Introduction

Customer Relationship Management (CRM) is an intelligent blend of marketing and information technology for serving the customers with greater care and value. CRM is a process of identifying, attracting, differentiating and retaining customers. It is a comprehensive approach for creating, maintaining and expanding customer relationship. CRM is the outcome of the continuing evolution and integration of marketing ideas and newly available data, technologies and organizational approaches. Bank as a service organization have excellent reasons to adopt a comprehensive CRM strategy. Customer needs, wants, desires keep changing day by day. Therefore it is necessary for the banks to adopt the changes in the market through tracking the customer wants and the needs. This is possible only when the organization has a close contact with its customers. Since customer is the life blood of any business organization and customer creation cost is costlier than customer retention cost, thus bank adopt CRM techniques for maintaining life relationship and by which they ensures customer loyalty and retention.

Statement of the Problem

The Customer Relationship Management (CRM) is a strategy evolved by the banks to solve the purpose of improving the marketing productivity and enhance mutual value for the parties involved in the relationship. It has the ability to increase the marketing effectiveness and efficiency that improve the marketing productivity and creates mutual values. Though the banks are aiming at improved customer relationship, the strategies evolved through CRM are not reaping the desired benefit to the banks. This throws an alert to the banks to analyse the challenges faced by them. The researcher has made an attempt to study the problems faced by the customers in respect of CRM practices in public sector banks.

* Head & Associate Professor of Commerce, St Xavier College, Palayamkottai ** Ph.D Research scholar, Dept of Commerce, St Xavier College, Palayamkottai

A Study on Problems Faced by the Customer in Relation to

Customer Relationship Management Practices

Objectives of the Study

1. To study the problems faced by the customers of the public sector banks in relation to CRM practices.

2. To analyse the problems faced by customers in relation to CRM practices

Hypothesis of the Study

• Ho: There is no significant difference in the problems relating to customer relationship management among the respondents in relation to their gender and age group.

Methodology

Source of the study

The data required for the study were collected from both primary and secondary sources. The primary data has been collected directly from the account holders of public sector banks by using interview schedule. The secondary data has been collected from the published journals, books, magazine and websites.

Sampling Design

The study is confined to account holders of the public sector banks in Tirunelveli District. There are188 branches for the public sector banks in Tirunelveli district. Out of 188 branches of the public sector banks, four public sector banks namely State bank of India is having 25 branches, Canara bank is having 35 branches, Indian bank have 24 branches and Indian overseas bank has 69 branches. The leading four public sector banks which are having 153 branches were taken for the study. From each of the 153 branches 4customers were selected randomly. In total 612 sample customers were selected from the major public sector banks.

Tools for Analysis

The data collected were processed further with the help of the appropriate statistical tools to analyse the data and to derive inferences. The statistical tool namely ANOVA test has been used for the analysis and to interpret the data.

Problems Relating to Customer Relationship Management

network of branches spread over the entire country with millions of customers, a complex variety of products and services offered, the varied institutional framework - all these add to the enormity and complexity of banking operations in India giving rise to complaints for deficiencies in services. This is evidenced by a series of studies conducted by various committees such as the Talwar Committee, Goiporia Committee, Tarapore Committee, etc., to bring in improvement in performance and procedure involved in the dispensation of hassle-free customer service.

The present paper presents the relationship between different types of problems in relation to customer relationship management of public sector banks such as operation of account related problem, enquiry counter related problem, problem related to technologies, employee related problem, ATM related problem, consultancy related problem and safe custody problem and the profile variables of the respondents.

Operation of Account Related Problem

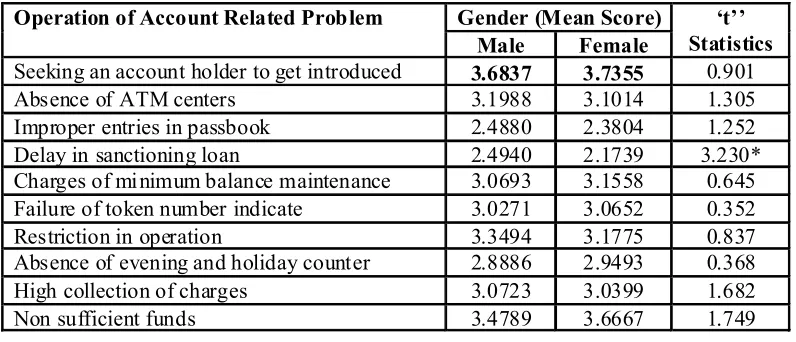

Respondent's problem about operation of account in relation to Gender

In order to find out the significant difference in operation of account related Problem among different gender group of customers of public sector banks in Tirunelveli

district, 't' test is attempted with the null hypothesis that, "there is no significant difference in operation of account related problem among different gender group of customers of Public sector banks in Tirunelveli district". The result of 't' test is presented in the Table 1.

Table 1 : Respondent's problem about operation of account in relation to Gender

Operation of Account Related Problem Gender (Mean Score) ‘t’’ Statistics Male Female

Seeking an account holder to get introduced 3.6837 3.7355 0.901

Absence of ATM centers 3.1988 3.1014 1.305

Improper entries in passbook 2.4880 2.3804 1.252

Delay in sanctioning loan 2.4940 2.1739 3.230*

Charges of mi nimum balance maintenance 3.0693 3.1558 0.645 Failure of token number indicate 3.0271 3.0652 0.352

Restriction in operation 3.3494 3.1775 0.837

Absence of evening and holiday counter 2.8886 2.9493 0.368

High collection of charges 3.0723 3.0399 1.682

Non sufficient funds 3.4789 3.6667 1.749

Source: Primary data *Significant at five per cent level

operation of account related problem among the different gender groups of respondents is identified in the case of operation of account related problem variable 'delay in sanctioning loan' since its 't' statistics is significant at 5 per cent level. So the null hypothesis is rejected.

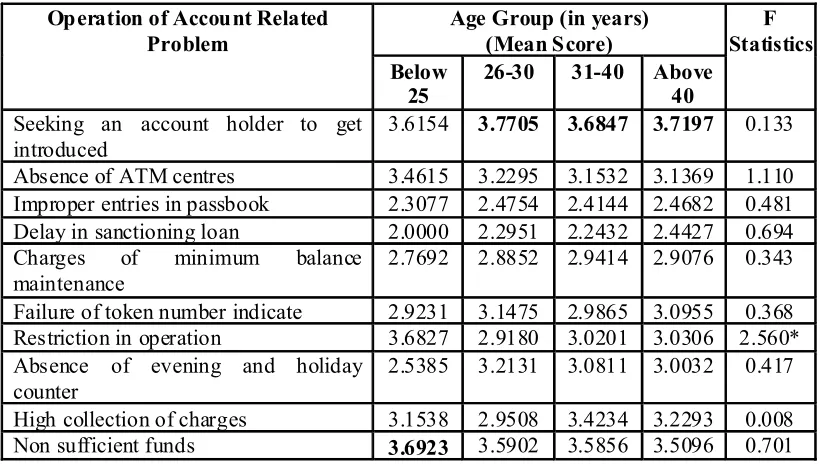

Respondent's problem about operation of account in relation to Age

Customers of different age groups face operation of account related problem at different level. In order to find out the significant difference in operation of account related problem among different age groups of customers of public sector banks in Tirunelveli district, 'ANOVA' test is attempted with the null hypothesis that , "there is no significant difference in operation of account related problem among different age groups of customers of public sector banks in Tirunelveli district". The result of 'ANOVA' test is presented in the Table 2.

Table 2 : Respondent's problem about operation of account in relation to Age

Operation of Account Related Problem

Age Group (in years) (Mean Score)

F Statistics Below

25

26-30 31-40 Above 40

Seeking an account holder to get introduced

3.6154 3.7705 3.6847 3.7197 0.133

Absence of ATM centres 3.4615 3.2295 3.1532 3.1369 1.110 Improper entries in passbook 2.3077 2.4754 2.4144 2.4682 0.481 Delay in sanctioning loan 2.0000 2.2951 2.2432 2.4427 0.694 Charges of minimum balance

maintenance

2.7692 2.8852 2.9414 2.9076 0.343

Failure of token number indicate 2.9231 3.1475 2.9865 3.0955 0.368 Restriction in operation 3.6827 2.9180 3.0201 3.0306 2.560* Absence of evening and holiday

counter

2.5385 3.2131 3.0811 3.0032 0.417

High collection of charges 3.1538 2.9508 3.4234 3.2293 0.008 Non sufficient funds 3.6923 3.5902 3.5856 3.5096 0.701

Source: Primary data *Significant at five per cent level

Enquiry Counter related Problem

Banks' systems should be oriented towards providing better customer service and they should periodically study their systems and their impact on customer service. Banks should have a Board approved policy for general management of the branches which may include the following aspects:-(a) providing infrastructure facilities by branches by bestowing particular attention to providing adequate space, proper furniture, drinking water facilities, with specific emphasis on pensioners, senior citizens, disabled persons, etc. (b) providing entirely separate enquiry counters at their large / bigger branches in addition to a regular reception counter. (c) displaying indicator boards at all the counters in English, Hindi as well as in the concerned regional language. Business posters at semi-urban and rural branches of banks should also be in the concerned regional languages.

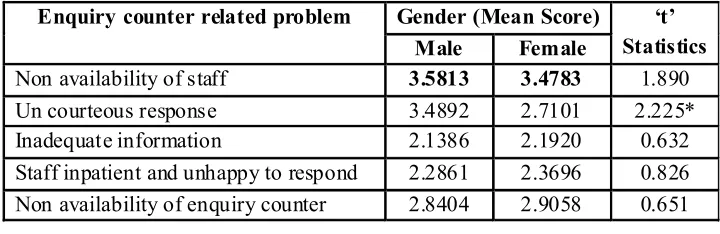

Respondent's problem about Enquiry Counter in relation to Gender

In order to find out the significant difference in enquiry counter related problem among different gender group of customers of public sector banks in Tirunelveli district, 't' test is attempted with the null hypothesis, "there is no significant difference in enquiry counter related problem among different gender group of customers of public sector banks in Tirunelveli district". The result of 't' test is presented in the Table 3.

Table 3 : Respondent's problem about Enquiry Counter in relation to Gender

Enquiry counter related problem Gender (Mean Score) ‘t’ Statistics Male Female

Non availability of staff 3.5813 3.4783 1.890

Un courteous response 3.4892 2.7101 2.225*

Inadequate information 2.1386 2.1920 0.632

Staff inpatient and unhappy to respond 2.2861 2.3696 0.826 Non availability of enquiry counter 2.8404 2.9058 0.651

Source: Primary data *Significant at five per cent level

From Table 3, it is understood that 'non availability of staff' is the important enquiry counter related problem among the male and female customers as their mean scores are 3.5813 and 3.478. As regards the enquiry counter related problem, significant difference among the different gender groups of customers are identified in the case of 'un courteous' response, since the 't' statistics is significant at 5 per cent level, the null hypothesis is rejected.

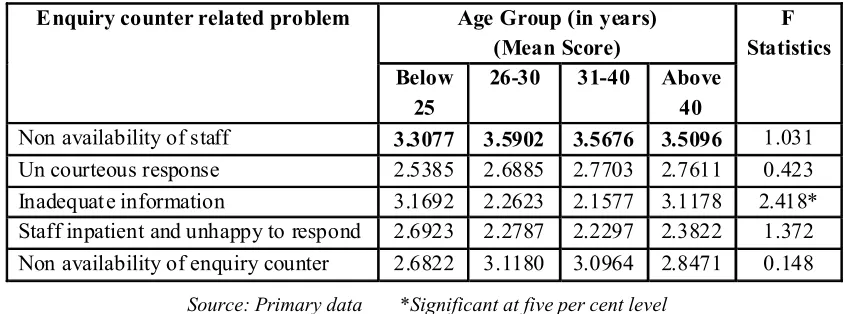

Respondent's problem about Enquiry Counter in Relation to Age

age groups of customers of public sector banks in Tirunelveli district". The result of 'ANOVA' test is presented in the Table 4

Table 4 : Respondent's problem about enquiry counter in relation to Age

Enquiry counter related problem Age Group (in years) (Mean Score)

F Statistics Below

25

26-30 31-40 Above 40

Non availability of staff 3.3077 3.5902 3.5676 3.5096 1.031 Un courteous response 2.5385 2.6885 2.7703 2.7611 0.423 Inadequat e information 3.1692 2.2623 2.1577 3.1178 2.418* Staff inpatient and unhappy to respond 2.6923 2.2787 2.2297 2.3822 1.372 Non availability of enquiry counter 2.6822 3.1180 3.0964 2.8471 0.148

Source: Primary data *Significant at five per cent level

From Table 4, it is understood that 'non availability of staff' is the important enquiry counter related problem among the customers who are in the age group of below 25 years, 26 to 30 years, 31 to 40 years and above 40 years as their mean scores are 3.3077, 3.5902, 3.5676 and 3.5096. The analysis shows that significant difference among the different age groups of customers are identified in the case of 'inadequate information', since its "F" statistics is significant at 5 per cent level. So the null hypothesis is rejected.

Problems Related to Technologies

Today's banks are facing the challenges of tightening budgets and continuous demands to reduce costs while handling the constant stream of new regulations. They are also under immense pressure to meet the increasingly complex demands of the real-time, digital customer. Technology is inevitably playing a core role in helping them address these issues. Many banks are transitioning from high-cost, in-house systems to more agile and flexible managed services, such as business process outsourcing, application management, and software-as-a-service (SaaS). The world is changing, and new entrants are entering the market. The very basics of how banks do business are evolving. To stay in the game, banks need to invest in leading-edge technology and innovation while ensuring their core infrastructures offer the right foundation for real organic growth and expanded customer wallet share.

Respondent's Problem about Technologies in relation to Gender

Table 5 : Respondent's problem about Technologies in relation to Gender

Problem related to technologi es

Gender (Mean Score) ‘t’ Statistics Male Female

Power supply probl ems 3.5572 3.5145 0.721

Machine problem 3.0452 3.0217 0.272

Inadequat e information 2.6566 2.6884 0.307

Lack of system knowledge 2.7741 2.8768 0.915

Network problems 3.8434 3.8551 0.166

Lack of training 3.6536 3.6014 0.631

Source: Primary data

From Table 5, it is understood that 'network problems' is the important problem related to technologies among the male and female customers as their mean scores are 3.8434 and 3.855. As regards the problems related to technologies, no significant difference among the different gender groups of customers are identified in the case of power supply problems, since the respective "t" statistics are not significant at 5 per cent level. So the null hypothesis is accepted.

Respondent's problems about Technologies in relation to Age

Customers of different age groups face problem related to technologies at different level. In order to find out the significant difference in problem related to technologies among different age groups of customers of public sector banks in Tirunelveli district, 'ANOVA' test is attempted with the null hypothesis, "there is no significant difference in problem related to technologies among different age groups of customers of public sector banks in Tirunelveli district". The result of 'ANOVA' test is presented in the Table 6

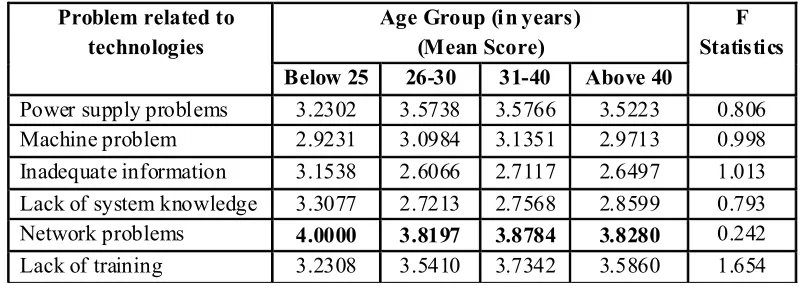

Table 6 : Respondent's Problems about Technologies in relation to Age

Problem related to technologies

Age Group (i n years) (Mean Score)

F Statistics Below 25 26-30 31-40 Above 40

Power supply problems 3.2302 3.5738 3.5766 3.5223 0.806 Machine problem 2.9231 3.0984 3.1351 2.9713 0.998 Inadequate information 3.1538 2.6066 2.7117 2.6497 1.013 Lack of system knowledge 3.3077 2.7213 2.7568 2.8599 0.793 Network problems 4.0000 3.8197 3.8784 3.8280 0.242 Lack of training 3.2308 3.5410 3.7342 3.5860 1.654

From the above Table 6, it is understood that 'network problems' is the important problem related to technologies among the customers who are in the age group of below 25 years, 26 to 30 years, 31 to 40 years and above 40 years as their mean scores are 4.0000, 3.8197, 3.8784 and 3.8280. It is evident from Table 6 that no significant difference in the problems related to technologies among the different age groups of respondents exists since their respective "F" statistics are not significant at 5 per cent level. So the null hypothesis is accepted.

Employee Related Problem

Banks that have set up employee relationship management will incur extra cost from the department. Sometimes employee relation does not live to the expectations in such a way that the problems that should be solved by it are still roaming within the organization. The division is supposed to monitor workplace challenges before the union does and solve them before they become a nuisance to the organization. Therefore any failure to tackle means unnecessary costs have been incurred by the banks. Single employer bargaining can be expensive because of the need to maintain a centralized employee relation.

Respondent's Problems about Employees in relation to Gender

In order to find out the significant difference in employee related problem among different gender group of customers of public sector banks in Tirunelveli district, 't' test is attempted with the null hypothesis, "there is no significant difference in employee related problem among different gender group of customers of public sector banks in Tirunelveli district". The result of 't' test is presented in the Table 7.

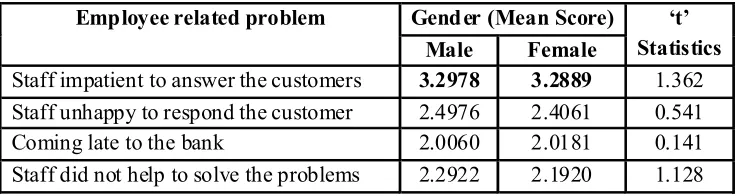

Table 7 : Respondent's Problems about Employees in relation to Gender

Employee related problem Gend er (Mean Score) ‘t’ Statistics Male Female

Staff impatient to answer the customers 3.2978 3.2889 1.362 Staff unhappy to respond the customer 2.4976 2.4061 0.541

Coming late to the bank 2.0060 2.0181 0.141

Staff did not help to solve the problems 2.2922 2.1920 1.128

Source: Primary data

groups of respondents since their respective "F" statistics are not significant at 5 per cent level. So the null hypothesis is accepted.

Respondent's Problem about Employees in relation to Age

In order to find out the significant difference in employee related problem among different age groups of customers of public sector banks in Tirunelveli district, 'ANOVA' test is attempted with the null hypothesis, "there is no significant difference in Employee related problem among different age groups of customers of public sector banks in Tirunelveli district". The result of 'ANOVA' test is presented in the Table 8.

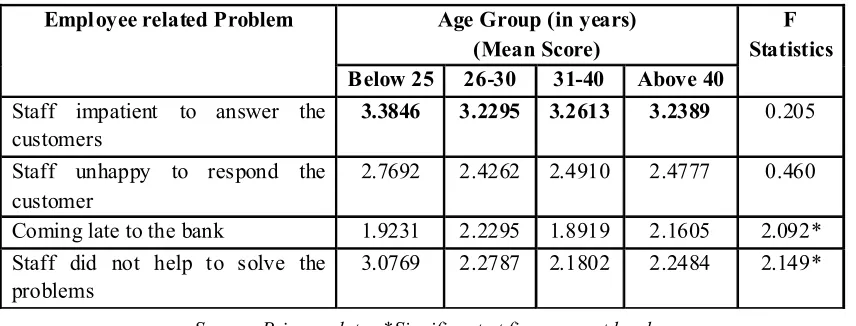

Table 8 : Respondent's Problem about Employees in relation to Age

Empl oyee related Problem Age Group (in years) (Mean Score)

F Statistics Below 25 26-30 31-40 Above 40

Staff impatient to answer the customers

3.3846 3.2295 3.2613 3.2389 0.205

Staff unhappy to respond the customer

2.7692 2.4262 2.4910 2.4777 0.460

Coming late to the bank 1.9231 2.2295 1.8919 2.1605 2.092* Staff did not help to solve the

problems

3.0769 2.2787 2.1802 2.2484 2.149*

Source: Primary data *Significant at five per cent level

From Table 8, it is understood that 'staff impatient to answer the customers' is the important employee related problem among the customers who are in the age group of below 25 years, 26 to 30 years, 31 to 40 years and above 40 years as their mean scores are 3.3846, 3.2295, 3.2613 and 3.2389. Regarding the employee related problem, significant difference among the different age groups of customers are identified in the case of 'coming late to the bank' and 'staff did not help to solve the problems' since their respective "F" statistics are significant at 5 per cent level. So the null hypothesis is rejected.

ATM Related Problems

Respondent's Problems about ATM in Relation to Gender

Table 9 : Respondent's Problem about ATM in relation to Gender

ATM related problem Gender (Mean Score) T Statistics Male Female

Networking problems 3.1295 3.1522 0.360

Machine complexity 2.6205 2.4384 2.368*

Failure to maintain sufficient balance 2.2982 2.2824 0.536 No alternate arrangement for power failure 2.9096 2.7464 1.738

Sometimes ATM under repair 3.0241 2.9384 0.890

Unsuitable location of ATM 2.9247 2.9273 0.025

ATM card struck inside machine 2.9940 2.9674 0.257

No cash 3.2771 3.3152 0.347

Source: Primary data *Significant at five per cent level

From the above Table 9, it is understood that the important ATM related problem among the male customers are 'no cash' and 'networking problems' as the mean score is 3.2771 and 3.1295 respectively. Table 9 further clearly shows that the important ATM related problem among the female customers are 'no cash' and 'networking problems' as their mean score is 3.3152 and 3.1522. As regards the ATM related problem, significant difference among the different age groups of customers is identified in the case of 'machine complexity', since its "F" statistics is significant at 5 per cent level. So the null hypothesis is rejected.

Respondent's Problem about ATM in Relation to Age

In order to find out the significant difference in ATM related problem among different age groups of customers of public sector banks in Tirunelveli district, 'ANOVA' test is attempted with the null hypothesis, "there is no significant difference in ATM related problem among different age groups of customers of public sector banks in Tirunelveli district". The result of 'ANOVA' test is presented in the Table 10

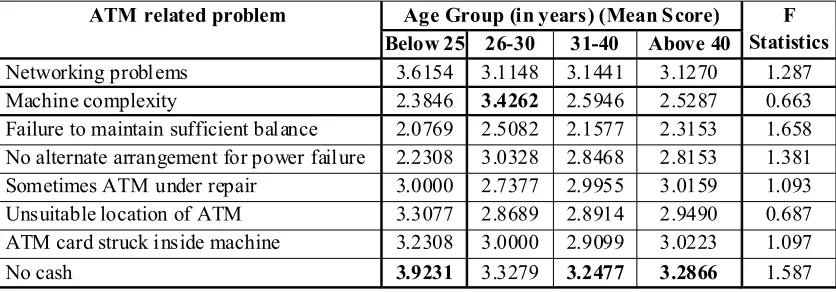

Table 10 : Respondent's Problem about ATM in relation to Age

ATM related problem Age Group (in years) (Mean S core) F Statistics Below 25 26-30 31-40 Above 40

Networking probl ems 3.6154 3.1148 3.1441 3.1270 1.287

Machine complexity 2.3846 3.4262 2.5946 2.5287 0.663

Failure to maintain sufficient bal ance 2.0769 2.5082 2.1577 2.3153 1.658 No alternate arrangement for power fail ure 2.2308 3.0328 2.8468 2.8153 1.381 Sometimes ATM under repair 3.0000 2.7377 2.9955 3.0159 1.093 Unsuitable location of ATM 3.3077 2.8689 2.8914 2.9490 0.687 ATM card struck i nside machine 3.2308 3.0000 2.9099 3.0223 1.097

No cash 3.9231 3.3279 3.2477 3.2866 1.587

From Table 10, it is understood that the important ATM related problems among the customers who are in the age group of below 25 years, 31-40 years, and above 40 years is 'no cash' as their mean score are 3.9231, 3.2477 and 3.2866. As regards 26-30 years of age the important ATM related problem is 'machine complexity' as its mean score is 3.4262. It is evident from Table 9 that no significant difference in the ATM related problem among the different age groups of respondents exists since their respective "F" statistics are not significant at 5 per cent level. So the null hypothesis is accepted.

Consultancy related Problem

Respondent's Problems about Consultancy in relation to Gender

In order to find out the significant difference in consultancy related problem among different gender group of customers of public sector banks in Tirunelveli district, 't' test is attempted with the null hypothesis, "there is no significant difference in consultancy related problem among different gender group of customers of public sector banks in Tirunelveli district". The result of 't' test is presented in the Table 11.

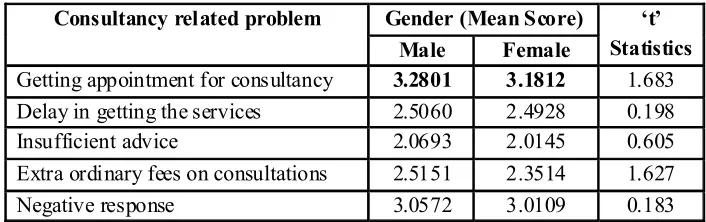

Table 11 : Respondent's Problem about Consultancy in Relation to Gender

Consultancy related problem Gender (Mean Score) ‘t’ Statistics Male Female

Getting appointment for consultancy 3.2801 3.1812 1.683 Delay in getting the services 2.5060 2.4928 0.198

Insufficient advice 2.0693 2.0145 0.605

Extra ordinary fees on consultations 2.5151 2.3514 1.627

Negative response 3.0572 3.0109 0.183

Source: Primary data

From Table 11, it is understood that the important consultancy related problem among the male and female customers are 'getting appointment for consultancy' as their mean scores are 3.2801 and 3.1812. It is evident from Table 11 that no significant difference in the consultancy related problem among the different gender groups of respondents exists since their respective "F" statistics are not significant at 5 per cent level. So the null hypothesis is accepted.

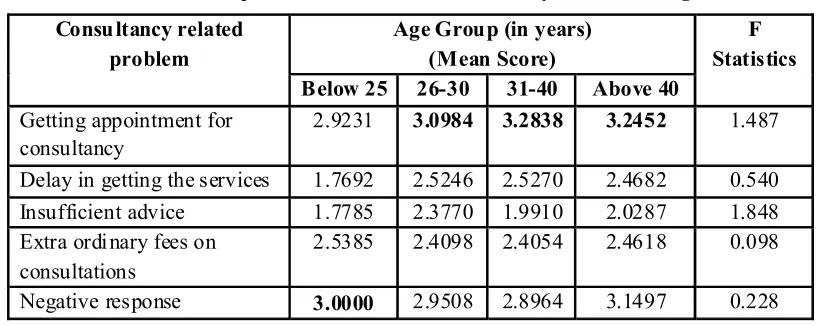

Respondent's Problem about Consultancy in Relation to Age

Table 12 : Respondent's Problem about Consultancy in Relation to Age

Consu ltancy related problem

Age Group (in years) (Mean Score)

F Statistics Below 25 26-30 31-40 Above 40

Getting appointment for consultancy

2.9231 3.0984 3.2838 3.2452 1.487

Delay in getting the services 1.7692 2.5246 2.5270 2.4682 0.540 Insufficient advice 1.7785 2.3770 1.9910 2.0287 1.848 Extra ordi nary fees on

consultations

2.5385 2.4098 2.4054 2.4618 0.098

Negative response 3.0000 2.9508 2.8964 3.1497 0.228

Source: Primary data

From Table 12, it is understood that the important consultancy related problem among the customers who are in the age group of below 25 years is 'negative response' as the mean score is 3.0000. The Table 12 further clearly shows that the important consultancy related problem among the customers who are in the age group of 26 to 30 years, 31 to 40 years and above 40 years are 'getting appointment for consultancy' as their mean score are 3.0984, 3.2838 and 3.2452 respectively. Regarding the consultancy related problem, there is no significant difference exists among the different age groups of customers, since their respective "F" statistics are not significant at 5 per cent level, the null hypothesis is accepted.

Safe Custody Problems

Safe deposit Lockers and safe custody services to its customers through its large number of branches, at a very reasonable charge.

Custody fees are calculated in accordance with the bank's current charges and commissions, which are available on request. The Bank reserves the right to change the charges and commissions from time to time. The Bank may charges for their extra ordinary services and expenses separately.

Respondent's Problem about Safe Custody in Relation to Gender

Table 13 : Respondent's Problem about Safe Custody in Relation to Gender

Safe custody problem Gender (Mean Score) ‘t’ Statistics Male Femal e

Restricted access 3.3825 3.3551 0.449

User inconvenience 2.8946 2.8478 0.575

Locker rent 2.3645 2.4493 0.759

Restricted usage 2.7380 2.6594 0.772

Charge on maintenance of the locker key 2.9729 3.0435 0.655

Size of the safe 3.9036 4.0072 1.039

Source: Primary data

From the above Table 13, it is understood that 'size of the safe' is the important safe custody problem among the male and female customers as their mean scores are 3.9036 and 4.0072 respectively. It is evident from Table 13 that no significant difference in the safe custody problem among the different age groups of respondents exists since their respective "t" statistics are not significant at 5 per cent level. So the null hypothesis is accepted.

Respondent's Problem about Safe Custody in Relation to Age

In order to find out the significant difference in safe custody problem among different age groups of customers of public sector banks in Tirunelveli district, 'ANOVA' test is attempted with the null hypothesis, "there is no significant difference in safe custody problem among different age groups of customers of public sector banks in Tirunelveli district". The result of 'ANOVA' test is presented in the Table.

Table 14 : Safe Custody Problem among different Age groups

Safe Custody Problem Age Group (in years) (Mean S core)

F Statisti cs Below 25 26-30 31-40 Above 40

Restricted access 3.4615 3.1311 3.3288 3.4459 2.724* User inconvenience 3.1538 2.6393 2.8514 2.9299 1.776

Locker rent 2.3846 2.2295 2.3423 2.4904 1.195

Restricted usage 2.0769 2.5902 2.7883 2.6815 1.233 Charge on maintenance of the

locker key

2.9231 2.8525 3.0766 2.9936 0.451

From Table 14, it is understood that 'size of the safe' is the important safe custody problem among the customers who are in the age group of below 25 years, 26 to 30 years, 31 to 40 years and above 40 years as their mean scores are 4.3077, 3.7705, 4.0270 and 3.9172 respectively. Regarding the safe custody problem, the significant difference among the different age groups of customers are identified in the case of the variable 'restricted access', since its "F" statistics is significant at 5 per cent level. So the null hypothesis is rejected.

Findings

• Among the different gender groups of respondents significant difference in the problem about operation of account is identified in the case of variable 'delay in sanctioning loan' whereas significant difference in the problems about operation of account among the different age groups of customers are identified in the case of variable 'restriction in operation'.

• Gender wise there is a significant difference in enquiry counter related problem in the case of 'uncourteous response' whereas among the different age groups there is a significant difference in enquiry counter related problem in the case of 'inadequate information'.

• There is no significant difference in the problems about technologies among the different age groups and gender groups of respondents exists

• Age wise there is a significant difference in the employee related problem have been noticed in the case of 'coming late to the bank' and 'staff did not help solve the problem' whereas gender wise there is no significant difference exists.

• Gender wise there is a significant difference in ATM related problem have been noticed in the case of 'machine complexity' whereas there is no significant difference in ATM related problem as regards different age groups of customers.

• Regarding the consultancy related problem, there is no significant difference exists among the gender and different age groups of customers.

• Significant difference among the gender and different age groups of customers are identified in the case of the variable 'restricted access'

Conclusion

References

1. Aravind Singh, "Customer relationship management-New Horizons in banking", Journal of banking, Vol.14, No.2.

2. Aravind Srinivastava and Pooja Purang, "Employee perception of job satisfaction: comparative study on Indian banks", Asian academy of management Journal, Vol.14, July.

3. Arpita Khare & Anshuman Kahre "Managing customer relationship using CRM technologies in India's financial sector", banks and bank systems, Vol.5, issue.1.

4. Augustine Garini and Prasanta Athra(1994) Customer service in Commercial banks-Expectations and reality, Indian Journal of Marketing, Vol.XXXIII, June.

5. Berry. L.L. (1983) "Relationship marketing of services: Growing interest Emerging perspectives" Journal of Academy of Marketing sciences, Vol.23, No.4

6. Bhat, Mushtaq (2005). Service Quality Perceptions in Banks: A Comparative Analysis, Vision, Vol. 9, No.1, January-March.

7. Bhat Mustaq, A. (2005) Correlates of Service Quality in Banks: An Empirical investigation, Journal of services Research, Vol.5, No.1, April-September.