Accounting Conservatism

By

(Richard) Zhe Wang

A thesis submitted to the Victoria University of

Wellington in fulfilment of the requirements for

the degree of Doctor of Philosophy in

Accounting

Victoria University of Wellington

Abstract

This thesis provides an in-depth examination of accounting conservatism, which is one of the oldest and most important principles of accounting (Sterling, 1967; Watts, 2003a). Two main questions relating to accounting conservatism are extensively studied in this thesis: (1) How to measure accounting conservatism? (2) Why do firms adopt accounting conservatism?

This thesis consists of three main chapters that answer these two questions from three different perspectives. The first chapter studies the existing empirical mea-sures of accounting conservatism from a construct validity perspective and con-cludes that construct validity of the existing measures is mixed to low.

The second chapter examines the validity and bias in the Basu (1997) measure of accounting conservatism – one of the most widely used measure of conservatism in the accounting literature. The second chapter shows, analytically and empiri-cally, that the Basu (1997) measure is biased upwards by the default risk of a firm, and proposes a new measure of conservatism that is free from this bias. This new measure of conservatism is called the “Default-Adjusted-Basu” measure.

The third chapter investigates the economic rationale for accounting conser-vatism, and proposes a signalling theory for accounting conservatism. In a debt market characterized by information asymmetry, a borrower firm’s degree of con-servatism can serve as a credible signal about that borrower firm’s level of operat-ing risk to the lenders in the debt market. Thus, one potential benefit of accountoperat-ing conservatism is that it can reduce the degree of information asymmetry in the debt market.

Acknowledgment

I am greatly indebted to my supervisors, Professor Tony van Zijl and Professor Ciarán Ó hÓgartaigh, for their invaluable guidance and support. They have played a role in my academic career far beyond that of merely supervising my thesis – they have helped me to become not only a better researcher, but a better person.

Studying at the School of Accounting & Commercial Law (SACL) of Victoria University of Wellington has been an extremely stimulating and rewarding expe-rience for me. SACL has a tradition of critical thinking and thinking “outside the box”, which has a profound influence on the way I conduct my own research. I therefore thank all of the staff and faculty members in SACL, for creating such a stimulating environment of scholarship. I also wish to express my gratitude to SACL for providing me with the SACL PhD scholarship. Special thanks goes to Professor Keitha Dunstan, the former Head of School, who has supported my pro-fessional development in many ways.

I am grateful to my fellow PhD students for their friendship, intellectual dis-cussions, and enjoyable BBQs outings. I am especially fortunate to have shared an office with Rahmadi Murwanto, a fellow PhD student, over the last three years. Many interesting discussions with Rahmadi have uplifted my spirit at the most dif-ficult times of my PhD.

Last, but not least, I would like to thank my parents for their endless support throughout my PhD. Without their love, I simply could not have completed this PhD.

Contents

Abstract 1 Acknowledgement 2 List of Figures 5 List of Tables 7 General Introduction 80.1 Background and motivation . . . 8

0.2 Overview of the chapters . . . 17

0.3 Contributions of the thesis . . . 22

1 Measures of Accounting Conservatism: A Construct Validity Perspec-tive 25 1.1 Introduction . . . 25

1.2 Existing measures of conservatism . . . 29

1.3 Construct validity & the existing measures of conservatism . . . 54

1.4 Discussion . . . 68

1.5 Conclusions . . . 77

2 The Impact of Default Risk on the Basu Measure of Accounting

Con-servatism 80

2.1 Introduction . . . 80

2.2 The link between the Basu asymmetric timeliness coefficient and default-risk . . . 84

2.3 A new measure of conservatism . . . 93

2.4 Proxies and data . . . 95

2.5 Main empirical results . . . 102

2.6 Robustness tests . . . 110

2.7 Conclusions . . . 118

2.8 Appendix . . . 120

3 The Signalling Role of Accounting Conservatism in the Debt Market with Asymmetric Information 126 3.1 Introduction and background literature . . . 126

3.2 Four basic properties of conservatism . . . 133

3.3 Model set-up . . . 148

3.4 Signalling equilibria . . . 154

3.5 Implications . . . 163

3.6 Conclusions . . . 166

3.7 Appendix A – proofs . . . 168

3.8 Appendix B – an empirical test of the signalling theory . . . 173

Conclusions and Implications for Future Research 180

List of Figures

2.1 Box-plot of distance-to-default (DD) – “normal firm-years” vs.

“out-liers” . . . 115

3.1 Basu earnings function (with discontinuity) . . . 136

3.2 Basu earnings function (without discontinuity) . . . 137

3.3 Earnings as a function of conservatism . . . 142

3.4 Debt value as a function of conservatism (Single-crossing property) 147 3.5 Equity value as a function of conservatism (Single-crossing property) 147 3.6 Timeline of the conservatism-signalling game . . . 149

List of Tables

1.1 A summary of the empirical literature on conservatism . . . 30

1.2 Statistics on the measures of conservatism in the paper survey . . . 40

1.3 Validation Criteria (sub-validities) . . . 55

1.4 Evidence of convergent validity . . . 60

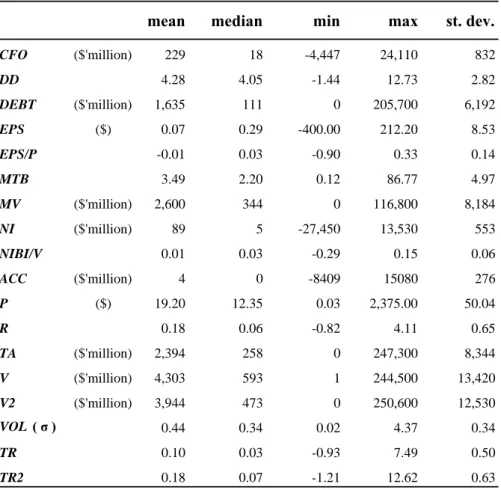

1.5 Descriptive statistics . . . 79

2.1 Descriptive statistics . . . 99

2.2 Correlation Table . . . 100

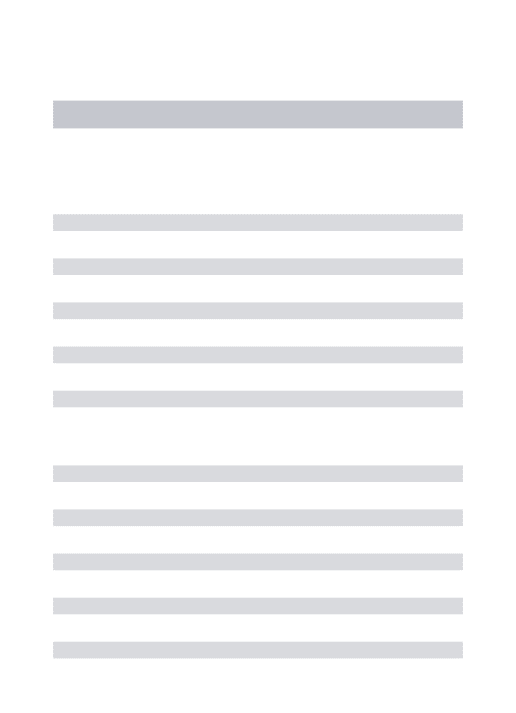

2.3 The association between the Basu measure of conservatism and distance-to-default (DD) . . . 104

2.4 The association between the Default-Adjusted-Basu (DAB) mea-sure and distance-to-default (DD) . . . 105

2.5 A simpler (and naive) version of the Default-Adjusted-Basu (DAB) measure . . . 109

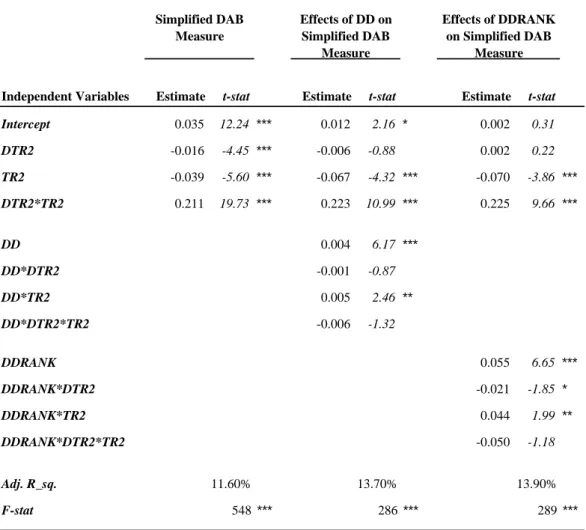

2.6 Robustness Test – Ball & Shivakumar’s (2005) AACF measure of conservatism and Distance-to-Default (DD) . . . 113

2.7 Robustness test - An alternative specification of Net Income Before Interest (“NIBI2”) in the DAB measure . . . 117

3.2 Basu AT & AACF regressions augmented by Asset Volatility (VOL) 178 3.3 Default-Adjusted-Basu measure and Asset Volatility (VOL) . . . 179

General Introduction

The accountant transcends the conservatism of the proverb, ‘Do not count your chicken before they are hatched,’ saying, ’Here are a lot of chickens already safely hatched, but for the love of Mike, use discretion and don’t count them all, for perhaps some will die.’

— Henry R. Hatfield (1927, p. 256)

0.1

Background and motivation

The subject of this thesis is accounting conservatism, which is one of the oldest and most important principles of accounting (Sterling, 1967; Watts, 2003a). Broadly speaking, conservatism is a tendency that accountants, when encountering uncer-tainties in economic transactions, choose to report lower estimates for the values of assets and revenues, but higher estimates for the values of liabilities and expenses. Conservatism in accounting ensures that costs are not understated in the accounts and revenues are not overstated. Conservatism appears to be closely related to the concept of realisation, as conservatism implies that a profit should not be recognized before it is realized. Sterling (1967) suggests that conservatism may in fact be the root of the realisation principle.

is a principle under which accountants exercise a reasonable degree of prudence in recognizing transactions subject to genuine economic uncertainties. The modern view of accounting conservatism does not seem to include, or permit, any deliberate manipulations of the accounts by understating income in one period and overstating income in a latter period, if there is no or little economic uncertainty surrounding the transactions. The latter behaviour is often called“big bath” accounting, which creates hidden reserves, and is inconsistent with the principle of accounting conser-vatism. The view of accounting standard setters towards conservatism and hidden reserves is clearly evident in FASB’s conceptual framework:

Conservatism in financial reporting should no longer connote deliber-ate, consistent understatement of net assets and profits. (FASB, 1980, para. 93)

Then in paragraph 95, the FASB conceptual framework indicates that: Conservatism no longer requires deferring recognition of income be-yond the time that adequate evidence of its existence becomes avail-able or justifies recognizing losses before there is adequate evidence that they have been incurred. (FASB, 1980, para. 95)

Therefore, while conservatism and the creation of hidden reserves are superficially similar, there is however a clear line that separates these two types of behaviours. Conservatism is a genuine, prudent response to uncertainty, whereas big bath ac-counting is a deliberate attempt to mislead the users of financial statements when there is in fact no uncertainty. As W. A. Paton so clearly pointed out,“sheer under-statement where it is possible to ascertain the actual facts is not conservatism but concealment.” (Paton and Stevenson, 1916, p. 237)

Modern accounting researchers recognise that conservatism has the effect of accelerating the recognition of economic losses and deferring the recognition of economic gains (e.g. Basu, 1997; Watts, 2003a). Therefore, economic losses are reflected in earnings faster than economic gains, under conservatism. This prop-erty of conservatism is described by Basu (1997) as the asymmetric timeliness of earnings, which has become the anchor for a number of empirical and theoretical works on accounting conservatism in recent years (see Watts, 2003b; Ryan, 2006, for literature reviews).

The asymmetric timeliness of earnings property of accounting conservatism, as described above, highlights the intertemporal nature of accounting conservatism: the recognition of unverifiable or unrealised economic gains in earnings are delayed until they subsequently become verifiable or realised in later periods. Thus, in a typ-ical life cycle of a firm, earnings tend to lag economic income by several accounting periods. In the early stages of the life of the firm where investment outlays tend to be high and revenues low, earnings tend to be lower than the economic income of the firm; but in the mature stage of the firm, where revenues are larger and more stable, earnings tend to catch up with the economic income or even exceed it (Monahan, 2005; Zhang, 2005). However, one should not argue that accounting conservatism is not always “conservative” simply because it may lead to lower earnings in one period and higher earnings in another. To make that argument would be to entirely miss the main purpose of accounting conservatism, which is to create a higher stan-dard of verification for recognition of good news, as a mechanism for coping with economic uncertainties. Thus, the intertemporal properties of earnings are merely a consequence of that main purpose of accounting conservatism, rather than the cause of it.

rule of inventory valuation. This well-known rule states that inventory values should not be written up when the market value of inventory exceeds its cost, but should immediately be written down when the market value falls below the cost. According to a renowned accounting historian, R. H. Parker (1969), the lower of cost and market rule was firmly established somewhere in the 19th century. George O. May reportedly said that by the time he entered the accounting profession in England in 1892, the rule had already been well established (Parker, 1969). This suggests that conservatism probably has been around since the 19th century at the latest, while some researchers argue that the time is even longer.1

Sivakumar and Waymire (2003) conducted a historical study into the account-ing of U.S. railroads at the beginnaccount-ing of the 20th century, usaccount-ing modern empirical methods. Their study shows that railroad companies in the US around the turn of the 20th century were not only conservative in their accounting methods and policies, but also gradually increased their levels of accounting conservatism, in response to changing regulations and other factors. This study provides some of the most convincing empirical evidence that accounting conservatism has existed for a long period of time, resonating the similar conclusion reached by accounting historians based on other (mostly non-empirical) methods.

Conservatism’s influence on modern accounting standards is pervasive, and ex-amples of accounting conservatism can be found in many modern accounting stan-dards. Apart from the lower of cost and market rule, which still remains in the US and international accounting standards today, many other rules and standards ex-ist that are examples of accounting conservatism. They include the impairment of fixed-assets, the expensing of the majority of the research and development costs,

1Basu (1997) argues that accounting conservatism has been established for at least 500 years in

Europe. Basu’s claim is supported by the historical evidence that traces the lower of cost and market rule back to Italy in the 15th century, and to France in the 17th century (Littleton, 1941).

provisions, and contingent assets and liabilities, among many others. All these rules or standards demonstrate the basic characteristic of conservatism, which is that ac-countants must exercise a degree of prudence in recognizing uncertain economic gains.

Empirical studies into accounting conservatism in the second half of the 20th century have provided ample evidence that accounting conservatism is a fundamen-tal characteristic of financial reporting in virtually all the developed countries in the world, and also in many developing countries (See Watts, 2003b; Ball et al., 2000; Bushman and Piotroski, 2006; Basu, 1997; Ball et al., 2003). This is an active area of research and more studies in this area are currently being undertaken.

The phenomenon of accounting conservatism has intrigued many accounting researchers since the very early stages of the development of accounting theory. However, there have been an eclectic and divided range of opinion about account-ing conservatism, and much of the argument has still to be resolved even today. Beginning in the late 1930s, and until the 1980s, conservatism had been criticised by a number of prominent accounting scholars, including Gilman, Hatfield, May and Paton (Chatfield, 1996). According to Chatfield (1996), some of the most fre-quently used arguments against conservatism are: (1) accounting conservatism is not consistent in that it produces lower income in one period and leads to higher income in another period; (2) accounting conservatism is arbitrary and gives man-agers too much discretionary power over reporting, among other problems.

However, as Watts (2003a; 2003b) has noted, despite the criticisms of conser-vatism, not only has accounting conservatism survived numerous accounting re-forms, regulations and economic crises in the past century, but also the average degree of accounting conservatism, in the US at least, has even increased slightly during the past 30 years or so. And this claim has been substantiated by many

em-pirical studies based on large samples of data from the US and worldwide. It seems that conservatism is extremely resilient in the modern economy.

For example, in regard to the lower of cost and market rule, Parker observes: “The astonishing thing about the lower of cost and market rule is its ability to survive attack. G. O. May was probably right in suggesting that most accountants are‘content to regard the demonstrated practical wisdom of the rule as outweighing any supposed illogicality’.” (Parker, 1969, p. 257)

But why do accountants want to conform with the “practical wisdom” of conser-vatism despite its criticisms? After all, is there any logic, if any, hidden behind the seeming illogicality of conservatism? In fact, finding that logic to support conser-vatism has become the main occupation of many positive accounting researchers over the last decade.

The main interest of contemporary accounting researchers in conservatism is to find the rationale, if any, behind conservatism, and thus to explain why conservatism is so resilient in the modern economy. While the search for rational explanations of conservatism is still ongoing, it has already paid big dividends. A large part of the recent advancements in the conservatism literature can be summarised in the fol-lowing five rational explanations of accounting conservatism:(1) the litigation risk explanation, (2) the debt-contracting explanation, (3) the managerial-contracting explanation, (4) the political cost explanation, and (5) the tax-incentive explana-tion(See Watts, 2003a, for a review of these explantions). These explanations have made conservatism, once unjustifiable in the eyes of Paton and Hatfield, signifi-cantly more justifiable.

be fueled by an additional factor – the movement against conservatism by account-ing standard setters, especially the FASB and the IASB. These accountaccount-ing standard setting bodies have been attempting to abandon the conservatism principle in favour of the “neutrality principle” (IASB, 2006; FASB, 2006). It is claimed that if the neu-trality principle is followed, there should be no downward bias in the reported net profit, even though there is some uncertainty as to the amount and the realisation of the profit. The chief justification for this view is that the conservatism principle ap-pears inconsistent with the qualitative characteristic ofrepresentational faithfulness

due to the bias it introduces. In contrast, neutrality is argued to lead to unbiased representations of the underlying economic performance and condition of the firm, thereby providing morereliable and relevantinformation to users of financial state-ments.

For example, in the discussion paper issued by the IASB in 2006 in a joint project with the FASB to review and revise the conceptual framework of accounting, the boards comment that:

However, the boards concluded that describing prudence or conser-vatism as a desirable quality or response to uncertainty would conflict with the quality of neutrality. Even with the proscriptions of delib-erate misstatement that appear in the existing frameworks, an admo-nition to be prudent is likely to lead to a bias in reported financial position and financial performance. Moreover, understating assets (or overstating liabilities) in one period frequently leads to overstating fi-nancial performance in later periods—a result that cannot be described as prudent. Neither result is consistent with the desirable quality of neutrality, which encompasses freedom from bias. Accordingly, the proposed framework does not include prudence or conservatism as

de-sirable qualities of financial reporting information. (IASB, 2006, para. BC2.22)

However, the above view taken by accounting standard setters is not shared by all accounting academics and practitioners. Many, including Watts (2003a; 2003b; 2006), disagree with the standard setter’s movement away from conservatism in the accounting conceptual frameworks and accounting standards. The dissenters argue that accounting conservatism is not as illogical as it may initially appear; conservatism is, in fact, driven by some fundamental economic forces, and is an

efficientreporting mechanism in response to the economic, legal and political envi-ronment in which firms operate. The dissenting opinion is primarily based on the five rational explanations of conservatism mentioned above and the results of recent empirical studies on accounting conservatism. Therefore, the proponents of conser-vatism argue that if conserconser-vatism is compulsorily replaced by neutrality, firms will likely adopt sub-optimal accounting techniques that will damage their economic efficiency, in particular theircontracting efficiency.

A controversy therefore arises between the supporters and the opponents of ac-counting conservatism, which may have in part stimulated the academic research into accounting conservatism in the past decade or so.2 It is hoped that the research

into conservatism will provide academics, standard setters, and policy makers with a deeper and richer understanding of the likely impacts of the policy of replacing the conservatism principle with the neutrality principle in the conceptual framework and in accounting standards.

Against this backdrop, this PhD thesis is the author’s own research efforts to at-tempt to understand the important and interesting phenomenon of accounting

con-2A good starting point for seeing the arguments in this debate is a pair of articles published by

each side of the debate in Journal of Accounting Economics (2001): Holthausen and Watts (2001) and Barth et al. (2001). And more recently, the view of the proponents of accounting conservatism

servatism. The main thrust of this thesis is to contribute to answering the following two questions:

Research Question (1): How can we empirically measure the degree of ac-counting conservatism?

Arguably, the first step towards understanding the causes and effects of the phe-nomenon of accounting conservatism is to be able to accurately observe and mea-sure it in empirical studies. That is not just true of accounting research, but true of science in general. The history of science is in some respect a history of obser-vations and measurements, careful and ingenious ones, of course. If Galileo had not constructed a superior and sharper telescope in the early 17th century, it would have taken astronomers much longer to realize that the earth goes around the sun, instead of the other way around. If Rutherford had not meticulously taken his ob-servations about the trajectories of alpha particles being shot through a very thin paper of gold, physicists would probably have taken years longer, if ever, to dis-cover the internal structure of atoms. For researchers of accounting conservatism and for any financial analysts interested in understanding the causes and effects of accounting conservatism, it is just as essential to first observe and measure the de-gree of accounting conservatism in financial reporting as it was for Galileo to first make better telescopes before peeking into the sky. Chapter 1 & Chapter 2 of this thesis are devoted to the task of measuring accounting conservatism.

Research Question (2): Why does conservatism exist in accounting, and why is the degree of conservatism higher in some firms than others?

After all, conservatism in financial reporting decreases the earnings and net book values of a firm, and in doing so, it could be claimed that conservatism distorts the information content of the firm’s financial reports. But why, under economic

uncertainty, does the accountant tend to report a lower and more conservative figure as the net profit out of all possible net profits? Is not the mean value, or even the median, of all possible net profits the best number to summarise the distribution of all possible net profits? If we look at the classical example of conservatism – the lower of cost and the market rule, why did the early accounting pioneers choose to report the the lower of cost and market value? Why not the higher of cost and market value, or perhaps theaverageof these two? So is there any rational explanations behind the tendency to report a low and more conservative net profit? As already noted, researchers have proposed several theories to explain accounting conservatism (see the literature review by Watts, 2003a). But these explanations are still far from being conclusive, and ongoing research is being conducted. Chapter 3 of this thesis contributes to this fledgling literature by proposing a new economic explanation for why accounting conservatism exists and why empiricists find that some firms are more conservative than others.

I now provide a brief overview of each of the three main chapters of the thesis (Chapters 1 to 3) as follows.

0.2

Overview of the chapters

Chapter 1: Measures of accounting conservatism: a construct

va-lidity perspective

3Chapter 1 provides a survey of the literature on accounting conservatism, with a focus on assessing the construct validity of existing measures of conservatism. Ac-counting conservatism has been the subject of intensive empirical research in the

past decade. It is essential for empiricists to develop a valid, accurate and reliable measure of accounting conservatism. To date, five key measures of conservatism have emerged in the literature: (1) Basu’s(1997) asymmetric timeliness of earnings measure (“AT”), (2) Ball and Shivakumar’s (2005) asymmetric-accruals-to-cash-flow measure (“AACF”), (3) the commonly suggested Market-to-Book ratio mea-sure (“MTB”), (4) Penman and Zhang’s (2002) Hidden Reserves Meamea-sure (“HR”), and (5) Givoly and Hayn’s (2000) Negative Accruals Measure (“NA”). However, few studies have examined, directly or tangentially, whether the applications of these measures produce facts or artefacts. Chapter 1 examines this issue from the perspective of construct validity and focuses on the the following aspects:

1. The main features of each of the five measures of accounting conservatism; 2. The construct validity of the five measures of conservatism;

3. Inconsistencies between the results of different measures of conservatism; 4. Biases in these measures of conservatism.

Chapter 1 first describes each of the five measures. Then, it considers these mea-sures against four of the sub-validities of construct validity, within the constraints imposed by the limited and mixed relevant evidence, and guided by construct valid-ity theory. While the available evidence is insufficient to reach a definite conclusion on the construct validity of the existing five measures of conservatism, the analysis of this chapter nevertheless suggests that the construct validity of these measures isweak. Chapter 1 then explores the challenges of measuring conservatism facing accounting researchers, and concludes with suggestions for future research.

Chapter 2: The impact of default risk on the Basu measure of

accounting conservatism

4Chapter 2 continues the previous chapter’s theme of examining the measures of accounting conservatism. But instead of surveying several measures in general, the chapter investigates the validity of one particular measure of conservatism – the Basu (1997) asymmetric timeliness measure (“AT”) – in great depth. Chapter 2 focuses on the Basu measure, because it is currently the most frequently employed measure of accounting conservatism in the accounting literature and has had the greatest impact on the literature.

Chapter 2 has two closely related objectives: (1) to analytically and empirically examine the impact of default risk on the Basu (1997) measure of conservatism; and (2) to design and test a new measure of accounting conservatism – the Default-Adjusted-Basu Measure, or the“DAB”measure.

In regards to the first objective, Chapter 2 first analytically shows that the Basu asymmetric timeliness coefficient is biased upward by the existence of default risk in a firm, and that the bias tends to increase with the level of default risk. The analytical model is primarily based on Merton’s (1974) classic call-option model of equity. The empirical evidence reported in Chapter 3 is consistent with this analytical proposition.

In regards to the second objective, Chapter 2 argues that the Default-Adjusted-Basu measure is likely to be more robust to the bias caused by default risk than the original Basu measure. The empirical tests reported in Chapter 2 indicates that the DAB measure is indeed free from the default-risk-bias.

The main proxy for default risk used in Chapter 2 is thedistance-to-default,

de-4A paper based on Chapter 2 is currently under second review atJournal of Accounting &

veloped by Merton (1974) and estimated by Vassalou and Xing’s (2004) iterative method. Vassalou and Xing’s (2004) iterative method enables the author to obtain a relatively accurate estimate for the distance-to-default for each firm-year. Further-more, the Vassalou and Xing (2004) method also yields the estimates for several essential inputs to the DAB measure.

Chapter 3: The signalling role of accounting conservatism in the

debt market with asymmetric information

Having examined the measures of conservatism in Chapters 1 and 2, Chapter 3 shifts the focus to the economic theories of conservatism. In particular, Chapter 3 investigates the signalling role of accounting conservatism in a debt market charac-terized by information asymmetry. Chapter 3 constructs a signalling game model in order to analyse firms’ decisions on their optimal degrees of conservatism under information asymmetry in the lending market. The market has asymmetric informa-tion because the borrower firms have private informainforma-tion about their true operating risk levels (proxied by asset volatility) that the lenders do not.

Based on this simple model, I show that the borrower firms’ decision on their optimal levels of accounting conservatism depend on their own operating risk. Un-der mild regularity conditions, the signalling game exhibits a “stable” separating equilibrium, in which the high risk firms adopt a low degree of conservatism and vice versa. By simply observing the degree of conservatism adopted by each bor-rower firm, the lenders in the debt market can correctly figure out the true level of operating risk in each borrower firm. As a result, conservatism becomes a credible signalling device for the borrower firms to reveal their private information about their true risk levels to the lenders in the debt market.

Chapter 3 also derives 4 basic properties of accounting conservative, which are stated as 4 lemmas. These basic properties mainly deal with the joint impacts of accounting conservatism and risk on firms’ earnings, thereby providing a direct link between conservatism, risk and earnings. While most of these basic properties are already well known in the accounting literature, the contribution of my analysis is to show that, using Basu’s (1997) definition of accounting conservatism, they can be rigorously proved with very few additional assumptions.

Appendix B to Chapter 3 offers some preliminary empirical evidence on what I call the signalling theory of accounting conservatism developed in the chapter. The results of the tests of whether firms with a lower degree of asset volatility (i.e., fundamental operating risk) adopt a higher degree of accounting conservatism, and vice versa, are consistent with the signalling theory of conservatism. Low-volatility firms indeed tend to have a higher degree of conservatism, and high-volatility firms indeed tend to have a lower degree of conservatism.

It should be noted that the risk addressed in Chapter 3 is of a very different kind from that addressed in Chapter 2. Chapter 2 deals withdefault risk, which is chiefly concerned with downward movements in the value of the firm, subject to a degree of leverage. In contrast, Chapter 3 deals with theoperating riskof the firm, as defined by asset volatility, which encompasses two-sided movements in the value of the firm, regardless of the degree of leverage. There are two key differences between these two types of risk: (1) default risk is one-sided, while asset volatility is double-sided, and (2) default risk is contingent upon the degree of leverage, while assets volatility is independent of leverage.

0.3

Contributions of the thesis

This thesis contributes to the accounting literature in the following six main areas: First, this thesis is the first in the literature that systematically examines the con-struct validity of existing measures of accounting conservatism. Other researchers, like Watts (2003b) and Ryan (2006), have surveyed the empirical measures of ac-counting conservatism, and (in the case of Ryan, 2006) the Basu measure in partic-ular. This thesis contributes to the literature by examining the construct validity of the existing measures in a systematic way. The result of my examination shows that the existing measures may suffer from low construct validity and further research is much needed in this area.

Second, this thesis contributes to the literature by identifying and testing a new kind of bias in the well-known Basu (1997) measure of accounting conservatism. The Basu measure is currently the most widely applied measure of accounting con-servatism (Ryan, 2006, and Chapter 1), and its validity has recently been questioned by Dietrich et al. (2007) and Givoly et al. (2007). This thesis examines the validity of the Basu measure from the perspective of the default risk of a firm. This thesis finds that an upward bias in the Basu measure of conservatism is induced by the existence of default risk in a firm. The greater the degree of default risk there is, the greater this bias in the Basu measure of conservatism.

Third, this thesis further contributes to the literature by constructing a new mea-sure of accounting conservatism – the Default-Adjusted-Basu (or “DAB”) meamea-sure - which is based on the original Basu (1997) measure but is free from the effects of default risk. Empirical testing of the DAB measure shows that it is very effective at removing the bias caused by default risk in the data. Therefore, the DAB measure is likely a more accurate and less-biased measure of accounting conservatism than

is the original Basu (1997) measure.

The fourth contribution of this thesis is that it proposes a new signalling the-ory of accounting conservatism. The model developed in Chapter 3 is currently the only signalling model of accounting conservatism in debt markets. In contrast, all but one of the existing analytical models that examine accounting conservatism, such as Givoly et al. (2007), Chen et al. (2007), and Kwon et al. (2001), are primar-ily moral hazard games, which focus on the role of accounting conservatism in an agency setting either between equity- and debt-holders, or between equity-holders and managers,ex post(i.e., after the signing of the lending contract or the compen-sation contract). In comparison, the proposed model isex anteand focuses on the behaviour of borrowers and lenders prior to the signing of the lending contract.

The only existing published study that examines accounting conservatism in the information asymmetry (and signalling) framework is Bagnoli and Watts (2005). Bagnoli and Watts (2005) show that a high degree of conservatism sends out a signal to the equity market that the managers of the firm expect good profits in the future, and conversely a low degree of conservatism signals that the managers expect low profits in the future. However, Bagnoli and Watts’ (2005) study focuses on the signalling role of conservatism in the equity market, whereas Chapter 3 of this thesis focuses on signalling role of conservatism in thedebtmarket.

One of the original contributions of the proposed signalling model is that it shows that low-risk borrower firms tend to adopt higher degrees of conservatism, while high-risk borrower firms tend to adopt lower degrees of conservatism. This conclusion somewhat contradicts the prevailing view on the debt-contracting role of conservatism, which typically asserts that high risk firms would adopt a higher degree of conservatism (e.g. Watts, 2003a,b; Lara et al., 2009b). The empirical evidence reported inAppendix B of Chapter 3lends direct support to the signalling

theory by showing that high-risk firms actually adopt a lower degree of accounting conservatism than do low-risk firms.

Fifth, Chapter 3 of the thesis further contributes to the conservatism literature by analytically deriving four basic properties of accounting conservatism. While most of these properties are already well-known in the accounting literature, this thesis is the first study that rigorously and analytically derives these properties as-suming little more than Basu’s (1997) definition of accounting conservatism as the asymmetric timeliness of earnings.

Finally, this thesis is the first study in the accounting literature to apply Vassalou and Xing’s (2004) iterative method of estimating default risk. Vassalou and Xing’s (2004) method is a relatively modern technique of calculating default risk and has shown considerable power in predicting firms’ default probabilities. In accounting research, Bushman and Williams (2009) have recently employed a simpler, but non-iterative, approach to measure the default risk in banks, first used by Ronn and Verma (1986). However, whilst simpler to implement, the non-iterative approach is not as accurate as the iterative approach used by Vassalou and Xing (2004), because the actual market leverage moves too fast for the non-iterative approach to reliably estimate firms’ asset volatility (Crosbie and Bohn, 2003, pp. 16-17). Therefore, the use of the Vassalou and Xing (2004) method in this chapter is an innovation in the accounting literature.

Chapter 1

Measures of Accounting

Conservatism: A Construct Validity

Perspective

1.1

Introduction

1Over the last decade, accounting conservatism has become the subject of an active field of empirical research in accounting. An interesting feature of the conservatism literature is the variety of existing measures of conservatism, and the apparent lack of consistency among these measures. From my review of the accounting conser-vatism literature, I have identified five key measures of accounting conserconser-vatism: (1) Basu’s(1997) asymmetric timeliness of earnings measure (“AT”), (2) Ball and

1A paper based on this chapter co-authored with my thesis supervisors is forthcoming in the

Journal of Accounting Literature(2009). I would like to thank the editor, Bipin Ajinkya, and the anonymous referee ofJournal of Accounting Literaturefor their valuable suggestions and construc-tive criticisms. I would also like to thank Stephen L. Taylor for his comments on an earlier version of this chapter during his tenure as the Don Trow Visiting Fellow at Victoria University of Wellington, as well the conference participants at the European Accounting Association 2008 Annual Meeting in Rotterdam, the Netherlands, for helpful comments.

Shivakumar’s (2005) asymmetric-accruals-to-cash-flow measure (“AACF”), (3) the commonly suggested Market-to-Book ratio measure (“MTB”), (4) Penman and Zhang’s (2002) Hidden Reserves Measure (“HR”), and (5) Givoly and Hayn’s (2000) Neg-ative Accruals Measure (“NA”). While there are several other approaches to mea-surement of conservatism, these five measures are the most widely applied and have had the most significant impact on the empirical literature on conservatism.

To the extent that these measures are used in empirical studies to test theories and hypotheses concerning accounting conservatism, the empirical results obtained may differ with the choice of measure used and therefore leave uncertainty about the validity and significance of the results obtained from any particular measure. Therefore, it is important that accounting researchers consider the validity of these measures of accounting conservatism. In this chapter, I attempt to address the ques-tion of the validity of the measures of accounting conservatism and focus on the following specific questions:

1. What are the main features of each of the five measures of accounting conser-vatism?

2. Could application of different measures of conservatism produce the same result?

3. How should the differences, if any, resulting from the use of different mea-sures of conservatism be interpreted?

4. Are there any biases in these measures of conservatism?

The above four questions set the key issues that are relevant to empirical researchers studying accounting conservatism. I address these questions by conducting a survey of the accounting conservatism literature using the methodological framework of

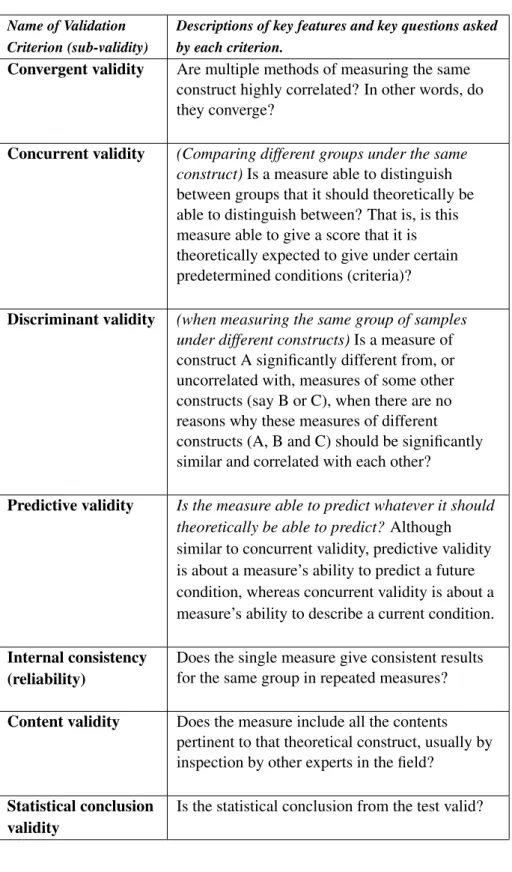

construct validity theory, as set out in Messick (1989), Cook and Campbell (1979) and others. Broadly speaking, construct validity addresses the question “are the measures representing what they are supposed to represent?” Construct validity provides a scientific framework for assessing this overall question and the subsidiary questions set out above. The concept of construct validity has been in existence for more than 50 years and has been applied in many branches of the social sciences, including psychology, education, sociology, organizational behavior and market-ing. In this chapter, I apply this well-established framework to analyze the issues surrounding the validity of the existing measures of accounting conservatism.

While the primary method of investigation in Chapter 1 is one of reviewing and analyzing the existing empirical literature on accounting conservatism, I also conduct some supplementary empirical tests in Section 1.3.1, because the existing empirical evidence is incomplete in regard to convergent validity. These simple empirical tests in Section 1.3.1 allow me to get a complete view of convergent va-lidity among all five measures of conservatism. Apart from Section 1.3.1, all other sections of Chapter 1 are based on the empirical evidence provided by the existing literature, and no further empirical tests are conducted.

The precise meaning of the construct of accounting conservatism has not been universally agreed upon by accounting researchers. A general interpretation of “conservatism” in accounting is articulated by the IASB, which states that conser-vatism is“a degree of caution in the exercise of the judgments needed in making the estimates required under conditions of uncertainty, such that assets or incomes are not overstated and liabilities or expenses are not understated” IASB (1989, p. 37). Nevertheless, compared to many other constructs or subject areas of accounting, the construct of conservatism does not have a well-articulated and as yet commonly agreed upon interpretation. Regardless of the meaning of conservatism, it is a

the-oretical construct that belongs to the world of ideas and, as such, can be linked to other constructs by analytical reasoning. On the other hand, the measures of con-servatism are operationalizations of the construct and application of the measures results in facts that simply reflect the relevant operationalizations. A fact observed regarding conservatism from applying any measure has no independent reference in any circumstance. In order for such facts to have significance they should obviously bear close correspondence to the underling theoretical construct.

The framework of construct validity provides a basis for discriminating between the different measures and thus it provides a useful approach to frame a review of the developing literature on conservatism. Although this chapter is mainly based on the existing evidence from the empirical literature, its contribution is to put the existing evidence into a new perspective – the perspective of construct validity.

The present survey reviews papers which adopt measures of conservatism that have been widely applied (and therefore constitutes a significant strand of the con-servatism literature) and have been published in peer-reviewed journals through to May 2009. Application of these criteria leads us to review the five measures of conservatism identified above, and my literature survey covers 53 journal articles as summarized in Table 1.1.2

The rest of this chapter is organized as follows: Section 1.2 reviews the tech-niques, strengths, weaknesses and the research applications of the five identified

2Papers that are not covered by the survey include Khan and Watts (2009) and Cotter and

Don-nelly (2006). Khan and Watts (2009) propose a measure of conservatism that is an extension of the Basu AT measure and assesses the firm-specific degrees of asymmetric timeliness. However, Khan and Watts’ paper was published after May 2009, my cut-off date for the literature review, and the measure proposed has to date not been widely adopted. Cotter and Donnelly (2006) propose a firm-specific measure of conservatism that is based on the accounting-policy choices made by each firm. The measure requires researchers to form subjective judgments about the degree of conservatism of a firm based on reading the firm’s statement of accounting policies in the annual report. The measure is inevitably subjective and would not be feasible for application to a large set of firms. The paper was published by a professional body and to date the proposed approach does not appear to have been adopted by other researchers.

measures of accounting conservatism. Section 1.3 critically evaluates the construct validity of these measures against a number of key validation criteria. Section 1.4 discusses the main challenges to construct validity in the measures of conservatism, and offers some suggestions for future research. Section 1.5 concludes the chapter.

1.2

Existing measures of conservatism

In this section, I review the techniques, rationales, and the strengths and weaknesses of the five existing measures of accounting conservatism. The measures are:

1. Basu’s (1997) asymmetric timeliness of earnings measure (AT),

2. Ball and Shivakumar’s (2005) asymmetric-cash-flow-to-accruals measure (AACF), 3. The Market-to-Book (or Book-to-Market) ratio,

4. Penman and Zhang’s (2002) hidden reserves measure (HR), and 5. Givoly and Hayn’s (2000) negative accruals measure (NA).

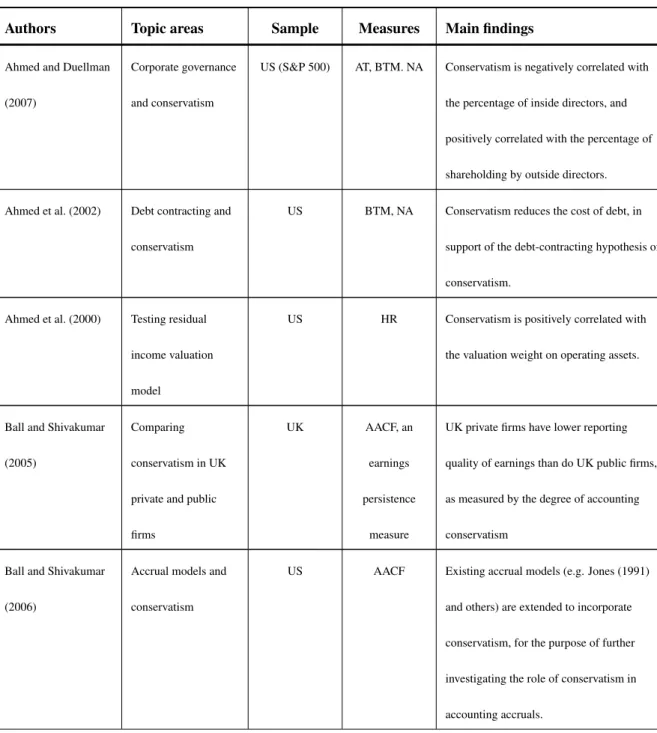

Table 1.1 summarizes the use of these five measures in the empirical literature sur-veyed, including the main topic area and key findings of each paper. Table 1.2 summarizes the frequency of the use of each measure in the papers surveyed. It can be seen from Table 1.2 that the frequency of use differs significantly, and the Basu AT measure is by far the most frequently used measure of conservatism in the literature. Below, we discuss the five measures individually.

Table 1.1: A summary of the empirical literature on conser-vatism

Authors Topic areas Sample Measures Main findings

Ahmed and Duellman (2007)

Corporate governance and conservatism

US (S&P 500) AT, BTM. NA Conservatism is negatively correlated with the percentage of inside directors, and positively correlated with the percentage of shareholding by outside directors. Ahmed et al. (2002) Debt contracting and

conservatism

US BTM, NA Conservatism reduces the cost of debt, in support of the debt-contracting hypothesis of conservatism.

Ahmed et al. (2000) Testing residual income valuation model

US HR Conservatism is positively correlated with the valuation weight on operating assets.

Ball and Shivakumar (2005)

Comparing conservatism in UK private and public firms

UK AACF, an earnings persistence

measure

UK private firms have lower reporting quality of earnings than do UK public firms, as measured by the degree of accounting conservatism

Ball and Shivakumar (2006)

Accrual models and conservatism

US AACF Existing accrual models (e.g. Jones (1991) and others) are extended to incorporate conservatism, for the purpose of further investigating the role of conservatism in accounting accruals.

Authors Topic areas Sample Measures Main findings

Ball et al. (2000) International differences in corporate governance and legal environment and conservatism

International AT Common law countries are more conservative in their financial reporting practices than code law countries as measured by Basu’s AT measure.

Ball et al. (2008) Equity vs. debt markets demand for conservatism

International AT This paper finds that conservatism increased with the relative importance of the debt market in each country.

Ball et al. (2003) Legal, political, and institutional factors’ impacts on conservatism

4 East Asian countries

AT In four East-Asia countries, conservatism is affected by several legal, political and institutional factors. Basu (1997) Asymmetric timeliness of earnings, litigation costs demand for conservatism US AT, an earnings persistence measure

Defined, measured and tested the asymmetric timeliness of earnings concept of conservatism, and show that conservatism level increases with higher litigation costs

Bauman (1999) Testing residual income valuation model (RIVM)

US HR Fixed assets accounting and R&D accounting are the most significant contributors to conservatism. Weak association between conservatism and RIVM parameters.

Authors Topic areas Sample Measures Main findings

Beatty et al. (2008) Debt-contracting benefits of conservatism

US (debt covenants)

AT, BTM, NA Debt-covenant modifications are associated with the demand for accounting

conservatism. Beaver et al. (2008) The simultaneity of

the Basu AT measure

US AT The Basu AT measure is significantly weakened if jointly estimated with Hayn’s (1995) non-linear ERC model, using a 2SLS method.

Beaver and Ryan (2000)

transitory vs. permanent components of BTM

US BTM Separate BTM into the transitory and permanent components. The permanent component is regarded as a measure of conservatism.

Beekes et al. (2004) Corporate governance of conservatism

UK AT The percentage of outside directors is positively associated with conditional conservatism.

Brown et al. (2006) Value-relevance and conservatism

International AT, AACF, BTM

For countries with higher accrual levels, some evidence shows that conservatism is associated with a higher level of value-relevance, although with conflicting evidence. Accrual density is another conditioning variable.

Bushman and Piotroski (2006)

Legal, political, and institutional factors’ impacts on conservatism

International AT, AACF Country-level variations in conditional conservatism associated with a variety of legal & political factors.

Authors Topic areas Sample Measures Main findings

Callen et al. (2009) Return/earning relationship, economic demands for conservatism

US A VAR based measure

A new measure of conservatism is developed based on the vector-auto-regressive (VAR) decomposition of stock returns, and is used to test the economic demands for conservatism.

Cheng (2005) Return on Equity (ROE), RIVM

US HR Abnormal return on equity (ROE) is decomposed into a conservatism component and an economic rent component. More conservative accounting leads to a higher ROE.

Choi et al. (2006) RIVM US a RIVM-based measure

Using analyst forecast information, this paper proposes and estimates a conservatism-correction method for the empirical tests of RIVM.

Choi (2007) Debt-contracting benefits of conservatism

Korea (mid-cap)

AT Conditional conservatism is increasing in a firm’s bank-dependence.

Dietrich et al. (2007) Econometrics of the Basu model

Monte Carlo simulations

AT Basu’s method is upwards biased and does not measure accounting conservatism. Francis et al. (2004) Costs of equity and

conservatism

US AT A study of the effects of various earnings attributes on the cost of equity (information risk proxy). Conservatism is one of them, but is shown to be not significant.

Authors Topic areas Sample Measures Main findings

Gassen et al. (2006) Earnings management and conservatism

International AT, NA, MTB, skewness of

earnings

Conditional conservatism and income smoothing appear to be distinct concepts, and are only weakly correlated. Giner and Rees (2001) International

differences

France, Germany &

UK

AT Earnings of UK firms are more conservative than the earnings of firms in France and Germany, as explained by the litigation cost hypothesis.

Givoly and Hayn (2000) historic trend of accounting conservatism US NA, an earning persistence measure

An empirical survey of the historical patterns of US accounting, developing the

non-operating accrual measure of conservatism.

Givoly et al. (2007) Validity tests of the Basu model

US AT An empirical investigation into the validity of the Basu measure, and shows that the Basu AT measure is not reliable. Grambovas et al.

(2006)

Conservatism in EU and US

EU & US AT Applying the AT measure and panel data techniques, financial reporting has become more conservative in both the US and the EU, and the degrees of conservatism in the US and and the EU are not markedly different. Huijgen and Lubberink (2005) UK-US Cross-listing and conservatism UK (cross-listed in US)

AT UK firms cross-listed in the US are significantly more conservative than UK firms that are not cross-listed in the US.

Authors Topic areas Sample Measures Main findings

Klein and Marquardt (2006)

Accounting losses US NA Negative non-operating accruals are associated with higher frequency of accounting losses. But accounting losses are determined by other non-accounting factors as well.

Krishnan (2005b) Auditor quality and conservatism

US AT, an earnings persistence

measure

Ex Arthur Andersen’s Houston clients showed less conservative earnings than other firms.

Krishnan (2005a) Auditor quality and conservatism

US AT The big 6 auditor’s industry experience is positively correlated with conservative reporting by their clients.

Krishnan (2007) Auditor quality and conservatism

US AT, AACF Ex Arthur Andersen’s clients switched to more conservative accounting practices compared to the control group, in order to reduce litigation risk following the Arthur Andersen’s collapse

LaFond and

Roychowdhury (2008)

Managerial-agency-problem’s demand for conservatism

US AT Conditional conservatism is negatively associated with managerial ownership in a firm.

LaFond and Watts (2008)

Information asymmetry and conservatism

US AT Conditional conservatism is increasing in information asymmetry, which is measured by the probability of an information-based trade (PIN score).

Authors Topic areas Sample Measures Main findings

Lara and Mora (2004) International accounting differences

8 European countries

AT, MTB Continental countries show higher balance sheet conservatism than the UK, however no significant difference in earnings

conservatism. Also found negative correlation between the Basu AT measure and the MTB measure of conservatism. Lara et al. (2009a) Corporate governance

and conservatism

US (S&P 1500) AT, AACF, NA Corporate governance quality is positively associated with the Basu measure of conservatism.

Lara et al. (2009b) Various determinants of conservatism (contracting, litigation, tax and political)

US AT, BTM In general, this study confirms the known factors that determine the degree of accounting conservatism.

Lara et al. (2005) Earnings management and conservatism

France, Germany &

UK

AT The Basu measure of conservatism is more significantly different between code law and common law countries, after discretionary accruals are controlled for.

Lobo and Zhou (2006) Sarbanes-Oxley Act and conservatism

US AT The level of conservatism increased after the introduction of SOX in the US.

Mason (2004) Testing residual income valuation model

US HR, MTB Conservatism is positively correlated with the valuation weight on operating accruals.

Authors Topic areas Sample Measures Main findings

Mensah et al. (2004) Analyst forecast US HR, NA Conservatism is negatively correlated with analyst forecast accuracy. The higher the conservatism, the lower the accuracy. It is an overt sign of market inefficiency.

Monahan (2005) RIVM, Earning/return relation

US HR Conservatism affects the earning/return relation only for firms with high growth in R&D, and impacts on the accuracy of RIVM estimates. Narayanamoorthy (2006) Post-Earnings-Announcement Drift (PEAD) US Asymmetric autocorrelation of standardized unexpected earnings (SUE)

The stock market systematically overlooked the predictable implications of conservatism for the time-series of earnings, leading to cross-sectional variations in PEAD.

Pae (2007) Conditional conservatism and unexpected accruals

US AT, AACF, MTB, HR

Conditional conservatism is found to be mainly achieved by managers manipulating unexpected accruals.

Pae et al. (2005) The negative correlation between the Basu measure and MTB

US AT, MTB This paper shows that Basu’s AT measure and the MTB measure are negatively correlated, and proposes the conditional vs. unconditional conservatism distinction. Penman and Zhang

(2002)

Equity valuation, market efficiency

US HR Conservatism results in lower earnings quality and the market is not efficient enough to see through the effects of conservatism on earnings.

Authors Topic areas Sample Measures Main findings

Pope and Walker (1999)

extraordinary items and conservatism

US vs. UK AT Compared to the US as a benchmark, UK’s FRS 3 tightens the reporting for

extraordinary items, reflected by a higher degree of conservatism in UK firms after the introduction of FRS-3.

Qiang (2007) Various determinants of conservatism (contracting, litigation, tax and political)

US Modified BTM and NA

In general, this study confirms the known factors that determine the degree of accounting conservatism, as well as the negative correlation between Basu measure and MTB.

Rajan et al. (2007) Return on Investment (ROI), RIVM

US HR Conservative and past growth jointly impact on firms’ return on investment (ROI). Roychowdhury and

Watts (2007)

Reconciling the Basu measure and MTB

US AT, MTB Basu measure and the MTB measure are reconciled, based on a valuation model. Ruddock et al. (2006) Non-audit-services

and conservatism

Australia AT High Non-Audit-Services are not related to conservatism, offering evidence that NAS does not impair audit quality/independence. Sivakumar and

Waymire (2003)

History of US railroad accounting

US (history) AT Early 20th-century U.S. railroads demonstrated increased conservatism following new fixed asset accounting rules issued by the Interstate Commerce Commission (ICC) in 1907 and 1908.

Authors Topic areas Sample Measures Main findings Zhang (2008) Debt-contracting benefits of conservatism US AT, NA, earnings skewness

Conservatism induces efficiency gains to lenders and consequently results in lower cost of borrowing if the market is efficient.

Table 1.2: Statistics on the measures of conservatism in the paper survey

Panel A: Frequency of the measures of conservatism in the paper survey

AT AACF MTB

/BTM NA HR Others

No. of papers 37 7 13 10 9 9

Panel B: Papers by the number of measures of conservatism used

1 measure 2 measures ≥3measures Total

No. of papers 32 13 8 53

1.2.1

Basu’s Asymmetric Timeliness Measure (AT)

Basu’s (1997) operationalization of accounting conservatism focuses on the impli-cation that earnings will reflect ‘bad news’ more quickly than ‘good news’, which is known as the asymmetric timeliness of earnings. Basu (1997) was the first to link asymmetric timeliness with accounting conservatism - the greater the asymmetric timeliness, the greater the degree of accounting conservatism. Empirically, Basu (1997) developed the following cross-sectional regression, also known as the Basu regression, to estimate the degree of conservatism (i.e. asymmetric timeliness):

EPSit

Pit =α0+α1DRit+β0Rit+β1RitDRit+εit

where:

• EPSit : Earnings per share for firm i year t

• Pit: Opening stock market price for firm i year t

• DRit: Dummy variable that is equal to 1 if the stock market return for firm i in year t is negative, and equal to 0 if the stock market return for firm i in year t is non- negative.

In essence, Basu (1997) regresses accounting earnings (EPS/P) on stock returns (R) separately for ‘good-news’ and ‘bad-news’ firm-year observations. A firm-year is deemed as a ‘good-news’ firm-year, if its market return is positive or zero, i.e.

Rit ≥0. Conversely, a firm-year is deemed as a ‘bad-news’ firm-year, if its stock return is negative, i.e. Rit<0. The estimated slope coefficient measures how timely the news embodied in the stock return is recognized in earnings, conditional on the sign of stock returns.

Technically, the Basu regression model uses the dummy variable, DR, to dis-tinguish between ‘good-news’ and ‘bad-news’, and thereby allows the slope co-efficients and the intercepts to differ between these two groups. Under good news (Rit≥0), DR is equal to 0 and the good-news timeliness coefficient isβ0. Under bad news (Rit <0), DR is equal to 1 and the bad-news timeliness coefficient isβ0+β1. Clearly,β1 is the asymmetric timeliness coefficient and is the primary indicator of

accounting conservatism in the Basu model. The greaterβ1is, the higher the degree

of conservatism.

Tables 1.1 and 1.2 show that Basu’s AT measure was used in 37 of the 53 papers reviewed by this chapter, making AT the most frequently used measure of conser-vatism in this survey. This finding supports Ryan’s (2006, p. 514) statement that the Basu AT measure is the most popular measure of conservatism in the literature. Ta-ble 1.1 also demonstrates that the papers using the AT measure cover a wide range of topic areas, including (i) the contracting hypothesis of conservatism, (ii) the lit-igation risk hypothesis of conservatism, (iii) the impact of corporate governance on conservatism, and (iv) the impact of auditor quality on conservatism, as well as

other topic areas.

In particular, I find that all international comparative studies of conservatism have without exception adopted the Basu AT measure. These international studies typically test the impacts of a variety of legal, political and institutional factors on the firm’s degree of accounting conservatism (for example: Bushman and Piotroski, 2006; Ball et al., 2000, 2003). Ball et al. (2008) use an international comparative empirical design to test the significance of the debt market relative to the equity market in influencing the firm’s degree of accounting conservatism and find that firms’ degree of financial reporting conservatism increases with the importance of the debt market in a country, but not with the importance of the equity market.

The literature has identified a number of strengths and weaknesses of the Basu AT measure [see Ryan (2006) for a comprehensive discussion on this topic]. The strengths of the Basu AT measure include: (1) it has been widely applied, and for nearly nine years it was the only measure in the literature to implement the asym-metric timeliness operationalization of conservatism;3 (2) many papers using the

AT measure have produced results that are consistent with their theoretical predic-tions, which increases researchers’ confidence not only in the theory but also in the measure itself (Ryan, 2006); (3) the AT measure is well suited to large-sample cross-sectional analysis, manifested by the use of the AT measure in the very large scale international comparative studies discussed earlier.

On the other hand, critics of the Basu AT measure have identified the following weaknesses: (1) the AT measure shows poor performance in time-series research designs (Givoly et al., 2007); (2) the AT measure does not work well when infor-mation is aggregated over a time-period (Givoly et al., 2007); (3) there are

econo-3The second measure implementing the asymmetric timeliness idea is the AACF measure, which

metric deficiencies in the AT measure, including a sample-variance-ratio bias and a sample-truncation bias4(Dietrich et al., 2007); (4) there is a simultaneity problem

in the relationship between earnings and stock returns (Beaver et al., 2008); (5) the AT measure does not provide a firm-specific measure of conservatism; (6) changes in economic rents should not be included in the stock return variable in the Basu regression (Roychowdhury and Watts, 2007); and (7) market mispricing may cause the stock returns to incorrectly reflect the true extent of the underlying economic news (Beatty, 2007).

These weaknesses suggest that the AT measure may be a biased estimator of the true degree of accounting conservatism in the sample. But the debate about the ex-istence and the direction of the bias in the AT measure is still unsettled in the litera-ture. Gigler and Hemmer (2001) and Dietrich et al. (2007) argue that the Basu mea-sure may be biased upward. Although the conclusions are similar, these two studies are based on very different theoretical grounds. Gigler and Hemmer’s (2001) study is based on an agency model of pre-emptive voluntary disclosure, while Dietrich et al.’s (2007) study is almost entirely based on econometric issues (see footnote 4 for Dietrich et al.’s main argument). Givoly et al. (2007) also come to a similar conclusion that the Basu measure is not valid, but do not provide any indication as to whether it is biased upward or downward.

On the other side of the debate, Ryan (2006) strongly supports the AT measure and argues that, with more robust model specifications as well as empirical designs, the AT measure may not be as strongly biased as it is argued by Dietrich et al.

4In Dietrich et al (2007), the sample-variance-ratio bias describes the well-known econometric

result that reverse regressions are generally biased, except in certain limited situations. The sam-ple truncation bias is caused by partitioning the samsam-ple into good-news and bad-news firms based on stock returns. However, at a more fundamental level, both problems appear to be caused by the fact that stock returns contain non-earnings news as well as earnings news, which introduces measurement errors to the regressor in the Basu AT regression.

(2007). In particular, he suggests that the validity and robustness of the AT measure can be improved by incorporating industry-specific proxies for economic ‘news’ and by controlling for the effects of business cycles (Ryan, 2006).

1.2.2

Asymmetric Accrual to Cash-flow Measure (AACF)

Ball and Shivakumar (2005) developed the AACF measure in order to estimate the degree of accounting conservatism in private (unlisted) companies, as Basu’s AT measure is not suitable for private companies given that there is no stock price information available for private companies. To overcome this difficulty, Ball and Shivakumar (2005) developed essentially the non-stock-market equivalent of the AT measure, which is based on the following cross-sectional regression:

ACCit=β0+β1DCFOit+β2CFOit+β3DCFOitCFOit+εit

where

• ACCit: Operating accruals, measured as ∆Inventory + ∆Debtors + ∆Other

current assets -∆Creditors -∆Other current liabilities - Depreciation.

• DCFOit: Dummy variable that is set to 0 ifCFOit ≥0 , and is set to 1 if

CFOit <0.

• CFOit: Cash-flow for period t.

In the regression above, the coefficient β3 is the AACF measure of accounting

conservatism. A higher β3 indicates a higher degree of accounting conservatism.

Clearly, the AACF measure and the Basu AT measure are based on the same fun-damental idea of asymmetric timeliness and are estimated from models with a very similar structure. In essence, both models regress an earnings variable on a proxy

for economic ‘news’. Both models employ dummy variables (DR and DCFO) to distinguish between ‘good-news’ and ‘bad-news’. The main difference between these two measures comes from their different choices of the proxies for economic ‘news’ and the response variable. The Basu AT model uses stock return as the proxy for news, whereas the AACF measure uses operating cash-flow as the proxy for news. In terms of the response variable, the Basu AT model uses total earnings, whereas the AACF measure selects only the accrual component of total earnings. Ball and Shivakumar (2005; 2006) use the accrual component of total earnings be-cause, in their view, accounting conservatism mainly influences the accruals com-ponent of earnings rather than the cash flows comcom-ponent.

Table 1.1 shows that, out of the 53 papers surveyed, only seven papers applied the AACF measure. This relatively low frequency is probably due to the AACF measure being the most recently developed among the five measures reviewed. However, it appears that conservatism researchers are increasingly interested in us-ing the AACF measure as an alternative to the Basu AT measure, given the criticisms of the Basu AT measure. For example, the concerns about validity of the Basu AT measure have led Lara et al. (2009a) to estimate the AACF measure in addition to the AT measure in their study of the relationship between corporate governance and accounting conservatism. The main reason for adopting the AACF measure in ad-dition to the AT measure, as explained by Lara et al. (2009a), is to ensure that the paper’s main empirical results obtained by the AT measure are not spurious.

The strengths and weaknesses of the AACF measure have not been discussed to any great extent in the conservatism literature, possibly due to the fact that this mea-sure is a relatively new one and its robustness has not yet been validated. To date, the conservatism literature has not identified any bias in the AACF measure either. Clearly, more validation research is required before the strengths, weaknesses and

any potential bias in the AACF measure can be fully understood.

1.2.3

The Market-to-Book (“MTB”) or Book-to-Market (“BTM”)

ratio

The idea underlying the use of MTB (or BTM) as a measure of accounting conser-vatism is that, ceteris paribus, a conservative accounting system tends to depress the net book value of a firm relative to the firm’s ‘true’ economic value. There-fore, a higher MTB (and a lower BTM) implies a higher degree of accounting con-servatism, and vice versa.5 The MTB measure is strongly rooted in the analytical

work based on the Residual Income Valuation Model (RIVM) (Feltham and Ohlson, 1995; Zhang, 2000; Beaver and Ryan, 2000). Feltham and Ohlson (1995) first intro-duced accounting conservatism in the RIVM context, and characterize conservatism as a tendency to bias downwards the book value of a firm relative to its market value. This manifestation of conservatism has been carried into later analytical work on conservatism, such as Beaver and Ryan (2000; 2005) and Zhang (2000).

In addition to the raw MTB (or BTM) ratio, Beaver and Ryan (2000) developed a refinement in using the BTM as a measure of conservatism, which has been quite widely applied in the literature. This refinement decomposes the BTM ratio into two components - the bias component and the lag component. Beaver and Ryan (2000) argue that the bias component of BTM should be interpreted as a measure of accounting conservatism. In order to decompose BTM, Beaver and Ryan (2000) regress BTM on a series of lagged stock returns, leading up to six lagged years, as in the following fixed-effect panel data regression:

5It should be noted that MTB is positive measure of conservatism, whereas BTM is a negative