Quarterly strategy outlook

Q1/2014

Authored by Invesco’s Asian investment team based in Hong Kong

Market wrap-up and outlook

What happened after the US Federal Reserve (Fed) finally pulled the trigger? The Fed’s asset purchase tapering began in December but did not stop the MSCI Asia ex-Japan Index from closing with a 3.4% gain over the fourth quarter, wrapping up the volatile year with a positive performance of 3.3% (Source: Bloomberg, total returns in USD). Although changing expectations about the timing of the Fed’s tapering induced much volatility throughout 2013, Asia ex-Japan equity markets enjoyed solid performance for the year, with gains supported by improving macroeconomic conditions in select countries.

Although Asia ex-Japan equity markets ended the quarter with positive returns, performance varied across countries. A standout performer was India, which closed out the quarter as the best-performing market in the region. The Indian market strongly rebounded upon the sweeping victory of the opposition party in four major state elections and its central bank’s surprise decision to not hike

benchmark interest rates. The Greater China region also fared well, supported by China’s encouraging reform blueprint announced at the Third Plenum. On the other hand, most Southeast Asian countries ended the quarter in negative territory. Thailand was the worst performer as the market succumbed to the intensifying political stalemate that started in October. Malaysia was an exception, with the market recovering from the previous quarter’s drawdown. Over the quarter, Asian currencies generally performed poorly against the US dollar. In particular, the Indonesian rupiah and Thai bhat did not recover from their weakness in the previous quarter.

At the start of 2014, we saw some market and currency volatility in select emerging market economies in Latin America, Europe, the Middle East and Africa. These were mainly triggered by the Fed’s tapering actions. In particular, those regions with weak fiscal and trade positions were most vulnerable to the selloff.

Against this current backdrop, what should we expect for the rest of the year?

The Fed’s commencement with tapering has, as expected, induced volatility in equity markets. Looking ahead, Asian equity markets are likely to oscillate in response to the pace of tapering, but countries with better macro positions should be more resilient. Despite recent capital outflows from select Asian countries, we believe the major economies in Asia could fend off a currency crisis given the expanding foreign exchange reserves that act as an important buffer. Most notably, China and Korea lead the pack, with their foreign exchange reserves hitting new highs. While we cannot rule out further volatility in future, we believe investors will eventually refocus on the country-specific

fundamentals and market performance to reflect such differentiation.

In Asia, elections and politics will be in the spotlight for the first half of 2014. India, Indonesia and Thailand are on the verge of starting a new chapter in their countries’ respective political scenes. In May, India will hold national elections, which have been somewhat foreshadowed by state elections held in December last year. Indonesia is also holding a legislative election in April and a presidential election in July. Potential presidential candidates have This document is for

Professional Clients and Financial Advisors in Continental Europe, and for Professional Clients in Dubai, Isle of Man, Jersey and Guernsey and the UK only and is not for consumer use. It is not intended for and should not be distributed to, or relied upon, by the public. All opinions and forecasts expressed are those of Invesco’s investment team based in Hong Kong as of 31 December 2013 and are subject to change without notice.

emerged, with the current Jakarta governor, Joko Widodo, one of the hot candidates. With a combined population of 1.51 billion people, Indonesia

comprises nearly 50% of the Asia Pacific ex-Japan population.1 As a result, that country’s elections

could have significant economic implications for the region over the medium term. Election results in India and Indonesia could pave the way for more policy visibility — an instrumental factor in reviving the corporate investments and government infrastructure projects that have been put on hold due to election uncertainties. Thailand, on the other hand, is not showing signs of breaking through its political deadlock. The country’s election and political changes will undoubtedly prove to be swing factors for market performance and economic growth with the new government setting the stage. We will continue to monitor the situation as it progresses.

While investors should saddle up for the potentially bumpy ride markets will give them as a result of the region’s changing political scenery, one should not ignore the ongoing structural reform efforts being made by China. The reform blueprint laid out at the Third Plenum will change the country’s economic landscape, which comprises more than half of Asia’s economic share. The crucial year for implementation of the structural reform plans announced at the Third Plenum is 2014. We have already seen swift follow-through on various reform matters being made by different ministries, including the state-owned enterprises reform pilot programme in Shanghai and the extension of urban residency status to migrant workers in cities. The reform package announced at the Third Plenum is structurally positive for China over the long term; however, emergence of any profound economic success may take some time. In fact, some reform directions needed for moving the country onto a healthy and sustainable growth trajectory could even introduce short-term volatility (or pain). Looking ahead, the next key market event to watch would be the National People’s Congress (NPC) annual session in March. The market anticipates further continuity with reforms, as historically NPC sessions have set the tone for the economic direction taken over the rest of the year.

1

Source: International Monetary Fund, JPMorgan data, 2013 population statistics

On a positive note, the recent Asian equity market correction has indeed brought valuation to an accommodating level compared with historical standards, with the 12-month forward price-to-earnings ratio falling to 11.4 times, well below the seven-year average of 12.6 times.2 It is also

interesting to note that Asia now offers expected earnings growth of 12.7% for 2014, as compared with 11% from the developed world.3

Differing from the macro headwinds, bottom-up stock analysis reveals an interesting set of investment opportunities: With macro/political uncertainties in select Asian countries in the first half of 2014, we believe stock picking is the key to portfolio outperformance for this year. We continue to focus on pockets of growth that stand to benefit from secular trends in various Asian economies. We believe companies that demonstrate a growth profile with quality characteristics will likely be more resilient amid market volatilities.

2

Source: Invesco, Factset, I/B/E/S, MSCI. 12-month forward price-to-earnings ratio of MSCI Asia Pacific ex-Japan Index, as of Jan. 31, 2014

3

Source: Invesco, Factset, I/B/E/S, MSCI. Twelve-month forward price-to-earnings ratio of MSCI Asia Pacific ex-Japan Index as of 31 January 2014.

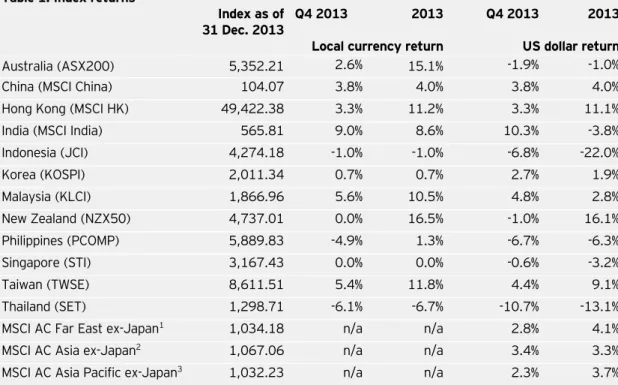

Table 1: Index returns

Index as of 31 Dec. 2013

Q4 2013 2013 Q4 2013 2013

Local currency return US dollar return

Australia (ASX200) 5,352.21 2.6% 15.1% -1.9% -1.0%

China (MSCI China) 104.07 3.8% 4.0% 3.8% 4.0%

Hong Kong (MSCI HK) 49,422.38 3.3% 11.2% 3.3% 11.1%

India (MSCI India) 565.81 9.0% 8.6% 10.3% -3.8%

Indonesia (JCI) 4,274.18 -1.0% -1.0% -6.8% -22.0% Korea (KOSPI) 2,011.34 0.7% 0.7% 2.7% 1.9% Malaysia (KLCI) 1,866.96 5.6% 10.5% 4.8% 2.8% New Zealand (NZX50) 4,737.01 0.0% 16.5% -1.0% 16.1% Philippines (PCOMP) 5,889.83 -4.9% 1.3% -6.7% -6.3% Singapore (STI) 3,167.43 0.0% 0.0% -0.6% -3.2% Taiwan (TWSE) 8,611.51 5.4% 11.8% 4.4% 9.1% Thailand (SET) 1,298.71 -6.1% -6.7% -10.7% -13.1%

MSCI AC Far East ex-Japan1 1,034.18 n/a n/a 2.8% 4.1%

MSCI AC Asia ex-Japan2 1,067.06 n/a n/a 3.4% 3.3%

MSCI AC Asia Pacific ex-Japan3 1,032.23 n/a n/a 2.3% 3.7%

Source: Bloomberg, as of 31 December 2013. All returns stated in the above table are price returns except for MSCI indices. Returns for China, Hong Kong, India, Far East ex-Japan, Asia ex-Japan and Asia Pacific ex-Japan are total returns.

1 MSCI AC Far East ex-Japan Index consists of the following nine developed and emerging market indices: China, Hong Kong, Indonesia, Korea, Malaysia, Philippines, Singapore, Taiwan and Thailand.

2 MSCI AC Asia ex-Japan Index consists of the following 10 developed and emerging market indices: China, Hong Kong, India, Indonesia, Korea, Malaysia, Philippines, Singapore, Taiwan and Thailand.

3 MSCI AC Asia Pacific ex-Japan Index consists of the following 12 developed and emerging market indices: Australia, China, Hong Kong, India, Indonesia, Korea, Malaysia, New Zealand, Philippines, Singapore, Taiwan and Thailand.

Country allocation

Despite a rocky start to 2014, we continue to hold on to our constructive view on Asia ex-Japan on the basis of its relative value versus the expanding premium of its developed market counterparts. Drawing from our model that ranks markets by relative macro fundamentals and change in comparison with the previous quarter, we are maintaining our preference for northern Asia markets without making drastic changes to our asset allocation this quarter. In particular, we remain positive on China, Taiwan and Korea, as their exports-driven industries should be poised to benefit from a more promising recovery outlook in

developed economies. In contrast, our cautiousness on the emerging economies of the Association of Southeast Asian Nations (ASEAN) has not reversed, despite recent corrections bringing valuation to a more reasonable level. Smaller, illiquid markets will likely remain vulnerable as tapering accelerates and creates pressure on the local currencies of those countries that currently have relatively weak account profiles.

China: On the back of strong absolute levels of gross domestic product (GDP) growth relative to the rest of the region, China achieved the second-highest score in our country model. We believe the country’s GDP growth rate can maintain levels

above the official growth floor of 7%, as it is still the fastest-growing economy in the region. Despite a near-term concern about the trust loan default issue, we believe the current situation is still manageable. More importantly, expanding foreign reserves continue to provide a strong buffer to absorb shocks in the system. Equity valuation remains compelling relative to historical standards. Coupled with a positive earnings growth outlook, we have maintained an overweight position in China.

Hong Kong: We reduced the target weight in Hong Kong from an overweight to an underweight position primarily due to the near-term capital flow

headwinds. Given the nature of Hong Kong’s open economy and its status as a global financial hub, capital flow volatilities triggered by US asset purchase tapering could pressure broad money supply. Within the Hong Kong economy, we see modest real wage growth as well as a slowing property market.

Taiwan: We have an overweight position in Taiwan. The revival of developed market macro demand has lent support to the Taiwanese economy as

confirmed by the recent uptrend in manufacturing. In the near term, we expect robust growth in industrial activity to continue, which will support a positive GDP growth outlook. At the corporate level, earnings growth is also supportive.

Korea: We have the largest overweight position in Korea, which achieved the highest score in our country model. Korea has a strong current account surplus, sizable foreign exchange reserves and a lower proportion of short-term foreign exchange borrowings. Amid a gradual recovery in developed markets’ economies, we expect exporters in Korea to benefit from upsides in earnings. With valuation still one of the cheapest in the region and well below the country’s historical average, the Korean equity market holds the potential for further rerating looking ahead. In particular, we continue to find many interesting core quality stocks that demonstrate resilience through the market cycle, especially in the consumption-related space on a bottom-up basis.

Singapore: We boosted the target weight in Singapore to an overweight position upon a better GDP growth outlook within which the service sector will remain a key growth anchor. An improving earnings growth outlook offers another dimension of support to this market.

Malaysia: We maintain an underweight position in Malaysia primarily due to the implementation challenges facing the fiscal consolidation policies to be carried out in 2014. Though fiscal credibility could be improved over the long run,

implementation of such measures as removal of the sugar subsidy and the power tariff hike creates near-term headwinds for the economy to grind

significantly higher.

Indonesia: We trimmed the target weighting in Indonesia from a slight overweight to a slight underweight in view of election uncertainties and the outlook of elevated inflation. Indonesia will hold legislative elections in April 2014 and the

presidential election in July. Companies may hold off making investments in the months running up to the elections, thus diminishing stimuli to the economy.

Thailand: We maintain an underweight position in Thailand, given the political overhang and weakening business sentiment. We do not see signs of major easing in anti-government upheavals, which have made and will continue to make the Thai market prone to net foreign investor outflows.

Philippines: We continue to maintain zero target weighting for this country due to its elevated valuation relative to its regional peers. As seen in the previous quarter, the market has been vulnerable to selloffs amid the “taper tantrum.”

India: We further added to the overweight position in India. We believe India’s GDP growth is bottoming out as exports recover and investment activities pick up. The increase in investment activities does not necessarily have to be driven by new project activities, but accelerating execution of existing projects would itself be a good starting point. Also, an improved current account deficit and balance-of-payment situation will better prepare India to face US tapering in 2014. On the political front, we believe the prospects for forming a stable

government in the 2014 national elections are rising and that this will pave way for the government to solve some of the Indian economy’s structural challenges. Sticky inflation does, however, remain a key risk to economic growth. Having said that, the new governor of the Reserve Bank of India places more emphasis on CPI inflation than his

predecessors and has shown a resolute stance to act should inflation remain elevated. Our model

continues to focus on companies that can benefit from the recovery in exports and growth in domestic consumption. The focus remains on companies with quality management and reasonable earnings growth visibility.

Australia: Australia remains an underweight allocation in our country model. Although the Reserve Bank of Australia kept interest rates on hold, officials continued to stress they would prefer to see a lower Australian dollar to stimulate the economy, which is driven by commodity exports that have yet to see a strong rebound. We hold an underweight position in Australia primarily due to the country’s lower GDP growth compared with its Asian peers as well as due to stretched equity valuation.

ASEAN: We are broadly underweight in ASEAN except Singapore — a position driven by the relative attractiveness of different country-specific

fundamentals. Although much of the knee-jerk reaction triggered by the US tapering talks has brought valuation to an accommodating level compared with historical standards, we believe ASEAN’s valuation is still not cheap relative to the rest of the region. Along with the ongoing political uncertainties and macro headwinds, we remain cautious and selective in this region.

Contact Information

Amsterdam +31 20 561 62 61 www.invesco.nl

Brussels +32 2 64 10 17 0 www.invesco.be

Dubai +9714 425 0950 www.invesco.ae

Frankfurt +49 69 29807 800 www.de.invesco.com Isle of Man, Jersey and Guernsey

+44 1534 607600 www.invescointernational.co.uk Madrid +34 91 78 13 02 0 www.invesco.es Milan +39 02 88074 1 www.invesco.it Paris +33 1 56 62 43 77 www.invesco.fr Stockholm +46 84 63 11 09 www.invescoeurope.com UK +44 1491 417600 www.invescoperpetual.co.uk Vienna +43 1 316 20 0 www.invesco.at Zurich +41 44 287 90 00 www.invesco.ch Important Information

This document is for Professional Clients and Financial Advisers in Continental Europe, and for Professional Clients in Dubai, Isle of Man, Jersey and Guernsey and the UK only and is not for consumer use. It is not intended for and should not be distributed to, or relied upon, by the public. All opinions and forecasts expressed are those of Invesco’s Asian investment team based in Hong Kong as of 28 February 2014 and are subject to change without notice.

The views expressed herein are those of Invesco’s Asian investment team based in Hong Kong, and do not refer to any specific Invesco product. They are based on current market conditions and are subject to change without notice. Opinions and views may differ from other Invesco Investment Professionals. This document does not form part of any prospectus. This document contains general information only and does not take into account individual objectives, taxation position or financial needs. Neither does this constitute a recommendation of the suitability of any investment strategy for a particular investor. While great care has been taken to ensure that the information contained herein is accurate, no responsibility can be accepted for any errors, mistakes or omissions or for any action taken in reliance thereon. The value of investments, and the income from them, can fluctuate (this may partly be the result of exchange rate fluctuations), and investors may not get back the full amount invested. Neither Invesco Asset Management nor any affiliate of Invesco Ltd. guarantee the return of capital, distribution of income or the performance of any fund or strategy. This document is not an invitation to subscribe for shares in a fund nor is it to be construed as an offer to buy or sell any financial instruments. As with all investments, there are associated inherent risks. Asset management services are provided by Invesco in accordance with appropriate local legislation and regulations. www.invescoeurope.com Issued in

-Austria by Invesco Asset Management Österreich GmbH, Rotenturmstrasse 16-18, A-1010 Wien.

-Dubai by Invesco Asset Management Limited, PO Box 506599, DIFC Precinct Building No 4, Level 3, Office 305,Dubai, United Arab Emirates. Regulated by the Dubai Financial Services Authority.

-France by Invesco Asset Management S.A., 18, rue de Londres, F-75009 Paris, which is authorised and regulated by the Autorité des marchés financiers in France.

-Germany by Invesco Asset Management Deutschland GmbH, An der Welle 5, D-60322 Frankfurt am Main, which is authorised and regulated by the Bundesanstalt für Finanzdienstleistungsaufsicht in Germany.

-Isle of Man by Invesco Global Asset Management Limited, George’s Quay House, 43 Townsend Street, Dublin 2, Ireland. Regulated in Ireland by the Central Bank of Ireland.

-Jersey and Guernsey by Invesco International Limited, 2nd Floor, Orviss House, 17a Queen Street, St Helier, Jersey, JE2 4WD. Regulated by the Jersey Financial Services Commission.

-Switzerland by Invesco Asset Management (Schweiz) AG, Stockerstrasse 14, CH-8002 Zürich.

-UK by Invesco Asset Management Limited, Perpetual Park, Perpetual Park Drive, Henley-on-Thames, Oxfordshire RG9 1HH, which is authorised and regulated by the Financial Conduct Authority.