econ

stor

www.econstor.eu

Der Open-Access-Publikationsserver der ZBW – Leibniz-Informationszentrum Wirtschaft

The Open Access Publication Server of the ZBW – Leibniz Information Centre for Economics

Nutzungsbedingungen:

Die ZBW räumt Ihnen als Nutzerin/Nutzer das unentgeltliche,

räumlich unbeschränkte und zeitlich auf die Dauer des Schutzrechts

beschränkte einfache Recht ein, das ausgewählte Werk im Rahmen

der unter

→ http://www.econstor.eu/dspace/Nutzungsbedingungen

nachzulesenden vollständigen Nutzungsbedingungen zu

vervielfältigen, mit denen die Nutzerin/der Nutzer sich durch die

erste Nutzung einverstanden erklärt.

Terms of use:

The ZBW grants you, the user, the non-exclusive right to use

the selected work free of charge, territorially unrestricted and

within the time limit of the term of the property rights according

to the terms specified at

→ http://www.econstor.eu/dspace/Nutzungsbedingungen

By the first use of the selected work the user agrees and

declares to comply with these terms of use.

Jaschke, Stefan; Stahl, Gerhard; Stehle, Richard

Working Paper

Evaluating VaR Forecasts under Stress The

German Experience

CFS Working Paper, No. 2003/32

Provided in Cooperation with:

Center for Financial Studies (CFS), Goethe University Frankfurt

Suggested Citation: Jaschke, Stefan; Stahl, Gerhard; Stehle, Richard (2003) : Evaluating VaR

Forecasts under Stress The German Experience, CFS Working Paper, No. 2003/32, http://

nbn-resolving.de/urn:nbn:de:hebis:30-10376

This Version is available at:

http://hdl.handle.net/10419/72644

No. 2003/32

Evaluating VaR Forecasts under Stress –

The German Experience

CFS Working Paper No. 2003/32

Evaluating VaR Forecasts under Stress – The German

Experience

*

Stefan Jaschke

1

, Gerhard Stahl

1

,

Richard Stehle

2

October 2003

Abstract:

We present an analysis of VaR forecasts and P&L-series of all 13 German banks that used

internal models for regulatory purposes in the year 2001. To this end, we introduce the notion

of well-behaved forecast systems. Furthermore, we provide a series of statistical tools to

perform our analyses. The results shed light on the forecast quality of VaR models of the

individual banks, the regulator's portfolio as a whole, and the main ingredients of the

compu-tation of the regulatory capital required by the Basel rules.

JEL Classification: K23, G28

Keywords: banking supervision, VaR, exploratory data analysis, backtesting

*

The first two authors point out that the views expressed herein should not be construed as being

endorsed by the BaFin.

In animportantregulatory innovation theBasel Committeeon BankingSupervisionhas

allowedforbankstousetheirowninternalmodels{ so-calledValue-at-Risk (VaR)

mod-els { for calculating the regulatory capital cushion needed to cover the market risk of

open positionsinan institute'stradingbook. Comparedwith thestandardizedmethods

the internal models approach oers a whole bunch of advantages within the process of

risk management, i.e., in measuring, monitoring and managing market risk for trading

portfolios. These advantagesinclude theconvergenceof economicand regulatory capital

(Matten; 2000), the avoidance ofduplicatedeorts forinternaland regulatory risk

mea-surement and, among others, the signaling of competence to the market, especially to

ratingagencies, by regulatoryapproval ofan internal model.

Lookingbackon theyear2001 we recognize thatanumberofsevereeventstook place

in the nancial markets. Not only the terrorist attack from September 11, but also a

signicant numberof interestrate decisionsofcentralbanks,theEnroncase, the

contin-uingdemiseofthe\neweconomy",andothers, tookplace. Obviously,mostoftheevents

mentionedwere unpredictablebutdramaticinsome sense. That the year2001 was

spe-cialisalso highlightedbythefactthat13 German banksproduced33 VaR exceptionsin

the year 2001 while14 German banksproduced17 VaR exceptions in 2002. Given the

turbulences of that year, it is natural to ask whether the forecast quality of VaR

mod-els over the year 2001 turned out to be satisfactory. A second question is whether the

portfolios of the supervisedbanks behave similarlyand whether the similarityincreases

in stress periods. Put in another way, how well is the supervisor's portfolio diversied

and is this aected by the special events of the year 2001? This is the rst article to

provide a detailedempirical analysis of (1)the performanceof the actualVaR forecasts

of all German banks that used internalmodelsfor regulatory purposes in 2001 and (2)

the interrelations among the prots and losses (P&L) of these banks, especially during

thestressperiods. Insofar,itiscomparableto theempiricalanalysisofsimilardatafrom

six US banks by Berkowitz and O'Brien (2002). The methodology employed, however,

dierssignicantly.

TheBasel paperon backtestingdescribesin-depththe regulatoryrequirementsonthe

forecast quality of the trading book asa whole in order to ensurean adequate

calcula-tion of regulatorycapital (Basel Committee on BankingSupervision;1996b). Numerous

publications reect VaR forecast evaluation, starting with Kupiec (1995), who points

out thelackof statistical powerof a backtesting that isbased on a binomial test

statis-tic. Crnkovic and Drachman (1996) propose the use of the Kuiper statistic, which is

a goodness-of-t type statistic based on the whole forecast distribution. Christoersen

(1998) draws the attention to backtesting based on specication tests, focussing on the

independence property to evaluate forecast quality. Inspiredby the ideasof Rosenblatt

(1952), Berkowitz (2000) proposed an approach that relies on conditioned forecast

dis-tributions. This is very much inthe spiritof the papers ofDawid, see(Dawid; 1982a,b,

1984, 1986;Seillier-Moiseiwitschand Dawid; 1993). Thisagainis inuencedbythe

liter-atureonwheatherforecasting(Murphyand Winkler;1987,1992). Adetailedoverviewof

backtesting issuesis given by Overbeckand Stahl (2000). The empiricalanalysis of the

forecastqualityinthispaperisinthespiritofDawid'sforecastevaluation. Thefactthat

rigorous justication of our approach is given in the appendix. The methodology used

to analyze the joint behavior of all banks includes a measure of co-movement and

sev-eral stress variablesusedto denestress periods. Finally,we consider howdistributional

parameters changeconditional onstress.

Beforedescribingthedataset,letusintroducesomenotation. WedenotebyVaR (

t

;)

theValue-at-Riskofaportfolio

t

,giventhelevelofsignicance. Withintheframework

of theBaselCommittee, issetto 99%. The VaRnumberVaR (

t

;) at timetdenotes

the quantileof thedistributionof thehypothetical, orclean,P&L

C t =v t+1 ( t ) v t ( t ); (1) where v t

() is the value of a given portfolio at time t. The random variable v

t+1 (

t )

denotes the at time t frozen portfolio, evaluated at prices of time t+1. The VaR is

interpreted as an upper boundof losses that might be surpassed only with probability

1 . Inthesequel wewillusethe shorthandnotation V

t

to denote VaR (

t

;99%).

Withinanobservation periodof 250 tradingdays2.5 violationsof theforecasts V

t are

to be expected on theaverage. Hence,if too manyviolationsoccur there isgoodreason

to doubt that the internal model's level of signicance is correctly covered. In order to

ensure a suÆcient forecast quality, the Basel Committee tied theamount of the capital

requirementstothenumberofVaRexceptionsofthemodel(BaselCommitteeonBanking

Supervision;1996a).

Itisofgreatpracticalimportancetonotethatfreezingtheportfolio{asstatedin(1){

isnotimperative. TheBaselCommitteealsoacknowledgesbacktestingVaRthatisbased

on actualtradingoutcomes. Inthatcase changes oftheportfoliocompositionduringthe

holdingperiod,feesetc. aresuperimposedonthehypotheticalP&L.Fromastatistician's

pointofview,thejudgmentofforecastqualityshouldbebasedonthehypotheticalP&L,

(1), because the VaR forecast assumes a static portfolio by construction. From a risk

managers point of view, however, the actualor economic P&L is actively managed and

reported. Obviouslybothwaystotacklethebacktestingproblemhavetheirintrinsic

mer-its. German legislationprescribesabacktestingbased on (1),whereastheUS legislation

admitsto basethebacktestingontheeconomicP&L,see(BerkowitzandO'Brien;2002).

2. Description of the Data Set

The data set considered here contains data from all thirteen German banks that used

internal models for regulatory purposes in the year 2001. The data set for each bank

consists of rst, VaR forecasts and second, the so-called clean, orhypothetical P&L for

all 253 trading days of theyear 2001. Most ofthe followingguresand tablesare based

on the normalized P&L and VaR time series. I.e., they are divided by the banks' full

sample standarddeviation of P&L to insurecondentiality.

Table1showssummarystatisticsofeach bank'sdata. ThecoeÆcientofvariation(i.e.,

the ratio of the standard deviation and the mean) of VaR in column 5 shows that for

the majority of the banks the variabilityof the VaR is relatively smallcompared to its

name oflosses VaR variationofVaR lossexceedingVaR A 22.51 3.15 1.83 2.68 0.84 0.00 B 6.48 0.00 2.62 4.51 0.29 1.34 C 5.98 0.61 2.18 4.05 0.14 0.00 D 5.58 0.19 2.55 3.29 0.26 0.00 E 7.79 0.43 2.56 1.69 0.87 0.56 F 16.99 2.10 3.52 2.11 0.52 1.63 G 3.71 0.20 2.42 2.15 0.23 0.24 H 5.72 0.01 2.12 2.25 0.23 1.49 I 15.03 1.58 4.55 1.07 0.87 0.73 J 4.04 0.67 2.98 3.03 0.39 0.37 K 5.28 0.00 2.24 2.20 0.11 1.37 L 4.57 0.22 2.75 3.85 0.20 0.00 M 3.35 0.12 2.45 2.58 0.18 0.00

Table1:Summarystatisticsofstandardizeddata. Thecolumnsgivekurtosis,

skew-ness,minusthe1%-quantileoftheP&L,theaverageVaR,thecoeÆcientofv

ari-ation oftheVaR,andtheaveragesizeofthelossexceedingVaR.BothP&Land

VaR arere-normalizedinsuch a way thatthestandarddeviation ofthe P&Lis

1 forall banks.

exceedingVaR,i.e., theestimate oftheexpectedshortfallE[ C

t V t j C t >V t ]. Note,

thatforthestandardnormaldistribution,theexpectedshortfallisapproximately0.34for

the99%condencelevel. The comparativelylargeaveragelosses exceedingVaR indicate

thepresenceofoutliers. Threeoutofthethirteenbankshadmorethanfourviolationsand

onlyfour had no violationsat all. For reasons of condentiality,theindividualnumbers

of violationsarenotreported here.

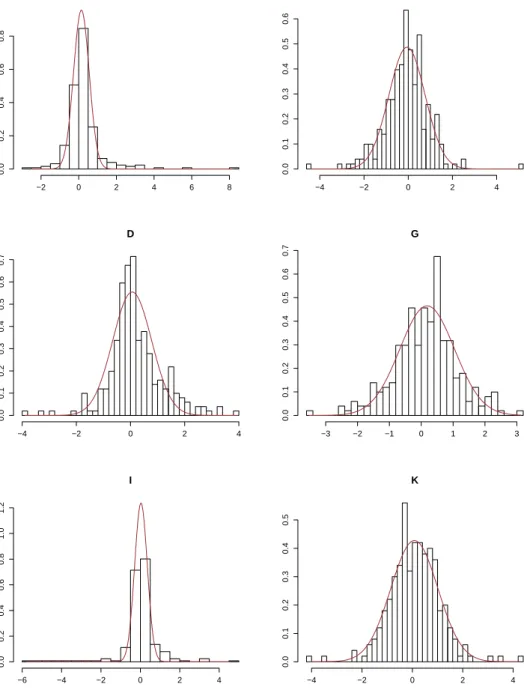

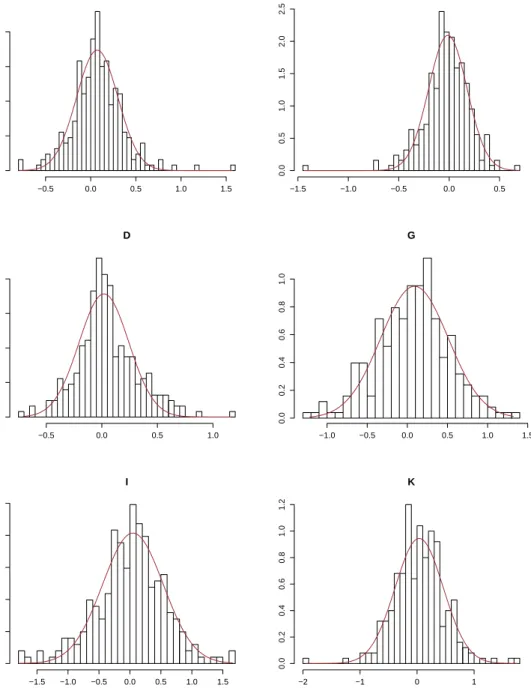

The six histogramsin gure 1 are representative forthe dataset. The histogramsare

fairlysymmetric,whichis inlinewiththeskewness intable 1. Takingintoaccount that

the data are standardized, the large range of the x-axis for bank I shows the presence

of extreme outliers. This suggests the use of robust estimates of locationand scale. To

be specic, we use the median F

1 0:5

as an estimate for the location parameter and the

interquartile range F 1 0:75 F 1 0:25

as an estimate of the scale parameter. In gure 1 the

tted normaldensitiesusethemedianasa robustestimator ofthemeanand normalized

interquartile range (F 1 0:75 F 1 0:25 )=( 1 0:75 1 0:25

) is a robust estimator of the standard

deviation. ( 1 0:75 1 0:25

1:349istheinterquartilerangeofthestandardnormal

distribu-tion.) ThisimprovestherepresentationofthebulkofthedatabyaGaussiandistribution.

Furthermore,itisevidentthatthelargeexcesskurtosis andskewnessofbank Iiscaused

bya fewextremeoutliers relative to thenormal distribution.

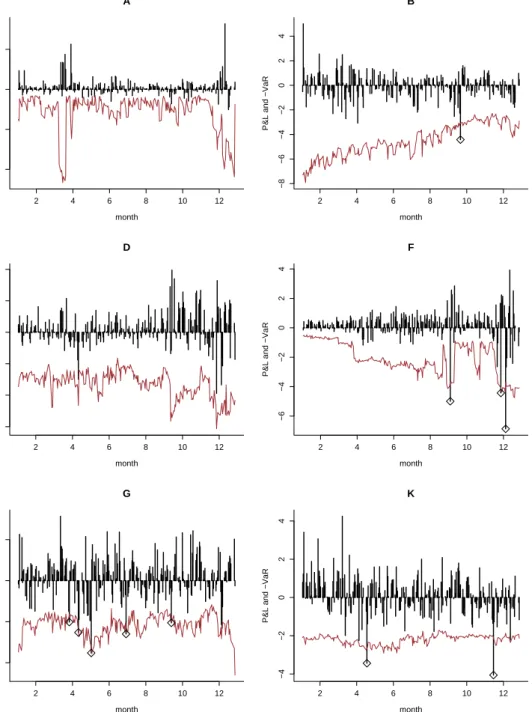

Figure2showsthetimeseriesof P&Land VaR oftheselected institutes. Ascan be

seen from banksBand F, forexample, itisnot reasonableto assumestationarity ofthe

P&L and VaR timeseries. Hence,the summary statisticsgiven intable 1 as wellasthe

histogramsingure 1 areto beinterpretedwithcare. BanksB, D,and F give a picture

A

−2

0

2

4

6

8

0.0

0.2

0.4

0.6

0.8

B

−4

−2

0

2

4

0.0

0.1

0.2

0.3

0.4

0.5

0.6

D

−4

−2

0

2

4

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

G

−3

−2

−1

0

1

2

3

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

I

−6

−4

−2

0

2

4

0.0

0.2

0.4

0.6

0.8

1.0

1.2

K

−4

−2

0

2

4

0.0

0.1

0.2

0.3

0.4

0.5

Figure 1:Histograms of the P&L and tted normal densities. The mean and

standard deviation of the tted normal density are estimated robustly by the

2

4

6

8

10

12

−

10

−

50

5

A

month

P&L and

−

VaR

2

4

6

8

10

12

−

8

−

6

−

4

−

20

2

4

B

month

P&L and

−

VaR

2

4

6

8

10

12

−

6

−

4

−

20

2

4

D

month

P&L and

−

VaR

2

4

6

8

10

12

−

6

−

4

−

20

2

4

F

month

P&L and

−

VaR

2

4

6

8

10

12

−

4

−

20

2

G

month

P&L and

−

VaR

2

4

6

8

10

12

−

4

−

20

2

4

K

month

P&L and

−

VaR

Figure 2:Time series of P&L and -VaR. The vertical dotted lines denote the date

0.0

0.2

0.4

0.6

0.8

1.0

0.0

0.2

0.4

0.6

0.8

1.0

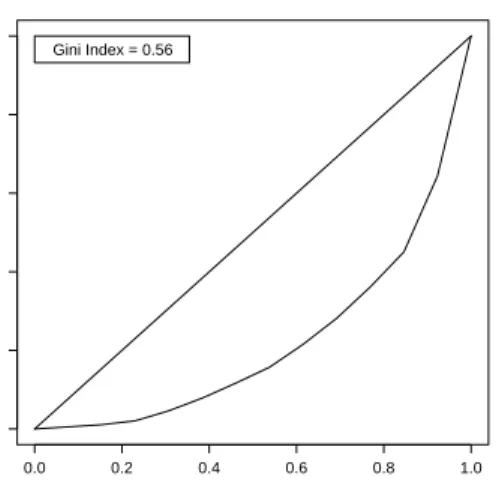

Lorenz curve of the average VaR

ranking in the sorted set

cumulative proportion

Gini Index = 0.56

Figure 3:Lorenz curve of the average VaR of all banks. The largest three banks

interms ofaverage VaR capture61%of theaggregated average VaRs.

Asthedescriptivestatisticsshow,bankstendto beconservative inthesensethatthey

overestimatetheirVaR.ThetraÆclightapproachis relatedto aone-sidedlossfunction,

asreportedintable 1. Hence,thisbacktest doesnotrecovertheinformationinthedata

about forecast quality of a VaR-model as a whole. In the next section we will have a

closer lookat forecast qualityusingmore powerfultools.

WeconcludethissectionwiththeLorenzcurveingure3,whichdepictsthe

concentra-tion ofrisksamong thethirteenbanksand givessomecomplementaryinformationabout

therelative \size"of thebanks.

3. Analyzing VaR-Forecasts for Each Bank Individually

In their paper on backtesting, the Basel Committee on Banking Supervision (1996b)

encourages institutes to apply backtesting procedures beyond the so-called traÆc light

approach. In this section, we make proposals for possible renements. The proposed

toolshavebeenusedbytheBundesanstaltfurFinanzdienstleistungsaufsicht(BaFin),the

Germansingleregulatorforintegratednancialservicessupervision,foracoupleofyears.

In the following, we use the term prediction-realization pair for the class of objects

((F t );C t ), where F t

denotes the whole forecast distribution and (F

t

) a parameter

thereof, e.g., a quantile, orthe distributionas awhole (=id). The summary statistics

from section 2 give a description of the prediction-realization pairs(V

t

;C

t

). In order to

evaluate theforecast qualityof VaR modelswe introduce astatistical modelthat allows

to incorporateadditionalinformationfrom theprediction-realizationpairs (F

t

;C

t ).

Thetime plotsdisplayed ingure2 showthatneither of thetime seriesC

t

nor V

t are

stationary. Fortheevaluationofaforecastmodelitisnaturalto lookfortransformations

T suchthatthetimeseriesT((F

t

);V

t

T(F t ;C t )=F t (C t ) (2)

isusedasastartingpoint. A forecastsystemisconsidered\good" (Dawid;1984, p.281),

ifthevaluesF

t (C

t

) are independentand uniformlydistributed,i.e., F

t (C

t

) iidU[0;1].

Thiscorrespondsto theconcepts\well-calibration"and\renement" (=\resolution")

asusedintheliteratureonweatherforecasting(MurphyandWinkler;1987,1992)insofar

as the condition F

t (C

t

) U[0;1] essentially means \well-calibration" and the temporal

independence of F

t (C

t

) is related to \renement" (Dawid; 1986; Seillier-Moiseiwitsch;

1993).

While it has been proposed (Berkowitz; 2000) that banks should report the realized

probabilities F

t (C

t

) to the supervisory authorities, the current rules only require the

reportingofC t andV t = F 1

(0:01). Theforecastevaluation(backtesting) aslaiddown

inthe BaselAmendment isdened intermsof theVaR-exceptions

T(V t ;C t )=1 fV t C t g : (3)

The drawbacks of this approach are discussedby Kupiec (1995). Seealso Lopez (1999)

and (Jorion;2001, chapter 6).

Inthis section,we suggestan approach that bridges thegap betweenthe information

presentedbytheprediction-realizationpairs(2)and(3) . Inthedelta-normalRiskMetrics

framework,theVaR-forecast V

t

is relatedtotheforecastofthestandarddeviationofthe

P&L, t ,as V t =z t ; (4)

where z is the standard normal 99%-quantile, (z) = 0:99. There, the standardized

returns aredenedas

R t :=T(C t ;V t )=zC t =V t ; (5)

(Longerstaey; 1996, chapter 11) and are iid standard normal under the specic model

assumptionsof thedelta-normal approach. Thisdenition(5)of standardizedreturns is

useful even if (4) is invalid. A rigorousjustication of this statement and thefollowing

approach isprovidedintheappendix. Thestandardized returnsprovidethe basisofthe

forecast evaluation inthispaper.

We callaVaR forecast systemwell-behaved

3 if R t iidF 2U G " ; where U "

is the "-neighborhood of the set of Gaussian distributionswith respect to the

Kolmogorovdistance intheset ofprobabilitydistributions:

U G " :=fFjsup x jF(x) (; 2 )(x)j";F ispdf;2R; 2 2(0;1)g (6) 3

Notethat\well-behaved"is nottobeinterpreted as\favorable fromasupervisorypointofview". It

asHuber'sgrosserror modelinthe literatureofrobuststatistics, F G " :=fFjF =(1 ")(; 2 )+"H;2R; 2 2(0;1)g; (7)

where H is an arbitrary probabilitydistribution, isan important subset of U

G " . In fact, if F 2 F G "

, then exist , , and H such that F = (1 ")(;

2

)+"H. Then the

Kolmogorovdistance betweenthedistributionsF and (;

2 ) is d(F;(; 2 ))=sup x2R jF(x) (; 2 )(x)j; =" sup x2R jH(x) (; 2 )(x)j ="d(H;(; 2 ))":

In terms of the P-P plot of F against normal, which plotsF(x) against (;

2

)(x) for

x 2 R, this means that the graph is (vertically) within an "-band of the diagonal. On

theotherhand,anypointwithinthatbandcanbereachedbythegraphofadistribution

F 2U

G "

.

TheGaussiandistributionwithrobustlyestimatedparametersts(byeye)remarkably

wellto thecenter of standardized returns R

t

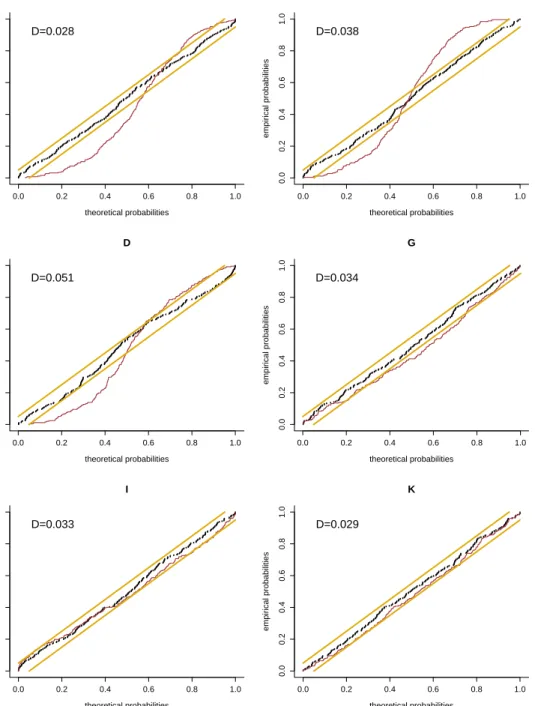

,seegure 4. The P-Pplot against normal

(gure5)alsoshowsthatthedistributionsofthestandardizedreturnsarerelativelyclose

tonormal,inthesensethattheyareintheclassU

G "

with"=0:05. (Infact,theempirical

distributionsof allbanksare inthisclass.)

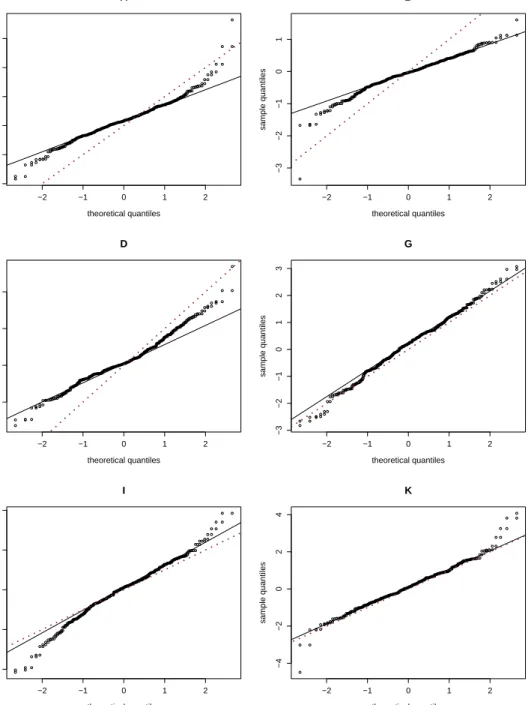

The P-P plot (and the Kolmogorov distance) does not detect large deviations from

normalityaslong asthey happen withsmall probabilities. A better pictureof thet in

the tails is provided by the Q-Q plot of F against normal, which plots F

1 (t) against 1 (; 2

)() for 2(0;1), see gure 6. Anotherdisplaywith emphasis on the tails is

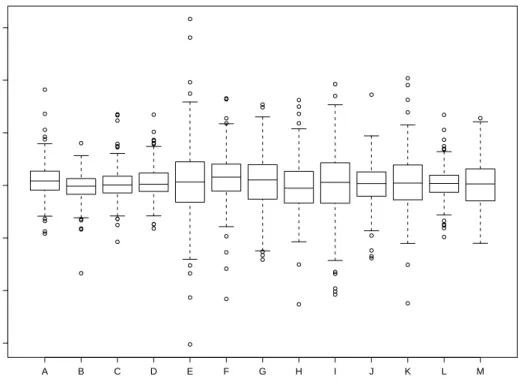

theboxplot, seegure7.

Diagnosticsthatillustrateserial(in-)dependenceofR

t

areprovidedbythecumulative

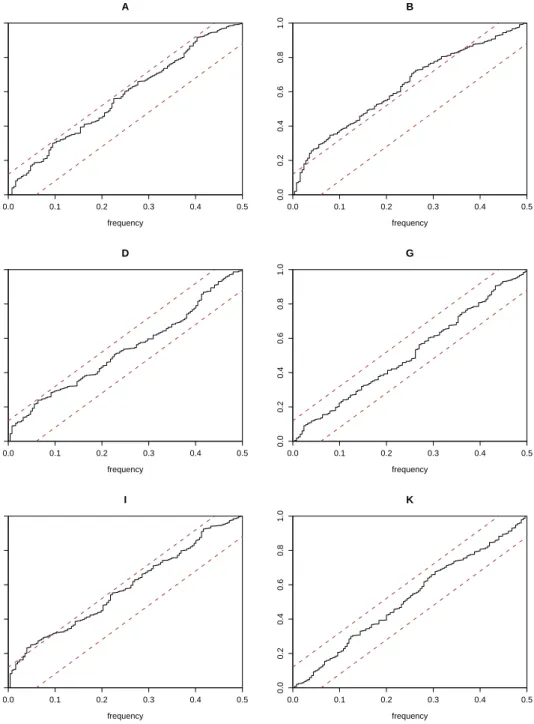

periodogramappliedtobothstandardizedreturnsandtheirabsolutevalues. Asexpected,

gure8showsthatthereisnosignicantautocorrelationinthestandardizedreturnseries.

Unliketheabsolutereturnsofmanynancialsecurities,theabsolutestandardizedreturns

of the banking books show no marked heteroscedasticity, see gure 9. Possibly reasons

are that the banks' VaR-forecasts successfully predict some of the heteroscedasticity of

their P&L-series. Another possible reason could be that the risk control limit system

lters outsome of theheteroscedasticityofthe originalreturns.

Thesetofwell-behavedVaR-forecastscontainsforecasts thatgrosslyover-or

underes-timate therespectivequantile. Undertheassumptionthatstandardizedreturnsarei.i.d.

standard normal, the inverse of the standard deviation of R

t

can be interpreted as the

recalibration factor. Thelargeritis,themorethebankoverestimatesitsVaR.Wewillcall

a forecast well-calibrated,iftherecalibration factor equals one

4

. Instead of looking only

at theempiricalstandard deviationof the standardized returnR

t

,one can alternatively

4

The relation between this notion of \well-calibration" and its denition in the forecast evaluation

literature can be made rigorous in more general settings than the delta-normal method, which is

A

−0.5

0.0

0.5

1.0

1.5

0.0

0.5

1.0

1.5

2.0

B

−1.5

−1.0

−0.5

0.0

0.5

0.0

0.5

1.0

1.5

2.0

2.5

D

−0.5

0.0

0.5

1.0

0.0

0.5

1.0

1.5

2.0

G

−1.0

−0.5

0.0

0.5

1.0

1.5

0.0

0.2

0.4

0.6

0.8

1.0

I

−1.5

−1.0

−0.5

0.0

0.5

1.0

1.5

0.0

0.2

0.4

0.6

0.8

1.0

K

−2

−1

0

1

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Figure 4:Histogramsofthe standardizedreturnandttednormaldensity. The

meanandstandarddeviationofthettednormaldensityareestimatedrobustly

0.0

0.2

0.4

0.6

0.8

1.0

0.0

0.2

0.4

0.6

0.8

1.0

A

theoretical probabilities

empirical probabilities

D=0.028

0.0

0.2

0.4

0.6

0.8

1.0

0.0

0.2

0.4

0.6

0.8

1.0

B

theoretical probabilities

empirical probabilities

D=0.038

0.0

0.2

0.4

0.6

0.8

1.0

0.0

0.2

0.4

0.6

0.8

1.0

D

theoretical probabilities

empirical probabilities

D=0.051

0.0

0.2

0.4

0.6

0.8

1.0

0.0

0.2

0.4

0.6

0.8

1.0

G

theoretical probabilities

empirical probabilities

D=0.034

0.0

0.2

0.4

0.6

0.8

1.0

0.0

0.2

0.4

0.6

0.8

1.0

I

theoretical probabilities

empirical probabilities

D=0.033

0.0

0.2

0.4

0.6

0.8

1.0

0.0

0.2

0.4

0.6

0.8

1.0

K

theoretical probabilities

empirical probabilities

D=0.029

Figure 5:P-Pplotofthe distributionofthestandardizedreturnagainsta

stan-dardnormal(dottedline)andattednormaldistribution(fatdotted

line). The mean and standard deviation of the tted normal distribution are

chosentominimizetheKolmogorovdistancetotheempiricaldistribution

func-tion. D is that minimal distance. The dashed lines are the envelope of all

−2

−1

0

1

2

−

2

−

1

0123

A

theoretical quantiles

sample quantiles

−2

−1

0

1

2

−

3

−

2

−

10

1

B

theoretical quantiles

sample quantiles

−2

−1

0

1

2

−

1

012

D

theoretical quantiles

sample quantiles

−2

−1

0

1

2

−

3

−

2

−

1

0123

G

theoretical quantiles

sample quantiles

−2

−1

0

1

2

−

4

−

20

2

4

I

theoretical quantiles

sample quantiles

−2

−1

0

1

2

−

4

−

20

2

4

K

theoretical quantiles

sample quantiles

Figure 6:Q-Qplotofthestandardizedreturn. Thedottedlinedenotesthestandard

normal distribution, the solid line denotes the normal distribution with mean

and variance estimated from the sample, and the small circles represent the

A

B

C

D

E

F

G

H

I

J

K

L

M

−

6

−

4

−

20

2

4

6

Figure 7:Boxplot of the standardized return. The box shows the interquartile

range and the middle line the median. The \whiskers" are drawn 1.5 times

the interquartile range away from the box. Any point further away is shown

individually.

lookat dierentestimates

^ p (R ):= 1 T T X t=1 jR t j p ! 1=p =c p (8)

ofthestandarddeviationofR

t forpowersp>0. (c p istheconstantc p =(EjXj p ) 1=p with

X beingstandardnormal.) Usingsmallerpowersp<2givesmorerobustestimatesthan

the usualestimate of thestandard deviation. Usinglarger powers p>2 givesestimates

of the standard deviation that are more sensitive, i.e., more dependent on the extreme

values of R

t

, than the usual estimate of the standard deviation (p= 2). By lookingat

^ p

(r) for dierent powers p, one can observe whether banks are well-calibrated at the

center orat thetails,respectively.

5

Table2showsestimatesof therecalibrationfactor,aswellasp-valuesfromtestingthe

hypothesis that this factor equals 1. These results are further illustrated by gure 10,

5

Notethat thevariousdierent^

p

(r)are estimatesof thestandarddeviationofR

t

onlyifthe R

t are

0.0

0.1

0.2

0.3

0.4

0.5

0.0

0.2

0.4

0.6

0.8

1.0

frequency

A

0.0

0.1

0.2

0.3

0.4

0.5

0.0

0.2

0.4

0.6

0.8

1.0

frequency

B

0.0

0.1

0.2

0.3

0.4

0.5

0.0

0.2

0.4

0.6

0.8

1.0

frequency

D

0.0

0.1

0.2

0.3

0.4

0.5

0.0

0.2

0.4

0.6

0.8

1.0

frequency

G

0.0

0.1

0.2

0.3

0.4

0.5

0.0

0.2

0.4

0.6

0.8

1.0

frequency

I

0.0

0.1

0.2

0.3

0.4

0.5

0.0

0.2

0.4

0.6

0.8

1.0

frequency

K

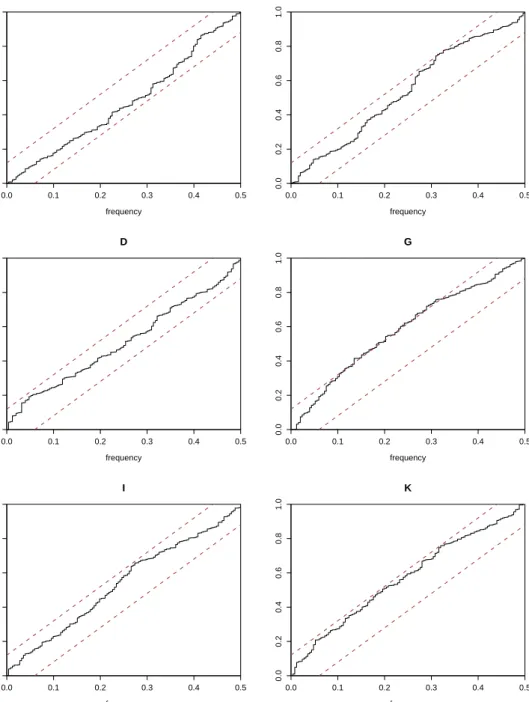

Figure 8:Cumulative periodogram of standardized returns. White noiseis

char-acterized by equal probabilities for all frequencies, which shows as a straight

line in the cumulative periodogram. 95%-condence bands are given for the

0.0

0.1

0.2

0.3

0.4

0.5

0.0

0.2

0.4

0.6

0.8

1.0

frequency

A

0.0

0.1

0.2

0.3

0.4

0.5

0.0

0.2

0.4

0.6

0.8

1.0

frequency

B

0.0

0.1

0.2

0.3

0.4

0.5

0.0

0.2

0.4

0.6

0.8

1.0

frequency

D

0.0

0.1

0.2

0.3

0.4

0.5

0.0

0.2

0.4

0.6

0.8

1.0

frequency

G

0.0

0.1

0.2

0.3

0.4

0.5

0.0

0.2

0.4

0.6

0.8

1.0

frequency

I

0.0

0.1

0.2

0.3

0.4

0.5

0.0

0.2

0.4

0.6

0.8

1.0

frequency

K

A 1:670 1:614 1:480 B 2:162 2:053 1:849 C 1:899 1:832 1:659 D 1:805 1:690 1:552 E 0:825 0:786 0:710 F 1:147 1:129 1:055 G 0:938 0:946 0:940 H 1:074 1:037 0:980 I 0:831 0:808 0:769 J 1:466 1:403 1:296 K 1:004 0:992 0:944 L 1:838 1:765 1:625 M 1:143 1:110 1:090

Table2:Robust and sensitive estimates of the recalibration factor. The

esti-mates 1=^

p

(r) (see equation (8) ) of the recalibration factor are computed for

powers p 2 f0:5;1;2g. p-values for the corresponding null hypothesis that the

recalibration factor is one (i.e., that the R

t

are iid standard normal) are

com-puted byMonte-Carlo simulation. Signicanceat the 5%-level isshownbyone

star and signicance at the1%-levelwith two stars.

showing the recalibration factor estimated with the empirical standard deviation (p =

2) and the interquartile range, respectively. Note that banks E and I are consistently

underestimating its VaR. Alsonote that all banks are close to the line with slope 0.84

and intercept 0. This means rst, that the distributions of their standardized returns

have slightly heavier tails than the normal distribution. Second, the estimate of the

recalibration factor dependsonlymoderatelyon howrobustlyit isestimated.

Thelocalaveragesoftheabsolutevaluesofthestandardizedreturns(=estimatesofthe

inverseof therecalibrationfactor usingp=1)ingure 11showonlymoderate variation

intime, except forsome unpredictedabsolutereturns ofbanksBand I.

Insummary,thestandardizedreturnseriesofalltradingbooksareremarkablycloseto

being\well-behaved"asdenedinthissection. I.e.,theyareclosetonormalinthesense

of the Kolmogorov distance and there areno obvious temporal dependencies. This isin

starkcontrasttotheconclusionsdrawnbyBerkowitzandO'Brien(2002). Theyshowthat

theVaR-forecastsofthesixUSbanksconsideredareinferiortothatofasimple

\reduced-form" model,i.e., a univariatetime seriesmodel applied directly to the individualP&L

series. Their conclusion is that the banks' forecasts \did not adequately reect changes

inP&Lvolatility". Theconclusionfromtheempiricalevidence presentedinthissection,

however,isthattheVaR-forecastsoftheconsideredGermanbanksare\essentiallyOK":

the conservative VaR-forecasts of most banks can be corrected by simply re-calibrating

them. Much of the non-normality of the standardized return distributions in the view

of thetail-sensitivegraphs(gure 6) can be traced back to theessentially unpredictable

A

B

C

D

E

F

G

H

I

J

K

L

M

1.0

1.2

1.4

1.6

1.8

2.0

2.2

0.8

1.0

1.2

1.4

1.6

1.8

robust estimate

usual estimate

Figure 10:Sensitiveand robustestimates ofthe recalibration factor,estimated

withthe usualestimateofthe standard deviation(p=2) andthe

in-terquartile range. BankstowardsnortheastoverestimatetheirVaR.Banks

towards southeast have outliers orheavy tails. The black linerepresentsthe

bestlinear t withintercept 0. Itsslopeis 0:84.

4. Analyzing P&L Series For All Banks Simultaneously

The analysis of themodel qualityfor banksindividuallygivesthe supervisor important

information concerning the supervision of each bank. On the other hand, the analysis

of cross-sectionalinterrelationsof thebanks,e.g.,co-movements, is atleastasimportant

becauseitshedslightontheaspectsof systemicrisk. Fromtheregulator'spointofview,

two adverse scenarios are important. The rst case is when the regulator's portfolio is

notwell-diversiedinthe sensethatall portfoliosbehave similarly. A more specic case

is,when portfoliosbehavesimilarlyinperiodsofstress.

Theeconomic relevanceof theP&Lseriesdominatesthatof theVaRnumbers. Hence

we perform our cross-sectional analysis from a P&L point of view. A natural point to

start withis thecalculation of correlations, say. Yet tablesforcross correlationsquickly

get unmanageable for larger numbers of banks. Instead of lookingat m(m 1)=2= 78

cross correlations, itmay be more usefulto look at them=13 correlationsbetweenthe

individualP&L seriesand an aggregated P&L-series. Theidentity

m X j=1 cov(C i ;C j )=cov(C i ; m X j=1 C j )=cov(C i ; X j6=i C j )+var(C i )

motivates to considerthe covariances cov(C

i ;

P C

j

01234

A

date

03−19

06−27

10−05

01234

B

date

03−19

06−27

10−05

01234

D

date

03−19

06−27

10−05

01234

G

date

03−19

06−27

10−05

01234

I

date

03−19

06−27

10−05

01234

K

date

03−19

06−27

10−05

Figure 11:Local estimates of the inverse recalibration factor. The dots showthe

absolutevaluesofthestandardizedreturns,jr

t j=c

1

,rescaledsuch,thattheycan

be viewed asestimates of theinverse recalibration factorunder thenormality

assumption. The horizontal lineshows theoverall average and theother line

a sliding 60-day average of the values jr

t j=c

1

. I.e., the horizontal line shows

the inverse of theestimated recalibration factor given inthe column \p =1"

A 0:114 0:070 B 0:206 0:154 C -0:102 -0:096 D 0:527 0:431 E 0:081 0:103 F 0:488 0:389 G 0:242 0:213 H -0:118 -0:076 I 0:475 0:333 J 0:241 0:186 K 0:244 0:163 L 0:392 0:270 M 0:289 0:264

Table3:Linear andrank correlations betweenindividual banks'P&Lwiththe

sum of the P&L of all other banks. The table shows Pearson's linear and

Spearman's rank correlations. The signicance in terms of the null hypothesis

of zero correlationismarked with one ortwo starsasbefore.

Fromtable 3weconcludethatonlybankHis noticablynegativelycorrelatedwiththe

rest,butthisisnotsignicantatthe5%-level. ItfurthertellsthatbanksA,C,andEare

not signicantlycorrelated to therest. Allother bankshave moderate, butsignicantly

positive correlationswiththe rest.

In order to understand the common movement of the time series of P&Ls in real,

monetary terms, we performed a principal component analysis, i.e., an eigen value

de-compositionof the covariance matrix of P&Ls. The resultsshow, that (1) althoughthe

three biggestbanksdominate theprincipalcomponent decompositionof P&Ls,themost

important factor onlyexplains46% of thevariance, thesecond 27%, and thethird13%,

and(2)thedominantfactorhasthemeaning\thebigbanksmoveinthesame direction".

Adierentquestioniswhatpossibleexplanatoryvariablesforexplainingtheco-movement

ofstandardizedreturnsare. Forthispurpose,weperformedaneigenvaluedecomposition

of the correlationmatrix of standardized returns. It shows that thecommon movement

of returns is remarkably \diverse" in the sense that the three most important factors

together explain only 47% of the variance (22%, 14% and 11% each) and there is no

dominantfactor.

A natural way to measure the degree of diversication is through the ratio of the

varianceof thecombinedportfolio and thesumof thevariances of itscomponents:

I t := ( P m i=1 C i t ) 2 P m i=1 (C i t ) 2 ; (9) If we replacein I t = ( P m i=1 R i t V i t ) 2 P m i=1 (R i t V i t ) 2

the time-dependent V i t byits average V i anddene w i := V i = m i=1 V i ,then we get I t := ( P m i=1 R i t V i ) 2 P m i=1 (R i t V i ) 2 = ( P m i=1 R i t w i ) 2 P m i=1 (R i t w i ) 2 ;

whichinthiscontext can beinterpretedasan indexof co-movement.

It is bounded below by zero and above as follows. If the banks' P&L-series would

be collinear, i.e., C i t = w i X t (with X t = P m i=1 C i t );w i > 0), then I t = 1 P i i=1 w 2 i . This

upperboundon I depends on thesizedistribution among banksand lies intheinterval

[1;m]. For the 13 banks under consideration, this upper bound is about 5:23, when

w i

is taken to be proportionalto the average VaR of bank i. If the banks' P&L-series

would be stochastically independent, then I

t

= 1. The other extreme occurs when the

banks' tradingwould bea zerosum game,i.e.,

P m i=1 C i =0 and consequently I t =0. In summary,I t

>1standsforpositivelycorrelatedP&Ls,I

t

=1for\normal"diversication,

and I

t

<1 forthepartialosettingof risksbeyond \normal" diversication.

Figure12shows thatlocalestimates ofI

t

areabove1 mostof thetime, butwellbelow

its upper bound5:23. The dramatic stock market movements in September 2001 seem

to have had some impact, but theincreases in medium-term interest rates beginning in

October a lot more. In our view, the index of co-movement shows that the portfolio of

the German regulator is quite well-diversied in general. In periodsof stress the index

increases, but only by a factor of about two, which lends support to the Basel safety

factor three.

Figure12suggests thatinthelatterpartoftheyear2001 therewasacommon\stress"

factor. In order to dene \stress" we have to distinguish between stress variables that

measure stress and stress events that denoteperiodsof stress.

Considertheaggregate stress dened in terms of excess losses

L t (c):= m X i=1 ( C i t V i t c) + V i t = m X i=1 ( C i t cV i t ) + (10)

where cis a constant tresholdand x

+

=max(0;x) denotesthe positivepart. Note, that

the aggregate stress in terms of excess losses has a monetary unit. L

t

(1) is the sum of

excess losses at theVaR-level and L

t

(0) isthesum of losses.

Giventhenotoriousunpredictabilityofnancialmarketreturns,extremelyhighprots

for some banks may also point to \stress". Hence, the aggregate stress dened in terms

of excess prots

G t (c):= m X i=1 ( C i t V i t c) + V i t = m X i=1 (C i t cV i t ) + (11)

may alsobe interestingto lookat.

In the absence of data on the counter party exposures of each bank and an analysis

of contagion risk based on such data, both L

t

(c) and G

t

(c) are stress variables that a

supervisoryauthoritymight want to monitor.

Thelinesinthetwo uppergraphsofgure13show2-weekaveragesofaggregate stress

1.0

1.5

2.0

2.5

3.0

03−19

06−27

10−05

Figure 12:Measureofco-movement. Thegraphshowsthelocal(solidline)andglobal

(dottedline)estimateoftheindexofco-movement. Thepointsarethesquared

aggregatedP&LdividedbythesumofthesquaredindividualP&Lsofagiven

day. The localestimate isa 60-day slidingaverage of thepoints.

VaR-level (c = 1). The top graph is based on prots while the graph in the middle is

based on losses. In order to see therelationto key risk factors, thebottom graphshows

a stockindexand an interest rate. Several interestingaspects ofthe dataappear:

Periodsoflargeexcessprotsdonotingeneralcoincidewithperiodsoflargeexcess

losses, whichis mostpronouncedintherst fourmonths.

Therewerethreeperiodsof \stress"interms oflosses: inApril,inSeptember, and

inNovember.

The Novemberstress wasthe largest.

While theApril stress waslarger than the Septemberstress interms of aggregate

losses (c = 0), the September stress was larger than the April stress in terms of

more extremelosses (c=0:5and c=1).

Visual comparison between the two risk factors and the aggregate stress in terms

01

0

2

0

3

0

4

0

Excess Profits

million EUR

03−19

06−27

10−05

0

0.5

1

−

50

−

40

−

30

−

20

−

10

0

Excess Losses

million EUR

03−19

06−27

10−05

0

0.5

1

0.7

0.8

0.9

1.0

date

normalized value

MSCI Europe

2Y EUR Swap Yields

Key Risk Factors

Figure 13:Two-week averages of aggregate stress for the excess loss tresholds

0,0.5, and 1. Thelinesinthersttwographsshow2-weekaveragesofG

t (c)

(top) and L

t

(c) (middle) for the tresholds c 2 f0;0:5;1g. The peaks show

the sumof excess losses at the VaR-level (c=1). Thelowergraph shows the

0.0

0.4

0.8

date

stress

03−19

06−27

10−05

Figure 14:Stress periods. The stress periods dened by ftjL

t

(c) > qg with c = 0:5

undq beingthe 80%-quantile ofL

t (c).

AnystressvariablelikeL

t

(c)can beusedto deneasetof\stressdays"ftjL

t

(c)>qg,

where q is some quantileof L

t

(c). Figure 14 shows thethus denedstress period,using

the tresholdc=0:5 andq the80%-quantileof L

t (c).

Having identied periods of stress, the next question is \How do properties of V, C,

and R change under stress?". In other words, we compare empiricaldistributions from

the whole timeinterval withempirical distributionsfrom the stress period as denedin

the previoussectionand depictedin gure14.

Figure15 compares theconditional and unconditionaldensitiesof the banks'P&L. It

shows that the variance increases drasticallyfor banks D and I under stress. Figure 16

is an alternative look at the conditional means and standard deviations. It shows that

whilethe standarddeviationsincrease understress, they do not exceedthe Basel safety

factor 3.

Conclusion

Thenotionofawell-behavedforecastsystemiscloselyrelatedtotheestablishedconcepts

ofwell-calibrationandrenement. ItgeneralizesthecalibrationcriterionF

t (C

t

)U[0;1]

to a neighborhood of the uniform distribution. We introduced exploratory statistical

tools(localestimatesoftherecalibrationfactor,themeasureofco-movement,conditional

distributions under stress)in order to study thisproperty forthe VaR forecast systems

of German banks. In the light of the analyses based on these tools we can draw three

kinds ofconclusions.

First,theVaRmodelsofGerman banksthat usethesemodelsforregulatorypurposes

work surprisingly well, even for the special year under consideration. I.e., the forecast

systems are well-behaved and the forecast quality is good. The fact that many banks

estimatetheirVaRwithabias can simplyberectied byre-calibratingtheforecasts,see

also (Buhleretal.;2002).

−2

0

2

4

6

8

10

0.0

0.2

0.4

0.6

0.8

A

clean PL

density

−6

−4

−2

0

2

0.0

0.1

0.2

0.3

0.4

B

clean PL

density

−6

−4

−2

0

2

4

6

0.0

0.1

0.2

0.3

0.4

0.5

D

clean PL

density

−4

−2

0

2

4

0.0

0.1

0.2

0.3

0.4

G

clean PL

density

−5

0

5

0.0

0.2

0.4

0.6

0.8

1.0

I

clean PL

density

−6

−4

−2

0

2

4

0.0

0.1

0.2

0.3

K

clean PL

density

Figure 15:Conditional densities. The solidlineshowsa kernel estimateof the

condi-tionaldensityof thebanks'P&L understress,whilethedottedlineshowsthe

−0.4

−0.2

0.0

0.2

0.8

1.0

1.2

1.4

1.6

1.8

2.0

mu/sigma

sigma

A

B

H

J

I

M

C

E

L

K

G

F

D

Figure 16:Conditional meansand standarddeviations ofcleanP&L.Thebank's

symbol represents the unconditional parameters, while the arrow points to

the parameters conditioned on stress. The x-axis shows the conditional and

unconditionalmean dividedbytheunconditionalstandarddeviation.

Third,ourempiricalanalysesconrmthearchitectureof theregulatoryframeworkfor

Value-at-Risk models. In particular, themain ingredients, i.e., the multiplication factor

three and thebacktesting penaltyfunctionare justied.

A. Well-Calibrated Forecasts

The literature on weather forecasting has developed an elaborate set of concepts and

diagnosticsfortheevaluationofprobabilityforecasts(MurphyandWinkler;1987,1992).

The two main concepts are calibration and renement. This section shows how our

denitionof \well-calibrated"is related to theestablishedone.

Given the joint distribution of an event a and a probabilityforecast p for this event,

information the forecast p contains about the event a is called renement or resolution

and is formalized and measured in dierent ways, see Dawid (1986). Partial orderings

among forecasts are based on thenotion thatp

A

is more rened than p

B

ifthe forecast

p B

can be derived from p

A

in a certain way. Complete orderings among forecasts can

be denedbytheexpected lossES(a;p) foralossfunction S,calledscoring rule inthis

context. Anotherwaytodenerenementforasequenceofforecastsandevents(a

i

;p

i

)is

to saythatthesubsequenceofeventscorrespondingto aspecicforecastp

,(a i ) fijp i =p g ,

should be stochastically independent. (Otherwise, it would be possible to improve the

forecast.)

In the context where we have a forecast

^

F for the probability distribution F of a

continuousrandomvariable C,theconcept ofwell-calibrationbecomes

PfC xj

^

Fg=

^

F(x); (12)

i.e., the forecast of each event based on C is well-calibrated (Dawid; 1984, p.281). If

^ F

is continuous, (12) impliesthat

^

F(C) isuniformlydistributedon[0;1]. Therequirement

that a sequence of \realized probabilities"

^ F t

(C t

) is stochastically independent is a kind

of renementrequirement.

Given thatbanks do notreportthe whole forecast distribution

^

F butonly a quantile

^

q():=

^ F

1

(),theimportantquestionisinwhichsenseandunderwhichconditionsthe

realizedprobabilitiesF(R

t

) ofthe standardizedreturns

R t :=C t q() ^ q t () (q()=F 1 ()) (13)

for some xed p.d.f. F can be taken as a substitute forthe \true" realized probabilities

^ F t (C t ). Iftheforecast ^

F comesfrom a location-scalefamilyof distributions,i.e.,

^

F(x)=F((x )=^^ ); (14)

and the location ^ is 0, then the realized probabilities of the standardized returns are

obviously aperfect substitutefor the\true" realizedprobabilities:

^ F t (C t )=F(C t =^ t )=F(C t q() ^ q t () )=F(R t ):

Interestingly,theconverse also holds.

Proposition 1 Let C be a random variable and F

0

its distributionunder the true

prob-ability. Let

^

F be a forecast for F

0

and F a xed \benchmark" distribution. Assume F,

F 0

, and

^

F are continuous and have support ( 1;1). Let q and q^ denote the inverses

of F and

^

F,respectively. Thevalue U =F(C

q() ^ q()

) has the same distribution as the re

al-ized probability

^

F(C) under the trueprobability measureif andonly if

^

F comes from the

scale-family ^ F(x)=F(x q() ^ q() ) .

P 0 fU pg=P 0 f ^ F(C)pg 8p2[0;1]: This implies F 0 F 1 (p) ^ q() q() =F 0 ^ F 1 (p) : Since F 0

is invertible, thisequation also holds for the arguments of F

0 (:). Setting x := F 1 (p) ^ q() q() ,thisleadsto ^ F(x)=p whichequals =F x q() ^ q() bydenitionofx. 2

The assumption that the banks' forecasts

^

F come from a location-scale family with

location 0 is a rather unrealistic one. We actually know from those banks that use

historical simulation and various delta-gamma-normal methodsthat the forecasts

^

F do

not in generalcome from such a family. In theempiricalanalysis,however, we observed

thattheempiricaldistributionofthestandardizedreturnsisremarkablyclosetonormal.

An interestingquestionisnowhowthetwo conceptsof well-calibrationarerelatedunder

theadditional assumption

R=C

q()

^ q()

F(:=) (15)

forsome xed benchmarkdistributionF and scale >0.

Proposition 2 Let

^

F beaforecast forthe distributionF

0

of arandom variable C andF

a xed \benchmark" distribution. AssumeF,F

0

,and

^

F arecontinuous andhavesupport

( 1;1). Let q and q^denote the inverses of F and

^

F, respectively. Assume that the

standardized returns R = C

q() ^ q ()

are known to come from the scale family (15) and the

forecast ^

F iswell-calibrated asin(12). Then =1andthe forecast

^

F \comeson average

from a scale-family" in the senseof

F(x)=E ^ F x ^ q() q() : (16)

In general it cannot be concluded, however, that each single forecast comes from a scale

family ^

F(x)=F(x=^).

Proof. We rstprove =1. Since

^

F is well-calibrated,

=PfC q()j^

^

=PfRq()g;

whichequals F(q()=) becauseof (15). Butthis implies =1.

Furthermore, F(x)=P C q() ^ q() x =E PfC q() ^ q() xj ^ Fg =E ^ F x ^ q() q() :

Example. Assume C = m+X; m G and X F

0 (:=

0

) are independent random

variables. Assume furtherthatthebankhasadvanceknowledge ofm (butnoknowledge

of X),thenthe forecast

^ F(x):=F 0 ((x m)= 0 )

iswell-calibratedinthesense(12), itcomesfromalocation-scalefamily,butthelocation

is notnecessarily0. The standardized returnbecomes

R=C q() ^ q() =(m+X) q() m+ 0 q 0 whereq 0 :=F 1 0

(). Thisequation showsthat theconditionaldistributionofR given m

comesfrom thelocation-scalefamilydenedbyF

0 .

Beingmore specic, assume F

0

is the standard normal distribution. Then the

distri-butionF observedbythesupervisorisacertainmixtureofnormaldistributionsand will

usuallyhave a dierentshapeasand fatter tails thanF

0

. 2

The proposition shows that the notion of well-calibration based on the standard

de-viation of R

t

diers from the notion of well-calibration in the sense of Dawid (1986),

unlessone makesadditionalassumptions. Forequivalence,oneneedstherather

unrealis-tic assumption that all individual forecasts come from a scale-family. Under theweaker

condition(15), well-calibrationimplies =1. I.e.,ifwe \observe"that thestandardized

returns R

t

areapproximatelynormal, thenthe variance of thestandardized returns is 1

forwell-calibratedforecasts. The condition(R

t

)=1asa criterionof well-calibrationis

to be understoodinthissenseinthepaper.

References

Basel Committee on Banking Supervision(1996a). Amendment to the capitalaccord to

incorporate marketrisks,http://www.bis.org/publ/bcbs24.pdf.

Basel CommitteeonBanking Supervision(1996b). Supervisoryframework fortheuseof

\backtesting"inconjunction withtheinternalmodelsapproach to market risk capital

http://www.uh.edu/~jberkowi/back.pdf. appeared in theJournal of Business and

Economic Statistics (October2001).

Berkowitz,J.andO'Brien,J.(2002).Howaccuratearevalue-at-riskmodelsatcommercial

banks?,Journal of Finance 57:1093{1112.

Buhler, W., Engel, C., Korn, O. and Stahl, G. (2002). Backtesting von

Kreditrisiko-modellen, in A. Oehler (ed.), Kreditrisikomanagement - Portfoliomodelle, Derivate,

Backtestingund Aufsicht, 2nd edn,Schafer-Poeschel,Stuttgart, pp.181{217.

Christoersen, P. (1998). Evaluating interval forecasts, International Economic Review

39:841{862.

Crnkovic, C. and Drachman, J.(1996). Qualitycontrol, RISK9(9): 138{143.

Dawid, A. P. (1982a). Intersubjective statistical models, Exchangeability in probability

andstatistics (Rome, 1981), North-Holland,Amsterdam, pp.217{232.

Dawid, A. P. (1982b). The well-calibrated Bayesian, J. Amer. Statist. Assoc.

77(379): 605{613.

Dawid, A.P. (1984). Statistical theory. The prequentialapproach, J. Roy. Statist. Soc.

Ser.A 147(2): 278{292.

Dawid, A. P. (1986). Probability forecasting, Encyclopedia of Statistical Sciences, John

Wiley&Sons, New York,pp.210{218.

Jorion, P. (2001). Value at Risk: The New Benchmark for Managing Financial Risk, 2

edn,McGraw-Hill, NewYork.

Kupiec, P. (1995). Techniques for verifying the accuracy of risk measurement models,

Journal of Derivatives 2:73{84.

Longerstaey, J. (1996). RiskMetrics technical document, Technical Report fourth

edition, J.P.Morgan. originally from http://www.jpmorgan.com/RiskManagement/

RiskMetrics/,now http://www.riskmetrics.com.

Lopez,J.(1999).RegulatoryevaluationofValue-at-Riskmodels,JournalofRisk1:37{63.

Matten, C.(2000). ManagingBank Capital,2nd edn, JohnWiley&Sons, Chichester.

Murphy,A.H.and Winkler,R. L.(1987). A generalframework forforecastverication,

Monthly Weather Review116:1330{1338.

Murphy,A.H.andWinkler,R.L.(1992). Diagnosticvericationofprobabilityforecasts,

International Journal of Forecasting 7: 435{455.

Overbeck,L.andStahl,G.(2000).Backtesting: AllgemeineTheorie,Praxisund

scherBanken, Diplomarbeit,Humboldt-Universitat,Berlin,Germany.

Rosenblatt,M. (1952). Remarksonamultivariatetransformation,Ann. Math.Statistics

23:470{472.

Seillier-Moiseiwitsch,F. (1993). Sequential probability forecasts and theprobability

in-tegraltransform, International Statistical Review61(3): 395{408.

Seillier-Moiseiwitsch,F. and Dawid, A. P. (1993). On testing the validityof sequential