International Journal of Emerging Technology and Advanced Engineering

Website: www.ijetae.com (ISSN 2250-2459, ISO 9001:2008 Certified Journal, Volume 8, Issue 2, February 2018)

1

The Role of Financial Sector Restructuring Process in the

Development of Commercial Banks in Libya

Sasi Elokkaz

Faculty of Business, Singidunum University, PO box 32 Danijelova St., Belgrade, Serbia

Abstract— The banking system is essential base for the

development of productive sectors in the national economy. The importance of the role it plays is in the pool of savings in other sectors and paid to the various investment channels through loans and credit facilities. Banking services provided by them and to whole society as the effectiveness of the role played by banks to be affecting a large extent in the structure of the banking system, the degree of organization, and the tasks entrusted to it and the powers conferred upon it.

The restructuring of banks which considers privatization , mergers and acquisitions in banking sector achieves financial andeconomic savings represented in increased growth rates, greater productivity, increased profits and expanded deposits base, which achieve international competitiveness through renewable technologies and qualified human resources; this was to be achieved in each bank individually.

This restructure will open new markets for revenue and creating the conditions for diversifying banking services, which would lead to strengthening the position of the bank in the banking market.

Keywords—financial sector, restructuring, merger, banks

I. INTRODUCTION

The Libyan banking sector plays an effective and prominent role in the development of the national economy; the sector is the main supporter and promoter of economic activity and development, particularly following the decision, on 11 September 1969, to nationalise banks operating in Libya.

If a group of accountants, and some analysts in the comparative economy were asked about the reasons for banks or financial institutions to merge and integrate with each other, they would give two sets of answers. However, there are two key factors affecting the need for financial institutions to enjoy a competitive advantage, namely technological developments, and economic liberalisation. Regarding technology, it is notable for removing the dividing lines that define specialisation among financial intermediaries. As a result, it enables merged partners to create huge financial supermarkets, where customers can take advantage of many financial services in one place, and at a lower cost.

With regard to economic liberalisation or deregulation, it has fundamentally changed banking concepts and location; for example, it has become possible for banks to engage in investment banking and brokerage activities, with the purchase and sale of securities, and other associated activities; moreover, geographical boundaries have ceased to exist, where banks are able to extend activities to different geographical areas.

The two former factors in their interaction together have led to the emergence of the global economy. This modern concept has added impetus to the merger and integration activities between financial institutions.

II. THE HISTORY OF THE BANKING SECTOR DEVELOPMENT IN LIBYA

The banking system of the national economy as the heart of the living, and influence (goods of banking system) is as the blood for human body, and it reflects the seriousness and importance of the banking system for the national economy. The creation of money like renew of blood is the function of the banking system, and plays a critical role within the national economy, as that the movement of economic activity is achieved through the banking system. Over the past years the competition increased between banks as units of the banking sector, where it was to increase the number of banks and their subsidiaries, as well as the emergence of many other non banking financial institutions that had a significant impact on the intensification of this competition, in addition to the adoption of these units on the traditional elements of marketing mixture (product, price, promotion and place).

The recent years in Libya witnessed many eminent developments, among which is privatization program embodied in submitting many capitals of business companies in the state to public subscription , in a manner that leads to increase of flow of capitals inside and abroad.

International Journal of Emerging Technology and Advanced Engineering

Website: www.ijetae.com (ISSN 2250-2459, ISO 9001:2008 Certified Journal, Volume 8, Issue 2, February 2018)

2

The state continued in supporting policies of liberation of exchange rates of foreign currencies, which caused stability of exchange rates. And the state continued disposition to liberate foreign commerce and encouraging export so as to actively contribute in supporting averages of economic growth and achievement of comprehensive development.Such results of economic growth reflected in the increase of challenges in the bank field before banks to escort such achievements and developments, as well as doing their role in the field of financing economic activity.

III. A BRIEF OVERVIEW OF THE BANKING ACTIVITY IN LIBYA AND THE CURRENT BANKING SYSTEM

The banking activities in Libya Began since the Ottoman period to establish the first agricultural bank in 1868 the city of Benghazi,(Aalbyian Alawal) and the last city, Tripoli in 1906 and during the Italian occupation the Italian bank opened branches as follows cantilena Bank 1912 Bank of Italians in 1912,the Bank of Naples in 1913 in addition to the establishment of two savings, one in Tripoli and the other in Benghazi was the mission of the banks at that time confined to the opening of credit to commercial and Italian colonizers only at the beginning of 1948 opened the British Barclays Bank branches in the other in Benghazi and Tripoli, and was engaged as a commercial activity as well as services that were performed British military administration in 1951 issued the interim government at the time Exchange Act No. 4 for the year 1951, which was founded by which of the Monetary Committee, which was

responsible for the management and the issuance of Libyan currency opened in the period 1951-1955 between the branches of the following banks (Bank of Naples - Sychelna - Bank of Rome), which had closed down the impact of Italy's defeat in World War II and opened in the same period branches of the British Bank of the Middle East and the Arab Bank, the Egyptian and Tunisian and Algerian bank. The opening of eight foreign banks to bear the nationalities of different countries are: UK / Italy / Egypt / Jordan / France, and mainly concentrated in the cities of Tripoli and Benghazi and most of these banks was related to the financing of trading operations, The Libyan National Bank began to engage in business as a commercial bank and the Department engaged in its work to central banking. It has been issued the Banking Act No. (4), for the year 1963, which changed the name under which the National Bank of Libya to the Central Bank of Libya.

The banking system has gone through after the Libyan important stages had a great role in changing the pattern and the policy of the device and its development phase has begun the stage of foreign ownership and nationalization approved until I got to the stage growth and development. The following is a brief explanation of these stages:

A - The period between the years (1951-1969 B - The second period (1963-1969):

C - The third period (1970-1993): D - The fourth period: (1993-2005)

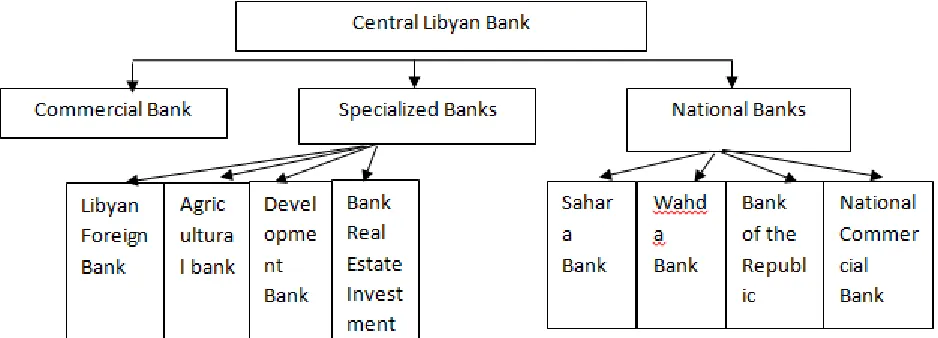

Figure (1) shows the structure of the general banking in Libya.

[image:2.612.73.542.507.676.2]International Journal of Emerging Technology and Advanced Engineering

Website: www.ijetae.com (ISSN 2250-2459, ISO 9001:2008 Certified Journal, Volume 8, Issue 2, February 2018)

3

IV. PRIVATIZATION AND MERGERS PROCESS IN LIBYANBANKING SECTOR

The main objective of the multiplicity of labels that indicate the substance to the policy of privatization, is the desire to adopt idiomatically appeals to the masses of people in the state that take this policy, and to convince the workers in the companies targeted by the privatization policy in cooperation with the State concerned in bringing about the transformation required in the form of management and ownership , and work to reduce the state's role in the economic field, so do not rule out the role perfectly, but to devote to planning, supervision and control over the strategic level, with the transfer of ownership of economic units public to the private sector, through the sale of partially or completely to the private sector, hence the concept of privatization is about to make room for the private sector, and reducing the role of the public sector, and by participating in the exercise of economic activities in the light of the principle of competition and equal opportunities, according to the rules of the market and the free economy, and in the framework of plans and programs are clear and explicit and realistic can be implemented.

Privatization is definition as transfer of ownership of units of the public to the private sector, as a result of economic recession and weak financial and administrative performance, as well as what the global economic globalization and increased competition.

In order to identify the policy of privatization on the international level, it requires study and analysis of the international concept of privatization and its objectives and the main criticism directed to them.

The restructure processes which considers privatization, merger and integration as a means to growth and cooperation and integration between the merged banks would lead to reducing the costs, opening of new markets for revenue and creating the conditions for diversifying banking services and strengthening the position of the bank in the banking market.

V. THE TRANSFORMATION TO PRIVATE SECTOR IN BANKING SYSTEM

The privatization policy can raise the efficiency of the company, which turns from the public sector to the private sector by reducing political influence on the decisions of the company, and put managers in the position of direct responsibility to shareholders, and to force public companies nature monopoly or quasi-monopoly on the face of competition and the reduction of its forces monopolistic, with the need to rid the state of the obligation imposed on it constantly cover the losses of public companies and the elimination of the fundamental problems plaguing the public sector.

The realization of the privatization policy to the goal of expanding the scope of private ownership would depend on the ability of the private sector and individuals to absorb the supply of public sector units for sale.

Difficult to transfer ownership of public enterprises to the private sector in a practical way without securities market is efficient, although experience has shown that in some developing countries.

Possible to carry out many of the studies and research on the relationship between the efficiency of the securities markets and the success of the goal of broadening the base of ownership.

Governments should normally not privatize banking sector before an appropriate regulatory framework has been established. This framework includes anti-trust regulation to ensure competition where feasible, and specialized regulation to oversee activities where an element of monopoly is likely to persist.

If banking sector are restructured prior to privatization, the time of restructuration is the point where future employment conditions, wages and benefits should be discussed with banks employees. The new regime would be compatible with prevailing conditions in the private sector.

International Journal of Emerging Technology and Advanced Engineering

Website: www.ijetae.com (ISSN 2250-2459, ISO 9001:2008 Certified Journal, Volume 8, Issue 2, February 2018)

4

The choice of privatization methods is be guided by the size of the enterprises to be sold, market conditions and the objectives of the privatization process.Privatization by allowing banks to adjust their own capital structure is supported by state. Strong governance mechanisms are in this case needed to ensure that bank management continues to act in the interest of the government owner.

The definition of the further analysis of techniques have revealed the importance of recognizing the role of employees in firms. If employees are given more influence and incentives, such as additional training, compensation, benefits their job satisfaction increases, which in turn encourages a customer-oriented approach and improves firm productivity.

VI. THE OBSTACLES AND PROBLEMS ENCOUNTERING THE PRIVATIZATION PROGRAM IN THE LIBYAN BANKING

SECTOR.

Privatization obstacles and difficulties in Libya:

A set of problems and difficulties are encountered in the course of privatization program in all world states. These obstacles may hinder the accomplishment of the goals which the privatization intends to accomplish. In this regard, the researcher dealt with the privatization program in Libya, indicating in the meantime some of these problems. He concluded that the most of these problems and obstacles which ought to be dealt with and treated are:

- Labour surplus problem.

- Increase in debits and obligations on companies and factories subject of privatization.

- Lack of existence of an organized security market. - The negative economic performance of the public

projects.

- Restriction to certain methods of privatization.

In a study about the obstacles encountered by the foreign investments, it has been shown that the most problems facing the foreign investors in Libya include:

- Poor infrastructure. - Poor local management. - Poor data and information. - Lack of sufficient guarantees.

- Business transactions depending on interpersonal relationships.

From the some open air interviews with Libyan businessmen, it was clear that the problems encountering the privatization processes include:-

- Shortage of local finance.

- The picture of the past policies which created lack of trust in private sector.

- Lack of administrative stability including the legislations and laws.

- Lack of organized budget and repayment of contractors due on time.

- Slowness of the banking procedures regarding opening of credits and granting of credit facilitations.

The national sector and the small projects in particular encounter several difficulties, most of which:

- Administrative and marketing problems.

- Shortage of well experienced and well qualified labour in the technical areas of concern.

- Lack of finance.

- Increase in the nonexistent credits. - Improper economic conditions.

VII. THE DIFFICULTIES FACING THE TRANSFORMATION PROGRAM IN THE BANKING SECTOR

- Lack of existence of clear monetary policies, while there are restrictions on the foreign currency transfer, and this does not encourage the privatization process. - - The existence of tax and duties laws which do not

encourage the growth and flourishing of the companies and private projects.

- Non sufficiency in the transparency and freedom of exchange of information relating to the local economic reality through IT and communications. - Shortage of the well drawn, well studied long term

administrative strategic plans which promote and encourage the transfer to the private sector.

- Absence of the lawful and legal guarantees sufficient to the stability of the privatization process, in addition to the lack of assurances that the big private companies would be transferred into public companies thereafter.

- The local market is small in size , and this does not encourage the spread of private companies and projects.

International Journal of Emerging Technology and Advanced Engineering

Website: www.ijetae.com (ISSN 2250-2459, ISO 9001:2008 Certified Journal, Volume 8, Issue 2, February 2018)

5

VIII. EXPENDING THE OWNERSHIP BASE IN THE LIBYANBANKING SECTOR

The transformation and expansion of the ownership base of the public commerce banks into the national sector falls in the frame of work transformation of a great number of public institutions and economic units into the national sector in a manner which can lead into their promotion of their economic efficiency . In this regard, the Central Bank of Libya intends behind the privatization program to accomplish the following:

- Realization of the banking competency both on the national and international levels.

- Keeping pace with the events and developments in the banking industries.

- Promoting the efficiency of the performance levels through the optimal utilization of the work force. - Support of the trust and transparency in the banking

system in a way leading to the improvement of the monetary system performance.

IX. THE PRACTICAL STEPS INTRODUCED BY THE CENTRAL BANK OF LIBYA FOR PRIVATIZATION OF BANKS

In compliance with the resolution of the General People's Committee no.(184) for the year 2001 concerning the permission to privatize some public companies and economic units, and on the decision issued by the secretariat of General People's Committee in its 33rd meeting for the year 2003 permitting the Central Bank of Libya to take the necessary procedures to privatize the Sahara Bank, therefore, the Central Bank of Libya took the following measures:

A technical committee was formed which was authorized to take the necessary procedures to privatize the Sahara Bank, supervising the various stages and steps of privatization process, in particular, the committee assumes the following tasks:

1.Determines the net real value and also the proper value of the share by using the proper evaluation methods.

2.To take the necessary procedures to float the shares forming the bank's capital for subscription and supervising the various stages of privatization. 3.Delivery of the new financial position to bank's board

of directors which will be chosen from among the general assembly after transformation of ownership (Privatization).

X. EVALUATING A COMMERCE BANK

The process of evaluation of a commerce bank includes a set of different steps consisting procedures and methods which conform with the nature of each item of the evaluation items. The most steps of evaluation procedures, including the processes and methods which need to be followed in order to arrive to the justified value of the financial position of the bank and thus to the justified value of the share are as follows:

- Step one: Data information gathering:

In this step, all data and information related to the concerned bank will be gathered. Such details would include all aspects relating to the various activity of the bank – Organizational – legal – financial – technical or otherwise

- Step two: Examination and auditing of the data and information.

- This step requires formation of specialized work teams in legal, financial and banking areas. Its task will be the examination and auditing the data and information which were gathered previously:

- The examination and auditing process includes: - Examination and auditing the legal form of the bank. - Examination and auditing all financial aspects which

include all items of the main accounts mentioned in the financial statement, the result accounts, among of which are the following items:

* Cash-trusts and balances (Deposits) at local banks, and the trusts and deposits with correspondences, the credit facilitations, documentary credits, performance bonds, promissory, investment portfolios, security bills, (notes), fixed assets, other debited balances, bank checks, outstanding accounts, allocations, the reserve for assets prices rise, copyrights.

International Journal of Emerging Technology and Advanced Engineering

Website: www.ijetae.com (ISSN 2250-2459, ISO 9001:2008 Certified Journal, Volume 8, Issue 2, February 2018)

6

- Comparison statements of a number of years,analyzing them horizontally or vertically according to the trends.

- The percent and rates relevant to the indicators of liquidity, debit and profitability.

After the completion of the analysis of the data and information obtained from the bank for the evaluation purposes , and according to the various reports gained by the work teams , a set of proper to evaluation methods as proper to the given item will be applied . Among the most important methods used in this regard:

1- The book value method.

2- The equivalent book value method. 3- The net current value method.

4- Any other method deemed proper by the evaluator.

Step four:- The results and recommendations.

In this step conclusions and results of the evaluation process are extracted and obtained, briefly reviewed, showing how they are achieved and the justification thereof and the comments of the evaluator regarding them.

The evaluation results reflect by preparing a financial position showing the assets and the real obligations of the bank, the equivalent value of the ownership rights and to the share, including the best alternatives which to be evaluated so to be a basis for the continuance of the success of the bank, like for example offering shares for subscription by natural and ordinary persons and through joint venture with safe authorities.

XI. PRIVATIZATION OF THE SAHARA BANK

A preview about the Sahara Bank

Sahara Bank was founded and started its activity in 1964. Libyan s and some foreign banks subscribed in the capital of the Sahara Bank. In 1970 and in the course of nationalization of banks and some other sectors, a decision was issued to nationalize this bank , that's the share of the foreign partner, which portion was reinstated to the Central Bank of Libya. Since its incorporation , the bank provided banking services to its customers , where it financed several public enterprises and private companies both serviceable and producers which enabled these institutions to execute their programs in the field of servicing the economic development in the country and in the framework of broadening the ownership base thus , enhancing the role of the national sector and opening the way for it for the investment in all and different economic activity and contributing into the execution of the economic development in the country.

In an attempt to promote and develop the banking sector and reconstruction of banks in a manner that achieves a competency reflects the efficiency of utilizing the resources and provision of well distinguished banking services, the Central Bank of Libya decided to sell its share in the Sahara Bank.

The nature of the Sahara Bank activity:

Carrying out all sorts of banking activities vested unto commerce banks, such as accepting under call trusts or the future trusts, opening of current bank accounts, grants loans and facilities, including the activity of foreign currency exchange and any other activity as set forth in the articles of incorporation of the bank.

The development of the bank capital and sources of financing:

With regard to the profits gained by the Sahara Bank during its years of activity, it distributed some of that profits on the shareholders and some of it added to the reserves, whether according to the rules set forth by the commerce law to form such reserves or the alternative reserves which were formed on the intention to support the financial position of the bank. Since the nationalization decision, the Sahara Bank capital was promoted and developed to become 21 million Dinars in 1995 and in 2000 it reached 63 million.

In its meeting held on 22.5.2005, the general assembly of the bank decided to adopt the outcomes of the privatization committee for the evaluation of the bank, it also decided to raise the bank's capital to 126 million Dinars, distributed on 12.600.000 shares, value of each share is 10 dinars per nominal share, provided that the increase in capital would be divided on the bank shareholders in the form of shares.

The bank's branches and correspondences:

1- The local branches /Agencies

There are 46 bank branches and agencies scattered all over the country, including 7 opened agencies.

2- Foreign correspondents:

The bank has a worldwide network of correspondents consisting more than 450 correspondents

3- The legal entity:

A joint venture company, registered in the trade register under no.2775.

4- The bank's legal term is 50 years,automatically renewed.

International Journal of Emerging Technology and Advanced Engineering

Website: www.ijetae.com (ISSN 2250-2459, ISO 9001:2008 Certified Journal, Volume 8, Issue 2, February 2018)

7

There 48 branches serving the customers scattered all over Libya. The list of agents/customers include holders of huge projects in addition to private companies both local and foreign , this important marketing position of the Sahara Bank makes it attractive for joining the banking system in Libya. The privatization process is a part of the reformation program of the Sahara Bank within the banking industry in Libya. Currently there is a program under process through some procedures which include linearization of the rules and regulations relevant to the banking activities such as modernization of the payment systems and establishment of credit offices.In this regard, it has been announced that French BNP PARIBAS Bank will be an strategic partner with the Sahara Bank , after it has been chosen by the Central Bank of Libya to be the first foreign bank provides complete banking activities and services in Libya, according to the strategic plan of the bank .

According to the new agreement BNP PARIBAS, offered 145 million euro (USD200) to purchase 19 shares, in addition to its right to increase its share up to 51% during the 3-5 years to come.

BNP PARIBAS enjoys good presence in the Mediterranean territory as the first development priority, in addition to its both local markets (France &Italy).

The bank is also, characterized by a strong position in countries such as( Morocco, Tunisia, Algeria and Turkey). BNP PARIBAS bank has been active in the Arabian Gulf states area for more than 34 years , where it carries its activity in five of those states include (Bahrain, Emirates, Qatar , Kuwait and Saudi Arabia).

The bank which is deemed among the most important European bank in banking services provision has a workforce of 48000 employees in this area. In fact, the bank is among the largest 15 banks in the world. It covers three basic sectors.

1- Investments of the banking institutions. 2- Wealth management.

3- The Banking partition activity.

XII. MERGERS AND ACQUISITION ACTIVITIES IN OPERATING BANKS IN LIBYA

The Central Bank of Libya launched a strategy of restructuring, development, and modernisation of the banking sector. This aimed at raising the level of services to the standard seen in international banking, and realising the Central Bank’s vision.

The strategy followed the political and economic policy trends expressed in Law No. 9 (1992), and Law No. 1 (2005) relating to banks, in addition to General People's Committee Decisions No. 134 (2006) and No. 122 (2004) establishing the Libyan stock market, and ratifying provisions regarding joint stock companies, respectively. The new policies included the restructuring of commercial banks, and a comprehensive programme to modernise, and improve the current performance of commercial banks so as to achieve success in a more liberal and competitive market.

In addition, commercial banks and the banking sector, in general, face significant challenges in coping with this phase of gradual liberalisation of the banking sector. This involves opening it up to international institutions, through mergers, and the entry of new partners; e.g. the European bank, BNP Paribas, formed a strategic partnership with Sahara Bank, and similarly, the Arab Bank with Al-Wihda Bank (the latter in July 2007). The Libyan banking industry is, therefore,required to keep up with the pace of modernity and development, and remain competitive. In addition, the performance and profitability of Libyan banks is subject to scrutiny and monitoring by foreign investors and buyers wishing to gain a foothold in the Libyan banking sector.

The concept of commercial banking is such that a commercial bank is any company that ordinarily accepts deposits into current accounts (payable on demand or after a fixed period), grants loans and credit facilities, and engages in other banking activities, according to the provisions set out in art 65/2 of Law No. 1 (2005). Under this law, a specialist banking entity, which is limited mainly to provision of funding and credit for specific activities, and does not accept deposits payable on demand, is not classed as a commercial bank. However, the Board of Directors of the Central Bank of Libya has discretion to allow a specialist bank to perform activities normally associated with commercial banking, for the benefit of stakeholders.

International Journal of Emerging Technology and Advanced Engineering

Website: www.ijetae.com (ISSN 2250-2459, ISO 9001:2008 Certified Journal, Volume 8, Issue 2, February 2018)

8

Article 73 of Law No. 1 (2005) requires each bank to keep a capital reserve, and to ensure that this reserve is maintained, taking priority over profit dividends distribution. In this context, no less than 25% of net profits must be directed to this reserve until half the paid up capital is achieved, and thereafter this is reduced to 10% of net profits to build up a reserve equal to the operating capital. Article 75 of Law No. 1 (2005) stipulates that banks must keep funds of no less than the total demand liability permanently within Libyan jurisdiction, in addition to an amount equal to the bank's paid-up capital.Furthermore, article 63/4 of Law No. 1 (2005) states that each commercial bank must establish within its management framework, an administrative unit called the Compliance Unit reporting directly to the Board of Directors. The functions of this unit are to follow-up compliance of the Bank and its commitment to the standards that govern daily banking activities, most importantly, monitoring capital bonuses, bank liquidity and reserves, and compliance with international banking standards.

Commercial banks are distinguished from other businesses in three important features relating to profitability, liquidity and security. The importance of these features is due to their tangible influence on shaping the policies related to the key activities undertaken by commercial banks.

Hence, the commercial banks were administratively restructured in accordance with Law No. 1 (2005), where separation in functions was introduced between the Chairman and members of the bank’s (part-time) Board of Directors and the functions of the (full-time) Director-General. The Law also stipulated that Board members must be no less than five, and no more than seven. Under these conditions, forty community banks were merged into the Community Banking Corporation, which was later transformed into a commercial bank in 2006.

In accordance with Resolution No. 49 (2006), some community banks were given the opportunity to either finish raising capital or merge with others no later than 31/3/2007.

Resolution No. 57 (2006) granted bank boards of directors the powers to close, merge, or change the use of bank branches, or convert them into bureaux de change, while the opening of new branches or bureaux remains a decision reserved for the Governors of the Central Bank of Libya.

By the end of spring 2008, all necessary arrangements were finalised for the merger of Ummah and gumhouria Banks into one bank, under the name gumhouria Bank, effective in late 2008.

With the announcement in 17/7/2007 by Central Bank of Libya (cbl.gov.ly) that BNP Paribas had been selected as Sahara Bank’s strategic partner, there were negotiations for many others to enter the Libyan banking market. Therefore,

Libyan commercial banks needed to restructure, and develop and implement change programmes to update and improve performance as the route to achieve profitability and success in a more liberal and competitive market.

Finally, several decisions were issued, including that of the Governors of the Central Bank No.56 (2006) regarding the ratification of the results of the study prepared on the entry strategy for foreign banks into the Libyan banking market, and the restructuring of both the banking and financial sectors. BNP Paribas had already entered as a strategic partner for Sahara Bank, while the Arab Bank had entered as a strategic partner for Wihda Bank.

The decision by the Governors of the Central Bank No. 1 (2008) related to Memoranda and Articles of Association of Libyan banks. The Central Bank Governors also approved the establishment of representative offices for foreign banks; currently, there are 20 such representative offices in the country.

International Journal of Emerging Technology and Advanced Engineering

Website: www.ijetae.com (ISSN 2250-2459, ISO 9001:2008 Certified Journal, Volume 8, Issue 2, February 2018)

9

Table 1Libya Consumer Price Index and inflation rates for period 2011 – 2015

Source: National Authority for Information, 2016 The future monetary policy trends

1. The emphasis is on the revision of the utilizations and rates of the monetary policy tools currently in use, the introduction of new tools that can be used in both financial and monetary markets and the improvement of the monetary and financial indicators that reflect the financial conditions of the banking sector.

2. Continuing the restructuring process of the banking sector through the expansion of its ownership base by selling the shares of Central Bank of Libya in the capitals of the commercial banks, the implementation of the international accounting and auditing standards, improving the loans portfolios of these banks through the independent credit decision making to minimize the risks.

3. Strengthening the banking control and emphasizing the banks commitment to legal requirements in the banking activity.

4. Enforcing the confidence in the banks, letting them compete in the provision of better more timely services, in addition to emphasizing the importance of having a special banking prosecution to resolve issues related to this sector.

5. Introducing new technologies in the banking activities through the completion of all stages of the National Payment System and benefiting of it in the areas of financial settlements, immediate check clearing, and working with credit cards system as means of payment for the commercial purposes and financial transfers, in addition to interlinking all banks and their branches with the Central Bank of Libya.

XIII. THE IMPORTANCE OF PRIVATIZATION AND MERGERS ACTIVITIES

The privatization has become one of the most significant economic phenomena of recent years. As a result of the big changes in global Politics concerning the role of governments regarding the private ownership of firms and property, the concept of privatization may be defined narrowly or broadly. It concerns with the sale of publicly owned enterprises assets or shares to individuals or private firms (the transfer of ownership from public to private).

There are a number of prerequisites for privatization to occur successfully, most importantly, the domestic and external private sector must be sufficiently equipped with adequate managerial and technical capabilities .however, based on the empirical findings of the study, the following tentative recommendations can be made to the Libyan government which may help to introduce and manage a strategic shift towards genuine privatization the banks in Libya.

1-The state must focus on the process of privatization as a way to achieve some of the social and economic objectives reflect the ability of institutions to develop itself in terms of improving the level of services and increase production.

International Journal of Emerging Technology and Advanced Engineering

Website: www.ijetae.com (ISSN 2250-2459, ISO 9001:2008 Certified Journal, Volume 8, Issue 2, February 2018)

10

3-Interest and encourage the work of scientific conferencesand seminars on the impact of privatization on the Libyan economy, in an attempt to see and take advantage of the views expressed, and previous experiences in this area.

4-Must take some important points for the current program of privatization, such as benefit from the Egyptian experience and Malaysian on privatization, in addition to providing a comprehensive reform plan for the institutions unsuccessful.

5-Generally speaking the results indicate that privatization led to on major improvements in the performance of banks, moreover, compared to the relevant literature on the impact of privatization on employment in developing countries, the results indicated that employment was increased, another important results was that there were many barriers and constraints facing the private sector in Libya.

6-Work to develop the stock market to cope with international markets in order to accommodate privatization policies. This would allow the smooth transfer of ownership of the privatized institutions to investors.

7-The major impetus for privatization of SOEs derives from the need to improve the performance of enterprises. However, in an economic environment in which other economic policy reforms implemented simultaneously and in sequence, it becomes difficult to isolate the effects of privatization alone on economic performance. However, as developing country starting its privatization programme at the end of the 1980s, Libya mainly aimed at increasing the productivity of its workforce, improves the level of services and improves conditions for the workforce financially. Financially this can be achieved through providing incentives and bonuses or any other means that encourage workers in increasing productivity. On the other hand by improving the working conditions for the workforce management can also achieve better performance.

8-the Economy in Libya is going through a new phase in terms of the pattern of ownership, as one of the main reasons for the restructuring of financial institutions, monarchy own have had a greater chance to achieve unless the checks in public ownership, and allow the foreign partner in order to achieve competitiveness and exploit all available capacity and starting more freely in the global financial markets And to improve the level of services.

However, the political circumstances in Libya blocked the continuation of the strategy developed for the privatization of banks, and open new horizons to domestic and foreign investment.

9-To realize the suggested methodology for optimal transformation of a domestic bank into a modern European bank it is essential to conduct a realistic analysis of the market in Libya. That will be the base for defining clear guidelines for the transformation of a domestic bank into a modern European bank, clear guidelines of selection, training and motivation of personnel; clear business strategy of a bank and clear goals setting.

XIV. RESULTS

Through the previous view of the theoretical framework and literature study and the results of statistical analysis is clear originality of this research and it's the first of its kind which deals with the role of financial sector restructuring process in the development of commercial banks in Libya and has turned out by answering the questions the following results.

1. There is weakness in the level of expertise for financial sector restructuring process in the development of commercial banks at all levels in Libya, which affects the performance of the work of banking sector. 2. Lack of studies is found to explain the role of financial

sector restructuring process in the development of commercial banks in Libya

3. Reduced levels of administrative decision makers in financial sector restructuring process in the development of commercial banks in Libya . There is weakness in the participation of employees in the preparation of plans of restructuring process and merger activities in the development of commercial banks in Libya

International Journal of Emerging Technology and Advanced Engineering

Website: www.ijetae.com (ISSN 2250-2459, ISO 9001:2008 Certified Journal, Volume 8, Issue 2, February 2018)

11

5. There is lack of coordination between the commercialbanks and universities and higher institutes specialized in the field of finance and banking so as to take advantage of them to attract some of the graduates, including specialists. And there is lack of clear plans for programs and policies that follow the scientific foundations in this field.

6. There are lacks of in some aspects of the organizational structure of the banks and in the multiplicity of departments and there is work with some overlap. And there is weakness in the levels of organizational culture on the levels of planning and development of financial sector restructuring process in commercial banks in Libya

7. There is a clear impact of organizational factors on commercial banks (planning, incentives, and creativity, and behavior, skills) to prepare plans and developmental projects for financial sector restructuring process in Libya. And there is lack of feasibility studies to develop the internal environment and the external environment for this process.

8. Followers of the decentralized style contribute to the increase of the level of performance of employees at commercial banks in Libya.

9. There is weakness in the level of coordination between departments and divisions of banks in financial sector restructuring process in commercial banks in Libya. And there is weak control on some facilities in terms of staff and their behavior.

10. There is lack of formal and informal communication in financial sector restructuring process in the development of commercial banks in Libya. And lack of training of officials of the departments of modern management methods and quality control negatively affects the role of financial sector restructuring process in commercial banks in Libya.

11. There is the absence of constructive competition between the financial institutions which regulate the conduct of their employees in order to achieve restructuring process in the development of commercial banks in Libya.

12. There is a clear failure by the departments in the preparation of plans and training programs for employees in financial sector restructuring process in commercial banks in Libya.

13. There is a weak use of modern scientific styles within departments and sections of the banks in financial sector restructuring process commercial banks in Libya.

14. There is lack of attention to the technical aspects of the Information Technology in banks and the use of technical factors in the development of plans and programs in financial sector restructuring process in commercial banks in Libya for the future.

15. There is lack of familiarity with some of the existing process of planning and designing strategic planning in financial sector restructuring process in the development of commercial banks in Libya

16. There is lack of encouragement by managers at the level of departments and sections of employees in financial sector restructuring process in the commercial banks in Libya

17. The senior management does not pay enough attention to the importance of integration and interaction in financial sector restructuring process in the development of commercial banks in Libya, and not a priority to study and assess this process and its failure to assess the work of banks in Libya.

18. The management staff in banks often does not see what is new in the evolution of modern management in financial sector restructuring process in the commercial banks in Libya and the development concepts and the use of incentive systems to international standards, and do not use scientific methods in the process of differentiation between strategic alternatives of the restructure and merger planning and banking sector development in Libya.

XV. RECOMMENDATIONS

Based on the results reached through the study and analysis, researcher recommends by the following:

1.The management in the Libyan commercial banks need to change their focus from traditional providing banking services on an ongoing basis to focus primarily on the restructuring process and merger activities increasing the quality and technology of banking services;

International Journal of Emerging Technology and Advanced Engineering

Website: www.ijetae.com (ISSN 2250-2459, ISO 9001:2008 Certified Journal, Volume 8, Issue 2, February 2018)

12

3. The research performed points the need to test thesystem to provide banking services and its implementation through the new marketing strategy for its banking services which is suitable for the restructuring process and merger activities in commercial banks in Libya.

4. There is a need for training of human sources within banks for restructuring process and merger activities and forcing use of modern training for their employees at all levels of administrative terms objectives, It also pointed quality of programs for trainers and trainees in order to raise the level of performances and skills. It is related to the expenses of the training which s are necessary and useful investment, so they have to be allocated in annual budget of the banks;

5. The need to adapt and develop the activities and elements of banking marketing different in accordance with the development of banking services and the restructuring process and merger activities, and the need to note the importance of marketing is personal increasingly important with the increase in dealing with electronic devices to provide banking services to customers directly without the presence of staff members of the bank;

6. The trend towards specialization in service and building an integrated banking system in the Libya from commercial banks and banks that the current community needs to make in the future;

7. The necessity of commitment to strategic planning of restructuring process and merger activities in the Libyan banks through the attention of senior management of the future direction of the Bank and its commitment to and support for the planning of restructuring process and merger activities and work to develop a good database and the establishment of effective control systems, including systems of incentives for staff.

8. Need to work to attract new and retain existing customers, as this is essential for the survival of the bank and its continuation;

9. The need for a strategy to develop new modern restructured and mergered banking services in the Libyan commercial banks;

XVI. SOME PROPOSED FOR FUTURE RESEARCHES

After closely examining the results of this study, the researcher can make the following recommendations for the further development of Libyan banking sector and its higher business efficiency:

1. It should be noted that the development of banking services have in the quality of services and how they are providing these services, so as to satisfy the maximum amount of unmet needs for customers to accomplish their work and achieve their goals;

2. The need for the use of various training centers, institutes and universities in the restructuring process and merger activities and development of banks, and the diffusion of banking culture in the educational and training programs in various stages;

3. Simplification of procedures and administrative restrictions in the field of to perform banking services, and to give greater freedom of action responsible for the management of banks to strengthen staff flexibility and adaptability;

4. The need to create an atmosphere of banking competition, because competition helps the emergence of aspects of the banking efficiency; ;

5. Need to take advantage of developments in banking services on a global level;

6. The need to avoid changes and shortcomings that relate to slowly complete banking operations through the monitoring process, processing and attention by senior management of the bank, so that it is making adjustments to some of the steps stages, familiar and accepted so that it is canceled and replaced;

7. Need to focus on the process of educating customers on the use of various electronic devices related to the provision of banking services, using various means possible, such as manuals that contain instructions on the use, advertising and other;

8. Exchange of expertise between the staff in Libyan banks and Arab and Islamic world through mutual visits, seminars and scientific conferences to exchange periodic and expansion of banking culture in order to explain the role of the restructuring process and merger activities ;

International Journal of Emerging Technology and Advanced Engineering

Website: www.ijetae.com (ISSN 2250-2459, ISO 9001:2008 Certified Journal, Volume 8, Issue 2, February 2018)

13

10. Libyan commercial banks would play an effective rolein restructuring process and merger activities and giving advice and financial and economic advice to their clients and work on the promotion of these essential services and development with the provision of internal organizations, including banks;

11. Need to work with marketing plans determine the detailed operational work programs for the various elements of the restructuring process and merger activities

12. Review of some of the banking legislation in order to fit with the requirements of the restructuring process and merger activities and the next stage of that and in line with the ownership and development of banking services and study the experiences of progress in modern technology.

XVII. CONCLUSION

The banking system for the national economy is like the heart of the living, and influence is as the blood for human body. It reflects the seriousness and importance of the banking system for the national economy. The creation of money like renew of blood is the function of the banking system as it plays a critical role within the national economy, as that the movement of economic activity is achieved through the banking system.

The importance of this research lies in the following points:

Banks represent a key and effective element in the Libyan economy. Therefore, as financial institutions, their effectiveness would necessarily lead to success and evolution of these banks, which will eventually lead to the country's development, growth and prosperity. Here lies the importance of the research to achieve economic progress through integration or merger, which would lead to achieving the desired goals, and achieving a highly efficient and effective banking sector. The research is also of great importance to bank managers and staff, in increasing their knowledge of the importance of using technology and its effectiveness, liberalising the economy, and enhancing competitiveness, and in the case of mergers and integration of banks helping in carrying out the tasks entrusted to them, efficiently and effectively.

The importance of the research also lies in the restructuring of banks, and developing and implementing a programme of integration and mergers, with improved performance to guide them to achieve profitability and success in a more liberal and competitive labour market economy, while eliminating the factors affecting the integration and merger of Libyan commercial banks.

Indeed, this acts as an indicator of success, and adds to buyers’, investors’, and other parties’ confidence, creates an attractive investment environment for international banks to bring their experience, skills and technologies, in cases of merger and integration, to provide services more efficiently and effectively.

The research also confirmed main objectives of the study:

1.Achieve bank restructure that allow strong and competitive banks to form, able to compete and survive in light of global competition.

2.The restructuring of banks achieves financial and economic savings represented in increased growth rates, greater productivity, increased profits and expanded deposits base, which achieve international competitiveness through renewable technologies and qualified human resources; this was to be achieved in each bank individually.

3.Expanding the opening of new markets for revenue and creating the conditions for diversifying banking services, which would lead to strengthening the position of the bank in the banking market.

REFERENCES

[1] Abdel-Badie Sakr, Mokhtar Hassan: Marketing skills and the promotion of banking services. (Beirut, Lebanon, first i 2007). [2] Abdul Aziz Abu Sabah - studies in the marketing of specialized

services, a practical approach (Amman, Jordan, Werra Foundation for Publishing and Distribution, 2006

[3] Abdul Rah Man Tawfiq, A program of management skills, developing the performance of strategic business units, status of the professional expertise of the Department, Third Edition, 2002.2003. [4] Abdulmoneem Ahmed Naka, Banks and money, Alexandria for

book, 2008.

[5] Adel Saharawi: the scientific evidence for the application of Total Quality Management (Cairo, Arab Media Company, 2000(. [6] Ahmed Badr: Origins of scientific research and curricula (and

agency publications, second edition, (2006).

[7] Ahmed Mahmoud Ahmed, Bank services marketing ( Theorical introduction - practical) Dar Albaraka for pub and distribution, 1st edition, 2001.

[8] Ali Abdel Salam Al-Amari, Ali Hussein Ajili (2000), Statistics and Probability Theory and Practice, (Valletta: Publications ELGA) . [9] Ali Abdel Salam Al-Amati, Ali Hussein Agile (2000), Statistics and

probability theory and application, (Valletta: Publications ELGA). [10] Ali Abdel Salam Al-Amati, Ali Hussein Agile (2000), Statistics and

probability theory and application, (Valletta: Publications ELGA), [11] Allhalh Ahmed Abdullah, Mustafa Mahmoud Abu Bakr (2002),

Scientific research steps defined its methods of statistical concepts, (Alexandria: University House).

[12] Appreciation of the sixth annual Forty of Central Bank of Libya, 2002 .

International Journal of Emerging Technology and Advanced Engineering

Website: www.ijetae.com (ISSN 2250-2459, ISO 9001:2008 Certified Journal, Volume 8, Issue 2, February 2018)

14

[14] Basher Altoergi, Bank management, op.cit.[15] Bashir Altmeur, Bank management and development (World Library Tripoli Libya P-1999).

[16] Bashir Mohamed Ashour Dervish, Mehdi Taher rich, Bahlul Falba Omar (2005), Scientific research in the science of administrative and financial principles and concepts and methods, (Tripoli: National Bureau for Research and Development) .

[17] Bashir Mohamed Darkish Ashour, Midi Taher rich, Omar al-Bahlul Falbi (2005), scientific research in the science of administrative and financial foundations concepts and approaches, (Tripoli: National Bureau for Research and Development)

[18] Central Bank of Libya, Department of Research and Statistics, (fiftieth anniversary of the establishment) 2006 .

[19] Beatty. R. Santomero. A. and Smirlock. M. Bank Acquisition premiums. Analysis and Evidence. Salomon Brothers Center for the Study of Financial Institutions. Monograph Series in Finance and Economics. Monogreph 1987 - 3.

[20] Benston, George J. Hunter, Willian C, and Wall, Larry D. Motivations for Bank Mergers and Acquisitions: Enhancing the Deposit Insurance Option Versus Earning Diversification. Journal of Money. Credit, and Banking, (27) August 1995, pp 777 - 778. [21] Berfer, Allen N and Humphrey, David B, Megamergers in Banking

and the Use of Cost Efficiency as an Antitrust Defense, The Antitrust Bulltion, 37 (Fall 1992), pp 541-600.

[22] Bank, Scale Economies, Mergers, Concentration, and Efficiency: The U, S. Experience, Financial Institution Center. the WHARTON School, University of Pennsylvania, July 1994

[23] Bonime, Seth D. Goldberg, Lawrence G, and White, Lawrence J, The Dynamics of Market Entry: The Effects of Mergers and Acquisitions on De Nevo Entry and Small Business Lending in the Barking Tndustry, The Federal Reserve Board, 20 and C sts, NW. Washington, DC, 20551, January 2000.

[24] Boyd, John H, and Stanley L, Grham, Investigation Bank Consolidation Trend, Federal Reserve Bank of Minneapolis Review, (Spring 1991), pp, 3 - 15.

[25] Cornett, Marcia Millon, and De Sankar, Medium of Payment in Carporate Acquisitions Evidence from Tnterstate Bank Mergers, Journal of Money Credit, and Banking vol 23, Issue 4 (November 1991), pp. 767-776.

[26] Central Bank of Libya, Law No. (1 (1373. R. / 2005 on the banks [27] Central Bank of Libya, The fourteenth annual report of the

Governing Council (1969-1970. Saleh Aalamin Alarbah, op.cit, [28] Chalice Haddad Sweden. System, the basics of marketing) Oman:

Al.Hammed Library for publication and distribution, P1, (2006). [29] Customize. Co (2002) atoms: Covers for community banker vol.

11no 10.

[30] Daniel M.. Stole, a full translation of the happiest Elias, Marketing and continuous improvement (Riyadh Library Obeisant first edition 2002),

[31] Demsetz. Rabecca S. and Strahan Philip E. The Consolidation of Financial Services Industry: Cause, Consequences. and Implications for the Future, Journal of Banking and Finance, vol 23, 1999. [32] De Young, Robert, Determinants of Cost Efficiencies in Bank

Merger, Working Paper 93 -1. Office of the Comptroller of Currency, August 1993.

[33] Dodd, Peter, The Market for Corporate Control: A Review of the Evidence, Midland Corporate Finance (Summer 1993), pp, 6 -19. [34] Drucker, Peter. The Five Rules of Successful Acquisition, Wall

Street Journal, October 15, 1981. p. 22.

[35] Dr. Mounir Ibrahim, an Indian management, commercial banks, "Introduction to decision making," Modern Arab Bureau, Alexandria, third edition ,2003.

[36] Dr. Hanawi, Mohammed, d. Abdel-Salam, MS, financial institutions,