ORIGINAL ARTICLE

The influence factors and international comparison of currency Crises

under abnormal flow of capital

He Yan

School of Finance, Shandong University of Finance and Economics, Jinan, Shandong, China

Abstract:The paper focused on improving the measurement methods about the scale of international capital flow and putting forward the Comprehensive Measuring Method by which to analyze and compare the abnormal flows of international capital of 11 countries in which currency crises occurred by the empirical tests. In addition, the author studied the influence factors and ways of abnormal flow of capital from three aspects, and tried to provide scientific early-warning tool and countermeasures for preventing currency crises.

Keywords:Abnormal flow of international capital; currency crisis; Comprehensive Measuring Method

1. Introduction

With the innovation and development of financial instruments, the time boundaries between long-term and short-term international capital flows are increasingly becoming blurred. Some long-term investment instruments (such as stocks, bonds etc.) can be transformed into good substitutes for short-term investments. But the short-term capital is very vulnerable and easy to turn into speculative capital (people often say “hot money”), so it is difficult to distinguish the boundaries between such short-term capital and “hot money”[1]. In this paper, international short-term capital is

considered as the same as “hot money”, while the abnormal flow of international capital refers to large-scale, unexpected and violent cross-border flow of international short-term capital, including large-scale capital inflow and outflow.

The measurement standard about abnormal flow of international capital is mainly based on the experience standard of International Monetary Fund (IMF), i.e. the ratio that balance of net errors and omissions in the balance of payments accounts for total import and export in the same period and same country should not exceed 5% which is an experience cordon for financial security. If the ratio is more than 5%, it is usually believed that the country could face to abnormal flow of international capital.

The currency crisis is the most frequent financial crisis and almost occurred in 2–3 years on average after 1990. The currency crisis is often understood as a phenomenon that the rate of depreciation of local currency in the short term exceeds the extent that a country can bear. The currency crisis is transitive and may spread to more countries or regions. When a lot of capital fleeing from a country’s market, it will form a run and make the country’s currency face a huge devaluation pressure [2]. Generally believed that a country with the fixed exchange rate regime is liable to cause

currency crises. Although the major currency issuing countries usually carry out the floating exchange rate regime, once these countries break out currency crises, there will be more extensive and profound effects on the worldwide economy and finance[3].

Copyright © 2018 He Yan. doi: 10.18686/fm.v3i2.1075

This is an open-access article distributed under the terms of the Creative Commons Attribution Unported License

(http://creativecommons.org/licenses/by-nc/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

2. Abnormal Flow of Capital under Currency Crises

Since the 1990s, the currency crises have occurred frequently. These crises have caused international financial markets in turmoil and serious impacts on the economy of countries and regions in crises[4]. In this paper, the author

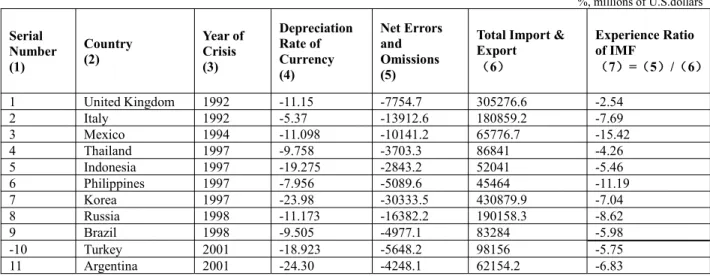

analyzes the depreciation rates of currencies in 11 countries with currency crises by the above experience method of International Monetary Fund (IMF), which can be used to calculate the situations of abnormal flow of capital in crises as shown in Table 1.

%, millions of U.S.dollars

Serial Number (1)

Country (2)

Year of Crisis (3)

Depreciation Rate of Currency (4)

Net Errors and Omissions (5)

Total Import & Export

(6)

Experience Ratio of IMF

(7)=(5)/(6)

1 United Kingdom 1992 -11.15 -7754.7 305276.6 -2.54

2 Italy 1992 -5.37 -13912.6 180859.2 -7.69

3 Mexico 1994 -11.098 -10141.2 65776.7 -15.42

4 Thailand 1997 -9.758 -3703.3 86841 -4.26

5 Indonesia 1997 -19.275 -2843.2 52041 -5.46

6 Philippines 1997 -7.956 -5089.6 45464 -11.19

7 Korea 1997 -23.98 -30333.5 430879.9 -7.04

8 Russia 1998 -11.173 -16382.2 190158.3 -8.62

9 Brazil 1998 -9.505 -4977.1 83284 -5.98

-10 Turkey 2001 -18.923 -5648.2 98156 -5.75

11 Argentina 2001 -24.30 -4248.1 62154.2 -6.83

Note: The column (7) refers to the quarterly average depreciation rate for local currency against the U.S. dollar. According to the experience method of IMF, if the result in the column (7) exceeds 5 per cent, it is believed that the abnormal flow of international capital would appear in the country. Data source: collected according to the IFS and BOPS databases of International Monetary Fund (IMF)

Table 1.Comparison on devaluation rates of currencies in currency crises by experience method of IMF The following conclusions can be drawn from Table 1:

First, the developed countries and developing countries are both possible for producing currency crises. The devaluation rates of local currencies in 11 countries with currency crises were generally between -5% and -25%. The average depreciation rate of three developed countries including the United Kingdom, Italy and South Korea was -13.5%, and the average depreciation rate of the other developing countries was -14%, which was slightly higher than that of the developed countries.

Second, the countries with the fixed exchange rate regime are more likely for currency crisis. For example, Thailand, Indonesia, Philippines, South Korea, Russia, Brazil, Turkey and Argentina implemented the pegged exchange rate regime before the currency crises broke out.

Third, not all countries had obvious abnormal flows of international capital before and during the currency crises and conformed to the experience method of IMF, e.g., the calculation results of the United Kingdom and Thailand in the column (7) do not exceed 5%, which indicates that the experience ratio of IMF could not predict all occurrences of currency crises accurately.

3. A Method for Measuring the Scale of Short-term Capital Flow

At present, the classical methods of estimating the scale of short-term capital flow in the world are as follows: (1) The adjusting method of non-direct investment. This method is the calculation method used by International Monetary Fund and Bank for International Settlements (BIS), and it is also divided into two ways: net error and omission adjustment method and items adjustment method. (2) Direct measurement method. It is a simple and intuitive method of calculation. (3) Indirect measurement method. It is a calculation method used by the World Bank. (4) Cline’s method.

This method was improved by Cline (Cline, 1987) on the basis of calculation method of Morgan Company. The above four methods are to calculate the scale of short-term capital flow from different angles and have different characteristics, but each method has obvious defect by itself, e.g., net error and omission adjustment method of

non-direct investment is easily affected by subjective judgment; direct measurement method underestimates the scale of short-term capital flow and indirect measurement method overestimates it; the calculation results by Cline’s method

often fluctuate greatly.

Considering the advantages and disadvantages of the above four methods, in this paper, the author puts forward a new method hereinafter named Comprehensive Measuring Method to measure the scale of short-term capital flow. This method is further improved based on net error and omission adjustment method of non-direct investment and Cline’s

method. The measuring formula is as follows:

(1)

Where is net short-term capital flow; is balance of capital and financial account; is balance of direct investment; is balance of capital account of banking system and monetary authority; is balance of goods trades;

is balance of current transfer; is balance of foreign direct investment; is net errors and omissions.

The formula (1) is used to calculate the net short-term capital flow of the above-mentioned 11 countries with currency crises as follows in Table 2.

millions of U.S.dollars

Country (1) Balance of Capital and Financi al Account s (2) Balance of Direct Investme nt (3) Balance of Capital Account of Banking System and Monetar y Authorit y (4) 20% of Balance of Goods Trades (5) 40% of Balance of Curren t Transfe r (6) 30% of Balance of Foreign Direct Investme nt (7) 40% of Net Errors and Omission s (8)

Net Short- term Capital Flow

(9)=(2)-(3)-(4)+(5)+(6)+ (7)+(8)

United

Kingdom -24118.1 2582 26037.64 -3437.36 -2789.36 4852.17 -3101.88 -57214.17 Italy -25393.9 1510.1 9589.0 276.4 -1300.24 452.82 -5565.04 -42629.06 Mexico -29826.7 -8156.4 -11156.71 -3252.88 1102.04 2446.92 -4056.48 -14273.99 Thailand -11691 -1459.6 8588.15 -893.34 122.56 668.07 -1481.32 -20403.58 Indonesia -4437.2 -1043.0 -2694.17 1031.0 207.6 320.4 -1137.28 -278.31 Philippine

s -8721.6 -997.0 -1319.93 -1747.6 317.6 322.2 -2035.84 -9548.31 Korea -8496 -661.2 8197.72 4791.82 1028.76 2269.02 -12133.4 -20076.32 Russia -24196 -2066.2 11391.97 2778.08 -233.88 1373.79 -6552.88 -36156.66 Brazil -29092.1 -16766 -6651.88 -948.8 455.2 5254.2 -1990.84 -2904.46 Turkey -7053.2 -2133.0 -6254.61 -3095.2 1885.2 816.6 -2259.28 -1318.27 Argentina -3813.9 -3969.4 -23718.56 3176.24 256.36 1187.25 -1699.24 26794.67

Note: On the column (9) in Table 2, the positive value indicates net short-term capital inflow and negative value indicates net short-term capital outflow.

Data source: collected according to the BOPS and IIP databases of the International Monetary Fund (IMF)

Table 2.Comprehensive measurements of short-term capital flows in 11 countries with currency crises As shown in Table 2, the short-term capital flights were common phenomena occurred in 10 countries with currency crises except Argentina. While the main reasons of currency crisis in Argentina were trade deficits and huge debts of local governments on mature. Therefore, the net short-term capital flow was not a direct cause of the currency

0 1 2 0

20%

140%

230%

340%

SF

0 2

1

0

SF

3 2 1 crisis in Argentina. The following analysis will be around the data of the other 10 countries except Argentina.

4. The Influence Factors of Currency Crises under Abnormal Flow of

Capital

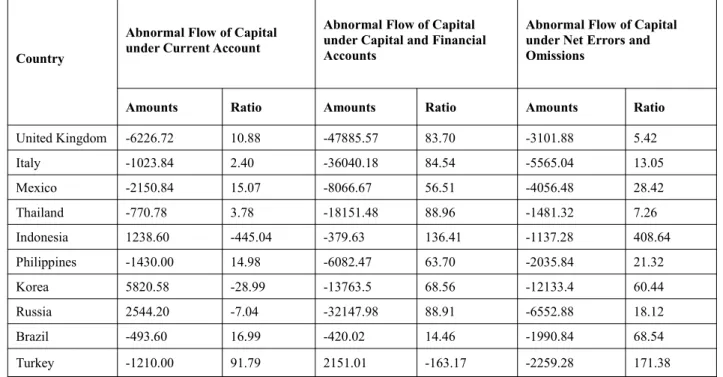

In this paper, the author analyzes the influence factors of 10 countries with large scale short-term capital flights before and during currency crises from the following three aspects: current account, capital and financial accounts, net errors and omissions. The results are shown in Table 3.

millions of U.S.dollars, %

Country

Abnormal Flow of Capital under Current Account

Abnormal Flow of Capital under Capital and Financial Accounts

Abnormal Flow of Capital under Net Errors and Omissions

Amounts Ratio Amounts Ratio Amounts Ratio

United Kingdom -6226.72 10.88 -47885.57 83.70 -3101.88 5.42

Italy -1023.84 2.40 -36040.18 84.54 -5565.04 13.05

Mexico -2150.84 15.07 -8066.67 56.51 -4056.48 28.42

Thailand -770.78 3.78 -18151.48 88.96 -1481.32 7.26

Indonesia 1238.60 -445.04 -379.63 136.41 -1137.28 408.64

Philippines -1430.00 14.98 -6082.47 63.70 -2035.84 21.32

Korea 5820.58 -28.99 -13763.5 68.56 -12133.4 60.44

Russia 2544.20 -7.04 -32147.98 88.91 -6552.88 18.12

Brazil -493.60 16.99 -420.02 14.46 -1990.84 68.54

Turkey -1210.00 91.79 2151.01 -163.17 -2259.28 171.38

Data source: calculated according to Table 2

Table 3.The results of analysis on influence factors of currency crises under abnormal flow of capital

As shown in Table 3, there were net short-term capital outflows under capital and financial accounts in the most countries with currency crises. All of countries with currency crises had net short-term capital outflows under net errors and omissions. The impacts of capital flow under current account were uncertain. There were 7 countries with currency crises which produced net short-term capital outflows except Indonesia, South Korea and Russia, and there were little influences in the most countries.

5. The Ways of Abnormal Flow of Capital under Three Influence Factors

5.1 The ways of abnormal flow of capital under current account

International short-term capital may flow under current account through trade or non-trade channels such as import and export, current transfer, etc. The goods trade is often main channel[5]. Speculators can evade capital regulation by

counterfeiting trade documents, transfer pricing and so on. The short-term capital flows under non-trade channels are mainly through current transfer such as study abroad, overseas remittance, multiple entries and exits from the frontier for purchasing more foreign exchanges from designated banks. Speculators split to purchase and sell foreign exchanges for the purposes of achieving cross-border flows of large amounts of illegal funds and evading customs supervision, which are similar to the moving-family tactics of ants.

5.2 The ways of abnormal flow of capital under capital and financial accounts

The capital and financial accounts in BOP mainly include direct investment, securities investment and other investments, which are main channels of “hot money” flow in opening countries[6]. In addition to foreign direct

investment (FDI) and overseas direct investment (ODI), trade credit, foreign short-term debt, currency swap and offshore banking business also constitute important ways to transfer short-term capital in the world.

5.3 The ways of abnormal flow of capital under net errors and omissions

The abnormal flow of capital under net errors and omissions are usually carried out through underground channels, such as underground banks, mobile banking, currency smuggling, etc.

In short, the ways of short-term capital flow could be legal or illegal, public or hidden[7]. Some short-term capital

flows are not initially based on speculation, such as trade credit. Only for the expected appreciation of forward interest rate or exchange rate of foreign currency, there will be some arbitrage behaviors for the companies or individuals holding foreign currencies as rational economic men. And other short-term capital flows are purely for the purpose of speculation. Using the loopholes in domestic capital account managements, the speculative capital could mix into current account, direct investment, etc., or simply enter the country through illegal channels such as underground banks.

6. Conclusion

Because of high level of economic developments, strong operation ability of financial market, long-time status of major reserve currencies and adopting the floating exchange rate regime, the developed countries are more effective than the developing countries in preventing currency crises. For the developing country, economic development is not balanced, financial market is underdeveloped, financial supervision is backward, the pegged exchange rate regime is usually used. Many developing countries have completely opened capital markets so early that lead to currency crises. The developing countries should fully open capital markets when they are more mature. At the same time, the developing countries should strengthen early warning and real-time monitoring of abnormal inflows of international capital and take measures to prevent currency crises.

Fund Project

Thanks for the support of National Social Science Fund Project of China! The Project Approval No.: 16BGJ004.

Reference

1. Prasad E, Rajan R. A pragmatic approach to capital account liberalization. Journal of Economic Perspectives 2008; 22(3): 149–172.

2. Frost J, Saiki A. Early warning for currency crises: What is the role of financial openness? Review of International Economics 2014; 22(4): 722–743.

3. Han Z. Rational expectations, capital inflow and currency crisis: Based on the macro effect analysis of capital flows. Studies of International Finance 2008; 8: 44–50.

4. Pop N, Valeriu IF. Crisis, globalization, global currency. Procedia Economics and Finance 2015;22: 479–484. 5. Haidar JI. Currency crisis transmission through international trade. Economic Modelling, 2012;29(2): 151–157. 6. Xiao W, Yin Z, Chen Y. Capital account liberalization, capital flow and financial stability: Based on macro

prudential perspective. World Economy Study 2016; 1: 28–38.

7. Li Z, Nie Z, Zheng Y. The formation, evolution and early warning of currency crisis in emerging market countries: Empirical research based on binary classification model. Journal of Financial Research 2012;12: 107–121.