729

Copyright © 2011-15. Vandana Publications. All Rights Reserved.

Volume-5, Issue-2, (April-2015)-International Journal of Engineering and Management Research Page Number: 729-737

Customer Perception on Mobile-Banking in Chhattisgarh

Ms. ChandrawatiNirala1, Dr Smt.B.B Pandey2 1

Research Scholar, Guru Ghasidas Vishwa Vidyalaya, Bilaspur (C.G), INDIA 2

Assistant Professor, Guru Ghasidas Vishwa Vidyalaya, Bilaspur (C.G), INDIA

ABSTRACT

India, which has 600 million active mobile phone connections, according to the Telecom Regulatory Authority of India (Trai), has one of the highest mobile penetrations in the world. But mobile banking as a concept is yet to take off in a big way even among the educated masses. The comfort with which people use internet banking to perform various banking transactions is yet to be seen in using a mobile as a tool for banking. Marketing challenges for banks are:-Competition, More demanding customers, Customers want services at less cost,Get services as quickly as possible.Issues like Customer Perception/awareness and Lack of new technological knowledge. A sample of 100 bank customer is chosen. Data is gathered through Questionnaire followed by small discussion with customers. Descriptive analysis is applied for interpretation. This paper explores the effect of Technology on Mobile banking. The purpose of paper is to find factor affecting customer perception towards usage of Mobile banking, shown light on barriers in Mobile banking services which will help the banks for improvement.

Keywords---- Customer Perception, Mobile banking.

I.

Due to the technological advancement banks have successfully improved its services and operations. Mobile banking has emerged as a popular mode of banking in India.

INTRODUCTION

Mobile banking has huge potential in a country like India where a major part of the population belongs to the unbanked category. The high penetration levels of mobile phones and low transaction costs involved in mobile banking are likely to be the potential growth drivers for these services. Almost of all mobile users now use their mobile for financial transactions. Although nearly all Indian banks provide some form of mobile banking service. I

Over the mobile phone which would include using the internet browser on the mobile phone to access the bank website and then do any of the financial

activities like paying utility bills, transferring money, paying an insurance premium, etc. Or using a mobile Application for easy and simple access to the Bank Mobile website to perform financial activities like viewing the bankbalance, transferring money, etc.

t is expected that all mobile users will bank online within the next year.

Banking and Mobile Phone

SMS banking is a type of technology-enabled service offering from customers, permitting them to operate selected banking services over their Telephone banking is a service provided by a othe perform without the need to visit a than branch opening times, and some financial institutions offer the service on a 24-hour basis. From the bank's point of view, telephone banking reduces the cost of handling transactions by reducing the need for customers to visit a bank branch for non-cash withdrawal and deposit transactions.

An overview of banking sector in Chhattisgarh

Chhattisgarh Banking & Finance plays a significant role in the over-all progress of the economy of the state. Banking sector of the sate involves a wide gamut of operational transactions such as cash withdraw and deposit various types of loans, acceptance and encashment of cheques, among many others.

Providing a number of flexible financial services like that of home loans, ATMs, car loans etc, the banking and financial institutions of the state forms a compatible base on which factors of economic growth gain a positive dimension. Almost all the nationalized banks of India are present in each of the districts of Chhattisgarh. State Bank of India, Union Bank, Vijaya Bank, Allahabad Bank, United Bank of India, syndicate Bank and Oriental Bank of Commerce are some of the prominent financial institutions that are present in the state of Chhattisgarh. Treating customers with all the advanced financial facilities, the banking & finance industry of the state strives to perform better than the best of all other fiscal organizations of India.

730

Copyright © 2011-15. Vandana Publications. All Rights Reserved.

Chhattisgarh recorded the highest growth of17.4 per cent y-o-y in the number of bank offices. There are 1,900 banking offices in the state as on September 2013. Over 42 per cent of the total SCB offices in the state belong to Nationalised banks, which grew by 20.7 per cent. This growth in Nationalised banks was highest among all major states in India. The private sector banks saw a growth of 24 per cent to 155 banking offices. Chhattisgarh topped the list with a growth of 6.8 per cent in the total bank offices across all major states. The spurt in offices of Regional rural banks was mainly seen in this quarter. These offices increased by 12.8 per cent over the June 2013 quarter.

Rationale of the study

The Indian banking system has the largest branch network spread over a vast area. In the era of cut throat competition, the survival of any bank depends upon the perception of customers. In this competitive market, irrespective of public, private and foreign banks, every bank need to deliver a more efficient, customer-focused and innovative offering than ever before to retain their existing customer and attract more number of prospective customers.

In the modern customer oriented era, every customer demands better services and advanced kind services from the banks, for that banking sector is striving hard to become increasingly customer-centric in order to survive and stay in the market for a longer period. Service quality, customer satisfaction, customer perception, customer loyalty, customer delight are major challenges for private and public sector banks.

II.

METHODOLOGY

The present study is based on primary data. The information relating to the customer perception towards Mobile banking by the banks in Bilaspur city is collected for the study through survey with the help of questionnaire. The total sample size of the study is 100. To meet up with the objectives of study 100 customers were selected as sample unit. So, the questionnaires were filled by 100 respondents which were structured with questions of demographic profile, mobile banking services and dimension in which derives perception to the customers.

To carry out the study in more accurate Probability sampling technique is being selected. We are chosen random selection method. In Bilaspur city we chosen four banks namely Bank of India, Bank of Baroda, State bank of India and Punjab National Banks. Customers of these banks are our respondent. Using coding method for analysis of data.

We have done personal interviews and we asked the person in front of us to fill the questionnaire.

Descriptive Research Design: It seeks to determine the answers to who, what, where, when and how questions. It is based on some previous understanding of the matter. Descriptive Research Design is used in this study because it will ensure the minimization of bias and maximization of reliability of

data collected. Research has got a very specific objective and clear cut data requirements.

III.

PRIOR APPROACH

Mobile banking

Varshney (2004)Mobile banking (also known as M-Banking, m-banking, SMS Banking etc.) is a term used for performing balance checks, account transactions, payments, credit applications etc. via a mobile device such as a mobile phone or Personal Digital Assistant (PDA).it is the convenient, simple, secure, anytime and anywhere banking.. Many new e-commerce applications will be possible and significantly benefit from emerging wireless and mobile networks. These applications can collectively be termed wireless e-commerce or mobile e-commerce.

Laforet (2005) research on customer attitude and adoption of Mobile banking showed there are several factors predetermining the customer’s attitude towards online banking such as person’s demography, motivation and behaviour towards different banking technologies and individual acceptance of new technology. It has been found that customer’s attitudes toward online banking are influenced by the prior experience of computer and new technology.

Wadhe (2013) customers are aware about Mobile banking service provided by their bank. Customers are familiar about various banking transactions that can be done with the help of Mobile banking. Customers think that Mobile banking is easy to use; it is very useful for them as it will give them flexibility to do transactions irrespective the time of day. Customers think that major advantage of Mobile banking

Internet Banking

According to Singhal (2008)factor analysis results indicate that ‘utility request’, ‘security’, ‘utility transaction’, ‘ticket booking’ and ‘fund transfer’ are major factors. Out of total respondents’ more than 50 % agreed that internet banking is convenient and flexible ways of banking and it also have various transaction related benefits. Thus, Providing Internet banking is increasingly becoming a “need to have” than a “nice to have” service.

Ramanigopal(2011) educational level of respondents influence the use of internet banking facility and highly satisfied with secrecy maintenance, transaction updating, account transfer and security followed by easy access while using the internet banking services. The success of Internet banking not only depends on the technology but also on, to the large extent the attitude, commitment and involvement of the operating at all levels and how far the customers reap the benefits from Internet banking services.

731

Copyright © 2011-15. Vandana Publications. All Rights Reserved.

India only environment that surrounds the publicdetermines the behaviour and decisions of the individuals. So if customer meets most of their colleagues or friends who are using Internet banking. Which may influence their decision to follow Internet banking option?

Technology Based Banking

Barnes (2002) WAP banking is another form of the Electronic banking that enables the user to communicate interactively with the bank. For this communication the client uses only GSM mobile phone with WAP service. With its options and the method of controlling WAP banking reminds an easy form of Internet banking. WAP is a universal standard for bringing Internet-based content and advanced value-added services to wireless devices such as phones and personal digital assistants (PDAs).

Benamati (2007) the adoption of electronic banking forces customers to consider concerns about password integrity, privacy, data encryption, hacking, and the protection of personal information.

IV.

OUR APPROACH

1.

OBJECTIVE OF STUDY

2.

Mobile Banking is important for Sustainability.

3.

To study what factors influence the usage of Mobile banking?

4.

To study the barriers of Mobile banking?

LIMITATION OF STUDY

This survey cover only 4 banks Bank of India (BOI), Bank of Baroda (BOB), Punjab National Bank (PNB) and State Bank of India (SBI). The scope of study is limited to Bilaspur city only.

ANALYSIS

Mobile banking in India seems to be catching on. Over the past two years, it has grown rapidly.

Here are five things that reveal the fast growing trend:

To analysis customer perception towards Mobile banking.

1. Mobile banking customers: The number of mobile banking users has jumped to 3.55 crore in 2013-14. In 2012-13, there were 2.25 crore mobile banking users. This number was merely 59.6 lakh in 2010-11. There is still a long way to go though. The total number of mobile phone users in India is 90 crore.

2. Transactions surge: The number of mobile transactions has surged dramatically as a result. There were 9.4 crore transactions as a result of the sharp rise in mobile banking users in 2013-14. In the year-ago period, the number of transactions was only 5.3 crore. This

means more people are increasingly relying on mobile transactions.

3. Value rising too: The value of mobile transactions jumped more than four times in just one year. Mobile users have found convenience in the use of mobile phone to transfer money. They are transferring more money through mobile phones than ever before. The total value of money transferred through mobile phones surged to Rs 22,400 crore in 2013-14 from Rs 5,130 crore in 2012-13.

4. Mobile for cost-saving: The RBI deputy governor has pointed out that banks should see mobile banking as an avenue of cost-saving rather than revenue generation. This means, the cost of bank transactions should go down sharply making it convenient for more people to use the banking system. This probably aligns with the government’s agenda of financial inclusion.

5. Electronic payments

M-banking services have no doubt promoted economic and sustainable development in the Indian economy at least, to a large extent. It is an invaluable and powerful tool for driving development, supporting growth,

promoting innovation and

enhancing competitiveness. Businesses, banks and other financial service industries are now turning to IT to improve business efficiency, service quality, attract new customers and retain already existing customers’ loyalty. M-banking has no doubt experienced explosive growth and has transformed the traditional payment practices and it has gradually led to a paradigm shift in marketing practices resulting in high performance in the financial service industry.

: There is an increasing trend towards electronic payment. According to RBI data, the National Electronic Fund Transfer or NEFT transactions grew over 60% in volume in 2013-14. The usage of debit cards has grown 28% during the same period. This shows an interest in making electronic payments from individuals. The government has given a boost to the Aadhaar project initiated by the previous United Progressive Alliance or UPA government. If Aadhaar is used for verification by mobile phone companies and banks, it could boost mobile banking usage.

732

Copyright © 2011-15. Vandana Publications. All Rights Reserved.

1. Demographic profile of the respondents

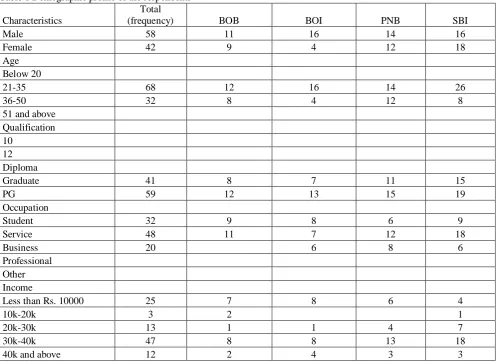

Table 1 Demographic profile of the respondents

Characteristics

Total

(frequency) BOB BOI PNB SBI

Male 58 11 16 14 16

Female 42 9 4 12 18

Age Below 20

21-35 68 12 16 14 26

36-50 32 8 4 12 8

51 and above Qualification 10

12 Diploma

Graduate 41 8 7 11 15

PG 59 12 13 15 19

Occupation

Student 32 9 8 6 9

Service 48 11 7 12 18

Business 20 6 8 6

Professional Other Income

Less than Rs. 10000 25 7 8 6 4

10k-20k 3 2 1

20k-30k 13 1 1 4 7

30k-40k 47 8 8 13 18

40k and above 12 2 4 3 3

Tables 1: shows the demographic descriptive statistics of the respondents from the selected banks. Gender as a personal variable was found to have a significant role in customer’s banking technology adoption. From the Table 1, it is found that BOB*, BOI*, SBI* and PNB* bank’s male respondents are more.

Qualification is the factor that makes the customer aware of the banking technology and also helps them in easy adoption. Among the four banks SBI bank has more qualified PG customers.

Note BOB: - Bank of Baroda, BOI:-Bank of India, SBI: - State Bank of India, PNB: - Punjab National Bank

2. General Question about Mobile- Banking.

Respondent %

General Question Yes No Uncertain

1 Do you know about Mobile Banking 98 2 0

2 Have you experience to operating Mobile Banking 60 30 10

3 Is you bank provide Mobile Banking facility 75 20 5

733

Copyright © 2011-15. Vandana Publications. All Rights Reserved.

Graph 1Interpretation:-98% Respondents know about Mobile Banking. But they don’t know how they can do transaction on Mobile phone, almost all respondent willing to use this banking facility.

3. Source of awareness for mobile banking

How do you know about Mobile Banking Respondent %

1 Television 29

2 Internet 22

3 From bank employee 15

4 Newspapers/ Magazines /Other Print ads 6

5 Friends/ family/ Colleagues using the service 28

Graph 2

Interpretation:-By survey design all respondent aware of Mobile banking. Television is the top source of awareness. Followed by friend /family/colleagues and Internet.

98

60

75

95

2

30

20

2

0 10 5 3

0 20 40 60 80 100 120

Do you know about Mobile

Banking

Have you experiance to operating Mobile

Banking

Is you bank provide Mobile Banking facility

Are you intrested to using this

facility

1 2 3 4

Respondent % Yes

Respondent % No

734

Copyright © 2011-15. Vandana Publications. All Rights Reserved.

4. What led to the usage of mobile banking

Sr.No. Factors influence the usage of Mobile banking

Strongly

Agree Agree Neutral Disagree

Strongly Disagree

1 Mobile phone is an easy to use device 96 4 0 0 0

2

I started using Mobile Banking as most of my

friends and colleagues were also using it 59 24 7 10 0

3 I am interested in new technologies 64 36 0 0 0

4 Can do banking anytime/ anywhere 53 12 35 0 0

5

Banking through the mobile saves a lot of time

52 48 0 0 0

6

Ability to conduct any financial transaction(railway

ticket, bill payment etc) 85 15 0 0 0

Strongly Agree Agree

Neutral Disagree

Strongly Disagree

0 10 20 30 40 50 60 70 80 90

100 96

59 64

53 52

85

4

24 36

12

48

15

0 7

0

35

0 0

0 10

0 0

0 0

0 0

0 0

0 0

Strongly Agree

Agree

Neutral

Disagree

735

Copyright © 2011-15. Vandana Publications. All Rights Reserved.

Interpretation:-When asked what attracted them to the service, the comfort and convenience of using their cell phone emerged as the top reason for most users. All segments of individuals and households have one and are adept at using it. The idea of doing basic banking on such a familiar device is the immediate attraction of mobile banking.

5. Barriers of Mobile Banking

Sr.No. Barriers of Mobile Banking

Strongly

Agree Agree Neutral Disagree

Strongly Disagree

1 At times there is no mobile network available 89 10 1 0 0

2 It is expensive to use the mobile for such activities 66 31 3 0 0

3

Mobile banking is not a secure and safe mode to do financial

transactions 32 27 27 14 0

4 Mobile banking is too complicated to use 29 24 11 32 4

5 Data transmission is very slow on the mobile 91 8 0 1 0

6 Lack of acknowledgement/receipt of the transaction at times 100 0 0 0 0

7 Most of the customers prefer traditional (Branch) banking 61 3 0 27 9

8 Some Banks charge high fees on using m-banking services 90 10 0 0 0

9 There is no human interface 74 19 0 7 0

Graph 4

736

Copyright © 2011-15. Vandana Publications. All Rights Reserved.

6. SMS Banking services

SMS Banking services Yes No

1 Periodic Account Balance Report 80 20

2 Reports of Credits on Account 100 0

3

Reports of withdrawals on

accounts 100 0

4

Minimum average monthly

balance 50 50

5 Tax filed alert 50 50

Interpretation:-Respondent of Chhattisgarh didn’tdifferentiate Mobile and SMS Banking. Interviewing with respondent knowing that they are availing of SMS services provided by bank. At the time of opening form customers are mention their Mobile number to get benefit of these services.The entire respondent get SMS alert at the time of Dr and Cr from their account.

7. Telephone Banking services

Telephone Banking services Yes No

1 Check a/c balance 40 60

2 Request new cheque book 74 26

3 Mini statement 21 79

4 Know about bank products 66 34

5 Purchase bank product e.g. Account opening 56 44

6 Stop cheque payments 36 74

Interpretation:-With the Help of toll free no/ customer care no of each bank respondent can do all this transaction on Mobile phone. Respondents use these services for requesting new cheque book, and know about bank product

FINDINGS

Table 1 describes the demographic profile of respondent. Male and Female ratio is 58:42. Male ratio is more it shows they are more interested in mobile banking. 68% customers are fall into age group 21-35. It shows Youth are more technology adopter. Among all four banks SBI customer are more qualified PG customer.

98% Respondents know about Mobile Banking. But they don’t know how they can do transaction on Mobile phone almost all respondent willing to use this banking facility.

By survey design all respondent aware of Mobile banking. Television is the top source of awareness. Followed by friend /family/colleagues and Internet.

Mobile phone is easy to operate; comfort ability and convenience are the main factor which leads to usage of Mobile Banking.

Mobile network is not available sometimes; lack of acknowledgement and its expensive to use i.e. transaction charges is more are the barriers in Mobile Banking.

V.

CONCLUSION

India mobile banking services are growing with the rapid growth. To better understanding of Mobile banking sector, we should know customer perception

towards these services. This survey present top source of awareness for Mobile banking are Televisionand Internet. Customer using Mobile banking because they dissatisfied from traditional modes of banking. Comfort and convenience are two important factors which influence customer to use Mobile banking. Technology problem and security concern are the biggest barrier for Mobile Banking. Banks Customer of Chhattisgarh are willing to avail all Mobile Banking services but due lack of technical knowledge and poor information structure i.e. network problem they are not properly utilized these services.

REFERENCES

[2] Barnes,S.(2002). Provision of Services via the Wireless Application Protocol: A Strategic Perspective. Electronic Markets, 12, 14-21.

[3] Benamati, S.(2007). Trust and Distrust in Online Banking: Their Role in Developing Countries. Information Technological for Development, 23, 161-175.

[4] Laforet, S., Li, X. (2005). Customer Attitudes Towards Online and Mobile Banking in China. International Journal of Bank Marketing, 23, 362-380. [5] Morawczynski, O. Miscione, G. (2008). Exploring Trust in Mobile Banking Transactions: The Case of

M‐Pesa in Kenya, Social Dimensions of Information and

737

Copyright © 2011-15. Vandana Publications. All Rights Reserved.

[6] Ramanigopal, C.S., G. P. (2011). CustomerPerception towards Internet Banking Services with Special Reference to Erode District. Asian Journal of Business and Economics, 1.

[7] Singhal, D.V. (2008). A Study on Customer Perception Towards Internat Banking: Indentifying Major Contributing Factor. The Journal of Nepalese Business Studies, V No.1, 111.

[8] Suriyamurthi,S., V. M. (2012). A Study on Customer Perception Towards Internet Banking. International Journal of Sales & Marketing Management Research and Development, 2 (3), 15-34.

[9] Varshney,U., R. V. (2004). A Framework for the Emerging Mobile Commerce Application. 10.

[10] Wadhe, P.A., S. G. (2013). To Study Customer Awareness & Perception Towards Usage of Mobile Banking. IBMRD's Journal of Management & Research .

Website

[2] http://indianexpress.com/article/technology/mobile-tabs/top-5-smartphone-brands-in-india-in-2014/

[3]