http://www.sciencepublishinggroup.com/j/jppa doi: 10.11648/j.jppa.20170102.11

Review Article

The Analysis of Advantages and Disadvantages of Third

Sector in Bangladesh Using ASA as Example or Case Study

Sefat Ara Nadira

1, *, Md. Enamul Haque

2, Tarique Al Kadir

3, Zhi Zhang

11School of Public Administration, China University of Geosciences, Wuhan, China 2

Department of Anthropology, Shahjalal University of Science and Technology, Sylhet, Bangladesh

3Department of Business Studies, Bangladesh National University, Dhaka, Bangladesh

Email address:

[email protected] (S. A. Nadira)

*

Corresponding author

To cite this article:

Sefat Ara Nadira, Md. Enamul Haque, Tarique Al Kadir, Zhi Zhang. The Analysis of Advantages and Disadvantages of Third Sector in Bangladesh Using ASA as Example or Case Study. Journal of Public Policy and Administration. Vol. 1, No. 2, 2017, pp. 47-55. doi: 10.11648/j.jppa.20170102.11

Received: November 5, 2017; Accepted: November 16, 2017; Published: December 20, 2017

Abstract: A country or a society is divide into three sectors, these are: public or state, private or market and nonprofit or third

sector. This paper will look at Non–governmental organizations (NGOs) as legally constituted organizations created by natural or legal people that operate independently from any form of government. In this sense, Association for Social Advancement (ASA) as an NGO will be use as a case study. ASA operate as a Micro Finance in Bangladesh helping to elevate poverty and improve living standard of the people. The paper will also look at ASAs mission or their purpose driven including their financial services, saving program, impact of ASA in Bangladesh some challenges they face including problems identified and then outline some recommendation and conclusion for ASA.Keywords: MFIs (Microfinance Institutions), MF-NGOs (Non Government Organizations That Provide Microfinance),

Bangladesh, Challenges, Third Sector Analysis, A Case Study of ASA1. Introduction

A society is divided into three sectors, these are: public or state, private or market and nonprofit or third sector. The nonprofit sector is arguably present in almost every society today but its nature and function which is neither state nor market vary from country to country. Therefore a third sector is referred to as non-government (NGOs) as they are non-profit making, donor driven and belong to the state or the private sector of an organization.

Non-governmental organizations (NGOs) are legally constituted organizations created by natural or legal people that operate independently from any form of government. The term originated from the United Nations, and normally refers to organizations that are not a part of a government and are not conventional for-profit businesses. In the cases in which NGOs are funded totally or partially by governments, the NGO maintains its non-governmental status by excluding

government representatives from membership in the organization. The term is usually applied only to organizations that persue wider social aims that have political aspects, but are not openly political organizations such as political parties. [1]

2. NGOs in Bangladesh

2.1. Functions of NGOs

Non-Government Organization (NGOs) started in this country in a limited scale as relief provides following the devastating cyclone in 1970, which claimed colossal human lives and properties in the coastal belt and the off-shore islands. Devastations caused by the War of Liberation in 1971 prompted other foreign and newly established local NGOs to mount relief and rehabilitation Programs.

emphasis from relief to socio- economic development and to pursue-initially rather haphazardly programs aiming at health care, family planning, income generation and self-reliance for the disadvantaged and the poor. As poverty continued to deepen and encompass ever larger numbers of people, more foreign NGOs came to work in this country and at the same time, the members of local NGOs grew fast.

2.2. Advantages of NGOs

a. They have the ability to experiment freely with innovative approaches and, if necessary, to take risks.

b. They are flexible in adapting to local situations and responding to local needs and therefore able to develop integrated projects, as well as sectoral projects.

c. They enjoy good rapport with people and can render micro-assistance to very poor people as they can identify those who are most in need and tailor assistance to their needs.

d. They have the ability to communicate at all levels, from the neighborhood to the top levels of government.

e. They are able to recruit both experts and highly motivated staff with fewer restrictions than the government.

2.3. Disadvantages

a. Paternalistic attitudes restrict the degree of participation in programme/project design.

b. Restricted/constrained ways of approach to a problem or area.

c. Reduced replicability of an idea, due to non-representativeness of the project or selected area, relatively small project coverage, dependence on outside financial resources, etc.

d. "Territorial possessiveness" of an area or project reduces cooperation between agencies, seen as threatening or competitive.

2.4. NGO Laws

a. The Societies Registration Act, 1860 b. The Trust Act, 1882

c. The Cooperative Societies Act, 1925

d. The Voluntary Social welfare Agencies (Registration and Control) Ordinance, 1961 (ordinance XLVI, 1961)

e. The Foreign Donations (Voluntary Activites) Regulation Ordinance, 1978 (Amended in 1982)

f. The Foreign Contributions (Regulation) Ordinance, 1982 (Ordinance XXXI of 1982)

g. The Companies Act, 1913 (Amended in 1994) h. The Microfinance Regulatory Law, 2006

i. Foreign Contributions (Voluntary Activities) Regulation Act, 2014 [9, 10, 11]

3. Third Sector in Bangladesh Using ASA

as Example or Case Study of NGOs

Association for Social Advancement (ASA) is a type of NGO that operate as a micro finance institution in Bangladesh.

Let’s take a look at micro finance before ASA.

4. The Status of Micro-Finance in

Bangladesh

Bangladesh is a small country with a total area of only 147,570 square kilometers. With a population of 130 million, the density is 981 persons per square kilometer; annual growth rate is 2.3%. However major part of the population is illiterate with 48% males (15+ years) being illiterate and 71% females (15+ year). The unemployment rate is a striking 35%, which is increasing by two million yearly. Seventy-six percent of the total population in Bangladesh is living in rural areas and 24% in urban area. The poverty level in rural areas is 40% and 14% in urban areas. Twenty-nine percent of the population is earning below $1 a day and 77% of the population is earning $2 a day.

Figure 1. 76% of the Population Lives in Rural Areas and 24% of the Population Lives in Urban Areas.

In the micro finance market of Bangladesh, 82% of clients are poor women. They are landless or have less than. 5 acres of cultivable land, and average monthly income is $50-$75. More than 50% of the clients live below poverty line. Borrowers are involved in various micro finance activities: 42% are involved in commerce and trading, 21% in livestock, 13% in agriculture, 7% in food processing, 5% in fisheries, 3% in transport and 9% in other activities. ASA remains NGO, and work under an ill-defined mandate from the government’s NGO Affairs Bureau. It is assumed that NGOs can collect savings from members organized in groups, but what exactly can they do with these savings, how are they safeguarded, and can NGOs collect deposits from the general public? Government is concerned about this problem and under process to formulate a national policy to address this issue. [8]

5. Introduction of ASA and the Founder

the underprivileged segment of the society in attaining better livelihood and acquiring means to escape poverty trap. Since its inception, ASA has been pursuing utmost its efforts in the cause of the downtrodden and uncared people. Microfinance is the core program of ASA with seven million clients across Bangladesh currently. Besides, it has been implementing a number of non-financial programs featuring Education, Healthcare, Sanitation, Hygiene and Agriculture support services. ASA is an absolutely self-financed organization and doesn’t take grants or donations of any kind from anywhere at home and abroad. The organization bears the non-financial program costs from its own resource generated out of the surplus of microfinance operation.

Figure 2. ASA Head Office.

6. ASA in Micro Finance Program

Women in Bangladesh and rural people are the worst sufferers and victims of social injustices. Half of the women of the population possess a very low status. A permanent development of their status would not be possible without changing social structure. Realizing this ASA was established in 1978. Initially ASA worked to raise social awareness of mass people. ASA understand from their experience, without self-dependence of poor people awareness creation is not possible. The first phase of ASA (1978-1985) was a radical organization seeking to empower the poor through social mobilization and “consciousness”. The second phase ASA (1985-1990) was a provider of offering health, education, women’s empowerment, etc. to its members. The third stage of ASA (1991-1997) was flexible but highly successful micro credit institution. The fourth stage of ASA (1997-till date) is a sustainable micro finance institution seeking to offer a broader array of savings services in addition to its loan products. Presently ASA has over 2.2 million members forming different groups with special emphasis on saving practice and 8000 staffs engaged in disbursing and collecting loan and

savings deposits. [2, 8]

The credit program for income generation that ASA operates evolved in 1991 to focus on the organization to date. ASA, in its present form, seeks to create employment opportunities by providing micro finance services for the socio economic empowerment of the poor. The programs adopted by ASA are micro credit, small business credit, regular weekly savings, voluntary savings and life insurance. The ASA’s micro credit and savings products are quite innovative. It is non-traditional, cost-effective, self-sustainable model, which is easy to implement for socio-economic development. ASA follows a simple, standardized, low-cost system of organization, management, savings and credit operations. The basic features of ASA’s micro credit model are:

a. Self-sustainability

b. Branch office without accounts personnel

c. Simple, easy, but effective record keeping/bookkeeping and working procedures

d. Innovative staff recruitment policy e. Training without cost

f. Innovative mid-level management structure g. Well-written ASA Working Manual

h. High degree of decentralization to the field level i. Simple, small and cost-effective branch structures j. Standardization in policies, procedures, equipment and logistics

In the year 1997 ASA was successful in the integration of the concept of sustainability with empowerment of disadvantage landless women of the rural and urban. The financial viability and the profitability of ASA led to the self reliant and sustainable model. ASA has specialized in the field of micro credit program operations.

7. Vision

Poverty alleviation, improvement of living standard and empowerment of the poor by providing financial service is the main focus as the poverty level is a 54% in the country. ASA’s institutional mission is to support, impel and strengthen the lower status economy for the poor sector through facilitating, dispensing and expanding savings and credit for those segments of the population that finds it difficult to have access to credit. The services that ASA provides are now strictly financial in nature. The institution with, a huge clientele, seeks to play a better role of financial intermediary among the poor by lending surplus funds of savers to those with an investment opportunity.

8. Mission or Purpose

a. Improve and strengthen the poor people life through credit disburse for income generating purpose and mobilize income by saving program.

c. The surplus money is collected and disbursed to the beneficiaries; hence ASA acts as a financial intermediary. [8]

d. Develop long-term relationship with existing members through frequent loans to make them self-reliant.

e. Reduce group members’ dependency on local moneylender when they face crisis.

f. Increase ASA’s internal fund, with reduction of donor and bank dependency.

g. ASA aims to reach 3 million borrowers in future while the current figure showing 2.2 million borrowers.

9. Credible Financial Services of ASA

ASA implies a non-traditional way of micro finance program. The methodology of the Grameen Bank and ASA are quite different. Since the poor people cannot have any collateral, thereafter Grameen Bank provides micro credit followed by group liabilities. This the basic foundation of the Grameen bank, however this is where ASA differs in function, which works through individual liabilities that allows for greater flexibility and simplicity.

ASA is one such organization, which has worked with ardently and successfully for the welfare of the people. To alleviate rural poverty ASA take initiative to involve their group members with income generating activities (IGA) like – trading, milk-cow rearing, poultry raising, vegetable gardening etc.. To do this ASA introduce “credit program” and poor women have created self employment by drawing loans from ASA, which helps them to become self-reliant. ASA is lifting up the living standards of the poor people and helping in rural development through its micro finance program. This program benefits especially the women, not only they play a more respectable role in the family but also assisting financially.

10. ASA Savings Program

Having significant impact in rural area ASA’s flexible saving program has been widely accepted. It has mobilized and promoted the saving habits among the people with the withdrawal facilities. Rural communities are enjoying rural banking services at the doorsteps. Savings is a universal practice among the poor according to their own way. ASA’s poor beneficiaries use their savings deposits:

a. to cope with periodic deficits, i. e.

b. for emergency access: to adjust to seasonal cash flow, c. to protect family from adversity, to loosen liquidity constrain

d. to balance cash flow over life cycle

Since ASA’s savings products are considered the supporting product of micro credit so that when credit is accessible, the poor also use credit for emergency purposes. One of the most effective tools for poverty alleviation is micro credit and the savings products are intrinsically connected to micro credit. In case of a crisis, be it natural or manmade; sickness or a social obligation like marriage, these events draw heavily on the resources of the family. And, in a resource poor branch, a

small blow can create disaster that savings can help avert. Therefore, savings components are beneficial for both the client and the MFI. Several study shows, the poor have small financial savings due to:

a. Lack of dependable, convenient deposit services b. They are costly to use

c. They are too rigid

d. Low, often negative real rate of interest

Micro finance programs should give more emphasis on making deposit services accessible, more dependable and convenient, less costly, flexible, and financially attractive to the poor. Most poor people believe they cannot generate financial savings on their own because their income is simply “not enough”. What they know and practice is:

11. Income–Consumption=Savings

Few years back when ASA introduced Associate and Long Term Savings beside existing Mandatory and Voluntary Savings program ASA experienced that due to their low level of income the net savings mobilization never increased. It is not very easy task to generate income or employment wages over night and in the same time with help of only micro finance program the poor people cannot have a regular income. So that sometime they prefer to hold money cash in hand for daily consumption to protect family from adversity since savings is the first instrument of poor households to alleviate economic deprivation. Different studies and field experiences show that poor people especially women always willing to deposit but their income is not good enough to do so. That is why finally ASA closed down the associate and long-term savings program those are unrealistic and burden for them. But in order to their gradual development ASA keep continue mandatory and voluntary savings those are accessible and efficient deposit services that will help poor households better manage their limited financial assets and smoothen consumption patterns. In the same time ASA credit program contributes directly to the poor households to an increase in production and income, which leads to capital stock expansion, and increase in productivity.

ASA has introduced (1) Weekly savings: Group members have to deposit a mandatory fixed amount every week: Tk. 10 for small credit program and Tk. 20 for small business credit program. (2) Voluntary savings: In addition to the weekly mandatory savings, group members are allowed to save any amount they wish. These savings programs promote the habit of saving while resulting in the accumulation of a huge amount of funds, which can be disbursed. ASA allows its member’s to withdraw their savings but they must maintain 10% of their current loan principal. Members receive 6% interest rate and interest paid on the basis of end balance.

departure for ASA in great part because it required a radical rethink of the organizational approach and institutional

culture”. [8, 14]

Figure 3. ASA Growth Rating structure (2000-2015).

12. Objective of the Savings Program for

the Poor Are Outlined Below

In The rural areas of Bangladesh there are no facilities available for the poor to deposit savings. Due to lack of savings, the poor people become helpless in emergency, especially during natural disaster and sudden accidents. To deal with such situations either they have to sell their assets and property or borrow money from the moneylenders at an exorbitant rate of interest. As a result of that they become poorer. If they can provide with the facilities of depositing small savings, it would be possible for them to escape from the vicious circle of moneylenders and save their assets and property. Moreover, this accumulated savings would be contributed in creating liquid assets and making them

self-reliant. Considering above factors, ASA has undertaken a savings program for its group members.

The goal is to make group members aware of the benefits of savings and offer a savings service for them. This will help them in capital formation and provide an opportunity to make the poverty alleviation program self-reliant without dependence on foreign assistance. Key objectives of the savings are:

a. To motivate members to deposit more savings from the excess of income of their income generating projects.

b. To use savings as a source of capital for income generating projects.

c. To use savings for emerging family needs. d. To introduce a doorstep services for the poor. e. To allow clients to accumulate funds [2, 4]

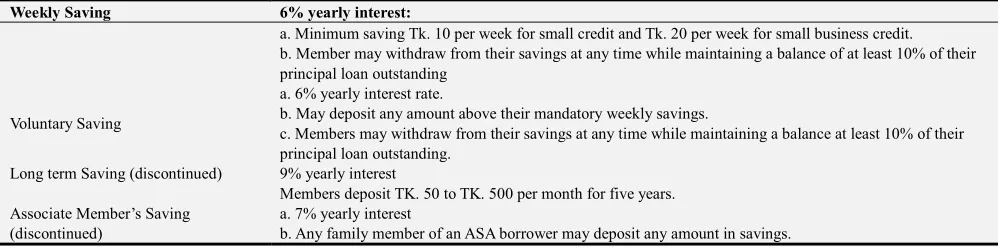

Table 1. ASA Saving Product.

Weekly Saving 6% yearly interest:

a. Minimum saving Tk. 10 per week for small credit and Tk. 20 per week for small business credit. b. Member may withdraw from their savings at any time while maintaining a balance of at least 10% of their principal loan outstanding

Voluntary Saving

a. 6% yearly interest rate.

b. May deposit any amount above their mandatory weekly savings.

c. Members may withdraw from their savings at any time while maintaining a balance at least 10% of their principal loan outstanding.

Long term Saving (discontinued) 9% yearly interest

Members deposit TK. 50 to TK. 500 per month for five years. Associate Member’s Saving

(discontinued)

a. 7% yearly interest

b. Any family member of an ASA borrower may deposit any amount in savings.

13. Challenges with Savings

Mobilizations

ASA faced some challenges in mass savings mobilizations. People’s confidence in MFIs especially middle class those are able to deposit did not develop in Bangladesh. Neither NGOs

are trust-worthy like other government conventional banks nor are peoples much interest about their rate of interest on deposits.

structure of the MFI does not go smoothly with the savings mobilization of the people. In the same group meeting, it is not so easy to mobilize savings from the mass people; it is also irrelevant and unfriendly. In an ongoing meeting, the savings collection will interrupt the credit collection and neither of the tasks can be performed effectively. A complete different structure of the same MFI with much more flexibility and options are needed to address this type of problem. Besides this, more smart and professional personnel to explore the opportunities operate middle class savings market. Due to their class and cultural conservativeness they used to deny sitting and spending time with the poor or hard core poor in the same group meeting. [8]

Where apex-funding body (PKSF) is giving loan in 7% interest, savings mobilization deposit is cost-involve factors giving 6% interest; 4% operational cost and total saving cost would be 10% (4% is assume as minimum operating cost). On the other hand, cost to lend money from the commercial and government bank is 15%. From this analysis it is clear that lending from PKSF is cheaper than other sources. ASA is interested to collect fund from PKSF since saving mobilization is not only costly but also capacity is limited. ASA staffs require more time and need more concentration to book keeping which increase administration cost. Though fund is available from PKSF (cheap fund), ASA wants to do or doing it for the sake of the poor people.

On the other hand, people cannot take part in multiple savings products, as they are living in the same source of income, income is not actually growing so we will see, the ultimate result is negative if they take part in multiple savings product. So, ASA, at presently introduced only two types of savings product: weekly mandatory and voluntary savings.

Again, to become trust-worthy like other national banks, MFIs cannot give high interest rate for savings mobilization, because this is not suitable plan for further investment. Moreover, PKSF is giving fund in low interest.

Timetable maintaining is not always possible for all class of people. So, in order to overcome these challenges, we need to work hard for structural and behavioral changes.

Donor Support:

Most of the MFIs of Bangladesh depend on the donor fund organization for capital to operate their micro credit programs. It is the common scenario. But donor dependency in long run is not good sign in terms of achieving sustainability. What will happen if they withdraw support from the program? So, alternative fund accumulating source is necessary. Saving program could be one important alternative for fund raising. ASA manage fund with institution’s own fund, members’ savings and loan form PKSF and loan from CORDAID.

Advantages of ASA:

a. They have the ability to experiment freely with innovative approaches and, if necessary, to take risks.

b. ASA provide support for health, education and women empowerment in rural areas.

c. ASA provide loan and saving service to the villagers.

14. Specialty of ASA’s Micro Finance

Programs

The ASA methodology was developed from the field through hands on approach. ASA runs like a client responsive financial institute and revises the financial products depending on the feedback from clients and staff. ASA’s main strength lies on its specialized financial services. Some of the key points behind ASA’s institutional sustainability are discussed below:

14.1. Organizational Structure

There is a standardized branch structure with a fixed number of credit officers for each branch and a fixed number of borrowers to be handled by each credit officer. Even all of ASA’s office furniture is standardized, with design quality and number of pieces per branch being uniform.

14.2. Selection of Borrowers

The main objective of ASA’s microcredit program is to provide financial services to the poor using small amounts of money. ASA never spends very much time for borrower assessment before the loan. ASA just needs to know if the individual is receiving less than $50 income a month (or a dollar per day). Mostly women are chosen because they are home during the day. The CO must visit the women’s house and her neighbors as well. This is why ASA can identify the borrower quickly.

14.3. ASA Group Meeting

ASA’s weekly regular group meeting group acts as a forum for women to share their experiences with each other and develop their business skills. They also gain advice and support in domestic issues and conflicts.

14.4. Credit Policies

ASA loan products are very simple and flexible as well. After only four weeks attending the group meeting and Tk. 10 savings in each week, loans are given quickly to the ASA members. Even after the last loan repayment a new loan can be given the same day. Borrowed money from ASA must be repaid through 46 installments per year with 15% flat rate charged on loans.

14.5. Savings Policies

Most MFIs do not allow savings withdrawal. ASA members can withdraw, but must always have 10% of the loan in their savings. Savings can be used to loan to other borrowers.

14.6. Operational Budget

field is the center of all actions for implementing ASA’s self-reliant development model. A branch office of ASA consists of one branch manager and four credit officers.

14.7. Risk Management

From the beginning ASA’s objective was to develop a cost effective microfinance model which can be attained through financial sustainability and meet overhead cost through service charges. There is no accountant and no cashier in the branch so record keeping has been made simple and easy. ASA took a revolutionary approach to its accounting system, which is completely different than the traditional system. All records regarding savings and credit accounts are possible to post in one page for a whole month.

14.8. Human Resource Management

ASA thinks that formal training is not very important for human resource development, but that on the job training is very valuable for micro finance operations. For example the credit officer of ASA has an opportunity to learn from the branch manager because they all sit at one table in the same room. They have the opportunity to develop their skills by sharing ideas and experiences through learning by doing. ASA always wants to hire a small number of people who are less educated so that they may reduce the operational cost. Since ASA’s system is easy to understand, people with less education can be utilized in a productive way. [8]

14.9. Leadership

ASA leadership plays a remarkable role in initiating new activities and diversifying the organization as per the peoples’ needs. The top management of ASA always tries to develop new products and flexible mechanisms if it seems to be viable. On the other hand, whenever ASA finds that the policy and procedures of microfinance programs are not effective or if there is any risk to reach the objectives, the management takes quick steps to modify or close the program.

14.10. Decentralized Management

ASA is able to have a simplified and flexible microfinance operation due to its highly decentralized management system. ASA field staffs are authorized to manage and run the programs independently, which is very helpful for fast expansion and cost-effective operation. Each and every ASA branch office performs all financial and administrative functions with the help of the well-written operational manual, without any prior approval from the head office.

14.11. Innovative Supervisory Structure

The regional manager (RM), divisional manager (DM) and auditor operate at the field level and use the field level offices. They do not have separate offices or staff. The monitoring system is very effective since the central and mid level management have close contact to field level staff.

14.12. Simple Methodology

ASA’s methodology has been developed to reduce paper work and formalities. There is decentralized decision making for quick decisions; standardized loan amounts, which reduce the need for calculating interests and reduces cost; and interest calculations on savings are included in a model, for the staff to follow. [8]

15. Impact of ASA’s Credit and Savings

Program

After participating at ASA’s micro credit program women were able to generate income for family need and also save surplus money. It increases their social status. ASA’s micro credit programs brought social well-being to the poor households. One impact assessment on how the poor are being benefited out of their efforts made in their own business has been done through a questionnaire by the ASA research section. According to the findings, the borrower’s status in their own household families has been improved satisfactorily. The findings shows that, for income generating activities, job has been created which reduced the unemployment problem and makes the program sustainable.

In the same time ASA’s Micro credit program helps to improve the life of rural people and increase their income. These small-scale economic enterprises have created employment opportunity for their neighbor who is unemployed.

16. Challenges with Project

Implementation

Several studies show small and mid-level NGOs manage 40%-50% loan fund by mobilizing savings. Savings program helps institution to present itself as a self-reliant organization. ASA able to raise 25.66% fund from saving mobilize of their total fund besides giving withdrawal flexibility. But more important that saving is saver’s power at good day but it is strong asset in a moment of crisis. It is one of the important tools to improve economic life of

As ASA offered attractive multiple saving schemes to group members like associate saving account and long-term saving along with attractive interest rate to mobilize more savings. But in reality ASA did not get a remarkable response because practically several members came to save from the same family and in most cases the person earning in one family us not more than one. So, income of one person is divided and saved into different accounts. This process increases saving accounts but does not increase saving deposits amount in fact.

17. Problem Identification

a. First constraint to implement the project is the lack of legal framework. It is mentioned previously that there is no proper law which can guide NGOs to mobilize saving. Existing law does not provide facility MFIs to mobilize savings from nonmembers. To overcome this problem government can help MFIs and Central bank can a play important role.

b. The structure of the Organization needs to be changed since people do not feel secured about their money with existing simple office structure of MFIs.

Members can save only during the group meeting, which held for less than an hour. Some of them can’t attend group meeting. They need to wait for next meeting. So that within this time it is very tough for members to keep this cash in hand.

c. Source of fund from PKSF is available with 7% interest rate. But estimated cost of mobilizing savings from members is minimum 10%. For this reason most of the MFIs are not interested to mobilize saving from members.

d. Few NGOs in Bangladesh fraud with their members. Though numbers are neglected but they escaped away with huge amount of savings deposits, which damaged whole market, and people lost their confidence on NGOs.

e. Credit and saving program is interlinked and transactions take place during the weekly group meetings. ASA collects both deposits-savings and installments in the same weekly meeting. As a result of that credit officer is more concern about the loan collection rather than voluntary savings deposits. [8]

18. Recommendations

a. They should impose proper law for the NGO’s to operate at ease, also seminars and meetings should be conducted to generate and formulate ideas to an effective legal framework. b. Through the market analysis we can classify total population in three groups: Rich, Middle, Poor and Very Poor. ASA do not expect more savings deposits from the very poor people since their weekly income is not more than $1 to $2. They should target the poor and middle class people to encourage them to deposit more savings. To attract middle class people MFIs need to change their office structure with a lucrative office environment, permanent building structure, and professional staffs that will help to increase people confidence.

c. In fact the beneficiaries of MFIs are able to save once in a week during their weekly meeting and branch office continues till 4:00 A.M. But time flexibility is so important to encourage saving mobilization. Most of the poor people work during the day and they receive their earnings at the evening after complete the day work. So, it is important to think about providing evening service or window service at the office.

d. They should arrangement and options for professional personnel for ongoing weekly meeting the mass savings collections to prevent interrupting the credit program.

e. MFIs policy is different than others financial institution and MFIs always emphasize on human quality and moral obligation. On top of that security or mortgage to secure the disbursed loan amount is not required. So, imposing the banking way of credit scoring methodology for MFIs is neither suitable nor the same savings program like bank are realistic one with lucrative interest rate.

It is important to encourage poor people to save. It is necessary to campaign through national media to teach and educate poor people about the advantage of saving.

Cost effective and innovative program should be developed to improve saving program. Through maximizing efficiency and little flexibility can change the structure and culture of the organization. Donor can supply fund to improve structure of the organization to attract more savers.

19. Conclusion

at ease. ASA established itself as a self-reliant organization after twelve years of successful operation of the micro credit program. Decentralized, diversified management has brought about ASA’s success.

References

[1] Mokbul, morshed Ahmad, The Non-Profit sector: World and Bangladesh.

[2] www.asa.org.bd

[3] Afsan Chowdhury, “Macro story of micro-credit” – Cover Story, Radio series on working children for the BBC, 2000.

[4] asa.org.bd/asa growth from 2000-2015.

[5] MRA (2009), NG0-MFIs in Bangladesh, Volume III, 2006. Micro Credit Regulatory Authority, Dhaka, Bangladesh.

[6] Morduch, J. “Does Microfinance Really Help the Poor: New Evidence from Flagship Programs in Bangladesh.” Paper, Department of Economics and HIID, Harvard University, and Hoover Institution, Stanford University, 1998.

[7] Mian, Md Nannu. 2014. NGO Laws in Bangladesh the Need to harmonize. global journal of politics and law Research. European center for Research, Training and Development UK. Vol. 2 No. 3. pp. 54-63.

[8] Ahmmed, Mostaq, Rural Financial Institutions: Savings mobilization ASA (Association for social advancement).

[9] Mian, Md. Nannu. 2014. NGO Laws in Bangladesh: The need to Hormonize, Global Journal of Politics and Law Research. European Centre for Research Training and Development UK. Vol. 2, no. 3. pp. 54-63).

[10] Archi, Rumana Amin. 2008. NGO Accountability; Undermines responsiveness to the Beneficiaries? Case studies from Bangladesh. Netherland: Institute of Social Science.

[11] Cousins William, "Non-Governmental Initiatives" in ADB, The Urban Poor and Basic Infrastructure Services in Asia and the Pacific". Asian Development Bank, Manila, 1991.

[12] ASA’s Culture, Competition and Choice: Introducing Savings Services into a Micro Credit Institution, Graham A. N. Wright, Robert Peck Cristen and Imran Matin, Published by Micro Save- Africa, 2001.