ROLE OF COMMERCIAL BANKS IN NON-PERFORMING ASSETS (NPAs)AND GDP GROWTH

Mohd Mubeen Siddiqui

1, Dr. Hari Om

2Department of Commerce

1,2

Full text

1,2

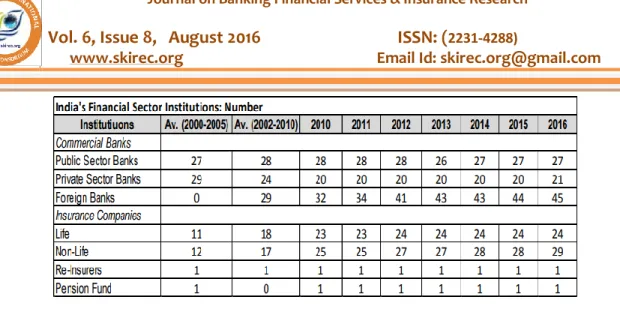

Figure

Related documents

The objective of this paper is to study and estimate origin-destination (O-D) city-pair passenger air traffic based on DGCA (Director General of Civil Aviation) airport statistics

Because binary masking is conservative (any invalid constituent fine pixel results in an invalid coarse pixel) it is guaranteed that the correlation is based on only data known to

Positions held: Argonne National Laboratory: resident student associate, 1973; research associate, 1974; assistant computer scientist 1975–1980; senior computer scientist 1980–

– Primary Latch Reinforcement (PLR) feature (optional) ensures no accidental terminal back- out of crimped contacts during vibrations of up to 10G – MX150 CE TM connectors accept

This elite 2 + 2 programme offers H.I.T.’s high achieving students the opportunity to obtain the BEng (Hons) Mechanical Engineering degree from the University of Bath, UK.. After

Eight morpho-anatomical properties of two-year-old needles of Pinus heldreichii (Bosnian pine) from the Scardo-Pindic mountain massif in Serbia (Kosovo, Mt. Ošljak)

18 Experience and Team Building 0.35 Positive relationship 19 Experience and Loyalty 0.67 StrongPositive. relationship 20 Experience and

The differently processed soybean had higher crude protein content than the control diet (38%CP) with sprouted soybean (42.00%) having the highest value, this reaffirmed the