Association for Information Systems

AIS Electronic Library (AISeL)

PACIS 2013 Proceedings

Pacific Asia Conference on Information Systems

(PACIS)

6-18-2013

Exploring the Influence of Trust on Mobile

Payment Adoption

Hua Xin

Auckland University of Technology, [email protected]

Angsana A. Techatassanasoontorn

Auckland University of Technology, [email protected]

Felix B. Tan

Auckland University of Technology, [email protected]

Follow this and additional works at:

http://aisel.aisnet.org/pacis2013

This material is brought to you by the Pacific Asia Conference on Information Systems (PACIS) at AIS Electronic Library (AISeL). It has been accepted for inclusion in PACIS 2013 Proceedings by an authorized administrator of AIS Electronic Library (AISeL). For more information, please [email protected].

Recommended Citation

Xin, Hua; Techatassanasoontorn, Angsana A.; and Tan, Felix B., "Exploring the Influence of Trust on Mobile Payment Adoption" (2013).PACIS 2013 Proceedings.Paper 143.

EXPLORING THE INFLUENCE OF TRUST ON

MOBILE PAYMENT ADOPTION

Hua Xin, Faculty of Business and Law,

Auckland University of Technology, Auckland, New Zealand, [email protected]

Angsana A. Techatassanasoontorn, Faculty of Business and Law,

Auckland University of Technology, Auckland, New Zealand, [email protected]

Felix B. Tan, Faculty of Business and Law,

Auckland University of Technology, Auckland, New Zealand, [email protected]

Abstract

The objective of this study is to explore antecedents of trust and the influence of trust on intention to use mobile payments. The research examines three dimensions of trust antecedents including trust perceptions of the mobile service provider, the mobile payment vendor and mobile technology. The results are based on a survey sample of 302 participants. PLS-SEM is employed in the data analysis. Results reveal that trust is a crucial factor of consumer’s intention to adopt mobile payment. Results highlight that characteristics of the mobile service provider, mobile payment vendor and mobile technology influence the development of trust on mobile payment. In particular, consumer’s perceptions of structural assurance and environmental risks of mobile technology have strong influence on mobile payment trust. Results also highlight that consumers’ perceived reputation of the mobile service provider and mobile payment vendor positively relate to mobile payment trust.

1

INTRODUCTION

Advanced Information and Communication Technologies (ICT), such as smart phones and ubiquitous Internet access, increase the mobility of individual’s life activities. The growth in mobile phone subscriptions has led to an increase in mobile applications, social networking and online games, as well as a growing consumer interest in mobile payments. Mobile payment is defined as a type of payment transaction processing in which a mobile device is utilised to initiate, authorise, confirm and complete a payment (Goeke & Pousttchi 2010). Mobile payments fall broadly into two categories:

point of sale (POS) contactless payments and mobile remote payments. The first requires both buyer’s and seller’s presence to complete transactions. Technology applied here is contactless radio technologies including near field communication (NFC), Bluetooth or infrared technologies. The latter represents payment that is made through either SMS (e.g., paying for car parks or paying at petrol stations) or wireless application protocol (WAP) (e.g., using mobile Internet to make a purchase).

Research shows that mobile payment has a promising future and firms should invest in the development and promotion of this payment method (Microsoft & M-com 2009). However, Pope et al.’s study (2011) suggests that mobile payment is still in its infancy. Similarly, MasterCard (2012a) conducted the study in 34 countries and reported that none of the countries has reached an inflection point in which mobile payments account for a major share of payments mix. To achieve a successful implementation of mobile payment services, it is crucial to understand the extent of consumers’ knowledge of mobile payments and their concerns about mobile payments. A review of mobile payment studies suggests that consumers express great concerns about privacy and security in mobile payments (Au & Kauffman 2008). Therefore, mobile payment systems should be designed to foster consumer confidence, reduce their uncertainties and perceived risks to increase the likelihood of wider consumer acceptance. Trust, in general, is an important factor that could reduce uncertainties and perceived risks in social or economic interactions especially when making important decisions or adopting new technology (Gefen 2000). Trust has found to be an important factor across technological contexts such as e-commerce (Gefen et al. 2003; Suh & Han 2003) and mobile commerce (Kim et al. 2009; Liu et al. 2009; Yang & Mao 2011). We believe that, to have a successful implementation of a mobile payment service, it is crucial to understand how consumers develop trust. In this study, we explore the antecedents of consumer trust in mobile payment systems.

However, there is a limited understanding of the antecedents of trust in a mobile payment system. Most previous studies on mobile payment adoption have treated consumer trust as a general construct (Andreev et al. 2012; Keramati et al. 2012; Mallet 2007; Shin 2010). Chandra et al. (2010) propose a trust-theoretical model that has two dimensions of consumer trust in the mobile payment system. These are consumers’ trust perceptions of mobile payment service providers and mobile technology. We believe that a mobile payment vendor, whom customers make payment to, is another entity that can influence consumer trust in mobile payment systems. This is because consumers are willing to make monetary transactions only with well-known and established businesses (Dahlberg et al. 2003). Andreev et al. (2011) found that consumer’s trust in mobile payment vendors is important in the decisions to adopt mobile payment. Chandra et al. (2010) also stated that the role of vendors is important in the mobile payment system. They suggest that future research should include consumers’ trust perception of vendors in the model. To address this gap in the literature, this research adds consumers’ trust perceptions of mobile payment vendors as an additional construct to Chandra’s proposed trust model. The objective of this study is to evaluate how characteristics of mobile service providers, mobile payment vendors and mobile technology shape the development of consumer trust in mobile payment. The research questions are:

1. What constitutes consumer trust in mobile payment?

2. What is the influence of characteristics of mobile payment vendors in the development of consumer trust in mobile payment?

2

RESEARCH MODEL AND HYPOTHESES DEVELOPMENT

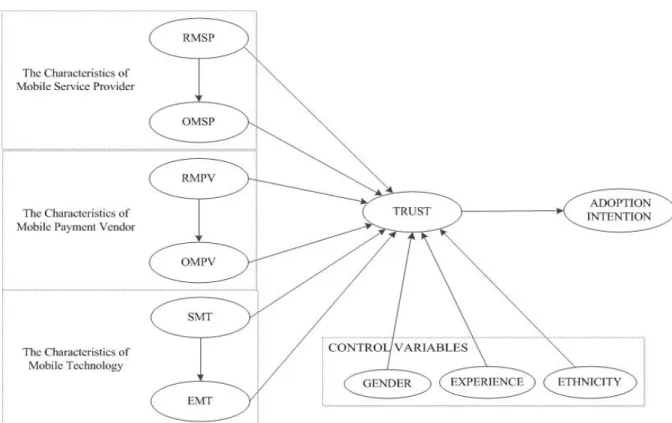

2.1 Research Model

A lack of trust is considered to be an obstacle to consumer’s technology adoption. The concept of trust can be defined with three characteristics. First, trust involves a dyadic relationship between a trustor and a trustee (Grazioli & Jarvenpaa 2000). The two parties rely on each other for mutual benefit (Siau & Shen 2003). There are three main entities in a mobile payment system: a mobile service provider (e.g., Vodafone, AT&T, Sprint), a mobile payment vendor (e.g., retail shops, supermarkets, cafés) and mobile network technology (e.g., 3G). In the context of this study, consumers and mobile payment trading partners (mobile service providers and mobile payment vendors) are forming a trustor and trustee relationship. Consumers expect that mobile service providers and mobile payment vendors will fulfil their expectations without taking advantage of their vulnerabilities (Chandra et al. 2010).

Second, trust involves risk and uncertainties (Siau & Shen 2003). There are no guarantees that mobile service providers and mobile payment vendors will live up to consumers’ expectations. Consumers may have concerns on possible opportunistic behaviours of mobile service providers and mobile payment vendors that may cost the loss of their privacy and money.

Third, the trustor (consumers) has faith in the trustee’s (mobile service providers and mobile payment vendors) integrity, honesty and benevolence (Mayer et al. 1995; Siau & Shen 2003). In addition to these three aspects of trust, mobile technology, as an enabler of mobile payment transactions, also plays a vital role in the development of consumer trust. In the early stage of mobile payment adoption, disappointing performance of mobile wireless technology (e.g., network breakdown in the middle of a transaction) will cause doubt from consumers on its ability to deliver consistent, reliable and secure performance (Siau & Shen 2003). Therefore, it is important to consider the influence of mobile technology as one of the factors that shapes trust in mobile payment.

According to Zucker’s (1986) trust production theory, the building of trust is mainly based on three modes. The first mode of trust production is characteristic-based trust, which pertains to the characteristics of trustees (mobile service providers and mobile payment vendors). This mode of trust involves a consumer’s belief in the integrity, ability, and benevolence of the mobile service providers and mobile payment vendors. The second mode of trust is the process-based trust,which relates to consumer’s experience with mobile service providers or mobile payment vendors. The last mode is the institutional-based trust, which relates to established guidelines in a mobile payment system (i.e., legal frameworks, third party guarantees). In the early adoption stage, consumers have not had any interactions with mobile service providers or mobile payment vendors in a mobile payment system. Therefore, the process mode of trust production is not relevant to the initial trust building process in mobile payment. In other words, the early stage of mobile payment trust is developed mainly through the characteristics of trustees (mobile service providers and mobile payment vendors) and the institutional based trust. McKnight et al. (2002) theorised that structural assurance and situation normality constitute institutional-based trust. Since mobile payment is a relatively new service, consumers may not familiar with the procedures and the environment of this payment method. As a result, they may not have a good knowledge about a normal situation of mobile payment. Therefore, situation normality is not highly relevant to the trust building process at the early stage of mobile payment adoption. In this research, we will examine institutional-based trust through the structural assurance of mobile technology.

This study extends the trust model in Chandra et al. (2010) by incorporating characteristics of the mobile payment vendor as an additional dimension of consumer trust in a mobile payment system. The research model is presented in Figure 1. Table 1 presents the definitions of key constructs.

Figure 1. Research Model

Construct Definition Reference

Perceived reputation of mobile service provider (RMSP)

The extent to which consumers believe in the mobile service provider’s competency, honesty, and benevolence

Chandra et al. (2010) Perceived opportunism

of mobile service provider (OMSP)

Possible opportunistic behaviour of the mobile service provider in relation to the consumer. It refers to the consumer’s risk in

transacting with a mobile service provider who might inappropriately exploit the consumer’s vulnerabilities.

Chandra et al. (2010)

Perceived reputation of mobile payment vendor (RMPV)

The extent to which consumers believe in the mobile payment vendor’s competency, honesty and benevolence.

New construct, adapted from Chandra et al. (2010) Perceived opportunism of mobile payment vendor (OMPV)

Possible opportunistic behaviour of the mobile payment vendor in relation to the consumer. It refers to the consumer’s risk in

transacting with a mobile payment vendor who might inappropriately exploit the consumer’s vulnerabilities.

New construct, adapted from Chandra et al. (2010) Perceived structural assurance (SMT)

The consumer’s perception about the institutional environment that all structures like guarantees, regulations, and promises are

operational for safe, secure and reliable transactions.

Chandra et al. (2010) Perceived

environmental risk (EMT)

Risk associated with the underlying technological infrastructure, which in the current study is the wireless mobile internet. Environmental risks refer to the transaction security related risks

faced by consumers while using a mobile payment service through a wireless network.

Chandra et al. (2010)

Consumer trust in mobile payment (TRUST)

The belief that mobile payment transactions will be accomplished reliably.

Sitkin & Roth (1993)

2.2 Hypotheses Development

2.2.1 Consumer Trust in Mobile Payment and Intention to Adopt Mobile Payment

Lack of trust is considered to be an obstacle to consumer’s technology adoption. Since mobile payment is a relatively new innovation, consumers may have uncertainties with its technology and operational environment (Chandra et al. 2010; Cyril et al. 2008). Some consumers may feel that they are in a vulnerable position because they have no control over transactions and their financial asset and privacy might be put at risk due to possible opportunistic behaviour made by trading partners (Chandra et al., 2010). Therefore, consumer trust plays a crucial role in the decision to adopt mobile payment. Previous studies on e-commerce and m-commerce consistently demonstrate that trust has a positive relationship with the intention to adopt technology (Chandra et al. 2010; Gefen et al. 2003; Liu et al. 2009; Yang & Mao 2011; Suh & Han 2003). Extending this logic to the mobile payment context, we believe that the higher level of trust the consumers place in mobile payment, the more likely their intention to adopt mobile payment will be. Thus we have:

H1: Consumer trust is positively associated with the intention to adopt mobile payment.

2.2.2 The Characteristics of the Mobile Service Provider

Chandra et al. (2010) identify two categories of mobile service provider characteristics that affect mobile payment trust: perceived reputation of the mobile service provider (RMSP) and perceived opportunism of the mobile service provider (OMSP).

RMSP is defined as “the extent to which consumers believe in the mobile service provider’s competency, honesty, and benevolence” (Chandra et al. 2010, p.565). When consumers do not have previous experience with a firm, they rely on its reputation to decide its trustworthiness (McKnight et al. 1998). Previous studies in e-commerce have shown that reputation of a firm positively associated with consumer online trust (Ba & Pavlou 2002; Koufaris & Hampton-Sosa 2004). Ba (2001) states that if consumers perceive a bad reputation of an online bank, they would be discouraged from conducting online transactions with that bank. In a mobile banking study, Liu et al (2009) also demonstrate a positive relationship between the reputation of a mobile banking service provider and consumer trust. Therefore, we posit that the reputation of a mobile service provider has a direct influence on consumer’s trust in mobile payment. Thus, we have:

H2a: Perceived reputation of the mobile service provider is positively associated with the level of consumer trust in mobile payment.

OMSP is defined as “possible opportunistic behaviour of the mobile service provider in relation to the consumer” (Chandra et al. 2010, p. 565). In some cases, a mobile service provider may engage in unethical behaviours such as distorting or disclosing information without notifying consumers. These actions may incur privacy or financial loss to consumers. If consumers have such negative experience with a mobile service provider, they tend not to believe or trust in mobile payment. Pavlou et al. (2007) report a negative relationship between a web vendor’s opportunism and consumer trust in online shopping. Mukherjee and Nath (2003) find that if consumers believe the bank is engaging or may engage in opportunistic behaviour, consumers are likely to lower their trust in online banking. By extending this logic to a mobile payment context, we argue that if consumers believe a mobile service provider may engage in an opportunistic behaviour, their trust in mobile payment will diminish. Therefore we propose:

H2b: Perceived opportunism of the mobile service provider is negatively associated with the level of consumer trust in mobile payment.

A good reputation of a firm is viewed as an asset to that firm. Siau and Shen (2003) claim that a good reputation of a firm implies the integrity of that business, thus fostering consumer trust in mobile commerce. Ba and Pavlou (2003) suggest that buyers believe that sellers with a good reputation are less likely to engage in dishonest or opportunistic behaviour on Bay. Previous research in e-commerce found a negative relationship between the reputation and the opportunism of a web vendor

in online shopping (Jarvenpaa et al. 1999). Chandra et al. (2010) also report similar findings in the mobile payment context. Therefore we have:

H2c: Perceived reputation of the mobile service provider is negatively associated with the level of perceived opportunism of the mobile service provider.

2.2.3 The Characteristics of the Mobile Payment Vendor

Mobile payment vendors refer to merchants that offer products or services along with a mobile payment option. The vendor and consumer form a seller and buyer relationship. Similar to Chandra et al. (2010), we examine the influence of perceived reputation of the mobile payment vendor (RMPV) and perceived opportunism of the mobile payment vendor (OMPV) on the formation of trust in mobile payment.

Gefen (2002) suggests that vendor trust in e-commerce consists of competence, integrity and benevolence. Applying this conceptualisation in mobile commerce, we define RMPV as the extent to which consumers believe in the mobile payment vendor’s competency, honesty and benevolence (Chandra et al. 2010; Gefen 2002). Previous IS research has shown a positive association between a seller’s reputation and the buyer’s trust in e-commerce (Gefen & Straub 2003; Jarvenpaa et al. 1999). Andreev et al. (2012) find a positive relationship between vendor trust and willingness to use mobile payment. Liu et al. (2009) also demonstrate that vendor trust positively associates with consumer trust in mobile banking. Therefore we have:

H3a: Perceived reputation of the mobile payment vendor is positively associated with the level of consumer trust in mobile payment.

OMPV refers to possible opportunistic behaviour made by a mobile payment vendor. Opportunistic behaviours include the trustee’s distortion of information and failing to fulfil promises and obligations made to the trustor (John 1984). In a study carried out by Grazioli and Jarvenpaa (2000), they find that perceived opportunistic behaviours made by Internet vendors weakens the relationship between trust in Internet vendors and trust in Internet shopping. If consumers perceive any opportunistic behaviour conducted by mobile payment vendors, they are likely to lower their trust in mobile payment. Therefore we have:

H3b: Perceived opportunism of the mobile payment vendor is negatively associated with the level of consumer trust in mobile payment.

Jarvenpaa et al. (1999) demonstrate that the perceived reputation of the Internet vendor is negatively correlated with opportunistic behaviours. They argue that Internet vendors with good reputations are perceived to be reluctant to put their reputations at risk by conducting opportunistic behaviours. Similar findings also are also supported by previous studies in online business (Ba & Pavlou 2002) and mobile commerce (Siau & Shen 2003). Extending this line of argument to mobile payment vendors, we believe that if consumers perceive a higher reputation of a mobile payment vendor, then they will perceive lower opportunism of that vendor. Therefore we have:

H3c: Perceived reputation of the mobile payment vendor is negatively associated with the level of its perceived opportunism.

2.2.4 The Characteristics of Mobile Technology

Consistent with Chandra et al.’s (2010) study, we examine two characteristics of mobile technology: perceived structural assurance (SMT) and perceived environmental risks (EMT). SMT is defined as “consumers’ perception about the institutional environment that all structures like guarantees, regulations, and promises are operational for safe, secure and reliable transactions” (Chandra et al. 2010, p.565). Structure assurance in the form of structures that can discourage possible opportunistic behaviour of the trustee parties (Kim et al 2009). Structural assurance is critical in shaping initial trust in technology and protecting consumers from uncertainties and risks (McKnight et al. 2002). Kim and Prabhakar (2004) argue that structural assurance plays a vital role in building up consumer trust especially in e-commerce. Previous studies in m-commerce find that structural assurance contributes

positively to consumer trust in mobile banking (Kim et al. 2009; Liu et al. 2009; Yang & Mao 2011). Following this line of arguments and empirical evidence, we argue that consumers will have a higher level of trust in mobile payment system if they believe that the structural assurance of mobile payment technology will provide them with safe, secure and reliable transactions, Therefore we have:

H4a: Perceived structural assurance is positively associated with the level of consumer trust in mobile payment.

EMT is defined as risk associated with the underlying technological infrastructure including “the transaction security related risks faced by consumers while using mobile payment services through a wireless network” (Chandra et al. 2010, p.565). Siau and Shen (2003) suggest that mobile technology related risks such as service breakdown of the wireless communication network and loss of transactions will significantly reduce the level of trust. Why? These risks may lead consumers to have doubt in mobile technology and its ability to deliver services. Liu et al. (2009) find that trust in a mobile wireless network positively affects consumers’ trust in mobile banking. Therefore we have: H4b: Perceived environmental risk is negatively associated with the level of consumer trust in

mobile payment.

Structural assurance in the form of third-party guarantees mitigates technological risks. Luo et al. (2010) find that consumers who have strong trust in structural assurance (i.e., legal and technology structures of wireless Internet) will believe that their financial and privacy data will be protected against transaction loss. Their study shows that structural assurance of mobile wireless Internet lowers the level of perceived risks in mobile banking. Kim et al. (2008) find that the presence of third-party guarantees has a negative effect on perceived risks in an online shopping environment. Similarly, Chandra et al. (2010) report a negative relationship between perceived structural assurance and perceived environmental risk in the mobile payment context. Therefore we have:

H4c: Perceived structural assurance is negatively associated with perceived environmental risk in mobile technology.

2.2.5 Control Variables

To better examine how characteristics of the mobile service provider, characteristics of the mobile payment vendor, and characteristics of mobile technology shape the way consumers develop their trust in mobile payment, we incorporate demographic factors (gender and ethnicity) and consumers’ experience with mobile banking as control variables on consumer trust in mobile payment. Salo and Karjaluoto (2007) suggest that individual demographics have a strong influence on the development of the trusting belief. Gender has shown to have an impact on trust in IT adoption studies (Awad & Ragowsky 2008; Gefen & Straub 1997). Dabholkar (1996) suggests that consumers’ experience with a similar technology is one of the factors influencing their trust in a new technology. Chandra et al. (2010) shows that consumers who have experiences with mobile Internet have higher trust in mobile payment systems compared to inexperienced consumers.

3

RESEARCH METHOD

The target population in this research is young adults. We chose undergraduate university students as representatives of this population. We chose university students because they are one of the main user groups of mobile phones and mobile networks (CNNIC 2010). Previous research (Scevak 2010) suggests that people under 30 years old are more willing to adopt mobile payment than other age groups. A sample of undergraduate students from two major universities in Auckland, New Zealand was chosen for the survey. Paper questionnaires were distributed to students on campuses. The survey instrument is adapted from validated measures in the literature (see Appendix A). All questions in the survey were measured on a 7-point Likert scale. Overall, 302 questionnaires were obtained and used in data analysis.

We used partial least square structural equation modelling (SEM) to test the hypotheses. PLS-SEM is appropriate for exploratory research. Hair et al. (2011) suggest that PLS-PLS-SEM is an

appropriate method for theory development and prediction. In addition, PLS-SEM can accommodate both reflective and formative constructs (Gefen et al. 2011) and can be used with fewer indicator variables (one or two) per construct (Hair et al. 2011).

We used SmartPLS 2.0 M3 (Ringle et al. 2005) to perform data analysis. We used the bootstrapping technique with 5,000 resamples to determine the significance levels for loadings, weights and path coefficients (Hair et al. 2011).

4

FINDINGS

4.1 Demographics

The sample has a relatively equal split between male (50.3%) and female (49.7%) respondents. The three main ethnic groups in the sample are Asian (41.4%), European (29.8%) and Maori/Pacific (17.6%). Overall, 97.6% and 62.1% of participants have experience with Internet banking and mobile banking respectively.

4.2 Instrument Validity and Reliability

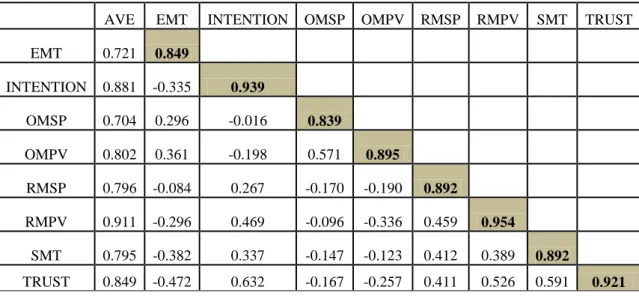

The loadings of the measurement items on their latent constructs and their composite reliability are reported in Appendix A. The values of the loadings range from 0.723 to 0.971, which are above the recommended threshold of 0.70, indicating that the indicator reliability is confirmed. The values of the composite reliability range from 0.877 to 0.968, which are above the acceptable value of 0.70, indicating that internal consistency is confirmed. The convergent reliability is tested by the average variance extracted (AVE) and the recommend threshold is 0.50. The values of AVE range from 0.704 to 0.911(see Table 2), suggesting that the convergent reliability is confirmed. For the discriminant validity, we check whether the square root of AVE of each construct is larger than the correlation of the construct concerned with other constructs. The bolded figures along the diagonal indicate that the square root of AVE exceed the off-diagonal correlations between the constructs (see Table 2). Hence, the discriminant validity is confirmed.

AVE EMT INTENTION OMSP OMPV RMSP RMPV SMT TRUST

EMT 0.721 0.849 INTENTION 0.881 -0.335 0.939 OMSP 0.704 0.296 -0.016 0.839 OMPV 0.802 0.361 -0.198 0.571 0.895 RMSP 0.796 -0.084 0.267 -0.170 -0.190 0.892 RMPV 0.911 -0.296 0.469 -0.096 -0.336 0.459 0.954 SMT 0.795 -0.382 0.337 -0.147 -0.123 0.412 0.389 0.892 TRUST 0.849 -0.472 0.632 -0.167 -0.257 0.411 0.526 0.591 0.921

The numbers in bold in the shaded diagonal cells are the square roots of the AVE.

Table 2. Discriminant validity: AVE diagonal 4.3 Structural Model

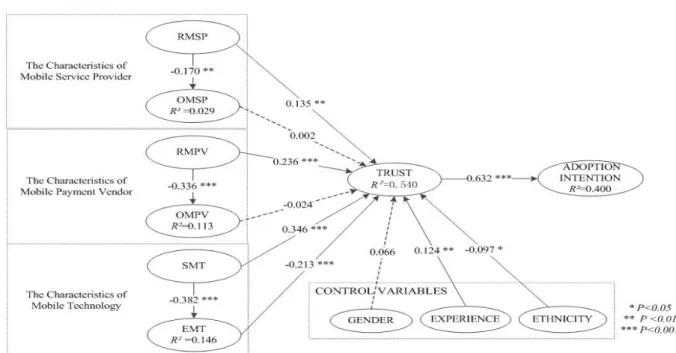

The PLS results are reported at Figure 2. The R²value for consumer trust in mobile payment (TRUST) is 0.540, which means that the three sets of trust building elements explain 54% of variance in mobile

payment trust. The model also demonstrates that TRUST explains 40% of variance in consumer’s intention to adopt mobile payment.

Figure 2. Results of Structural Model

As seen from Figure 2, consumer trust in mobile payment (TRUST) has strong influence on consumers’ intention to adopt mobile payment (INTENTION), hence H1 is supported. Perceived reputation of mobile payment vendor (RMPV), perceived structural assurance (SMT) and perceived environmental risk (EMT) have strongly significant effects on TRUST (p <0.001). Hence, H3a, H4a and H4b are supported respectively. Perceived reputation of mobile service provider (RMSP) also has a positively significant effect on TRUST (p <0.01), thus H2a is supported. However, perceived opportunism of mobile service provider (OMSP) and perceived opportunism of mobile payment vendor (OMPV) have no significant influence on TRUST. Hence, H2b and H3b are not supported respectively. This may be because the law relating to information and technology communication (ICT) is well developed in New Zealand. Consumers have built strong confidence in the legal system and its regulation of business. Hence, the OMSP and OMPV do not exert influence on TRUST. RMSP has a negative significant effect on OMSP (p<0.01), hence H2c is supported. There are a highly negative significant relationship between RMPV and OMPV (p<0.001), SMT and EMT (p<0.001). Hence, H3c and H4c are supported respectively. For the control variables, consumer’s experience with mobile banking (EXPERIENCE) (p <0.01) has significant influence on TRUST. This finding is consistent with previous IS studies which investigate the influence of experiences of using a technology on the intention to adopt a similar technology (Dabholkar 1996; Kim et al. 2008). Results also reveal that ethnicity identity (ETHNICITY) (p <0.05) also has an influence on TRUST. This finding suggests that people with different ethnicity identity may have different trusting behaviours towards mobile payment adoption. Results show that GENDER has no influence on TRUST. This may be caused by the increased participation in mobile technology by female users has resulted in convergence of trusting behaviour (Kolsaker & Payne 2002). Table 3 summarises the result of this study.

Paths Coefficient

(β)

t-value

(t) R² Supported?

H1: TRUST INTENTION 0.632*** 16.127 0.400 YES

H2a: RMSP TRUST 0.135** 2.684 0.540 YES

H2c: RMSP OMSP -0.170** 2.710 0.029 YES

H3a: RMPV TRUST 0.236*** 4.635 YES

H3b: OMPV TRUST -0.024 0.642 NO

H3c: RMPV OMPV -0.336*** 6.075 0.113 YES

H4a: SMT TRUST 0.346*** 6.509 YES

H4b: EMT TRUST -0.213*** 4.980 YES

H4c: SMT EMT -0.382*** 8.311 0.146 YES

***p<0.001; **p<0.01; *p<0.05

Table 3. Summary of results 4.4 Post-hoc Analysis

To evaluate the explanatory power of our model, we compared competing models in terms of R²

change for TRUST. In particular, we compared our proposed model with Chandra et al.’s (2010) trust model to test whether adding the characteristics of the mobile payment vendor (RMPV and OMPV) increases explained variance in TRUST. We followed a similar procedure used in Chandra et al. (2012) and Teo et al. (2008) for R² comparison. We used an F-test to test the statistical significance (Chin 2010).

Effect size (ƒ²) (Cohen 1988): is calculated by:

ƒ²= (R²proposed model - R²Chandra et al. (2010))/ (1-R²proposed model)

The F-test formula (Chin 2010) is calculated by:

(With K2-K1 and N- K2-K1 degree of freedom)

Where R1² is from the Chandra et al.’s (2010) model and R2² is from our proposed research model. K2 is the number of predictors in our proposed research model and K1 is the number of predictors in Chandra et al.’s (2010) model, and N is the sample size.

The calculated effect size is 0.089 (See Table4). According to Cohen (1988), an effect size between 0.02 and 0.15 indicates a small effect; an effect size between 0.15 and 0.35 indicates a medium effect; and an effect size greater than 0.35 indicates a large effect. Thus, we use 0.089 to indicate a small effect size. This could be explained from a small increase in explanatory power in R² values from 0.499 in Chandra et al. (2010) to 0.540 in the proposed research model (Chandra et al. 2012; Teo et al. 2008). The F-test for the change in R² is 13.013 (p<0.001), indicating that the change in R² is statistically significant. Based on these results, we conclude that adding the characteristics of mobile payment vendor (RMPV and OMPV) has a small yet statistically significant increase in explanatory power to TRUST. This means that there is a need to consider the characteristics of the mobile payment vendor together with other variables when examining consumer trust in mobile payment.

Chandra et al. (2010) Proposed Research Model

R² 0.499 0.540

Effect Size (ƒ²) 0.089 (small effect size)

F-test 13.013 (p<0.001)

5

DISCUSSION

The results reveal that consumers’ trust in mobile payment significantly influences their intention to adopt mobile payment. Our finding is consistent with previous mobile payment studies (Chandra et al. 2010; Keramati et al. 2012; Thair et al. 2010). This indicates that trust in mobile payment is a critical factor that consumers consider when making mobile payment adoption decisions.

Mobile service providers and mobile payment vendors are both important entities in a mobile payment system. The results show that the perceived reputation of the mobile service provider and mobile payment vendor are positively related to trust in mobile payment. These findings are in line with previous research in mobile payment (Chandra et al. 2010). In a recent study, Andreev et al. (2012) demonstrate that vendor trust increases consumers’ willingness to use mobile payment. The positive relationship between reputation of trading partners and trust is also supported in other IS contexts. For example, Connolly and Bannister (2008) find that the trustworthiness of Internet vendors increases the level of trust in Internet shopping. Liu et al. (2009) report the significant relationship between mobile service providers and consumer trust in mobile banking.

Our results suggest that perceived opportunism of the mobile service provider and mobile payment vendor are not related to consumers’ trust in mobile payment. This finding is consistent with Chandra et al.’s (2010) study of mobile payment trust among consumers in Singapore. In their study, they cited the strict law-enforcement environment in Singapore and mobile service providers’ unwillingness to involve in opportunistic conducts as a plausible explanation. In this study, a plausible reason might be that, according to a mobile payments readiness index report (MasterCard 2012b), consumers have strong confidence in the New Zealand legal system and its regulation of business. The law relating to ICT is well developed and consumers believe that their financial assets and transactions are being well protected. As a result, consumers may believe that mobile service providers and vendors are not likely to violate the law by conducting opportunistic behaviours. Hence, the perceived opportunism of the mobile service provider and mobile payment vendor are not significant factors of mobile payment trust in this study.

The findings suggest that characteristics of mobile technology are the important element in building mobile payment trust. This indicates that consumers may be concerned about security, reliability and privacy risks with mobile payment transactions. Both perceived structural assurance and perceived environmental risk have significant effects on mobile payment trust. This finding is in line with Chandra et al.’s (2010) mobile payment study and is also consistent with previous studies in mobile banking (Liu et al. 2009; Yang & Mao 2011). This finding highlights that mobile technology-related regulations and safeguards are crucial for consumers to believe that their financial transactions and personal data are being properly protected. It also indicates that consumers take the environmental risk related to mobile technology seriously whether they should trust mobile payment.

We also observe a significantly negative relationship between perceived structural assurance and perceived environmental risk. This indicates that developing adequate structural assurance can reduce the level of technological risks that consumers perceive. Some structural assurance mechanisms include government regulations on ICT-related transactions, the enforcement of ICT-related law, and the establishment of trusted institutions acting as guarantors.

In relation to the control variables, we observe that mobile banking experience and ethnicity identity play a role in consumer’s intention to adopt mobile payment. Consumers with mobile banking experience have stronger intention to adopt mobile payment than those who do not have experiences with mobile banking. This is in line with the findings of Dabholkar’s (1996) study. In his study, he suggests that consumers’ experience with a similar technology is one of the factors influencing their trust in a new technology. The results also show that ethnicity identify as a culture factor, has an influence on consumer’s intention to adopt mobile technology. This may suggest that people come from different culture background have different trusting behaviours towards mobile payment adoption. This finding is consistent with other IS studies such as the use of IT is differed between American and Japanese (Straub 1994) and culture influences the adoption of B2B e-commerce in Taiwan (Thatcher et al. 2006).

6

IMPLICATIONS AND LIMITATIONS OF THE STUDY

Mobile payment involves sharing a consumer’s account and financial information with a mobile service provider and mobile payment vendor. Therefore, it is crucial to develop consumers’ trust with relevant parties to realise broader adoption of mobile payment. This research examines consumer trust in mobile service providers, mobile payment vendors, and mobile technology. Results strongly support that trust is a crucial factor to consumers’ intention to adopt mobile payment. All three trust-building elements have a significant influence on mobile payment trust. Results highlight that, among all the factors, the structural assurance of mobile technology is one the most significant factors affecting mobile payment trust.

6.1 Implications

This research has both theoretical and practical implications. For the theoretical implication, this research extends Chandra et al.’s (2010) trust-theoretic model by adding the characteristics of the mobile payment vendor as another set of trust-building elements. Our empirical findings strongly support that perception of the mobile payment vendor shape consumers’ trust in mobile payment. Therefore, our understanding of mobile payment trust formation will not be complete if we exclude characteristics of the mobile payment vendor from the theoretical model. For the practical implication, we find that the institutional trust reflected in structural assurance has the most significant impact on consumers’ trust in mobile payment. This indicates that mobile payment designers and practitioners should incorporate relevant technology and services including “delivering mobile alerts and information services to consumers in the first instance to develop channel trust; providing and communicating service guarantees and real-time customer process; reinforcing safety and security within the aesthetics and syntax of the consumer’s experience; and visibly delivering best practice payment technology elements, such as transaction identifiers and effective repudiation management” (Microsoft and M-com 2009 p.12). These strategies may help consumers perceive mobile payment as a safe and secure channel to conduct financial transactions.

6.2 Limitations and Future Research

There are a few limitations in this study. First, there is a possibility of common method bias as we use a self-reported survey. Therefore, readers should keep this issue in mind when interpreting the results from this study. Second, this study targeted a set of potential consumers of mobile payment in Auckland, New Zealand. Therefore, readers should exercise caution to the generalisability of the results (Chandra et al. 2010; Vance et al. 2008). Third, mobile payment has not been implemented in Auckland yet. Therefore most of our informants have not had actual experience or know people who have experiences with mobile payment. This implies that our study focuses on the early stage of trust formation in mobile payment. Although the informants have not had direct experience with mobile payment, they are aware of what a mobile payment transaction involves. In the survey instrument, we provide contextual details to explain various mobile payment parties along with examples. In addition, most informants (62.1%) are familiar with mobile banking. So, we believe that their responses are reliable and valid. However, it is important to point out that trust building is a complex and time consuming process. Our study focuses on the initial trust formation. There is a possibility that consumers may demonstrate different trust behavioural patterns in the future. We suggest that future research compares pre-adoption and post-adoption of mobile payment trust behaviour and find out whether trust behaviours change over time.

References

Andreev, P., Duane, A., and O’Reilly, P. (2011). Conceptualising consumer perceptions of contactless m-payments through smart phones. Paper presented at the IFIP WG 8.2 International Federation for Information Processing on Researching the Future, Turku, Finland.

Andreev, P., Pliskin, N. and Rafaeli, S. (2012). Drivers and Inhibitors of Mobile-Payment Adoption by Smartphone Users. International Journal of E-Business Research (IJEBR), 8(3), 50-67. Awad, N.F. and Ragowsky, A. (2008). Establishing trust in electronic commerce through online and

word of mouth: An examination across genders. Journal of Management Information Systems, 24(4), 101-121.

Ba, S. (2001). Establishing online trust through a community responsibility system. Decision Support System, 31(3), 323-336.

Ba, S. and Pavlou, P. (2002). Evidence of the effect of trust building technology in electronic markets: Price premiums and buyer behavior. MIS Quarterly, 26(3), 243-268.

Au, Y. A. and Kauffman, R. J. (2008). The economics of mobile payments: Understanding

stakeholder issue for an emerging financial technology application. Journal Electronic Commerce Research and Applications, 7(2), 141-164.

Chandra, S., Srivastava, S. C. and Theng, Y. L. (2010). Evaluating the role of trust in consumer adoption of mobile payment systems: An empirical analysis. Communications of the Association for Information Systems, 27(1), 561-588.

Chandra, S., Srivastava, S. C. and Theng, Y. L. (2012). Cognitive absorption and trust for workplace collaboration in virtual worlds: An information processing decision making perspective. Journal of the Association for Information Systems, 13(10), 3.

CNNIC. (2010). 26th statistical survey report on the internet development in China. Retrieved from

http://www.cnnic.net.cn/.

Chin, W. W. (2010). How to write up and report PLS analyses. In Handbook of partial least squares, Vinzi, V. E., Chin, W. W., Henseler, J., & Wang, H. (eds.), Berlin: Springer, 655-690.

Cohen, J. (1988). Statistical power analysis for the behavioral sciences. New York: Academic Press. Connolly, R. and Bannister, F. (2008). Factors influencing Irish consumers’ trust in Internet shopping.

Management Research News, 31(5), 339-358.

Cyril, U., Eze, G. G. G. G., Ademu, J., and Tella, S. A. (2008).Modeling user trust and mobile payment adoption: A conceptual framework. Communications of the IBIMA, 3, 224-231. Dabholkar, P. A. (1996). Consumer evaluations of new technology-based self-service options: An

investigation of alternative models of service quality. International Journal of Research in Marketing, 13(1), 29-51.

Dahlberg, T., Mallat, N. and Öörni, A. (2003). Trust enhanced technology acceptance model-consumer acceptance of mobile payment solutions: Tentative evidence. Stockholm Mobility Roundtables, 22-23.

Gefen, D. and Straub, D. W. (2003). Managing user trust in B2C e-services. E-service Journal, 2(2), 7-24.

Gefen, D. and Straub, D.W. (1997). Gender differences in perception and adoption of e-mail: An extension to the technology acceptance model. MIS Quarterly, 21(4), 389–400.

Gefen, D. (2002). Reflections on the dimensions of trust and trustworthiness among online consumers. ACM SIGMIS Database, 33(3), 38-53.

Gefen, D., Karahanna, E. and Straub, D. W. (2003). Trust and TAM in online shopping: An integrated model.MIS quarterly, 27 (1), 51-90.

Gefen, D., Rigdon, E. E. and Straub, D. W. (2011). Editor's Comment:

An Update and Extension to SEM Guidelines for Administrative and Social Science Research. MIS Quarterly, 35(2), iii-xiv.

Gefen, D. (2000). E-commerce: The role of familiarity and trust. Omega, 28 (6), 725-737. Goeke, L., and Pousttchi, K. (2010). A scenario-based analysis of mobile payment acceptance. In

Mobile Business and 2010 Ninth Global Mobility Roundtable (ICMB-GMR). p. 371-378. IEEE. Grazioli, S., and Jarvenpaa, S. L. (2000). Perils of Internet fraud: An empirical investigation of

deception and trust with experienced Internet consumers. Systems, Man and Cybernetics, Part A: Systems and Humans, IEEE Transactions on, 30(4), 395-410.

Hair, J. F., Ringle, C. M. and Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. The Journal of Marketing Theory and Practice, 19 (2), 139-152.

Jarvenpaa, S. L., Tractinsky, N. & Saarinen, L. (1999). Consumer trust in an Internet store: A cross cultural validation. Journal of Computer – Mediated Communication, 5(2), doi: 10.1111/j.1083-6101.1999.tb00337.x.

John, G. (1984). An empirical investigation of some antecedents of opportunism in a marketing channel. Journal of Marketing Research, 21(3), 278-289.

Keramati, A., Taeb, R., Larijani, A. M. and Navid Mojir. (2012). A combinative model of behavioral and technical factors affecting ‘Mobile’-payment services adoption: An empirical study. The Service Industries Journal, 32(9), 1489-1504.

Kim, D. J., Ferrin, D. L. and Rao, H. R. (2008). A trust-based consumer decision-making model in electronic commerce: The role of trust, perceived risk, and their antecedents. Decision Support Systems, 44(2), 544-564.

Kim, G., Shin, B. and Lee, H.G. (2009). Understanding dynamics between initial trust and usage intentions of mobile banking. Information System Journal, 19(3), 283-311.

Kim, K.K., and Prabhakar, B. (2004). Initial trust and the adoption of B2C e-commerce: The case of Internet banking. ACM SIGMIS Database, 35(2), 50-64.

Kolsaker, A. and Payne, C. (2002). Engendering trust in e-commerce: A study of gender based concerns. Marketing Intelligence & Planning, 20(4), 206-214.

Koufaris, M. and Hampton-Sosa, W. (2004). The development of initial trust in an online company by new customers. Information and Management, 41(3), 377-397.

Liu, Z., Min, Q. and Ji, S. (2009). An empirical study on mobile banking adoption: The role of trust. In Proceedings of the 2009 Second International Symposium on Electronic Commerce and Security, p. 7-13, IEEE Computer Society.

Luo, X., Li, H., Zhang, J., and Shim, J.P. (2010). Examining multi-dimensional trust and multi-faced risk in initial acceptance of emerging technologies: An empirical study of mobile banking services. Decision Support Systems, 49(2), 222-234.

MasterCard. (2012a). Mobile Payments Readiness Index: A Global Market Assessment. Retrieved from http://mobilereadiness.mastercard.com/reports/process.php?cl=gl.

MasterCard. (2012b). Mobile Payments Readiness Index: New Zealand. Retrieved from http://mobilereadiness.mastercard.com/reports/process.php?c%5B%5D=nz&x=130&y=22. Mallet, N. (2007). Exploring consumer mobile payment adoption: A qualitative study. Journal of

Strategic Information System, 16(4), 413-432.

Mayer, R. C., Davis, J. H., and Schoorman, F. D. (1995). An integrative model of organizational trust. Academy of Management Review, 20 (3), 709-734.

McKnight, D.H., Cummings, L.L. and Chervany, N.L. (1998). Initial trust formation in new organizational relationships. Academy of Management Review, 23(3), 473-490.

McKnight, D. H., Choudhury, V. and Kacmar, C. (2002). Developing and validating trust measures for e-commerce: An integrative typology. Information Systems Research, 13(3), 334-359. Microsoft and M-Com. (2009). Mobile Payments: Delivering compelling customer and shareholder

value through a complete, coherent approach. Retrieved from http://www.microsoft.com/en-nz/download/details.aspx?id=23905.

Mukherjee, A. and Nath, P. (2003). A model of trust in online relationship banking. International Journal of Bank Marketing, 21(1), 5-15.

Pavlou, P. A., Liang, H., and Xue, Y. (2007). Understanding and Mitigating Uncertainty in Online Exchange Relationships: A Principal-Agent Perspective. MIS Quarterly, 31(1), 105-136. Pope, M., Pantages, R., Enachescu, N., Dinshaw, R., Joshlin, C., Stone, R., and Seal, K. (2011).

Mobile payments: The reality on the ground in selected Asian countries and the United States. International Journal of Mobile Marketing,6(2), 88-104.

Ringle, C.M., Wende, S. and Will, S. (2005). SmartPLS 2.0 (M3) Beta. Hamburg.

Http://www.smartpls.de.

Salo, J., and Karjaluoto, H. (2007). A conceptual model of trust in the online environment. Online Information Review, 31(5), 604-621.

Scevak, N. (2010). Forrester Research mobile media and messaging forecast, 2010 to 2015 (Western Europe). Retrieved from

http://www.forrester.com/rb/Research/research_mobile_media_and_messaging_forecast,_2010/q/i d/57671/t/2.

Shin, D. H. (2010). Modeling the interaction of users and mobile payment system: Conceptual framework. International. Journal of Human–Computer Interaction, 26(10), 917-940. Sitkin, S., and Roth, N. L. (1993). Exploring the limited effectiveness of legalistic remedies for

trust/distrust. Organization Science, 4(3), 367-392.

Straub, D.W. (1994). The effect of culture on IT diffusion: E-mail and fax in Japan and the US. Information System Research, 5(1), 23-47.

Suh, B., and Han, I. (2003). Effect of trust on customer acceptance of Internet banking. Electronic Commerce Research and Applications, 1(3), 247-263

Siau, K. and Shen, Z. (2003). Building customer trust in mobile commerce. Communications of the ACM, 46(4), 91-94.

Teo, T. S. Srivastava, S. C., and Jiang, L. (2008). Trust and electronic government success: An empirical study. Journal of Management Information Systems, 25(3), 99-132.

Thair, A., Suhuai, L. and Peter, S. (2010). Consumer acceptance of mobile payments: An empirical study. International Conference on New Trends in Information Science and Service Science (NISS), p. 533-537, IEEE.

Thatcher, S.M.B., Foster, W. and Ling, Z. (2006). B2B e-commerce adoption decisions in Taiwan: The interaction of cultural and other institutional factors. Electronic Commerce Research and Applications, 5(2), 92-104.

Vance, A., Elie-Dit-Cosaque, C. and Straub, D. W. (2008). Examining trust in information technology artifacts: The effects of system quality and culture. Journal of Management Information Systems, 24(4), 73-100.

Yang, G. and Mao, Y. (2011). A research on the model of factors influencing consumer trust in mobile business. International Conference on E-Business and E-Government (ICEE), p. 1-5, IEEE. Zucker, L. G. (1986). Production of trust: Institutional sources of economic structure, 1840–1920.

Appendix A: Item Loading and Composite Reliability

Constructs Code Indicators Loading

Composite Reliability Intention to adopt Mobile Payment (INTENTION) -Reflective INT1

Given a chance, I intend to adopt

mobile payments in the future. 0.948

0.957 INT2

Given a chance, I predict that I will frequently use mobile payments in the

future. 0.951

INT3

I will strongly recommend others to

use mobile payments. 0.917

Mobile Payment Trust (TRUST)

-Reflective

T1

I trust mobile payment systems to be

reliable. 0.908

0.957 T2

I trust mobile payment systems to be

secure. 0.901

T3

I believe mobile payment systems are

trustworthy. 0.946

T4 I trust mobile payment systems. 0.929

T5*

Even if the mobile payment systems are not monitored, I would trust them

to do the job correctly. 0.527*

Perceived Reputation of mobile service provider

(RMSP)

-Reflective

RMSP1

I believe MOBILE SERVICE

PROVIDER has a good reputation. 0.880

0.921 RMSP2

I believe MOBILE SERVICE PROVIDER has a reputation for

being fair. 0.895

RMSP3

I believe MOBILE SERVICE PROVIDER has a reputation for

being honest. 0.903 Perceived Opportunism of mobile service provider (OMSP) -Reflective OMSP1

I believe that MOBILE SERVICE PROVIDER may use customer

information without permission. 0.833

0.877 OMSP2

I believe that MOBILE SERVICE PROVIDER might alter information

in its own self-interest. 0.840

OMSP3

I believe that MOBILE SERVICE PROVIDER may promise things

without actually doing them. 0.845

Perceived Reputation of mobile payment vendor(RMPV)

-Reflective

RMPV1

I believe MOBILE PAYMENT

VENDOR has a good reputation. 0.936

0.968 RMPV2

I believe MOBILE PAYMENT VENDOR has a reputation for being

fair. 0.971

RMPV3

I believe MOBILE PAYMENT VENDOR has a reputation for being

honest. 0.956 Perceived Opportunism of mobile payment vendor (OMPV) -Reflective OMPV1

I believe that MOBILE PAYMENT VENDOR may use customer

information without permission. 0.904

0.924 OMPV2

I believe that MOBILE PAYMENT VENDOR might alter information for

its own self-interest. 0.903

OMPV3

I believe that MOBILE PAYMENT VENDOR may promise things

without actually doing them. 0.879

Perceived Structural

Assurance(SMT) SMT1

I believe mobile technology has enough safeguards to make me feel comfortable using it to make mobile

Constructs Code Indicators Loading

Composite Reliability

-Reflective

SMT2

I feel assured that legal and technological structures adequately

protect me from problems on the

mobile technology. 0.868

SMT3

I feel confident that encryption and other technological safeguards on the mobile technology make it safe for me

to make mobile payments. 0.926

SMT4

In general, the mobile technology provides a robust and safe environment to perform mobile

payments. 0.896

Perceived Environmental Risk (EMT)

-Reflective

EMT1*

Information about my mobile payment transactions would be known

to others. 0.556*

0.911 EMT2

I believe mobile payment transactions

may be modified or deleted by others. 0.723

EMT3

I believe there is a high probability of losing a great deal in using mobile

payment systems. 0.890

EMT4

I would label adopting mobile

payment systems as a potential loss. 0.863 EMT5

I believe that overall riskiness of

mobile payment systems is high. 0.909 * dropped due to low loadings