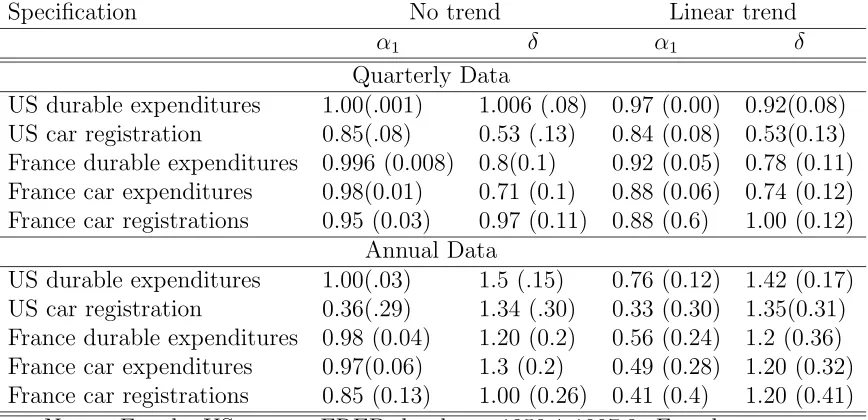

Table 1: ARMA(1,1) Estimates on US and French Data

Specification No trend Linear trend

α1 δ α1 δ

Quarterly Data

US durable expenditures 1.00(.001) 1.006 (.08) 0.97 (0.00) 0.92(0.08)

US car registration 0.85(.08) 0.53 (.13) 0.84 (0.08) 0.53(0.13)

France durable expenditures 0.996 (0.008) 0.8(0.1) 0.92 (0.05) 0.78 (0.11)

France car expenditures 0.98(0.01) 0.71 (0.1) 0.88 (0.06) 0.74 (0.12)

France car registrations 0.95 (0.03) 0.97 (0.11) 0.88 (0.6) 1.00 (0.12) Annual Data

US durable expenditures 1.00(.03) 1.5 (.15) 0.76 (0.12) 1.42 (0.17)

US car registration 0.36(.29) 1.34 (.30) 0.33 (0.30) 1.35(0.31)

France durable expenditures 0.98 (0.04) 1.20 (0.2) 0.56 (0.24) 1.2 (0.36)

France car expenditures 0.97(0.06) 1.3 (0.2) 0.49 (0.28) 1.20 (0.32)

France car registrations 0.85 (0.13) 1.00 (0.26) 0.41 (0.4) 1.20 (0.41) Notes: For the US, source FRED database, 1959:1-1997:3. French

ARMA(2,1)

Bernanke (1985): PIH with durable goods and cost of adjust-ments implies:

et = α0 + α1et−1 +α2et−2 +εt −(1−δ)εt−1

Table 2: ARMA(2,1) Estimates on US and French Data

Specification No trend Linear trend

α1 α2 δ α1 α2 δ

US durable expenditures 1.95 (0.07) -0.95 (0.07) 0.13 (0.1 ) 0.62(0.7) 0.33(0.7) 1.24 (0.7) US car registration 0.89 (0.31) -0.04 (0.21) 0.5 (0.3) 0.89(0.31) -0.04(0.21) 0.5 (0.3) France durable expenditures 0.7(0.4) 0.3(0.4) 1.03 (0.4 ) 0.7(0.4) 0.2 (0.4 ) 1.0 (0.45) France car expenditures 0.8 (0.3) 0.2(0.3) 0.9(0.3) 0.65 (0.2) 0.2 (0.3) 0.96 (0.4) France car registrations 0.85 (0.24) 0.09 (0.22) 1.43(0.23) 0.72 (0.36) 0.09 (0.23) 1.35 (0.35) Notes: Estimation done on quarterly data. For the US, source FRED database, 1959:1-1997:3.

ARMA(1,q)

Caballero (1990): PIH with durables and slow adjustment. et = α0 +α1et−1 +εt+ ρ1εt−1 +. . .+ρqεt−q

According to Caballero: δ = 1 +

q

l

ρl

On US data, Caballero finds δ = 5% annually.

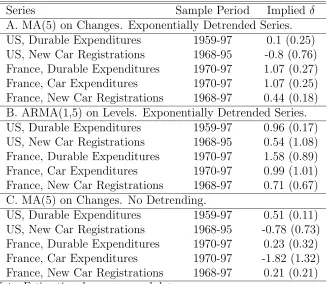

Table 3: ARMA(1,q) Representations for Annual Data

Series Sample Period Implied δ

A. MA(5) on Changes. Exponentially Detrended Series.

US, Durable Expenditures 1959-97 0.1 (0.25)

US, New Car Registrations 1968-95 -0.8 (0.76)

France, Durable Expenditures 1970-97 1.07 (0.27)

France, Car Expenditures 1970-97 1.07 (0.25)

France, New Car Registrations 1968-97 0.44 (0.18)

B. ARMA(1,5) on Levels. Exponentially Detrended Series.

US, Durable Expenditures 1959-97 0.96 (0.17)

US, New Car Registrations 1968-95 0.54 (1.08)

France, Durable Expenditures 1970-97 1.58 (0.89)

France, Car Expenditures 1970-97 0.99 (1.01)

France, New Car Registrations 1968-97 0.71 (0.67)

C. MA(5) on Changes. No Detrending.

US, Durable Expenditures 1959-97 0.51 (0.11)

US, New Car Registrations 1968-95 -0.78 (0.73)

France, Durable Expenditures 1970-97 0.23 (0.32)

France, Car Expenditures 1970-97 -1.82 (1.32)

France, New Car Registrations 1968-97 0.21 (0.21)

ARMA(1,q) II

Summary and Modeling Strategy

DATA:

• From VAR:

– income and prices matter.

– fluctuations in sales in response to income shocks.

• From ARMA(1,q): PIH is not a good framework, even in the long run. Not robust.

• ARMA(1,1) seems to be a robust finding.

MODEL:

• Model does not rely on PIH.

• Directly specify the individual optimization problem.

• Lumpiness: Discrete choice at the individual level.

• Heterogeneity in age of cars.

Dynamic Discrete Choice Model

• agent with a car of age i in state Z = (p, Y, ε), z = (y).

• either KEEP or REPLACE.

• probability δ of breakdown.

Value:

Vi(z, Z) = max[Vik(z, Z), Vir(z, Z)]

where

Vik(z, Z) = u(si, y+ Y, ε) +β(1−δ)EVi+1(z, Z) +

βδ{EV1(z, Z)−u(s1, y+ Y, ε) +u(s1, y +Y −p +π, ε)}

and

Vir(z, Z) = u(s1, y +Y −p+ π, ε) +β(1−δ)EV2(z, Z) +

βδ{EV1(z, Z)−u(s1, y+ Y, ε) +u(s1, y +Y −p +π, ε)}.

Utility function:

u(si, c) =

i−γ + ε(c/λ)

1−ζ

1−ζ

=⇒ Hazard function at the individual level:

Exogenous Process

Yt = µY +ρY YYt−1 +ρY ppt−1 + uY t

pt = µp+ ρpYYt−1 +ρpppt−1 + upt

εt = µε+ρεYYt−1 +ρεppt−1 +uεt

The covariance matrix of the innovations u = {uY t, upt, uεt} is :

Ω =

ωωYpY ωωY pp 00

0 0 ωε

• estimate the process for (pt, Yt) in first stage

Aggregate Sales

• Aggregate hazard function:

H(i, Z;θ) = h(i, z, Z;θ)φ(z)dz

• Aggregate Sales:

St =

i

H(i, Zt;θ)ft(i)

• Cross sectional distribution:

ft+1(1) = St

ft+1(i) = [1−H(i, Zt;θ)]ft(i−1)

Estimation: Methodology Stochastic Dynamic Programming Problem ? Predicted Hazard Function ? Aggregation over Households ?

Predicted Sales and C.D.F.

?

Parameters θ

Simulated Moments from Aggregate Data

6 ? Match ? 1 PPPPPP q No Yes

Actual Moments from

Estimation Method

Parameters to estimate: θ = {γ, δ, λ, ζ, σy, ρεY, ρεp, ωε}

Objective function to minimize:

LN(θ) =αL1N(θ) + L2N(θ)

• Matching predicted and observed sales (conditional on prices and income):

L1

N(θ) =

1 T T t=1

(St −S¯t(θ))2 − 1 N(N −1)

N

n=1

(Stn(θ)−S¯t(θ))2

where

– St: aggregate sales of new cars.

– N number of draws for the unobserved taste shock.

• Matching Moments:

L2

N(θ) =

i={5,10,15,AR,MA}

αi( ¯Fi−F¯i(θ))2

where

– F¯i, i = 5,10,15: average fraction of cars of age i across all periods.

Estimation and Results

Table 4: Estimated Parameters for Discrete Choice Model

U.S.

Non Linear Case Linear Case

Parameters Estimates S.E. Estimates S.E.

γ 0.02 0.0015 0.02 0.002

δ 0.038 0.0025 0.03 0.003

ζ 1.49 0.0037 0

-λ 483.5 10.5 1.6e-5 1.4e-06

σε 0.085 0.015 0.03 0.097

σy 0.52 0.016 0.26 0.013

ρε,p 1.14e-4 4.2e-05 -3.9e-5 1.9e-05

Pseudo-R2: 0.69 0.52

P(Overidentification test) 0.84 0.60

FRANCE

Non Linear Case Linear Case

Parameters Estimates S.E. Estimates S.E.

γ 0.017 0.003 0.028 0.014

δ 0.061 0.016 0.06 0.03

ζ 1.46 0.007 0

-λ 108.0 12.5 6e-6 2.8e-06

σε 0.215 0.09 0.06 0.037

σy 0.99 0.003 0.44 0.22

ρε,p 1.2e-4 4.3e-05 -2.9e-5 1.5e-05

Pseudo-R2: 0.61 0.52

P(Overidentification test) 0.91 0.67

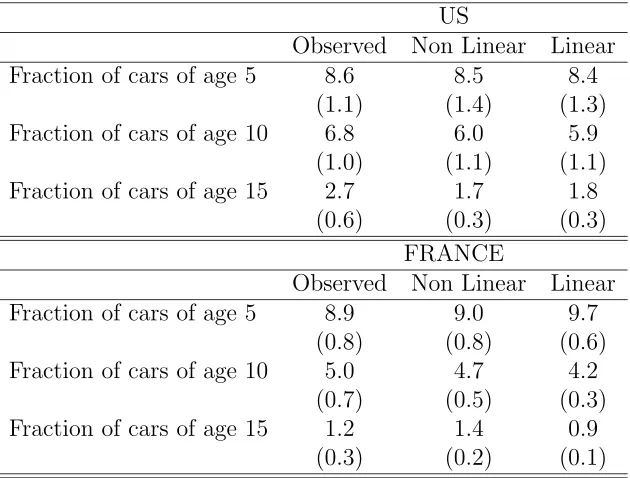

More on the Fit

Table 5: Observed and Predicted Moments from CDF

US

Observed Non Linear Linear

Fraction of cars of age 5 8.6 8.5 8.4

(1.1) (1.4) (1.3)

Fraction of cars of age 10 6.8 6.0 5.9

(1.0) (1.1) (1.1)

Fraction of cars of age 15 2.7 1.7 1.8

(0.6) (0.3) (0.3)

FRANCE

Observed Non Linear Linear

Fraction of cars of age 5 8.9 9.0 9.7

(0.8) (0.8) (0.6)

Fraction of cars of age 10 5.0 4.7 4.2

(0.7) (0.5) (0.3)

Fraction of cars of age 15 1.2 1.4 0.9

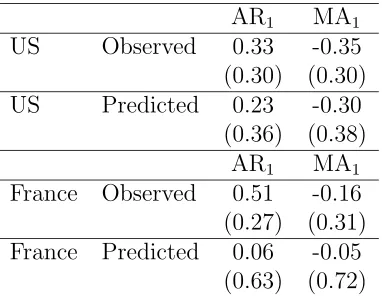

ARMA Representation of Simulated Data

Table 6: ARMA Coefficient Observed and Predicted.

AR1 MA1

US Observed 0.33 -0.35

(0.30) (0.30)

US Predicted 0.23 -0.30

(0.36) (0.38)

AR1 MA1

France Observed 0.51 -0.16

(0.27) (0.31)

France Predicted 0.06 -0.05

(0.63) (0.72)

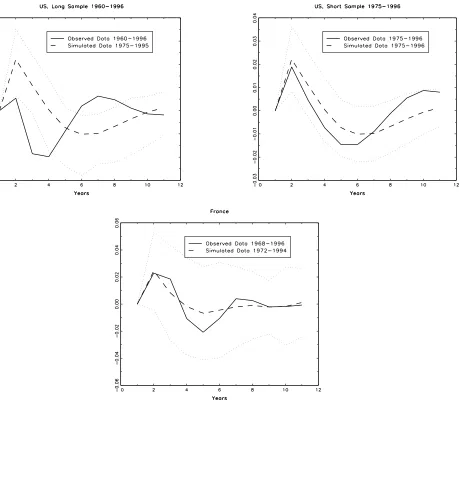

Note: Monte Carlo results obtained over 100 replications with sample length 21 (France), 28 (US). French estimates on annual car registration, 1972-1994. US estimates on annual car registrations 1968-1995. All ARMA models included a linear trend.

VAR Representation

• Simulated data from our model

• Unrestricted linear VAR estimation, IRF created

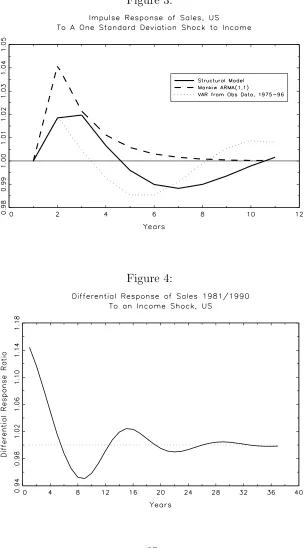

More on IRF

Compare:

• IRF computed from simulation of structural model.

• IRF computed from observed data with ARMA(1,1).

• IRF computed from observed data with linear VAR.

Note:

• IRF from ARMA: ρt−1(ρ−α)

– ρ > 0 =⇒ No oscillations possible.

– ρ−α > 0 =⇒ δ >1−ρ. With ρ 0.6 =⇒ δ > 0.4

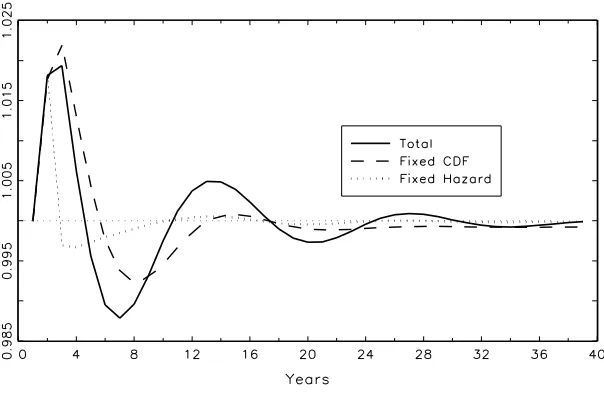

Decompositions

Recall:

Aggregate Sales:

St =

i

H(i, Zt;θ)ft(i)

Oscillations of sales as a result of a shock:

• Endogenous movement in CDF.

• Serial correlations in prices and income: Hazard shifts.

=⇒ How important are these two sources?

• Decompose IRF into shifts in CDF and shifts in hazard.

IRF Decompositions

Sales: interaction of Hazard function with CDF.

St =

k

IRF Decomposition

Cross Effect of Prices and Income

Yt = µY +ρY YYt−1 +ρY ppt−1 + uY t

pt = µp+ ρpYYt−1 +ρpppt−1 + upt

Time Series Decomposition

Sales: interaction of Hazard function with CDF.

St =

k

Hk(zt, θ)ft(k)

Decomposition:

St −St−1 = ∆StHaz + ∆StCDF + ut

=

k

[Hk(zt;θ)−Hk(zt−1;θ)]ft−1(k)

Shifts in Hazard

+

k

Hk(zt;θ)[ft(k)−ft−1(k)]

Shifts in CDF +ut

• Total Contribution of ∆StCDF to ∆St ?

• Contribution of ∆StCDF to ∆St at different frequencies ?

R2

Conclusion

Our model is able to :

• reproduce various aspects of the data and time series im-plications:

– reconcile aggregate ARMA(1,1) results with micro ob-servations.

– Impulse response functions.

– fit decomposition shifts Hazard/CDF, at different fre-quencies.

Without requiring nonsense values for the micro parame-ters.

• investigate the sources of dynamics:

– role of endogenous evolution of CDF (small)

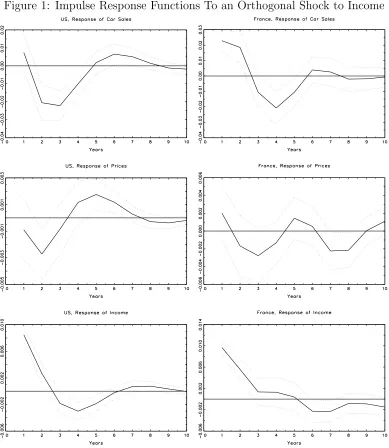

Figure 1: Impulse Response Functions To an Orthogonal Shock to Income

Figure 3:

Figure 5: