CZECH UNIVERSITY OF LIFE SCIENCES

FACULTY OF TROPICAL AGRISCIENCES

Department of Economics and Development

Proposal for a creation of collateral system for microfinance sector: a tool for

development and reduction of systemic risk

Dissertation thesis

Student: Dipl. Kfm. Tomáš Hes Supervisor: Doc. Ing. Karel Srnec, CSc. Prague, August 2013

2 Acknowledgement:

I would like to express deep thanks to doc. Ing. Karel Srnec Ph.D., prof. Ing. Luboš Hes DrSc., Mudr. Ludmila Hesová, Ing. Matěj Marek and many other supporters of the research. Tomáš Hes

Declaration

I, Tomáš Hes, declare that this thesis, submitted in fulfillment of requirements for the PhD. degree, at Faculty of Tropical Agriculture of the Czech University of Life Sciences Prague, is wholly my own work unless otherwise referenced or acknowledged.

In Prague 20.08. 2013 --- Tomáš Hes

3

List of figures

1. Number of microfinance clients at present time

2. Virtous spiral of empowerment of women through microfinance

3. Global microcredit interest rates, yields, cost of funds by target market, cost of total cost funds, drivers of interest yields by target market

4. Multiple principal-agent relationship from the point of view of microfinance institutions, with every tandem relationship increasing the cost of funds

5. Overview of securities and derivatives, regulated exchanges and OTC markets 6. MPI calculation

7. Comparison of VIX and CVI indices 8. IECS – GMFA tandem

9. GMFA

10.GMFA Gurantee Fund 11.IECS

12.IECS cap-and-auction system

13.Marginal costs of negative externalities of complexity

List of tables

1. Descriptive statistics on variables used for testing of H1 and H2

2. Summary of Objectives and Methodology of H1 – H2

3. Results of H1 – H2

4. Descriptive statistics used for H3 – H5

5. Summary of Objectives and Empirical Methodology of H3 – H5

4

List of abbreviations

AT Agency Theory

BIT Bilateral Investment Treaty CDOs Collateralized Debt Obligations CDS Credit Default Swaps

CMOs Collateralized Mortgage Obligations EMH Efficient Markets Theory

ERM Enterprise risk management

FC Financial Crisis 2007-2008

FIH Financial Instability Hypothesis

GMFA Global Microfinance Financial Authority

HDI Human Development Index

IECS International Externality Commodification System

IKE Imperfect Knowledge Economies

IMF International Monetary Fund PAR30+ Portfolio at risk older than 30 days LICs Low Income Countries

LDC Least Developed Countries

MFI Microfinance Institution

MGDPI Millenium Development Goals Progress Index MIV Microfinance Investment Vehicle

MPI Microfinance Penetration Indicator NBFI Non-bank Financial Institutions

NGO Non-Governmental Organisation

ODA Official Development Aid

OECD Organisation for Economic Cooperation and Development OLS Ordinary Least Squares

SIV Special Investment Vehicle

SMME’s small (including micro-) and medium-sized enterprises SPV Special Purpose Vehicle

5

Table of contents

List of figures ... 3

List of tables ... 3

List of abbreviations ... 4

Table of contents ... 5

Abstract ... 8

Aim of the dissertation ... 9

Used methods and materials ... 10

1. Introduction ... 13

2. Microfinance ... 14

2.1. Evolutionary implication on the nature of modern microfinance ... 15

2.2. Microfinance and Human Development ... 18

2.3. Microfinance and Millenium Development Goals ... 21

2.4. International funding as a backbone of the sector ... 22

2.5. Funding costs contributing to high cost of microcredit ... 24

2.6. Sectoral weaknesses caused by lack of global coordination ... 26

2.7. Criticism of Microfinance ... 28

2.8. Review of selected background theories related to microfinance ... 30

2.8.1. Principal - Agent Theory and the role of collateral ... 30

2.8.2. Welfare economics ... 31

2.8.3. Human Development Theory ... 32

2.8.4. Gender Inequality Theory ... 33

3. Review of contemporary risk transfer innovations ... 33

6

3.2. Derivatives and microfinance ... 36

3.3. Securitisation and microfinance ... 38

3.4. Crowdfunding lending through securitized flows ... 39

4. Microfinance and endogenous systemic risks ... 40

4.1. Complexity and risk transfer innovations in financial markets ... 42

4.2. Structured finance as a source of systemic risk ... 43

4.3. Regulation of financial innovations and NBFIs ... 44

4.4. Theories concerned ... 46

4.4.1. Efficient Market hypothesis and Financial Instability Hypothesis ... 46

4.4.2. Financial Transaction Taxes ... 47

4.4.3. Social Cost Concept ... 48

4.4.4. Market Failure Theory ... 48

4.4.5. Regulatory Capture of Financial Regulation ... 49

5. Relationship between microfinance and chosen development indices ... 49

5.1. Literature review ... 50

5.2. Hypothesis ... 52

5.3. Variables ... 53

5.3.1. Dependent variables ... 53

5.3.2. Independent variables ... 55

5.4. Estimation method ... 57

5.5. Robustness of results. ... 58

5.6. Interpretation of results ... 58

5.7. Limitations of the model ... 59

7

6.1. Literature review ... 60

6.2. Hypothesis ... 61

6.3. Variables ... 62

6.3.1. Dependent variable ... 63

6.3.2. Independent variables ... 63

6.4. Estimation method of hypotheses H3 - H5 ... 66

6.5. Interpretation of results ... 67

6.7. Limitations of the model ... 68

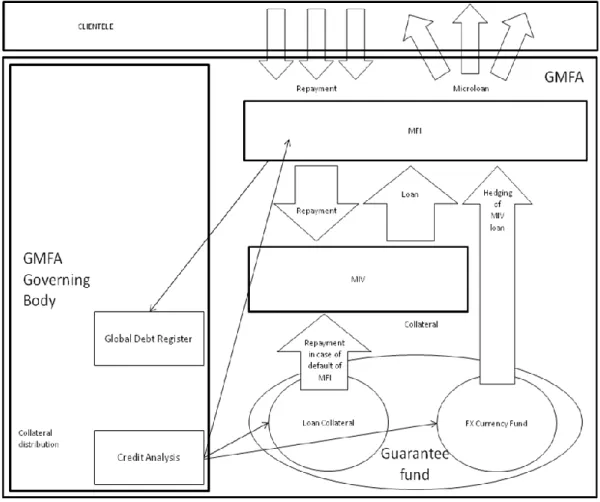

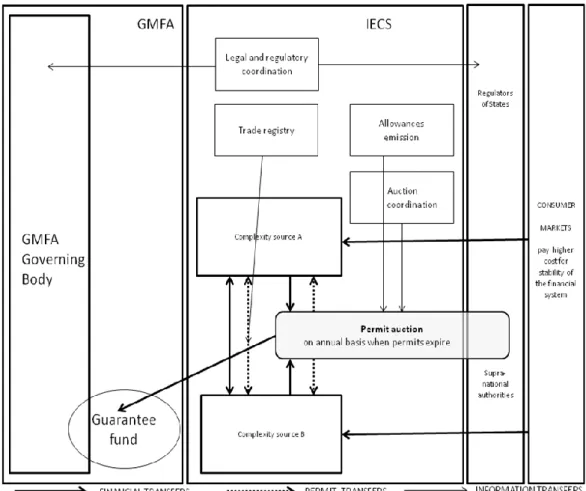

7. New macroprudential regulation – externality trading market of risk commodification ... 69

7.1. Proposed IECS – GMFA ... 70

7.2. GMFA and its functions ... 72

7.3. GMFA Guarantee Fund ... 74

7.4. IECS and its functions ... 76

7.5. Cap-and-auction system ... 77

7.6. Further implications of IECS – GMFA from the point of view of mentioned problems ... 79

7.7. Obstacles to GMFA-IECS and suggested strategies to overcome them... 80

8. Conclusion ... 82

References ... 84

Annex A ... 93

Annex B ... 95

Annex C ... 97

Annex D ... 100

Annex E ... 101

8

Abstract

While developing countries suffer from insufficient capital volume placed in their development agenda through microfinance institutions with their potential of contribution to human development, financial markets are on the other hand becoming worryingly complex, with complexity acting as a negative externality to the ecosystem of global finance. The dissertation focuses on interrelatedness between microfinance, structured finance and human development and investigates potential linkages from the point of view of global systemic risks as well as from the point of view of a development potential. Having found a correlation between microfinance and human development indices and on the other hand no correlation between microfinance and global capital markets, the work proposes establishment of a macroprudential global regulation that draws borders of a protected territory within the financial system for microfinance institutions that produce positive externalities in form of human development. This territory is further complemented by a funding mechanism tied to a complexity reduction scheme of a global cap and trade offset system trading quants of

negative externalities for collateral which secures microfinance funding. Such system reduces complexity of structured finance and on the other propulses funding to the microfinance sector characterized by low complexity and development potential for underdeveloped regions while reducing global systemic risks and cost of microcredit for the poor.

Key words: risk, microfinance, collateral, human development, funding

Abstrakt

Zatímco rozvojové země trpí nedostatkem trvale udržitelného kapitálu aplikovaného prostřednictvím mikrofinančních institucí, rozvinuté finanční trhy se znepokojivě vymykají kontrole díky bouřlivému rozvoji inovací, které generují negativní externality poškozující globální finanční ekosystém. Disertace zkoumá propojení mezi kapitálovými trhy a

mikrofinančním sektorem z úhlu pohledu lidského rozvoje a globálních systémových rizik, stejně tak jako potenciálu mikrofinančního sektoru. Zjištěná nízká korelace mezi

mikrofinančním sektorem a kapitálovými trhy a zároveň rozvojový potenciál mikrofinančních nástrojů potvrzuje smysl ustanovení mechanismu financování mikrofinančních institucí v kombinaci s regulačním režimem, který analogicky k systému emisních povolenek monetizuje

9

negativní externality vznikající na trhu strukturovaných financí. V navrženém mechanismu hraje komplexita roli kontaminantu a mikrofinanční systém roli recipienta příjmů z emise povolenek redukující komplexitu obchodů se strukturovanými produkty. Mikrofinanční sektor tak na jedné straně umožňuje snížit složitost moderních finančních trhů a na straně druhé díky svému rozvojovému dopadu urychluje trvale udržitelný rozvoj skrze

mikrofinanční služby, charakterizované jednoduchými závazkovými vztahy a rozvojovým potenciálem, při snižování globálních systémových rizik.

Klíčová slova: microfinance, garance, dohledatelnost dluhu, deriváty, komplexita

Aim of the dissertation

The purpose of the dissertation is to propose a creation of a global macroprudential1 regulatory mechanism, which will serve as an exchange of externalities related to arguably two major problems of global economy, the thread of systemic risk arising from structured financial markets and low level of human development caused by low financial access. The work demonstrates, justifies and proposes a specific territory within the developing financial sector, classifying and targeting microfinance as a financial intermediation carrier of positive externalities related to social and economic development for marginalized societies as well as a risk mitigation instrument. The research goal, serving as a base for the final proposal, is to demonstrate on base of empiric evidence the assumption that microfinance markets are detached from capital markets on global level and therefore represent low level of systemic risk as well as contribute to welfare of societies, especially in gender and human development related issues as shown on high correlation with the selected development indices. The

proposed separation of microfinance from the point of view of international investment as a protected social finance territory therefore constitutes an opportunity to manage future development of yet immature financial systems and to certain extent curb and anchor the interconnected volalities of financial systems through an intelligent linkage with financial sectors in development, characterized by low financial interconnectedness and positive

1

Macro-prudential regulation is concerned with the stability of the financial system as a whole, while micro-prudential regulation is concerned with the health of the individual deposit taking institution.

10 externalities of microfinance.

The final proposal cemented by statistical evidence overarching the descriptive as well as the research parts of the dissertation, creates a consequent proposition of a functional connection of the aforementioned topics into a global risk commodification mechanism, a cap-and-auction market. Such mechanism caps negative externalities reducing complexity of structured finance and at the same fuels income from the emission of allowances to a

guarantee fund, which provides capital to undernourished microfinance sector while benefitting the target populations.

The description of a variety of sectors, topics as well as underlying theories serves as a lateral objective of the work, showing in a wide panorama the wide of different concepts of risk management and financial intermediation at present time, exposing their scope and significance, and inducing the chosen research.

Used methods and materials

The dissertation studies the sector of microfinance as a specific part of global finance from the positivist point of view of its contribution to human social development. In order to lay bare the entourage, interconnectedness and conjunctures of each field, the dissertation presents in sequential expositions interrelated topics beginning with microfinance, risk transfer innovations and human development. The expositions are constructed in a

telescopical progression from the historical evolution that predetermines the present state and from the general to the specific, extending the chosen specific chapters of every topic. The panorama of the building blocks of the studied phenomenons renders the potential to explore its interlocked individual parts and to view them in their perspective. The scenery presents reasoning argument for the selected research and derived final proposal and serves to

understand the wider interplay of the topics within the global economy, why is microfinance beneficial and why is it important to regulate complexity as well as why it is important to fund microfinance institutions and forms a concluding reason why there is a need for the proposed mechanism. Following the general background, synthesis of the aforementioned parts leads to a formulation of several hypotheses on the phenomenon of low correlation of microfinance markets with international capital markets, as well as positive contribution to the gender development, human development and Millenium Development Goals achievement.

11

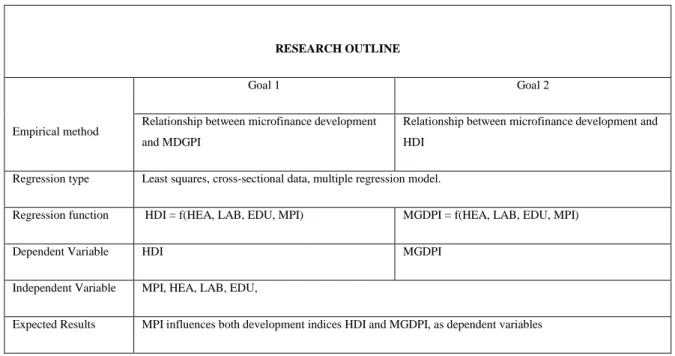

In the first set of hypothesis H1 - H2 we study microfinance as a propulsor of human

development in relationship to two indices of Human Development Index (HDI) and Millenium Development Goals Progress Index (MDGPI). We assume microfinance can deepen and accelerate the advancement of the aforementioned processes beyond the use of microcredit and therefore we extend the current measures, by creating a new sectoral outreach indicator, Microfinance Penetration Index (MPI), complementing the current microfinance outreach indicators by inclusion of saving volume and savers to previously used portfolio volume and borrower numbers. Expected existing correlation of the panel data analyzed through OLS simple regression cross-sectional analysis justifies the potential for a creation of global regulation mechanism, inducing to microfinance a specific financial regulation, and also reasserting the developmental meaning of the proposed cap-and-auction mechanism.

H1: Depth of the microfinance sector as per microfinance penetration indicator

positively correlates with HDI.

H2: Depth of the microfinance sector as per microfinance penetration indicator

positively correlates with MGDPI.

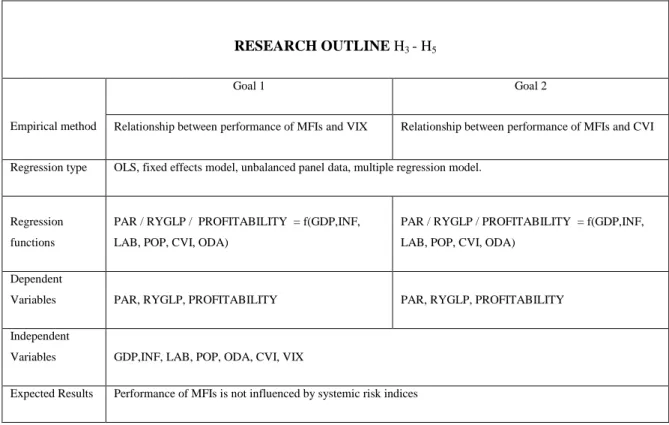

In the second set of hypothesis H3 - H5 we study microfinance as a mitigant to

systemic risk propulsor, which supports the thesis on mutual offsetting potential between microfinance and two systemic risk indices. Expected non-existing / low correlation of the aggregate regional panel data on performance of microfinance institutions (MFIs) with two capital market systemic risk indices analyzed through OLS simple regression analysis justifies the potential for a creation of cap-and-auction mechanism reducing complexity of structured finance. The confirmed hypotheses support the thesis on mitigation potential of volatilities of structured finance through their anchoring in local microfinance portfolios and thus reduction of global systemic risk.

H3a: Profitability of MFIs does not correlate with systemic risk index VIX2

H3b: Profitability of MFIs does not correlate with systemic risk index CVI3

2 VIX – CBOE Volatility Index shows the market's expectation of 30-day volatility. It is constructed using the implied volatilities of a wide range of S&P 500 index options. The VIX is a widely used measure of market risk. (CBOE, 2013)

12

H4a: Portfolio at risk4 (PAR) of MFIs does not correlate with systemic risk index VIX

H4b: PAR of MFIs does not correlate with systemic risk index CVI

H5a: Real yield5 on gross loan portfolio (RYGLP) of MFIs do not correlate with

systemic risk index VIX

H5b: RYGLP of MFIs dos not correlate with systemic risk index: CVI

The final proposal consists of a description of the global cap-and-auction – collateral mechanism, including several schemas which elaborate into more detail its functioning, followed by a graphic as well as a simple expression of its advantageousness to society. During the elaboration of the dissertation, numerical, descriptive as well as other materials were utilized. Annual data on the performance of systemic risk indices was obtained through publicly accessible resources of Chicago Board of Exchange and University of Singapore. Data on the sector performance of structured finance was obtained through databases of International Monetary Fund (IMF), World Bank (WB), Bank of International Settlements (BIS). The data on CDS was obtained in International Swaps and Derivatives Association (ISDA) database and EDHEC-Risk Institute. The HDI data was obtained from public database of UNDP, while the MDGPI data was acquired in the database from Center for Global Development. Socioeconomic regressors were acquired from the World Development Indicators (WDI) database maintained by World Bank.

The microfinance dataset comprises of up to 17 years of microfinance industry data period of 1995-2012 from 2,100 MFIs with 93 million borrowing clients gathered by the “Microfinance Information Exchange (MIX) Premium” database available to registered scholars, the prime source of global microfinance data at present worldwide. Panel data is structured in regional clusters on annual basis, with MFIs grouped by MIX in respective six worlds regions. For PAR in total 10,067 annual values were available, for profitability 7,305 3 Corporate Volatility Index is constructed by Risk Management Institute at the National University of

Singapore. The CVI selected is a Value-weighted CVI (CVIvw) aggregated with each firm weighted by its capitalization taking into account the size of each firm, based on S&P 500 index. (RMI, 2013)

4

Portfolio at risk is the value of loans outstanding past due more than 30 days, including the unpaid principal balance, the past due and future installments, loans that have been restructured or rescheduled. We have chosen PAR30+ as the most frequently used measure for portfolio quality in microfinance.

5

Real Yield on Gross Portfolio is inflation adjusted Nominal Yield on Gross Portfolio. Nominal Yield on Gross Portfolio is composed by sum of Interest and Fees on Loan Portfolio, divided by Gross

13

annual values and for profitability annual 11,323 values. Data collection is based on microfinance sector reporting standards and coherent with International Financial Reporting Standards. Apart from annual monitoring the data quality of all participating MFIs, the MIX Market applies certain adjustments, including accounting for inflation and loan loss

provisioning.

The systemic risk of microfinance was investigated by regressing a number of financial variables against selected market indices made available by mentioned institutions. Studies of authors aimed at studying theories of economic growth and development were procured mainly from the Library of Czech University of Life Sciences (CULS).

Peer-reviewed articles from authors dealing with the relevant problematic are provided principally through IDEAS Economic Research portal, as well as other academic papers accessible in academic databases.

1.

Introduction

Financial infrastructure belongs to key fabrics of advanced societies. Financial access improves efficiency of capital allocation and reduces transaction costs, mitigates risks, transforms idle savings into productive investments and in doing so increases quality of human life. Yet while populations in developed countries may perceive access to financial services as self-evident part of daily life, 3.6 billion people in developing countries are deprived of amenities of mature financial infrastructures (Robinson, 2001). Microfinance, despite its varied shortcomings, is a tool of advancement filling this gap. The colossal mission of infrastructural extension lying ahead is an an opportunity to confine part of the nascent financial industry within boundaries of socially responsible concept, drafting the limits of socially responsible financial systems before they develop. The current popular view of the sector is however afflicted by simplification blending in development idealism,

neoliberal pragmatism and critism gone astray, compounding different, often incompatible or juxtaposed concepts into an incongruous notion of “microfinance”. Different notions of microfinance should be distinguished and kept apart, for the sake of correspondence of what microfinance is, what it is not, what should it accomplish and represent. The call for

differentiation between social microfinance and commercial microfinance is one of the purposes this dissertation, while the other is concerned with a concrete proposal of how to take advantage of two qualities that microfinance harbours: manifold impact on human development and its detachment from capital markets making microfinance insulated from systemic risk.

14

The dissertation views both topics, of microfinance development as well as increasing level of public bads caused by financial complexity, as parallely evolving processes that could be linked in order to enhance development as well as reduce global risk level for mutual benefit. The linkage is established in a worldwide regulated area of financial development, funding socially responsible microfinancial intermediaries with capital stemming from commodified cost put by regulators on negative externalities generated by structured finance.

The proposed market based mechanism introduces a cap-and-auction platform that allows creation of a market for trade with noxious complexity with the proceedings being hold in a collateral fund impulsing leverage capital in order to grow social microfinance.

Several arguments support such proposal as a supporting body of evidence. The first one is the impact of microfinance on human development. The second argument is the low correlation of microfinance markets with capital markets as well as smaller size of MFIs embedded in their local contexts, when compared to large financial institutions, having a clear benefit of reduction of systemic risk and complexity.

2.

MicrofinanceFormal financial sector denies the poor clientele financial services because of perceived risks and high costs involved in tiny transactions and the inability of the poor to provide bankable guarantees. Complicated loan procedures, lack of infrastructure in

underdeveloped regions, combined with lack of formalized assets, limit poor people's access to sources of credit and amenities of financial markets. Microfinance services fill in the gap of the formal finance, being retail financial services that are relatively small when compared to the income of a typical individual. Specifically, the average outstanding balance of a

microfinance loan is no greater than 250% of the average GNI per capita (Mixmarket, 2013), with the average loan balance per borrower reaching 655 dollars in 2009 (Mixmarket,2010). Even when low-income people lack access to a formal financial system, they actively use a spectrum of informal providers for loans, savings, insurance, and fund transfers (Collins et al., 2009). The function of microfinance is therefore not only of providing more choice of less risky and more favourable alternatives, but to present an opportunity for populations to step on a path to move out of shadow economics Agents of microfinance, MFIs, provide financial services to the poor including credit, savings, insurance and other financial services tailored to the development environs. Microfinance sector can be also characterized by common features of informational constraints, segmentation of clientele, interlinkage, interest rate variation, rationing and exclusivity (Ray, 1998). MFIs are more profitable where access to the formal

15

financial system is low, in line with the findings of market-failure hypothesis: MFIs respond to need unstatisfied by banks and flourish where the banking sector fails (Vanroose et al., 2012).

From a macroeconomic perspective for some countries microcredit already represents an important portion of both gross domestic product (GDP) and of the totality of private credit. For these countries6, abrupt changes in microcredit could implicate macroeconomic implications as a large number of borrowers are excluded from credit markets (Di Bella, 2011).

Inadequate supply of productive capital caused by shortage of collateral, often a consequence of a highly unequal distribution of wealth and especially exacerbated in rural areas, contributes to slow development of societies (BMZ, 2012). Collateral that enables secured lending thus belongs to core elements of development finance. It was innovative contractual collateralization of social relationships7 that made emergence of modern microfinance possible, resulting from the market failure of financial sector, associated with information asymmetry, non-competitive markets, insufficient infrastructure and

externalities. The key achievement of microfinance is its success in providing uncollateralized loans with low default rates. In 2009, only 5 percent of credits had delinquency older than 90 days delinquent (Buera, 2012). MFIs accept alternative collateral, as in case of insufficient physical collateral, peer pressure of solidarity groups is accepted, holding those mutually responsible for the sum of loan within each group obliging the borrowers to repay the loan.

2.1. Evolutionary implication on the nature of modern microfinance

The birth of the modern microfinance occurred at a time of a paradigm shift characterized by deregulation, privatization, globalized free trade and neoliberal market oriented approaches. Despite the recent popularity of “microfinance revolution”8, the neologist coinage of “microfinance” refers to an ancient concept recently reinvented into a

6

Low income countries (e.g., Bolivia, Cambodia, Kenya, Mongolia Nicaragua, Tanzania, Vietnam), transition economies (e.g. Armenia, Bosnia & Herzegovina, Kyrgyz Republic, Tajikistan), emerging economies (e.g. Peru).

7

Neighourhood relationships became collateralizable, permitting passive assets to attract productive capital.

8

The term “Microfinance revolution” describes the expansion of small-scale financial services to the poor in developing countries in the second half of 20th century.

16

movement that surprisingly reached popularity in few decades. Microfinance phenomenon is thus also intrinsically linked to modern media as well as the end of cold war, which permitted the global public focus attention in new directions, while countless local social finance initiatives existed since times immemorial yet remained unscathed due to lack of medialisation. Informal financial subsystems existed in Asia since the early starts of the Chinese hui systems, the Indian chit funds or the arisan in Indonesia dating back more than 3000 years in form of savings clubs or burial societies (Seibel, 2005). In Africa, rotating savings and credit associations can be traced back to Nigerian esusu at least 500 years ago, becoming the seed of microfinance in Americas as they were exported along with the slave trade (Seibel, 2005). European microfinance developed during the seventeenth century, as a direct consequence of population increase and resulting poverty, in parallel to commercial banking. In Ireland and Germany, where today former MFIs account for almost half of banking assets, regulators introduced mainstreamed prudential regulation of the sector during the beginning of the twentieth century. (Seibel, 2005)

Modern microfinance arose in the 1970s as a response to findings on inefficiency of subsidized credits provided by statal development banks, when protectionist financial strategies have resulted in poor loan recovery, high costs and insolvency (Adams, Von Pischke and Graham, 1984). The basic tenets underlying the traditional credit approach were in consequence supplanted by the "financial systems approach". This approach viewed credit as another type of financial service priced freely in order to secure permanent inflow of productive capital and elimination of rationing and led to a shift towards local, sustainable institutions based upon strict market principles.

The modern concept embodied microcredit9 as a basic stone of microfinancial service, propulsed by simple, universally transferable credit methodology characterized by 4 - 6 months credit period, weekly repayments with well defined target clientele and later expanded to savings, remmittances, insurance and other services10. In 1970s, institutions such as

Grameen Bank and ACCION International achieved high repayment rates and overcame presumptions of development practitioners who believed that the poor belonged to a high-risk social group, due to underdeveloped infrastructure and deficient business culture (Christen,

9

No global standard definition of “microcredit” exists. General practice from the experience of regulators who crafted own definitions defines at least three characteristics in local contexts, related to the use of funds, maximum amount and definition of the customer. (CGAP, 2012)

10

This fact probably stays behind the use of microfinance outreach indicators, describing mostly only credit and borrowers, while leaving behind savings and savers. This outreach was tackled by this dissertation by introducing new outreach measure, MPI.

17

2000). The Millenium Development Goals strategy, the last chapter of global development effort following the post-war predecessors such as Structural Adjustment Programs and ensuing Poverty Reduction Strategy Papers, embraced microfinance as one of the principal multidisciplinary tools of fight against poverty. In consequence, the year 2005 was

proclaimed by the UN the Year of Microcredit, followed by Nobel Prize provided to Yunnus in 2006 for his achievements in Grameen Bank, leading to world wide popularization. The sector experienced its first major downturn before the start of financial crisis in 2007 (FC), as portfolio risk increased due to deep rooted lack of controls, excessive growth and profit-orientation affecting social objectives and raising moral hazards (Lutzenkirchen,2012).

Today, in several countries microloans represent an important fraction of their GDP11 and exert strong influence on national economy. In 2013, the microfinance industry was deemed to affect 621.5 millions of poorest family members12 worldwide, serving 195 million active clients serviced by 3,703 reporting institutions (Microcredit Summit, 2013). Estimates reckon that more than 500 million entrepreneurs remain excluded (Planet Finance 2012) requiring access to microfinancial services. Despite the high margins and low default rates that conquered wide popularity for microfinance only a small part of MFIs reach

sustainability. Out of the 1300 institutions registered in 2006 in the Mixmarket database 57% were in state of financial loss (Mixmarket, 2006). Oliva-Beltrán mentions that that only1% of the MFIs are economically viable, with 200 out of estimated 10,000 MFIs concentrating majority of clients (Meehan, 2005). This phenomenon can be explained by the difficulty of graduation of the complex microfinance mechanism into sustainabity and an uncritical

popularization sector, causing a precipitous influx of activists and unexperienced businessmen with little experience and knowledge with financial administration. Speed of its development currently exceeds the evolutionary pace of the supporting subsystems such as the legal frameworks and internationally compatible nomenclature, which in turn blades the risk statistics and gives rise to new types of risks, requiring new types of financial regulation.

The pattern of the past evolution of modern microfinance described above biases its present structure. Rapid, uncoordinated expansion of a globally applicable concept, yet explicitely local and therefore varied by default, led to creation of a fragile system lacking a

11 Examples are Bangladesh (0.03), Bolivia (0.09), Kenya (0.03), and Nicaragua (0.1), as calculated using loan data from the Microfinance Information Exchange and domestic price GDP from the Penn World Tables.( Buera

et al., 2012)

12For the measurement of poverty was applied Progress out of Poverty Index (PPI), USAID Poverty Assessment Tool (PAT), FINCA Client Assesment Tool (FCAT), CGAP Poverty Assessment Tool, Participatory Wealth Ranking (PWR)

18

regulatory, taxonomic and filosofically sound base, with clearly distinguished concepts. Microfinance therefore lacks universally acceptable classification discerning social and commercial objectives and stratifying the variety of existing socio-commercial approaches, harbouring inner schism. Inconsistencies laid bare during the recent FC, with potentially serious issues being accumulated under the surface, point out that an opportunity to build a global system of socially oriented finance, may be lost if no concerted action is undertaken in a joint global effort.

Fig.1 Number of microfinance clients at present (Microcredit Summit, 2013)

2.2. Microfinance and Human Development

The term ‘human development’ refers to ‘human capabilities’, posibility of choice and a capacity to achieve well-being (Sen, 1994). ) While every human one has got the right to lead a life of quality with balanced socio-economic participation in a society, such

achievement is one of the major human rights challenges of the 21st century (UNDP, 2000) The poor and disadvantaged people are also vulnerable to different types of risks with fewer mechanisms disponible to deal with risks.

Microfinance programs provide tools of several risk management instruments to the poor and disadvantaged that permit them to take more risk, such as credit for micro enterprise and so provide them an opportunity to move out of poverty (Holzmann, Sherburne-Benz & Tesliuc 2003), and thus microcredit becomes a means of human

19

development (Holzmann & Jorgensen 2001). Credit constraints might be one of the causes of poverty (Karlan et al., 2008) and microcredit, by tackling the credit constraint, thus

contributes to human development. Access to finance may help reducing poverty in two ways: through the economic growth effect and the distributional effect (Bourguignon, 2004).

Poverty reduction thus can be achieved by growth of the average income of the population and through spill over effect of created wealth, changing the income distribution of income.

Many studies have indicated the lack of access to finance as one of the major bottlenecks for people to combat poverty (Hulme and Mosley, 1996; Beck and Demirgüç-Kunt, 2008). Microfinance can be considered merit good as it generates positive externalities such as development of social networks cemented by group lending mechanisms,

improvement of gender equality as well as financial infrastructure, including financial literacy indirectly benefitting the society in a wide scope of manners. Providing the poor with

facilities to save and to have access to credit without intervention helps them to manage risks, increase their incomes, elevate life standards, and increase their security, autonomy, self-confidence and social status within the households. By empowering members to establish their own organisations, microfinance integrates procedures on democratic basis that help people surmount conflicts. (Dunford, 2006).

Studies conducted by Hossain (1988), Mustafa et al. (1996), Khandker and Pitt (1998), Latifee (2003), Khandker (2003), on several microfinance organization’s clients in

Bangladesh found out that participation in microfinance program improved poor households ability to generate higher income in households, net working capital, fixed assets, increase spending on food, medical care and education. Khandker and Pitt (1998) showed

improvement of household welfare as a result of increasing labor market participation and children’s schooling. Sutoro (1990) in Indonesia, Mosley (1996) in Latin America, Dunn in 2005 in Bosnia also noted similar positive impacts of microcredit. Al Mamuns study

measuring the impact of af urban microcredit program on the quality of life of their low-income clients in Peninsular Malaysia, concludes that participation in microcredit program leads to improvement of therespondent’s quality of life.

Microcredit develops new markets, promotes a culture of entrepreneurship and reduces household vulnerabilities to risks and external shocks. At the community level,

microenterprises contribute to growth by bringing in income from outside the community, preventing income from leaving the community, stimulating market linkages and providing lower cost of goods and services, contributing to the economic inclusion and growth of micro-entrepreneurs through contribution to virtuous development cycles of capital accumulation,

20

investment and job creation. Improving access to financial services provides the poor the opportunity to undertake productive investments, yet, thanks to adverse selection, poor infrastructure and moral hazard problems in combination with the fact that the poor lack sufficient collateral, the underprivileged populations usually have no or limited access to finance. Beck et al. (2007) finds that higher financial development induces the incomes of the poor to rise quicker than the average income, while in particular higher financial development leads to increases of economic growth with 40 percent of the increase resulting from the reductions in income inequality, while the remaining percentage coming from the impact of financial access on economic growth. Li et al. (1998) show that income inequality differs widely between countries, while one of the explanations for these differences is explainable by capital market imperfections, as income inequality tends to be higher in countries where financial market imperfections are deeper. Gender inequality remains an important barrier to human development, as gender issues despite major progress, have not yet gained gender equity (HDR, 2010). In the past two decades, modern microfinance has become symbolic flagship of empowerment of women worldwide and important argument in the fight against gender inequality. Women are the key clientele of most microfinance programs, accounting for more than two thirds of clients as out of to the estimated 124,293,727 clients of

microfinance belong to the poorest when they took their first loan, 82.7%, or 102,749,643, were women13 (Microcredit Summit Campaign, 2012).

Women are a targeted beneficiary of the microfinancial activities, not because of their traditional disadvantage in access to financial services as to men, but since the general

experience have proved them to be more reliable, more financially responsible with better repayment performance and are more likely than men to invest their income in the household (Littlefied et al., 2003). According to Bernstein (2007), evidence indicates that societies are better off if they transfer money to women, using microfinance rather than simple cash payments to execute this transfer, since because male and female adults provide for their children unequally and children are better off when their mothers have higher incomes. Some important MFIs originated from women’s associations14 (UN, 2005). Asian Development Bank study considered gender in all aspects of microfinance projects a greater role in household generation of cash, involvement in expenditures and generation of savings,

13

Mixmarket database (2008): 704 MFIs reaching 52 million borrowers with MFIs using the solidarity lending methodology targeted 99.3% female clients and MFIs using individual lending targeted 51% female clients.

14

NABW Malawi, ATRB Nigeria, COWAN Nigeria, Zambuko Trust Zimbabwe, SEDA Tanzania, Yetemali (Guinea), CSIM Mali, MECM Mauritatnia, Zakoura Foundation Morocco.

21

ability to generate higher incomes on their own and greater role in business decisions, acquisition of more skills and expanding their network of support system, increased acquisition of assets (ODE, 2008). Women operating in groups of clients earn a voice in capital investment decisions affecting their communities and thus increase build up of the present social capital, transcending financial and economic impacts (Mayoux 1999b).

Microfinance teaches that the security one receives from holding money takes form not in a barrier from public life but in decisions, choices, investment (Bernstein, 2007). Access to financial services empowers women in becoming more assertive and more likely to participate in family and political decisions, more able to confront systemic gender inequities (Littlefied, 2003).

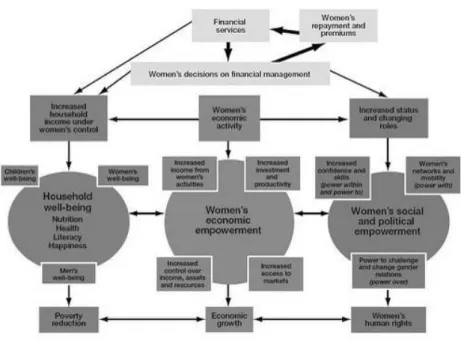

Fig. 2 Virtous spiral of empowerment of women through microfinance (IFAD, 2009)

2.3. Microfinance and Millenium Development Goals

Access to financial services helps the poor to achieve the MDGs15 in a sustainable way. Financial services enable the marginalized populations to increase incomes, and consequently diversify their human, social and economic assets. There is already enough

15

The MDGs are globally-adopted targets for reducing extreme poverty by 2015. They address income poverty, hunger, and disease; lack of education, infrastructure and shelter; and gender exclusion and environmental degradation

22

evidence to state with confidence that microfinance contributes to achievement of the Millennium Development Goals (Dunford, 2006).The positive impact of microfinance on poverty reduction is more related to the first six out of seven Millennium Goals and substantiates a beneficial affect on increases in income and reductions in vulnerability, causing microfinance to belong to stabile mainstream development tools of the present time (Morduch, 2001). Evidence shows that the poor invest in a wide scope of assets: more sane nutrition, health, access to schooling, a better facilities in their homes, and foster growth of their microbusinesses (CGAP, 2010). CGAP notes that whilst there are occasional cases of negative impact, by and large the evidence is very supportive of significant MFI impact against the MDGs. A more detailed study is provided by Morduch and Haley (2002) who compile evidence in relation to the MDGs in a substantial literature review. Their conclusion is that the MDGs contribute to six of the eight MDGs, apart from environmental sustainability and global partnerships.

Khandker’s study of from a massive survey of households participating in one of the programs of Grameen Bank and BRAC provides convincing evidence of microfinance impact on poverty, drawing from the experience of three of the world’s largest microfinance

programs with massive outreach to the poor in one of the world’s poorest countries

(Dunford,2006). German development agency GTZ states in 2005 that microfinance projects make significant, empirically verifiable contributions to attaining the MDGs, with many positive impacts are discernible, primarily in food, school education and health as well as in the status of women reflected in the society.

The goal of the dissertation, proposing a multidisciplinary, international body acting in favour of socialy empathic microfinance sector in the present complex, interconnected world of today, is precisely intended to fill in the gap, which may be of high importance as the expansion of microfinance services in developing countries is increasingly driven by commercial investors who do not assess MFIs performance according to MDG criteria (Greeley, 2005).

2.4. International funding as a backbone of the sector

The major challenge for microfinance is to reach sufficient scale in order to fill in the demand for financial services. The “absurd gap” between the supply of microfinancing and

23

the potential demand for it, reaches 3.6 billion people in developing countries without access to formal finance and 1.8 billion people representing an unmet demand for credit services (Robinson, 2001). MFIs, dependent on secured financing sources, are limited in their access to funding. Financing of their customers in consequence faces the same constraints. The lack of capital funding is universally recognized as a significant barrier for the evolution of the sector. Most MFIs are not regulated and therefore are not allowed to accept deposits from the public, and so sources of external finance are key element for MFIs. These however differ by type of institution. NGO providing microcredit usually rely on donor funding, cooperatives and credit unions gather membership fees and deposits, while the banks, limited MFIs and savings banks fund their loan portfolios with member savings and commercial loans.

Satisfying demand requires exponentially increasing cash flows, rendering existing funding resources insufficient. Despite the size of the present SRI16 market, encompassing almost a tenth of all professionally managed assets17 and despite the fact that year by year more investors seek double bottom line, 18 the importance of microfinance lacked behind among ESG19 issues. Thus, mere 0.02% of the total of European SRI flows in 2009 was channelled to microfinance according to Eurosif20. The role of microfinance as SRI asset is still marginal for SRI market, albeit crucial for the future of microfinance(Eurosif, 2010) and SRI21 is already the largest source of international funding, reaching 47% in 2005 (Eurosif, 2010). Eurosif 22 concludes that microfinance will be of significant interest to SRI investors in the upcoming future. The total funding to the sector is expected to triplicate to USD 20 bn by 2015 (Harris, 2009).

Over the last decade, the total volume as well as share of foreign funding has increased. While ten years ago external funding was almost exclusively provided by public sources, with microfinance becoming an attractive opportunity, private investors became a more important source of funding. Between 2005 and 2007, foreign investments in

16 Socially Responsible Investment 17 Est. €7.5 trillion in 2009 (Eurosif, 2010)

18 Combination of financial return and social impact 19 Environment, Social, Governance

20 The European Sustainable Investment Forum 21

The potential of the SRI market is enormous as within the period 1995 – 2010, the SRI registered 380% growth reaching $7.06 trillion (Threadneedle, 2011). During the crisis period 2007 - 2010 the universe of professionally managed assets has remained flat while SRI assets have enjoyed growth (Greenmoney, 2010). 22 The European Sustainable Investment Forum

24

microfinance increased five-fold (Deutsche Bank, 2012).The global development community acknowledges that there is no alternate to private funding, because of the limits of the

historically major source of public funding from development financial institutions. Private funding by crossborder microfinance investment vehicles (MIVs) thus provides a fundamental link between local microfinance initiatives and international sources of capital and is considered the only source capable of filling the global gap of access to finance. The total estimated investment by different international funders varies between annual 8.7 billion USD (Symbiotics, 2013) - 13 billion USD (IAMFI, 2011), out of the total microfinance loans outstanding portfolio of over $44 billion USD (Gurgaon, 2010). Almost a third (29%) of the total of microfinance funding is channeled through international financing vehicles23 and continues to grow fast (Hes et al., 2011).

Microfinancial funding needs are still neglectable in comparison to capital flows in developed countries, while the sum of human life improvement potential, raised through provision of access to financial services, is dimensionless.

2.5. Funding costs contributing to high cost of microcredit

From the beginnings of modern microfinance, its most controversial feature has been the interest rate charged by microlenders (Rosenberg et al., 2013). Overall interest rates of MFIs are high due to the elevated risk, high cost of funding, increased personal assistance to every client and higher transaction costs than the usual bank loans, eventhough significantly lower than applied by informal lenders. The high cost of microcredit, born by the poor, represents the backbone of the criticism of microfinance. As of 2011, the average annual interest rate of microfinance sector on global level was of annual 27 % (Rosenberg et al., 2013). Microfinance lending is information-intensive lending. Compared to secured

conventional bank loans, microfinance lenders require less collateral per dollar loaned. Loan monitoring is fundamental and takes place via many channels, through weekly repayments rule, frequent personal contact with credit officer and peer pressure. The monitoring and control activities permitted reduction of collateral requirements by reducing the scope for moral hazard in the use of funds. Monitoring and social sanctions are, despite all, costly

23

In 2013, there were 111 registered internationally acting Microfinance Investment Vehicles (MIVs), consisting out of 48 Fixed Income Funds, 18 Mixed Funds and 18 Equity Funds (Symbiotics MIV report, 2013).

25

substitutes for collateral (Conning, 1999). Rising monitoring and delegation costs within MFIs easily mount as outreach is extended to poorer segments of borrowers24.

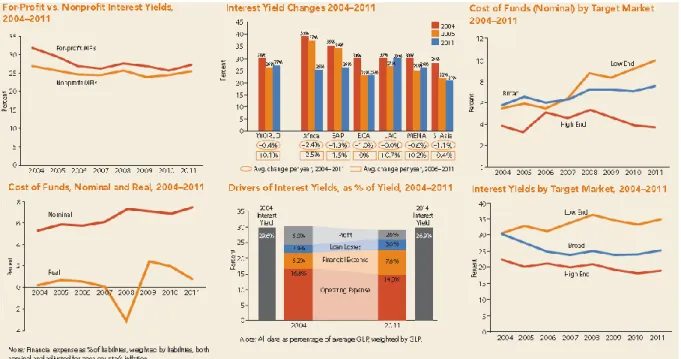

Nevertheless, the high level of microloan cost is caused not only by high operation costs, but also by high cost of funding, representing 30-40 % of of the total cost. According to CGAP, in 2011 the average percentage of financial expense was 7.8% of the interest (see Fig. 2). Paradoxically, although the global interest rates, average returns on equity, as well as the percentage of borrowers loan payments that constitute profits keep falling, lenders

focusing on a lowend clientele recorded between 2004-2011 rise of interest rates along with operating expenses and cost of funds (Rosenberg et al., 2013), which is a tendency futher confirming the dissertation thesis on the pressing need of regulation of the sector so that it would boost development by providing cheaper capital to the the poorer stratas of society rather than to the better-off clientele.

Fig 3. Global microcredit interest rates, yields, cost of funds by target market, cost of total cost funds, drivers of interest yields by target market (CGAP - Rosenberg et al., 2013)

24

The fact that operations costs of microcredit are by default high is proven by the fact that even microfinance non-profit organisations as well as cooperatives, with clients – members voting on the interest rate themselves are to pay, charge average interest rates not significantly lower than commercial microcredit, in order to maintain the MFIs within sustainability.

26

2.6. Sectoral weaknesses caused by lack of global coordination

Microfinance harbours a tension between supporters of social justice grounding and supporters of extension of financial system feasible under commercial conditions (Hes et al., 2012). Despite the convergence of view of microfinance as a tool to fight world poverty, significant debates have stirred in recent years over objectives and methods as well as appropriate regulation policies, (Morduch, 1998). Despite being local in its nature,

microfinance is substantially influenced by globally acting stakeholders. This refers not only to cross-border funding, fuelling about a third of microfinance portfolios, but more

importantly to popularization forces advancing the sectors frontiers, through technological and methodological innovations. Such involvement of leveraging powers propulsed by global consciousness as well as drives of international capital markets presents invaluable

opportunities as well as unprecedented risks for international development on planetary scale. Commercialisation in combination with excessive profit-orientation belongs to the main cause for the problems in microfinance causing transfer of wealth from the poor to MFI managers and owners, as well as increasing overindebtedness (Deutsch Bank, 2012).

Present microfinance is enwrapped in nomenclative disarray. Reputation of

microfinance may be harmed by dichotomies between rhetoric and practice or may fail the test of a serious asset class. The current groundwork has succeeded in attracting much popularity, but has neglected to build a shared regulatory base, in order to to protect both the poor and the investorship. Differences can be found in financial terminology, in MIV

nomenclature used by development financial institutions as well as by rating agencies.

Definitions differences, lack of standards, accounting, and auditing procedures default lead to the ambiguity of the information and the risk of confusion, both the client and the MFI and financial resources in the long term causing uncertainty that has implicit costs leading to an increased risk.

One of the major risks of global financing is unhedged FX risk. MFIs extend loans to their clients in local currencies and therefore hard currency investments leave them with FX exposure, increasing the danger of bankruptcies, shifting the FX risk to MFIs. According to 2013 Symbiotics MIV report, the unhedged portion of MIV investment increased more than fourfold in the past years from 2.5% in 2010 to 11.3% in 2012, with 76% of fixed-income investments to MFIs being denominated in euros or dollars, while estimated 50 % of MFIs have no access to protection from foreign exchange risk. MFIs can suffer substantial losses if

27

the value of the domestic currency starts depreciating in relation to the foreign currency,with their assets dropping relative to its liabilities (CGAP, 2006). In addition to the depreciation risk, MFIs are exposed to convertibility risk25 and transfer or remittance risk. Lack of solution to FX related uncertaneity not only creates risks for individual MFIs, but discriminates against whole regions with exotic, volatile currencies, such as Middle East and Sub-Saharan Africa.

Another problem typical for a young sector without proper regulation is that growing numbers of practitioners are relying unethical practices in developed financial markets, such as false information, usurious rates and lack of customer protection, leading to exploitation of the poor (Park, C.K., 2007). In consequence, global media antagonistically oversimplify the industry as a financial predatory endeavour, while at the same time denoting microfinance as one of the most promising tools to combat poverty.

These ethical failures usually concentrate in lack of transparent pricing, excessive rates and abusive loan recovery. Pricing transparency is essential to promote efficiency, as well as consumer protection as non-transparent pricing, common in microfinance, eliminates

imperfections generating higher margin opportunities. The consumer exploitation potential results from market failure, caused by little competition or by the misinformation of the consumership. MFIs routinely hide the real interest cost by charging interest on the face value of the loan rather than on declining balance, charge up-front fees or force security deposits deducted from the compulsory savings (Hes et al., 2012).

The inaccurate representation of portfolio quality belongs to the principal reporting weaknesses of MFIs. Discrepancies are common and many well-known institutions have experienced at least one significant portfolio crisis, sustaining delinquency and defaults above what they report to the public (CGAP, 2009). Misleading reporting leads to bankruptcies of MFIs, besides mismanagement, feable internal controls, over-indebtedness of the clientship and failures of the rating agencies to spot the coming crisis,26 which are frequent, but receive few publicity and thus get repeated in time and space, without collective knowledge being accumulated. The Andhra Pradesh case in 2006, where private microfinance program clashed with programs organized by government of Andhra Pradesh, leading to accusations of MFIs of usury, only confirms the need for neutrality and detailed, globally valid definitions of the microfinance operational standards. The neoliberal financial systems approach that has become increasingly dominant, leads MFIs to pursue sustainability through raising financial margin, expecting that MFIs will begin to wean themselves from a reliance on donor and

25

Foreign currency not available for sale. 26 Fitch Rating Agency

28

adopt banking practices, as profits are expected to attract private investment to the sector. World Bank, CGAP, USAID and other multilateral institutions have been particularly resolute in urging this approach in their guidelines, and conditioning further subsidies on the

attainment of specific performance and sustainability targets (Conning, 1999). There is however a risk that this approach can embody the Icarus Paradox, with the success of microfinance fueled by the logic of “financial systems” becoming own downfalls architect.

Advocates of what has been labeled the welfarist approach say that a focus on targeted outreach rather than outreach related to scale. They claim that an insistence on cost recovery and the elimination of subsidies would force MFIs to shed the poorest from their portfolios because they are the most costly to attend (Hulme and Mosley, 1996). Some NGOs argue that adoption of a financial systems approach will divert attention away from other important social objectives such as empowering the most vulnerable clientel, arguing that sustainable microfinance in particular, may be doing more harm than good by increasing the indebtedness of the vulnerable ones (Dichter, 1997).

2.7. Criticism of Microfinance

The critics of microfinance form a robust group amongs the development practitioners. The criticism is widespread and in many cases cemented by strong evidence. The underlying concept of the criticism is that microfinance is based on a false premise of "privatization of welfare" assuming that poor people can make themselves richer providing they have access to credit, yet wealth creation is a collective endeavour requiring skills and knowledge with functioning institutions, rather than isolated achievement. In a similar tone, while lack of access to credit can be one of contributing privations for rural poverty, the general causes of poverty are complex and cannot be simply reduced to lack of credit (Roth, 1997).

Despite positive association of MFIs with lower levels of poverty indices, most MFIs do not target the very poorest ones and therefore their importance in the quest of poverty elimination is overstated (Imai et al., 2012). The results of empirical studies give evidence that the microfinance programs aid richer segment of those considered poor, since high number of the institutions exclude the poorest ones. Mahajan states (2010) that in some cases,

microcredit even reduces cash flow to the poorest of the poor causing harm, when loans are not used for the productive use but for consumption smoothing instead. The consumption

29

smoothing leads to overindebtedness, with serious consequences for the clientele, further aggravated by the high cost of capital for the clientele, as MFIs have to charge high interest rates in order to be sustainable.

Finally, microfinance can be unsuccessful at creating prosperous small businesses in the long run and leads to overcrowding in local markets. Overcrowding results from limited options in terms of technology, skills and financial resources and microfinance doesn't solve these. Bateman (2013) concludes that the programmed shift of microfinance development policies has been a seriously adverse evolution, and it now ranks as one of the most damaging policy interventions of all time, as the expansion of microcredit thus establishes and

accelerates debilitating deindustrialisation and infantilisation of local markets.

Studies found found, in some cases, that program participation led to an increase in domestic violence for women in the short term, however over time men started to accept more of women’s participation, which eventually led to a decrease in violence in the long term (Littlefied et al.,2003)

While the criticism is a key element in the further narrowing of the sectorial evolution, it is be difficult to trace the lines of critique and to apply them to worldwide practice. Serious differences vary between microfinance organizations, policies and methodologies, yet most use same taxonomy making generalizations difficult, if not utterly incorrect. The sector is composed from townsands of particular entities operating in local markets, with their peculiar DNAs, origins and unique sets of cultural and macroeconomic constellations and most of them use same definitions for different contents27. Generalizing critique of microfinance is useless if no concrete conclusions are drawn, or unless a pattern composed from elements identical to all participants can identified, distilled and presented. It is wrong to infer from a

particular case sector wide conclusions.

Therefore, the microfinance movement should be considered a potent development force induced by a number of motives, capable of mobilizing idle elements in economy marked by a varying degree of success in execution of microfinance projects, rather than a set of fixed methods and in this view then be subjected to simple corrective actions. The incipient extension of microfinance taxonomy, making clearer distinctions between related terms in order to tackle negative issues in a more concrete way, belongs to proposals of this

dissertation.

27As an example can serve the term „microcredit“. While in developing countries it denotes small scale credit of

30

2.8. Review of selected background theories related to microfinance

2.8.1. Principal - Agent Theory and the role of collateral

Principal-Agent Theory proposed in the works of Ross and Mitnick, and further expanded in the 1980s by Fama and Jensen analyzes information asymmetry in a principal-agent relationship, arising when a principal contracts an principal-agent to act on his behalf. The deviation from the interest of the principal by the agent, the 'agency costs' consist of the costs inherently associated with using an agent and the costs of techniques to mitigating the

problems associated with a use of an agent or employing mechanisms to align the interests of the agent and of the principal.

Credit relationships exhibit characteristics of an agency problem, as agents, the borrowers, act on behalf of the principal, the lenders, whose funds must be repaid.

Information asymmetries usually arise in agency relationships because one of the parties owns privileged information. In a lender-borrower relationship, the principal can be unable to monitor the actions or the type of the agent. Consequently, the principal must invest resources to recognize agent types or to induce agents to undertake actions not damaging the interests of the lender.

Collateral is a key feature of a loan contract and a partial solution to principal-agent problem, present in microfinance. Collateral helps MFIs to solve two main problems. It limits losses in the case of default, but it also solves the problem of asymmetric information between MFIs and borrowers. Theories about collateral and the asymmetric information problem consider collateral either as a signaling instrument providing MFIs with information about the borrower’s quality as quality borrowers know that the chance of default on the loss of their collateral is unlikely and therefore are more willing to pledge collateral in compensation of more favorable contract terms than low-quality borrowers. Hence, collateral helps reduce adverse selection by signaling (Stiglitz and Weiss, 1981).

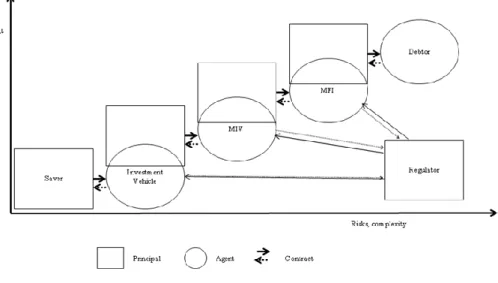

CGAP (2008) identifies poor governance as a major obstacle to MFI growth, attributing the major hindrance to principal-agent problems, also because an important part microfinance sector is fuelled by external funding and therefore burdened with extremely high information assymetry. A principal-agent relationship is central to the microfinancing issues, as it leads to increase of cost of capital as well as loss of information originating on all levels

31

of financial intermediation tandems: between general public affected by negative externalities of systemic risks in the role of principals and government regulator in the role of agents, between government regulators in the role of principals delivering will of political electorate to financial-intermediaries management in the role of agents, between financing MIVs and MFIs, between marginalized populations affected by poverty and global development advocates in their role of agents and in obvious principal-agent problem within lender

borrower relationship between microfinance managers and debtorship, contributing to market failures in financial sector.

Fig. 4 Multiple principal-agent relationship from the point of view of microfinance institutions, with every tandem relationship increasing the cost of funds

2.8.2. Welfare economics

Welfare economics uses microeconomic techniques to evaluate well-being of population within an economy, analyzing social welfare of the individuals. Welfare

economics stipulates a welfare improvement in Pareto efficiency28 terms, treats income and goods distribution, including equality, in reference to the overall welfare of the society. The approach has been influential in development policy circles where the emphasis on multi-dimensionality has shaped the evolution of the Human Development Index measure. There are two most important approaches to welfare economics: the Neoclassical School and

28

32

the approach of New Welfare Economics. Neoclassical approach developed

by Edgeworth, Sidgwick, Marshall, and Pigou assumes that utility is cardinal,

scale-measurable by observation and that all individuals having comparable utility functions. Based on the mentioned assumptions, it is possible to calculate the total social welfare

function simply by adding up the individual utility functions. The New Welfare approach recognizes the differences between the efficiency and the distribution aspects and treats them differently, while efficiency is measured by ordinal utility. Inefficiencies, as understood by welfare economist also present in microfinance are market failures, externalities, imperfect market structures, social cost, price discrimination and asymmetric information

related principal–agent problems.

2.8.3. Human Development Theory

Human development theory belongs into the framework of welfare economics and explores the issues studied by welfare economics and considers them fundamental to the development process. It focuses on measuring well-being and uneconomic growth that comes at the expense of human health as well as seeks to evaluate economic policies in terms of their effects on the well-being of all members of the community. It goes further in seeking how to optimize well-being by some explicit modeling of how social capital can be deployed to optimize the overall sum of human capital in the community. The most famous proponent of human development theory is Amartya Sen, the co-author of modern measurement of HDI, a measure successfully displacing the focus of attention of the states from mechanical indicators of economic progress as GNP and GDP to indicators that come closer to reflecting the well-being of populations.

The theoretical foundations laid by Human Development Theory encouraged policy makers to pay attention to replace the lost income of the marginalized populations, as, for example, through state funded works projects, and to maintain stable prices for food, as well as to social reforms leading to improvements in education and public health,as precedents to economic reform.

33 2.8.4. Gender Inequality Theory

Gender inequality is a fact of life in many worlds regions, particularly in developing countries (Cuberes et al., 2012). Gender-inequality theory is one of main types of feminist theories29 that attempt to understand the differences between men and women in the society, forming part of mainstream Human Development theory and belonging to the framework of Welfare Economics. Gender-inequality theory postulates that women's experience of social existence is profoundly unequal to men's. Supporters of the theory argue that women have the same capacity as men, but that patriarchy and the sexist patterns of the division of labor, has denied women the opportunity to participate in the life of societies, leading to gender

stratification harmful for the society, benefiting the rich at the expense of the poorest ones. Feminist gender inequality theoretics deny the historical inevitability of the division of labor between sexes and argue therefore that goals of poverty alleviation should also include measurements of empowerment as a sign of well-being, as women have been isolated to the household spheres and left without a role in the public sphere. According to feminists, the sexual division of labor needs to be shifted in order for women to achieve equality(Anderson

et al., 2009; Ritzer et al., 2004).

3.

Review of contemporary risk transfer innovations

Risk30 is a notion understood in many distinct ways in different cultural contexts. In broad terms, the risk is considered as a potential that an action will lead to an possibility of loss, being the undesired deviance from the norm measured in different ways and can be distinguished from uncertainty as risk can be measured. Where as Holzheu and Douglas (1993, 1994) argue that risk is socially constructed as each society decides what is to be feared, financiers consider risk to be neutral and quantifiable. In finance, risk is a probability that the return achieved on an investment will differ from the expected outcome, including the possibility of loss of the original investment.

Risk is at the heart of financial intermediation including microfinance (Gonzalez,

29

Gender Differences, Gender Inequality, Gender Opression, Structural Oppression (Crossman, 2013).

30

The neologist term appeared in the Middle Ages when the term „risicum“ was used in sea trade operations and its ensuing legal problems of loss and damage (Luhmann, 1996).