Munich Personal RePEc Archive

Saving behavior in low- and

middle-income developing countries

Reinhart, Carmen and Ogaki, Masao and Ostry, Jonathan

University of Maryland, College Park, Department of Economics

January 1995

Online at

https://mpra.ub.uni-muenchen.de/13757/

IMF

WORKINGPAPER

O 1995 International Monetary Fund

Thii is a Wking Paper and the authw(s) wMJd &me

any commEntJ on the p a n t wxc. Citatbm Jhwkl mkr a Working Pqxr 06 he International M o n e w Fund. mm cioning the aufhw(s), and the date of isauanoe. 'lhc &M

ex+ arc those of the author(s) and do not n c u s a d y

rc-nt those of the Fund.

WP/95/3

INTERNATIONAL MONETARY FIMD

Research

DepartmentSaving Behavior in Low- and

Middle-Income

Developing

Countries:

A

ConmarisanPrepared

by

Masao Ogaki, JonathanD.

Ostry, andCarmen

M.

Reinhartl

J

Author

f

zedfor

distribution

by

Peter

Wickham

January 1995Abstract

The impact

o f

changesin

real interest rates on saving and growth isa central issue

in

development economics.According

toone familiar view,

afinancial liberalization

programwhich

increasesreal

interest ratesshould

encourage saving, therebyboosting

investment andgrowth.

While

suchliberalizations

have

indeed typically succeededin raising

realinterest rates,

their

impacton

privatesaving

has

been mixed.This

paper uses macroeconomic data

for

a sampleof

countrieswith

diverseincome levels

t o estimate a modelin which

the intsrtemparal elasticity of substitution varieswith

the level of wealth. The estimated parametersare

then

used ta calculate,in

the contextof

a simple endogenous growth model, the responsivenessof

saving to real interest x a t e changes forcountries

atdiffering

stagesof development.

3EL

Class1

f

icationNumbers:

E21,F41,

F 4 3 , 011, 016, 057I

J

Ogaki: Departmentof

Economics,Ohlo

S t a t eUniversity; Ostry

andReinhart: Research Department, International Monetary

Fund.

Any viewsexpxessed

in

this papex are those of the authors and should not beattributed to the institutions

with

which

theyare

affiliated.

The

authorswish

tothank

seminar participants atthe

IMF andOhio

StateUniversity,

aswell

as Sergio Rebelo, Michael Sarel,Miguel

Savastano, andPeter

Wickham

for

helpful comments and suggestions, and Jared Romeyf o x

excellent

research

-

Ti

-

Contents

Summary

I .

Introduction31. S t y l i z e d Facts

111. Analytical Framework

IT.

Estimation Strategy andEmpirical Results

1.

Data issues2. Empirical methodology and estimation results

a. The

f i r s t

step: estimating the intratemporale l a s t i c i t y

of

substitutionb. The second s t e p : estimating the intertemporal

parameters

V . Saving and the Rate

of

Interest1. A simple model of endogenous growth 2 . Results

V I

.

Canclus ionsText

Tables1.

Food as aPercent of

T o t a lPersonal Expenditure for

S e l e c t a d Countries, 19902 . Personal Saving Rates for S e l e c t e d Countries

3 . Canonical Cointegrating Regression Results

4 . The intertemporal Parameters: Generalized Method of

Moments Results

5.

The

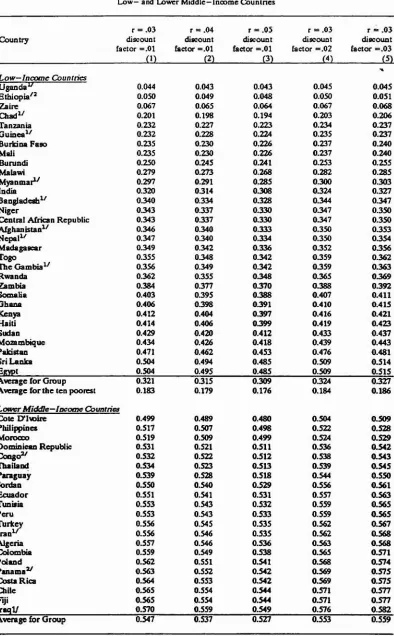

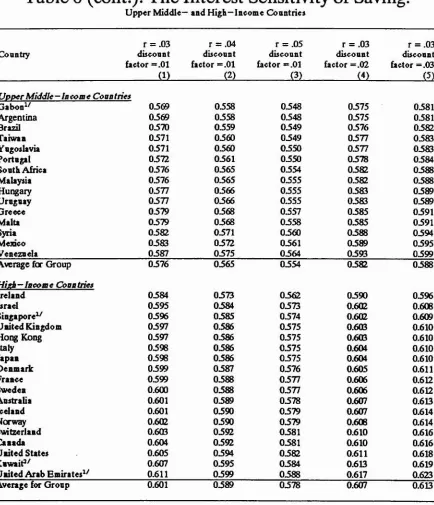

Intertemporal Elasticity. of Substitution: Low-and L o w e r Middle-fncoms Countries

6.

The Interest Sensitivity of Saving: Low- andLower

Middle-Income Countries

Chart

1.

The

Intertemporal Elasticity ofSubstitution

u

iii

The

responsiveness of- saving to changesin

seal i n t e r e s t rates is akey

parameterin the

evaluation of the effectsof

anumber o f

exogenousand

policy-induced shocks in

developing countries. Financial sector reforms havetypically

resulted in increases inreal

interest xatesin

developing countries, but the response of saving--andthe

e f f e c t s on investment andgrowth--have been much less clear-cut.

In

addition, the effects on the externalcurrent

account balance of fiscal policychanges

that alterdomestic interest rates depend

on

the

responsiveness ofprivate

saving to movements in r e a l rates of return.Finally,

temporary tenasof

trade shocksor

trade liberalizatians that are not credible contribute to movements inccmsumption rates of interest (which measure the true cost of consuming today relative to consuming tomorrow)

in

developing countries ,the

effectsof

which on

the

current account dependcritically on

the

e l a s t i c i t yof

saving w i t h respect: to thereal

i n t e r e s t rate.Empirical evidence suggests t h a t the intertemporal elasticEty

of

substitution in consumption

(on

which the interest rate elasticity of saving depends) variesconsiderably

acrossdeveloping

countries.This

paperargues

that a main reason for t h i s variation

may

be

acountry's

levelof

development. Specifically, because

of

therole of

subsistence consumptionin

household expenditure, low-income developing countries w i l l typicallye x h i b i t a n e g l i g i b l e response

of

saving to movementsin

real interest r a t e s . As the p e r c a p i t a income level r i s e s , the fraction of the budget left aftersubsistence needs have been met increases. As only this fraction of the budget is sensitive to movements

in raal

interest rates, the model implies anonlinear

relationship between the Intertemporal e l a s t i c i t yof

substitutionand the

level

of development.The

interest rate e l a s t i c i t yof

saving shouldtherefore

be

much higherin middle-income

than

in

low-income countries(where it will be close to

zero),

but

it w i l lbe only slightly

higherin

high-income

than

in

middle-income

countries, where subsistence p l a y s littlerole

in

the expenditure patterns of most households.These notions f i n d support in the data. Using macroeconomic data from

a sample of countries w i t h diverse income levels, the paper concludes that a

model in

trhich the

intertemporal e l a s t i c i t y of substitutionis an

increasing

function

of

the

gap between permanentincome

andthe

subsistence consumpttonlevel cannot be rejected. The model implies v e r y

different

responsesof

private savfng to (exogenous and policy-induced) raal interest rate

shocks,

I.

I n t r o d u c t i o nThe

impact of changesin

real i n t e r e s t rates on saving, investment,and economic growth, is a central issue

in

development economics. According ro onefamiliar

view (see, for example, McKimon (1973) andShaw (1973)),

an

increase in real interest rates in developing countriesshould

encourage

saving and expand the supplyof

creditavailable

todomestic investors, thereby enabling the economy to grow more quickly.

Indeed, a

number

of liberalization p'rograms supported by the international financial institutions over the years havehad

as their explicit objectiveto increase i n t e r e s t rates from levels t h a t in many cases

were

substantially negativein

weal terms.While

increasesin real

interest rateshave

oftenbeen

the outcome o fsuch

liberalization

e p i s o d e s (see,for

example,Calbis (1993)), their impact

on

domestic saving and investmenthas

beenunclear. L/

There

is l i t t l e consensusin

t h e empirical literatureon

the

interaction between saving and the real rate of interest ( s e e , for

instance, Savastano

(1994)

andSchmidt-Hebbel,

e t al. (1992) for areview

a £ this literature). Some researchers have been unable to d e t e c t much of

an effect of changes in real interest rates on domestic saving in

developing counrries

.

For example, Giovannini ( 1 9 8 5 ) finds that inonly

five

of the eighteendeveloping

countriesin

h i s sample are consumptionand saving sensitive to changes

in

the real i n t e r e s t rate.He

cancludest h a t f o r

the

majority of cases,"the

responseof

consumption growth to t h ereal rate of

i n t e r e s t is insignificantly differentfrom

zeroh' [page215)

and t h a tone

should therefore expect " n e g l i g i b l e responses of aggregatesaving to the real rate of interest [in developing countries]" (page

197).

Rossi (1988) a l s o finds t h a t "increasesin

the real r a t eof

return are n o tlikely to

e l i c i t substantial increasesin

savtngs, especiallyin

low-incomedeveloping countries" (page 104).

In

a model with asingle

consumptiongood, O s t r y and Reinhart ( 1 9 9 2 ) confirm these

findings;

but when a disaggregated commodity struc'turc that allows for traded and nontradedgoods is assumed, these authors f i n d higher and statistically significant

estimates of t h e intertemporal e l a s t i c i t y of substitution. However,

regional differences emerge, with

Asian

countries showing a greaterresponsiveness to real interest rate changes. 2J

The finding

of

a zero or near-zero interest rase sensitivity of savingin a

number

of developing countries has led researchers to consider a number of alternativehypotheses

that could help to explain t h i sresult.

One suchhypothesis is that consumption

in

developing eauntriesmay

bemore

r e l a t e d to subsistence consideratians--particularlyin

the case of low-income4/

For

a v i e wrunning

contrary

t othe

McKinnon-Shaw hypothesis,

seeBuffie

(1982)

and van Wijnbergen(1983).

For an analysis of the Uruguayanexperience with

financial

liberalization, see de Melo and Tybout (1986).2/

Ostry andReinhart 11992)

attributed thesedifferences

to t h e presencecountries--than to intertemporal consumption smoothing.

J

I

If

householdsmust:

first achieve a subsistence consumption level, letting intertemporalconsiderations g u i d e their decisions

only

f o rthat

p o r t i o n of their budgetleft

after subsistence has been satisfied,then

the intertemporal elasticity of substitution and the interest-rate sensitivity of private saving w i l l beclose to zero for countries at or near subsistence consumption Levels, and

rising

thereafter.A second reason why the intertemporal elasticity of substitution

may

be smaller

for

low-income countries concerns the relativeshare

of

n e c e s s i t i e s

in

t h e budgetsof

relatively poorhouseholds. If

necessities(for

example, food) are less substitutablethrough

time than other goods,then the intertemporal e l a s t i c i t y of substitution will be lower

for

households with a larger proportion of necessities in their budgets than for householdswhere such

goods areless

important. The implication wouldbe

that

for

relatively poor countrieswhere

budget shares of food arerelatively

high, the interest-rate e l a s t i c i t y ofsaving

wouldbe

relativelylow. 2J

It is indeed noteworthy that food consumption accounts for a markedly

lower share of total expenditure

in

high incomathan in low income

countries. As

shown in

Table 1,

food consumption accounts f o r less thantwenty percent of t o t a l expenditure in most industrial countries and for only 8 percent of t o t a l consumption in the United S t a t e s .

For

middle-incomecountries such as Mexico and Thailand,

the

share is often 3 0 - 4 0 percent,while for t h e poorer countries the share of food approaches 60-70 percent ( s e e Mitchell and lngco (1993)).

Empirical

supportfor

thesehypotheses

isfound

inAtkeson

andOgaki

(1993).

Specifically, using a panel of data on Indian households,they find

t h a t the intertemporal e l a s t i c t t y of substitution of the richestsix households in their data s e t is approximately 1.6 times that of the

poorest six households.

Thus,

fromtheir

results, the e f f e c t so f

the

l e v e lof

wealthon

theintertemporal

elasticityof

substitution would indeedappear to be economically significant.

h/ For

models t h a t stressthe

role played by

subsistence considerationsin

eonsumption/saving d e c i s i a n s , see Rebelo (1992) and Easterly (1994).On the b a s i s of a similar argument, Rebelo (3992) argues that

financial

liberalization in

low-income developing countries is unlikely toproduce large e f f e c t s

on

saving and economic growth. F o r a discussion ofthe

effectsof financial

market deregulationi n

developing countries, seeGalbis (1993). For an analysis that highlights

stylized

facts concerningthe differences in saving behavior between l o w - and middle-income developing countries, see two recent World Bank

volumes

(World Bank (1993, 1 9 9 4 ) ) ,dealing respectively w i t h the performance

of

the

economiesof

East Asia andTable 1.

Food

as

a

Percent of Total Personal

Expenditure for Selected Countries

Country

Percent

Law-Income Countntnes

HondurasIndia

Sierra

Leone

SriLanka

Sudan

Average

for

Qrmp

Lower

Middle-Inmmc

Caunr'es

Colombia

Ecuador

Fiji Jamaim Jordan Philippints Thailand

Average for Group

Up- Middle-

I n m e

Coun

Greece

Malaysia

Mexico

South

Amca

Venezuela

Average

for

aroup

High

-Income

Caunmtnes AustraliaCanada

Belgium

Sweden

United

Kingdom

United State Average

for Orwp

Note:

For chsifiation

of

cconomfm

byIncome

I&

see

World

Bank

(1 W b )There a r e , however, additional reasons

why

saving may be l e s sresponsive to changes

in

real interest rates in low-income than in middle-incame countries. Rossi (19881, for example, argued that low-income

developing countries are characterized

by

pervasiveliquidity

constraintswhich

imply

that consumption growthin

such countries is morelikely

tof o l l o w

income

growth than changesin

expected ratesof

return.J

l

Theempirical evidence appears t o point to the presence of liquidity

constraints in many developing countries; however, Haque and Montiel (1989) highlight t h a t the severity of these constraints varies considerably across

countries.

More

recently, Vaidyanathan (1993) showedthat the

incidence of liquidity constraints among households i sinversely

r e l a t e d t o the degree ofeconomic development

which

wouldimply--following

Rossi (1988)--that savingin poorer countries should be less responsive to interest rate changes. 2J

Lastly,

i t could beargued

that failure t o d e t e c t a systematicrelationship bemeen

saving and

real interest rates across countriesand across time may a l s o be due to considerable variation in

the

economic signzficance and information content ofthe

real rates n f return themselves.Lack of sophistication and depth in domestic financial markets or direct

regulation may result

in

nominal interest rates that do not adequately reflect expectations about the underlying economic fundamentals. This problem m a y be particularly severe for some o f the poorer countries.In

addition, lack of information

on

inflation expectations is a problem that, as the literature on the peso problem has shown, may be especially relevantfor

high-inflation

countries and/or episodes,While a number of hypotheses have been put forward to suggest t h a t

saving behavior in developing countries is a f f e c t e d by the Level of

development, there

has

so far been little systematic empirical investigationof

this

issue atthe

macroeconomic level i n the l i t e r a t u r e .Yet

from apolicy perspective, the issue is of

central

importance, since for example,the e f f e c t s on--inter

alia

investment and growth--of a number of p o l t c yactions frequently undertaken by developing countries--including financial

liberalizarion, reducing capital controls, and the transmission of fiscal

and commercial policy

changes

to thecurrent

account--willall be governed

l

J

Deaton ( 1 9 8 9 )has

a l s o emphasized the importance of liquidityconstraints in explaining consumption/saving behavior in developing

countries.

2

J Vaidyanathan (1993)

also

foundthat

financial liberalization

in

developing

countries reducedthe

severity of borrowing constraints.Although no direct t e s t s were undertaken,

the

implicationwould be

that

financial liberalization, by

reducingthe

fractionof

households f o rwhich

liquidity constraints are

binding,

should increase the interest-ratesensitivity

of

privatesaving.

For a direct test of t h i s hypothesis, seeto some degree by t h e responsiveness o f saving to i n t e r e s t rate

changes.

l

J

With this in mind, the purpose of this paper is to q u a n t i f y empirically

t h e response of c o n s ~ p t i o n / s a v i n g t o

changes in

thereal

rate of i n t e r e s t .W e proceed

in t w o

s t e p s . First, we use macraecanomic data f o r a sample ofcountries with diverse income levels to estimate a

model

t h a tallows

theintertemporal elasticity of substitution to vary with the level of wealth. W e then use

the

estimated parametexs to calculate,in

the context of asimple endogenous

growth

model, t h e elasticityof saving

with

respect to changes in the real rate of interest.The remainder of the paper is organized as follows. Section

I1

presents some s t y l i z e d facts on saving behavior and income levels and

focuses

on

the differences between low- and middle-income developing countries. Section 111 describesthe

analytical

framework,while

SectionIV

discusses t h eempirical

methodology and summarizes theestimation results. The response of saving to changes

in

real interest rates is examinedin

the context of a simphe endogenous growth model in Section V. The implications for policy and future research are taken upin

the

final

section.11. Stylized Facts

A model, such as the one developed

in

this paper,

t h a t emphasizes the role of subsistence consumption, has t w o main p r e d i c t i o n s about savingbehavior, First, saving rates should increase with the level

of

wealth atthe

initial stages of development, with the largest increasesin

the savingI;/

In addition to policy-induced shocks, the transmission of a temporaryterms of trade disturbance, through its effect on the consumption r a t e of

i n t e r e s t , depends

crucially on

the sensitivity ofsaving to

intertemporal relative prices (see, f o r example, Svensson andRazin

(1983)

andOstry

(1988)).

In

the area of commercial policies, noncredibleliberalizarions will also generate changes in consumption rates of

i n t e r e s t as

households

may view the reductionin

import p r i c e s (associated w i t h tariff reductions) as a temporary phenomenon ( s e e ,for

axample,Razin

and Svensson (19831, Calvo (1987, 1988,

1989)'

Edwards and O s t r y ( 1 9 9 0 ) and O s t r y (1991a,b)). The extent to which such noncredible liberalizations willinduce a consumptian boom (and a current account deterioration) therefore depends

on

t h e intertemporal e l a s t i c i t y of substitution in consumption.The

finding that:this

parameteris

Lowin

anumber of

countriesmay

help torationalize the empirical

findings

of Ostry and Rose(1992)

that

tariffshave little systematic effects an saving and current account behavior.

Finally,

the transmission of f i s c a l p o l i c y changes (which engender movementsin domestic interest rates) to

the

current accountwill be governed

in partby

the

responsiveness of private saving to real Interest rates ( s e e , f o rrate occurring as a country moves f r o m

low-

to middle-income levels. lJ

Second,

saving should become more responsive t o changesin

real

interest rates as countries become r i c h e r . The first prediction follows d i r e c t l yfrom

tlfie role of subsistence consumptionin t h e

low-income developing countries, andthe

fact that the share of subsistencein

t o t a lconsumption declines

with

income.2/

The second p r e d i c t i o n may a l s obe r e l a t e d to subsistence considerations, since intertemporal incentives should

only

a f f e c tthat

portion a £ the budget left over after subsistencehas been achieved, t h a t i s , discretionary income.

With regard to saving rates, a model t h a t stresses the role of

liquidity constraints offers a different p r e d i c t i o n ;

if

poor consumers c a m o r borrow but face an uncertainincome

stream,the

demand f o rprecautionary saving rises ( s e e , f o r instance, Deaton (1989)).

Hence, it may be the poorest lfquidity-constrained consumers t h a t save

more. However, as w i t h

the

subsistence model, the responsiveness ofsaving to changes in interest rates rises with the level of wealth as

liquidity constraints become less binding.

Among countries in various income groups,

the

patterns of savingrates that emerge are broadly consistent w i t h

the

predictions of thesubsistence model. As Table 2

highlights

for selected countries, private saving is, on average, considerably lowerfor

the

poorestdeveloping countries,

where

the saving rate is about onehalf

t h a t ofthe high-income group.

4J

Xn f a c t , such differences also appear withinregions. According to the World Bank {1994a), median gross domestic saving as a percentage of GDP

(1987-91

average) was 5.6 percent forthe low income African countries and 19.0 percent f o r the middle-income African countries (the average was 7.7 percent).

As predicted, t h e

relationship

between thelevel of

income and thesaving r a t e appears to be nonlinear

for

the countries in our sample ( s e eRebelo (1992)); the largest increases

in

the saving rates occur in thetransition from low- to lower middle-income, where the average personal

saving rate rises by 5.5 percent (Table 2 ) . The average f o r the upper middle-income countries is s t i l l 2 . 8 percent above t h a t of the lower

middle-income group,

but

there appears to be relatively littledifference

(0.5

percent) betweenthe

average saving ratesin

the

hfgh-income and upper middle-income countries

in our

sample.- -.

1/

In fact, in such models ( s e e Rebelo (1992) and Sarel (1994)), t h esavLng rate need n o t increase

in

the transition from middle tohigh

incomelevels.

2J S e e , f o r example Barro (1990) and Rebelo (1992).

This

precautionary motive, without explicitly modelling l i q u i d i t yconstraints, is empirically investigated

in

Ghosh and O s t r y(1994).

Table

2.

Personal Saving

Rates

for

Selected Countries

(lW-I1)9J a * e n g n . ~ ~ e ~ n ~ d )

-

GNPpr&&Mdult b M d % # a 8ia 1915

s

19CO-:7 -#! P-tdGDPT V i 6395 -Ilf

Ehrkwa R& W6 111

8882 135

h h d r g m r 9168 4 3

TOP %SF9 14.0

! h d i a 1144.4 62

Ghana 1161.1 6.1

H& 1210.4 4 5

1 197.9 1 8 2

S w m h 1311.0 8.1

N- l W J 95

P 8 k a u 1m 230

Lm5*

1m9 753m.o 143

S r i h h 2156.1 1 98

Rdik m79 322

-8- 3576 127

-

217RI 1111El* ZZMD 15.0

p b i i p p e 8 ' 2- 162

~d

24724 209M i mReplib B11.1 118

Tbrihd m1.4 pa

3LI&tl 146

3773.4 145

Peru 3B65 244

k*

3531 6 21.43%25

m

U t h 4lM.O I 2 7

PdradY 43W.6 2&S

CWe 4ST7F87d 1 2 8

Still, there appear to be sharp differences in savings rates t h a t

cannot be accounted

for

by the

subsistence model.For

example,saving

rates in L a t i n

America

are

well below

those observedin many

Asiancountries, despite similar income levels.

J

l

As pointed out in WarldBank

(19931, gross domestic saving as a percentage of GDP was n e a r l y 40 percent f o x the high-performing (middle-income) Asian economiesin

1990;

it is argued that these relativelyhigh

saving rates werean

engine of growth in many of these countries, since t h e y financed higher rates of investment as well.The role o f

real

interest ratesin saving

behavior ismore

difficultt o gauge. One

problem--which

is particularly importantin Africa,

isthat

financial

markets remain t h i n and governments s e t interest s a t e s , frequently at non-market levels. As pointed o u tin

a recent WorldBank

study on Africa (World Bank ( 1 9 9 4 a ) ) , "most countries

[in Africa] have

few banks, and

...

there is l i t t l e scope for 'true' market-determination o f interest rates" (page114).

This

feature of credit marketsin low-

income countries may i t s e l f make saving less responsive to interest rates

Nevertheless, there is some evidence t h a t financial savings increased

as a resulr o f the increase in real interest rates associated with

l i b e r a l i z a t i o n of financial markets, b o t h in Africa and elsewhere among

developing countries.

For

example, among the Asian countries, the increasein

real interest rates in Taiwan Province ofChina

in1949

contributed to a sharp increasein

savings. Similar results were achievedby

Indonesia and Korea, and more recently, by Argentina,Chile,

Mexico, and Pakistan(see Uorld Bank (1993) and the references therein). There is also some

evidence t h a t r e f o r m programs

in

Africa have succeededin

raising domesticsavings, For example, as documented in World Bank (1994a), median gross

domestic saving

climbed

3 . 3 percentage p o i n t sfor

the six African countriesw i t h a large improvement in macroeconomic p o l i c i e s (whlch consisted

of

f i v e m a i nindicators,

oneof which

was interestrate

policy),

compared to ad e c l i n e

of

3 . 3 percentage pointsfor

countriesw i t h

p o l i c y deterioration.In

general,moving

real fnterestrates

fromsharply

negative to mildlypositive

levels

seems to be a posicive factorin

mobilizing domesticsavings, although there is no particular evidence

that

the effectivenessof such policies rises with the level of development, as

the

subsistencemodel would suggest.

An

investigationof this

issue is undertakenin

thefollowing three sections.

U

Income distribution within a country is often argued to exertan

independent influence an saving behavior, but w e are unaware of any

111.

Analvtical

FrameworkWe begin by describing the maximization problem faced by a

representative household in a given country. Since our ultimate purpose is to examine cross-country differences in saving behavior, we do n o t

assume that representative hauseholds

in

different countries haveidentical preferences. As in Ostry

and

Reinhaxt (19921, we adopt a two-goodframework that distinguishes between traded and nontraded goods. As argued

in

that

paper, it is important to estimate the intertemporal elasticity ofsubsritution

with

a two-good model in order to avoid biaswhen

the relativep r i c e

of

traded and nontraded goods (thereal

exchange rate) variesconsiderably through t i m e , as we will discuss later. W e allow

for

cross- country variation in both the intratemporal e l a s t i c i t y of substitutionbetween traded and nontraded goods and t h e intertemporal elasticity of

substitution.

The

assumptionis

that

the latter varies systematically withthe level

of

wealth, We beginby

describing,in

equations(1)-(7)

below, the optimization problem at the n a t i o n a l level.Consider

then

an economy withan infinitely-lived

representativehousehold whose objective is to choose a c o n s ~ t i o n stream t h a t maximizes:

subject t a the series

of

budget constraints:and the transversality condition:

where Q is the expectations operacor conditional on information available

at time 0 ; Bt denotes the real level of debt carried from period t to period

t+l w i t h Bdl given; (

1 ) -

=r

is thereal

interest rate (in termsof the numeraire)

on

the

debt soR;

is the associated world real discountfactor; m (n) denotes consumption of importables (nontradables) and p (q)

denoted the r e l a t i v e p r i c e of

m

(n)

in termsof

the numeraire;p

is thesubjective discount factor; and E

(PI

denotes the intratemporal(intertemporal) elasticity of substitution.

I

J

An intratemporalelasticity oaf subsritution greater (less) t h a n one implies gross

substitutability ( c o m p l e m e n t a r i q ) between traded and nontraded goods;

a value of

unity

corresponds to the logarithmic utility case. Theintertemporal elasticity

of

substitution reflectsthe

sensitivityof

consumption (and therefore saving) t o changes in intertemporal p r i c e s ( i . e . the consumption rates of i n t e r e s t ) ,

with

higher values indicatinggreater sensitivity.

The problem of the representative

consumer in

agiven

country is to choosean

optimal sequenceI%,

r+, Btlthat

maximizes(1)

subject to ( 2 )and ( 3 ) . The first order necessary conditions

for

an optimum are:Equation (4) is the intertemporal

Euler

equation a s s o c i a t e d with importables consumptionin

two consecutive p e r i o d s ; it states that the marginal utilitycost

of

givfng upone unit of

at s h e t should be equated to the expected u t i l i t y gain from consuming one more unit of m at t+l. Equation ( 5 ) is theanalogous condition relating the marginal rate of substitution between

consumption

of

goodn

at t and t+l torhe relevant

intertemporalrelative

p r i c e . Finally, equation ( 6 ) is the nonstochastic fLrst order conditionequating

the

intratemporalmarginal

rateof

substitution betweenimportables and nontradables to the corresponding relative price ratio.

It can be verified t h a t equations (4)-(6) are net kdependent.

Specifically,

combining equation ( 6 ) with either of the t w oremaining

equations y i e l d sthe

third.

Therefore, given

that

the nonstochasticfirst

order condition holds, equations ( 4 ) and (5) do not provideindependent restrictions on the evolution a£ consumption through time.

l

J

Following the discussionin

Section 11, we allow f o r cross-countryThe main difference between

the

model

described above and standardEuler-equation models t h a t

have

been applied previously to developingcountries (far example, Giovannini (1985) and Rossi (1988)) relates to the goods structure.

In

the above model, we allow for consumption oft r a d a b l e s and nontradables s i n c e the latter appear to account for a large

fraction of the consumption

basket

in

many developing countries. Moreover,imposing a one good structure can seriously bias the resulting estimates of preference parameters,

If

the real exchange rate (the relative p r i c eof traded and nontraded goods) varies over time, as is the case

in

moscdeveloped and developing countries, aggregate consumption

will

respond tothose price changes. This is because a change in the real exchange rate

alters the consumption rate of interest. As

such channels

are

ignored

in

a one-good structure, the empirical results from such modelsmay

beb i a s e d .

J

l

For example,the

finding

that

intertemposal elasticitiesof

substitution are insignificantly different

from zero in

t h e majority of developing countries w a s found by O s t r y and Reinhart (1992) not to berobust to a relaxation of

the

one-good assumption.Given time series d a t a on importables and nontradables consumption,

and on interest rates,

and

import, expast, and nontradables p r i c e s , it isp o s s i b l e to estimate the system consisting o f ( 4 ) - ( 6 ) and recover the main parameters o f interest.

Since

(6) must

holdidentically

(in the

absenceof measurement e r r o r ) , and since (&) and ( 5 ) are not independent given t h a t (6) h o l d s , we can eliminate ( 6 )

or

(5) from the estimation. Therestrictions on the j o i n t behavior of consumption of importables and

nontradables, the terms

of

trade, andthe

relevant rate of return, i m p l i e dby the maximization of the expected utility function given by (1) s u b j e c t to the constraints given in ( 2 ) and

( 3 1 ,

are summarized in equation (4).In addition, given the assumption

of

rational expectations, we can useequation (&) to define the disturbance :

where

q

mustbe

uncorrelatedwith

any

variable that isin

the informationset

of

agents at time t.With

t h e optimization problem of a representative householdin

a givencountry

fully

described, it remains to be s p e c i f i e dhow

intertemporalparameters governing saving behavior vary systematically across countries.

In what follows, we rake a particularly simple approach motivated

by

aStone-Geary

preference specification (as described, f o r example,by

Rebelo (1992)). We adopt a specification in which the intertemposall

e l a s t i c i t y

of

substitution i san

increasing function ofthe

gap between permanent income and the subsistence level of consumption,viz:

where pi denotes

the

intertemporal elasticity of substitution in country i ; y ' is a measure of permanent income in countryi;

and -y is a constant whichP

r e f l e c t s subsistence consumption.

Clearly,

equation ( 8 ) is s i m i l a r to theStone-Geary preference s p e c i f i c a t i o n but w i t h permanent income replacing consumption. Conceptually, we focus on income rather than consumption

in

order to make transparent the connection between the intertemporale l a s t i c i t y of substitution and the level of development (i.e., income per

c a p i t a ) . Equation (8) shows t h a t the interest-rate s e n s i t i v i q of aggregate

consumption ( a s well as the level

of

saving i t s e l f ) w i l l be lower asthe

ratio, 7/y;1, approaches unity and wealth is only sufficient to support a subsistence level

of

consumption.fV.

Estimation Strateev and EmiricalResults

1.

Data issuesThe parameters of the representative

household's

utility functionoutlined

in

t h e previous section are estimated using annual time-series data f o r thirteen countries.The

law-income countries in the sample are:Egypt, Ghana, India, Pakistan, and S r i

Lanka;

the low-middle incomecountries consist of Colombia, Costa Rica, C b t e drIvoire, Morocco, and the

Philippines;

three upper-middle-income countries are also included inthe

analysis:

Brazil,

Korea, and Mexico. Data coverage for eachcountry

beginsin

1968 and ends anywhere between 1983 and 1992.As equations ( 7 ) and ( 8 ) h i g h l i g h t , estimation of the intertemporal and intratemporal elasticities of substitution requires data on household

consumption of traded and nontraded goods,

the

terms of trade, and permanent income or wealth.While

time series on the terms o f trade arereadily

available,

consumption data are generally not disaggregated intotraded and nontraded goods and estimates

of

wealth are scarce. Withregard to

the

disaggregation of consumption, the methodology applied isd e s c r i b e d in detail in Ostry and Reinhart (1992). B a s i c a l l y , we assume

that

the

nontraded goods s e c t o r of the economy consists of p u b l i c andprivate services while traded goods production emanates f r o m the

agriculture,

mining and industrial s e c t o r s . Consumption of importablescan

then

be

constructed using t h e supply-side data and dataen

e x p o r t sand i m p o s t s

of

consumer goods. Consumption of nontraded goods arecalculated residually as total private consumption less consumption of

importables. The relevant price deflators f o r

the

consumption of tradedand nontraded goods are price indices

for

i p o r t s and services,the absence of these, a

money

market ratewas

employed.Finally,

as a proxy f o r permanent income, an averageof

real income per equivalent adultfor the period 1980-87 w a s used.

U

2 . E m ~ i r i c a l methodolow and estimation results

In this subsection, w e apply Cooley and Ogaki's

(1991)

two-step procedure to obtain estimates forthe

intratemporal e l a s t i c i t y ofsubstitution between t r a d e d and nontxaded goods and f o r the intertemporal

elasticity of substitution. A similar procedure, which was applied

independently

by Ostry

and Reinhart(19921,

uses a cointegration approachto obtain first-stage estimates of the intratemporal parameter

and

Hansen and Singleton's ( 1 9 8 2 )Generalized

Method o f Moments(GMM)

approach to obtain (second-step) estimatesof

the intertemporal parameters.a. The first step: estimating the intratemporal elasticirv of substitution

Many

economic time series canbe

modelled as beingdifference

stationary with d r i f t.

Under

such conditions, the notionsof

s t o c h a s t i cand deterministic cointegration are useful in

examining the

interactionbetween t w o or more variables of interest. J2 Suppose that the

components of a vector series X ( t 3 are 1(1) p r o c e s s e s w i t h d r i f t ;

if

a linear combination of X ( t ) , say X X l t ) , is trend stationary, the components of X(t) axe said to be (stochastically) cointegrated with a cointegrating vector A . Consideran

additional restriction that the cointegrating vectoreliminptes the deterministic trends as

well

asthe

stochastic trends, sothat h X ( t ) is stationarv.

This

r e s t r i c t i o n is called t h e deterministic cointegration restriction.Standard unit root t e s t s suggest t h a t it is reasonable ta model the

relative price of traded

and

nontraded goods andthe

consumption r a t i o(of nontraded to traded goods) as

I(1)

processes. 3J W e now focuson

the relationship among these two variables.The

intratemporal f i r s t order condition (equation 6 ) implies that t h e l o gof

the relative

price and thelog of the consumption r a t i o are cointegrated with the deterministic

I

+

/

A 1 1 series are available upon request.Stochastic cointegration and the deterministic cointegration

restrictions were defined by Ogaki and Park (1989) and Campbell and

Perron

(1991).

Efficiencygains

f r o m estimating the cointegrating vectorsby imposing

the detrerministic e~integration restriction were discussedby

West (1989) f o r the one-regressor case and

by

Hansen (1992) and Park (1992)for

the multiple-regressor case.cointegration restriction.

1/

If

cointegration o b t a i n s , we can recover aconsistent estimate of the intratemporal e l a s t i c i t y of substitution, E . 2J

To test for cointegration, we employ

Park's

(1992)Canonical

CointegratingRegression (CCR) procedure. 3J

There are several advantages associated with

CCR.

First, t h e estimatedparameters, a and E in t h i s case, are not

only

consistent {as isOLS),

b u t a l s o asymptotically efficient and median unbiased. Second, unlike OLS,the

asymptotic distributions of CCR estimators are nuisance-parameter freeand normal conditioned on the regressors. This Latter feature a l l o w s

for

the usual interpretationof the

standard errors and thereforefar

hypothesis

testing. Third, as MonteCarlo

experiments show (seePark

andOgaki

(1991)), CCR

estimators have bettersmall

sample properties thanJohansen's estimators.

This

latter feature makesCCR

particularlyattractive for the present application, where

the

data are annual andthe

sample size is limited.

R~arranging terms, taking logs. and introducing a disturbance term (to allow,

for

example, f o r measurement errar) equation ( 6 3 becomes:Equation (9) is

likely to

sufferfrom

simultaneity bfas, since relativeprices are determined endogenously, and the

error

termmay

be s e r i a l l ycorrelated.

4/

To correctfor

the

potential presence ofsuch nuisance

parameters,

long-run

cavariances are estimated and used to transform thedata, As shown in Park (19921, the transformed data w i l l be cointegrated

with the same parameter vector as fhe original data.

Under the

null of

cointegration, an important property ofthe CCR

procedure isthat

linear restrictions can be t e s t e dby

X2 tests.ZJ

These

x2

tests are used in a regressionwith

spurious deterministictrends

addedto test

for

deterministic and stochastic cointegration.For

t h i s

purpose,the CCR procedure is a p p l i e d to a regression

As shown

by

H a l l(1978),

consumption is arandom

walk when the

real

interest rate is assumed to be constant. Since we allow

the

real i n t e r e s t rate to vary over time, the first difference of the log of consumption can be serially correlated.This will a l s o y i e l d a point estimate f o r the parameter a,

which

isrelated to the consumption

share.

See Ogaki (1993a) f o r a more d e t a i l e d explanation

of

CCR-basede s t b a t i o n and testing.

Note that the OLS estimator is consistent b u t

n o t

efficient because oflong-run

simultaneity bias. 5L e t H ( p , q ) denote the standard

Wald

statistic to test thehypothesis

tj + ~ = q p + 2 = . . . ~

=0,

where the variance ofI+

has been replaced with elementsq

of the long r u n covariance matrix ( s e e Park (1990)). Under the null of a

cointegration H(p, q ) converges to a x L In particular, the H(0,l) 4 - P '

s t a t i s t i c t e s t s the deterministic cointegrating restriction,

which

issuggested

by

t h e intratemporalfirst

order condition, On the other hand,the

H[l,q)

t e s t s f o r stochastic cointegsation.Table 3 reports the CCR resulss.

I

J

Asshown in

column(13,

w i t hthe exception of Korea, the intratemporal elasticity o f substitution,

r ,

is estimated to be positive, consistent w i t h our theoretical priors. Tn

the case of Korea, where t h e estimate of E is significantly negative, the

H(0,l)

test statistic presented incolumn

( 2 ) a l s o rejectsthe

specification,

implied by

the model atthe

0.1 percent level. It ispossible that

the

assumption of homothetic preferences impliedby

the CES utility function is causing problemsin

this

case. 2J For the remainingcountries, the point estimates f o r E range from a l o w

of

0 . 3 8 to a high of2.16;

for eight of the 13 countries the intratemporal e l a s t i c i t y ofsubstitution exceeds unity, implying gross substitutability between traded

and nontraded goods. For the Philippines, the p o i n t estimate of E is

positive but is n o t significantly s o , and the

H(0,l)

test is significant at the 1 percent level, implying that the null of deterministic cointegration is rejected; however, the null of stochastic cointegration cannot berejected (columns ( 3 )

and

( 4 ) ) at standard significancelevels.

For theother countries, none

of

the H ( 0 , l ) test statistics are significant ac the1

percent level and only a f e w ofchem

are

significant at the 5 percentlevel,

indicating that thenull

hypothesis of deterministic cointegrationcannot be rejected.

.- -. - - - - -

We

usedOgaki's (1993b) GAUSS CCR

Package forthe

CCR

estimations.The

CCR

procedure requires an e s t i m a t e of thelong-run

covarianceof

thedisturbances

i n

the

system.

We usedPark

andOgaki's

(1991)

methodw i t h

Andrews and Monahan's (1992) prewhitened

HAC

estimator with the QSkernel.

A first-orderVAR

was used for prewhitening. Wefollowed Andrews

andMonahan (1992)

with

the maximum absolute value of the elements of A (theirnotation) was set to 0.99.

h d r e w s ' s

(1991) automatic bandwidth estimator, ST, was c~nstructed fromfitting an

AR(1)

to each disturbance.21

See, f o r example, Atkeson and Ogaki(1993),

foran

attempt t o model-

nonhamothetic preferences w i t h an extended addilog utility function. These

authors assume time

separability

of

preferences over t w o goods,in

order toT a b l e 3 . Canonical Cointegrating Regression Results

Country

Brazil

Colombia 0.678 5.363 0.687 0.836

(0.214) (0.021) ( 0 . 4 0 7 ) ( 0 . 6 5 8 )

C o s t a Rica 1.132 0.474 1.087

1.934

(0.179)

(0.491) ( 0 . 2 9 7 ) (0.371)Mexico

Sri Lanka 1.587 0.669 0 . 6 7 4 1 . 7 3 7

(0.157) (0.414) (0

-419)

( 0 . 4 1 4 )India

Korea

Pakistan 2.075 0.558 2 . 2 5 6 3.942

(0.267)

(0.455) (0.133) (0.139)Philippines 0.382 7 . 9 8 9 0 . 6 9 5 2.040

( 0 . 3 3 3 ) (0.005

>

(0.404) (0.361)Ghana

Morocco