AN EVALUATION OF THE PREDICTIVE

VALUE OF BANK FAIR VALUES

BY

OLUDIMU OLUSEUN EHALAIYE

A thesis

submitted to the Victoria University of Wellington in fulfilment of the requirements for the degree of

Doctor of Philosophy

Victoria University of Wellington 2014

i

ACKNOWLEDGEMENTS

I am very grateful to my supervisors, Professor Tony van Zijl and Professor Mark Tippett for the unflinching support, priceless guidance and immense encouragement they provided to me throughout the writing of this thesis. Both Mark and Tony have gone to great lengths to ensure I succeed not just on the PhD, but in life too. I could not have asked for any better supervisors to have led me on my PhD journey. My gratitude also goes to Professor Keitha Dunstan (Bond University, Australia), Dr Ekoja B. Ekoja, Mr Emma Oki and Olayinka Moses (University of Jos, Nigeria), Iyinoluwa Ologe (Monash University, Australia), Dr Carolyn Cordery, Dr Bhagwan Khanna, Dr Thu Phuong Truong, Dr Noor Houqe, Kevin Simpkins and Jane Perry for their assistance during the period of my study at Victoria University of Wellington.

To every other member of staff and PhD colleagues of the School of Accounting and Commercial Law, Victoria University of Wellington, I say a big thank you for your profound support, advice and camaraderie. Special thanks to Nam Le, for your friendship, ideas and chitchat throughout our time together on the PhD.

I wish to express my gratitude to Victoria University of Wellington (VUW) for providing me with the VUW Doctoral Assistantship and PhD Submission Scholarship and the Steel family for granting me the R.W Steel Scholarship in Accounting. I am also grateful to the University of Jos, Nigeria for granting me a training leave for my PhD studies.

My sincere love and thanks goes to my church and nuclear families; in particular my wife- Yemisi and my daughters- Tomi and Ifeoluwa, whose love and support have been the bedrock of my success. I am also grateful to the ELIM Wellington family, my mum and brothers who have cheered me on all the way. To my late dad, this thesis is dedicated to your memory and to God; I could not have become what I am without You.

ii

STATEMENT OF ORIGINAL AUTHORSHIP

I hereby declare that this submission is my own work and to the best of my knowledge it contains no materials previously published or written by another person, or substantial proportions of materials which have been accepted for the award of any other degree or diploma at Victoria University of Wellington or any other educational institutions, except where due acknowledgement is made in this thesis. Any contribution made to the research by others, with whom I have worked at Victoria University of Wellington or elsewhere, is explicitly acknowledged in this thesis.

I also declare that the intellectual content of this thesis is the product of my own work, except to the extent that assistance from others in the project’s design and conception or in style, presentation and linguistic expression is acknowledged.

Signature:

iii

ABSTRACT

This thesis examines whether the net asset fair values of banks possess predictive ability for the banks’ future cash flows and earnings. This is an important issue considering the arguments for and against the wider use of fair value accounting for banks’ financial instruments and the claim by some that fair values during economic recessions (where markets may be illiquid) are irrelevant and largely unreliable. A number of studies have found that the explanatory power of bank fair values when compared to traditional historical cost are more value-relevant based on capital market reactions. However, there is a very limited literature on how bank fair values are related to the future performance (e.g. earnings and cash flow) of banks. This study fills this gap by providing empirical evidence on the relationship between U.S. bank fair value disclosures and banks’ future performance as measured by operating cash flows and earnings over a three-period future horizon. Furthermore, the thesis provides evidence on the relationship between bank fair values, in terms of the levels classification introduced during the 2008 global financial crisis, and the future performance of banks, thus showing whether market illiquidity affected the underlying relationships.

The study examines two distinct periods. The first study period, 1996-2005, was based on annual data of banks with minimum total assets of $US150 million as of year 1996. The second study period from 2008-2010 (this period encompassed the global financial crisis period and also the levels classification of bank fair values according to SFAS 157), was based on quarterly data of banks with minimum total assets of $US150 million as of the first quarter of 2008.

The thesis provides strong evidence that there is a predictive relationship between bank fair values and future bank performance. The evidence is strong during the first study period from 1996 to 2005 where the current net asset fair values of on-balance sheet financial instruments of banks were significantly associated with future operating cash flows and operating earnings of such banks over a three-year future time horizon. However, the predictive relationship between net asset bank fair values and operating cash flows is stronger than the predictive relationship between net asset bank fair values and operating earnings.

In the second study period, from 2008 until 2010 the empirical results show strong evidence that there is a predictive relationship between level 1 and level 2 bank fair values and future operating cash flows. The findings from the empirical results were that the current quarter’s level 1 and level 2 net asset fair values of banks were significantly associated with the future quarters’ operating cash flows of such banks. The level 3 net asset fair values of such banks in most cases were not significantly

iv

associated with the banks’ future quarterly operating cash flows. The corresponding relationships for operating earnings were that the current quarter’s level 1 net asset fair values of banks were positively associated with the future quarters’ operating earnings of such banks. However, the level 2 net asset fair values of banks were negatively associated with the future quarters’ earnings of such banks. This result is in contrast to the results obtained when the predictive relationship between level 2 bank fair values and future operating cash flows was evaluated, where it is found that both level 1 and level 2 net asset bank fair values are positively related to future quarterly bank cash flows. Further empirical analysis showed that a possible reason behind this disparity was that there was a structural change in the relationship between bank operating cash flows and operating earnings over the course of the first and second study periods, where, in particular, for the second study period (which includes the period of the global financial crisis) there was a systematic downward bias in operating earnings relative to the operating cash flows of the sampled banks. This in turn makes operating earnings a poor proxy for operating cash flows during the second study period.

The findings from this study provide confirmation that net asset fair values have predictive ability as argued by Ball (2008); Barth (2006b) and Tweedie (2008). The study findings that net asset fair values have predictive ability is consistent with the FASB’s view that the asset values shown in firm financial statements should communicate information about the potential future financial performance of the affected firms (FASB 2010:17). Furthermore, the study also confirms that objectively determined bank fair values based on market prices rather than model based bank fair values provide greater predictive value in relation to future performance as measured by operating cash flows.

Lastly, this thesis showed that during the first study period (where there was no financial crisis) that bank size, capital adequacy and growth prospects, had little impact on the results obtained, while for the second study period, there were cases where bank size and bank capital ratios did have a significant impact on the predictive relationship between bank fair values and future cash flows.

The study contributes to the fair value accounting and accounting standard-setting literature and highlights that fair values have predictive ability, especially with respect to future operating cash flows of banks, both during and outside of periods of financial crisis.

v

TABLE OF CONTENTS

ACKNOWLEDGEMENTS... i

STATEMENT OF ORIGINAL AUTHORSHIP ... ii

ABSTRACT ...iii

TABLE OF CONTENTS ... v

LIST OF TABLES AND FIGURES ... x

GLOSSARY AND ABBREVIATIONS ... xv

CHAPTER ONE: INTRODUCTION ... 1

1.1 Motivation ... 3

1.2 Theoretical Framework... 5

1.3 Research Methodology ... 6

1.4 Summary of key Findings ... 7

1.5 Organisation of the Thesis ... 9

CHAPTER TWO: ACCOUNTING STANDARDS, FAIR VALUE ACCOUNTING AND FINANCIAL INSTRUMENTS ... 11

2.1 FASB Conceptual Framework and the Decision-usefulness (Relevance) Doctrine ... 12

2.2 The primacy of “Relevance” over “Reliability” and the move to “Representational Faithfulness” ... 15

2.3 U.S. Standard-Setting history and the movement towards more Fair Value Accounting ... 17

2.4 Fair Value, Fair Value focused standards and IASB Harmonisation ... 19

2.4.1 What is Fair Value? ... 19

2.4.2 Fair-value focused standards issued by the FASB and IASB ... 22

2.5 Financial Instruments Measurement, Valuation and Fair Value Accounting ... 27

2.5.1 What are financial instruments? ... 27

vi

2.5.3 The Case for fair value measurement of financial instruments ... 33

2.5.4 The Case against fair valuation and measurement of financial instruments ... 35

2.6 Fair Value Accounting, Financial Crisis and the recent Procyclicality Debate .... 38

2.6.1 Evidence for and against the procyclical nature of FVA in the crisis of 2007-2009 ... 39

2.6.2 Reaction to additional guidance provided for fair value accounting rules during the crisis ... 40

2.7 Summary ... 42

CHAPTER THREE: REVIEW OF RELATED LITERATURE ... 45

3.1 Brief Historical Background of the Fair Value Concept in Accounting ... 46

3.2 Theory of Fair Value and Accounting Measurement bases... 51

3.3 Value-Relevance and Fair Value Accounting ... 65

3.3.1 The Value Relevance and Reliability of fair values based on a capital markets correspondence approach pre- SFAS 157 ... 69

3.4 The Value-relevance of Fair values - The Predictive ability approach ... 78

3.5 Fair Values and Managerial Discretion ... 82

3.6 Fair Value Accounting and the last two Economic Recessions ... 84

3.6.1 The 2001 U.S. Economic Recession: The Dotcom Bubble ... 85

3.6.2 The 2007 Global Financial Crisis... 85

3.7 Value Relevance of fair values -Post SFAS 157 ... 86

3.8 Summary ... 88

CHAPTER FOUR: THEORETICAL FRAMEWORK AND HYPOTHESES DEVELOPMENT ... 90

4.1 Decision-Usefulness, Efficient Market Hypothesis and Firm Value ... 91

4.2 Agency Theory, Managerial Incentives and Financial Performance ... 95

4.3 Future Cash flows, Future Earnings and Fair Values ... 99

vii

4.5 Summary ... 102

CHAPTER FIVE: RESEARCH METHODOLOGY ... 103

5.1 Study Period ... 103

5.2 Data Sources ... 105

5.3 Sample Selection ... 106

5.3.1 Sample Selection: First Study Period, Annual Data: 1996-2005 ... 107

5.3.2 Sample Selection: Second Study Period, Quarterly Data: 2008-2010 ... 110

5.4 Measures of Bank Fair Values, Cash flows and Earnings ... 112

5.4.1 Bank Fair Values for the annual data from 1996 to 2005... 112

5.4.2 Bank Fair Values for the quarterly data from 2008 to 2010 ... 112

5.4.3 Cash flows ... 112

5.4.4 Earnings ... 113

5.5 Hypotheses Testing Procedures ... 113

5.5.1 Data Transformation and Regression Diagnostics ... 120

5.5.2 Sensitivity and Robustness Analysis ... 123

5.6 Summary ... 127

CHAPTER SIX: RESULTS: FAIR VALUES AND FUTURE CASH FLOWS .... 129

6.1 Descriptive Statistics ... 129

6.2 Multivariate Results ... 143

6.2.1 Bank Fair Values and Future Operating Cash flows pre-SFAS 157 (Hypothesis 1a) ... 143

6.2.2 Bank Quarterly Fair Values and Future Operating Cash flows post-SFAS 157 (Hypothesis 2a)... 145

6.3 Sensitivity and Robustness Tests ... 151

6.3.1 Multicollinearity Issues ... 151

viii

6.3.3 Specific fair value asset and Liability regressions for the first study

period ... 171

6.3.4 Further Robustness Tests ... 174

6.4 Summary ... 176

CHAPTER SEVEN: RESULTS: FAIR VALUES AND FUTURE EARNINGS ... 178

7.1 Descriptive Statistics ... 178

7.2 Multivariate Results ... 191

7.2.1 Bank Fair Values and Future Operating Earnings pre-SFAS 157 (Hypothesis 1b) ... 191

7.2.2 Bank Quarterly Fair Values and Future Operating Earnings post-SFAS 157 (Hypothesis 2b)... 193

7.3 Sensitivity and Robustness Tests ... 200

7.3.1 Multicollinearity Issues ... 200

7.3.2 The Influence of Bank Characteristics ... 203

7.3.3 Specific fair value asset and Liability regressions for the first study period ... 219

7.3.4 Further Robustness Tests ... 223

7.4 Summary ... 225

CHAPTER EIGHT: SUMMARY AND CONCLUSION ... 228

8.1 Summary and Main Findings ... 228

8.2 Discussion and Contribution ... 235

8.2.1 The Performance Prediction Value of Bank Fair Values ... 235

8.2.2 The Performance Prediction Value of Bank Fair Values during Financial Crisis... 236

8.2.3 Fair Value Cash flow Prediction versus Fair Value Earnings Prediction.. 237

8.2.4 Bank Operating Cash flows versus Bank Operating Earnings during the Global Financial Crisis ... 237

ix

8.2.6 Bank Capital Adequacy, Bank Fair Values and Bank Future Cash Flows ... 240

8.2.7 Growth Prospects and the Predictive Value of Bank Fair Values... 241

8.2.8 Liability Fair Values, Credit-rating downgrade and Profit Benefits ... 242

8.2.9 The Inverse Hyperbolic Sine Transformation... 242

8.2.10 Specific Asset and Liability Fair Values Predictive Value ... 243

8.3 Limitations and Directions for Future Research... 243

REFERENCES ... 246

APPENDIX ONE: Extract of fair value estimates reported by Associated Banc-Corp for the year 1996 ... 259

APPENDIX TWO: Extract of the Levels classified fair values according to SFAS 157 reported by Associated Banc-Corp for the first quarter of 2008 ... 261

APPENDIX THREE: Sample Banks with future Operating Cash flows at time t+1 ... 266

APPENDIX FOUR: Sample Banks with future Operating Cash flows at time t+2 ... 273

APPENDIX FIVE: Sample Banks with future Operating Cash flows at time t+3 ... 280

APPENDIX SIX: Sample Banks with future Operating Earnings at time t+1... 286

APPENDIX SEVEN: Sample Banks with future Operating Earnings at time t+2 ... 292

x

LIST OF TABLES AND FIGURES

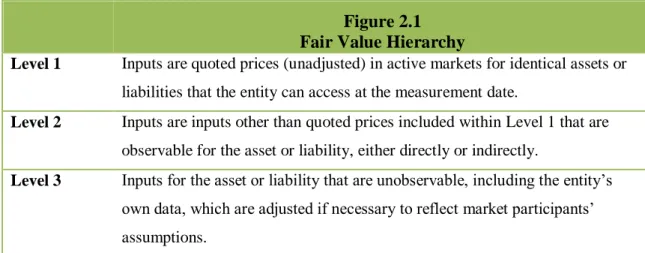

Figure 2.1: Fair Value Hierarchy ... 30

Figure 2.2: Application of Fair Value Hierarchy Levels ... 30

Table 3.1: Advantages and Disadvantages of Various Accounting Measurement Bases... 53

Table 3.2: The Fair Value View Versus The Alternative View ... 58

Table 5.1: Sample Selection Procedure for first study period (1996-2005) ... 109

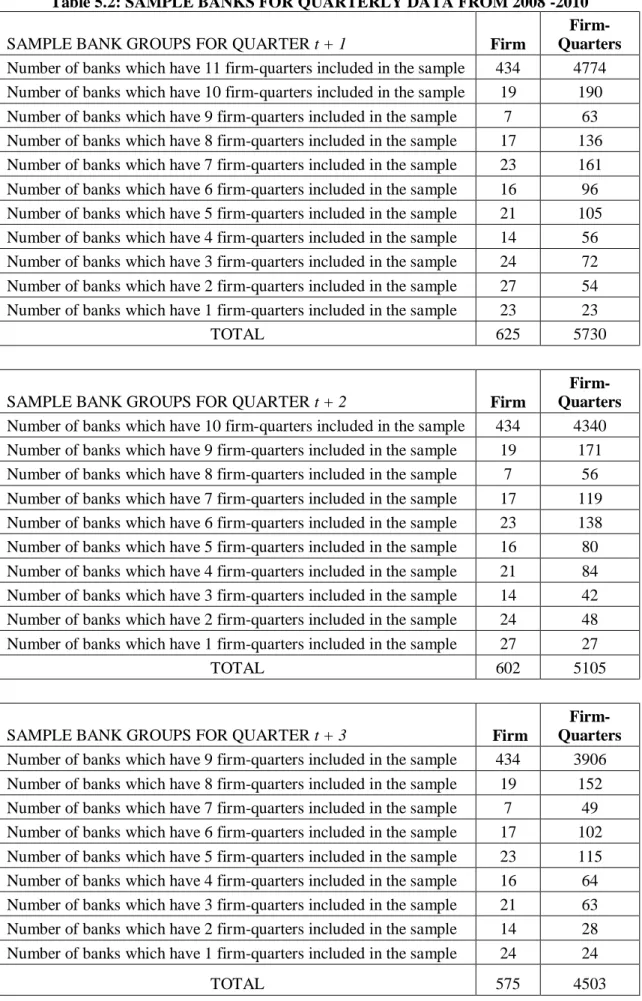

Table 5.2: Sample Banks for Quarterly Data from 2008-2010 ... 111

Table 5.3: Model specifications for the relationships between bank fair values and their future cash flows and earnings for annual data covering the period 1996 to 2005 ... 114

Table 5.4: Definitions of Dependent and Independent Variables for annual data covering the period 1996 to 2005 (Panel A). ... 116

Table 5.4: Definitions of Dependent and Independent Variables for annual data covering the period 1996 to 2005 (Panel B). ... 116

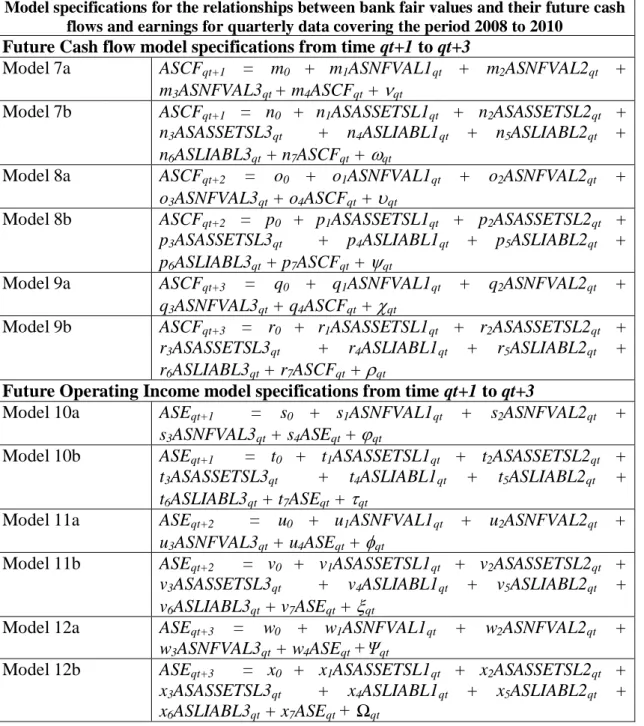

Table 5.5: Model specifications for the relationships between bank fair values and their future cash flows and earnings for quarterly data covering the period 2008 to 2010 ... 117

Table 5.6: Definitions of Dependent and Independent Variables for quarterly data covering the period 2008 to 2010 (Panel A). ... 119

Table 5.6: Definitions of Dependent and Independent Variables for quarterly data covering the period 2008 to 2010 (Panel B). ... 119

Figure 5.1: Inverse hyperbolic sine function graph over the domain–5 ≤x≤ 5. ... 121

Figure 5.2: Logarithm function graph. ... 121

Table 5.7: Model specifications for the relationships between specific fair values of classes of assets and liabilities and their future operating cash flows and operating earnings for annual data covering the period 1996 to 2005. ... 124

Table 5.8: Definitions of Dependent and Independent Variables for the specific fair value data covering the period 1996 to 2005 (Panel A). ... 125

Table 5.8: Definitions of Dependent and Independent Variables for the specific fair value data covering the period 1996 to 2005 (Panel B). ... 125

xi

Table 6.1: Descriptive Statistics for the first study period (1996-2005) for the

variables in $US millions ... 131

Table 6.2: Descriptive Statistics for the first study period (1996-2005) for the transformed data ... 132

Table 6.3: Descriptive Statistics for the second study period (2008-2010) for the variables in $US millions ... 135

Table 6.4: Descriptive Statistics for the second study period (2008-2010) for the transformed data ... 137

Table 6.5: Correlation Matrices (Panels C1-C3) for the first study period (1996-2005)... 138

Table 6.6: Correlation Matrices (Panels C4-C6) for the first study period (1996-2005)... 139

Table 6.7: Correlation Matrices (Panels D1-D3) for the second study period (2008-2010) ... 141

Table 6.8: Correlation Matrices (Panels D4-D6) for the second study period (2008-2010) ... 142

Table 6.9: Relationship between bank net fair values and operating cash flows in future years 1, 2 and 3. ... 144

Table 6.10: Relationship between bank fair value assets, liabilities and operating cash flows in future years 1, 2 and 3. ... 145

Table 6.11: Relationship between Levels Net bank fair value assets and operating cash flows in future quarters 1, 2 & 3. ... 148

Table 6.12: Relationship between Levels bank fair value assets, liabilities and operating cash flows in future quarters 1, 2 & 3. ... 149

Table 6.13: Multicollinearity Test for Model 1a (Using Condition Index)... 153

Table 6.14: Multicollinearity Test for Model 1a (Using VIF Factor) ... 153

Table 6.15: Multicollinearity Test for Model 1b (Using Condition Index) ... 153

Table 6.16: Multicollinearity Test for Model 1b (Using VIF Factor) ... 153

Table 6.17: Multicollinearity Test for Model 7a (Using Condition Index)... 153

Table 6.18: Multicollinearity Test for Model 7a (Using VIF Factor) ... 154

xii

Table 6.20: Multicollinearity Test for Model 7b (Using VIF Factor) ... 154 Table 6.21: Relationship between bank net fair values and operating cash flows

in future years 1, 2 and 3. ... 156 Table 6.22: Relationship between Levels Net bank fair value assets and operating

cash flows in future quarters 1, 2 and 3. ... 158 Table 6.23: Relationship between Levels bank fair value assets, liabilities and

operating cash flows in future quarters 1, 2 & 3. ... 161 Table 6.24: Relationship between bank net fair values and operating cash flows

in future years 1, 2 and 3. ... 162 Table 6.25: Relationship between Levels Net bank fair value assets and operating

cash flows in future quarters 1, 2 and 3.. ... 164 Table 6.26: Relationship between Levels bank fair value assets, liabilities and

operating cash flows in future quarters 1, 2 & 3. ... 168 Table 6.27: Relationship between bank net fair values and operating cash flows

in future years 1, 2 and 3 with and without an asset growth variable, during the first study period. ... 172 Table 6.28: Relationship between Levels Net bank fair value assets and operating

cash flows in future quarters 1, 2 and 3 with and without an asset growth variable, during the second study period.. ... 173 Table 6.29: Relationship between bank specific asset and liability fair values and

operating cash flows in future years 1, 2 and 3, during the first study period.. ... 174 Table 7.1: Descriptive Statistics for the first study period (1996-2005) for the

variables in $US millions. ... 180 Table 7.2: Descriptive Statistics for the first study period (1996-2005) for the

transformed data. ... 181 Table 7.3: Descriptive Statistics for the second study period (2008-2010) for the

variables in $US millions. ... 183 Table 7.4: Descriptive Statistics for the second study period (2008-2010) for the

transformed data. ... 185 Table 7.5: Correlation Matrices (Panels C1-C3) for the first study period

(1996-2005). ... 186 Table 7.6: Correlation Matrices (Panels C4-C6) for the first study period

xiii

Table 7.7: Correlation Matrices (Panels D1-D3) for the second study period

(2008-2010). ... 189

Table 7.8: Correlation Matrices (Panels D4-D6) for the second study period (2008-2010). ... 190

Table 7.9: Relationship between bank net fair values and operating earnings in future years 1, 2 and 3.. ... 192

Table 7.10: Relationship between bank fair value assets, liabilities and operating earnings in future years 1, 2 and 3. ... 192

Table 7.11: Relationship between Levels Net bank fair value assets and operating earnings in future quarters 1, 2 and 3. ... 195

Table 7.12: Relationship between Operating Cash flows and Operating Earnings across the two study periods.. ... 196

Figure 7.1: Relationship between Operating Cash flows and Earnings during the first study period. ... 197

Figure 7.2: Relationship between Operating Cash flows and Earnings during the second study period. ... 197

Table 7.13: Relationship between Levels bank fair value assets, liabilities and operating earnings in future quarters 1, 2 & 3. ... 200

Table 7.14: Multicollinearity Test for Model 4a (Using Condition Index). ... 202

Table 7.15: Multicollinearity Test for Model 4a (Using VIF Factor). ... 202

Table 7.16: Multicollinearity Test for Model 4b (Using Condition Index). ... 202

Table 7.17: Multicollinearity Test for Model 4b (Using VIF Factor). ... 202

Table 7.18: Multicollinearity Test for Model 10a (Using Condition Index). ... 202

Table 7.19: Multicollinearity Test for Model 10a (Using VIF Factor). ... 203

Table 7.20: Multicollinearity Test for Model 10b (Using Condition Index). ... 203

Table 7.21: Multicollinearity Test for Model 10b (Using VIF Factor)... 203

Table 7.22: Relationship between bank net fair values and operating earnings in future years 1, 2 and 3.. ... 205

Table 7.23: Relationship between Levels Net bank fair value assets and operating earnings in future quarters 1, 2 and 3. ... 208

xiv

Table 7.24: Relationship between Levels bank fair value assets, liabilities and operating earnings in future quarters 1, 2 & 3. ... 211 Table 7.25: Relationship between bank net fair values and operating earnings in

future years 1, 2 and 3. ... 212 Table 7.26: Relationship between Levels Net bank fair value assets and operating

earnings in future quarters 1, 2 and 3. ... 214 Table 7.27: Relationship between Levels bank fair value assets, liabilities and

operating earnings in future quarters 1, 2 & 3. ... 217 Table 7.28: Relationship between bank net fair values and operating earnings in

future years 1, 2 and 3 with and without an asset growth variable, during the first study period. ... 221 Table 7.29: Relationship between Levels Net bank fair value assets and operating

earnings in future quarters 1, 2 and 3 with and without an asset growth variable, during the second study period.. ... 222 Table 7.30: Relationship between bank specific asset and liability fair values and

operating earnings in future years 1, 2 and 3, during the first study period.. ... 223

xv

GLOSSARY AND ABBREVIATIONS

AAA The American Accounting Association

AICPA American Institute of Certified Public Accountants

APB Accounting Principles Board

ASB Accounting Standards Board of the United Kingdom

CoCoA Continuously Contemporary Accounting

EDGAR Electronic Data Gathering, Analysis and Retrieval

FASB Financial Accounting Standards Board

FIFO First in First out

FVA Fair Value Accounting

GAAP Generally Accepted Accounting Principles

GPFR General Purpose Financial Reports

IAS International Accounting Standards

IASB International Accounting Standards Board

IASC International Accounting Standards Committee

IFRS International Financial Reporting Standards

JWG Joint Working Group of Standard Setters

LIFO Last in First out

SEC The United States Securities and Exchange Commission

SFAC Statement of Financial Accounting Concepts

SFAS Statement of Financial Accounting Standards

U.K. The United Kingdom

1

CHAPTER ONE INTRODUCTION

During the recent global financial crisis from 2007 onwards, the issue of “Fair Value Accounting” (FVA), as laid down by international standard setters, notably the International Accounting Standards Board (IASB, hereafter) and the United States based Financial Accounting Standards Board (FASB, hereafter), has come under heavy scrutiny and criticism1. The issues involved strike at the core of the accounting profession and its place in the modern globalised economy. This is true of the profession’s financial reporting role and the impact different accounting measurement bases may have on financial market stability. Two main questions summarise the FVA debate and they can be described as “accounting to who” and “accounting for what?” These issues, though not new, have deepened with respect to the FVA debate during the global financial crisis and answers are being sought within and outside accounting circles to chart the course for the way forward.2

What value then is “fair”? And to whom is this value fair? These questions have generated significant debate over the years, but in this study I examine the above questions from the perspective of the FASB3. The FASB in its recent conceptual framework has taken the stand that accounting information should be primarily focused on existing and potential investors, lenders, and other creditors who cannot command

1

A number of discussion papers have criticised the role of FVA on valuation of financial institutions assets claiming it worsened the financial crisis. e.g. American Bankers Association (2008) and Wallison (2008).

2

Statements from politicians, regulators and other market participants show significant interest in the accounting rules and principles related to FVA. The U.S. Congress, the G7’s Financial Stability Forum (FSF) and the Institute of International Finance (IIF) have all given opinions on FVA.

3

The IASB and the FASB have worked together on the harmonisation of their fair value accounting related standards and Conceptual Frameworks.

2

reporting entities to provide information directly to them (FASB, 2010:7). The FASB believes that a single general purpose financial report will to a large extent meet the needs of these investors and lenders (FASB, 2010:7). Hence, in this thesis the concept of for whom “fair value is fair” focuses on the investor. What constitutes the fair value of an asset to an investor? Fair value estimates are expected to represent the present value of the expected future cash flows associated with an asset [or liability] (Barth, 2000:19; Ryan, 2008a:12). Consequently, fair value should be those values most value-relevant to investors when making investment decisions. A series of studies have established the greater relevance to the investor of fair values in relation to capital market reactions, especially when fair values are compared with the traditional historical/amortised cost concepts of accounting for net assets (Barth, 1994; Barth, Beaver, and Landsman, 1996; Eccher, Ramesh, and Thiagarajan, 1996; Song, Thomas and Han, 2010).

The FASB also states that the two fundamental qualitative characteristics of financial information are “relevance” and “faithful representation”. According to the FASB (2010:16):

If financial information is to be useful, it must be relevant and faithfully represents [sic] what it purports to represent.

Financial information is relevant if it is capable of making a difference in the decisions made by users, if it has “predictive value”, “confirmatory value”, or both. Financial information has predictive value if it can be used as an input to processes employed by users to predict future outcomes and it has confirmatory value, if it provides feedback about prior evaluations. For example, revenue information for the current year should be useful as a basis for predicting revenues in future years (predictive value) and

3

revenue information of the current year should be comparable to predictions in past years (confirmatory value) (FASB, 2010:17).

If asset fair values are an estimate of the future shown today, they should possess predictive value unless the estimates are incorrect, since they are supposed to reflect the expected financial performance of such assets which can be measured either by cash flows or earnings. Hence, an important question is whether the cash flows provided by an asset in the future are associated with the fair values of such assets today? Also, it is worthwhile to consider whether there is a relationship between the future earnings from assets and the fair values of such assets today. This isolates the importance of the predictive value of net assets as a significant aspect of the relevance qualitative characteristic of accounting information in the context of the FASB Conceptual Framework.

Thus the purpose of this thesis is to examine whether the net asset fair values of banks possess predictive ability for the banks’ future performance as measured by the banks’ operating cash flows and earnings.

1.1 Motivation

During the global financial crisis, objections to the application of fair value accounting by financial institutions, especially by banks and their lobby groups, have increased (Laux and Leuz 2009; Ryan, 2008a:18).4 The interesting issue though is that during the boom era (pre-the 1st quarter 2007) financial institutions did not lament the use of fair values as they have done recently. Robert Herz, then chairman of the FASB, mentioned that a group of financial institutions in 2006, under more favourable securities market

4

A significant number of discussion articles were published in 2008 on fair value accounting in CFO.com making the topic the most popular of 2008 for discussion by the website. Many of the articles represented adversarial views by bankers on the use of fair values during the economic downturn.

4

conditions, called on the FASB for the choice of fair value measurements for parts of their balance sheets (Katz, 2008a). Since the financial crisis began the tune has changed from extolling the virtues of fair values to the many calls for its suspension. This call grew loud, especially with the application of SFAS 157: measurement of fair values, with regard to issues about illiquidity, prudential/regulatory guidelines compliance and references to forced selling of assets to raise capital, which has been argued to further depress prices (Ryan, 2008a; Plantin, Sapra and Shin, 2008).

Although the recent crisis has hit financial institutions on a significant scale, the reality, however, is that the primary attention of FASB standards is on investors and hence it is important to know whether fair values do have predictive value. Advocates of fair value accounting have responded to the bankers’ protests by suggesting that fair values provided warning for the banks that the market was taking a downward turn, thus hinting at the performance predictive qualities of bank fair values (Ball, 2008; Tweedie, 2008). McGregor (2012), a former IASB board member, commented that in the wake of the global financial crisis a number of commentators had observed that the effect of the global financial crisis could have been much worse if accounting standards had not forced companies to recognise the effects of falling prices in their financial statements sooner than might otherwise have been the case. This statement affirmed the importance of fair value accounting as it is the only current accounting measurement basis that recognises falling prices in the financial statements.

This research is therefore motivated based on this background debate, as it seeks to find answers to the following specific research questions:

5

1. Do the fair values summarised in bank financial statements predict future cash flows and earnings (future financial performance)?

2. In particular, did bank fair values have predictive value in relation to banks’ future financial performance during the 2007/2008 global financial crisis?

Robert Herz, then FASB chairman, was asked, “Did SFAS 157 correctly sound an early alarm on the financial crisis-or did it make a bad situation worse?” (Katz, 2008b). There have been a number of studies that have addressed the second part of the question relating to procyclicality (e.g. Badertscher, Burks, and Easton, 2011; Laux, 2012; Shaffer, 2010). In contrast, only a few studies have attempted to address the first part of this question dealing with predictability in bad economic times?

1.2 Theoretical Framework

The theoretical framework of this thesis is based on the conceptual ideal of decision-usefulness which underpins the fair value paradigm and the efficient market hypothesis, which gives credence to the fair value (based on exit prices) reporting approach espoused by the FASB and IASB. This leads on to the theoretical framework between the market value of bank equity and the fair values of its assets and liabilities as summarised in its published financial statements as developed in the academic literature. Agency theory is used to explain why managers have incentives to over (or under) estimate reported fair values and how this could lead to systematic biases in the fair values summarised in banks’ published financial statements. The firm valuation model, based on the future cash flows a firm expects to generate, is used to explain how future cash flows are linked to the fair values summarised in a firm’s financial statements for its assets and liabilities. Following on from this, I develop hypotheses connecting the fair values summarised in a firm’s published financial statements, with

6

its future cash flows and its future earnings. Specifically, the hypotheses I develop address the question of whether there is a significant relationship between the on-balance sheet financial instrument fair values reported by banks and their future cash flows and earnings. Also this relationship is considered in light of the 2008-2010 global financial crises and the levels classification of fair values under SFAS 157.

1.3 Research Methodology

This thesis employs two distinct study periods. The first covers the ten-year period from 1996 until 2005. The ending year of 2005 was selected in order to avoid contamination of the dataset with the second study period. The second study period runs from 2008 until 2010. The first study period from 1996 to 2005 employs annual data of U.S. banks with over $US150 million in total assets as of the year 1996. The second study period, 2008-2010, covers the global financial crisis which came into full effect in 2008 and bank financial statements prepared over this period reflected the requirements of SFAS 157, which was introduced in 2007.

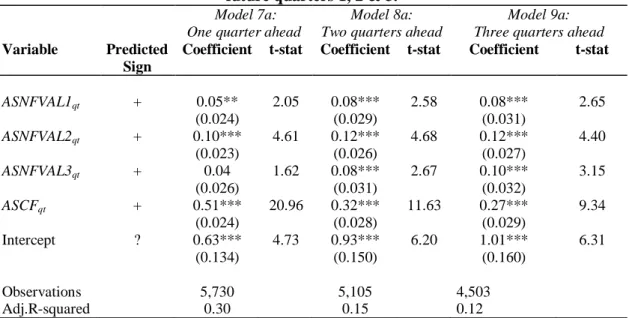

For the first study period, 1996 until 2005, the final sample includes 1,229 firm-years of data for banks having one year ahead (t+1) future cash flows, 1,162 firm-years for banks having two year ahead (t+2) future cash flows and 942 firm-years for banks having three year ahead (t+3) future cash flows. The sample also includes 1,150 firm-years for banks having one year ahead (t+1) future operating earnings, 1,081 firm-years for banks having two year ahead (t+2) future operating earnings and 875 firm-years for banks with three year ahead (t+3) future operating earnings. In relation to the second study period, which employs quarterly data covering the period from 2008 until 2010, the final sample employs a total of 5,730 firm-quarters for banks having one quarter ahead (t+1) future cash flows and operating earnings, 5,105 firm-quarters for banks

7

having two quarter ahead (t+2) future cash flows and operating earnings and 4,503 firm-quarters for banks having three quarter ahead (t+3) future cash flows and operating earnings.

For the first study period (1996-2005) bank fair values were measured as the fair values of financial instruments disclosed in the notes to the financial statements as mandated by SFAS 107. For the second study period (2008-2010), bank fair values were measured according to the levels classified fair values as mandated by SFAS 157. A set of multivariate linear regression models were developed and estimated using ordinary least squares in order to test the hypothesised relationships between bank fair values, future operating cash flows and future operating earnings. The data employed were transformed using the inverse hyperbolic sine function (Laubscher, 1961). This transformation was applied in order to render the data more compatible with the assumptions of the general linear regression model. Most important, however, is that in comparison with other common transformations the inverse hyperbolic sine transformation can deal with negative values.

1.4 Summary of key Findings

The empirical results summarised in this thesis provide strong evidence that there is a predictive relationship between bank fair values and future bank performance. The evidence is strong during the first study period, from 1996 until 2005, that current net asset fair values of on-balance sheet financial instruments of banks were significantly associated with the future years’ operating cash flows and operating earnings of the banks. However, the evidence is stronger for the predictive relationship between bank fair values and operating cash flows than for the predictive relationship between bank fair values and operating earnings.

8

For the second study period, from 2008 until 2010, which employed quarterly data,5 the empirical results provide strong evidence that there is a predictive relationship between level 1 and level 2 bank fair values and future operating cash flows. The findings from the empirical results were that the current quarter’s level 1 and level 2 net asset fair values of banks were significantly positively associated with the future quarters’ cash flows of the banks. The level 3 net asset fair values of the banks were mostly not significantly associated with the banks’ future quarterly cash flows.

With regard to whether there is a predictive relationship between bank fair values and their future operating earnings during the second study period, the findings from the empirical results were that the current quarter’s level 1 net asset fair values of banks were positively associated with the future quarters’ earnings of such banks. However, the level 2 net asset fair values of banks were negatively associated with the future quarters’ earnings of such banks. This result is in contrast to the results noted above, for the predictive relationship between level 2 bank fair values and future operating cash flows. Further empirical analysis showed that a possible reason behind this difference was that there was a structural change in the relationship between bank operating cash flows and operating earnings over the course of the first and second study periods, where, in particular, for the second study period (which includes the period of the global financial crisis) there was a systematic downward bias in operating earnings relative to the operating cash flows of the sampled banks. This in turn makes operating earnings a poor proxy for operating cash flows during the second study period.

Several robustness and sensitivity tests relating to the empirical procedures employed especially with respect to the impact of bank size, capital adequacy and growth

5

This period encompassed the global financial crisis period and also the levels classification of bank fair values according to SFAS 157.

9

prospects were carried out. Overall, the robustness tests had little impact on the results obtained for the first study period. However, for the second study period, there were cases where bank size and bank capital ratios did have a significant impact on the predictive relationship between bank fair values and future cash flows. Also during the second study period the structural change in the relationship between bank operating cash flows and operating earnings had a perverse effect on the estimated regression equations relating bank fair values to operating earnings. This structural change in the relationship between bank operating cash flows and operating earnings during the second study period may have accentuated the impact that bank size and bank capital ratios have on the predictive relationship between bank fair values and earnings.

1.5 Organisation of the Thesis

The remainder of this thesis is organised as follows. Chapter two examines the history of standard setting by the FASB and the shift towards more fair value accounting as a measurement basis, particularly for financial instruments. It also assesses the case for and against reporting financial instruments at fair value in bank financial statements. The fair value accounting empirical research literature is reviewed in chapter three. This review compares the theoretical case for the implementation of fair value accounting to the other measurement bases. It also deliberates on the empirical literature, particularly in relation to the relevance of fair values in the stock market valuation of the banks comprising my sample. In chapter four, the hypotheses relating to bank net asset fair values and their future cash flows and earnings are developed. These hypotheses are all based on the decision-usefulness doctrine supported in the FASB and IASB Conceptual Frameworks, the efficient markets hypothesis and the market valuation model. Agency theory is also employed to explain why firm

10

management may act opportunistically in determining the fair values to be reported in a firm’s published financial statements. In chapter five, the sample selection process, data collection methods and the hypothesis testing procedures employed in the study of the relationship between U.S. bank fair value disclosures and their future operating cash flows and operating earnings are explained. Chapter six presents and discusses the descriptive statistics and multivariate regression results obtained from the hypothesis testing procedures with regard to the relationships between bank fair values, current year operating cash flows and future operating cash flows. In chapter seven, the descriptive statistics and multivariate regression results obtained from the hypothesis testing procedures with regard to the relationships between bank fair values, current year operating earnings and future operating earnings are presented and discussed. The thesis concludes in chapter eight with a summary and discussion of the key findings and their implications, as well as an overview of the contribution, limitations and suggested directions for future research.

11

CHAPTER TWO

ACCOUNTING STANDARDS, FAIR VALUE ACCOUNTING AND FINANCIAL INSTRUMENTS

This chapter examines the accounting standards setting environment and its relationship with fair value accounting and financial instruments. Section 2.1 discusses the Financial Accounting Standards Board’s (FASB) Conceptual Framework and its emphasis on the decision-usefulness doctrine. In section 2.2 the FASB’s stand on the primacy of relevance over reliability (both providing the basis for decision-usefulness) is explained. The replacement of the term reliability by the term representational faithfulness in the Conceptual Framework is also discussed. In section 2.3 the historical circumstances that led towards the adoption of more fair value oriented accounting in the U.S. are described. Section 2.4 reviews the meaning of fair value emphasising the FASB and International Accounting Standards Board’s (IASB) market value requirement for fair value as the “exit price”. A summary of fair value focused accounting standards under both the FASB and IASB regimes and the influence of the joint IASB/FASB harmonisation project on the definition of fair value in IFRS 13 is also discussed in this section. In Section 2.5 I examine the detailed requirements relating to the valuation of financial instruments under FASB and IASB accounting standards. I also consider the arguments which have been made both for and against the various requirements that appear in these standards. The chapter concludes in section 2.6 with a discussion of recent developments in fair value accounting; specifically, the role of fair value accounting during the 2007 global financial crisis, the procyclicality debate, which relates to the exacerbating effects of fair values on economic cycles and reactions to the additional guidance provided by the Financial Accounting Standards

12

Board in regard to the interpretation of the fair value accounting standards rules during this period. A summary of the chapter is provided in section 2.7.

2.1 FASB Conceptual Framework and the Decision-usefulness (Relevance) Doctrine

The Financial Accounting Standards Board (FASB) was established in 1973, replacing the Accounting Principles Board (APB) of the American Institute of Certified Public Accountants (AICPA). The FASB is a private, not-for-profit organisation whose primary purpose is to develop generally accepted accounting principles (GAAP) in the public interest within the United States. The Securities and Exchange Commission (SEC) has designated the FASB as the organisation responsible for setting accounting standards for public companies in the U.S.

The foundation on which the FASB achieves the purpose for which it was created is referred to as the Conceptual Framework. The FASB specifies in its Conceptual Framework the objectives of financial reporting and standard setting, as well as the criteria standard setters use in selecting among accounting alternatives (Barth, 2006a:9). According to the FASB, the Conceptual Framework is a coherent system of interrelated objectives and fundamental concepts that prescribes the nature, function, and limits of financial accounting and reporting and that is expected to lead to consistent guidance in relation to technical accounting and reporting issues (FASB, 2010). The FASB communicates the Conceptual Framework through its Statements of Financial Accounting Concepts (SFAC) and/or Concepts Statements.

The first Concept Statement issued by the FASB in 1978 was on the objectives of financial reporting by business enterprises. The primary objective of financial reporting

13

highlighted in this statement was to provide information that is useful to present and potential investors and creditors and other users in making rational investment, credit, and similar decisions. It goes further to specify that financial reporting should provide information about the economic resources of an enterprise, the claims to those resources, and the effects of transactions, events, and circumstances that change its resources and claims to those resources (FASB, 1978). This primary basis is referred to as “decision-usefulness”. It focuses the financial reporting objective on the information needs of investors and other users of financial statements when they make economic decisions relating to the reporting entity (Barth, 2006a:9).6 Decision-usefulness emphasises the primary qualitative characteristic of accounting information called “relevance.” Financial information is relevant if it has the capacity to make a difference in a decision by helping users to form predictions about the outcomes of past, present and future events or to confirm or correct prior expectations (FASB, 1980). It can thus be said that right from the establishment of the FASB the decision-usefulness doctrine has been a primary criterion from which accounting standards are generated and developed. Staubus (1999:163) remarked: “Decision-usefulness has been the organising criterion for accounting policy and accounting scholarship for over forty years”. Williams and Ravenscroft (2009) imply further, that policy makers in choosing among data and alternative ways to present the selected data would select the reporting technique which produces the information most useful for economic decision-making by certain designated users. Hitz (2007) acknowledged that the decision usefulness paradigm was established as an official standard setting objective only with the formation of the FASB and the Conceptual Framework. However, this was a

6

In financial reporting research this is also consistent with the information perspective (Beaver,1998; Barth, 2006a:11) which focuses on accounting as providing information for financial statement users about the firm’s financial condition and performance.

14

crystallisation of earlier developments going back to the articulation of criteria for standard setting/financial reporting that was put forward in the AAA monograph A Statement of Basic Accounting Theory (hereafter ASOBAT) in 1966 (AAA, 1966), the Trueblood Report of 1973 (Hitz, 2007; Young, 2006) and APB Statement No. 4: Basic Concepts and Accounting Principles Underlying Financial Statements of Business Enterprises (Accounting Principles Board, 1970).7

The 1966 monograph ASOBAT made a significant contribution in cementing the decision-usefulness doctrine for standard-setting (Young, 2006; Hitz, 2007; Sutton, Cordery and van Zijl, 2010). ASOBAT viewed accounting as a financial information reporting system and the aim of the system was to provide economic information that would inform judgments and decisions by users of such information (Stamp, 1984). This essentially made relevance of financial information for information users the top priority of the accounting process. The contribution of APB Statement No. 4 (1970) to the decision-usefulness paradigm was that it formally articulated the move to promote the information perspective over that of stewardship in accounting standards (Beaver,

1998; Storey and Storey, 1988; Sutton, et al. 2010). The AICPA commissioned

Trueblood Committee Report in 1973 provided postulates that would give direction to the subsequent FASB Conceptual Framework and also advanced arguments for decision-useful, relevant, investor-focused general purpose financial reports (Sutton, et al. 2010; Smith, 1996). The FASB’s Conceptual Framework project drew heavily on the recommendations of the Trueblood Committee and progressively showed an increasing focus on prospective and decision-useful information that, while conceding

7

An historical discussion of the influences that gave rise to the decision-usefulness paradigm can be found in Hendriksen and van Breda (1991, pp. 92-115, 126-131) and Young, 2006. A critique of the evolution of the decision-usefulness paradigm can be found in Williams and Ravenscroft (2009).

15

multiple users, increasingly prioritized investors and creditors as the target of general purpose financial reports (Sutton, et al. 2010; Parker, 1982; Giroux, 1999).

It is important to appreciate the role of the decision-usefulness doctrine which is key to the FASB’s standard setting processes because this doctrine has significantly influenced the move towards more fair value accounting measurement in accounting. Standard setters have increasingly argued that fair value is more relevant (decision-useful) especially with regard to the measurement of financial instruments than the more traditional measurement metric referred to as historical cost.

2.2 The primacy of “Relevance” over “Reliability” and the move to “Representational Faithfulness”

In 1980 the FASB issued Statement of Financial Accounting Concepts No. 2 (SFAC No. 2) (FASB, 1980). In this statement it made clear that the two primary qualities that make accounting information useful for decision-making were “Relevance” and “Reliability”. The FASB however acknowledged that the choice of an accounting alternative should produce information that is both more reliable and more relevant; however, it may be necessary to sacrifice some of one quality for a gain in the other (FASB, 1980).

Reliability was defined in SFAC No. 2 as “the quality of information that assures that information is reasonably free from error and bias and faithfully represents what it purports to represent” (FASB, 1980: 10). Evaluating accounting information choices on the basis of these two qualities led many to believe that relevance and reliability cannot be achieved simultaneously. Hence, there was a question as to what trade-offs are involved between them (Barth 2006a:9).

16

The FASB and the International Accounting Standards Board (IASB) started a joint project to converge their Conceptual Frameworks in 2005. One of the outcomes of this project was to eliminate the term reliability and replace it with the term “representational faithfulness”. According to the FASB (2010:16):

“If financial information is to be useful, it must be relevant and faithfully represents [sic] what it purports to represent.”

This was done because the two boards concluded that the term reliability is widely misunderstood and representational faithfulness more accurately reflects what the term reliability was intended to portray (Barth, 2006a:10 ; Power, 2010).

Even with this change from reliability to representational faithfulness there still exists some tension between relevance and faithful representation because there have been arguments that the value(s) in the financial statements that may be relevant (in this sense of being focused on investors and shareholders) may not be the best value to fulfil all the characteristics that will make such a value representationally faithful. These characteristics include Completeness, Neutrality and Freedom from error/Verifiability. The reality is that values shown in financial statements are not precise; some are estimates, and these estimates may be the most relevant value available to shareholders. However, we may not be sure that these estimates are complete, free from error, neutral and hence, representationally faithful. This is why this tension exists. A particular area where this tension is very apparent in accounting today is the issue of fair value accounting applications by both the IASB and the FASB.

17

2.3 U.S. Standard-Setting history and the movement towards more Fair Value Accounting

According to Jensen (2007) the Historical Cost8 measurement regime has been

employed in the standards of U.S. GAAP from its inception. Hence, traditionally the historical cost basis of measurement has played a very significant role in the shaping of accounting standards. Also, following the creation of the Securities and Exchange Commission (SEC) in 1934 and until the 1970s, the SEC continued to support historical cost as the primary basis for accounting measurement by not supporting proposed methods for upward asset revaluations and restatements (Zeff, 2007). The Great Depression of the 1930s that began with the stock market crash of 1929 also influenced the SEC into requiring historical cost measurement as the method of valuation during this period. This was because overstatement of asset values was seen as being in part to blame for the market crash of 1929 and the follow on Great Depression (Barlev and Haddad, 2003).

However, from the 1970s fair value accounting started to gain more prominence in the standard–setting process. Whittington (2008) identified the fierce and unresolved debates with respect to the issue of inflation accounting9 in the 1970s among standard-setters as a catalyst for the consideration of alternative measures to the historical cost paradigm; and fair value was a valid alternative to consider.

8

Historical Cost accounting is an accounting principle requiring all financial statement items to be based on depreciated original cost. It is usually based upon the dollar amount originally exchanged in an arms-length transaction, an amount assumed to reflect the fair market value of an item at the transaction date.

9

Accounting for asset values during inflationary periods was a vexing problem for standard setters as the historical cost values of such assets quickly became irrelevant to users of financial statements during these times.

18

The Savings and Loans Crisis in the U.S. during the 1980s brought into sharp focus the deficiencies of the historical cost accounting regime which was the prevalent reporting system at the time (Hitz, 2007). This crisis showed how with the help of the historical cost regime, these Savings and Loans companies were able to selectively trade their financial assets (Johnson and Swieringa, 1996). They did this by keeping the loss-making assets on their books at their historical costs (which were higher than their fair values) and sold the assets which were trading above their book values (historical costs). This was a process of ‘cherry picking’ or ‘gains trading’ (Hitz, 2007). These opportunistic practices prompted regulatory intervention by the SEC which among other things advised the FASB to develop an accounting standard for certain debt securities to be valued at their market value (fair value) rather than amortized cost (Wyatt, 1991; Cole, 1992; White, 2003). This regulatory reaction to the Savings and Loans Crisis provided the momentum for the implementation of fair value measurement and the movement towards an increase in fair value oriented accounting standards within the FASB and the IASB.

Also, with the decision-useful and investor-focused emphasis of financial information at the heart of the Conceptual Framework, fair value accounting has continued to be favoured as the best accounting measurement regime that meets these criteria. This was supported by the Jenkins (1994) Committee Report which assumed market efficiency and made the case for more user-focused financial statements and fair values (Sutton, et al. 2010)

Finally, in recent times the wave of more complex financial instruments, especially derivatives, have called into question the validity of historical cost as a measurement

19

regime for financial statement items that can experience rapid changes in prices (Wharton, 2001). Siegel (1995) explains:

“The impetus for change in accounting comes in part from a series of developments in the capital markets: marketing of and trading in complex financial instruments, including derivatives, investments in highly-leveraged and other high-risk securities, and expansion of the role of institutional investors. Some of these investments have resulted in substantial and highly-publicised losses, such as bank losses (and failures) resulting from loans on real estate with impaired value, losses by pension funds and municipalities resulting from leveraged investments and investments in derivatives.”

In considering these complex financial instruments, historical cost measurements have been found to be considerably less helpful and relevant for users of such information. Hence, fair value accounting has been advocated as a better alternative measurement regime for these complex financial instruments (Siegel, 1995; Barth, 1994; Wyatt, 1991).

2.4 Fair Value, Fair Value focused standards and IASB Harmonisation

2.4.1 What is Fair Value?

In simple terms, fair value is the realisable value of an asset or liability in an orderly market. According to SFAS 157 (FASB, 2006a) and IFRS 13 (IASB, 2011) fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. In reality, though, fair value is quite a challenge to define as many factors come into play in determining what fair value is.

20

In its purest form, assuming a fully efficient, liquid and perfect market, fair value should equal market value (Level 1). However, in the real world, where markets are not completely liquid for some assets and liabilities, fair value as described by the FASB and the IASB could be estimated from the values of identical assets which are traded in a liquid market (Level 2) or estimated through model valuations (Level 3) where the inputs used are based on as much relevant market information as possible.

It is important to mention that the market value based on the FASB and IASB requirements, considered as fair value, is the “exit price”; i.e. the price at which an asset could be sold on the reporting date (SFAS 157, IFRS 13). Fair value estimates are expected to represent the present value of the expected future cash flows associated with a financial statement item (Barth, 2000:19; Ryan, 2008a:12; Whittington, 2008:157). Furthermore, the present value of the expected cash flows is determined by discounting at the current market rate of return, and it is considered to reflect all available information up to the measurement date (Chisnall, 2001).

Prior to the issue of IFRS 13, the IASB defined fair value differently from SFAS 157. In paragraph 9 of IAS 39, fair value was defined as “the amount for which an asset could be exchanged, or a liability settled, between knowledgeable, willing parties in an arm’s length transaction”.

Concerning the measurement issues involving fair value estimation, IAS 39 provides three classifications: Active markets for which quoted prices are available, inactive markets for non-equity instruments, and inactive markets for equity instruments. For financial instruments trading in active markets, the appropriate quoted price of an asset held (or liability to be issued) is the current bid price, whereas for assets to be acquired (or liabilities to be held), it is the current ask price. When current bid and ask prices are

21

unavailable, the price of the most recent transaction can be used provided that there has not been a significant change in economic circumstances since the time of the transaction. Additionally, quoted prices can be adjusted if the firm can demonstrate it is not fair value (for example, distress sales). In the absence of an active market for a non-equity financial instrument, IAS 39 specifies that the preferred valuation technique must be the most commonly used procedure by market participants to price the instrument (for example, if the valuation technique has been demonstrated to be able to provide reliable estimates of fair value obtained in actual market transactions). The selected valuation technique needs to be consistent with recognized economic methodologies for valuing financial instruments, and the firm needs to calibrate the valuation technique periodically by testing it for validity using prices from any observable current market transactions in the same instrument (or based on any available observable market data). Finally, for equity instruments (and any linked derivatives) that do not have a quoted market price in active markets, IAS 39 requires that these instruments are to be measured at fair values only if the range of reasonable fair value estimates is not significant, and the probabilities of the various estimates can be reasonably assessed. Otherwise, the firm is precluded from measuring these instruments at fair value (IASB, 2003a, Yong, 2010).

The differences between the fair value definitions in SFAS 157 (IFRS 13) and IAS 39 include that SFAS 157’s definition is explicitly based on the concept of an “exit price,” whereas the IAS 39 definition of fair value is based on neither the exit price nor the entry price of a financial statement item. SFAS 157 uses the “market participants” view whereas the IAS 39 definition of fair value uses the concept of a “willing buyer and seller.” In particular, SFAS 157 states that the fair value of a liability is the price that will be paid to transfer a liability, whereas IAS 39 defines the fair value of a liability as

22

the amount for which it will ultimately be settled (Yong, 2010). As with SFAS 157, IAS 39 states that fair value estimation is not the amount that a firm would receive or pay in a forced transaction, involuntary liquidation, or distress sale (paragraph A69). Also in tandem with SFAS 157, paragraph 48 of IAS 39 regards the best evidence of fair value as quoted prices in an active market. Finally, while IAS 39 does not unequivocally classify valuation inputs into Level 1, Level 2, and Level 3 categories as specified in SFAS 157, it does stipulate that the chosen valuation technique should make maximum use of market inputs and depend as little as possible, on firm-specific inputs (Yong, 2010).

The adoption of IFRS 13 is significant as it can be seen that the IASB worked together with the FASB on these standards as part of the convergence project on the issue of fair value accounting, especially with regard to accounting for financial instruments, thereby settling the differences between the SFAS 157 and IAS 39 definitions highlighted above.

2.4.2 Fair-value focused standards issued by the FASB and IASB

The FASB in the U.S. has issued several standards that require disclosure or recognition of accounting amounts using fair values particularly with regard to financial instruments where such standards have been most significant in their effects. Landsman (2007) provides an overview of these standards. Two important disclosure

standards are SFAS 107, Disclosures about Fair Value of Financial Instruments

(FASB, 1991) and SFAS 119, Disclosure about Derivative Financial Instruments and

Fair Value of Financial Instruments (FASB, 1994). SFAS 107 requires disclosure of fair value estimates of all recognised assets and liabilities, and as such, was the first standard that provided financial statement disclosures of fair value estimates of the