Management Plan 2015

DG Competition

2

Contents

Part 1.Mission statement 4

Part 2. This year's challenges 6

2.1. Sector Priorities 6

2.2. Priorities for Policy Activities 8

2.3. Statement on the DG's efforts to ensure capacity to deliver on the priorities 9

2.4. Key Performance Indicators 9

Part 3. General objectives of the policy 11

3.1. To enhance consumer welfare in the EU and efficiently functioning markets by

protecting competition 12

3.2. To promote competition culture in the EU and worldwide 16

Part 4. Specific objectives for operational ABB activities 19

4.1. ABB Activity "Control of State aid" 19

4.1.1. Better targeted growth-enhancing aid 20

4.1.2. Prevention and recovery of incompatible aid 27

4.2. ABB activity "Cartels, antitrust and liberalisation" 30

4.2.1. Cartels 30

4.2.2. Other anti-competitive agreements and practices 31

4.3. ABB activity "Merger control" 39

4.4. ABB activity "Policy coordination, European Competition Network (ECN) and

international cooperation" 41

4.4.1. Competition policy 42

4.4.2. Coherent application of EU competition law by national competition authorities

and courts 48

4.4.3. Coherent private enforcement of EU competition law 50 4.4.4. Ensure compensation for victims of EU competition law infringements 51

3

Part 5. Horizontal activities 56

5.1. Policy strategy and coordination 56

5.1.1. Strategy: delivering results 56

5.1.2. Competition advocacy and transparency 56

5.1.3. Internal and external communication 58

5.1.4. Highest standards in the enforcement of competition policy 58

5.2. Management of the DG 62

5.3. Specific efforts to improve economy and efficiency of financial an non-financial

activities 70

5.3.1. Staff allocation 70

5.3.2. Access to file 71

Annex 1. Indicative plan of evaluations and studies 72

4

P

ART1.M

ISSION STATEMENTThe mission of the Directorate-General for Competition is to enable the Commission to make markets deliver more benefits to consumers, businesses and the society as a whole, by protecting competition on the market and fostering a competition culture

.

DG Competitiondoes this by enforcing competition rules and through actions aimed at ensuring that regulation takes competition duly into account among other public policy interests.

Competition is not an end in itself. It is an indispensable element of a functioning internal market guaranteeing a level playing field. It contributes to an efficient use of society's scarce resources, technological development and innovation, a better choice of products and services, lower prices, higher quality and greater productivity in the economy as a whole.

Therefore, competition policy contributes to the wider Commission objectives1, in particular to boosting jobs, growth and investment, a connected Digital Single Market, a resilient Energy Union with a forward looking climate change policy, a deeper and fairer Internal Market with a strengthened industrial base and a deeper and fairer Economic and Monetary Union.

The European Union is the world's largest economic and trading area. The EU's unique asset and distinct comparative advantage on the global scene is its internal market, which encompasses over half a billion consumers and more than 20 million companies. Since its inception, the on-going process of improving and expanding the Single Market has gone hand in hand with the development of EU competition policy.

The European Commission, together2 with the national competition authorities, enforces EU competition rules, based on Articles 101-109 of the Treaty on the Functioning of the EU (TFEU), to make EU markets work better, by ensuring that all companies compete equally and fairly on their merits in the internal market. This benefits consumers, businesses and the European economy as a whole. Within the Commission, the Directorate-General for Competition is primarily responsible for these direct enforcement powers.

DG Competition carries out its mission mainly by taking direct enforcement action against companies or Member States when it finds evidence of unlawful behaviour – be it anti-competitive agreements between firms, abusive behaviour by dominant companies or attempts by government to distort competition in the internal market by providing some companies undue advantages over others3. At the same time, EU competition policy encourages granting of better targeted aid that addresses market failure or equity objectives4. Such aid has a beneficial impact on competitiveness, employment and growth, and thus on the welfare of society as a whole.

1

Political Guidelines for the new European Commission as presented by President Juncker of 15 July 2014, http://ec.europa.eu/priorities/docs/pg_en.pdf#page=5

2 Article 101 and 102 TFEU.

3 Council Regulation (EC) No 1/2003 of 16 December 2002 on the implementation of the rules on

competition laid down in Articles 81 and 82 of the Treaty, OJ L 1, 04.01.2003, p. 1-25.

4 Council Regulation (EU) No 733/2013, of 22 July 2013 amending Regulation (EC) No 994/98 on the

application of Articles 92 and 93 of the Treaty establishing the European Community to certain categories of horizontal State aid, OJ L 204, 31.7.2013, p. 11-14; See also http://ec.europa.eu/competition/state_aid/modernisation/index_en.html for the State aid Modernisation.

5

Finally, EU merger control5 aims to prevent the emergence of market structures which impede effective competition or result in the deterioration of market structures where competition is already less effective.

DG Competition channels its limited resources on the most harmful practices in key sectors, and works in partnerships with other policies to support the delivery of other policy objectives in a pro-competitive way at EU and national level. It works in close partnership with national competition authorities and national courts to ensure an effective and coherent application of EU competition law, thereby contributing to a level playing field in the internal market. DG Competition provides guidance about the competition rules and their enforcement to improve legal certainty for stakeholders. It also strives to ensure transparency, due process and predictability for its stakeholders and private enforcement of EU competition law.

In the international context, DG Competition strives to shape global economic governance by strengthening international cooperation in enforcement activities and making steps towards increased convergence of competition policy instruments across different jurisdictions. DG Competition aims at maintaining and strengthening the Commission’s reputation world-wide and promoting international cooperation in this area.

5

Council Regulation (EC) No 139/2004 of 20 January 2004 on the control of concentrations between undertakings (the EC Merger Regulation), OJ L 24, 29.01.2004, p. 1-22.

6

P

ART2.

T

HIS YEAR'

S CHALLENGES2015 marks the first full year of the new Commission whose mandate was outlined on 15 July 2014 in the President's Political Guidelines6. The Political Guidelines sets a new Agenda for Jobs, Growth, Fairness and Democratic Change. The ten top priority areas include among others a Growth, Jobs and Investment Package, an Energy Union, a Digital Single Market and a fairer internal market with a strengthened industrial base.

To this end, more collaborative and integrated working methods7 have been put in place. Accordingly, competition policy – where the Commission exercises exclusive competences - is also expected to support the Commission's action in top priority policy areas listed in the Political Guidelines8. Every effort will therefore be made to ensure that EU competition policy makes markets work as well as possible, delivering concrete benefits to consumers and businesses. In so doing, EU competition policy also promotes efficiency and innovation, to the benefit of growth and the society as a whole.

Competition policy supports several other major EU policies such as the digital agenda, energy policy, financial service policy, industrial and internal market policy as well as the fight against tax evasion. It does so mainly through enforcement activity, i.e. fighting and preventing cartels, abuses of dominant positions and anticompetitive mergers as well as by facilitating better targeted growth-enhancing State aid. By mobilising its knowledge of key markets it can also share its expertise with other Commission's services in support of the top priorities outlined in the Political Guidelines.

2.1.

Sector Priorities

In 2015, DG Competition enforcement action will target sectors and areas that are the most relevant for the Commission's priorities as outlined in the Political Guidelines.

The Energy Union

Energy is one of the sectors in which completing the Single Market will bring significant benefits to Europe’s consumers and businesses. Building an Energy Union based on energy efficiency, security of supply and sustainability requires investment in and development of energy infrastructure. For such action to bring the maximum benefits, it must be pursued in full respect of and through consistent enforcement of the EU's internal market and competition rules. This may require the assessment of a large number of complex transactions involving State aid as well as the need to provide guidance. Indeed, most of the national mechanisms for supporting renewables, generation capacity and infrastructure investment involve State aid. The new Energy and Environmental Aid Guidelines will help better targeting public support to renewable energy

6

Political Guidelines for the new European Commission as presented by President Juncker on 15 July 2014, http://ec.europa.eu/priorities/docs/pg_en.pdf#page=5

7

The Working Methods of the European Commission 2014-2019, Communication from the President to the Commission C(2014) 9004 of 11 November 2014.

8

Mission letter to the Commissioner of Competition Vestager by President Juncker 1 November 2014. http://ec.europa.eu/commission/sites/cwt/files/commissioner_mission_letters/vestager_en.pdf

7

sources while promoting the use of subsidies to improve interconnections and cross-border networks.

Antitrust enforcement can also help to ensure fair and non-discriminatory access to energy infrastructure, remove obstacles to market integration and foster competition between and within Member States. Competition enforcement ensures that companies would not maintain or reinstate barriers to competition; current investigations are looking into potential abuses of dominance in eastern and central European markets.

Competition policy is thus a significant tool to ensure competitive energy prices on a sustainable basis and one of the pillars required to build a genuine Energy Union.

A Connected Digital Single Market

Creating a connected Digital Single Market aims to make Europe a world leader in information and communication technology, areas which increasingly occupy DG Competition and engage its staff in continuously keeping up with rapid developments in these fields. The more the integration of the Digital Single Market progresses, the greater the need for EU competition rules to ensure a fair level-playing field for all companies offering their goods and services on-line and in digital form across the EU. Through recent and substantial cases, DG Competition has gained valuable expertise that it can contribute to the Digital Single Market priority set out in the Political Guidelines. While the Commission has already approved a number of significant mergers between European network providers, telecom market consolidation is expected to continue in the new mandate, requiring vigilance and robust enforcement by DG Competition also in the future. A characteristic of such fast-moving markets is that dominant positions can develop quickly. In particular, network effects can tip the market in favour of a particular player resulting in a near-monopoly level of dominance. In the knowledge-based sectors DG Competition will continue its Google antitrust case, establishing all relevant facts needed for concluding this complex investigation on competition grounds.

Financial Services

Financial services are an area in which competition policy has made a significant positive contribution over the past years. Due to its systemic importance and its role in providing access to finance to the real economy, DG Competition will remain active in the financial services sector. By 2015, the Banking Resolution structures will have become operational. Nevertheless, where necessary, DG Competition will continue to play a role in the restructuring of banks. DG Competition will continue with its investigations into potentially anti-competitive behaviour, such as the possible manipulation of reference benchmarks, the alleged collusion between certain banks to protect their CDS market making business by foreclosing exchanges as well as alleged infringements in the area of payments. To facilitate access to finance, investment and growth, DG Competition also intends to contribute to the creation of a well-regulated and integrated Capital Markets Union, as envisaged in the Political Guidelines. This Capital Markets Unions, which is under way, is scheduled to encompass all Member States by 2019.

8 The Investment Package

The Jobs, Growth and Investment Package has recently been adopted9. Competition policy, and in particular the new State aid control rules recently implemented in the framework of the State Aid Modernisation, can contribute towards the target of EUR 315 billion investment over the next three years. For instance, the Broadband State Aid Guidelines encourages the deployment of broadband infrastructure; research and innovation will benefit from the increased possibilities of public support offered by the R&D&I State aid Framework and the Risk Finance Guidelines; several hundreds of major projects within the EU cohesion policy, most of which related to different forms of infrastructure, will involve State aid and will require DG Competition's scrutiny to ensure that the spending is cost-effective and in line with overall EU objectives.

Tax Planning

The fight against tax evasion and avoidance is a further significant priority of the new Commission.

This issue already is, and will continue to be, a priority for DG Competition. DG Competition has established a dedicated Task Force to investigate specific tax planning practices by multinationals and to verify that Member States ensure a level playing field respecting State aid rules when they design corporate tax systems. More specifically, the recently opened investigations aim at ensuring that Member States do not circumvent State aid rules to help multinational enterprises avoid paying their fair burden of tax. The Task Force Tax Planning will continue to work on such cases in 2015.

2.2.

Priorities for Policy Activities

The policy initiatives that DG Competition intends to pursue in 2015 include the following:

− Ensure an effective implementation of the State aid Modernisation package via a new partnership with Member States, including adoption of a Commission Communication on the notion of State aid;

− Guidelines on the application of the specific rules laid down in Articles 169, 170 and 171 of the CMO Regulation for the olive oil, beef and veal and arable crops sectors, which aim to provide concrete explanations and technical parameters for the undertakings and ensure that the National Competition Authorities and courts apply the new rules consistently;

− Finalise the bulk of the Impact Assessment for the report to the Parliament and Council on the functioning and future of the Insurance Block Exemption Regulation;

9

Political Guidelines for the new European Commission as presented by President Juncker of 15 July 2014. Package adopted on 26 November 2014, see http://europa.eu/rapid/press-release_IP-14-2128_en.htm

9

− Monitor the implementation of the Damages Directive10

− In view of maintaining EU competition law instruments aligned with market realities and contemporary economic and legal thinking, DG Competition will hold Regulation 1/2003 and EU Merger Regulation under continued review11.

2.3.

Statement on the DG's efforts to ensure capacity to deliver on the priorities

The ability to maintain the highest standards in competition policy enforcement in 2015 strongly depends on the ability to keep attracting, motivating and retaining high-quality staff. This forms the core of our HR objectives.DG Competition's project-based and legally obligatory activities with strict deadlines, combined with growing case complexity require constant attention to efficiency improvements. Therefore, DG Competition continues to:

I. Operate an organisational model based on flexible use of resources across the organisation whereby projects and cases go through a priority assessment and staffing decisions take into account workload measurement, as well as necessary competences and skills;

II. Invest substantially in increasing the efficiency of its operations, especially through IT development in areas such as rationalisation of case management systems and procedures, forensic IT, e-Discovery, Genis and mobile indexing.

2.4.

Key Performance Indicators

Four of our five key performance indicators measure the performance of the main competition policy instruments: Antitrust and Cartels, Mergers and State aid. While these indicators do not pretend to deliver an exhaustive account of DG Competition's work or its impact on markets, they constitute the core quantifiable indicators of our work. To understand our impact on the market each year, DG Competition is monitoring (1) the benchmark for (observable) customer benefits resulting from cartel prohibition decisions and (2) the benchmark for (observable) customer benefits resulting from horizontal merger interventions. The aim is to keep these two indicators stable over time.

The key performance indicators for State aid control are (3) the percentage of State aid granted by Member States for horizontal objectives of common interest and (4) the overall cumulative level of crisis aid to the financial sector actually used by Member States, expressed as percentage of GDP. While the aim for the third indicator is to increase, the fourth indicator should stop increasing once economic recovery progresses.

10 Directive of the European Parliament and of the Council on certain rules governing actions for

damages under national law for infringements of the competition law provisions of the Member States and of the European Union, 2013/0185 (COD) of 26 November 2014, see http://ec.europa.eu/competition/antitrust/actionsdamages/damages_directive_final_en.pdf

10

The final key performance indicator, (5) implementation of case management rationalisation, represents DG Competition's horizontal activities. It measures the progress of the DG-Competition-lead ICT project to develop a new Case Management system for the participating DGs and thus contribute to the modernisation and rationalisation of case and document management in the Commission.

11

P

ART3.

G

ENERAL OBJECTIVES OF THE POLICYThe general objectives of DG Competition are i) to enhance consumer welfare and efficiently functioning markets in the EU by protecting competition and ii) to promote competition culture in the EU and worldwide. Through pursuing these general objectives, competition policy will for its part contribute to the improvement of the functioning of the Single Market, a key lever for competiveness and growth.

Efficiently functioning markets in the EU will bring economic opportunities, improve productivity, drive down costs and boost competitiveness for companies of all sizes. Undistorted competition also fosters competitiveness in a global context: a competitive Single Market prepares European companies to do business on global markets and to succeed. This is key to creating growth and jobs in Europe.

DG Competition engages in competition advocacy in relation to other Commission services, other EU institutions and at national and international levels, with the aim of shaping the regulatory framework and policy initiatives in a competition-friendly way. Competition-friendly regulation and competition culture create favourable conditions for investments and innovation, which enhances consumer welfare and efficiently functioning markets, enables growth and contributes towards more convergence.

The increased convergence of competition regimes worldwide is a prerequisite for the effectiveness and success of EU competition policy in a globalised economy. DG Competition continues to promote international convergence both bilaterally and in international venues such as the International Competition Network, the OECD or UNCTAD, and will continue to closely cooperate with the competition authorities of the Member States, gathered in the European Competition Network (ECN).

However, while being direct, the causal link between EU competition policy and wider Commission objectives, including economic growth, is not exclusive, since the latter is dependent on a number of external factors outside the control of EU competition policy (general economic environment, business strategies, Member States' policies etc.). The same is true for the

jobs, growth, investment and competitiveness Antitrust/cartel

enforcement: pushing for lower (input) prices, promoting innovation and

preventing market foreclosure

State aid policy: encouraging growth-enhancing public spending and ensuring a level playing field Merger control: keeping markets

open and efficient Competition-friendly regulation and advocacy in relation to other Commission services and Member

States

International cooperation: tackling

the challenges of globalization

12

contribution that competition policy brings to achieving several European Union's other key objectives and headline targets12. Therefore, while the contribution of competition policy cannot be directly inferred from a series of indicators, structural policies, of which competition policy is one, contribute towards reaching these objectives.

3.1.

To enhance consumer welfare in the EU and efficiently functioning markets by

protecting competition

The added value of EU competition policy

The objective at the heart of EU competition policy is to enhance consumer welfare and efficiently functioning markets by protecting competition from market distortions whether originating from Member States (distortive State aids) or market players including public undertakings with special or exclusive rights (distortive unilateral or coordinated behaviour), or mergers that would significantly impede effective competition. Undistorted competition on the market enhances consumer welfare and promotes productivity and growth through allocative efficiency (entry of more efficient firms and exit of less efficient firms), productive efficiency (incentives for a firm to become more efficient) and dynamic efficiency (innovation moving the technological frontier).

DG Competition prioritises its actions to maximise the impact on the functioning of markets. Enhancing market efficiency also requires a focus on sectors with the greatest relevance for the competitiveness of EU economy and the greatest – direct or indirect – effect on consumers. Therefore, tackling anti-competitive practices in key sectors such, ICT, telecommunications, energy, and financial services, where increased competition will also have beneficial spill-over effects on many other downstream sectors, aims at maximising the contribution of competition policy towards the EU's overall objectives. Competition enforcement thus contributes13 to the Commission's strategic priorities14 and efforts aimed at exploiting the full potential of the Single Market. Enhancing consumer welfare also means that priority must be given to the most serious competition infringements such as cartels, especially in sectors close to final consumers

The more harmful anti-competitive practices are, the greater the need there is for competition policy to intervene. Cartels belong to the most harmful restrictions of competition and therefore high priority continues to be given to the effective detection, prosecution and deterrence of cartels. For the same reasons, other anticompetitive agreements, abuses of dominant positions and mergers that would significantly impede effective competition must also continue to be targeted by enforcement action. Furthermore, by keeping markets open, EU competition policy ensures that the benefits of globalisation are passed through to European consumers. EU competition policy also protects European consumers against the potentially harmful aspects of

12

Europe 2020 targets. See http://ec.europa.eu/europe2020/europe-2020-in-a-nutshell/targets/index_en.htm

13

Mission letter to the Commissioner of Competition Vestager by President Juncker 1 November 2014. http://ec.europa.eu/commission/sites/cwt/files/commissioner_mission_letters/vestager_en.pdf

14

Political Guidelines for the new European Commission as presented by President Juncker 15 July 2014, http://ec.europa.eu/priorities/docs/pg_en.pdf#page=5

13

globalisation by targeting international cartels, mergers and abusive practices of firms of any nationality that harm European consumers.

While State aid is in general harmful, as it distorts incentives in markets, it may enhance consumer welfare by addressing a market failure or an equity concern. The Treaty recognises this dichotomy and State aid control aims to prevent Member States from issuing aid unless the proper conditions are met. Aid to research and development, aid that protects the environment, aid to facilitate access to finance for SMEs and aid that attracts investment to weaker regions are all examples of growth-enhancing policies and "good aid". At the same time, aid that reduces growth, such as aid to keep failing companies on the market, should be avoided.

Measuring the added value of EU competition policy

For the purposes of an annual review of its cartel and merger enforcement, DG Competition provides for a quantitative assessment of the results achieved by the Commission in protecting competition. The benchmark for the (observable) customer benefits resulting from Commission decisions attempts to estimate the benefits to consumers from cartel prohibition decisions and horizontal merger interventions15. Based on this benchmarking exercise, the observable customer benefits from cartel decisions adopted in 2013 were in the range of EUR 4.89-5.66 billion16. The observable customer benefits following the Commission’s decisions in 2013 prohibiting a horizontal merger or clearing such a merger subject to remedies, were between EUR 0.3 and 0.7 billion17. It should be emphasised that this benchmark does not include any benefits stemming from better quality or wider choice, other effects of competition policy, such as productivity gains or impact on jobs, any possible pass-on to final consumers in the case of intermediary goods or services, or deterrent effect18. It also is important to note that the above estimates cover only a part of the enforcement activities of DG Competition, cartels and horizontal mergers, and therefore underestimate the actual impact of EU competition enforcement on consumers19. As regards the quality of its enforcement actions, the success rate before the European Courts in competition cases (antitrust/cartels, mergers and State aid) provides an important annual

15 The benchmarking exercise is based on a number of assumptions, which are further explained in

footnotes 26 and 27 below and represent one method (among other potential approaches, none of which can be considered comprehensive or absolute) to arrive at a quantitative estimate.

16 The approach followed to benchmark the observable customer benefits from terminating a cartel is

explained in footnote 26. The figure for the customer benefits relating to cartel decisions adopted in 2014 will be provided in the Annual Activity Report 2014.

17 The methodology for benchmarking the observable customer benefits deriving from the Commission's

horizontal merger decisions is explained in footnote 27. The figure for the customer benefits relating to horizontal merger decisions adopted in 2014 will be provided in the Annual Activity Report 2014.

18 For the deterrent effect of fines and impact of antitrust rules, see further ABB activity Cartels, antitrust

and liberalisation under section 4.2.

19

Enforcement action against abuses of dominant positions and other anti-competitive agreements as well as liberalisation and State aid control also engender substantial consumer benefits but for these types of practices, no single generalised benchmark is available due to the great heterogeneity of cases. Therefore, DG Competition rather carries out selected individual ex-post case studies. The same applies to DG Competition's activities concerning policy coordination, European Competition Network and international cooperation activities.

14

indicator of the Commission's performance in this respect. In 2015, DG Competition aims to achieve a success rate of at least 70% at the European Courts.

In addition, DG Competition measures and compares its performance in a number of fields related to the quality and impact of its work. In 2014, it conducted for the second time

Eurobarometer Standard Qualitative Study20 whereby professional stakeholders21 provided their views on some key quality parameters22 related to DG Competition's work. The Study also contributes to more targeted and dynamic communication and interaction with DG Competition's professional stakeholders. The Study finds, for instance, a consensus across stakeholder groups on the priority sectors23 that DG Competition should focus on, which correspond also to sectors where European citizens24 identify competition concerns. There was also widespread agreement that DG Competition’s work generally promotes competition, raises awareness and acts as deterrent25. DG Competition aims to continuously increase its level of performance in this respect and plans to conduct these surveys again in 2019 to obtain updated information.

20 Eurobarometer Standard Qualitative Study – DG Competition Stakeholder Survey (2014) to be

published in 2015, http://ec.europa.eu/competition/publications/reports/surveys_en.html

21

Professional stakeholders included companies, lawyers, economic consultancies, business and consumer associations, national competition authorities and ministries involved in DG Competition's work in 2010-2013.

22

These parameters include i) Soundness of legal and economic analysis (clarity and comprehensibility of decisions, predictability of decisions, predictability of fines imposed, understanding the markets and quality of economic analysis) ii) Transparency and procedural fairness (level of transparency of DG Competition's work, listening and informing in a timely manner, publication of non-confidential versions of decisions, stakeholder consultations on new rules, observance of procedural rules and burden on businesses and organisations), iii) Economic effectiveness (effectiveness of detection policy, deterrent effect of fines, impact of existing antitrust rules on planned business transactions, timeliness of decisions, focus on the right sectors, adaptation to the technological changes and globalisation, Impact on the markets, use of settlements in cartel cases and commitment decisions in antitrust cases, enforcement of decisions and contribution to the EU's economic growth) and iv) Communication and promotion of competition culture (clarity and comprehensibility of external communication, choice of communication and media channels and promotion of competition culture and policy convergence at the international level).

23

Eurobarometer Standard Qualitative Study – DG Competition Stakeholder Survey (2014), Aggregate Report p. 42, to be published in 2015,

http://ec.europa.eu/competition/publications/reports/surveys_en.html

24

Flash Eurobarometer 403 – Citizens’ Perception about Competition Policy (2014) to be published in 2015 p. 7, http://ec.europa.eu/competition/publications/reports/surveys_en.html According to the survey, across the EU as a whole, problems resulting from a lack of competition are most likely to have occurred in the energy sector (28%), followed by transport services (23%) and pharmaceutical products (21%). Lower numbers are identified in the telecommunications and Internet sector (18%), food distribution (14%) and financial services (12%).

25

Eurobarometer Standard Qualitative Study – DG Competition Stakeholder Survey (2014), Aggregate Report p. 44, to be published in 2015,

15 General objective 1: To enhance consumer welfare in the EU and efficiently functioning markets by protecting competition

programme-based (please name the related spending programme)

⌧ Non programme-based

Impact indicator 1: Benchmark for the observable customer benefits resulting from Commission decisions prohibiting cartels and from corrective horizontal merger decisions.

Rationale: Quantitative indicator to ensure positive impact of competition enforcement on consumer welfare

Source: DG Competition calculation

Baseline (2013) Target (2015)

Cartel prohibition decisions26: EUR 4.89-5.66 bn Horizontal merger decisions27: EUR 0.3-0.7 bn

Stable level

26

The approach followed to benchmark the observable customer benefits from discontinuing a cartel (prevented harm) consists in multiplying the assumed increased price brought about by the cartel (called the “overcharge”) by the value of the affected products or markets and then by the likely duration of the cartel had it remained undetected. A 10% to 15% overcharge is assumed. This is conservative when compared to the findings of recent empirical literature which report considerably higher median price overcharges for cartels. In order to estimate what the likely duration of the cartel would have been if it had continued undetected, a case-by-case analysis was carried out. This analysis focussed on the particular circumstances of each case and an assessment of important quantitative indicators, including the specific market conditions, the lifespan of the cartel, the ease of reaching and renewing cartel agreements as well as the potential reactions of outsiders (such as new entrants). The cartels are classified into three categories: "unsustainable", "fairly sustainable" "very sustainable". It is assumed that the cartels in the first category would have lasted one extra year in the absence of the Commission's intervention, the cartels in the second category 3 years, and the cartels in the third group 6 years. The assumptions concerning the likely duration of the cartels are made prudently to establish a lower limit rather than to estimate the most likely values. Finally, the estimates obtained are also conservative because other consumer benefits, such as innovation, quality and choice are not taken into account.

Financial services:

The consumer benefit calculation for the cartels is based upon the termination of the cartels in their entirety. Moreover, the methodology for the calculation of the consumer benefits in financial services was adjusted to reflect the specificities of the financial markets, namely the calculation of overcharge. This adjustment led to a substantial decrease in the consumer benefits compared to the calculation with the default parameters used for non-financial industries. See DG Competition Annual Activity Report 2013, p. 38 http://ec.europa.eu/atwork/synthesis/aar/doc/comp_aar_2013.pdf

27

The approach followed to benchmark the observable customer benefits from the Commission’s intervention in the form of a prohibition of a horizontal merger or a clearance of such a merger subject to remedies consisted in predicting the change in consumer surplus. The prevention of anticompetitive effects such as the negative impacts on innovation and choice, even though some cases are also largely based on non-price effects, especially effects on innovation, are not taken into account. In practical terms, the calculation of the predicted change in consumer surplus arising from the Commission's intervention in each product market is based on three factors: (i) the total size (by value) of the product market concerned, (ii) the likely price increase avoided and (iii) the length of time that this market would have taken to self-correct either by the arrival of a new entrant or by the expansion of existing competitors. The expected price increase is set at 3-5%, a value in line with current academic literature, albeit a conservative estimate. The lower boundary of the estimate is based upon a 3% price increase lasting for two years, the higher boundary upon a 5% price increase for a duration depending on the barriers to entry of the affected market. The stable target is a planning assumption. As the merger control activity is driven by notifications, it is not possible to provide a clear target for this indicator.

16

Impact indicator 2: Success rate before the European Courts in competition cases

Rationale: Indicator for the quality of enforcement decisions following the review by the European Courts

Source: Legal Service statistics as reported annually to the Global Competition Review28

Baseline (2012) Target (2015)

79% (State aid);

90% (antitrust and mergers)

70%

Impact indicator 3: Impact of competition policy and enforcement on the markets Rationale: Qualitative indicator to estimate long-term market impact of competition enforcement

Source: DG Competition Stakeholder Survey29

Baseline (2014) Target (Next survey foreseen in 2019)

4.8 (scale 1-7) Increasing trend

Impact indicator 4: Impact of competition enforcement on economic growth

Rationale: Qualitative indicator to indicate the long-term impact of competition enforcement as an accelerator of economic growth

Source: DG Competition Stakeholder Survey30

Baseline (2014) Target (Next survey foreseen in 2019)

3.6 (scale 1-5) Increasing trend

3.2.

To promote competition culture in the EU and worldwide

DG Competition engages in advocacy activities and promotes competition culture in the EU and world-wide. This section outlines the main types of activities DG Competition carries out to foster competition culture. Maintaining and strengthening the Commission’s reputation world-wide and promoting international cooperation in this area is also defined as a priority for the new Commission in the field of competition policy31.

Contributing to competition-friendly EU legislation

DG Competition uses its sector and market knowledge to contribute to other Commission policy initiatives and regulation. The main purpose is to shape the regulatory framework and policy initiatives in a competition-friendly way.

Fostering convergence and cooperation between competition authorities across the globe The multiplication of jurisdictions with competition legislation and enforcement mechanisms has been on one hand a positive development and evidence of the global recognition of the

28

As reported in http://globalcompetitionreview.com/surveys/article/36089/european-unions-european-commission-directorate-general-competition/

29 Eurobarometer Standard Qualitative Study – DG Competition Stakeholder Survey (2014), Aggregate

Report p. 44, to be published in 2015,

http://ec.europa.eu/competition/publications/reports/surveys_en.html

30 Eurobarometer Standard Qualitative Study – DG Competition Stakeholder Survey (2014), Aggregate

Report p. 48, to be published in 2015,

http://ec.europa.eu/competition/publications/reports/surveys_en.html

31

Mission letter to the Commissioner of Competition Vestager by President Juncker 1 November 2014. http://ec.europa.eu/commission/sites/cwt/files/commissioner_mission_letters/vestager_en.pdf

17

importance and benefits of healthy competition. On the other hand, diverging competition regimes present a challenge to international businesses.

The Commission seeks to reinforce the role of competition policy in international economic cooperation and cooperates with competition agencies globally. Such regulatory and enforcement cooperation helps to ensure a level playing field for European companies on global markets. At bilateral level, the Commission engages in a wide range of cooperation activities with competition authorities in third countries on the basis of bilateral agreements or Memoranda of Understanding. The Commission is also active in international competition-related fora such as the Competition Committee of the OECD, the International Competition Network (ICN), the WTO and UNCTAD raising the awareness of European competition policy priorities.

Explaining competition policy and its benefits

Knowledge of the benefits of competition is essential for citizens to exploit their opportunities as consumers, for businesses to compete on the merits and for policy makers to bring initiatives that support smart, sustainable and inclusive growth as well as to be efficient and non-distortive market operators. Better understanding of the advantages of competition helps consumers make informed choices between products and services offered. It encourages businesses to refrain from anti-competitive agreements and behaviour. It makes public administrations better understand how competition can contribute to addressing wider economic problems. Explaining competition policy and demonstrating its benefits to citizens and stakeholders at all levels is also defined as a priority for the new Commission in the field of competition policy32.

To examine EU citizens’ perceptions of competition and possible lack of competition in certain sectors and knowledge about, and sources of information on, competition policies and decisions, DG Competition launched in 2014 Flash Eurobarometer Citizens’ Perception about Competition Policy33. According to the results of the survey, more than 80% of EU citizens believe that competition between companies can lead to better prices, more choice, innovation and economic growth. On the question used as an indicator, 74% of EU citizens respond that effective competition has a positive impact on them as a consumer. The citizens form their opinion based on information from multiple sources, mostly television and newspapers (over 60% according to the same survey), which also sets the framework for the Commission's communication efforts in this context34. DG Competition plans to share the results of the survey with national competition authorities in the European Competition Network (ECN) for the benefit of competition advocacy efforts by the Commission and the national competition authorities.

32 Mission letter to the Commissioner of Competition Vestager by President Juncker 1 November 2014.

http://ec.europa.eu/commission/sites/cwt/files/commissioner_mission_letters/vestager_en.pdf

33 Flash Eurobarometer 403 – Citizens’ Perception about Competition Policy (2014) to be published in

2015, http://ec.europa.eu/competition/publications/reports/surveys_en.html See also Flash EB 264 EU citizens’ perceptions about competition policy (2009), http://ec.europa.eu/competition/publications/reports/surveys_en.html

18 General objective 2: To promote competition culture in the EU and worldwide

programme-based (please name the related spending programme)

⌧ Non programme-based Impact indicator 1: Promotion of competition culture

Rationale: Qualitative indicator to estimate the success of DG Competition's advocacy activities Source: DG Competition Stakeholder Survey35

Baseline (2014) Target (Next survey foreseen in 2019)

4.9 (scale 1-7) Increasing trend

Impact indicator 2: Percentage of positive replies in surveys conducted among citizens agreeing that effective competition has a positive impact on them as consumers

Rationale: Indicator to measure citizens' view of competition Source: Eurobarometer Citizens' Survey36

Baseline (2014) Target (Next survey foreseen in 2019)

74% Increasing trend

35 Eurobarometer Standard Qualitative Study – DG Competition Stakeholder Survey (2014), Aggregate

Report p. 53, to be published in 2015,

http://ec.europa.eu/competition/publications/reports/surveys_en.html

36

Flash Eurobarometer 403 – Citizens’ Perception about Competition Policy (2014), p. 6, to be published in 2015, http://ec.europa.eu/competition/publications/reports/surveys_en.html

19

P

ART4.

S

PECIFIC OBJECTIVES FOR OPERATIONALABB

ACTIVITIES DG Competition has the following operational activities:• Control of State aid;

• Cartels, antitrust and liberalisation; • Merger control;

• Policy coordination, European Competition Network and international cooperation. DG Competition has a two-dimensional instrument-sector matrix organisation. DG Competition is comprised of ten Directorates (A to H, R and the Chief Economist's team). Five of the ten Directorates (the so-called “Markets and Cases Directorates”, i.e. Directorates B to F) have a sectoral focus on: energy and environment (Directorate B), information, communication and media (Directorate C), financial services (Directorate D), basic industries, manufacturing and agriculture (Directorate E) and health, transport, post and other services (Directorate F). Each of these sectoral Directorates is comprised of units specializing in the application of the main competition enforcement instruments (antitrust, merger control and State aid control, respectively) to the given sector. Directorate E also includes a Task Force, which investigates the food supply chain and food prices in more detail.

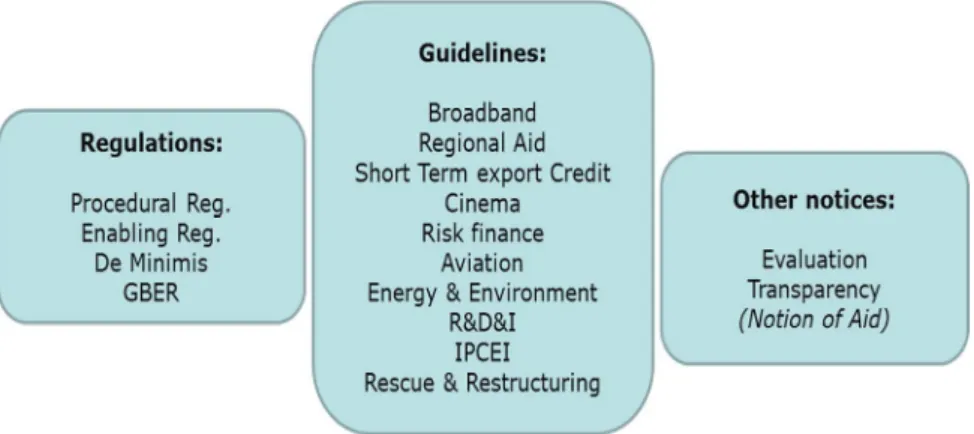

A separate Directorate (Directorate G) is dedicated to cartel enforcement. Directorate H is responsible for applying most of the horizontal (i.e. non-sector specific) State aid rules, such as those relating to regional aid, R&D&I aid, risk finance aid and fiscal aid. It is also in charge of enforcing recovery decisions and coordinating monitoring. The Directorate also includes a Task Force on Tax Planning Practices. Directorate A is in charge of policy for all competition enforcement instruments, in addition to the European Competition Network, international relations and private enforcement. Directorate R is in charge of document management, human resources management, financial management, IT, logistics and buildings and the management of issues related to security, ethics and business continuity.

4.1.

ABB Activity "Control of State aid"

State aid control is an integral part of EU competition policy and a necessary safeguard to preserve effective competition and free trade in the Single Market.

The Treaty establishes the principle that State aid which distorts or threatens to distort competition is prohibited in so far as it affects trade between Member States (Art. 107(1))37. However, State aid, which contributes to well-defined objectives of common European interest without unduly distorting competition between undertakings and trade between Member States, may be considered compatible with the internal market (under Art. 107(3)). In principle, any new aid that Member States intend to introduce has to be notified to and approved by the Commission before it can be implemented.

37

In addition, subsidies granted by EU Member States may also be subject to international agreements, such as the WTO subsidies agreement.

20

In principle, Member States need to notify aid measures and wait for Commission approval before implementing them. However, the procedural rules allow Member States also to notify aid schemes. Once cleared by the Commission, individual aid can be disbursed without prior notification under such schemes. In addition, the Commission has adopted Block Exemption Regulations (BER) allowing Member States to implement aid schemes without prior notification. Today, in volume terms close to 90% of aid awards are not individually examined by the Commission, but are granted on the basis of previously approved aid schemes or BER.

In addition to notification-based ex ante control, the Commission also monitors and reviews existing aid schemes (Art. 108(1)), i.e. aid schemes approved in the past and block-exempted schemes, to ensure compliance and to adapt them to market developments. When Member States grant State aid without prior notification, and such unlawful aid also turns out to be incompatible with the internal market, the Commission must order the Member State concerned to recover the aid from the beneficiaries.

In 2014, a major overhaul of EU State aid control was completed, and entailed inter alia a revision of almost all compatibility rules, the procedural regulation and the general block exemption regulation. In the broader context of the EU's agenda to foster growth, State aid policy facilitates well-designed aid targeted at market failures and objectives of common European interest. The Commission can now focus its enforcement activities on cases with the biggest impact on the internal market, streamlining rules and accelerating decisions. The objectives of DG Competition's control of State aid activity are to: i) ensure that aid is growth-enhancing, efficient and effective, and better targeted in times of budgetary constraints and where aid is granted, it does not restrict competition but addresses market failures to the benefit of society as a whole and ii) effectively prevent and recover incompatible State aid.

4.1.1.

Better targeted growth-enhancing aid

State aid can distort competition by giving some companies undue advantages over others. Therefore, the Commission will continue to apply increased scrutiny in order to tackle cases of "bad" aid. That is, public interventions that are not in line with State aid rules and which are considered not to contribute to common interest objectives and economic growth.

Where aid is granted, DG Competition seeks to ensure that it addresses market failures or equity objectives that have a beneficial impact on competitiveness, employment and growth, and thus on the welfare of society as a whole. Accordingly, DG Competition aims at ensuring that the aid is targeted at horizontal objectives of Community interest, such as regional development, employment, environmental protection, promotion of research and development and innovation, risk capital and development of SMEs. This is in line with the Europe 2020 Strategy, according to which "State aid policy can … actively contribute to the Europe 2020 objectives leading to a more sustainable, productive and growth oriented economy, by promoting and

21

supporting initiatives for more innovative, efficient and greener technologies, while facilitating access to public support for investment, risk capital and funding for research and development."38 The State aid Modernisation initiative aims at enhancing economic efficiency and the effectiveness of public spending and spurring growth on the Internal Market. It allows the Commission's State aid policy to focus on "good" aid, in line with the Commission's wider objectives. It also contributes to focus State aid scrutiny on the most distortive cases by, in particular, enlarging the scope of application of the General Block Exemption Regulation (GBER) which removes the notification obligation for Member States.

Energy and environment

State aid control in the areas of energy and environment is an important part of competition policy, as it contributes to creating conditions for sustainable use of resources and thereby to fulfilling the Europe 2020 goals.

As part of the State aid modernisation package, the new Energy and Environmental Aid Guidelines (EEAG) entered into force on 1 July 2014 to reflect the Commission's knowledge in the field and the latest technological and market developments. The new EEAG have brought the assessment criteria in line with the common principles underlying other State aid guidelines. EEAG also simplified and revised the assessment of several existing aid categories, notably aiming at making RES support schemes more market oriented. Finally, EEAG have introduced new aid categories, enlarging their scope to energy infrastructure, capacity mechanisms and aid for energy intensive users compensating them for the financing RES costs. The new EEAG thus reflect the closer link between environmental and energy policies and have therefore been renamed to also include energy.

During 2014, Member States continued to extensively promote renewable energy sources (RES) to achieve the national RES and CO2 reduction targets by 2020 and beyond. Based on the provisions of the 2008 Environmental Aid Guidelines (EAG) and, since mid-2014, of the new Energy and Environmental Aid Guidelines (EEAG), the Commission adopted a high number of decisions in this area. Those Commission decisions aim at avoiding over-compensation and competitive distortions through the RES schemes. Furthermore, in line with the EU's energy and climate change objectives, the Commission has positively assessed a number of Member States' interventions aimed at energy efficiency, better infrastructure including the modernisation of district heating and aid to high efficiency co-generation installations. The Commission has also taken its first decision on a capacity mechanism which concerns the United Kingdom. To enhance competition and ensure a level playing field in the energy sector, the Commission also closed several in-depth investigations39. In 2015, the Commission will continue to assess Member States'

38

EUROPE 2020 A European strategy for smart, sustainable and inclusive growth, p. 19,

http://ec.europa.eu/eu2020/pdf/COMPLET%20EN%20BARROSO%20%20%20007%20-%20Europe%202020%20-%20EN%20version.pdf

39

Decisions concerned the granting of aid for the construction of the nuclear power plant at Hinkley Point in the United Kingdom and the German Renewable Energy Act (EEG) including relief of energy intensive users from the RES financing.

22

interventions with the horizontal objectives of promoting the internal energy market and environmental protection. The focus will be on reforming RES support schemes in line with the new EEAG provisions, on investigating existing and planned capacity mechanisms and on assessing fossil fuel subsidies.

Telecoms sector

State aid also contributes to the Commission's objectives on the Digital Single Market. The Commission State aid decisions complement private investments in areas which are not profitable on commercial terms and are necessary to achieve those objectives, when it is established that the measures are pro-competitive. As regards the market for broadband, telecoms and related markets, DG Competition is actively pursuing a number of investigations, in order to ensure that aid is targeted and meets the criteria to foster an optimal infrastructure market in the EU.

In 2015, the Commission will continue to ensure compliance of its 2013 and 2014 decisions concerning less-populated areas in all Spanish regions, enforcing the principle of technological neutrality. The Commission will continue its pending investigation regarding alleged compensation to private broadcasters for the liberation of the first digital dividend in Spain as well as the investigation regarding the presumed aid to Numéricable in France allegedly benefitting from a telecoms infrastructure for free.

Regarding the audio-visual sector, the Commission will pursue the formal investigation opened in 2014 into a German aid scheme for the benefit of video on demand distribution which is financed by parafiscal levies charged on domestic but also foreign video on demand distributors.

Finally, the Commission will pursue the ongoing investigation of existing aid to the Polish broadcaster TVP on the basis of new legislation and new public service remits that are being designed in order to comply fully with the requirements of the Broadcasting Communication.

Financial sector

Since the crisis started, the European Union used State aid rules as a substitute for the lacking resolution tools in the EU, a shortcoming that will be solved by the establishment of the Single Resolution Board on 1 January 2015 (see below in section 4.4.1.1). Up to 30 September 2014, the Commission oversaw the restructuring of 111 banks – equivalent to around one quarter of Europe’s banking sector in terms of assets – out of which 33 had to be liquidated. The task is not finished, with 12 ongoing cases at present.

In 2014, the situation in the financial markets improved as banks were able to raise significant amounts of capital through various means. Nevertheless, additional effort is still needed to consolidate the positive signs of recovery. The activity of DG Competition in the area of State aid control ensured a consistent policy response to the financial crisis throughout the EU, and significantly contributed to limiting distortions of competition between beneficiary financial institutions within the internal market, while at the same time limiting the use of taxpayers' money to the minimum necessary. Of particular relevance was the activity in the context of the programs in Greece, Ireland, Portugal, Spain and Cyprus. Also, the emergency decisions adopted

23

for some Bulgarian Banks and the Portuguese Banco Espirito Santo as well as the restructuring decisions for major Greek Banks should be noted. Significant activity was also devoted to monitoring the correct implementation of the over 66 restructuring decisions adopted since the beginning of the crisis. In addition, DG Competition was intensely involved in numerous transversal tasks relating to the future establishment of the Single Resolution Board, the implementation by Member States of burden sharing as required under the State aid rules, and the negotiations of the Banking Recovery and Resolution Directive, Deposit Guarantee Schemes Directive and the Single Resolution Mechanism regulation for their State aid related aspects. In 2015, the levels of activity are likely to remain very high in countries undergoing an adjustment program, but also across the Union more broadly, the outcome of the comprehensive assessment exercise published on 26 October 2014, and the work resulting from the cooperation with the Single Resolution Board that will become operational as from 1 January 2015.

Transport

In the field of air transport and airports, the Commission will ensure in 2015 a proper implementation of the guidelines on State aid to airports and airlines40 which entered into force on 4 April 2014. In particular, the Commission will analyse the notifications regarding operating aid to regional airports and will verify that the phasing out of such aid is correctly implemented. As regards maritime transport, the Commission will advance ongoing investigations notably concerning Malta and Greece. In the field of rail transport, the Commission will in 2015 continue investigations to check that incumbent companies do not benefit from unjustified financial advantages constituting barriers to entry for new competitors. The Commission will verify that rail companies do not benefit from overcompensation when operating services of general economic interest.

Taxation

In the context of the current economic crisis and the fiscal issues faced by EU Member States, and against the background that around one trillion euros is lost to tax evasion and avoidance every year in the EU41, fighting tax fraud, tax evasion and tax avoidance has been recognized as one of the major priorities of President Juncker for the years to come.

Tax evasion and tax avoidance can be the result of aggressive tax planning, which is a means of reducing tax liability by shifting profits to jurisdiction where they are not or only to a limited extent subject to tax. Aggressive tax planning can amongst others be pursued by making use of preferential tax schemes, for example coordination centres42 or by individual tax rulings. They all have in common that they result in a loss of tax revenue in the Member State where economic value is created but not taxed, and in Europe as a whole because the tax eventually paid is less than it would be at the place where the economic value is created. This presents a social equity

40 OJ C 99 of 4.4.2014, p. 3.

41

http://europa.eu/rapid/press-release_IP-12-1325_en.htm

42

See for instance Commission Decision 2003/757/EC of 17 February 2003, Belgian Coordination centres, (OJ L 282, 30.10.2003). The Commission announced in 2014 its intention to replace the guidelines in the consolidated notion of aid communication.

24

issue, as the revenues foregone from untaxed multinationals need to be compensated, which normally increases the burden on less mobile income of SMEs and from labour.

Furthermore, from the perspective of the dislocation of activities, aggressive tax planning can present a threat to the sustainable growth of the internal market if some Member States were to offer exit points for the entirety of European profits of multinationals in exchange for the creation of some jobs on their territory and a limited tax payment.

On this basis the focus of the Commission's State aid investigations in 2015 will remain on direct business taxation (corporate tax) measures that provide a selective advantage to individual undertakings or specific sectors, such as lower taxation levels accepted by Member States for individual companies by way of tax rulings, tax exemptions for state owned companies, of lower tax levels or tax breaks for certain sectors or activities.

In 2014 the Commission opened four cases on tax rulings regarding Apple (Ireland), Fiat Finance & Trade and Amazon (Luxembourg) and Starbucks (Netherlands) and it will continue these investigations in 2015. In parallel, work on potential tax avoidance will continue in a number of areas, regarding individual cases and schemes, in line with the priorities of the agenda set by Commission President Juncker43. The Commission has also recently extended information enquiry on tax rulings practice to all Member States to get a full picture of the tax rulings practices in the EU to identify if and where competition in the Single Market is being distorted through selective tax advantages.

Regional aid

Regional aid is an important instrument in the EU's toolbox to promote greater economic and social cohesion. With the adoption of the GBER and the approval of the new regional aid maps for the 28 Member States in the course of 2014, the framework for regional State aid in the period 2014-2020 is complete.

Although the scope of the new GBER has been further widened in the area of State aid, there are still a range of regional aid measures that will need to be notified to and assessed by the Commission (sectoral aid schemes, aid to large investment projects, aid to investment in new products and new process innovations, aid to investment by companies that have closed down or intend to close down the same or similar activities elsewhere in the EEA, notification of evaluation plans). Based on past experience, DG Competition expects Member States to start submitting such new notifications from 2015 onwards.

In addition, DG Competition is deeply involved in the analysis of the competition aspects (mainly State aid aspects) of the partnership agreements and the operational programmes submitted by Member States in the context of the new programming period for the European Structural and Investment (ESI) Funds. DG Competition will also be co-operating closely with the ESI Fund related Commission services to build up know-how on State aid policy in the managing authorities of the Member States to ensure that co-financed operations are implemented in

25

compliance with State aid rules. A special effort will be needed to provide clear guidance on the State aid aspects of large infrastructure projects co-financed by the ESI Funds.

R&D&I

One of the headline targets of Europe 2020 strategy is for R&D&I investments in the EU to reach 3% of GDP. Smart and sustainable growth also depends on the potential to innovate. State aid rules are designed to activate the EU's potential to invest in more and better R&D&I. With this in view, the Commission has adopted a new R&D&I Framework and new provisions for R&D&I aid under the GBER, both of which entered into force on 1 July 2014. The objective of this reform is to pave the way for Member States to support R&D&I more frequently and efficiently, to mobilise additional private investment, and to promote collaboration between academia and industry as well as carry out public procurement of R&D, including pre-commercial procurement, without uncertainty about the presence of any indirect aid to industry. The new rules are designed to go hand in hand with other EU initiatives aimed at promoting R&D&I activities, such as Horizon 2020.

In parallel to this policy reform, the Commission has continued to deal, during 2014, with a significant number of notifications concerning both horizontal schemes and large individual aid measures. As regards the latter, seven important decisions have been adopted in 2014 authorising R&D&I aid in strategic sectors such as ITC, aerospace, energy and key enabling technologies (KETs). Some of these decisions required significant changes to the originally notified measures with a view to ensuring well-designed and proportionate aid, while minimising its potential negative effects on competition. Following the entry into force of the new rules, it is to be expected that a larger number of measures will fall under the GBER.

Risk Finance

Following extensive consultations with Member States and stakeholders, the Commission has set up a simpler, more flexible and generous State aid framework for the provision of risk finance to SMEs and mid-caps. The new rules are contained both in the new Risk Finance Guidelines and in the new GBER, both of which entered into force on 1 July 2014. Their aim is to attract and channel private financing to support the public policy goals of economic growth and job creation, which is particularly important in times of economic crisis. By enhancing the incentives of private sector investors - including institutional ones – to invest and increase their funding activities in this critical area of SME financing, the new rules mirror other EU initiatives designed to promote wider use of financial instruments in the context of new support programmes such as Horizon 2020 or COSME.

Moreover, in 2014, the Commission continued to apply the existing rules on risk capital aid, as well as in the area of urban regeneration, by adopting some 15 decisions including one complex case which could be cleared only after the opening of formal proceedings. The entry into force of the new rules, which have substantially enlarged the scope of the block exemption, will enable the Commission to focus its attention on measures that may seriously harm competition or fragment the internal market.

26

Other sectors

Work will continue on State aid enforcement in the area of sports, including on the ongoing investigations into alleged aid to several professional football clubs in The Netherlands and Spain. Other aid schemes and ad hoc interventions in the sports sector, which were not notified but have been brought to the Commission's attention by other means, will be taken up with the Member States for further assessment.

In the health care sector, the Commission will continue the formal investigation procedure, initiated in October 2014, into the financing of the public hospitals of the IRIS network in the Brussels-Capital region.

In the postal services sector, the trend of privatisations of incumbent operators could continue as projects exist in Romania, Greece and Italy to privatise part of the national incumbent operator. The Commission will also continue the formal investigation initiated in August 2014 regarding a compensation fund mechanism to finance the Universal Postal Service provided by ELTA in Greece for the years 2015-2019. Such funds, put in place in several Member States, would in general amount to State aid and have the potential to excessively distort competition if they impose disproportionate and/or discriminatory contributions on competitors of the universal service providers.

In the current transition period related to the State Aid Modernisation package, including new transparency rules applicable to Member States, DG Competition reflects on potential new result indicators for this ABB activity and continues to report on the activity by using existing indicators.

Relevant general objective(s): To enhance consumer welfare in the EU and efficiently functioning markets by protecting competition

Specific objective 1: Better targeted growth-enhancing aid programme-based (please name the related spending programme)

⌧ Non programme-based Result indicator 1: Overall level of non-crisis State aid granted by Member States to industry and services; expressed by percentage of GDP

Rationale: Indicator to benchmark the level of State aid44 in the EU economy Source of data: State Aid Scoreboard and DG Competition calculation

Link: http://ec.europa.eu/competition/state_aid/scoreboard/index_en.html

Baseline (2013) Target

0.45% Decrease45

44 Notified State aid. 45

Due to overall changes implemented as part of State Aid Modernisation (SAM), as well as Renewable Energy Sources (RES) and fiscal related state aid programs, the previous benchmarks will not be fully comparable. After the transition period of SAM implementation has ended, the indicators, baselines and targets will be reviewed and updated.

27

Result indicator 2: Overall level of crisis aid to the financial sector actually used by Member States, expressed as percentage of 2013 EU 28 GDP

Rationale: Indicator to measure the gradual phasing out of crisis aid measures of temporary nature and the linked risk of competition distortion in the financial services.

Source of data: State Aid Scoreboard and DG Competition calculation Link: http://ec.europa.eu/competition/state_aid/scoreboard/index_en.html

Baseline (2013) Target

8.1%46 Phasing out as soon as economic recovery

allows

Result indicator 3: Percentage of State aid granted by Member States for horizontal objectives of common interest.

Rationale: Indicator to ensure that state aid is targeted at horizontal objectives of Community interest, such as regional development, employment, environmental protection, promotion of research and development and innovation, risk capital and development of SMEs.

Source of data: State Aid Scoreboard - The information is based on the annual reports provided by Member States pursuant to Article 6(1) of Commission Regulation (EC) 794/2004 and comprises expenditure granted by Member States through existing aid measures which fall into scope of Article 107(1) TFEU.

Link: http://ec.europa.eu/competition/state_aid/scoreboard/index_en.html

Baseline (2013) Target

85.1% Increase47

Output Indicator 1: Number of opening decisions

Rationale: Indicator to demonstrate level of enforcement activity also for deterrence purpose Source of data: DG Competition case management system (ISIS)

Baseline (2013) Target

45 No target48

4.1.2.

Prevention and recovery of incompatible aid

DG Competition's State aid control activity also aims at ensuring effective prevention and recovery of incompatible State aid in order to prevent that Member States re-create artificial barriers to intra-community trade.

46

This consists of the following two components (calculated as % of EU GDP 2013): total recapitalisation and asset relief measures 2008-2013: EUR 661.4 billion (5.1 %); outstanding guarantees and liquidity measures for 2013: EUR 386.9 billion (3.0 %).

47

State Aid Modernisation (SAM) has changed the scope of sectorial aid and, consequently, the previous benchmarks will not be fully comparable. After the transition period of SAM implementation has ended, the indicators, baselines and targets will be reviewed and updated.

48 As far as merger and State aid enforcement is concerned, DG Competition's activities are largely driven

by notifications by companies and Member States. It is therefore not meaningful to identify a target. As far as antitrust and cartel enforcement is concerned, it would not be possible to formulate a numerical target as such target would depend on the number of infringements (which could be lower