A Boundary Element Formulation for the Pricing of

Barrier Options

Shih-Yu Shen1, Yi-Long Hsiao2

1Institute of Applied Mathematics, National Cheng-Kung University, Taiwan 2Department of Finance, National Dong Hwa University, Taiwan.

Email: [email protected], [email protected] Received March 13, 2013; revised April 25, 2013; accepted May 1,2013

Copyright © 2013 Shih-Yu Shen, Yi-Long Hsiaoy. This is an open access article distributed under the Creative Commons Attribu-tion License, which permits unrestricted use, distribuAttribu-tion, and reproducAttribu-tion in any medium, provided the original work is properly cited.

ABSTRACT

In this article, we derive a boundary element formulation for the pricing of barrier option. The price of a barrier option is modeled as the solution of Black-Scholes’ equation. Then the problem is transformed to a boundary value problem of heat equation with a moving boundary. The boundary integral representation and integral equation are derived. A boundary element method is designed to solve the integral equation. Special quadrature rules for the singular integral are used. A numerical example is also demonstrated. This boundary element formulation is correct.

Keywords: Boundary Element Method; Black-Scholes Equation; Moving Boundary; Option Pricing; Barrier Option

1. Introduction

Boundary element methods are efficient for solving lin- ear partial differential equation. In this paper we discuss a boundary element formulation for the pricing of barrier options. An option which is activated or deactivated once the price of the underlying asset reaches a set level is called a barrier option. The predetermined level is called the barrier. There are two types of barrier options, “in” and “out” options. A barrier option is said to be of knock-out type, if the option is de-activated when the stock price hit the barrier.A payment (the rebate) may be made when a knock-out barrier option is de-activated. The rebate amount may depend on the time of hitting. A barrier option is said to be of knock-in type if the option is activated upon hitting. Barrier options are path-de- pendent exotics. Although our method can be applied on both types, we formulate the method for knock-out call. A knock-out call with constant barrier and zero rebate is easy to price. In this study, we deal with options with time-varied barrier and non-zero rebate.

Since the publication of Black and Scholes’ [1], and Merton’s [2] papers in 1973, the Black-Scholes model has become the preferred framework for option pricing. In the Black-Scholes model, the option price is consi- dered as a function of stock price and time. The option

price can be obtained by solving the Black-

Scholes equation. In 1979, Cox, Ross and Rubinstein [3]

,

c s t

published a paper detailing how the option price can be obtained by evaluating the expected value. Since then, most researchers use probability methods to price options. Some researchers report pricing barrier options by using probability methods as outlined in the literature. For ex- ample, Kunitomo and Ikeda [4] used a serial solution for the probability of the asset price reaching in an interval at the maturity without hitting curved boundaries. As a result, the expected value of the option could be obtained. Geman and Yor [5] followed Kunitomo and Ikeda’s me- thod but used Laplace transform to simplify the formu- lation, while Plesser [6] also followed the same argu- ments but used contour integral to calculate the inverse Laplace transform. In this study, we solve the Black- Scholes equation to obtain the barrier option price.

The Black-Scholes equation is a non-homogeneous linear partial differential equation (PDE). Pricing plain options only needs to solve the initial value problem. However, pricing barrier options and some other exotic options necessitate solving initial-boundary value pro- blems. Domain type numerical methods, such as finite difference method and finite element method, are used to solve these kinds of problems, as in [7-9]. Using a set of variable transformations, the Black-Scholes equation can be converted into a homogeneous linear PDE, i.e., a heat

barrier options. BEMs are rarely applied to financial pro- blems, although Shen and Wang used a BEM to evaluate the expected value of stock price [10].

A stock option represents a contract where the holder is endowed with the right, but not the obligation, to buy or sell a fixed number of shares of a specified common stock at a specific price on or before a certain date. A call option endows the holder with the right to buy the shares, and a put option endows the holder with the right to sell the shears. The stock, the specific price and the certain date are called the underlying asset, the exercise price and the maturity date respectively. In this paper, the price of a barrier option is modeled as a solution of the bound- ary value problem, and a boundary element method is designed to solve the problem. The outline of the paper is arranged as follows. In Section 2, we introduce the ma- thematical model of the knock-out call option. The re- sulting problem is a boundary value problem of a heat equation. In Section 3, the integral representations of the solution of the boundary value problem are derived. An effective boundary element method is designed to solve the boundary value problem in the following section. In Section 5, we show the results of a simple example. The results show the formulation is correct. The last section is a short conclusions.

2. The PDE and the Boundary Conditions

A knock-out call has a barrier. When the stock price touches the barrier, the option becomes null and the op- tion writer may pay the immediate rebate to the option holder. Hence, the value of the option is determined when the stock price touches the barrier. If the stock price does not touch the barrier before maturity, the holder may exer- cise his/her options with the exercise price at maturity.

We follow the arguments of Black and Scholes [1]. The call option price satisfies the Black-Scholes

equation,

,

c s t

2 2

2

2 , , ,

2 s s c s t rs sc s t tc s t rc s t, ,

(1.1)

where s is the underlying asset price, is the time to

maturity, is the risk-free interest rate, and t

r is the

volatility of the underlying asset price.

At maturity, the payoff of the option has to be the maximum of sse and 0, where se is the exercise

price. Therefore, the initial condition is

,0 0, if ., if

e

e e

s s

s c s

s s s s

(1.2)

When the underlying asset price touches the pre- determined barrier s tu

at the time to maturity , theoption holder will receive the immediate rebates t

R t .

Hence, the boundary conditions are

u ,

c s t t R t , (1.3)

A set of variable transformations is used to simplify the mathematical problem. Let

ln ,

x st (1.4)

, ert

ex t,u x t c t

, (1.5)where

2

2

r

. The Black-Scholes equation will be

transformed to a heat equation,

2

,

2 uxx x t u x tt

, . (1.6)

The initial condition becomes

0

0, if ln

,0 ,

e , if ln

e x

e e

x s

u x u x

s x s

(1.7)

and the new boundary conditions are

r ,

r

u b t t R t , (1.8)

where the transformations of the barrier and rebate are

ln

,r u

b t s t t (1.9)

ert

r

R t R t

, (1.10)The PDE (1.6), the initial condition (1.7) and the boundary conditions (1.8) compose a well-posed bound- ary value problem. In the following sections, we derive the boundary integral equation and solve the equation numerically.

3. The Integral Representation

The solution of the boundary value problem can be for- mulated by an integral representation. We describe the integral representation briefly and then perform a limi- ting process to obtain the boundary integral equations in this section. Let G x t x t

, ; ,0 0

be a fundamental solu-tion of the dual equation of Equation (1.6), that is

2 2

0 0 2 0 0

0 0

, ; , , ; ,

2

, ,

G x x t G x t x t

t x

x x t t

(1.11)

where

x t, is the 2-D Dirac delta function. There is a fundamental solution G

x t x t, ; ,0 0

,

0 0

2 0

0 2

2

0 0

, ; ,

1

exp ,

2 2

G x t x t

x x

H t t t tt t

(1.12)

00

0

1, if 0

.

0, if 0

t t H t t

t t

2

0 0

0 2 , , , ; , d

0.

r l T b t

xx t

b t u x t u x t G x t x t x

dt(1.13)

Since u x t

, fulfills Equation (1.6) in domain

x t, 0 t T x, b tr

, we obtain the integral representation for the point Applying the integration by parts on Equation (1.13),

x t0,0

in domain . The integral representation iswe have

2

0 0 0 0 0 0 0

2

0

0 0 0 0 0

0

d

( , ) , , ; , , ; , d

2 d

, , ; , d ,0; ,

2

r

T

r x r r r

T b

x r r

u x t u b t t G b t t x t b t G b t t x t t t

u b t t G b t t x t t u x G x x t x

d

(1.14)

Because the solution u x t

, is continuous on the set,

x t, 0t , b tr

T x , the limit has to be

the boundary value when the point

x t0,0 approaches the boundary point

b tr

0 ,t0

, that is

0 0

2

0 0 0 0 0 0 0

2

0

0 0 0 0 0

0

d

, lim , , ; , , ; ,

2 d

, , ; , d ,0; , d

2

r

r

T

r r x r r r

x b t

T b

x r r

u b t t u b t t G b t t x t b t G b t t x t t

t

u b t t G b t t x t t u x G x x t x

d .

(1.15)

Be noted that

0

0 0

2 2

0 0 0 0 0 0

0 0

1

lim , , ; , d , , , ; , d ,

2 2 2

r

T t

r x r r r x r r

x b t

u b t t G b t t x t t u b t t u b t t G b t t b t t t

−

(1.16)where the principal value integral is defined as

0 2 0 2

0 0 0 0

0 , 2 , ; , d lim0 0 , 2 , ;

t t

r x r r r x r r

u b t t G b t t b t t t u b t t G b t t b t t t

− , d .

(1.17)

Therefore, Equation (1.15) becomes

0 0

0

2

0 0 0 0 0 0 0 0

2 0

0 0 0 0 0

0

1 d

, , , ; , d , , ;

2 2 d

, , ; , d ,0; , d

2

r

t t

r r x r r r r r r

t b

x r r r r

u b t t u b t t G b t t b t t t u b t t b t G b t t b t t t

t

u b t t G b t t b t t t u x G x b t t x

− , d

(1.18)

In Equations (1.18), ux

b t tr

,

is unknown function. For convenience, let

,

r x r .

f t u b t t (1.19)

Substituting the boundary conditions (1.8) into Equation (1.18), we obtain Equation (1.20).

0 0

0

2

0 0 0 0 0

2

0

0 0 0 0 0

0

1 d

, ; , d , ; , d

2 2 d

, ; , d ,0; , d

2

r

t t

r r x r r r r r r

t b

r r r r

R t R t G b t t b t t t R t b t G b t t b t t t

t

f t G b t t b t t t u x G x b t t x

0 0

Equation (1.20) is the boundary integral equation for the unknown function fr

t .4. Boundary Element Formulation

In this section, a boundary element method is designed to solve the moving boundary value problem. In order to evaluate u x t

, , the function fr

t of Equation (1.20)have to be first.

We consider that the problem tim

solved

has to be solved on the e interval

0,T . To start the discretization, the timeinterval

0,T is divided into n elements. Let ti i tbe the nodes, and ti i 1 t

be the collocation

2

points, where t T n

and .

rete b ies be

1, 2, ,

i n

r

Let the disc oundar xi b tr

i

, discreteboundary velocities r

r r1 i i iv x x t, and discrete

boundary values r

i r

u R , the boundaries

are approximated by p ear functions. Thus the

i

t . In this way iecewise lin

approximated boundarie b tr

is

r

r i i

b t x tt

(1.21)for

1 1 .

r

i

v

i1, i

t t t .

sing piecewi U

ha

se constant interpolating functions, we

(1.22) ve

1 , n rr i i

i

R t u t

1 , n rr i i

i

f t f t

(1.23)where R tr

and

r

f t are the approximations for

r

R t and fr

t , r ively, andift t t espect

11 1,

, 1, 2, , 0, if or

i i i

i i

t i

t t t t

n.

Substituting these approximations into the boundary integral Equation (1.20) at the collocation points, we have

1 1 1 1 1 2 0 0 1, d , ; , d

2 2

, ; , d ,0; , d

2 i i i i r i n t r r

r k i t x r r k k i i t r r k k

i i

n

t b

r

i t r r k k r k k i

t t t u v G b t t b t t t 2

1 n r ti , ;

R t u G b t t b

f G b t t b t t t u x G x b t t x

− (1.24) Let, d ,

1

, i , ;

i t r

i t r

D x t G b x t

(1.25)

1

, i , ; , d

i

t r

i t r

E x t G b x t ,

and; , d .

(1.26)

0

0

, br ,0

I x t

u G x t (1.27)The quadrature rule for can be

follows.

,

r i

D x t derived as

1 1 2 2 2 1, , ; , d exp d

2 2

i i

i i

r r i i i

t t

r

i t r t

x v t x

D x t G b x t

t t

(1.28)Let

z t and

r r

r xi vi t ti x

, then

1

12 2 2 2 2 2 2 2 1 1

, exp d exp exp

2 2

2 2

i i

i i 2

d . 2

r r

t t t t

r r r i i

i t t t t

v v z

D x t z z

z z z z

(1.29)Assuming is small, the integral approximates

r rv zi

1

i i

t t

2 1 22 2 2

2

, exp

r r r r iv vi

D x t 1 exp d ,

2 2 2

i i

t t

i r

i t t z

z z

(1.30)where 1

2

i i

i i

t t

t t

0 2 22 2 22 2 2

1 2

, exp d exp

2 2

2 2 2

a

D s erf

s s

and (1.31)

2 2 , , 2 exp . 2 P v v v (1.32)Then we have the quadrature rule for r

, ,i

D x t

1

,

, , ,

r i

r a r i a r i r i i

D x t

D t t D t t P v t t

, ,

where

(1.33)

r r

,r xi vi t ti x

Similarly, quadrature rules for r

, isi

E x t

2

1

i a i i r i i 2 i

1

, , , , , , ,

r

r r i r

r a r

v

E x t E tt E tt P v tt D x t (1.34)

re whe

2 20 2 3

2 , exp d 2 2 , 2 a E z z z sign erf

1, if 0.1, if 0

sign

Simpson’s rule is used for the quadrature rule of integral I x t

, . Let

, , ,

r

i k i r k k

D D b t t (1.35)

, , ,

r i k

E Ei b tr k tk

(1.36)

,

.k r k k

I I b t t (1.37)

The boundary integral Equation (1.20) becomes

2 , 1

2

k k

r r r rr

u v D f D I

(1 , , 1 1 1 2 2 2 k r r k i i ki

i i i k i i k k

i i

u u E

.38)

and where r k f , i k E nging

are the unknowns. It should be

and are zeros when

earra Equation (1.38), ve

noted that

,

i k

D

R

ik.

we ha 2 2 1 1 2 2 k

r r r

k k i k

i

f u u E

, 2 1 , , 1 1 1 2 i k k

r r r

i i i k i i k k

i i

u v D f D I

,

2 Dk k

(1.39)Equation (1.39) is the stepping equation. Therefore, we may solve f1r,f2r, 3r, , nr

(1.25)-(1.27), the nu

f f sequen-

tially. By using the functions merical

solution of u x t( , ) is

2 1 2 1 1 , , 2 , , 2 n r r i i i n nr r r r r i i i i i

i i

u x t u E x t

u v D x t f D x t I x t

, . (1.40)The option price c s t

, can be obtained by the in-verse transformation,

, e rt

lnc s t u (1.41)

where

, ,st t

2

2

r

.

5. A Numerical Example

In this section,a numerical example is presented to verify the boundary element formulation. We compute the pri- ces of an option with a barrier. we consider a knock-out call. The barrier su

t su

txer

is 100, i.e. is a constant

with respect to time to maturity. The e cise price

seand rebate

R are 80 a assetnd 0 respe of underlying

ctively. The volatility

and risk free interest rate

rare 0.02 a ectively. In t , close form

solution is available. Figure 1 shows the option price

gure, time to maturity n with dashed line. The

le, B

to a e

nd 0.2 resp his case

with respect to asset price. In this fi is 0.5. The exact prices are draw

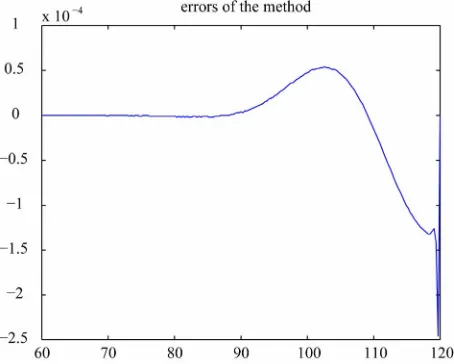

solid and dashed lines can not be distinct. Therefore we use Figure 2 to show the differences between the exact

and numerical solutions. The differences are small.

6. Conclusion

[image:5.595.63.541.87.606.2]Figure 1. The numerical and exact solutions of c s t

, solutions arecide in . In

this figure, time to maturity is 0.5. The exact drawn with dashed line, but the two curves coin figure. Here

this 0.2

and n500 are used.

Figure 2. The differences between the exact and num solutions. The differences are small.

Finally, the method is applied to a barrier option. This formulation is correct.

S

637-659. doi:10.1086/260062

erical

REFERENCE

[1] F. Black and M. Scholes, “The Pricing of Options and Corporate Liabilities,” Journal of Political Economy, Vol. 81, No. 3, 1973, pp.

[2] R. C. Merton, “Theory of Rational Option Pricing,” Bell

Journal of Ec nt Science, Vol. 4,

No. 1, 1973, pp.

onomics and Manageme

141-183. doi:10.2307/3003143

[3] J. C. Cox, S. A. Ross and M. Rubinstein, “Option Pricing: A Simplified Approach,” Journal of Financial Economics,

Vol. 7, 1979, pp. 229-264.

doi:10.1016/0304-405X(79)90015-1

[4] N. Kunitomo and M. Ikeda, “Pricing Options with Curved Boundaries,” Mathematical Finance, Vol. 2, No. 4, 1992,

pp. 275-298. doi:10.1111/j.1467-9965.1992.tb00033.x

[5] H. Geman and M. Yor, “Pricing and Hedging Double- Barrier Options: A Probabilistic App

cal Finance, Vol. 6, No. 4, 1996, pp. 3

roach,” Mathemati-

65-378.

doi:10.1111/j.1467-9965.1996.tb00122.x

[6] A. Pelsser, “Pricing Double Barrier Options Using La- place Transforms,” Finance and Stochastics, Vol. 4, No.

1, 2000, pp. 95-104. doi:10.1007/s007800050005

[7] R. Zvan, K. R. Vetzal and P. A. Forsyth, “PDE Methods for Pricing Barrier Options,” Journal of Econo

namics & Control, Vol. 24, No. 11, 2000,

mics Dy-

pp. 1563-1590.

doi:10.1016/S0165-1889(00)00002-6

[8] S. Sanfelici, “Galerkin Infinite Element Approximation for Pricing Barrier Options and Options with Discontin- uous Payoff,” Decisions in Economics and Finance, Vol.

27, No. 2, 2004, pp. 125-151.

doi:10.1007/s10203-004-0046-1

A. M. L. Wang, Y. H. Liu and Y. L. H

[9] siao, “Barrier Op-

tion Pricing: A Hybrid Method Approach,” Quantitative Finance, Vol. 9, No. 3, 2009, pp. 341-352.

doi:10.1080/14697680802595593

[10] S. Y. Shen and A. M. L. Wang, “On Stop-Loss Strategies for Stock Investments,” Applied Mathematics and Com- putation, Vol. 119, 2001, pp. 317-337.

[image:6.595.59.286.346.528.2]