11

Copyright © 2011-15. Vandana Publications. All Rights Reserved.Volume-5, Issue-1, February-2015

International Journal of Engineering and Management Research

Page Number: 11-16

Opinion towards the Important Perspectives of Balanced Scorecard - A

Study with Special Reference IT & ITEs Employees’ of Coimbatore

District

Shyam Umasankar K K1, Dr. Shani J2 1

Research Scholar, Karpagam University, Coimbatore, INDIA 2

ABSTRACT

Indian IT Services is valued at US $ 50 billion sector, BPM valued at USD 20 billion sector, Engineering crossed US $ 10 billion and Software products, Internet & Mobility are emerging sectors in the country. Today, existing and new companies are expanding their IT services to build India as the hub for analytics, mobility, and social collaboration verticals across the healthcare and medical devices sector.The concept of Balanced Scorecard (BSC) is too much relevant in the present era of emerging intense global competition, where the organizations are facing increasingly knowledgeable, demanding customers and activist shareholders.This article aims to analyse opinion of

IT & ITES employees’ towards the important perspectives of

balanced scorecard (Information Technology Enabled Services) employees’, working in Coimbatore district.

Research Supervisor, Karpagam University, Coimbatore, INDIA

Keywords- BPM,Balance Score Card,.Information

technology, Information Technology Enabled Services

I.

INTRODUCTION

Information Technology/ Information Technology Enterprises (IT/ITES), is an arched type of a knowledge economy. IT firms in India, contributes around SIX per cent to nations GDP and earn around 25per cent of export revenues for the Indian economy. Unlike traditional manufacturing and service firms, these firms are characterized by low capital intensity, low Research & Development (R&D) intensity, high knowledge intensity and high human capital intensity. Thus, managing IT/ITES firm poses a gamut of challenges distinct from the challenges that the traditional Managers faced. Moreover, knowledge intensive services employ technical specialists (for example IT engineers in IT firms). Although these specialists have a technical orientation, they rarely have an orientation towards management of IT/ITES businesses.

Lack of managerial inefficiencies demands timely implantation of Balanced Score Card by the IT & ITES firms.It must be a clearly established fact that the objective of any measurement system should be to motivate all managers and employees to implement successfully the business units’ strategy. Those companies that can translate their strategy into measurement system will be able to execute their strategies more effectively because they communicate their objectives and their target groups in a meaning manner. The communication, makes managers and employees focus on the critical drivers enabling them to align investments, initiatives and actions accomplishing strategic goals. Balanced Score Card is a management concept, which can be interpreted, enacted and implemented in various ways for the successful performance of an organization as balanced score card is based on management by objective (MBO) concept. Employees’ behavioral aspects and positive attitudes toward the balanced scorecard (BSC) are very essential for the successful of implementation BSC.

II.

METHODOLOGY

12

Copyright © 2011-15. Vandana Publications. All Rights Reserved.III. OBJECTIVE AND ANALYSIS

This article will prove helpful to the IT & ITEs company’s employees, experts and research scholars in understandingIT & ITES employees’ opinion towards the important perspectives of balanced scorecard.So the primary objective of the study is as follows:

1. To analyse the IT & ITES employees’ opinion towards the important perspectives of balanced scorecard implemented in the organisation by using KMO test and Factor analysis

IV.

STATISTICAL TOOL USED

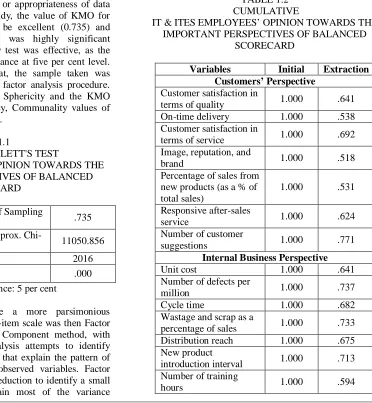

Factor analysis technique has been applied to find the underlying dimension (factors) that exists in the 64 variables relating to the IT & ITES employees’ opinion towards the important perspectives considered in the balanced scorecard of their organization In the present study, Kaiser-Meyer-Oklin (KMO) Measure of Sampling Adequacy (MSA) and Bartlett’s test of Sphericity were applied to verify the adequacy or appropriateness of data for factor analysis. In this study, the value of KMO for overall matrix was found to be excellent (0.735) and Bartlett’s test of Sphericity was highly significant (p<0.05). Bartlett’s Sphericity test was effective, as the chi-square value draws significance at five per cent level. The results thus indicated that, the sample taken was appropriate to proceed with a factor analysis procedure. Besides the Bartlett’s Test of Sphericity and the KMO Measure of sampling Adequacy, Communality values of all variables were also observed.

Table 1.1

KMO AND BARTLETT'S TEST

IT & ITES EMPLOYEES’ OPINION TOWARDS THE IMPORTANT PERSPECTIVES OF BALANCED

SCORECARD

Kaiser-Meyer-Olkin Measure of Sampling

Adequacy .735

Bartlett's Test of Sphericity Approx.

Chi-Square 11050.856

DF 2016

Sig .000

Level of Significance: 5 per cent

In order to provide a more parsimonious interpretation of the results, 64-item scale was then Factor analyzed, using the Principal Component method, with Equamax rotation. Factor analysis attempts to identify underlying variables or factors that explain the pattern of correlations within a set of observed variables. Factor analysis is often used in data reduction to identify a small number of factors that explain most of the variance

observed in a much larger number of manifest variables. In the current study, rotation factor analysis is performed to measure the IT & ITES employees’ opinion towards the important perspectives considered in the balanced scorecard of their organization is depicted in Table:1.2 to 1.4.

Five factors extracted together account for 69.207 per cent of the total variance (information contained in the original 64 variables). This is pretty good, because the researchers are able to economize on the number of variables (from 64 researchers have reduced them to five underlying factors), while the data lost only about 30.793 per cent of the information content (69.207 per cent is retained by the five factors extracted out of the 64 original variables). Since the idea of factor analysis is to identify the factors that meaningfully summarize the sets of closely related variables, the rotation phase of the factor analysis attempts to transfer initial matrix into one that is easier to interpret. Equamax rotation method is used to extract meaningful factors.

TABLE 1.2 CUMULATIVE

IT & ITES EMPLOYEES’ OPINION TOWARDS THE IMPORTANT PERSPECTIVES OF BALANCED

SCORECARD

Variables Initial Extraction

Customers’ Perspective

Customer satisfaction in

terms of quality 1.000 .641

On-time delivery 1.000 .538

Customer satisfaction in

terms of service 1.000 .692

Image, reputation, and

brand 1.000 .518

Percentage of sales from new products (as a % of total sales)

1.000 .531

Responsive after-sales

service 1.000 .624

Number of customer

suggestions 1.000 .771

Internal Business Perspective

Unit cost 1.000 .641

Number of defects per

million 1.000 .737

Cycle time 1.000 .682

Wastage and scrap as a

percentage of sales 1.000 .733

Distribution reach 1.000 .675

New product

introduction interval 1.000 .713

Number of training

13

Copyright © 2011-15. Vandana Publications. All Rights Reserved.Stock-out percentage 1.000 .706

Percentage of

components outsourced 1.000 .731

Ratio of number of skilled employees to total employees

1.000 .651

Innovation and Growth Perspective

Market share 1.000 .656

Growth in market share 1.000 .601

Percentage of sales from

new products 1.000 .571

Percentage of sales from

new customers 1.000 .718

Raw material substitutes 1.000 .762 Number of employee

suggestions 1.000 .619

Vendor development 1.000 .608

Reduction in cycle time 1.000 .531

Growth rate in

knowledge assets 1.000 .660

Financial Perspective

Return on investment 1.000 .727

Day’s working capital 1.000 .676

Cash flow return on

investment (CFRO) 1.000 .758

EVA 1.000 .550

Current ratio 1.000 .654

Growth rate in tangible

assets 1.000 .511

Investors/ Shareholders Perspective

EVA 1.000 .582

Market value added

(MVA) 1.000 .677

Cash value added

(CVA) 1.000 .664

Dividend per share 1.000 .576

Real asset value enhancr

(RAVE) 1.000 .653

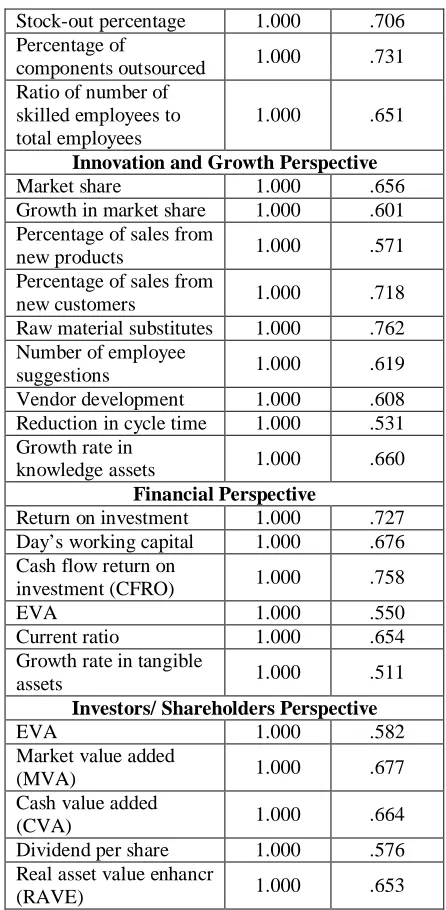

Five factors were identified as being maximum percentage variance accounted. The variable X8, X9, X10, X11, X14, X15, X16, X17, X18, X35, X36 and X37 constitute the factor I and it accounts for 17.381 per cent of the total variance. The variable X38, X39, X40, X43 and X45 constitute the factor II and it accounts for 13.855 per cent of the total variance. The variable X56, X57, X60, X61, X62, X63 and X64 constitute the factor III and it accounts for 12.958 per cent of the total variance. The variable X19, X23, X24, X25, X26 and X27 constitute the factor IV and it accounts for 12.851 per cent of the total variance. The variable X29, X30, X31, X32, X47, X48, X49 and X50 is grouped as factor V and it accounts for 12.161 per cent of the total variance.

TABLE 1.3

IT & ITES EMPLOYEES’ OPINION TOWARDS THE IMPORTANT PERSPECTIVES OF BALANCED

SCORECARD

Variables Initial Extraction

Suppliers’ Perspective

Inbound logistics cost as

a percentage of sales 1.000 .545

Average payment period

to suppliers 1.000 .609

Supplier performance in

terms of time and quality 1.000 .661

Fill rate 1.000 .785

Number of suppliers 1.000 .541

Number of duplicated

functions minimized 1.000 .623

Number of product improvements with supplier partnerships

1.000 .593

Supplier performance in terms of reduction in variance in time and quality

1.000 .535

Inventory carried (in terms of no of days & amount) by supplier

1.000 .791

Employees’ Perspective

Sales per employee 1.000 .559

Employee cost as a

percentage of sales 1.000 .515

Attrition rate 1.000 .525

Value added per

employee 1.000 .515

Competitive Perspective

Market share 1.000 .637

Company cost vis-à-vis

industry average 1.000 .697

New product

development 1.000 .798

Number of brands vis-à-vis total brands in the market

1.000 .593

Availability/development of raw material

substitutes

1.000 .569

Environmental and Social Perspective

Efficiency in material

and energy use 1.000 .566

Water/Air quality

monitoring 1.000 .585

Number of environmental incidents/accidents

1.000 .649

14

Copyright © 2011-15. Vandana Publications. All Rights Reserved.products

Green procurement 1.000 .706

Investment in

environment protection 1.000 .565

Waste produced per quantity of finished product

1.000 .571

Specific pollutant quantities, e.g., Nox, Sox, CO, Pb, CFCs

1.000 .642

Percentage of waste

recycled 1.000 .505

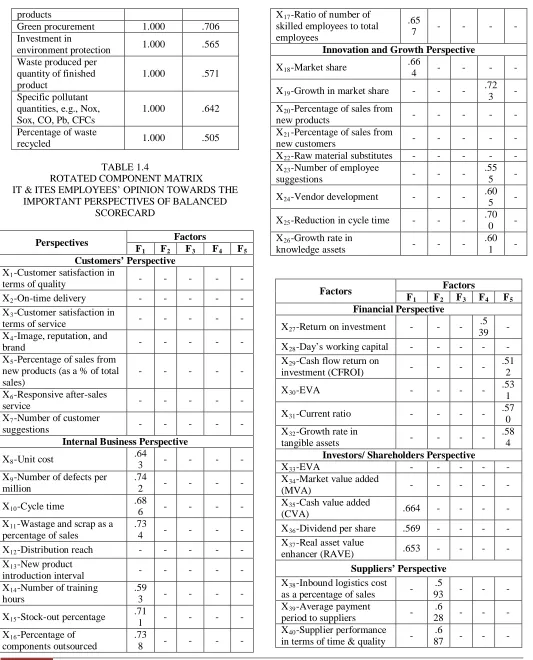

TABLE 1.4

ROTATED COMPONENT MATRIX IT & ITES EMPLOYEES’ OPINION TOWARDS THE

IMPORTANT PERSPECTIVES OF BALANCED SCORECARD

Perspectives Factors

F1 F2 F3 F4 F5

Customers’ Perspective

X1-Customer satisfaction in

terms of quality - - - - -

X2-On-time delivery - - - - -

X3-Customer satisfaction in

terms of service - - - - -

X4-Image, reputation, and

brand - - - - -

X5-Percentage of sales from new products (as a % of total sales)

- - - - -

X6-Responsive after-sales

service - - - - -

X7-Number of customer

suggestions - - - - -

Internal Business Perspective

X8-Unit cost .64

3 - - - -

X9-Number of defects per million

.74

2 - - - -

X10-Cycle time .68

6 - - - -

X11-Wastage and scrap as a percentage of sales

.73

4 - - - -

X12-Distribution reach - - - - -

X13-New product

introduction interval - - - - -

X14-Number of training hours

.59

3 - - - -

X15-Stock-out percentage .71

1 - - - -

X16-Percentage of components outsourced

.73

8 - - - -

X17-Ratio of number of skilled employees to total employees

.65

7 - - - -

Innovation and Growth Perspective

X18-Market share .66

4 - - - -

X19-Growth in market share - - - .72

3 -

X20-Percentage of sales from

new products - - - - -

X21-Percentage of sales from

new customers - - - - -

X22-Raw material substitutes - - - - -

X23-Number of employee

suggestions - - -

.55

5 -

X24-Vendor development - - - .60

5 -

X25-Reduction in cycle time - - - .70

0 -

X26-Growth rate in

knowledge assets - - -

.60

1 -

Factors Factors

F1 F2 F3 F4 F5

Financial Perspective

X27-Return on investment - - - .5

39 -

X28-Day’s working capital - - - - -

X29-Cash flow return on

investment (CFROI) - - - -

.51 2

X30-EVA - - - - .53

1

X31-Current ratio - - - - .57

0 X32-Growth rate in

tangible assets - - - -

.58 4

Investors/ Shareholders Perspective

X33-EVA - - - - -

X34-Market value added

(MVA) - - - - -

X35-Cash value added

(CVA) .664 - - - -

X36-Dividend per share .569 - - - -

X37-Real asset value

enhancer (RAVE) .653 - - - -

Suppliers’ Perspective

X38-Inbound logistics cost as a percentage of sales -

.5

93 - - -

X39-Average payment

period to suppliers -

.6

28 - - -

X40-Supplier performance in terms of time & quality -

.6

15

Copyright © 2011-15. Vandana Publications. All Rights Reserved.X41-Fill rate - - - -

X42-Number of suppliers - - - -

X43-Number of duplicated

functions minimized -

.6

17 - - -

X44-Number of product improvements with supplier partnerships

- - - -

X45-Supplier performance in terms of reduction in variance in time and quality

- .5

57 - - -

X46-Inventory carried (in terms of no of days & amount) by supplier

- - - - -

Employees’ Perspective

X47-Sales per employee - - - - .56

6 X48-Employee cost as a

percentage of sales - - - -

.51 6

X49-Attrition rate - - - - .54

2 X50-Value added per

employee - - - -

.54 4 Factors Factors F F

1 2 F3 F4 F5

Competitive Perspective

X51-Market share - - - - -

X52-Company cost vis-à-vis

industry average - - - - -

X53-New product development - - - - -

X54-Number of brands vis-à-vis

total brands in the market - - - - -

X55-Availability/development of

raw material substitutes - - - - -

Environmental and Social Perspective

X56-Efficiency in material and

energy use - -

.6

43 - -

X57-Water/Air quality monitoring - - .6

47 - -

X58-Number of environmental

incidents/accidents - - - - -

X59-Eco-performance of products - - - - -

X60-Green procurement - - .5

06 - -

X61-Investment in environment

protection - -

.5

82 - -

X62-Waste produced per quantity

of finished product - -

.6

53 - -

X63-Specific pollutant quantities,

e.g., Nox, Sox, CO, Pb, CFCs - - .6

53 - -

X64-Percentage of waste recycled - - .6

09 - -

Eigen value 1 1 . 1 2 4 8. 86 7 8. 29 3 8.2 25 7. 78 3

% of Variance

1 7 . 3 8 1 13 .8 55 12 .9 58 12. 851 12 .1 61 Cumulative 1 7 . 3 8 1 31 .2 36 44 .1 94 57. 046 69 .2 07

Level of Significance: 5 per cent TABLE 1.5

SUMMARY OF ROTATION FACTOR ANALYSIS AND CRONBACH ALPHA

IT & ITES EMPLOYEES’ OPINION TOWARDS THE IMPORTANT PERSPECTIVES OF BALANCED

SCORECARD

Fact ors

Variables included in the factors

Cronbach’s Alpha

F

Unit cost, Number of defects per million, Cycle time, Wastage

and scrap as a percentage of sales, Number of training hours,

Stock-out percentage, Percentage of components outsourced, Ratio of number of

skilled employees to total employees, Market share, Cash

value added (CVA), Dividend per share and Real asset value

enhancer (RAVE).

1 .870

F

Inbound logistics cost as a percentage of sales, Average payment period to suppliers, Supplier performance in terms of

time & quality, Number of duplicated functions minimized

and Supplier performance in terms of reduction in variance in

time and quality.

2 .846

F

Efficiency in material and energy use, Water/Air quality monitoring, Green procurement,

Investment in environment protection, Waste produced per

quantity of finished product, Specific pollutant quantities,

16

Copyright © 2011-15. Vandana Publications. All Rights Reserved.e.g., Nox, Sox, CO, Pb, CFCs and Percentage of waste

recycled.

F

Growth in market share, Number of employee suggestions, Vendor development, Reduction

in cycle time, Growth rate in knowledge assets and Return on

investment.

4 .787

F

Cash flow return on investment (CFROI), EVA, Current ratio, Growth rate in tangible assets, Sales per employee, Employee cost as a percentage of sales, Attrition rate and Value added

per employee.

5 .777

Factor analysis is used to find out the association between IT & ITES workers’ level of awareness towards the functioning of balances Score. The Cronbach’s reliability values (.870, .846, .815, .787 and .777) indicate significant correlation between the IT & ITES employees’ opinion towards the important perspectives, considered in the balanced scorecard of their organization..

V.

CONCLUSION

From the study it is clear that the 64 variables are reduced to five factors namely F1 to F5.

[4] Bindu Nair and DR. AshishPareek (2011), A study of the various performance management systems adopted by select Indian private sector Organizations, Volume No.2, Issue No. 6, ISSN 0976-2183, PP.43-46, June

. for example factor 1 includes Unit cost, Number of defects per million, Cycle time, Wastage and scrap as a percentage of sales, Number of training hours, Stock-out percentage, Percentage of components outsourced, Ratio of number of skilled employees to total employees, Market share, Cash value added (CVA), Dividend per share and Real asset value enhancer (RAVE ) that has the reliability value of 87%. and in the same way remaining factors have been rotated and the t & ites employees’ opinion towards the important perspectives of balanced scorecard has been studied

REFERENCES

[1] Asa Romeo Asa, NavneelShalendra Prasad, Maw MawHtay (2013), Balanced Scorecard: A Paradigm Measure Of Business Strategy and Firm Performance, International Journal of Scientific and Technology Research, Volume .2, IssueNo. 4, ISSN 2277-8616,April. [2] Ayesha Farooq and ZareenHussain (2011), Balanced Scorecard Perspective on Change and Performance: A Study of Selected Indian Companies, Journal of Global Strategic Management, IssueNo.10, PP. 27-38, December. [3] Banker, R.D., H. Chang and M.J. Pizzini, (2004), The Balanced Scorecard: Judgmental effect of performance Measures linked to Strategy, The Accounting Review, PP. 1-23.

[5] Hoque, Z. and James, W (2000),Linking Balanced Scorecard Measures to Size and Market Factors: Impact on Organizational Performance, Journal of Management Accounting Research, Volume No.12,PP. 1-17.

[6] Iqra Abdullah, Iqra Abdullah, TahiraUmair, Yahya Rashid and BasharatNaeem (2013), Developments on Balanced Scorecard: A Historical Review, World Applied Sciences Journal, Volume No.21, Issue No.1, PP.134-141, ISSN 1818-4952